22 April 2021

By Maynard Paton

Results summary for S & U (SUS):

- A predictably Covid-blighted statement that confirmed extra write-offs of £19.5m, full-year profit diving almost 50% and the first annual dividend cut since at least 1987.

- Various calculations indicate credit quality at SUS’s motor-finance division declined by approximately 10%, due mostly to payment holidays.

- Management’s webinar comments claimed property-loan profit could quintuple to £5m within the next three years.

- Reduced net debt, interest charges at 3% plus fresh borrowing facilities suggest no obvious funding concerns.

- The £24 shares may already reflect improved collection rates, recovering loan transactions, new loan quality at a five-year high and the generally upbeat directors. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own SUS

- Results summary

- Revenue, profit and dividend

- Advantage Finance: Loan provisions

- Advantage Finance: Credit quality

- Advantage Finance: Payment holidays

- Advantage Finance: New loans

- Aspen Bridging

- Financials

- Valuation

Event links, share data and disclosure

Event: Preliminary results and presentation for the twelve months to 31 January 2021 published 30 March 2021 and results webinar hosted 31 March 2021 (email registration required)

Price: 2,400p

Shares in issue: 12,145,260

Market capitalisation: £291m

Disclosure: Maynard owns shares in S & U. This blog post contains SharePad affiliate links.

Why I own SUS

- Provides ‘non-prime’ credit to used-car buyers and property developers, where disciplined lending and reliable service have supported an enviable dividend record.

- Boasts veteran family management with 40-year-plus tenure, 50%-plus/£145m-plus shareholding and a “steady, sustainable” and organic approach to long-term growth.

- Offers the prospect of improved post-pandemic fortunes based on enhanced credit scoring, extended marketing partnerships and promising diversification into property loans.

Further reading: My SUS Buy report | All my SUS posts | SUS website

Results summary

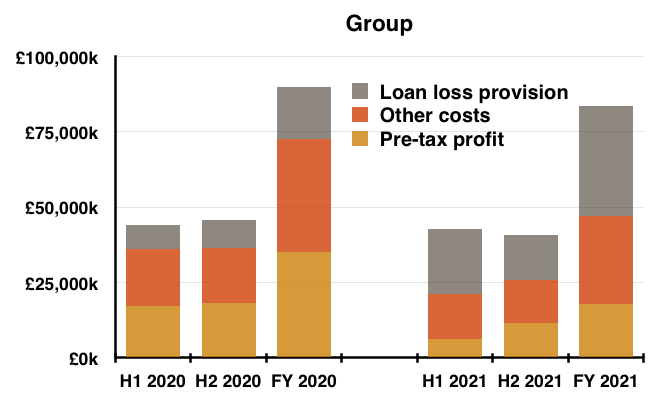

Revenue, profit and dividend

- Interim figures published during September had already confirmed these FY 2021 numbers would show significant pandemic disruption.

- But updates during December and February had revealed encouraging commentary about the second half and the potential for recovery.

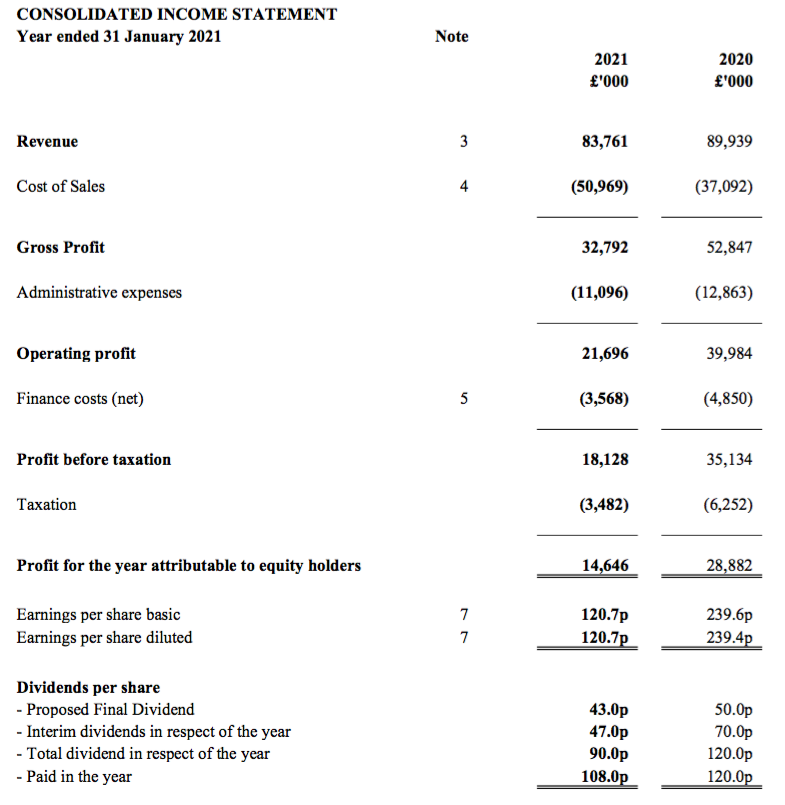

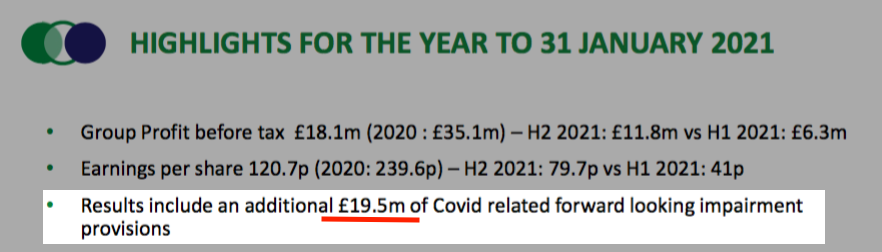

- For the full year, revenue slipped 7% but profit dived almost 50% following an additional Covid-19 bad-debt provision of £19.5m:

- The extra write-off meant profit fell back to levels last seen during 2016:

| Year to 31 January | 2017 | 2018 | 2019 | 2020 | 2021 |

| Revenue (£k) | 60,521 | 79,781 | 82,970 | 89,939 | 83,671 |

| Operating profit (£k) | 26,871 | 32,978 | 39,101 | 39,984 | 21,696 |

| Other items (£k) | - | - | - | - | - |

| Finance cost (£k) | (1,668) | (2,818) | (4,541) | (4,850) | (3,568) |

| Pre-tax profit (£k) | 25,203 | 30,160 | 34,560 | 35,154 | 18,128 |

| Earnings per share (p) | 170.7 | 203.8 | 233.2 | 239.6 | 120.7 |

| Dividend per share (p) | 91.0 | 105.0 | 118.0 | 120.0 | 90.0 |

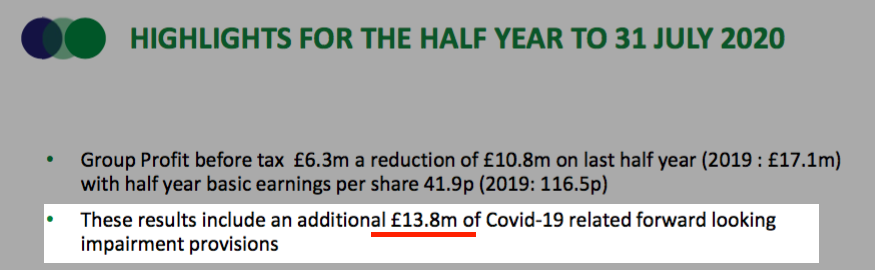

- September’s interim presentation revealed an additional Covid-19 provision of £13.8m…

- ….which meant the second half included a further £5.7m pandemic write-off.

- The finance director implied during the H1 webinar that the initial £13.8m provision ought to have reflected the bulk of the pandemic bad loans:

“We think [the £13.8m] is more of a one-off charge, it certainly should be, therefore the idea of IFRS 9 being forward looking is that you recognise some of the Covid impacts now as you understand them and then there’s only an adjustment going forward within the P&L account rather than another hit, unless we get hit by Covid-20 or Covid-21, in which case I will be wrong and I will come to you sheepishly and say that.“

- I was therefore surprised the Covid-19 provision for H1 was increased by 41% to £19.5m for the full year.

- The finance director explained (not very sheepishly) during the latest webinar that the £5.7m H2 provision reflected the extra lockdowns, additional FCA payment holidays and further repossession restrictions experienced after the first half (i.e. from 01 August 2020).

- Still, the lower pandemic provision for H2 versus H1 meant H2 2021 profit fell ‘only’ 35% from H2 2020 (from £18.1m to £11.8m):

- The additional £19.5m Covid-19 provision related entirely to Advantage Finance, the group’s car-loan subsidiary.

- The additional £19.5m Covid-19 provision meant Advantage’s run of 19 consecutive years of profit growth came to an abrupt end.

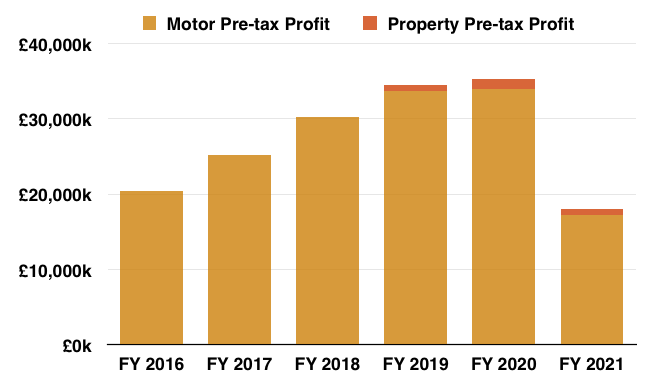

- Despite the additional pandemic write-offs, Advantage continues to dominate SUS’s profitability:

- SUS’s property-loan division, Aspen Bridging, delivered a very small profit although management was very confident of far greater future contributions (see Aspen Bridging).

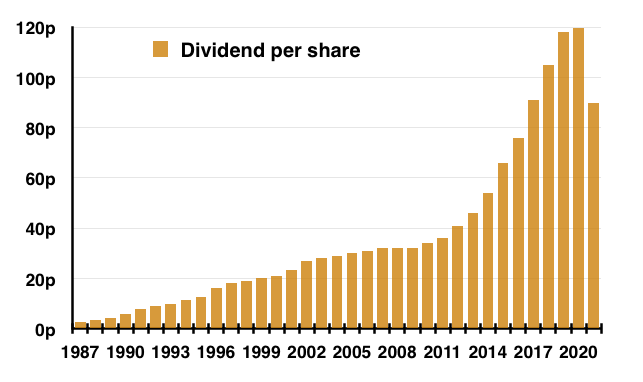

- Management said during the previous H1 webinar that the group was aiming to declare a full-year dividend of between 80p and 100p per share.

- These FY 2021 results unveiled a 43p per share final payout to give a total annual dividend of 90p per share.

- The final dividend was reduced by 14% versus a 35% reduction to the H1 payout.

- The full-year dividend reduction was the first for SUS since its payout was reinstated during 1987:

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Advantage Finance: Loan provisions

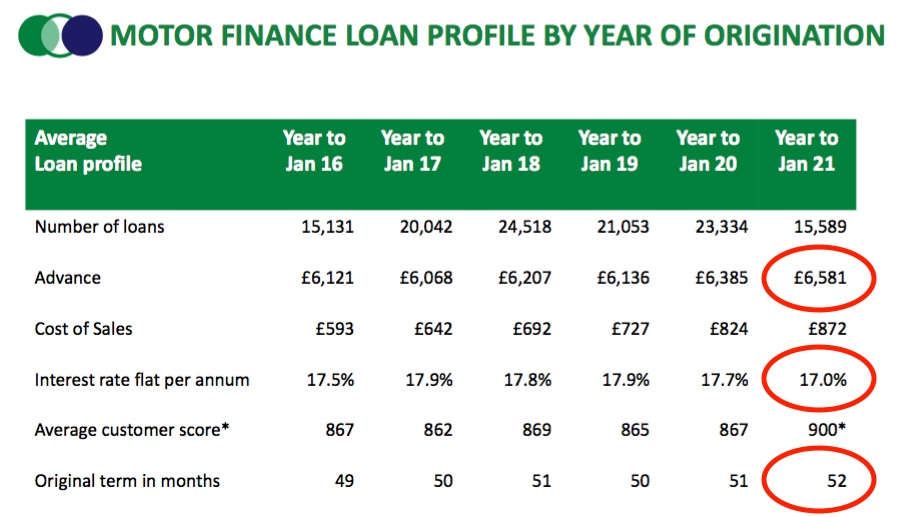

- The typical Advantage Finance customer has a patchy-but-improving credit history and borrows approximately £6.5k to buy a five-year-old used car.

- The customer is then expected to pay back £11.7k over 52 months — equivalent to a flat c17% interest rate:

- Customers are described by management as ‘non-prime’ — “borrowers that have had a problem in the past but are on an upward trend” (point 3).

- Management noted on the webinar that customers on average repay £9.5k of the £11.7k expected.

- Collecting £9.5k of £11.7k implies 18.8% (i.e. £2.2k/£11.7k) of money loaned is never repaid.

- That 18.8% proportion is reflected by the c18% bad-debt provisions against total money loaned for FY 2019 and FY 2020 below:

| Year to 31 January | 2019 | 2020 | 2021 |

| Motor | |||

| Gross amounts receivable (£k) | 316,655 | 344,131 | 339,349 |

| Less loan provision (£k) | (57,845) | (63,374) | (92,583) |

| Net amounts receivable (£k) | 258,810 | 280,757 | 246,766 |

| Loan provision/Gross amounts receivable (%) | 18.3 | 18.4 | 27.3 |

- For this FY 2021, the bad-debt provision included the aforementioned Covid-19 charge of £19.5m and represented 27% of total money loaned.

- The 27% proportion suggests SUS will now receive 73%, or £8.5k, of every £11.7k expected.

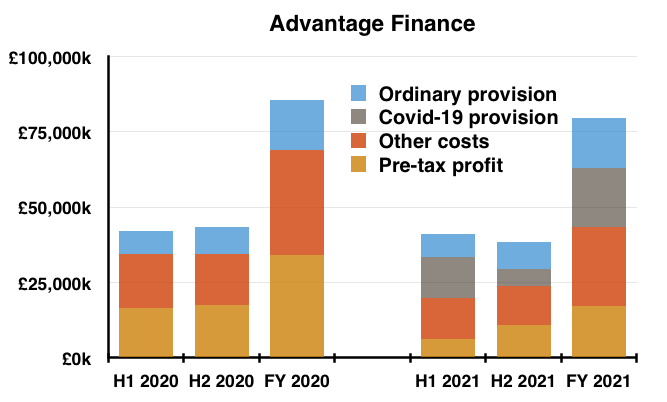

- The chart below shows the effect of the extra Covid-19 provisions (grey boxes) on Advantage’s income:

- Note the ordinary loan provision (blue boxes) for FY 2021 matched that recorded for FY 2020 (at £16.5m).

- Note, too, that other costs (red boxes) for FY 2021 reduced by 30% (to £13.6m) due mostly to processing 33% fewer new loans (from c23k to c16k).

- Management described Advantage’s overall performance as “very creditable“.

Advantage Finance: Credit quality

- SUS said:

“This year, despite the payment holidays which affected nearly 21,000 of our customers and resulted in an estimated £13m lower collection, total cash collected at Advantage was £180m against £196m last year.

This resulted in a monthly collection rate against contractual due of nearly 84% (2020: 94%) which, despite Covid, reflects the excellent relationships Advantage has always enjoyed with its customers.“

- Total cash collected declining by £16m to £180m implies an 8% reduction to credit quality.

- Monthly collection rates declining from 94% to 84% implies an 11% reduction to credit quality.

- The 8% to 11% deterioration to credit quality is supported by various other calculations.

- Collecting the aforementioned £8.5k instead of the usual £9.5k from each £11.7k expected suggests an 11% reduction to credit quality.

- The following table shows revenue (i.e. loan interest received) per customer dropping 10% to £1,253 during FY 2021:

| H1 2020 | H2 2020 | FY 2020 | H1 2021 | H2 2021 | FY 2021 | ||

| Revenue (£k) | 42,089 | 43,376 | 85,465 | 41,187 | 38,366 | 79,553 | |

| Average no. of customers | 60,571 | 63,112 | 61,667 | 63,849 | 63,129 | 63,488 | |

| Revenue/customer (£) | 1,390 | 1,375 | 1,386 | 1,290 | 1,215 | 1,253 |

- This next table shows total revenue (i.e. loan interest received) from every £1 of outstanding loans dropping 12% to 23.3p during FY 2021:

| H1 2020 | H2 2020 | FY 2020 | H1 2021 | H2 2021 | FY 2021 | ||

| Revenue (£k) | 42,089 | 43,376 | 85,465 | 41,187 | 38,366 | 79,553 | |

| Average gross amounts receivable (£k) | 324,785 | 338,523 | 330,393 | 343,751 | 341,360 | 341,740 | |

| Revenue per £1 gross amount receivable (p) | 25.9 | 25.6 | 25.9 | 24.0 | 22.5 | 23.3 |

- Revisiting that earlier table…

| Year to 31 January | 2019 | 2020 | 2021 |

| Motor | |||

| Gross amounts receivable (£k) | 316,655 | 344,131 | 339,349 |

| Less loan provision (£k) | (57,845) | (63,374) | (92,583) |

| Net amounts receivable (£k) | 258,810 | 280,757 | 246,766 |

| Loan provision/Gross amounts receivable (%) | 18.3 | 18.4 | 27.3 |

- …total bad-debt provisions increased by almost £30m to £93m during FY 2021.

- That £30m represents an extra 9% of the total loans outstanding of £339m.

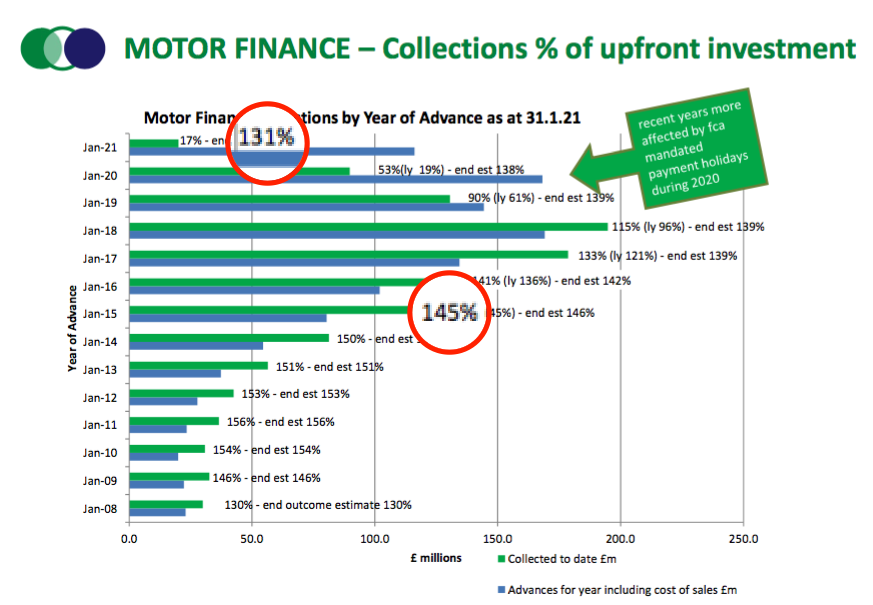

- The presentation slide below shows loans arranged during FY 2015 — that is, with the subsequent five-year repayments barely affected by the pandemic — generating total cash collections representing 145% of the initial money lent:

- The same slide also reckons loans arranged during FY 2021 — that is, with the subsequent five-year repayments affected heavily by the pandemic — could generate total cash collections representing 131% of the initial money lent.

- Total cash collections declining from 145% to 131% implies a 10% reduction to credit quality.

- As far as I can tell, the above calculations all point to the pandemic causing credit quality to decline by between 8% and 12%.

- I would have gratefully accepted credit quality declining by between 8% and 12% at the start of the pandemic.

Quality UK investment discussion at Quidisq. Visit forum.

Advantage Finance: Payment holidays

- The lower credit quality relates mostly to the payment holidays allowed by the FCA.

- The last FCA update on the subject was published on 25 March 2021 and noted:

- Borrowers could apply for payment holidays until 31 March 2021;

- Borrowers could take total payment holidays of up to six months;

- All payment holidays will end on 31 July 2021, and;

- Repossession restrictions had been lifted on 31 January 2021.

- SUS has previously expressed frustration at the payment holidays. In fact, management claimed during the H1 webinar that 40% of customers that had enjoyed a payment holiday were not financially affected by the pandemic.

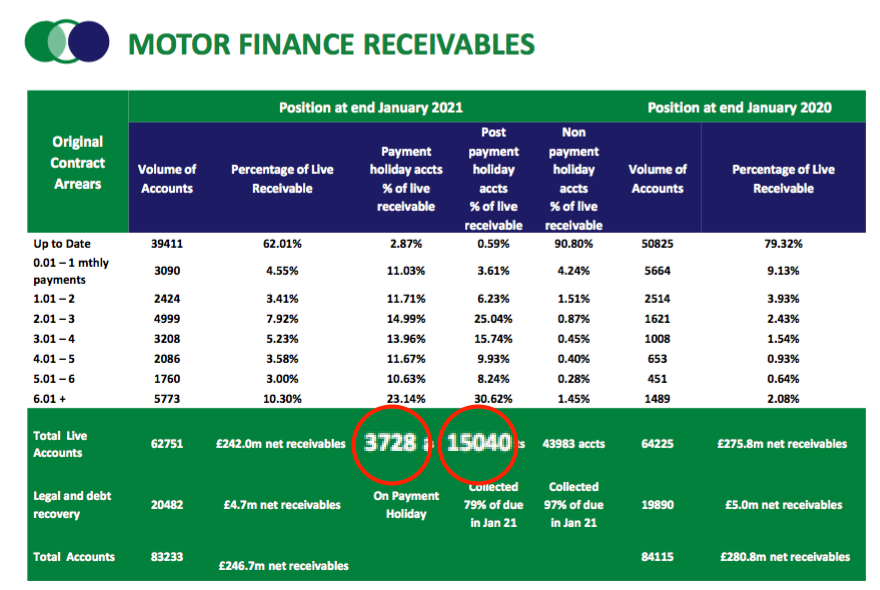

- The preceding H1 results said 16,500 Advantage customers had taken a payment holiday. This FY 2021 statement said the number had risen to nearly 21,000, although the presentation slides suggested the figure was closer to 19,000:

- £242m owed by 62,751 accounts suggests each Advantage customer has on average £3,857 still to repay.

- 3,728 customers were taking a payment holiday at the 31 January 2021 year end, and may still owe Advantage a total of approximately £14m (3,728*£3,857).

- 15,040 customers had concluded a payment holiday before the 31 January 2021 year end, and may still owe Advantage a total of approximately £58m.

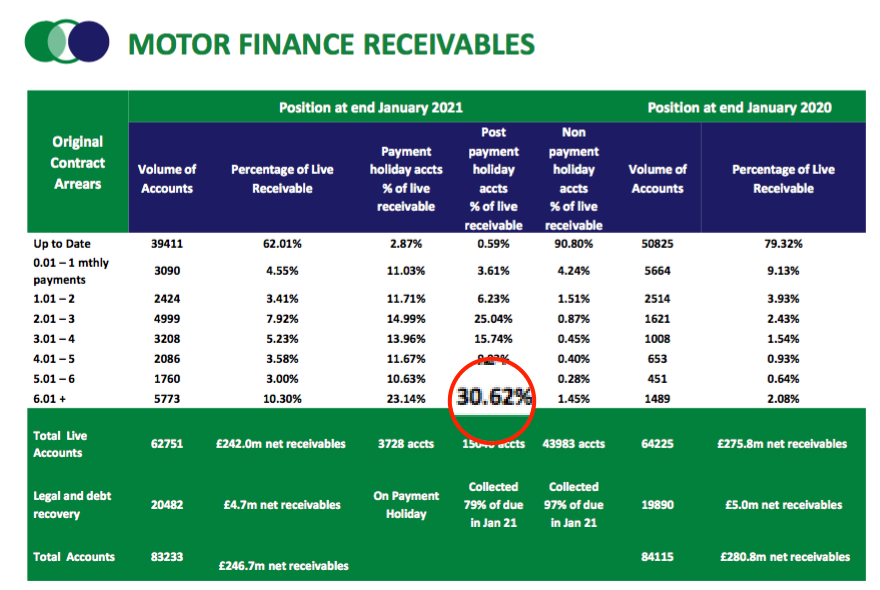

- Note that 30.62% of accounts that had taken a payment holiday were more than six months behind with their payments:

- With payment holidays lasting no more than six months, this 30.62% cohort appears not to have recommenced payments.

- But on the flip side, 69.38% of post-holiday accounts were less than six months in arrears, which might suggest the majority of holiday-payment customers have recommenced payments.

- The recommencement of payments from holiday accounts is underlined by the improving collections rate.

- The preceding H1 statement had revealed overall Advantage collections had “rebounded to 85% of due“.

- Then the December update said collection rates were “87.5% of due“.

- And then the February update said monthly collections had “improved to 90% of contractual terms due“.

- For comparison, the collection rate for the comparable FY 2020 was 94%.

Advantage Finance: New loans

- New car loans issued during H2 matched the number issued during H1:

- SUS reckoned new loans came with better credit quality:

“This year has seen further strengthening of [Advantage’s] under-writing “black box” as it has continued to widen its use of credit information and refine its scorecard… Evidence of the improvement in customer repayments this should bring about is in our first payment statistics which at 98.5% are now up on pre-Covid levels.“

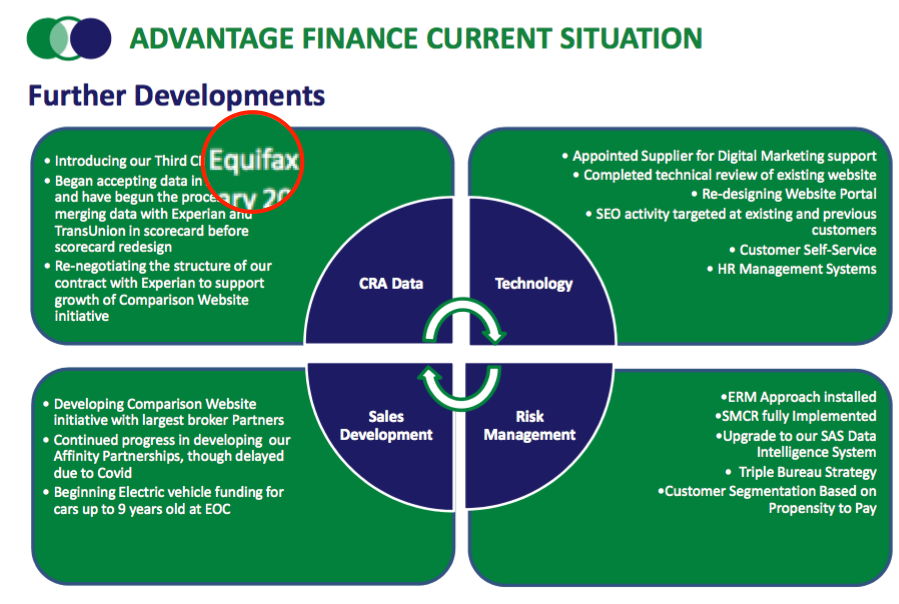

- The presentation indicated Equifax had joined Experian and TransUnion as data suppliers to Advantage’s “underwriting black box“:

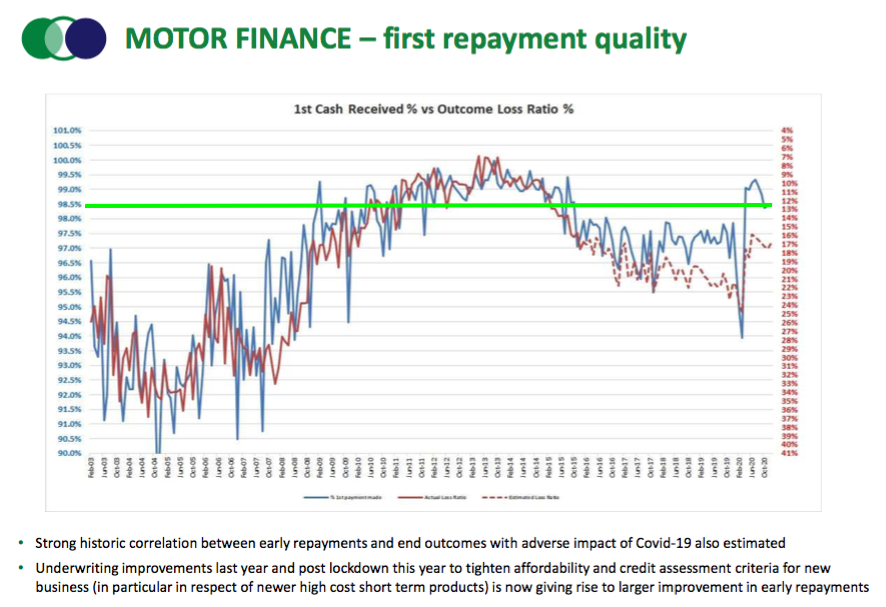

- Advantage’s first-payment statistics remain encouraging:

- The blue line (left axis) reflects the percentage of customers making their first payment on time.

- At 98.5%, the proportion is back to levels last seen five years ago.

- The unbroken red line (right axis) shows the actual ‘outcome loss ratio’, which correlates strongly to the first-payment percentage.

- The dotted red line (right axis) shows the predicted ‘outcome loss ratio’, which has diverged slightly from the blue line to reflect the greater uncertainty of repayments following the pandemic.

- Management has previously mentioned the first-payment improvement from 2007 to 2012 was due to the banking crash prompting rivals to withdraw from the sector.

- During that time Advantage faced less competition for its target ‘non-prime’ customers.

- Competition then returned and credit quality therefore softened, until the pandemic prompted much tighter underwriting and other lenders to hibernate once again.

- The implication — perhaps — is that the blue line can remain favourable in a manner similar to that experienced between 2007 and 2012.

- Management implied on the webinar that Advantage enjoyed a 10% market share of the non-prime sector, with Moneybarn, owned by Provident Financial, at 30%-35%.

- With a better quality of customer, perhaps the number of new car loans does not need to recover to pre-Covid levels for Advantage’s profit to recover to pre-Covid levels.

Aspen Bridging

- Established four years ago, Aspen offers property bridging loans for small/individual property developers/investors with awkward financial circumstances.

- To date £111m has been lent through 234 property loans with a monthly interest rate of approximately 1% and a typical term of 11 months. These case studies give a flavour of the transactions involved:

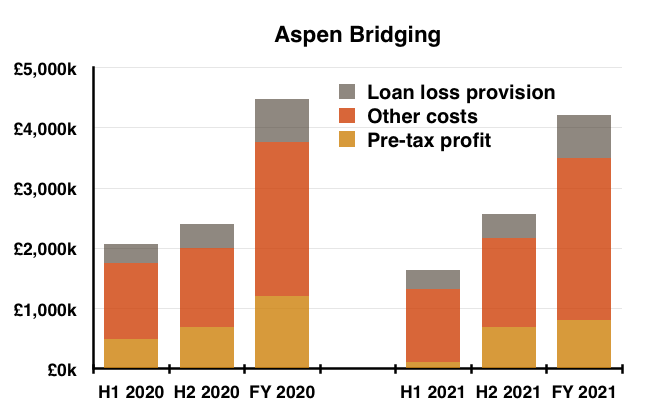

- Aspen’s profit rebounded strongly during H2 following the lockdown-depressed H1:

- Aspen lent a bumper £32m through 55 new agreements during H2. By comparison, H1 witnessed £11m lent through 25 new loans while FY 2020 witnessed £31m lent through 57 new loans.

- Aspen did not suffer any Covid-19 write-downs. SUS in fact confirmed:

“Loan quality has improved over the past year and Aspen now has no loans past due and no defaults over the entire book.“

- S&U claimed a more competitive product range, new broker relationships and incentivised “key partners” had helped create the promising outcome.

- A combination of a revitalised housing market and loans backed by property (and not used cars) presumably assisted Aspen’s progress.

- SUS was bullish on Aspen’s future, saying the improved loan quality had given the division…:

“… both the base and the momentum for… substantial growth it expects in the coming year. As a result, our deliberately cautious investment in the business is anticipated to double during the coming year and this is expected to deliver a significant rebound in profits.”

- Management comments on the webinar were even more optimistic, with talk of a £5m Aspen profit within two to three years.

- A £5m Aspen profit represents a quintupling of the division’s £0.8m FY 2021 contribution.

- Management also mentioned on the webinar that Aspen’s return on capital employed (ROCE) could be “12% at scale“.

- Attaining a £5m profit from a 12% ROCE implies invested capital of £42m is required.

- For perspective, Aspen reported its £0.8m profit on assets of £34m for this FY 2021.

- Aspen’s assets of £34m comprised 69 agreements of an c£493k average and represented 14% of the group’s entire net loan book.

- Note that Aspen’s deputy chief executive, Jack Coombs, was recently appointed as a main board director.

- The appointment could signal Aspen becoming of greater importance to the wider group.

Financials

- Fewer transactions during FY 2021 (total advances dropped from £180m to £146m) meant collections went towards reducing debt rather than funding new customer loans.

- Net debt finished the year £19m lower at £99m:

| Year to 31 January | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating profit (£k) | 26,871 | 32,978 | 39,101 | 39,984 | 21,696 |

| Depreciation (£k) | 253 | 294 | 414 | 450 | 520 |

| Net capital expenditure (£k) | (308) | (1,040) | (785) | (265) | (1,112) |

| Working-capital movement (£k) | (48,488) | (68,881) | (19,041) | (24,067) | 20,901 |

| Net debt (£k) | (49,167) | (104,990) | (108,037) | (117,844) | (98,794) |

- SUS’s working-capital movements broadly show the net effect of new money loaned versus repayments received.

- During the years preceding FY 2021, working-capital movements were always negative as SUS reinvested customer repayments into new loans.

- The £21m positive working-capital movement for the year was derived mostly during H1:

| H1 2020 | H2 2020 | FY 2020 | H1 2021 | H2 2021 | FY 2021 | ||

| Operating profit (£k) | 19,410 | 20,574 | 39,984 | 8,298 | 13,398 | 21,696 | |

| Working-capital movement (£k) | (20,717) | (3,350) | (24,067) | 18,804 | 2,097 | 20,901 | |

| Other cash-flow movements (£k) | (5,234) | (5,737) | (10,971) | (6,183) | (3,474) | (9,657) | |

| Operating cash flow (£k) | (6,541) | 11,487 | 4,946 | 20,919 | 12,021 | 32,940 |

- The aforementioned bumper lending by Aspen during H2 probably caused the lower cash generation during the second half.

- After a net £19m was used to repay debt, full-year cash flow from operations of £14m was used to fund dividends of £13m and capital expenditure of £1m.

- Bank interest during the twelve months was £3.5m, implying SUS’s borrowings incur interest at approximately 3%. The implied rate for H2 was lower at 2.8%.

- The 2020 annual report (point 16) claimed SUS borrows money from mainstream banks at 4% to then lend out at 28%.

- The wide, 24% net interest margin is required to cover debt impairments and operating costs, and in turn earn a respectable return on the capital employed (see below).

- The annual interest payment was covered a reasonable 9-10x by operating cash flow.

- Net debt of £99m compares to a group net loan book of £281m.

- SUS’s lenders do not seem too worried about the group’s borrowings. This FY 2021 statement revealed more debt had been taken on:

“Over the next two years our growth prospects and strategy will require additional funding. This is why post year-end we have put in place additional longer-term facilities of £50m on terms up to eight years. This provides total committed Group facilities of £155m which will be augmented as required.“

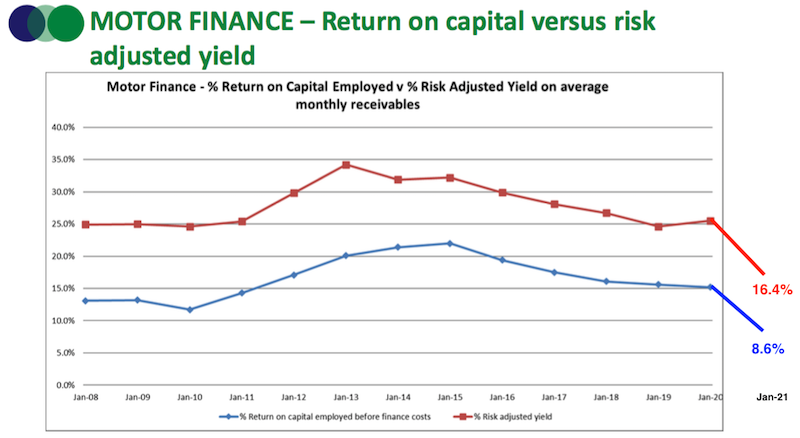

- After omitting the stats at the half year, SUS reported Advantage’s ROCE was 8.6% and risk-adjusted yield was 16.4%.

Note: risk-adjusted yield is a ‘profit margin’ KPI used by SUS and is calculated as:

(revenue – loan provision) / average outstanding customer loans

- SUS did not include the usual slide showing Advantage’s ROCE and risk-adjusted yield, so I have amended last year’s slide below:

- Advantage’s ratios were of course depressed by the extra Covid-19 loan impairments.

- The group’s overall margin and return on equity were impacted as well:

| Year to 31 January | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating margin (%) | 44.4 | 41.3 | 47.1 | 44.5 | 25.9 |

| Return on average equity (%) | 15.2 | 16.7 | 17.6 | 16.8 | 8.1 |

- How the ratios perform from here remains very relevant to shareholders.

- I am hopeful Advantage’s ROCE and risk-adjusted yield will eventually return to pre-pandemic levels (and the missing slide can therefore return).

- SUS maintains a tiny defined-benefit pension scheme that last carried a surplus (point 18).

Which is best for stock-screening: Stockopedia or SharePad? See my verdict.

Valuation

- Management sounded a confident tone for recovery:

“Although uncertainty still surrounds the economic climate following Covid, the skies are definitely brightening.”

“My confidence in our superb staff, our financial strength and sound strategy allows me to predict a return to S&U’s habitual levels of success.“

“All this means that S&U’s habitual caution should now be seasoned with ambition and optimism for the next two years.“

“We fully expect to see a gradual and sustained rebound in Group Profits. Current initiatives in both businesses may even accelerate this recovery.”

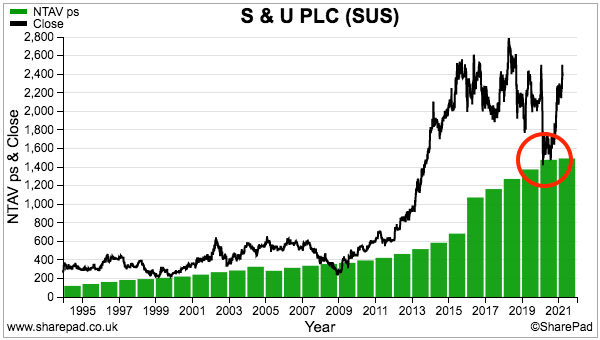

- The share price has responded and no longer trades anywhere close to the depressed book-value levels of last year:

- In fact, the recent £24 price was occasionally seen prior to the pandemic… suggesting upside potential from a full earnings recovery is now quite limited.

- A return to pre-pandemic FY 2020 earnings of 240p per share would place the £24 shares on a ‘post-pandemic’ P/E of 10.

- These shares have typically traded on a very average/modest multiple. The £28 peak achieved during May 2018 equated to a trailing P/E of 13.7.

- The recent share-price revival seem understandable and may reflect:

- The end to payment holidays, a return to greater collections and no further Covid-19 write-offs;

- Potential market-share gains as competitors struggle with their lower-quality loans;

- A history of recovering well following the banking crash;

- Enhanced “black box” calculations leading to new customer quality at a five-year high;

- Much higher profits from Aspen;

- Promising initiatives such as affinity schemes, comparison websites and electric-vehicle funding, and/or;

- Sale volumes at Advantage perhaps having recovered to 100% of the pre-pandemic budget:

- Possibly the main support for a likely recovery is the presence of canny veteran executives, who through various family parties control at least 50% of SUS and have been involved at the company since the mid-1970s.

- The 2020 annual report (point 7) reminded shareholders of the long-term benefit of these owner-managers:

“Family investment and management has over the last 80 years been reflected in ambition for growth and for new markets buttressed by a conservative approach to risk, to treasury activities and to return on capital employed…”

“Mr Anthony Coombs was appointed Chairman in 2008 as part of an established succession plan reflecting the Coombs family’s majority holding in S&U, the identity of interest between management and shareholders and the consequent success of the Company.”

- The “conservative approach to risk” appears to have proven its worth during this FY 2021.

- While a profit recovery is awaited, the 90p per share dividend gives a 3.75% income at £24.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

S & U (SUS)

Directorate changes published 14 April 2021

Very possibly a significant boardroom development for two reasons — the growing influence of Aspen Bridging, and long-term executive succession.

Here is the full text:

———————————————————————————————————–

S&U plc (LSE: SUS), the specialist motor finance and bridging lender, announces that in the light of his family’s relocation to Switzerland, Fiann Coombs will not be seeking re-election as a Director of S&U plc at the forthcoming AGM and will therefore be resigning from the role on the AGM date of 20th May 2021. The Board would like to thank Fiann for his wise and astute advice and guidance over the 19 years he has been a Director.

S&U plc separately announces the appointment of Jack Coombs to the Board of S&U plc as an Executive Director with immediate effect. Jack is a 33-year-old Chartered Accountant who joined the S&U Group in 2016 as Group Development Executive, having previously worked in PwC’s Valuations team. Jack is Fiann’s brother and he is a major shareholder in S&U plc owning 1,677,147 ordinary shares representing 13.82% of total voting rights. He is currently working as a Director of our successful and profitable property bridging subsidiary Aspen Bridging Limited.’

———————————————————————————————————–

I must admit I was not sure whether Jack Coombs was future leadership material. Seems like Jack’s uncles, brothers Anthony and Graham Coombs (executive chairman and executive deputy chairman respectively), have decided he could be. Jack Coombs is in his 30s while Anthony and Graham Coombs are both late-60s.

Jack Coombs received the bulk of his 1.7m shares from Jennifer Coombs during August last year (RNSs here and here). 1.7m shares at £24 each is £40m. The 2020 annual report said brother Fiann owned 284k shares worth £7m. I note Jack’s 1.7m shares exceed the 1.3m owned by Anthony Coombs and the 1.6m owned by Graham Coombs.

The blog post above recounts management webinar remarks of Aspen aiming for profit of £5m (versus <£1m for FY 2021), and this appointment I reckon says that growth prospect is more than just the usual optimism from company directors.

Hi Maynard,

Great article on a company which I have a lot of admiration for, and hold shares. Your analysis of the impact of the pandemic on credit quality is very good. I like the way you have looked at it from a number of angles.

I watched the presentation on Investor Meet Company and was surprised at how bullish Mr Coombs was (not naturally bullish character). I was also very impressed by the lengths they went to answer all of the questions put to them. This is quite unusual in my experience and shows an alignment with shareholders.

I am hoping that the H2 additional bad debt provision will prove to be over cautious and can be partially reversed in due course due to better receipts. I suspect they would have been forced by auditors to put through very prudent provisions, as the year end was at the height of the recent lock down. So I would hope this will surprise on the upside in due course.

One bear point:

Upstart.com

Comment noted from a post on Stockopedia. This is an American “disrupter” which is looking at the application of AI to consumer credit lending. It is something to have in the back on mind when thinking about an investment in this industry as I would have thought there is potential for AI to significantly impact insurance in the future. Upstart talk about :

Higher approval rates

Lower loss rates, therefore lower cost for everyone

Automated experience for customers, reducing cost

Hi James

Glad you found the blog post of use. Must admit getting my head around all the stats took a while. Yes, management was bullish on the IMC webinar, especially on the property side. The text in the results RNS was a tad more optimistic than usual as well. So the omens seem positive. Management did answer lots of questions on the webinar, although I must admit some of the questions were somewhat unsophisticated and would have been answered from reading the annual report. A good alignment of shareholders does exist, and the next generation of Coombs has been appointed to the main board. So I am hopeful that alignment can continue for some time.

Good point on AI. Not something I had considered. If AI genuinely works, then the entire lending and perhaps insurance industries could be ripe for disruption. Of course the lenders may adopt/apply AI themselves. The credit-scoring agencies may be at risk here. If SUS can apply AI to its own data without the need for external credit-scoring info, then maybe SUS could benefit. Also, management has said the company “sells to people, not algorithms” (point 3) — and I dare say an experienced employee could determine a good borrower from a bad borrower during a phone conversation, unlike an AI computer perhaps.

Maynard

S & U (SUS)

AGM Statement and Trading Update published 20 May 2021

A promising update. Here is the full text interspersed with my comments:

——————————————————————————————————————

S&U PLC, the leading specialist motor finance and property bridging lender, issues a trading statement for the period 1st February 2021 to the 19th May 2021 prior to its AGM today. As last year, Covid restrictions dictate a closed AGM but S&U will be holding a question and answer session for registered shareholders at 11:30 am today, the 20th of May. Details on how to access the conference are in note 9 of the AGM notice.

As outlined in our Chairman’s statement accompanying the full-year results published in March, the Group has weathered the Covid pandemic and its consequences quite superbly. All S&U staff are well and looking forward to the new “normality”. For Advantage Finance (“Advantage”) this means that currently 60 staff are back at our Grimsby offices with 120 expected to return at the end of June. Aspen Bridging (“Aspen”) also expects to return to its Solihull offices by the end of June.

All staff, however, are being given the option of flexible continued homeworking, to which they have adapted so successfully over the past year.

As a result of their sterling efforts, the Group continues its strong recovery as both motor and housing markets revive and as, more generally, the UK is poised for 7% GDP growth this year. Profitability for the period in our Advantage motor finance business and in Aspen, our property bridging arm, was ahead of group projections. Loan advances and collections rates in the period were ahead of the same period last year, whilst Group net receivables are now around £295 million.

——————————————————————————————————————

Profitability running “ahead of group projections” is encouraging. Net receivables were £281m at the end of January 2021, indicating a £14m advance in the subsequent 3.5 months. Net receivables peaked at £302m at January 2020, so perhaps the current run-rate of new loans will set a new record by the January 2022 year end.

——————————————————————————————————————

Advantage Finance

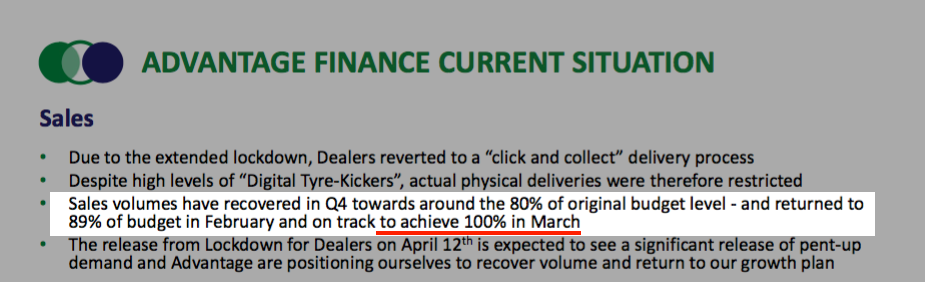

Advantage Finance has produced an excellent first quarter, ahead of expectations, and continues to invest in operational improvements which will strengthen its market position, risk profile and efficiency.

Although the bounce in loan advances anticipated following the reopening of motor dealerships in April was less than expected, year on year advances growth continues to accelerate and new business quality has continued at a very good level. Advantage continues to develop its offering across the non-prime motor spectrum, which is reflected in the quality of new customers it is attracting. As well as developing closer links with its loyal introducer partners, Advantage is making good progress in its own digital marketing and in providing loans for the nascent electric vehicle market. Indeed, Advantage is supporting the Finance and Leasing Association in its work to try to create a Green Finance Guarantee with HM Treasury.

Monthly collection rates are cumulatively above budget and an excellent £12.6 million of monthly collections were reached in April. Covid-related FCA “payment holidays” have now fallen to just 1,200 customers from the cumulative 21,527 customers originally taking such deferrals. Customers unaffected by “payment holidays” maintain their usual excellence, and even those returning from “payment holidays” have now returned to levels at 85.4% of due, as the labour market strengthens and consumer confidence revives.

Hence, the trends currently observed at Advantage make us optimistic that profit recovery and advances growth will meet our expectations this year. We are laying the foundations for a return towards Advantage’s historic levels of profitability.

——————————————————————————————————————

A first quarter “ahead of expectations” and “new business quality has continued at a very good level” sound positive.

Monthly collections of £12.6m for April compare to a £12.0m average for the six months to January 2021. Payment-holiday customers of 1,200 compare to 3,728 at January 2021. Payment-holiday customers repaying 85.4% of due compares to 79% for January 2021. So improvements all round.

Group net receivables of £295m less Aspen net receivables of £50m (see below) indicate Advantage net receivables are £245m.

Advantage net receivables were £246m at January 2021, therefore indicating the cited “profit recovery” will be led initially by improved credit quality rather than extra loans.

——————————————————————————————————————

Aspen Bridging

Fuelled by a rising and buoyant residential property market in which price levels currently stand 7% ahead of 2020, Aspen, is set for a record year. Early transaction numbers have been boosted by Aspen’s authorisation for the Government guaranteed CBILS scheme, so that current net receivables have reached over £50 million. Whilst the past quarter has also seen an increase in average gross loan size to £1 million per deal, book quality is at its best ever level. Thus, the first quarter saw repayment collections at £11.5 million – or nearly three times the figure last year.

Profitability in the first quarter reflects this and April saw a record surplus for the business. Costs remain close to budget despite systems investment and new recruitment, reflecting the increase in business. Meanwhile underwriting processes and standards continue to be refined, valuations remain conservative, and overall maximum gross LTVs have reduced to just 59%.

——————————————————————————————————————

Net receivables of £50m compare to £34m at the end of January 2021. So up more than 50% in 3.5 months. April seeing a “record surplus” is welcome, too. Maybe the executives were right when they claimed during the results webinar that Aspen could deliver a £5m profit during the next 2-3 years.

——————————————————————————————————————

Treasury

Both our very encouraging business prospects and our traditionally conservative Treasury policy have resulted in further strengthening of S&U’s Treasury position during the first quarter. The latter is reflected in Group gearing of just 60%, and current medium-term facilities standing at £155 million against borrowings of £111 million. In my statement for S&U’s full-year results, I said that “our growth prospects and strategy will require additional funding”; I am therefore pleased to report an additional £25 million of funding arranged during the period. This takes Group facilities to £180 million, which provides appropriate scope for the Group’s future growth.

Commenting on S&U’s trading outlook, Anthony Coombs, S&U chairman, said:

“The financial year has started very well for S&U – a recovery which, as the British economy resumes growth, we expect to continue. With our habitual determination, imagination and commitment we remain very confident as to the Group’s prospects for this year.”

——————————————————————————————————————

Borrowings of £111m compare to £99m at January 2021. Gearing at 60% compares to 55% at January 2021 but 65%-68% for Januarys 2018, 2019 and 2020. So still scope for debt to advance c10% without gearing breaching recent levels.

Management on the results webinar did not rule out gearing heading to 90% in the next few years if the right opportunities appeared (mainly for Aspen I think).

Banking facilities were £130m at January 2021, and were subsequently lifted to £155m and now to £180m, which implies SUS is preparing for notable expansion. The normally conservative chairman meanwhile sounds very bullish, suggesting a return to FY 2020 levels of profitability may occur sooner than had been expected.

Maynard

S & U (SUS)

Publication of 2021 annual report

Here are the points of interest:

1) Strategic report

Some snippets about the used-car market:

1.5 million loan applications a year compares to 1.35+ million for FY 2020 and 0.75+ million for FY 2017.

Electric-vehicle financing opportunities may become “significant” during the next five years:

Further confirmation of the positive prospects for Aspen, and why the division can outmanoeuvre large banks:

A reminder of what underpin’s SUS’s success:

2) Risks

No major changes here.

SUS seems to take a dig at having to make an economic forecast, but nevertheless reckons “pent up demand” should revive the economy:

Some new risk text for this year, including a claim of an “excellent” FCA relationship:

3) Testimonial

Another namecheck for super-employee “Natalie“:

“Natalie” was cited in testimonials within the FY 2018, FY 2019 and FY 2020 annual reports.

I do wonder if these testimonials genuinely refer to Natalie, or whether the name is simply made up to keep staff anonymous.

4) Corporate social responsibility

Formal complaints remain low, and relate mostly to the quality of the car:

By providing hire-purchase finance, S&U is on the hook for any unsatisfactory-quality vehicles.

Action has been taken to lower energy usage:

5) Director pay

The profit before tax target for FY 2021 was originally £38.5m — up 9.6% on FY 2020:

Bonuses were still paid to the executives despite profit before tax being £18.1m, because that profit result was deemed to be a “major accomplishment“:

Bonuses were limited to £25k or less. The executive chairman’s bonus has never topped £50k since at least 2010.

The executive chairman and executive deputy chairman continue to enjoy good salaries given the day-to-day operations at Advantage are run by Graham Wheeler:

Mr Wheeler is on £250k/year, while his predecessor was on £400k/year before retiring:

Salaries are commendably frozen for FY 2022, in line with the wider workforce.

Changes to director pay confirm no further option schemes:

“Shadow” options act like conventional options but the payment is in cash.

Good to see the directors like to talk more about auditing than their remuneration:

6) Auditor

Mazars will replace Deloitte as auditor for FY 2022:

Deloitte had been auditor for 23 years:

7) Key audit matters

Materiality continues to be £1.8m, although the calculation is now 1% of net assets rather than the standard 5% of pre-tax profit:

The text reads as if the net asset-based measure for materiality will remain post-Covid. Always good to see a full-scope audit for the entire group.

Not surprisingly the loan-loss provision calculations have involved greater audit work. The extra work relates to “staging“, and the emergence of payment holidays leading to lots of customers falling into the hitherto rarely used ‘Stage 2’ arrears category (Stage 1 being an initial estimate for all customers and Stage 3 being actual arrears). The audit risk for this matter of course increased during the year:

This entire paragraph was new for FY 2021:

The stages are formally described below:

At least the risk of revenue-recognition problems did not change:

8) Impairment accounting policy

Lots of additional text for Stage 2 impairments. Essentially such payment-holiday impairments have no precedent and so more guesswork than usual has been required:

Confirmation that these Stage 2 impairments carry more risk than typical Stage 2 impairments:

Some helpful numbers for investors wishing to calculate alternative loss provisions:

9) Customer receivables

The text says 6,298 customers had enjoyed payment holidays and were not in arrears at the year end, but had become a greater credit risk. All are now classified as Stage 2 accounts:

Stage 2 customers represented £12.7m of the £36.7m total impairment charge:

I think if there is any ‘over-provisioning’ done by SUS, it will be with these 6,298 customers. Maybe if most continue to pay as normal, some of that £12.7m charge can be written back to future earnings.

10) Employees

SUS commendably did not let go or furlough any employees:

Employee numbers actually increased by 6 to 190…

…but their total cost fell by £355k. Total workforce costs represented 10.6% of revenue, which given the pandemic is impressively commensurate with the 9.6%-11.2% range seen since 2017. The average employee cost was £47k, down from £50k. I suspect the lower wage bill was due to lower bonuses and other pandemic-related savings.

Revenue per employee was £441k, down from £489k and the lowest since 2016. Revenue per employee at Advantage was £479k, down from £528k and again the lowest since 2016.

11) Interest rates

SUS borrows at 4% to lend out at 27%:

The 27% figure was the lowest reported since at least 2008, and compares to 28% for FY 2020 and 31% for FYs 2017 and 2018. I am not sure whether the lower rate of customer borrowing reflects a better quality loan-book or increased competition.

12) Options

Confirmation of very few conventional options:

The present LTIP scheme has run its course and will not be replaced (see point 5 above).

13) Pension scheme

No problems here. Scheme assets of £1.1m plus annual (pre-Covid) earnings of £29m look more than enough to sustain annual benefits of £41k.

The scheme has in fact been closed to new members for more than 40 years.

Maynard

S & U (SUS)

Trading update published 10 August 2021

A positive statement. Here is the full text interspersed with my comments:

——————————————————————————————————————

S&U plc, the motor and property finance specialist, today issues its trading update for the period from its AGM Statement of the 20th May to the 31st July. It will announce half year results on the 28th September 2021.

Trading

S&U continues to trade well, ahead of expectations in terms of profitability, collections and book debt quality. Despite recent inconsistency and incoherence in the Government’s path out of Covid lockdown, particularly in the travel sector, consumer appetite and business confidence is gradually returning, amid expectations of a 7% UK growth rate in GDP for the year.

At S&U, this has been reflected in strong Advantage motor finance applications and for Aspen in the strength of the residential property market — although both slightly constrained by a present lack of supply of both used vehicles and homes for sale. This lack of supply will gradually be corrected as the economic recovery gathers pace. Coupled with very strong cash collections, rigorous and realistic underwriting and the Group’s habitual financial strength, S&U’s return to sustainable and robust growth promises a successful performance this year.

——————————————————————————————————————

Good news is never buried. The first line — “S&U continues to trade well, ahead of expectations in terms of profitability, collections and book debt quality — tells the story.

What is very important is collections doing well, e.g. “Coupled with very strong cash collections“. The main threat to this business had been the non-payment of existing loans; this danger appears to be receding.

——————————————————————————————————————

Advantage Finance

The period has seen Advantage enjoy a profitable, controlled and cash generative recovery as it continues to gradually increase, month by month, to nearer normal levels of new business. Whilst continued sensibly cautious underwriting, and a lack of supply, have seen transaction numbers slightly under an ambitious budget, this has been more than offset by a superb collections performance with related bad debt attrition and impairment more benign than anticipated. As a result, net receivables are stable versus the previous year-end, risk adjusted yield is ahead of budget, and operational cost is well within budget.

The result will be a significant increase in Advantage’s half year profit, comfortably beating budget, and a gradual return towards its habitual levels of ROCE.

This return will be buttressed by the continuous stream of improvements that our excellent team in Grimsby and its Chief Executive, Graham Wheeler, are making to the business. More detail will be provided at half year and these include refinements to the scope and range of its customer offering; new simple access for customers to make online payments; new arrangements with industry partners to boost our dealership capability, and improvements to make our social media marketing more effective.

In addition, Advantage continues to prepare for what will be a significant opportunity in the financing of hybrid and electric used cars. Whilst Covid, initial pricing and the currently inadequate charging network have so far restrained growth, ultimately this new market will provide benefits for our customers, protection for the environment and profitable growth for S&U.

——————————————————————————————————————

All very encouraging.

A “superb collections performance with related bad debt attrition and impairment more benign than anticipated” coincides with the ending of payment-holiday applications on 31 March and the end of the actual payment holidays on 31 July. The loan-loss provisioning in the forthcoming interim results will therefore be fascinating to see. S&U may even have ‘over-provisioned’ its FY 2021 figures.

Transaction numbers falling short is not too concerning in the circumstances. They should improve in time when supply becomes available and the various dealership partnerships are launched. What counts now is the existing loan book being repaid.

——————————————————————————————————————

Aspen

Over the past two months, Aspen, our property bridging business, has continued the encouraging trends reported in May. Net receivables are now at just under £58 million against £18.5 million a year ago, and book quality and repayments continue to be very good.

Much of this net receivables growth has been due to Aspen’s successful offer of Government backed CBILS loans to larger and more established developer customers. Whilst the original CBILS scheme is being wound down, the additional contacts Aspen have made has boosted its market credibility and introducer reach. To consolidate this, Aspen has sharpened its product offering, and its competitive loan to value offer, and, at the same time, strengthened its underwriting team to ensure a speedy and bespoke service to all areas of the property bridging market.

The result is a good half year’s performance and a sound basis for further progress.

——————————————————————————————————————

All sounds promising.

——————————————————————————————————————

Treasury

Following the increase in overall Group funding facilities in the first quarter to £180m, current borrowings levels of £116m (up from £110m in the period) give substantial headroom for growth.

Commenting on S&U’s trading outlook, Anthony Coombs, S&U chairman, said:

“As Britain gradually emerges from the effects of Covid, S&U is demonstrating by its debt quality, collections performance, customer service and product improvements, the inherent strength and potential future profitability of the Group. The challenge now is to grasp these opportunities for new growth. I am confident that we will do so.”

——————————————————————————————————————

Also sounds promising.

Maynard