09 March 2021

By Maynard Paton

Results summary for Tristel (TSTL):

- A satisfactory pandemic-assisted performance, with revenue up 14% and profit up between 12% and 31% depending on the adjustments made.

- Sales were bolstered by Brexit stock-piling, which will unwind during H2, with underlying UK progress still difficult to interpret.

- Overseas sales improved a useful 20% although the United States regulatory project and other ventures remain very slow burners.

- The 21% operating margin seems impressive in light of “one-off” payroll costs and the headcount increasing 19% to prepare for future growth.

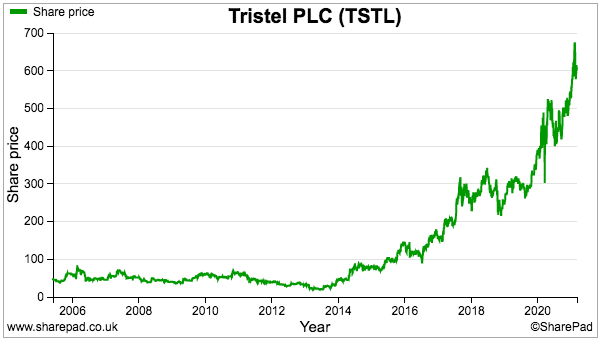

- The 48x P/E looks stratospheric, but permanently greater demand for hospital disinfectants, further expansion plus growing economies of scale may justify a lofty rating. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own TSTL

- Results summary

- Revenue, profit and dividend

- Product revenue and gross margin

- UK

- Nanosonics and Ambu

- International

- United States

- Byotrol, Rinse Assure and MobileODT

- Share options

- Financials

- Valuation

Event links, share data and disclosure

Event: Interim results and online presentation (slides here) for the six months to 31 December 2020 published 22 February 2021

Price: 600p

Shares in issue: 46,998,443

Market capitalisation: £282m

Disclosure: Maynard owns shares in Tristel. This blog post contains SharePad affiliate links.

Why I own TSTL

- Develops medical-instrument disinfectants that are repeat-purchase and face limited direct competition due to multiple patents, instrument-manufacturer approvals, scientific testimonies, secret ingredients and regulatory hurdles.

- Enjoys a sizeable and resilient UK market position alongside significant opportunities abroad, with Covid-19 possibly creating an irreversible trend of greater disinfectant usage.

- Boasts financials that showcase high margins, growing economies of scale, robust returns on equity, decent cash flow and no debt.

Further reading: My TSTL Buy report | All my TSTL posts | TSTL website

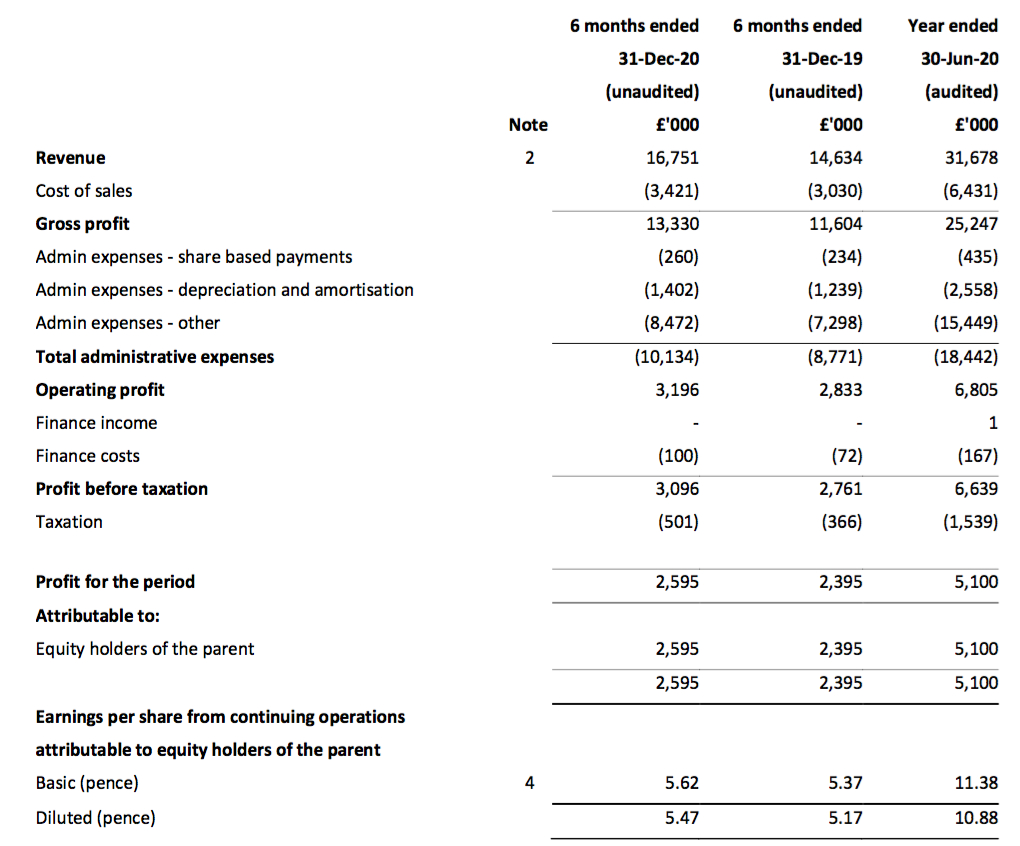

Results summary

Revenue, profit and dividend

- These H1 figures surpassed the 10% growth projections cited within December’s AGM statement.

- Revenue in fact improved 14% while pre-tax profit before share-based payments climbed 12%.

- The results set a fresh first-half record for the eighth consecutive year.

- But interpreting TSTL’s underlying profit growth remains awkward. Distortions include:

- Notable share-based payments (see Share options);

- Expenses associated with the US regulatory project (see United States);

- Unspecified “one-off” payroll costs (see Financials);

- Unrealised foreign-exchange gains and losses (see Financials), and;

- Fair-value investment gains cheekily recognised last year as operating income (see FY 2020 Financials).

- The following table calculates operating profit before share-based payments, declared US costs, unrealised foreign-exchange gains/losses and fair-value investment gains:

| H1 2019 | H2 2019 | H1 2020 | H2 2020 | H1 2021 | |||

| Operating profit before SBP, US costs, unrealised FX and FV gains (£k) | 2,485 | 3,538 | 2,966 | 4,086 | 3,511 | ||

| Share-based payments (£k) | (196) | (656) | (234) | (201) | (260) | ||

| US costs (£k) | (100) | (400) | (150) | 70 | - | ||

| Unrealised FX (£k) | - | (72) | 140 | 17 | (55) | ||

| Fair-value gains (£k) | - | 98 | 111 | - | - | ||

| Operating profit (£k) | 2,189 | 2,508 | 2,833 | 3,972 | 3,196 |

- First-half operating profit before share-based payments, declared US costs, unrealised foreign-exchange gains/losses and fair-value investment gains advanced 18%.

- US costs were not revealed within the results RNS nor the presentation. The 18% advance assumes such costs were zero.

- However, TSTL did say US costs of £750k could be expected for FY 2021 within the FY 2020 announcement.

- As such, US costs of, say, £375k during this H1 would mean first-half operating profit before share-based payments, the estimated £375k US costs, unrealised foreign-exchange gains/losses and fair-value investment gains actually rallied 31%.

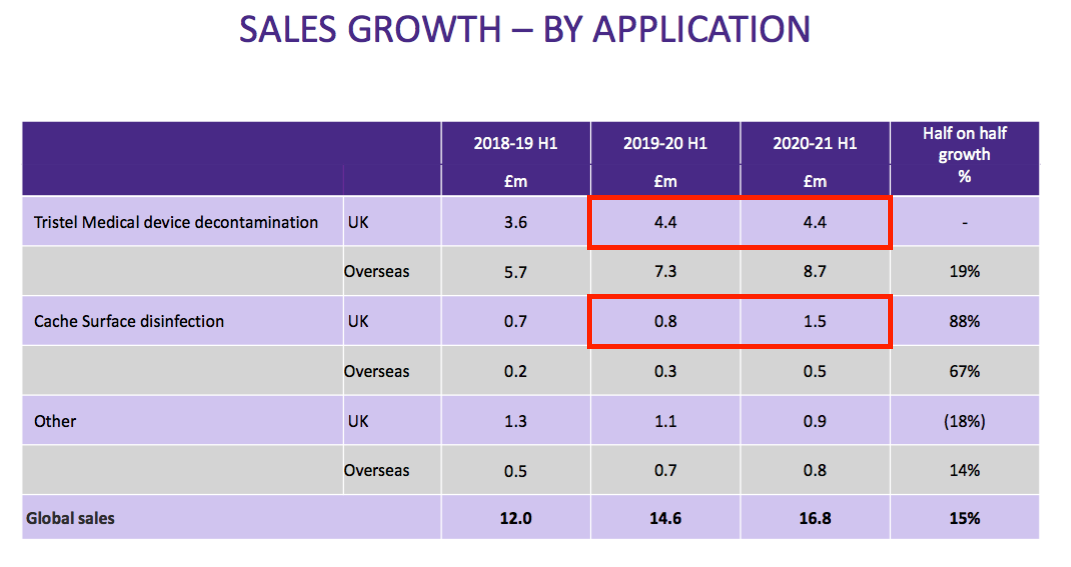

- The divisional-reporting re-jig that accompanied the FY 2020 results meant these figures provided greater insight into TSTL’s past product profitability (see Product revenue and gross margin).

- The reporting re-jig, which lumped the UK and Europe together, also left TSTL providing only approximate figures for UK progress.

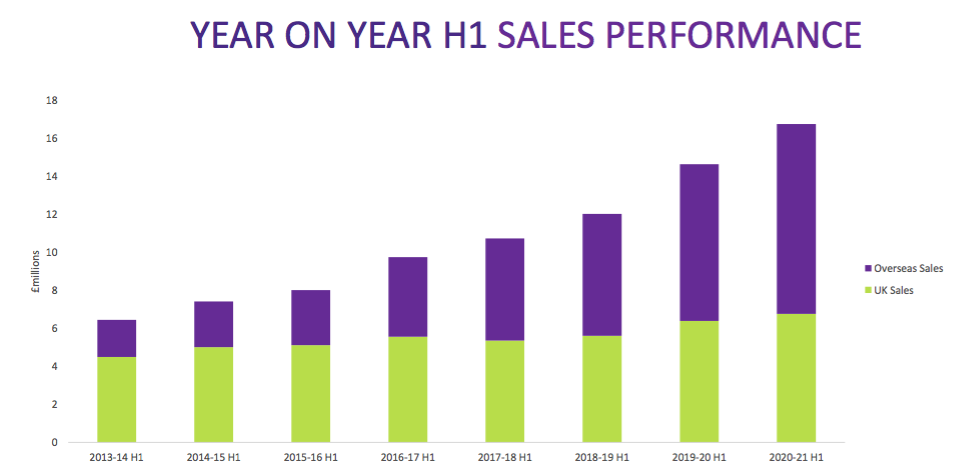

- TSTL said UK revenue gained 8% and overseas revenue climbed 20%. Overseas revenue currently represents 60% of group revenue, versus 50% for H1 2018, 30% for H1 2014 and 8% for H1 2011:

- After the FY 2020 final dividend was raised a relatively modest 10%, the interim dividend fared a little better with a 12% lift.

Product revenue and gross margin

- The FY 2020 reporting re-jig allocated revenue and gross profit into three categories:

- The various wipes and foams used to clean hospital medical devices (such as endoscopes, tonometer prisms and endo-cavity probes);

- The disinfectants used to clean hospital surfaces (such as bedside tables, mattresses and floors), and;

- Other products, including ‘legacy’ disinfectants for pharmaceutical cleanrooms and veterinary practices.

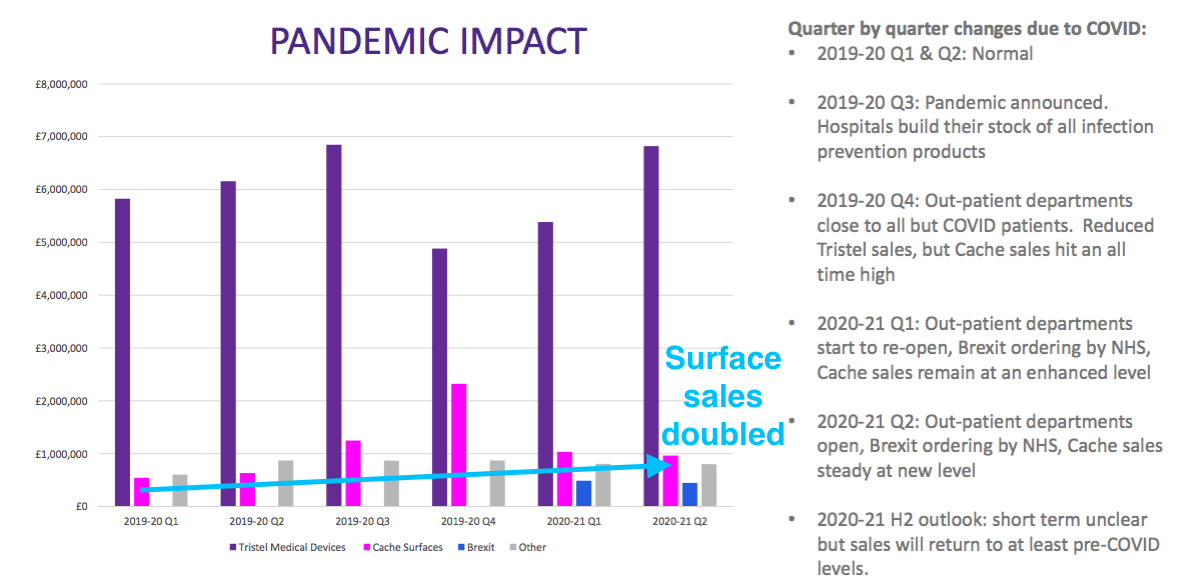

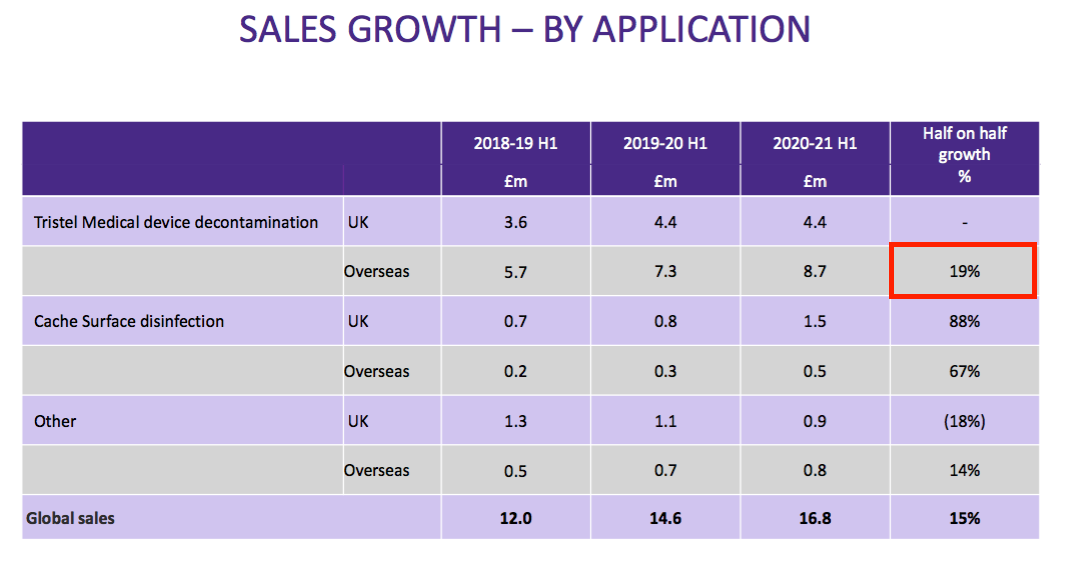

- TSTL commendably published a revised Pandemic Impact slide to outline how the three categories performed during the last 18 months:

- As noted within the FY 2020 statement, demand during the initial lockdown switched from device disinfectants (purple bars above) to surface cleaners (pink bars above) after hospitals deferred routine medical procedures and enhanced their cleaning regimes.

- Progress appears to have since ‘normalised’, although sales of device disinfectants were “lower than budget” during the first seven weeks of the second half due to the latest lockdown.

- Revenue from hospital surface cleaners looks to have stabilised at £1m a quarter — approximately double the level recorded before the pandemic.

- These H1 figures revealed total hospital-related revenue climbed 18% on H1 2020:

| Revenue (£k) | H1 2020 | H2 2020 | FY 2020 | H1 2021 | |

| Hospital medical devices | 11,700 | 11,797 | 23,497 | 13.,107 | |

| Hospital surfaces | 1,100 | 3,782 | 4,882 | 2,036 | |

| Hospital total | 12,800 | 15,579 | 28,379 | 15,143 | |

| Other | 1,834 | 1,465 | 3,299 | 1,608 | |

| Total | 14,634 | 17,044 | 31,678 | 16,751 |

- Total H1 hospital-related revenue was just £400k shy of the level witnessed during H2 2020. Management claimed during the presentation that H2 2020 was supported by “an element of panic buying” following the initial lockdown.

- TSTL’s re-jigged reporting revealed significant gross-margin variations had occurred during the initial lockdown of H2 2020. In particular, the gross margin of surface cleaners jumped from 63% to 81%:

| Gross margin (%) | H1 2020 | H2 2020 | FY 2020 | H1 2021 | |

| Hospital medical devices | 83.7 | 78.0 | 80.9 | 84.5 | |

| Hospital surfaces | 63.1 | 80.8 | 76.8 | 63.0 | |

| Hospital total | 81.9 | 78.7 | 80.2 | 81.6 | |

| Other | 61.0 | 94.2 | 75.8 | 60.6 | |

| Total | 79.3 | 80.0 | 79.7 | 79.6 |

- The gross-margin fluctuations suggest the sudden sales switch from device disinfectants to surface cleaners during H2 2020 was accompanied by:

- Commensurate changes to product pricing to reflect demand, and/or;

- Sudden fluctuations to raw-material costs.

- For this H1, gross margins for device disinfectants returned to 85% while gross margins for surface cleaners returned to 63%.

- The overall 82% hospital-product gross margin underlines how TSTL can turn commodity raw materials (i.e. chemicals, packaging, and so on) into products that buyers are willing to pay a premium for.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

UK

- UK hospital-related sales increased by £0.7m, or 13%, to £5.9m during this H1 following greater demand for surface cleaners:

- TSTL admitted the performance had been bolstered by Brexit stock-piling:

“In preparation for [the Brexit] transition, last September the NHS purchased approximately £0.9m of Tristel medical device disinfectant products and has held them in a dedicated storage facility. We anticipate that this stock will be fed back into the NHS Supply Chain network from May 2021 but have no visibility on the time this might take. The release of this inventory will have some negative impact on second half sales of medical device disinfectant products in the UK.”

- Exclude the Brexit stock-piling, and UK hospital-related revenue fell 4% to £5.0m — with UK medical-device revenue dropping 20% to £3.5m.

- TSTL said the 20% reduction reflected deferred medical procedures:

“Tristel product sales in all countries have been adversely affected as patient examinations have been deferred.”

- However, overseas medical-device revenue gained 19% during this H1…

- …suggesting the NHS postponed a much greater number of medical procedures than health services abroad.

- The Brexit stock-piling alongside the divisional-reporting re-jig makes studying TSTL’s UK progress very difficult.

- The UK remains by far TSTL’s largest and most mature market, and serves as a guide as to the sales potential of other countries.

- Just how the Brexit stockpiling of medical-device disinfectants will affect H2 UK sales remains to be seen. TSTL did not disclose UK medical-device revenue within the FY 2020 figures, and their absence from the next FY 2021 figures would leave the exact H2 Brexit impact unclear.

- Bear in mind TSTL’s FY 2020 UK performance contained two peculiarities:

- Lower H2 2020 UK revenue despite the initial lockdown boost to sales, and;

- Reduced revenue from the NHS supply chain for the full year.

- Maybe something untoward really is developing within the UK, which is why TSTL re-jigged the reporting and lumped the UK together with Europe. That way any adverse UK developments would not be so obvious to outsiders.

- But is something untoward developing within the UK? I don’t know.

- A few points to consider:

- Five years ago TSTL claimed: “Slowing growth in the United Kingdom is due to the very high levels of market penetration”. H1 UK hospital-related sales have since climbed 79%;

- Reported UK progress during H1 2017 and H1 2019 was muddled by NHS “bulk purchasing” and endoscopy reclassifications respectively;

- The impact of likely Brexit stock-piling was first mentioned during FY 2018 and influenced the results for FY 2019, and;

- This time last year UK sales of medical-device disinfectants improved an impressive 22%.

- Factor in as well the operational mysteries of the NHS supply chain and TSTL’s pricing framework with the health service, and perhaps assessing UK progress in any particular year will always be difficult.

- Assuming TSTL’s competitive ‘moat’ — a large collection of patents, industry verifications and manufacturer approvals — remains wide, I am hopeful the UK should not be cause for concern.

- But it never hurts to check whether the ‘moat’ does indeed remain wide…

Nanosonics and Ambu

- Nanosonics (NAN) is a quoted Australian company that manufactures a high-level disinfection machine called trophon. The machine cleans only ultrasound probes:

- NAN does not currently enjoy a significant UK presence. During FY 2020, only 9% of NAN’s revenue — approximately £6m — was generated outside of North America.

- But NAN’s 2020 annual report did show a Worcestershire NHS Trust ordering 17 trophons:

- NAN admitted NHS trophon interest had faltered during the initial lockdown:

“The onset of COVID-19 caused a decrease in conversion of our pipeline to new installed base during Q4. However, we remain confident that the underlying fundamentals for ongoing adoption remain strong.”

- I understand UK hospitals employ trophon machines and TSTL’s products side by side. This document from a Leicester NHS Trust provides some insight into the practicalities:

“Due to widespread use of ultrasound across UHL trust and community sites, it is not feasible to have a trophon machine available in all locations. In these situations, the Tristel Trio Wipe System must be used to decontaminate intracavity probes.”

- The TSTL directors have in the past claimed the trophon machines “break down”.

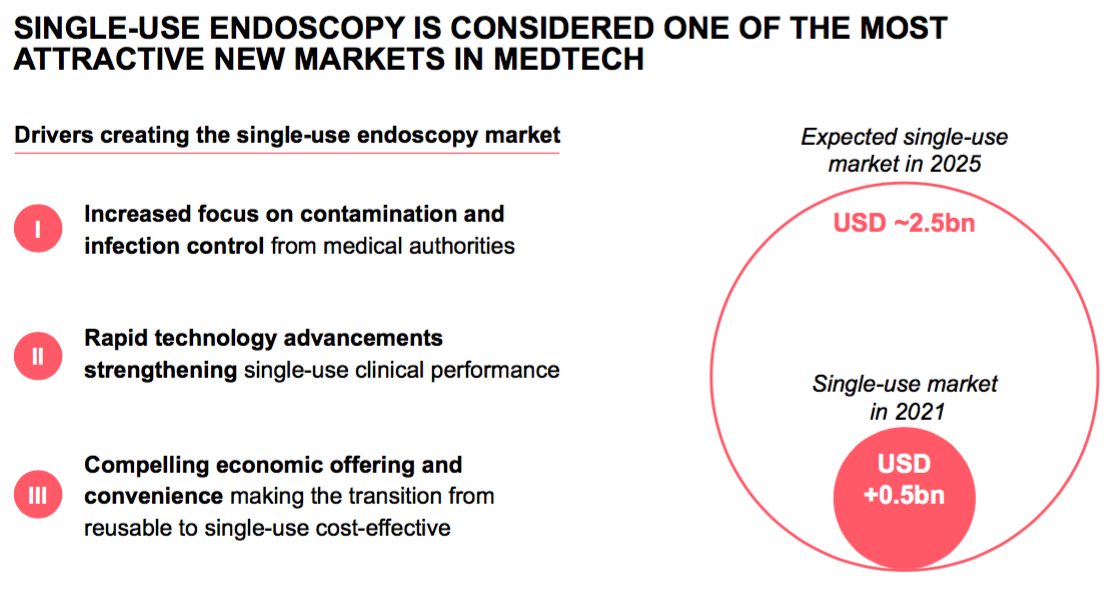

- The competitive threat from Ambu (AMBU) appears greater than that from NAN.

- AMBU is a quoted Danish company that manufactures single-use endoscopes among other medical devices.

- Single-use endoscopes do not require any disinfection, which is bad news for TSTL.

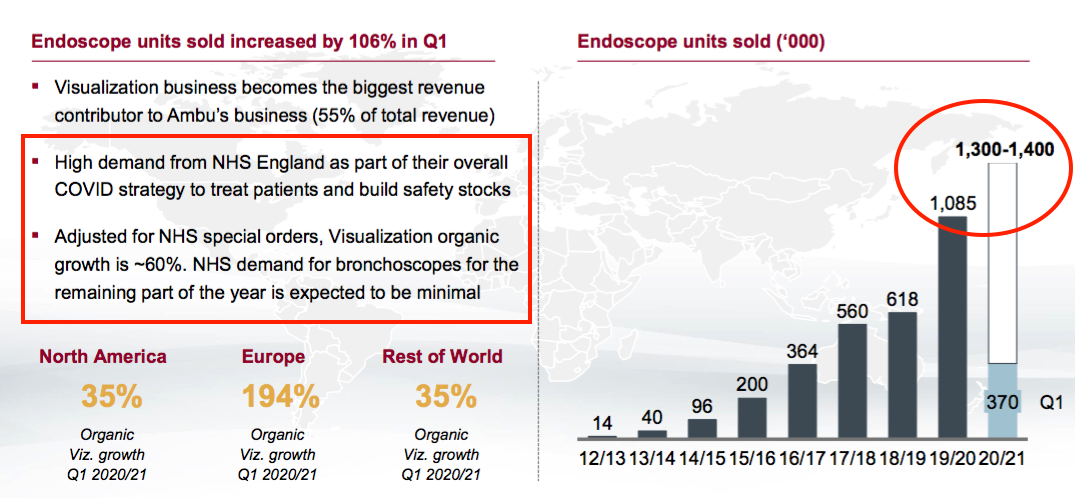

- AMBU may have a greater presence in the UK than NAN. During FY 2020, 55% of AMBU’s revenue — approximately £230m — was generated outside of North America.

- Sales of AMBU’s endoscopes have surged during recent years. The company predicts volumes could improve by between 20% and 30% during FY 2021:

- The NHS has acquired single-use bronchoscopes, too.

- AMBU claims the pandemic has “accelerated the development of the single-use endoscopy market”…

- …and an online search for single-use medical devices found these other suppliers:

- Haag-Streit;

- Karl Storz, and;

- Timesco

- I confess I do not know whether single-use medical devices will eventually disrupt TSTL’s progress.

- For now I am hopeful that:

- Manufacturers of repeat-use endoscopes will not let their market share slide without a fight, and;

- Hospitals presently using repeat-use endoscopes will continue to use them.

- Management’s response to my question about single-use endoscopes at TSTL’s 2019 open day did not suggest imminent shareholder trouble.

- Yet AMBU’s sales have not stopped growing since that response.

- I would welcome any insight from healthcare professionals on the prospects for trophon machines and single-use medical devices. You can reach me through the comment box below, the Quidisq forum or my contact form.

International

- Total H1 overseas revenue gained a welcome 20%:

| Overseas revenue | H1 2019 | H2 2019 | H1 2020 | H2 2020 | H1 2021 | ||

| Australasia (£k) | 1,660 | 1,639 | 1,700 | 1,830 | 1,900 | ||

| China & Hong Kong (£k) | 560 | 622 | 620 | 1,000 | 800 | ||

| Germany/Central Europe (£k) | 2,230 | 2,380 | 2,490 | 2,830 | 2,800 | ||

| Western Europe (£k) | 400 | 1,740 | 1,750 | 2,850 | 2,400 | ||

| Italy (£k) | - | - | 300 | 370 | 400 | ||

| Malaysia (£k) | - | - | - | - | 200 | ||

| Total in-house (£k) | 4,850 | 6,381 | 6,860 | 8,880 | 8,500 | ||

| Distributors (£k) | 1,560 | 1,582 | 1,390 | 1,880 | 1,500 | ||

| Total (£k) | 6,410 | 7,963 | 8,250 | 10,760 | 10,000 |

- But H1 overseas revenue was 7% below that recorded for H2 2020, with Western Europe (France and Benelux) experiencing a 16% drop.

- I presume Western Europe witnessed more deferred patient examinations than some of TSTL’s other overseas markets.

- Still, the performance of Western Europe following the purchase of the associated distributor during 2018 remains impressive.

- Western Europe sales prior to purchase (FY 2018) were €3.1m.

- Doubling up Western Europe revenue of £2.4m for this H1 gives €5.3m at the average 1.11 GBP:EUR seen during the six months.

- Western Europe revenue may therefore have improved 71% (€5.3m / €3.1m) (in euro terms) within three years.

- Prior to purchase, 18% of Western Europe revenue related to non-TSTL products. The 71% improvement may therefore understate the sales progress of TSTL products.

- TSTL acquired its Italian distributor during 2019. Tristel Italia sales prior to purchase (FY 2019) were €700k.

- Doubling up H1 Italian revenue of £0.4m gives €0.9m at the average 1.11 GBP:EUR seen during the six months.

- Italian revenue may therefore have improved 27% (€0.9m / €0.7m) (in euro terms) within two years.

- TSTL has never disclosed the profit contributions from Western Europe or Italy, but the sales omens from both divisions seem promising.

- The Malaysian distributor became a TSTL subsidiary at the start of this H1 and management remarks a year ago claimed the operation enjoyed “close on £1m of gross sales to hospitals”.

- But the Malaysian subsidiary reported sales of only £200k during this H1, which therefore looks odd.

- Management confirmed during the online presentation that the group’s Indian distributor would commence sales this month.

Quality UK investment discussion at Quidisq. Visit forum.

United States

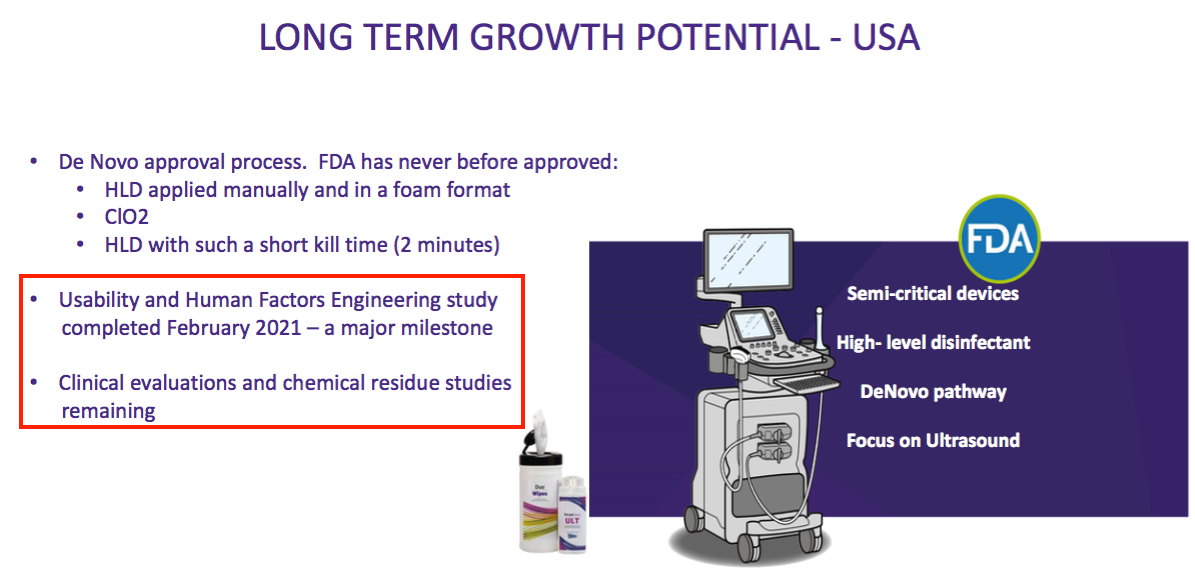

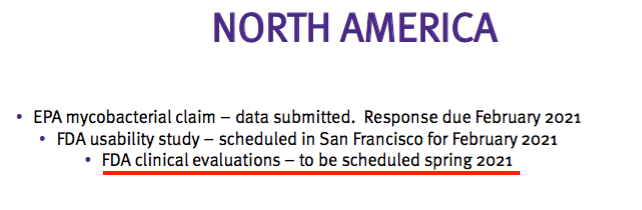

- TSTL’s United States regulatory project continues to advance:

“We continue to make good progress in our USA regulatory project. We have recently completed the Usability and Human Factors Engineering study which represents an important milestone on our path towards completing our De Novo submission.”

- The “Usability and Human Factors Engineering” studies were finished on schedule, which leaves just two FDA studies still to be completed:

- Management did not disclose when the remaining FDA studies would be undertaken.

- However, the FY 2020 presentation suggested one of the remaining studies was scheduled for “spring 2021”:

- Recent management comments concerning the US project have been relatively positive.

- The FY 2020 results revealed the scope of the FDA application had been expanded, while December’s AGM statement described US progress as “very encouraging”.

- But let’s not forget TSTL started the US project way back in 2014, bungled an FDA pre-application during 2018, withdrew all timescale guidance during 2019 and is still to submit a formal product application for FDA approval.

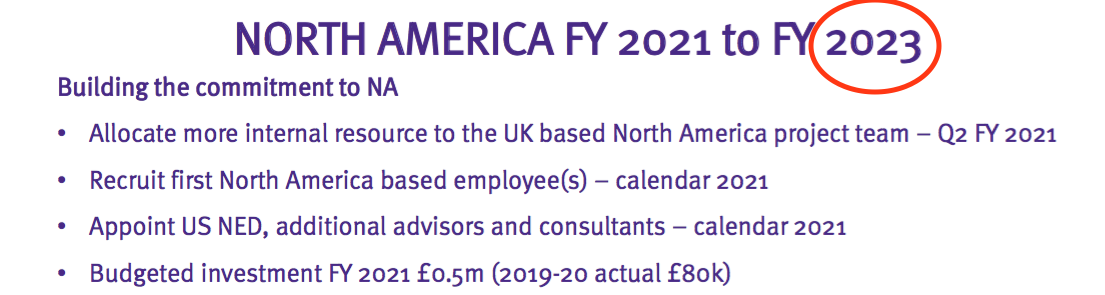

- I would like to think TSTL is now much closer to the FDA-approval finish line that it is to the FDA-approval start line.

- The FY 2020 powerpoint implied the resources required to begin trading within the States — assuming regulatory approval is one day granted — would be in place by FY 2023:

- Unlike previous results and presentations, the US costs expensed during this H1 were not disclosed.

- Disclosing US costs allows shareholders to better gauge the group’s underlying profitability. US costs are presently accompanied by no US revenue.

- Total US project expenditure before this H1 had totalled £1.8m:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Operating profit before US costs (£k) | 2,698 | 4,402 | 4,480 | 5,197 | 6,885 |

| US costs (£k) | (130) | (500) | (500) | (500) | (80) |

| Operating profit (£k) | 2,568 | 3,902 | 3,980 | 4,697 | 6,805 |

- The FY 2020 presentation said the US project would cost £750k during FY 2021 to cover the existing and new product applications:

- I continue to guess/hope TSTL can submit an FDA application during calendar 2022.

- Meaningful US revenue may then occur during 2024, some ten years after the project was launched.

Byotrol, Rinse Assure and MobileODT

- TSTL announced a collaboration with Byotrol (BYOT) during March 2020.

- The agreement involved TSTL paying BYOT for materials and formulations to enhance the performance of its hospital surface cleaners.

- TSTL said at the time the BYOT products would give “access to intermediate level disinfectants that are effective against bacteria, viruses and yeasts in accordance with the requirements of European Test Norms”.

- TSTL has never mentioned the collaboration since.

- But BYOT has shed further light on the arrangement. From BYOT’s FY 2020 statement:

“The Tristel agreement relates to three specific surface care technologies targeted for use in hospitals in UK and Ireland, two of which will be dispensed from Tristel’s proprietary ‘Cache’ system of innovative packaging solutions. The agreement has a duration of 10 years, is exclusive in hospitals in the UK and Ireland and non-exclusive elsewhere and will pay to Byotrol a combination of product supply payments, royalties and fees, based on success but with meaningful minimum guarantee payments to Byotrol each year.”

- Although BYOT’s latest (interim) statement did not mention TSTL, the headline numbers suggested the agreement is proving beneficial (at least to BYOT):

“H1 [Professional] revenues increased to £5.66m from £1.77m, including £0.59m of royalty and licensing revenue compared to £35,000 in the comparable period.”

- TSTL remains quiet about its fledgling ventures.

- Rinse Assure was cited as a possible money-spinner a year ago…

- …but the product (perhaps due to hospitals suddenly facing other priorities) has yet to be recognised in a subsequent powerpoint.

- TSTL no longer mentions its £807k MobileODT shareholding.

- This investment was made during 2017, and the persuasive slides about disinfecting mobile colposcopes have not been witnessed since:

Share options

- Significant share-based payments have featured regularly within TSTL’s accounts.

- Between FY 2016 and FY 2020, share-based payments reduced aggregate operating profit by £2.7m, or 11%.

- This H1 witnessed share-based payments reduce operating profit by £260k, or 7.5%:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 | H1 2020 |

| Operating profit before SBP (£k) | 3,242 | 4,023 | 4,645 | 5,549 | 7,240 | 3,456 |

| Share-based payment (£k) | (674) | (121) | (665) | (852) | (435) | (260) |

| Operating profit (£k) | 2,568 | 3,902 | 3,980 | 4,697 | 6,805 | 3,196 |

- The payment charges relate mostly to management options that vest only if the share price reaches certain targets.

- The (somewhat controversial) 2015 senior management options were granted when the shares were 96p and only vested if the price reached 136p.

- The (less controversial) 2018 management options were granted when the shares were 275p and only vested if the price reached 350p, 425p and 500p.

- I welcome options where vesting is dependent on share-price advances, because such options:

- Are straightforward to understand;

- Have targets that cannot be fudged, and;

- Only come good if outside investors have benefitted, too.

- IFRS 2 requires companies to record a share-based payment charge even if the options turn out to be worthless.

- IFRS 2 can also understate the eventual value of options.

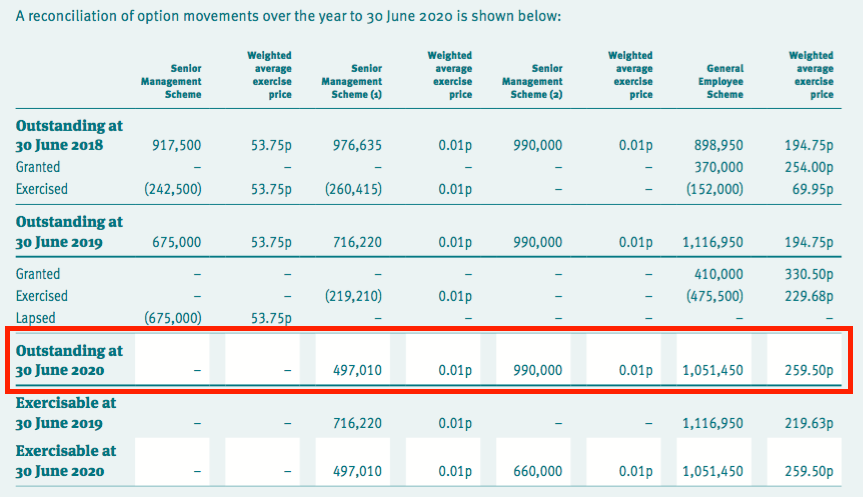

- For example, TSTL’s 2020 annual report (point 16) showed 2,538k outstanding options:

- 2,538k options could turn into shares worth £15m at the recent 600p share price.

- TSTL’s aggregate share-based payment charge is nowhere near £15m.

- A better way of assessing share options is to consider their dilutive effect on the company’s market cap.

- The table below shows how TSTL’s share count has increased due to options during the last five years:

| Year to 30 June | 2016 | 2017 | 2018 | 2019 | 2020 |

| Options exercised (k) | 773 | 584 | 443 | 661 | 773 |

| Year-end share count (k) | 42,165 | 42,749 | 43,192 | 44,563 | 45,297 |

| Options outstanding (k) | 3,060 | 2,776 | 3,783 | 3,498 | 2,538 |

| Proceeds from exercised options (£k) | 500 | 299 | 358 | 541 | 789 |

(Note: an extra 710k shares were issued during FY 2019 to part-fund an acquisition)

- At the start of FY 2016, the then 101p share price supported a £42m market cap.

- At the end of FY 2020, the then 425p share price supported a £193m market cap.

- The five-year market cap gain was therefore £151m.

- During the same five years, 3.2 million TSTL options converted into shares.

- Those 3.2 million extra shares were worth £13.6m at the then 425p.

- During the same five years, TSTL received £2.5m following the exercise of those 3.2 million options.

- The net value of the options exercised during those five years was therefore £11.1m (£13.6m less £2.5m).

- As such, between FY 2016 and FY 2020, shareholders arguably forfeited £11.1m to option holders but retained a £151m market-cap gain.

- Handing over approximately 7% of the market-cap gain after the share-price quadrupled during five years does not seem completely outrageous to me.

- TSTL granted 800k further options at the start of calendar 2021 when the shares were 500p and the market cap was £233m.

- These 800k options will vest fully if, alongside certain profit achievements, the shares trade at 750p during FY 2024.

- 800k options turning into shares at 750p gives a potential share award of £6m.

- TSTL’s market cap at 750p with an extra 800k options exercised would be £355m, and net exercise proceeds to TSTL would be just £8k.

- Shareholders foregoing £6m while retaining a market-cap gain of £122m (£355m less £233m) does not seem completely outrageous to me.

- TSTL’s share count as at the end of FY 2020 will increase by 7.4% to 48,535k if all 3,338k outstanding options (2,538k at the year end plus the 800k granted thereafter) are exercised.

- Those 3,338k outstanding options have exercise prices ranging from 1p to 412p and would raise approximately £2.8m for TSTL if all are converted into shares.

- Rather than adjust profits for (potentially misleading) share-based payment figures, earnings per share can be adjusted to use the completely diluted 48,535k share count.

- Whether TSTL’s directors and employees deserve 3,338k options — and the potential to convert them into shares worth £20m — is of course debatable.

- For now at least, I presume few TSTL shareholders are complaining about options when the shares have jumped six-fold since the start of FY 2016.

Financials

- TSTL’s H1 operating margin before share-based payments remained healthy at 21%.

- Note that TSTL’s H1 profitability was understated by a “one-off payroll-related cost”:

“Overheads excluding share-based payments, depreciation and amortisation increased by £1.2m, or 16%. Included in the increase is a one-off payroll-related cost associated with share option exercises, and the first contribution of costs from Malaysia. Excluding both these costs, underlying overhead expenses increased by only 3% in the half compared with last year.”

- The text above implies the extra payroll (and Malaysian) overheads were approximately £1m — which seems remarkably high given reported operating profit was £3.2m.

- Is TSTL really saying reported operating profit would have been 31% greater at £4.2m without the extra payroll/Malaysian overheads?

- I am reluctant to read too much into these calculations, because payroll costs and Malaysian overheads are expenses that are here to stay.

- Note also that TSTL’s headcount increased by 19% during the six months:

“During the period we increased global headcount by 31, from 164 at 30 June, to 195 at 31 December. We have bolstered our marketing, product management, product development, quality management and regulatory teams to prepare for the growth that we anticipate once hospital patient examinations return to their pre-pandemic levels in all countries, and the Cache product range is marketed globally. Included in the headcount increase are five employees in our newly operational Malaysian subsidiary.”

- Employee costs excluding directors came to £9.3m for FY 2020 (point 9), and a 19% greater workforce implies another £1.8m may be added to the wage bill for FY 2021.

- TSTL keeping the H1 operating margin (before share-based payments) at 21% following this recruitment drive feels very impressive.

- The additional wages may be obscuring some growing ‘economies of scale’, as the extra workers were taken on to “to prepare for… growth” and so may not have contributed much to revenue to date.

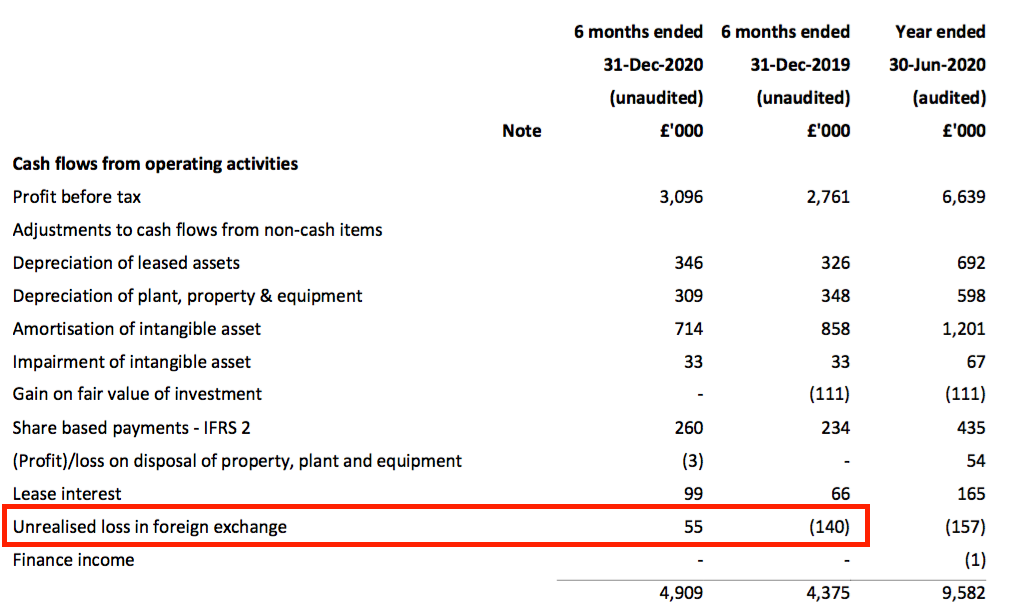

- The cash flow statement showed profit for this H1 was reduced by £55k due to an unrealised foreign-exchange loss, but profit for the comparable H1 2019 was increased by £140k by an unrealised foreign-exchange gain.

- Unrealised foreign-exchange gains and losses occur when outstanding debtors and creditors denominated in overseas currencies are translated into GBP at the balance sheet date.

- Such gains and losses can hinder or flatter reported profits through no fault of the company. (Profits can also be hindered or flattered by realised foreign-exchange gains and losses, but companies do not disclose realised movements.)

- The books also showed adjusted earnings of £2.8m and proceeds from exercised options of £0.3m converting almost fully into free cash, with £1.8m spent as dividends and £1.2m added to the bank balance.

- Half-year cash stood at £7.3m while bank debt remains zero.

- Management said during the presentation that the cash position had since increased to £8.1m

- The 2020 annual report (point 5) stated TSTL considers a “minimum cash balance of £4 million is appropriate — providing adequate protection against unexpected events…”

- TSTL carries no final-salary pension obligations.

Which is best for stock-screening: Stockopedia or SharePad? See my verdict.

Valuation

- TSTL did not adjust its financial guidance for FYs 2020, 2021 and 2022.

- TSTL expects revenue to have compounded at an annual average rate of between 10% and 15% during those three years.

- Meeting the bottom-of-the-range 10% level requires FY 2022 revenue of £34.8m.

- Trailing twelve-month revenue is presently £33.8m — meaning TSTL needs to lift sales by only £1m within the next 18 months to meet its guidance target.

- Finding extra sales of only £1m during the next 18 months is very achievable — even with the company claiming it is “difficult to forecast sales for the second half”.

- TSTL’s other three-year targets are:

- Ebitda (before share-based payments) remaining at 25% or more, and

- Profit before tax (and share-based payments) increasing each year.

- TSTL’s present valuation appears to be looking far beyond the firm’s guidance to FY 2022.

- TSTL’s reported operating profit was £3.2m for this H1.

- The following adjustments give an ‘underlying’ operating profit of £3.9m:

- Adding £260k to ignore share-based payments;

- Adding £375k to ignore (possible) US regulatory costs, and;

- Adding £55k to ignore unrealised foreign-exchange losses.

- Doubling up the performance, adjusting for full-year lease costs (£200k) and then applying standard 19% UK tax leads to earnings of £6.1m.

- Using the aforementioned 48,635k share count to assume every outstanding option is exercised, earnings of £6.1m convert into 12.6p per share.

- The 600p share price could therefore be trading at 48x my option-adjusted earnings guess.

- My valuation sums could be fine-tuned further for the cash position, “one-off payroll-related” costs and other items, but the stratospheric 48x multiple already tells a story.

- A premium share-price rating may well be justified given:

- Covid-19 has probably created an irreversible trend of hospitals enhancing their cleaning and disinfection regimes;

- The 19% workforce expansion shows confidence of capturing further sales within markets such as Western Europe, India and (eventually) the US.

- The accounts indicate TSTL’s disinfectants enjoy attractive economics and a worthwhile competitive position, and;

- Extra payroll/workforce costs during this H1 may have obfuscated TSTL’s true profitability and economies of scale.

- Remember, too, that the latest option grant pays out in full at 750p.

- But whether trophon machines and/or single-use endoscopes and/or something else will eventually derail TSTL’s growth ambitions and the 48x P/E remains to be seen.

- The trailing 6.46p per share twelve-month dividend meanwhile supports a lowly 1.1% income.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Wow Maynard, this is a truly impressive analysis. Your efforts are much appreciated and the competitor review was the first time I had seen anything of the like for TSTL.

I can add little but have a couple of comments.

I think there is a possibility that TSTL may get acquired if progress continues, I am wondering if this is helping maintain such a punchy share price.

My other thought is whether the rise of “disposable/single use” might get impacted by the Green lobby and help limit the impact on TSTL.

Hi BerksBee,

Thanks for the comment and I am glad you found the write-up useful. Yes, I am sure TSTL could be acquired at some point although I tend not to speculate on such matters. But there is no controlling shareholder to please and FDA approval (if it ever happens!) might bring the company onto a few more radars. The environmental impact of single-use devices could help matters (at least that is what management reckons) but I believe the instruments are recycled. Ambu continues to grow strongly in the meantime.

Maynard

Tristel (TSTL)

Trading Update published 26 April 2021

Oh dear — sales of medical-device disinfectants have not recovered as quickly as TSTL had hoped. TSTL did say in the H1 statement above that such sales had been “lower than budget” at the start of H2, and that it was “difficult to forecast sales for the second half”.

Here is the full text interspersed with my comments:

———————————————————————————————————–

As explained in our half-year report of February, second half sales in all markets started very slowly because of the impact of COVID-19 on patient examinations. In the UK, this trend has continued through our third quarter to 31 March and shows little sign of reversing meaningfully before year-end.

Whilst medical device disinfectant sales in the UK are significantly impacted by activity levels in the NHS, surface disinfectant product sales have continued to gain market share and UK sales for this product range to end of third quarter were £2.3m, 47% higher than in the same period last year.

Very encouragingly, at the end of the third quarter, sales of our 13 overseas subsidiaries and to our international distributor network have increased by 7% over the comparable period last year.

Combining our medical device and hospital surface disinfectants in both our home and overseas markets into a year-end outlook, we now expect global sales to exceed £31m, which is comparable with last year. This predicted outcome reflects a transient difficulty in the UK, caused by the impact of COVID-19 on patient examinations. We expect the situation to correct next year.

———————————————————————————————————–

Global sales were £31.7m for FY 2020, so let’s assume “we now expect global sales to exceed £31m, which is comparable with last year” translates into another £31.7m.

Global revenue was £16.8m for H1, so assuming £31.7m implies H2 global revenue of £14.9m — some 12-13% below the comparable H2.

UK surface-disinfectant sales of £2.3m for (I presume) the first three quarters seems about right. This slide from the blog post above…

… indicates Surface sales of £1.5m for H1 2021 and therefore another £0.8m was generated for Q3.

Overseas revenue up 7% for (I presume) the first three quarters indicates Q3 overseas sales took a turn for the worse.

Overseas revenue was £10.0m for H1 2021, up 20% on the £8.3m for H1 2020. H2 2020 overseas sales were £10.8m, so assuming an equal split, perhaps overseas sales for Q123 2020 were £8.3m+£5.4m = £13.7m.

7% up on £13.7m = £14.7m for Q123 2021, which less the £10.0m reported for H1 2021 gives £4.7m for Q3 2021. £4.7m is 13% down on my £5.4m Q3 2020 guess, and matches my above calculation for total H2 revenue dropping 12-13%.

My adapted chart below shows my best guess of Q3 2021 and Q4 2021, and is based on Q4 2020 and Q1 2021, which were impacted by the first lockdown:

To arrive at my predicted £14.9m revenue for H2 2021, sales of medical-device disinfectants come in at £11.1m, with surface sales of c£2m and other sales of c£1.8m.

The orange bars represent the additional medical-device disinfectant income needed to get to £14.9m assuming surface/other sales remain as they were. These orange bars therefore imply (perhaps!) the reduction to sales of medical-device disinfectants is slightly less this time around than during the original lockdown.

———————————————————————————————————–

The departments and types of treatment that we focus upon are experiencing many of the longest NHS waiting times. NHS sources quoted recently in the Press state the total numbers of people waiting for examinations in ENT is circa 366,000; ophthalmology 494,000; urology 270,000; cardiology 194,000, and gynaecology 265,000. These departments account for most of our medical device disinfectant product sales, and they also represent the highest patient waiting numbers in UK hospitals outside of orthopaedics, trauma, and general surgery. We understand that the NHS is making available a £1.5bn Elective Recovery Fund to accelerate the restoration of services and treatment for as many people as possible.

Looking out to next financial year, we expect demand conditions in the UK to improve significantly. However, in these uncertain times we believe that we must take a cautious approach. Whilst our global revenues continue to diversify away from the UK, our home market remains our largest exposure to one healthcare system. The NHS 2021/22 priorities and operational planning guidance published on 25 March 2021 states

“While [the vaccination programme] gives us cause for optimism, we do not yet know what the pattern of COVID-19 transmission will look like over the next 12 months and it is clear that the impact of the last year will be felt throughout 2021/22 and beyond.”

———————————————————————————————————–

The postponement of less pressing medical procedures was signalled in the H1 results. Clearly TSTL thought the resumption would occur sooner that it will. The NHS document TSTL referred to should be worth reading.

———————————————————————————————————–

Whist this year has been challenging, we have a strong balance sheet and have continued to build our team in preparation for future expansion. Accordingly, our cost base has risen during the year by approximately £0.8m, or 6%, excluding our investment in our North American regulatory programme. Given the scale of the opportunity in the United States, we have intensified our focus on our FDA and EPA regulatory programme and by year-end will have spent £750,000 in generating the scientific data required by the agencies compared to £80,000 last year. We will provide a detailed update with our year end results.

The consequence of sales being lower than anticipated in the year to 30 June 2021, at a gross profit margin of 80%, and a cost base that has increased, is that pre-tax profit (before share-based payments) is now expected to be not less than £5m.

———————————————————————————————————–

US costs of £750k matched the prediction cited within the FY 2020 presentation. A “detailed update with our year-end results” might suggest notable FDA progress could be reported in October.

The projected £5m pre-tax profit before SBPs compares to £7.1m for FY 2020. The H1 pre-tax profit before SBPs of £3.4m means H2 should deliver only £1.6m — versus £4.1m for H2 2020. So the sales shortfall has led to a major impact on profit.

An 80% gross margin matches gross margins witnessed during recent years and implies H2 2021 gross profit was £14.9m * 80% = £11.9m. If H2 pre-tax is £1.6m, then H2 admin costs (before SBPs) are £11.9m less £1.6m = £10.3m — versus £9.5m for H2 2020.

The £0.8m increase to H2 admin costs looks about right given the figures in the RNS concerning the greater US project expenditure and the workforce expansion.

———————————————————————————————————–

Balance sheet and dividends

Our cash position of £8m gives us security and stability. The interim dividend of £1.2m (2.62 pence per share) will be disbursed at the end of April as detailed in the half year report.

The expectation for the final dividend is 3.93 pence, giving a total of 6.55p for the year. The Board commits to make a final dividend payment at this level irrespective of the level of year-end profit.

Outlook

We remain very confident that sales and profits growth will resume next year and the investments that we have made in people, systems and new market registrations will lay the foundation stones for strong growth in the years ahead.

———————————————————————————————————–

Cash was £7.3m at the half year, so the reported £8m suggests £0.7m was added during Q3. An extra £0.7m cash for the quarter seems about right if my H2 2021 pre-tax guess of £1.6m proves accurate.

A 3.93p final dividend is just 2% higher than the comparable FY 2020 final dividend of 3.84p.

The shares at 570p remain highly priced at 45 times my 12.6p per share earnings guess from the blog post above. Clearly earnings for the current year will now come in well below that 12.6p, so the immediate questions at present are i) how long will TSTL’s sales and earnings take to recover? and ii) what are the growth prospects beyond that recovery?

All in all, an update that was perhaps not a complete surprise, but the elevated valuation does not leave any room for serious problems. The sales shortfall does seem temporary to me.

Maynard

Tristel (TSTL)

Ambu half-year 2021 results published 12 May 2021

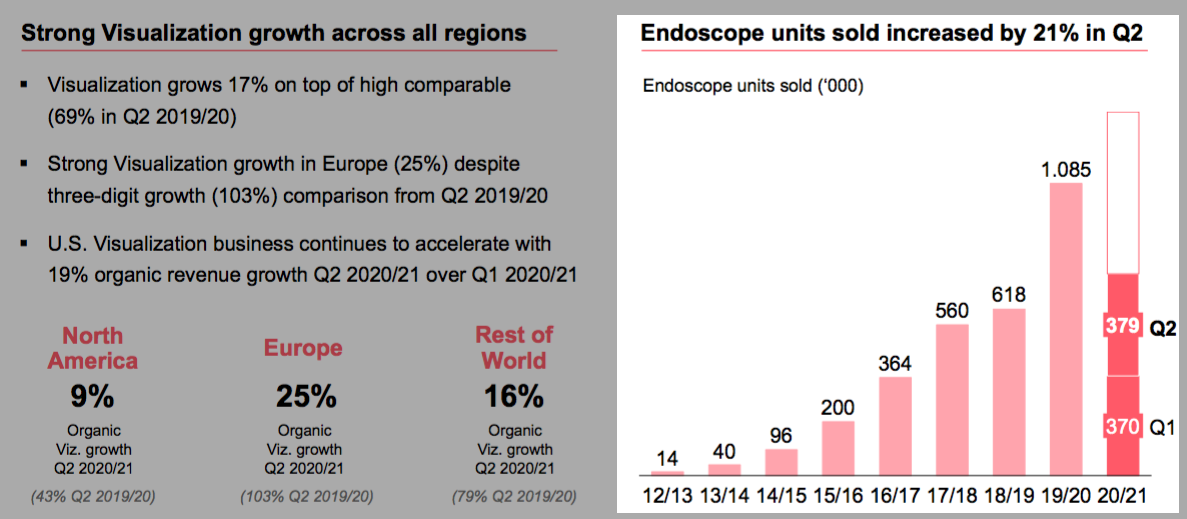

Sales of single-use endoscopes still booming at Ambu:

———————————————————————————————————–

Sales of single-use endoscopes reached 379,000 units for the quarter and 749,000 units for the half-year. Sales volumes were thus up 21% and 52%, respectively, relative to last year.

———————————————————————————————————–

Some unnerving slides from the accompanying presentation:

———————————————————————————————————–

———————————————————————————————————–

———————————————————————————————————–

———————————————————————————————————–

I need to look at this single-use threat closer.

Maynard

Tristel (TSTL)

Regulatory approval for EPA, Canada and South Korea published 24 June 2021

This RNS was a ‘Reach’ announcement — such statements convey non-regulatory information and ought not to be price sensitive. But the information TSTL provided appeared positive and included a few interesting snippets. Here is the full text interspersed with my comments:

——————————————————————————————————————

United States Environmental Protection Agency (EPA)

Tristel received its first approval from the EPA for its foam-based disinfectant for surfaces in April 2018. We successfully enhanced the performance claims of the product with a second approval in January 2019 and then registered the product in three States before curtailing the nationwide registration programme until a third submission could be made to bolster further the competitive positioning of the product. This submission was made in October 2020 and we have now received the third approval for Jet. This expands the product’s efficacy claims to include mycobacteria, and all efficacy claims are within a contact time of two minutes. We expect to complete State-by-State registration by the end of June 2022, including California where our existing registration will require amendment, which can be a lengthy process.

We have appointed Parker Laboratories, New Jersey, as our United States manufacturing partner for Jet and will sell the product through Parker’s nationwide network of distributors on a non-exclusive basis, commencing in FY23. Other distribution channels will be put in place ahead of the US launch.

——————————————————————————————————————

I think this means Parker Labs will finally have something to manufacture after agreeing a collaboration with TSTL back in March 2018!

I am not expecting revenue fireworks following this EPA approval, but let’s see what demand there is for a quality surface disinfectant in the States. Selling this surface disinfectant in the States may also provide an early indication of the likely uptake (or not!) for the high-level Duo ultrasound disinfectant still awaiting an FDA submission.

——————————————————————————————————————

Health Canada

Tristel Duo OPH has been approved by Health Canada as a class 2 medical device and is included in Health Canada’s Medical Device License Listing. Duo OPH is a high-level disinfectant intended for use on ophthalmic instruments including ultrasound devices and re-usable tonometers and lenses that contact the cornea.

We sell Duo OPH in over 15 countries and worldwide sales in FY21 will be approximately £650,000. Duo OPH is the only specialist high-level disinfection product for ophthalmic devices in the world. Awareness of the need for high-level disinfection in diagnostic eye care is growing, although COVID-19 caused ophthalmologists and optometrists in all countries to curtail their activities in 2020.

Parker Laboratories will manufacture the product and we are in discussions with potential distribution partners in Canada.

An explanation of the infection risks in ophthalmology can be found here.

——————————————————————————————————————

I get the impression Duo OPH, with revenue of £0.65m (just 2% of 2021 revenue of £31m) from 15 countries, may have limited sales potential in Canada. Nonetheless the approval opens up a new market.

——————————————————————————————————————

South Korea Ministry of Food and Drug Safety

We obtained approval for the Tristel Sporicidal Wipe from the Korean Ministry of Food and Drug Safety in March 2019. The application had taken four years as our chlorine dioxide chemistry had to achieve approval as a new drug. The Sporicidal Wipe is the key component in our Trio Wipes System, which is widely used for small endoscopic devices used in ear, nose and throat clinics.

Tristel Duo ULT has now been approved as a high-level disinfectant for ultrasound devices, and with Trio will be sold throughout South Korea by HP&C Ltd., Tristel’s distributor since 2013.

Duo is a hand-held dispenser which applies the Company’s powerful chlorine dioxide chemistry as a foam to the surface of medical devices. Tristel Duo is widely used throughout Europe, the Middle East and the Asia-Pacific region and the Company is seeking approval for Duo ULT from the United States Food and Drug Administration (FDA). Worldwide sales of all Duo branded products for medical device disinfection, including Duo ULT and Duo OPH, will exceed £4.3m in FY21.

Paul Swinney, CEO of Tristel commented: “Every regulatory approval we achieve represents an important milestone in our progress, and these three approvals are very significant.

“The enhanced claim set that we have achieved for Jet now justifies taking the product through state-wide registration in the USA and gearing up our manufacturing and distribution partnership with Parker Laboratories.

“The approval of Duo OPH by Health Canada represents our first successful registration of a medical device high-level disinfectant in North America. We are actively pursuing a submission to the USA FDA for Duo ULT and we are buoyed by this successful application in Canada.

“The approval in South Korea increases the visibility of our chlorine dioxide technology in the country and extends our distributor’s involvement into more clinical areas within a hospital.”

——————————————————————————————————————

Not sure whether South Korea will become a major TSTL market. The text above refers to the approval of the flagship wipe disinfectant in Korea during 2019, and yet TSTL has never really mentioned the country since. All I have in my notes is from this 2020 write-up:

* Management also disclosed its South Korean distributor sells ‘non-core’ products worth approximately £250k a year — but had struggled to sell a £60k order of ‘core’ disinfectants.

* The Korean distributor is apparently “very reluctant” to ask TSTL for onward-sales assistance.

Useful to know all Duo products generated revenue of £4.3m, to represent 14% of total 2021 revenue. I am guessing one of the main Duo contributors is Duo ULT, the ultrasound disinfectant that is still awaiting that FDA submission. Mind you, if Duo ULT at most generates sales of c£4m worldwide right now, then US sales of the product (if/when they eventually arrive) may not be immediately huge in terms of total group revenue. I can only hope subsequent FDA applications for TSTL’s wipes and other disinfectants will be less protracted, to justify the initial time taken to get a smaller product approved first.

Maynard

Tristel (TSTL)

Trading update published 21 July 2021

Sadly there was no TSTL open-day HQ extravaganza, or indeed an online open-day with webinar as seen last year, to coincide with this July update. Just a plain RNS.

Here is the full text interspersed with my comments:

——————————————————————————————————————

In the last update on 25 April, the Company stated that second half sales in all markets had started slowly because COVID-19 was causing the postponement of hospital admissions and fewer patient examinations with medical devices that Tristel’s products disinfect. The effect of the pandemic was being felt more acutely in the UK than in overseas markets. Conversely, sales of Tristel’s surface disinfectant products were ahead compared to last year.

In April, sales for the year ending 30 June were anticipated to be £31m and pre-tax profit (before share-based payments) to be no less than £5m.

As the fourth quarter progressed, demand for the device-based products accelerated as hospital out-patient departments gradually returned to pre-pandemic levels of activity. Surface disinfectant product sales have continued to grow.

It is expected that the upturn in sales activity, combined with a gross margin maintained at 80% and tight control over operating costs, will translate into sales of £31m (2020: £31.7m) and pre-tax profit (before share-based payments and the exceptional item explained below) of £5.5m (2020: £7.1m) for the year.

——————————————————————————————————————

Well the April statement said

“we now expect global sales to exceed £31m, which is comparable with last year”, which suggested a repeat of the £31.7m from 2020 for 2021. So £31m is a little disappointing, as I had hoped TSTL was ‘sand bagging’ its sales projection.

At least the pre-tax profit is higher than April’s prediction, but profit numbers can be ‘managed’ (e.g. juggling costs associated with the FDA submission, investment gains being recorded as operating income (see below), etc), and only the details in the full annual results will explain what has really occurred.

——————————————————————————————————————

In 2017, Tristel made an equity investment in a medical device company focussed upon women’s health. The investment led to a close collaboration between the two companies which has been a key influence in the development of Tristel’s 3T App and new exciting product development initiatives that are underway involving AI, and for which several patent applications have been made.

The Company’s shareholders had initiated a sale process for the business to enable the technology to find a home within a larger medical device company with the resources to succeed in the United States market. The process has not been successful to date, and whilst the company continues to operate as a going concern, Tristel will take a conservative approach to the carrying value of the investment, totalling £0.8m, and fully impair this in the financial year just ended. This expense is non-cash and will be recorded as an exceptional item.

——————————————————————————————————————

All this relates to MobileODT, and in the blog post above I did write:

*TSTL no longer mentions its £807k MobileODT shareholding.

*This investment was made during 2017, and the persuasive slides about disinfecting mobile colposcopes have not been witnessed since.

The write-off is therefore no great surprise. No surprise either to see TSTL deem the write-off to be exceptional. Note that the MobileODT investment did enjoy a £98k gain during 2019, and TSTL cheekily accounted for that gain as standard operating income. TSTL’s accounting treatment therefore depends on whether the investment has gained or lost value!

TSTL originally invested $750k, which looks to be cash lost despite TSTL’s usage of that awful “non-cash charge” phrase.

As I understand, the AI involved in this product was used to detect cervical cancer through images. I am unsure how TSTL can apply that same AI to disinfectants.

——————————————————————————————————————

As announced on 24 June 2021, Tristel has succeeded in gaining its first regulatory approval in Canada for the Duo OPH disinfectant for ophthalmic devices, and an enhanced approval for additional efficacy claims from the USA EPA for the Jet surface disinfectant product. A more detailed update on the progress of the USA FDA submission for Duo ULT for ultrasound probe disinfection and the commercial development plan for North America will be provided with the final results in October 2021.

——————————————————————————————————————

I do hope this “more detailed update” is an omen of positive submission news on the FDA application.

——————————————————————————————————————

Balance sheet and dividends

The Company’s cash position on 30 June 2021 was £8m compared to £6.2m last year.

The Board has committed to declare a final dividend of 3.93 pence, making a total of 6.55 pence for the year. This distribution level represents a one-off divergence from the Company’s stated dividend policy of two-times cover.

Outlook

Towards the end of the financial year the Company witnessed an increase in hospital admissions and patient examinations. The Company is confident that sales and profits growth will resume this year and the investments made in people, systems and new market registrations will lay the foundation for strong growth in the years ahead.

Paul Swinney, CEO of Tristel, commented: “The second half of the year was a frustrating period for the Company. Since Spring 2020 our ordinarily stable and predictable business has been disrupted by both Brexit and the pandemic. We have waited for signs that healthcare provision in our main twenty-five markets would return to normal, and finally we are seeing signs of this occurring.”

——————————————————————————————————————

Cash of £8.0m sounds about right. Cash at the end of H1 was £7.3m and the H1 dividend of £1.2m has since been paid. The cash position therefore increased by a net £1.9m (£8.0m less £7.3m plus £1.2m) during H2, which is close enough to the £2.1m pre-tax profit for H2 (the projected £5.5m less the H1 £3.4m). The £0.2m difference presumably relates to tax.

Interestingly enough, the April update said cash then was £8m, which was before the £1.2m H1 dividend payment due at the end of April. So TSTL seems to have generated cash of £1.2m during May and June, and only £0.7m between January and April.

Accurately interpreting short-term cash levels is always difficult, but the movements do seem to back up the management talk of disinfectant demand returning to “normal“.

Maynard