07 May 2021

By Maynard Paton

Results summary for Tasty (TAST):

- A predictably awful performance, with total sales down 46% and sales at operating restaurants down by approximately 30%.

- H2 was not as bad as H1, witnessing improved cash flow and much lower write-offs.

- A loan from Barclays may indicate TAST’s future is “assured“, but effective net cash of £0.25m is not a huge safety buffer.

- Indoor dining should resume within two weeks, which ought to enhance cash flow and alleviate overdue obligations.

- A new option scheme that pays out in full if the shares reach 16p gives some indication of the possible recovery upside from the recent 7p. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own TAST

- Results summary

- Revenue, losses and Barclays

- Covid-19 impact

- Financials: Cash flow and going concern

- Financials: Landlords and leases

- Immediate prospects

- Valuation

Event links, share data and disclosure

Event: Preliminary results and annual report for the 52 weeks to 27 December 2020 published 07 April 2021

Price: 7p

Shares in issue: 141,089,758

Market capitalisation: £9.9m

Disclosure: Maynard owns shares in Tasty. This blog post contains SharePad affiliate links.

Why I own TAST

- Disastrous ‘legacy’ shareholding bought initially due to experienced family management building and selling two quoted restaurant chains for £200m-plus.

- Bombed-out share price might provide substantial recovery upside… assuming the business does not go broke before the pandemic subsides completely.

- A Barclays loan, an imminent return to inside dining and a new executive option plan provide hope that the worst may now have passed.

Further reading: My TAST Buy report | All my TAST posts | TAST website

Results summary

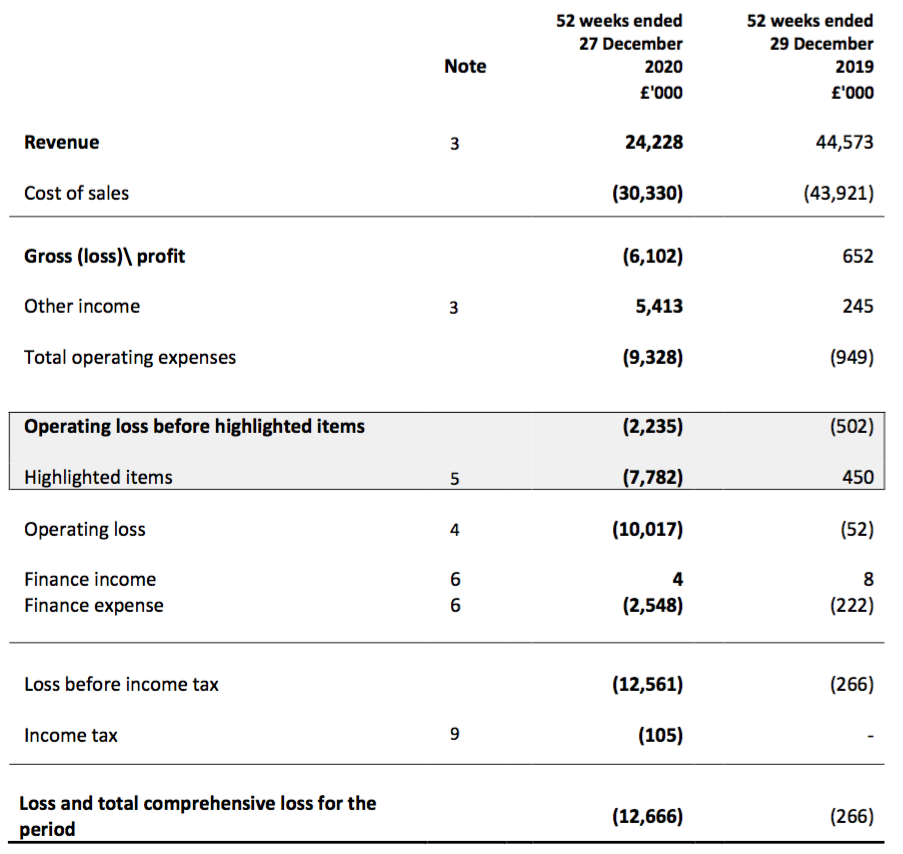

Revenue, losses and Barclays

- Terrible H1 figures plus further pandemic disruption during H2 had already guaranteed an awful FY 2020 performance.

- Annual revenue dived 46% and would have created a £7.7m operating loss were it not for government support of £5.1m:

| Year to c31 December | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue (£k) | 45,847 | 50,309 | 47,278 | 44,573 | 24,228 |

| Operating profit (£k) | 4,692 | 1,101 | (655) | (787) | (7,692) |

| Pre-opening costs (£k) | (642) | (413) | - | - | - |

| Other income (£k) | - | - | 177 | 245 | 5,413 |

| 'Highlighted items' (£k) | (3,925) | (9,956) | (11,087) | 490 | (7,738) |

| Net finance cost (£k) | (213) | (202) | (252) | (214) | (2,544) |

| Pre-tax profit (£k) | (88) | (9,470) | (11,817) | (266) | (12,561) |

| Earnings per share (p) | (1.56) | (13.84) | (19.42) | (0.23) | (8.98) |

| Dividend per share (p) | - | - | - | - | - |

- H2 was not as bad as H1. Government support helped deliver a small ‘underlying’ operating profit between July and December:

| H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | ||

| Revenue (£k) | 21,126 | 23,447 | 44,573 | 8,723 | 15,505 | 24,228 | |

| Gross profit (£k) | 20 | 868 | 897 | (5,581) | (521) | (6,102) | |

| Operating profit before other income (£k) | (667) | (120) | (787) | (6,303) | (1,389) | (7,692) | |

| Other income -- grants (£k) | - | - | - | 3,462 | 1,684 | 5,146 | |

| Other income -- sublets (£k) | 9 | 236 | 245 | 150 | 117 | 267 | |

| Operating profit after other income (£k) | (658) | 116 | (542) | (2,691) | 412 | (2,279) | |

| 'Highlighted items' (£k) | (27) | 517 | 490 | (6,951) | (787) | (7,738) |

- ‘Highlighted items’ — essentially a mix of write-offs and restructuring costs offset by a lucrative property disposal and a peculiar property write-back — were much lower during H2, too.

- The H2 effort prompted Barclays to release a £1.25m four-year loan to TAST during January 2021.

- This Barclays loan could actually signal TAST has survived the pandemic.

- The Barclays arrangement was proposed during September and that announcement said:

“The Facility is available to be drawn down until 7 February 2021, however, draw down is restricted until the future of the Company is assured through restaurant closures and creditor arrangements.”

- Lifting the loan restriction implies Barclays believes TAST’s future is now “assured” following subsequent site closures and creditor arrangements.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Covid-19 impact

- The stronger H2 was due to a longer period of ‘normal’ trading.

- To recap, H1 witnessed:

- All restaurants open fully with “generally encouraging” trading up to 24 March, and;

- All restaurants then shut until late May, followed by a phased re-opening for takeaways and deliveries.

- For H2, most of TAST’s restaurants re-opened from 4 July for inside dining, with August benefiting from the government’s Eat Out To Help Out (EOTHO) scheme.

- TAST organised its own EOTHO promotion during September and October, suggesting the original EOTHO was successful.

- But the industry faced greater operating restrictions from September, with November’s full lockdown allowing deliveries/takeaways only. December then witnessed some restaurants re-open for inside dining.

- TAST admitted “trading during the historically crucial [Christmas] period was poor“.

- TAST started the year with 57 restaurants and finished the year with 54 following one lucrative disposal and two lease surrenders (see Financials: Landlords and leases).

- Sales per restaurant therefore dived 43%:

| Year to c31 December | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue (£k) | 45,847 | 50,309 | 47,278 | 44,573 | 24,228 |

| Year-end restaurants | 61 | 64 | 60 | 57 | 54 |

| Average restaurants | 54.5 | 62.5 | 62 | 58.5 | 55.5 |

| Revenue per restaurant (£k) | 841 | 805 | 763 | 762 | 437 |

- But that lucrative site disposal occurred at the start of January, while only 38 sites were open at the end of the year.

- The average number of restaurants actually operating during the year could therefore have been (56+38)/2 = 47.

- Sales per that 47 average come to £515k, which is 32% down on FY 2019.

- A similar sales reduction is derived from comparing revenue to employees:

| Year to c31 December | 2016 | 2017 | 2018 | 2019 | 2020 |

| Revenue (£k) | 45,847 | 50,309 | 47,278 | 44,573 | 24,228 |

| Employees | 1,019 | 1,184 | 1,049 | 1,028 | 810 |

| Revenue per employee (£k) | 44,992 | 42,491 | 45,070 | 43,359 | 29,911 |

- Revenue per employee dropped 31% to £30k during the year.

- These calculations suggest the disruption cut revenue at open restaurants by almost a third — which does not seem too horrific given the operating restrictions and reduced inside dining throughout the twelve months.

Financials: Cash flow and going concern

- Cash generation during H2 was much better than H1:

| H1 2019 | H2 2019 | FY 2019 | H1 2020 | H2 2020 | FY 2020 | ||

| Net increase in cash (£k) | (1,955) | 2,213 | 258 | (1,410) | 4,868 | 3,458 | |

| Adjustments | |||||||

| Bank loan repayment (£k) | (4,565) | (200) | (4,765) | (1,652) | - | (1,652) | |

| Proceeds from sale of property (£k) | 523 | (15) | 508 | 1,862 | 177 | 2,039 | |

| Free cash flow (£k) | 2,087 | 2,428 | 4,315 | (1,620) | 4,691 | 3,071 | |

| Other income -- grants (£k) | - | - | - | 3,462 | 1,684 | 5,146 | |

| Free cash flow before grants (£k) | 2,087 | 2,428 | 4,515 | (5,082) | 3,007 | (2,075) |

- H1 had witnessed a worrying free cash outflow of £1.6m despite government grants of £3.5m.

- However, H2 enjoyed a free cash inflow of £4.7m, or £3.0m before government grants.

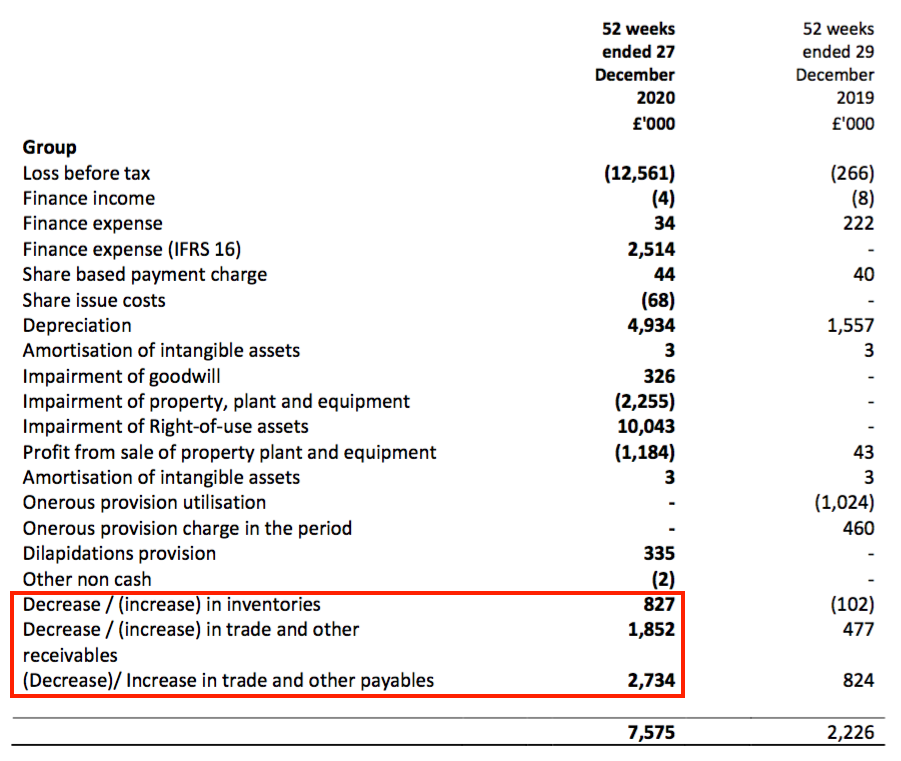

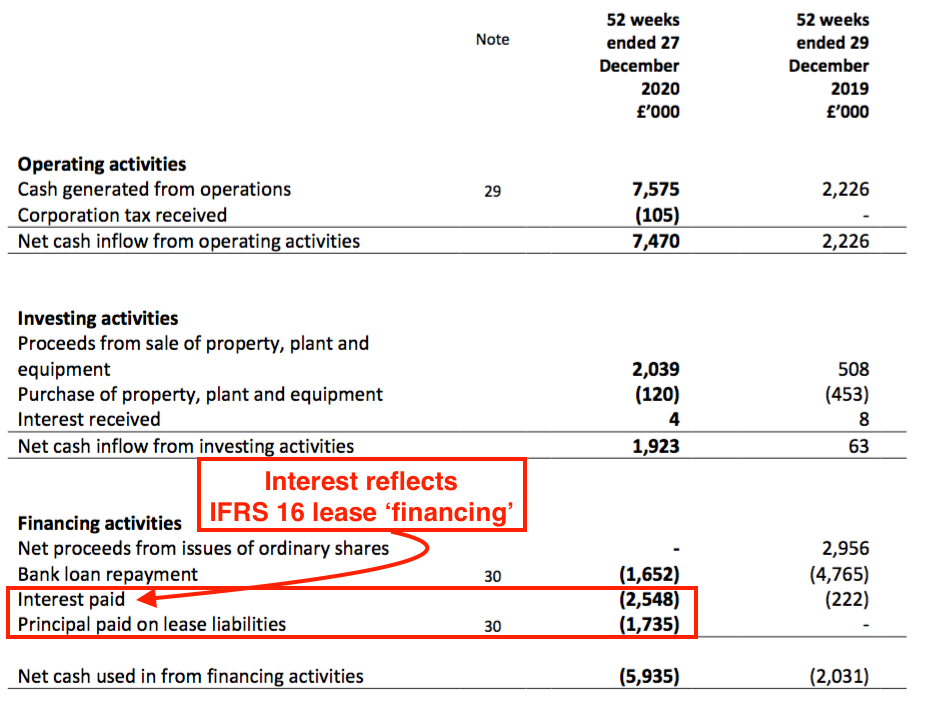

- TAST’s free cash flow for the full year was bolstered by a favourable £4.0m working-capital movement…

- …but was also reduced by cash lease payments of £4.3m:

- TAST admitted the favourable working-capital movement was caused by “a deferral of payments due to landlords, HMRC and other trade creditors“.

- Cash lease payments were not recorded during H1, meaning the full £4.3m lease payment was paid during H2 (see Financials: Landlords and leases).

- The H2 cash inflow allowed cash to finish the year at £8.0m.

- Conventional debt was all cleared following the lucrative property sale at the start of the year and thereafter remained at zero.

- TAST acknowledged the deferred payments due to landlords, HMRC and other creditors totalled £6.5m and — if paid as normal — would have left year-end cash at £1.5m.

- ‘Underlying’ net cash following the Barclays loan is therefore £1.5m less £1.25m = just £0.25m.

- £0.25m is not a huge buffer to help limit any further pandemic disruption.

- For the time being, shareholders just have to trust:

- Landlords, HMRC and other creditors remain patient for their £6.5m;

- Cash generation occurs during the current H1 2021 (see Immediate prospects), and;

- Barclays’ assessment of TAST’s future really is “assured“.

- Note that TAST amended its ‘going concern’ text.

- The H1 statement had said a “material uncertainty” may exist:

“At the time of approving the interims, the Directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. In reaching this conclusion the Directors have considered the financial position of the Group, together with its forecasts for the next 12 months and taking into account possible changes in trading performance. The going concern basis of accounting has, therefore, been adopted in preparing the interim financial report. However, the Directors note that there may be material uncertainty in relation to going concern due to the effects of Covid-19 and the impact of ongoing losses.

- But this FY 2020 statement altered the last line and admitted a “material uncertainty” does now exist:

“However, the Directors note that the effects of Covid-19 and the impact of ongoing losses indicate the existence of a material uncertainty that may cast doubt over the Group’s ability to continue to apply the going concern basis of accounting.“

- Wishful thinking perhaps, but the amended ‘going concern’ text could be more for the attention of stubborn landlords that have yet to agree a rent reduction…

Quality UK investment discussion at Quidisq. Visit forum.

Financials: Landlords and leases

- These FY 2020 results contained an update on landlord rent negotiations:

“The Group has now successfully achieved consensual lease concessions and rent reductions to March 2021 on more than two-thirds of the estate. The Group is continuing negotiations with landlords and other creditors regarding outstanding debts.”

- The H1 statement had indicated the rent negotiations would be completed by the end of November.

- The negotiations continuing into April clearly indicate some landlords are holding out for their full rent payments.

- I suspect the line below from these results was not received very well by the obdurate landlords:

“Given the current third lockdown and the moratorium expected to end in June 2021, we now anticipate that we may require further landlord support.“

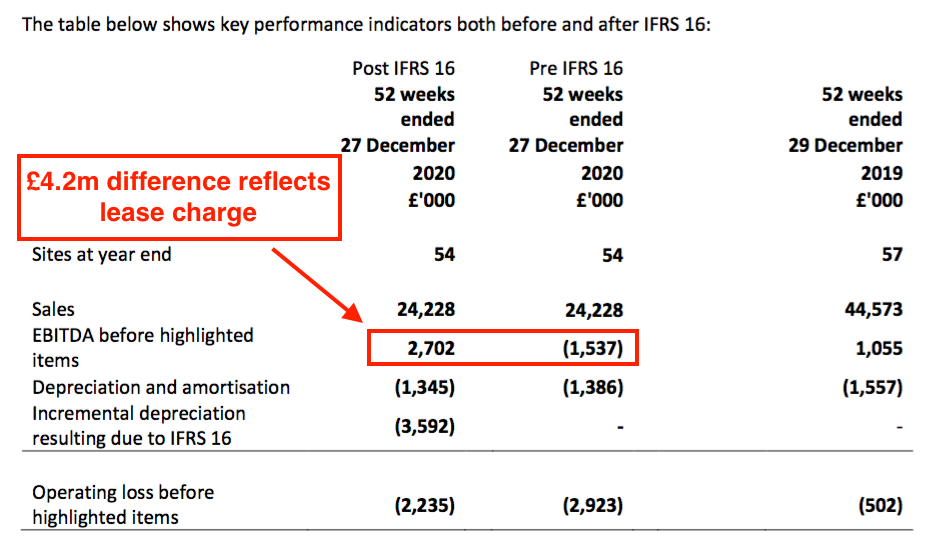

- TAST published pre- and post-IFRS 16 versions of the headline performance, from which lease costs could be deduced:

- The £4.2m difference between the Ebitda numbers represents the pre-IFRS 16 lease cost that, post-IFRS 16, is now reflected within the depreciation expense and financing charge.

- For FY 2019, the pre-IFRS 16 lease cost was £5.5m.

- The figures boil down to lease costs for FY 2020 declining from £5.5m to £4.2m, or 24%.

- This 24% reduction will reflect three fewer restaurants within the estate and the rent reductions that have (presumably) been agreed part-way through the year.

- I am hopeful further landlord negotiations can lead to additional lease-bill reductions.

- The aforementioned cash lease payments of £4.3m do suggest TAST paid all of the implied £4.2m rent charge for the year.

- As before, TAST hinted that a Company Voluntary Arrangement (CVA) could be Plan B should landlord negotiations not succeed:

“The Group is continuing to work with its advisers, KPMG, to assess the potential impact of Covid-19 on the business and the various strategic options available to the Group. With the progress made on consensual negotiations with landlords and other creditors, the Group has to date managed to prevent a CVA. However, with dine-in restrictions in place until May 2021, there is additional pressure on cash reserves. The Board will continue to explore all options but are hopeful that with continued creditor assistance, a more formal procedure may be avoidable.“

- A CVA may be just the radical action TAST needs to reshape the group entirely.

- After all, this business struggled during 2017, 2018 and 2019 with unprofitable restaurants — and the pandemic now provides management the opportunity to instigate far-reaching (and much-needed) changes to the estate.

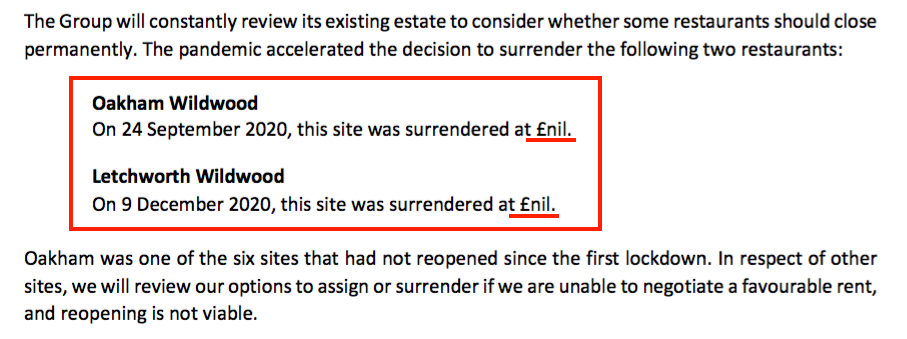

- Rather encouragingly, TAST managed to surrender two restaurants during the year without financial penalty:

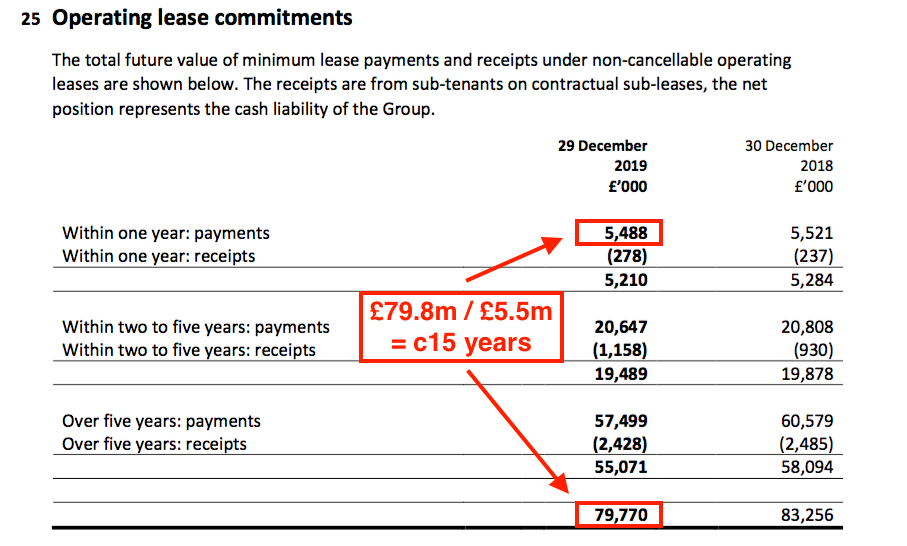

- The implementation of IFRS 16 brought TAST’s lease obligations onto the balance sheet.

- Total lease obligations were £55.1m on a net present value basis.

- The accompanying right-of-use asset was £39.8m, which arguably suggests TAST would pay £15.3m (£55.1m minus £39.8m) less to rent its properties were it to commence the same leases today.

- The FY 2019 figures suggested TAST’s leases ran for an average of approximately 15 years:

Management changes

- An important attraction to my initial TAST investment was the presence of Adam and Sam Kaye as directors.

- Alongside a rich heritage of Kaye restaurant successes during the 1960s, 1970s and 1980s, I had naturally assumed TAST would become another Kaye winner.

- But greater competition and higher costs meant TAST could never achieve the same economics of ASK or Prezzo with the same middle-of-the-road menu…

- …and the roll-out of new restaurants came to an abrupt end during 2017.

- Profit then turned to losses, and then the pandemic arrived.

- Both Kaye brothers have now decided to “focus on their other commercial interests“.

- Adam Kaye was a TAST non-exec and left the board during September. But he does remain an executive director of cinema chain Everyman Media.

- Sam Kaye was TAST’s co-chief executive, but became a non-exec during December and will leave the board on 14 May.

- The Kayes’ “other commercial interests” are primarily commercial properties. Some of the properties are occupied by TAST.

- TAST’s related-party transactions show TAST paid £426k to Kaye-related ventures during FY 2020 — down 24% to match the wider lease-bill reduction (see Financials: Landlords and leases):

- I had always wondered whether the Kaye brothers were ‘property men’ or ‘restaurant men’. I suppose their board departures has answered that question.

- Adam and Sam Kaye alongside other family members presently retain a 32%/£3m TAST shareholding.

- Leading TAST now is long-time co-chief exec Jonny Plant, who has become sole chief executive.

- His appointment was accompanied by a notable option award, which pays out in full if the share price trades at 16p or more by 2025.

- Mr Plant currently owns 5% of TAST but may control almost 15% if the 16p share price is achieved and triggers the full option award.

Immediate prospects

- TAST confirmed the business required customers dining inside to prosper:

“While delivery helps keep some sites open, the high cost of delivery erodes our margin. Dine-in is central to the business.”

- Outdoor dining recommenced last month while indoor dining is planned to recommence on 17 May.

- TAST is optimistic:

“Trading outside of lockdown has been encouraging, and we look forward to a promising period after the current lockdown ends.“

- But everything depends on the pandemic easing as the government’s ‘roadmap’ expects.

- Restaurant group Fulham Shore (FUL) has provided early hope of positive sector trading:

“Group sales in the week ended Sunday 18 April 2021 were very encouraging, being not only ahead of the previous week, but also ahead of the same week two years ago in April 2019 (as April 2020 was in the first lockdown, it is not comparable). These trading results were achieved without any inside seating and our colleagues in the restaurants deserve great credit as demand has far exceeded the number of seats available at peak times.“

- FUL achieved greater sales from 70 sites during the first week of outside dining than from normal trading at 61 sites during the same week two years ago.

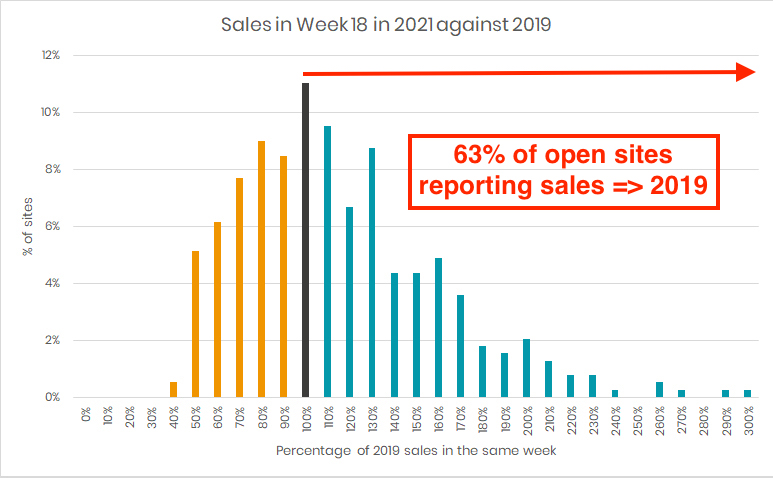

- Hospitality software specialist S4 Labour provides wider insight.

- S4 said the first week of outside service led to a 9.1% like-for-like sales increase on the same week during 2019.

- But the second week of outside service saw like-for-likes down 10.5% and the third week saw like-for-likes down 1.2%.

- The weather may of course influenced demand for outdoor dining and created the like-for-like fluctuations.

- Perhaps encouragingly, S4 claims 63% of sites that had re-opened for outside trade reported sales at least equal to the level of the same week from 2019:

- TAST presently has:

- 23 restaurants available for outside service;

- 17 restaurants for takeaways and deliveries only, and;

- 14 restaurants closed.

- I am hopeful the return of inside dining will herald, as TAST anticipates, a “promising period” that can resuscitate cash flow and alleviate overdue obligations.

- With less than two weeks before inside service resumes, I would like to think any creditor/bankruptcy dramas would have emerged by now.

- Fingers crossed the landlords, HMRC and other creditors will allow TAST to benefit from inside dining before asking for their money.

- The government’s furlough scheme runs until 30 September should further problems arise.

Which is best for stock-screening: Stockopedia or SharePad? See my verdict.

Valuation

- The aforementioned option scheme for Mr Plant gives some indication as to the scale of TAST’s possible recovery.

- Achieving 16p within four years from the recent 7p equates to a 20%-plus share-price CAGR.

- Certainly the present £10m market cap does not seem expensive… assuming of course:

- Social restrictions are eventually lifted;

- Diners return to TAST’s restaurants;

- Suitable revenue and profit can be achieved, and;

- The group does not go broke beforehand.

- A ‘return to normality’ that witnesses TAST operate, say, around 50 restaurants with, say, sales of around £750k each should bring in total revenue somewhere between £35m and £40m.

- Lower rents, fewer problem sites and less immediate competition could perhaps lead to a modest 5% margin and maybe an operating profit of approximately £1.8m.

- The £10m market cap at 7p versus a possible £1.8m profit does suggest the 16p option-scheme target is not completely out of reach.

- Mind you:

- A 5% margin may be very ambitious given TAST suffered negative margins during 2018 and 2019;

- One-third of TAST’s restaurants have yet to have their rents renegotiated, and;

- An effective £0.25m net cash position does not leave much headroom for further pandemic setbacks.

- The shares fell to 1p during November, at which point my entire TAST investment had lost 87%.

- At 7p I am down 71% and at 16p I would be down ‘only’ 47%. I require 34p to get back to breakeven.

- Having stuck with the shares all the way to 1p, I am minded to keep hold and see how any recovery plays out — especially with inside dining set to resume within just two weeks.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Its been some ride, thanks for the update Maynard, very comprehensive as usual. I too continue to hold

Tasty (TAST)

Directorate Change published 19 May 2021

An encouraging appointment. Always useful to have a non-exec with hands-on industry experience. Mr Samúelsson replaces Sam Kaye who departed the board earlier in the month.

Here is the full text:

——————————————————————————————————————

Further to the announcement on 23 December 2020, Tasty (AIM: TAST), the owner and operator of restaurants in the casual dining sector, is pleased to announce the appointment of Harald Samúelsson as an independent non-executive director, with immediate effect.

Harald Samúelsson has over 20 years of experience in the UK restaurant industry. From 2000 to 2008, Harald helped grow Strada Restaurants from 4 to 54 restaurants in the UK in a senior operations position. In 2008, Harald joined Côte Restaurants as joint Managing Director, growing the group from 2 to 72 restaurants. In 2013, Harald co-led a management buy-out of Côte with CBPE Private Equity for £100m and in 2015 co-led a sale of Côte to BC Partners for £245m. During his Côte tenure, Harald was also joint Managing Director at Bill’s restaurants from 2010 to 2012. In 2016, Harald joined Honest Burgers as a Senior Advisor and set up a property development company in Spain with projects in the Valencia, Madrid and Barcelona areas.

Keith Lassman, Non-executive Chairman, commented: “I am delighted to welcome Harald to the Board. His considerable industry experience will be hugely beneficial to us as the Group looks forward to the sector recovering from the pandemic.”

The directorships and partnerships currently held by Harald Sam ú elsson and over the five years preceding the date of appointment are as follows:

Mr Harald Alexander Sam ú elsson , aged 53

Current directorships/partnerships

Viking Tulip Properties SL

Previous directorships/partnerships

Viking Tulip Consultancy Limited

Harald Sam ú elsson does not hold any ordinary shares in the Company and there are no further disclosures to be made pursuant to Schedule 2 paragraph (g) of the AIM Rules.

——————————————————————————————————————

Maynard

Tasty (TAST)

Operational update published 21 May 2021

Confirmation that most restaurants have re-opened for indoor dining. Here is the full text:

——————————————————————————————————————

Tasty (AIM: TAST), the owner and operator of restaurants in the casual dining sector, is pleased to announce that, following the lifting of the lockdown restrictions on Monday 17th May, 47 of its 54 sites are currently fully open to trade. All appropriate measures are in place to ensure government guidelines concerning social distancing and customer safety are fully adhered to.

The Company intends to provide an update on trading towards the end of June 2021.

——————————————————————————————————————

The FY 2020 results said 6 sites had not re-opened after March 2020, one of which (Oakham) was sold. So 5 problem sites remain, plus it seems another 2 have emerged given 7 sites in total are presently shut.

Maynard

Tasty (TAST)

Publication of 2020 annual report

Here are the points of interest:

1) Risks

Some minor additional text for FY 2020:

The same People risk applies, but maybe headlines such as Hospitality ‘struggling to fill thousands of jobs’ could mean operational difficulties for TAST.

I note TAST’s recent emails have been highlighting vacancies for chefs — something that was never done before Covid:

Brexit departures not an issue, at least according to TAST.

TAST adds a thank-you to suppliers:

2) Section 172

New for FY 2020 — a Section 172 statement. Nothing too revealing, and I suspect not a priority for management to compile:

3) Streamlined energy and carbon reporting

New for FY 2020 — some energy stats. Something else management probably could have done without compiling at present:

4) Corporate governance

No major changes from FY 2019. But there were some minor amendments to the employee section, which reveals five apprentice schemes versus three from FY 2019:

Apprenticeships may help TAST counteract the aforementioned skills shortage (see point 1 above). Female chefs may help, too:

The small-print also revealed the board had weekly calls and is now “fully committed” to TAST, rather than just “committed” as per FY 2019:

5) Key audit matters

‘Transition to IFRS 16’ replaced ‘Going concern’ as a key audit matter:

I am hopeful the switch means TAST’s ‘going concern’ is less of a concern to the auditor. The other key audit matter remains the impairment of property, plant and equipment.

6) Audit

A full-scope audit for the whole group:

Materiality lifted to £200k from £130k feels odd during a year when the group decreased in size:

The materiality increase gives the impression the auditor is not delving as deep as it did for FY 2019.

7) Going concern

The text included snippets of relatively promising non-lockdown trading:

8) Useful lives

Fixtures, fittings and equipment continue to have a ten-year useful life:

My analysis last year indicated ten years was optimistic when compared to other sector operators. I would venture the write-offs TAST has suffered during the last few years ought to have prompted a shorter useful life and, therefore, higher depreciation charges.

I note the useful life of Computers has changed to five years. Before FY 2020, their useful life was a ridiculous 20 years.

9) Employees

Staff productivity obviously suffered during FY 2020:

Revenue per employee was £30k, versus £41k-£46k for FYs 2010-2019. Average staff cost, though, was kept at £18k. Restaurant staff per restaurant was 14.3, down from the usual 17-20 seen since FY 2010.

10) Director pay

After taking pay cuts/waivers during FY 2019, the board resumed normal wages for FY 2020:

Not surprisingly given her extra workload, the FD took home the largest salary.

11) Inventories

“Smallware” represents crockery and utensils:

The year-end inventory position is academic, but the £6.1m inventory expense represented 25% of revenue and within the 23%-27% range seen since FY 2012.

12) Trade receivables

Unpaid customer invoices remain insignificant:

13) Trade and other payables

Perhaps no surprise trade and other payables have increased by almost £3m as TAST defers payments to preserve cash:

14) Provisions

Not ideal that TAST has admitted £335k will be needed to repair a number of restaurants:

15) Options

The 3.78 million options below do not include the 15.68 million options granted to the chief exec after the year end:

16) Cash flow error

An erroneous double entry can be excused given the accounting/reporting workload:

Maynard

Tasty (TAST)

Trading update published 29 June 2021

A promising update in the circumstances, with a prediction of “robust” summer trading. Takeaway sales could be sustained, too, while rent revisions have been agreed on more than 80% of the estate (previously more than 66%). Here is the full text.

——————————————————————————————————————

Tasty (AIM: TAST), the owner and operator of restaurants in the casual dining sector, is pleased to announce the following update on trading.

As announced on 21 May 2021, following the lifting of the lockdown restrictions on 17 May 2021, we reopened most of our estate and now 49 of the Company’s 54 sites are fully open for trade. All appropriate measures are in place to ensure government guidelines concerning social distancing and customer safety are adhered to and monitored.

Takeaway and delivery sales performed well during the most recent lockdown and throughout H1. The Company has made good progress in expanding delivery and click and collect across all sites. We have been particularly pleased with the continued good performance of our takeaway sales which, even after dine-in reopened, have continued to perform well. Our rollout of our new takeaway sub-brands, Out the Box and Out the Box Asia, has progressed well and is contributing an additional revenue stream.

Since the relaxation of indoor dining restrictions, the six-week period to 27 June 2021 as a comparison to 2019 has shown strong like-for-like growth. Trading has benefitted from significant pent-up demand, and we are encouraged by the initial strength of our overall trading performance despite the restaurants having restricted capacity due to social distancing.

The Board believes that, as a result of international travel restrictions, increased disposable income and a general strong desire to go out, trade will remain robust throughout the summer months.

Notwithstanding this, the Company is taking measures to combat the challenges ahead posed by supply chain disruption, recruitment issues, wage inflation, the reintroduction of business rates, and the reduction in furlough and VAT support.

The Company has strengthened its people and marketing departments and Harald Samuelsson, who joined the Company as a Non-executive Director on 19 May 2021, is an invaluable addition to the Board.

The Company has agreed consensual lease concessions and rent reductions on more than 80% of the estate and is continuing to negotiate with the remaining landlords and other creditors to settle any outstanding debts.

We would like to take this opportunity to thank everyone who has supported us to get through these difficult times, especially our hardworking staff, landlords and creditors.

——————————————————————————————————————

Maynard