09 March 2023

By Maynard Paton

Results summary for System1 (SYS1):

- H1 2023 revenue falling 15% to FY 2012 levels and underlying cash losses running at £2m-plus raised further doubts about SYS1’s services, marketing, pricing and expenditure.

- Despite encompassing “all strategic options” and the board’s composition, a three-month strategic review simply “validated” SYS1’s existing plans with a greater focus on the United States.

- A management presentation revealed the transition to automated Data services still requires old-style consultancy work, and overlooked questions about partnerships, cash flow and expenses.

- The unsatisfactory H1, underwhelming strategic review and frustrating Q&A were thankfully followed by two former executives proposing very welcome board changes.

- Fresh executive leadership seems needed to maximise SYS1’s “superb, proven suite of products” and re-establish worthwhile levels of profit. I support the proposed board changes and continue to hold.

Contents

- News links, share data and disclosure

- Why I own SYS1

- Results summary

- Revenue and profit

- Strategic review

- Reasons to Believe

- Data versus Consultancy

- Partnerships

- Customers and employees

- Financials

- Capital Markets Day: strategic optimism

- Capital Markets Day: strategic confusion

- Capital Markets Day: new information

- Capital Markets Day: other Q&A

- Valuation

- Receipt of requisition notice

- Stefan Barden

- Verdict on proposed board changes

News links, share data and disclosure

News: Interim results and presentation for the six months to 30 September 2022 published 30 November 2022, Q3 trading update published 23 February 2023, Capital Markets Day update, webinar and presentation published/hosted 28 February 2023 and receipt of requisition notice published 07 March 2023.

Share price: 190p

Share count: 12,678,829

Market capitalisation: £24m

Disclosure: Maynard owns shares in System1. This blog post contains SharePad affiliate links.

Why I own SYS1

- Advertising research specialist that predicts the success of television adverts, with progress resting upon “the most accurate, cheapest and quickest” data and follow-up guidance that is “the best in the industry”.

- Partnerships with ITV and LinkedIn support welcome transition from bespoke consultancy towards ‘scalable’ data services and should attract greater customers at lower cost.

- Proposed board changes could finally exploit the group’s “superb, proven suite of products” and rescue shareholders from very unsatisfactory financial performances.

Further reading: My SYS1 Buy report | All my SYS1 posts | SYS1 website

Results summary

Revenue and profit

- A disappointing H2 2022 loss followed by a very mixed October update…

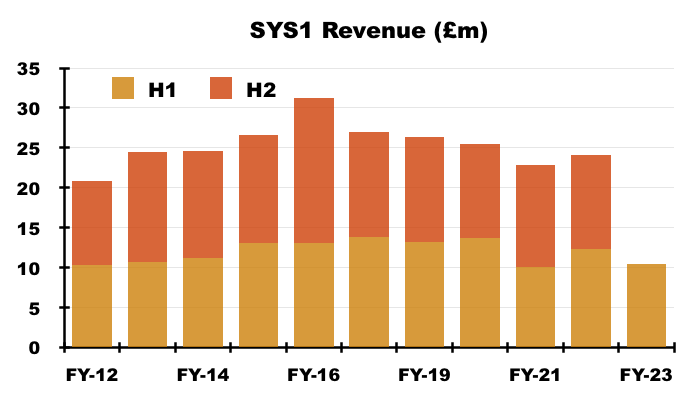

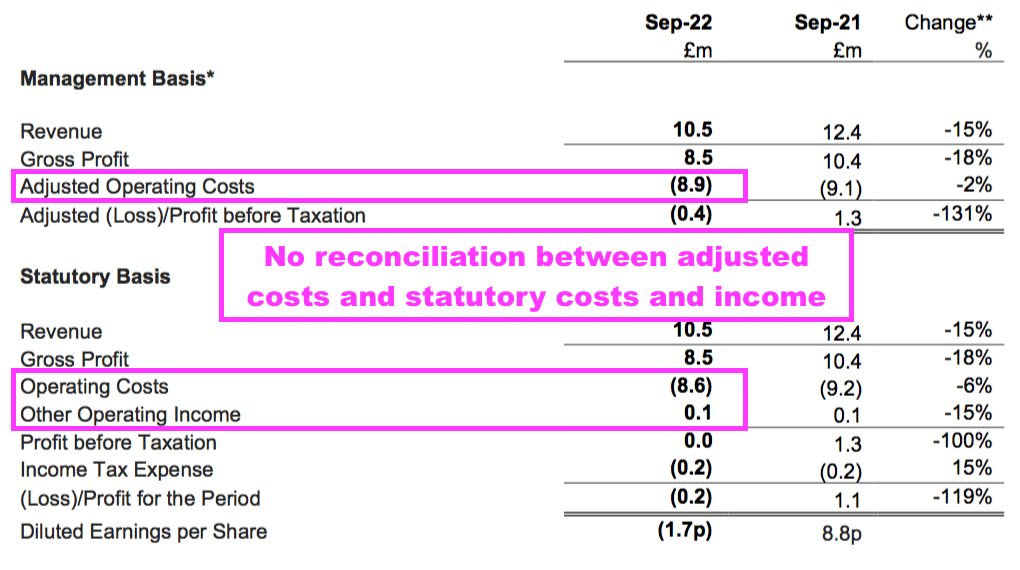

“Consequently, total H1 revenue declined 15% on the comparable period last year to £10.5m from £12.4m in H1 last year, in line with management’s expectations.

Adjusted Operating Costs reduced by 1% to £9.0m, and the Company expects to report an Adjusted Pre-Tax Loss of £0.4m in the first half, compared to an Adjusted Pre-Tax Profit of £1.3m in H1 last year. At Statutory Pre-Tax Profit level, the Company expects to break even in the first half, down £1.3m on H1 last year.

H1 period-end cash, net of borrowings, was £6.6m, compared to £8.7m at end-March 2022, an outflow for the period reflecting the Adjusted Pre-Tax higher working capital and the repurchase of shares on market.”

- …had already set the tone for this rather unsatisfactory H1 2023.

- The headline figures all matched October’s update, with H1 revenue at £10.5m, the H1 adjusted pre-tax loss at £0.4m and H1 net cash at £6.6m.

- H1 revenue fell 15% due to the “continuing decline in our complex consultancy products”, which was not surprising given SYS1 warned of a “sudden and unanticipated reduction in…bespoke consultancy project sales in the US” during the preceding Q4 2022.

- SYS1 also said UK and European H1 sales were affected by “budgetary response[s] to the Ukraine invasion and associated economic shocks“.

- Aside from the pandemic-disrupted H1 2021, H1 revenue was the lowest since H1 2012 (£10.4m):

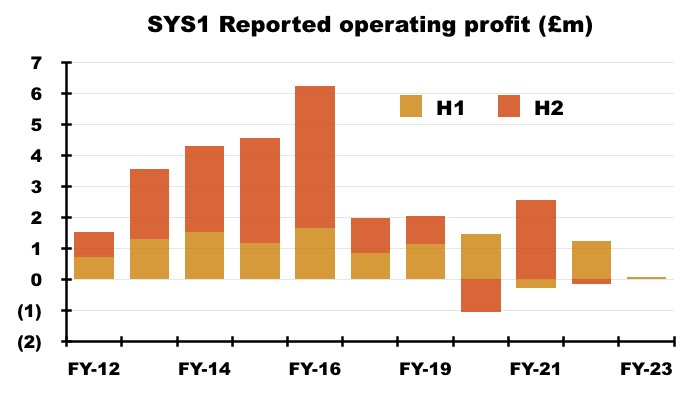

- Reported operating profit was just £78k, which before the £224k generated through ‘other operating income’ translated into a £146k operating loss:

- Other operating income comprises sub-let rental receipts and government research grants.

- The reported £78k operating profit followed the preceding H2’s reported £228k operating loss and, pandemic aside, led to the group’s weakest twelve-month profit performance since the 2006 flotation.

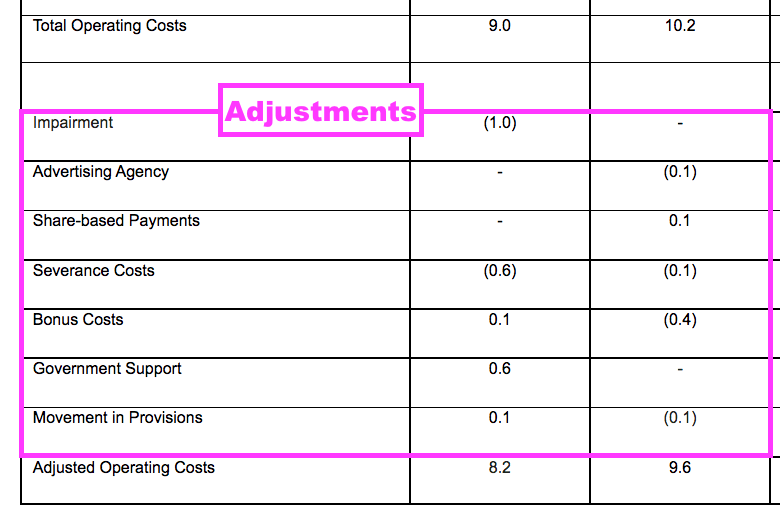

- H1 adjusted operating costs were £8.9m while H1 statutory operating costs and income were a combined £8.5m:

- SYS1 claimed its adjusted figures excluded items that “impede easy understanding of underlying performance” (see Financials).

- SYS1 did not disclose exactly how its adjusted costs reconciled to its statutory costs, which is bad form and did in fact “impede easy understanding of underlying performance”.

- SYS1’s results have not offered an “easy understanding of underlying performance” for some time.

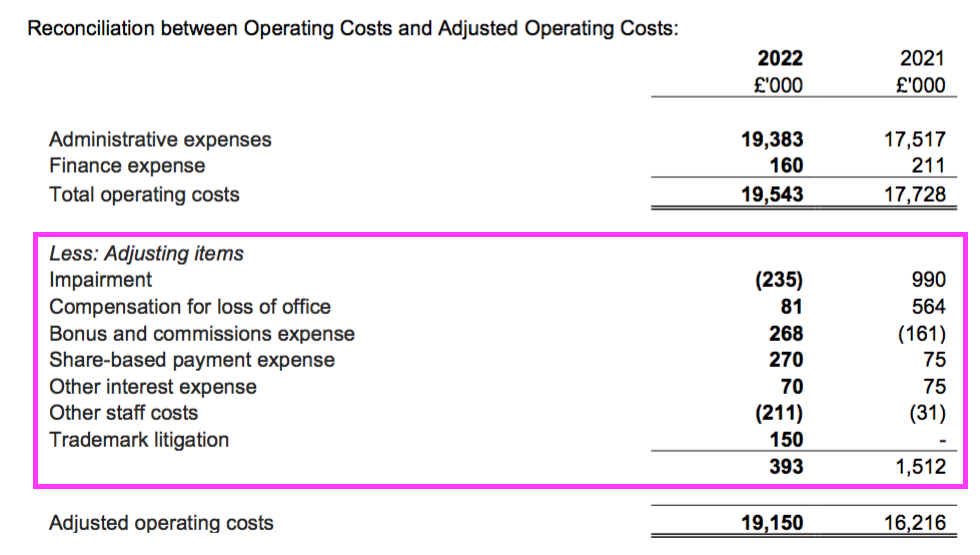

- Adjusting items have featured during FYs 2021 and 2022…

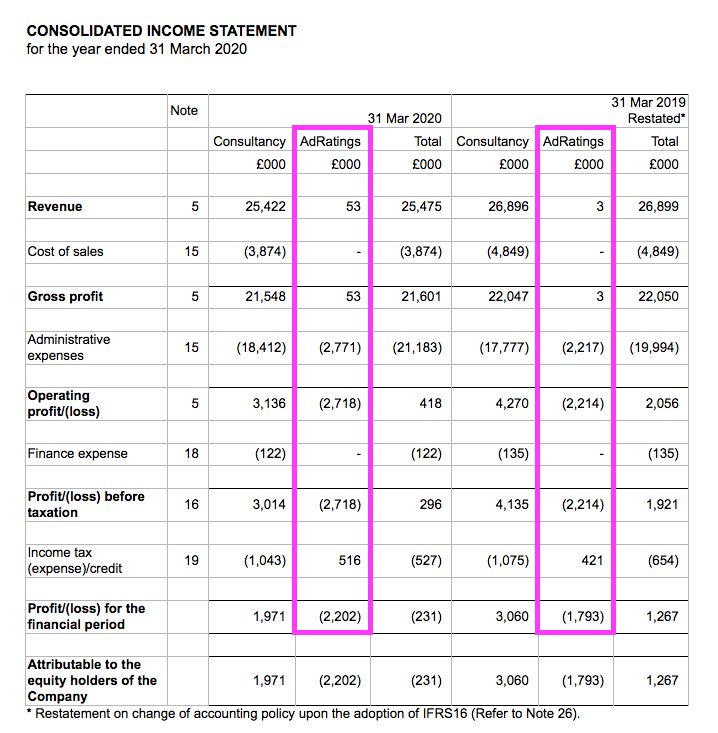

- …while significant AdRatings costs were segmented for FYs 2019 and 2020:

- This H1 witnessed SYS1 return to capitalising IT expenditure, with £654k spent on new systems that bypassed the income statement (see Financials).

- SYS1 previously capitalised IT spend of £1.4m for AdRatings during FYs 2019 and 2020, only for it all to be written off following insufficient sales.

- History therefore suggests SYS1 should continue to expense IT spend, and this H1’s £0.4m adjusted pre-tax loss should arguably have been reported as a c£1m loss.

Strategic review

- This H1 statement published the conclusion of the group’s three-month strategic review.

- To recap, SYS1 announced the review during August and stated “all strategic options” would be explored:

“Whilst the Company can continue with its current strategy, the Board believes that it is important to ensure that it has explored all strategic options to capitalise on System1’s current market opportunity to deliver shareholder value, including considering the value it can create in its current form, the options for increasing organic growth through forming partnerships, and external or internal investment to grow revenue by leveraging the significant investment made in automated predictions technology.

- The coinciding appointment of non-exec Conrad Bona suggested the review was instigated by 5.5% shareholder Mediqon.

- Management confirmed during the 2022 AGM that institutional shareholders had “prompted” the strategic review:

“It was in discussion with some of our institutional shareholders, who are obviously very concerned about capital allocation as well, that they suggested to us what are your very best uses of your capital, should we be returning it to shareholders and it is that what prompted the review that we are now in.“

- The 2022 AGM revealed 30%-plus protest votes against certain non-execs, which led to the strategic review “specifically” encompassing the board’s composition:

“The Board consulted with certain shareholders ahead of the AGM, and believes that the directors, as elected at today’s AGM, possess a good mix of skills and experience necessary to oversee the Company and deliver its’ strategy, but will specifically review the Board’s composition as part of the previously announced strategic review.”

- Given the unsatisfactory profit performances during this H1 and the preceding H2, a study of “all strategic options” alongside “specifically” assessing the board’s membership could have created a very welcome/radical/intriguing outcome to the review.

- But the review simply “validated” SYS1’s “existing successful focus” on its current services, along with no board departures and no external appointments.

- The review concluded SYS1 should devote greater attention to:

- Digital ads;

- Partnerships with media groups, such as the existing tie-ups with ITV and LinkedIn;

- Partnerships with industry agencies, such as Omnicom/BBDO, and;

- The United States.

- Management changes were limited to:

“John Kearon, currently Founder and CEO, will become Founder & President from 1 December, with the priority task of securing new business and partnership opportunities in the US, where he will spend most of the first half of 2023. John will no longer act as CEO but will remain a director of the Company.

James Gregory, currently COO, will be appointed CEO from 1 December to lead the execution of the new strategy, complete our digital transformation and scale the business“

- And financial ambitions were limited to:

“Our goal is to become a ‘Rule of 40’ company, whereby we will target the sum of our data revenue growth rate and adjusted EBITDA margin to be in excess of 40%, delivering a value enhancing blend of growth and return.“

- The review’s conclusion was not exactly the welcome/radical/intriguing outcome I had thought possible.

“It appears they are just crossing their fingers and hoping John Kearon performs a sales miracle in the US. All very underwhelming. I wonder how the activist investor will react to this? I can’t imagine he was in support of such a damp squib.“

- At least the review finally extinguished ideas of a tender offer and other capital-allocation distractions:

“We are cancelling the £1.5m buyback tender offer announced in June, in order to provide more growth capital for the business.“

Reasons to Believe

- The H1 2023 presentation completely overlooked some very bullish management commentary made during FY 2021.

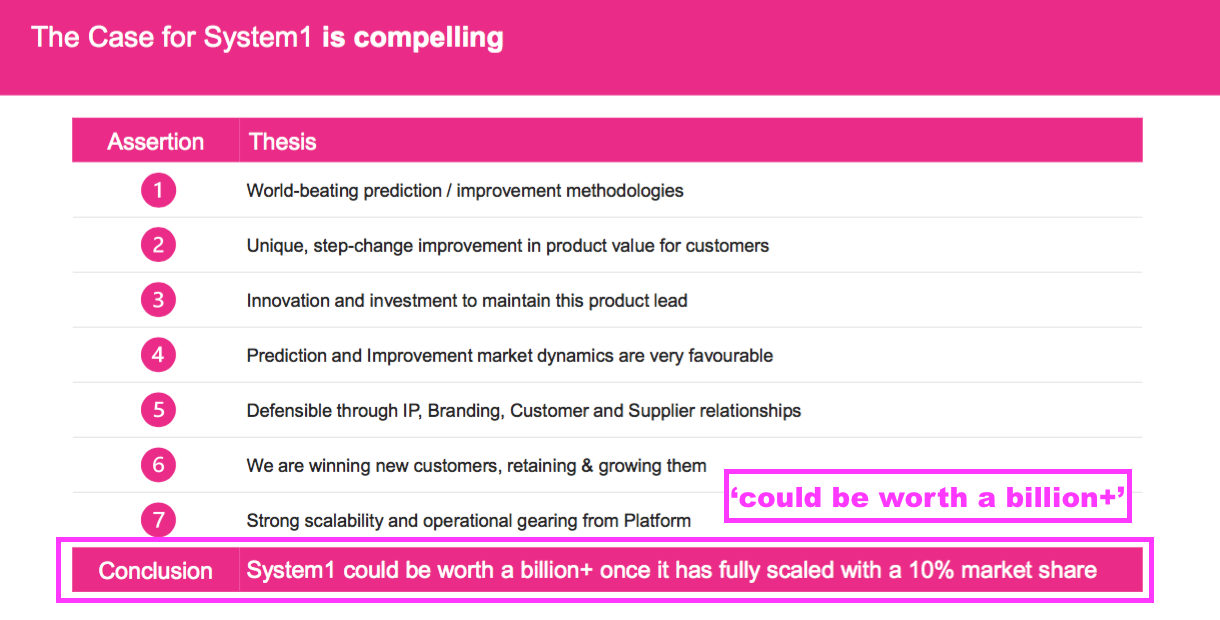

- As a reminder, the FY 2021 results explained why SYS1 could “credibly become a global winner in marketing predictions” through seven ‘Reasons to Believe’.

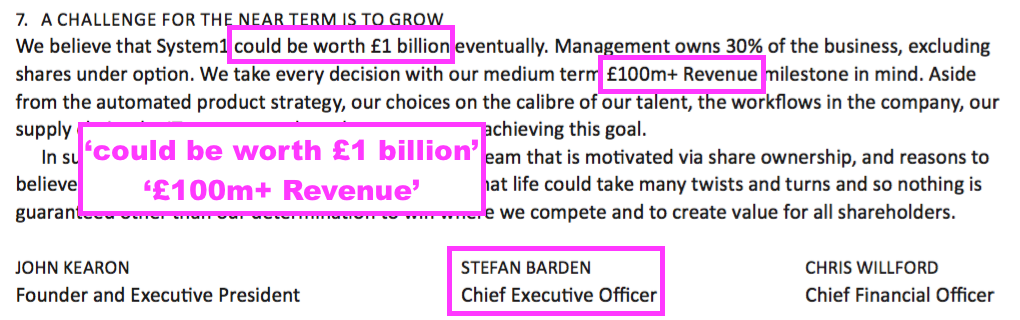

- Number 7 of FY 2021’s ‘Reasons to Believe’ included a bold £100m-plus revenue target (versus revenue of £23m at the time) and an even bolder eventual market cap of £1 billion (versus a market cap of £40m at the time):

“7. A challenge for the near term is to grow

We believe that System1 could be worth £1 billion eventually. Management owns 30% of the business, excluding shares under option. We take every decision with our medium term £100m+ Revenue milestone in mind. Aside from the automated product strategy, our choices on the calibre of our talent, the workflows in the company, our supply chain, the IT systems, and much more support achieving this goal.“

- The Reasons to Believe were then updated for FY 2022, and number 7 did not repeat the ambitions for revenue or for the market cap:

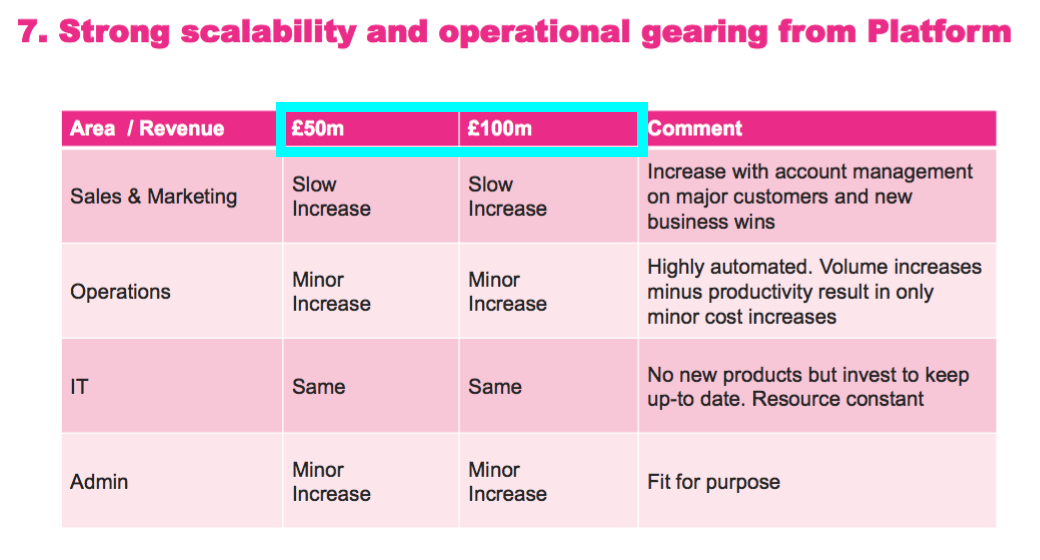

“7. Strong scalability and operational gearing from platform

For speed to market, we launched our market leading, automated prediction products as standalone products, allowing our customers the benefits of testing fast and often over the last year. Now that we have built and launched these products, we are building a fully integrated platform, with a customer friendly user interface.“

- At least SYS1’s FY 2022 presentation claimed the group could be “worth a billion+ once it has fully scaled with a 10% market share”:

- But the £100m-plus (and the £50m-plus) revenue ambition was last seen within the H1 2022 presentation:

- I asked about the watering down of the Reasons to Believe text at the 2022 AGM. Management replied:

“The ambition is as strong and as big as it has always been. But at the same time, let’s keep it real. Realism and belief.”

- The “realism” no doubt reflected the Q4 2022 profit warning that blighted the FY 2022 results.

- The H1 2023 presentation ominously did not refer to projected market shares, market caps or market revenue at all.

- This effective U-turn on the bold ambitions cited within the original Reasons to Believe coincided with the conclusion of the strategic review.

- Concluding the strategic review would have been the ideal opportunity for management to re-emphasise its market share, market cap and market revenue ambitions.

- And yet the chance for SYS1 to reassure shareholders about these longer-term targets was lost… at least at the H1 stage (see Capital Markets Day: strategic optimism).

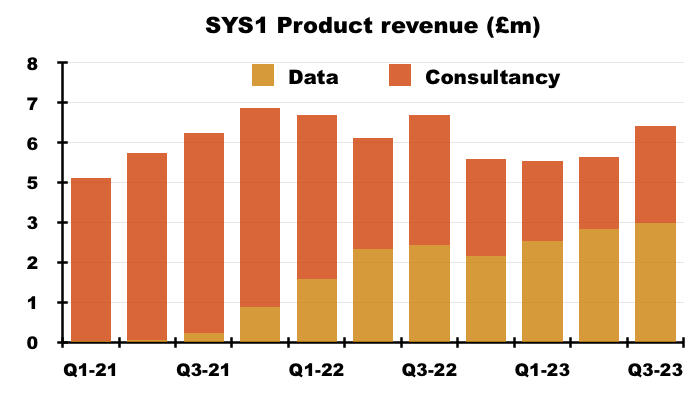

Data versus Consultancy

- This H1 statement reiterated SYS1’s transition from supplying bespoke consultancy work to providing automated data services:

“Our transformation to a digital/data-led business is well underway.”

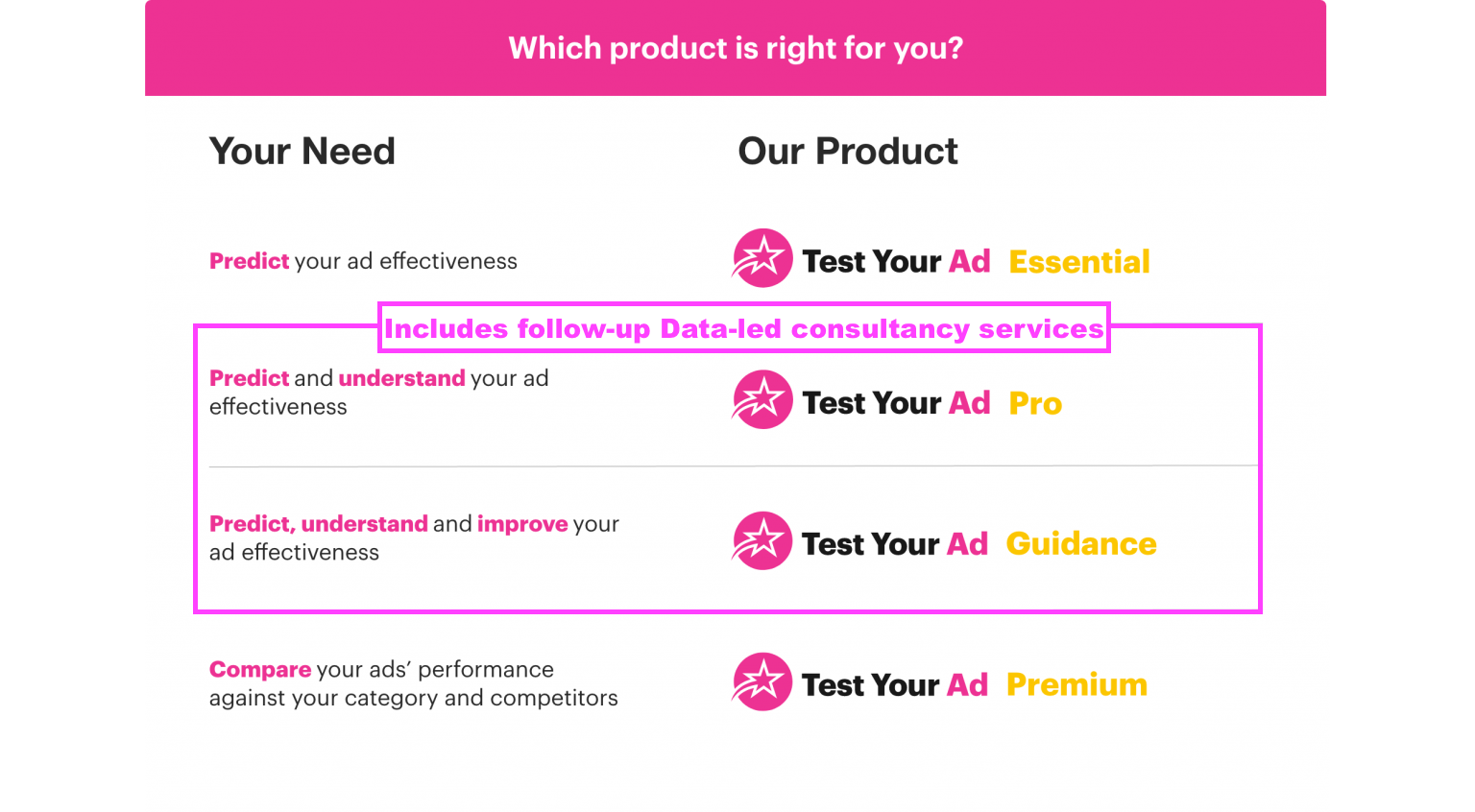

- Data products are led by Test Your Ad…

- …which was launched during April 2020 and allows customers to upload proposed television adverts to SYS1 and receive a report within 24 hours based upon the verdict of an online panel (example pdf here):

- The Capital Markets Day hosted during April 2022 included a demo of Test Your Ad from 12m00s:

- Data revenue is supported by Test Your Brand and Test Your Idea, which perform the same online-panel function for company brands and product ideas:

- Test Your Brand and Test Your Idea were launched during November 2021 and May 2022 respectively.

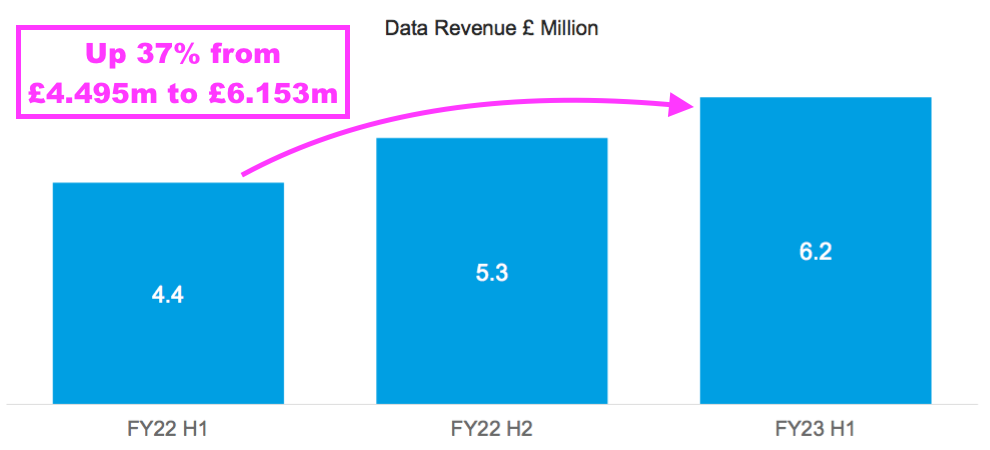

- This H1 revealed Data revenue up 37% to £6.2m:

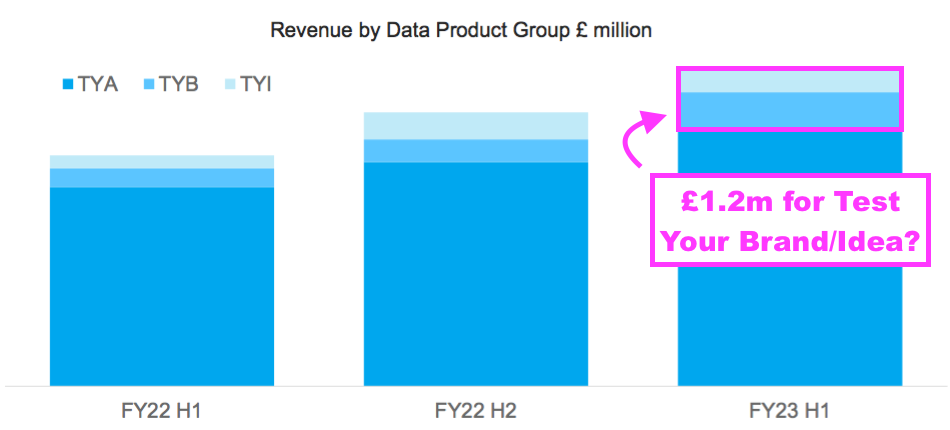

- Boding well perhaps is Test Your Brand and Test Your Idea earning a greater aggregate share of Data revenue:

- Test Your Brand and Test Your Idea look to have generated revenue of approximately £1.2m during this H1 (or 19% of Data revenue), versus approximately £5.0m for Test Your Ad.

- For the preceding FY 2022, Test Your Brand and Test Your Idea may have generated revenue of approximately £1.6m (or 16% of Data revenue) versus approximately £8.1m for Test Your Ad.

- Note that SYS1 has in the past claimed the market sizes for Test Your Brand and Test Your Idea are both more than double the market size for Test Your Ad:

- But that claim was not repeated… at least within the H1 2023 presentation (see Capital Markets Day: strategic optimism).

- February’s Q3 update disclosed Q3 2023 Data revenue advancing 18% to a new £3.4m quarterly high:

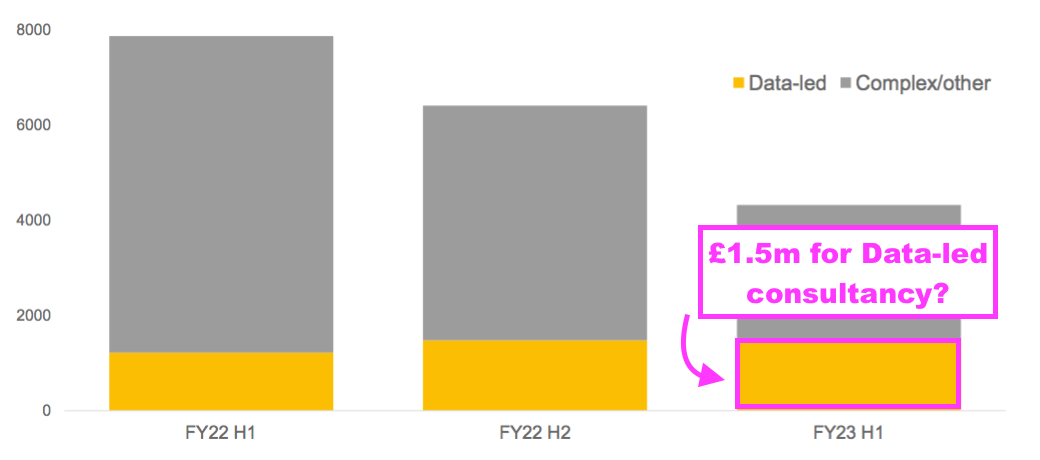

- Note that SYS1’s Consultancy revenue includes new-style Data-led consultancy as well as the old-style bespoke research:

- Data-led consultancy consists of follow-up improvements and guidance from SYS1’s advert experts:

- Data-led consultancy looks to have produced revenue of approximately £1.4m-£1.5m during each of H1 2022, H2 2022 and this H1 2023…

- … and for some reason does not appear to be growing as quickly as Data revenue.

- Maybe that is why SYS1 did not report exact revenue from the differing consultancy types… despite the comparable H1 2022 suggesting otherwise:

“In future reporting periods we will report the revenue from standard consultancy separately from the complex bespoke projects.”

- I estimate Data and Data-led consultancy represented 73% ((£6.2m+£1.5m)/£10.5m) of total H1 2023 revenue (see Capital Markets Day: new information).

Partnerships

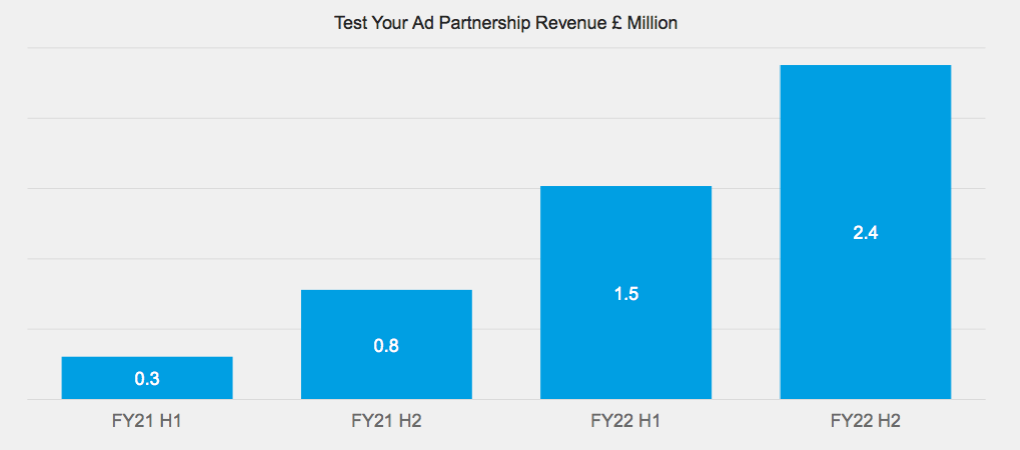

- The preceding FY 2022 revealed the growing influence of partnerships on SYS1’s revenue:

- Revenue from partnerships during FY 2022 was £3.9m and was “the most significant source of new business“:

“The most significant source of new business has been through partnerships with advertising agencies and media platforms like LinkedIn, ITV, and Globo.“

- Partnerships with high-profile media groups underpin SYS1’s claim of being a “global industry thought leader with a superb, proven suite of products” that “outperforms… competitors on the key measure of ‘predictiveness’ as well as on speed and cost“.

- My FY 2022 sums pointed towards partnerships being responsible for approximately 75% of new business.

- This H1 did not disclose details of partnership-derived income.

- But SYS1 did declare the following goal as part of the strategic review:

“Significantly increase our focus on commercial partnerships with major ad platforms/media owners such as LinkedIn and ITV. These platforms provide the Company with access to multiple advertisers at significantly reduced customer acquisition costs.”

- Mind you, if partnerships with the likes of LinkedIn and ITV were already SYS1’s most significant source of new business during FY 2022…

- …and such partnerships already gave SYS1 access to customers at “significantly reduced” costs…

- …then why did this H1 and the preceding H2 2022 incur such unsatisfactory profit performances?

- SYS1’s strategic review added:

“Furthermore, we will target advertising & media agency groups, such as Omnicom/BBDO, and professional service firms who provide advertising effectiveness advice to multiple clients, with a view to including our ‘Test Your’ and ‘Improve Your’ products in their suite of service recommendations, again reducing customer acquisition costs.”

- The case for advertising agencies to utilise SYS1’s services was made by industry guru Mark Ritson during this SYS1 podcast:

Customers and employees

- SYS1 disclosed the number of Data customers for this H1:

“We had 240 Data customers in H1, of which 85 were new.”

- H1 Data revenue of £6.2m gives annualised Data revenue per Data customer of approximately £51k.

- £51k per Data customer does not sound a lot when clients name-checked within the preceding FY 2022 included adidas, Sky, Aldi and Intel.

- The preceding FY 2022 said:

“Our Test Your Ad automation, increased industry profile, and Partnerships with ITV, LinkedIn, Globo, enabled us to win 209 new customers in the year, many of which are industry leaders like Lenovo and H&M. Our total customer base rose to 465, an increase of 17%.”

- 240 Data customers during this H1 compares to 465 total customers during FY 2022.

- 85 new Data customers during this H1 compares to 209 total new customers during FY 2022.

- The customer numbers disclosed for the preceding FY 2022 and this H1 were not like-for-like, although the differences relate to old-style Consultancy clients that management implied at the 2022 AGM the group was no longer trying to attract:

“The focus of the sales team… is building the future business, which is the Test Your Ad, Test Your Brand, Test Your Idea platform“

- Bear in mind customers may not need to use SYS1’s services during any particular H1 or H2.

- But the customer stats nonetheless suggest the run-rate of new clients did not improve during this H1 versus FY 2022.

- The effectiveness of the sales and marketing team during this H1 appeared to deteriorate versus FY 2022 as well.

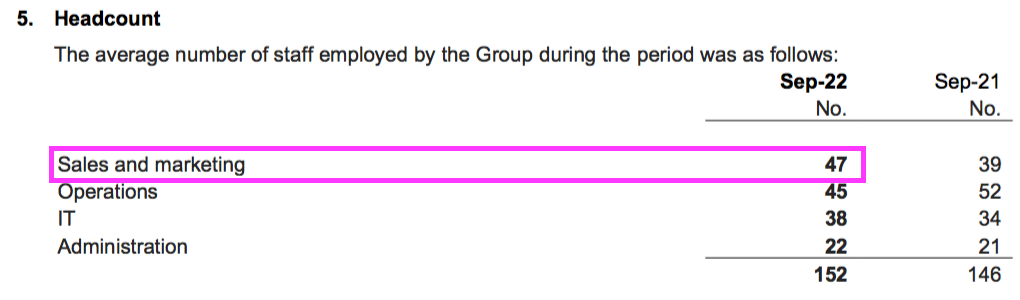

- SYS1 employed 47 people within its sales and marketing department during this H1:

- 47 sales people winning 85 new Data customers during this H1 gives an annualised Data customer win rate of 3.6 per person.

- For FY 2022, 43 sales and marketing employees attracted 209 total new customers, giving a total customer win rate of 4.7 per person.

- Suffice to say, SYS1’s inconsistent reporting of customer numbers (total for FY 2022 versus Data-only for H1 2023) does not help shareholders understand the progress the business is making.

- The activities of the sales and marketing team were outlined during February’s Capital Markets Day, with productivity influenced by lots of ‘hand holding’ to convert large companies into customers (see Capital Markets Day: strategic confusion).

Financials

- SYS1’s unsatisfactory financial performance during this H1 and the preceding H2 leaves the group’s net cash position as the primary accounting attraction.

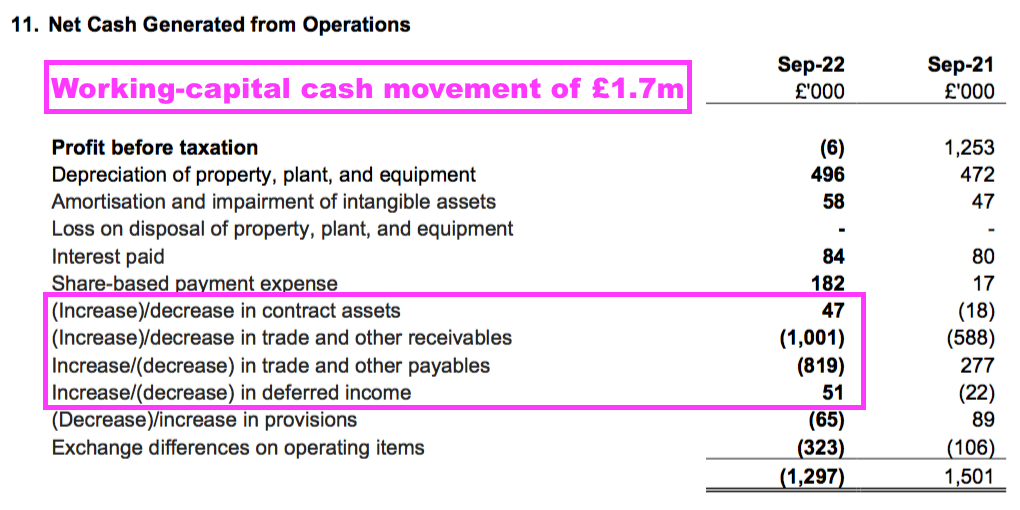

- Net cash declined by £2.1m to £6.6m during this H1.

- Adjusting for share buybacks (£0.1m) and foreign-exchange gains on cash held in the bank (£0.7m), the underlying H1 cash outflow was a very unwelcome £2.6m.

- A £1.7m working-capital outflow was a major cash-flow movement, and largely reversed the £2.2m inflow witnessed during the preceding FY 2022:

- Trade and other receivables at £5.5m was the largest balance-sheet entry after cash, and the £5.5m represented 25% of trailing twelve-month revenue that was not out of keeping with previous H1 results.

- Bypassing the income statement were IT costs of £654k:

“During the period ended 30 September 2022, the company has capitalised £654k of development costs in respect of three key projects: the credit platform, the notifications service and the team management system. The platforms were not complete as at the period end; therefore no amortisation has been recognised.”

- Deciding to capitalise IT development costs is not a good accounting look when:

- Previous IT development costs were capitalised but then written off because of insufficient product sales, and;

- Reported profit has become minimal.

- H1 bank debt of £2.5m matched that from the preceding FY 2022, and the subsequent Q3 statement confirmed all the borrowings had been repaid.

- The Q3 statement also revealed net cash had declined a further £1.5m to £5.1m, due in part to “high quarter-end working capital following a strong December”.

- Attempting to even out possible seasonal working-capital fluctuations, net cash between Q3 2022 and Q3 2023 declined by £3.0m, or £2.3m excluding share buybacks.

- That £2.3m cash outflow would have been flattered somewhat by the aforementioned foreign-exchange gains on cash sat in the bank (£0.7m for this H1).

- The over-riding concern is underlying cash flow absorbing at least £2m — and perhaps close to £3m — during the 9-12 months to December 2022…

- …which if continued could reduce SYS1’s £5.1m cash position to zero within two years.

- At least the subsequent Q3 update said net cash ought not to reduce during Q4 2023.

- The aforementioned absence of a reconciliation of adjusting items is a backward step for SYS1’s reporting. The company used to disclose adjusting items clearly within its H1 results up until H1 2021:

- Aggregate net adjusting items for FYs 2020, 2021 and 2022 came to £3.8m, and have been significant versus the £3.3m aggregate pre-tax profit reported during the same three years:

- SYS1’s ongoing lack of profit turns the spotlight onto its cost base.

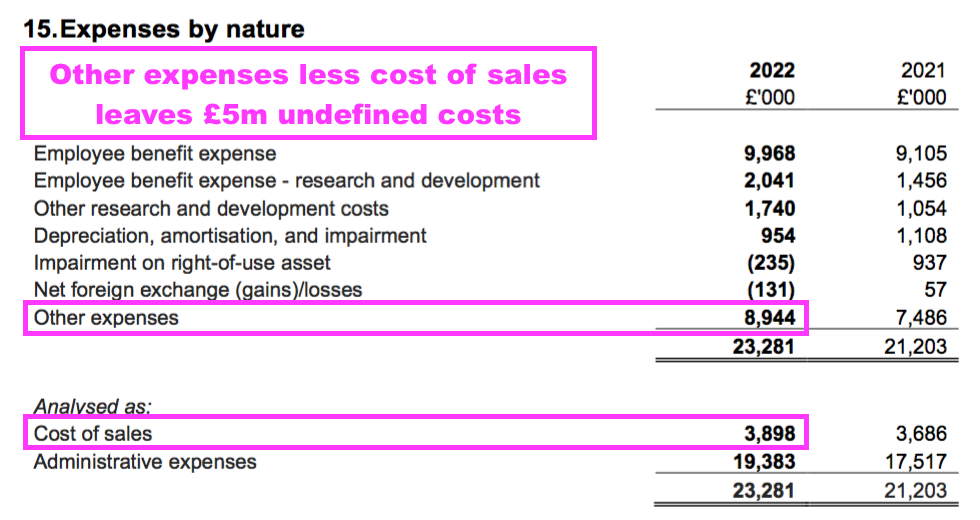

- The 2022 annual report divulged total undefined ‘other expenses’ of £8.9m:

- Subtracting cost of sales (e.g. payments to panellists and translators) of £3.9m then gives undefined ‘other expenses’ of £5.0m.

- Undefined ‘other expenses’ of £5.0m represented 19% of FY 2022 revenue, which is the highest proportion among my 11 shares.

- Among my 11 shares, undefined expenses range from 0% of revenue at Andrews Sykes (FY 2021) to 18% at Tristel (FY 2022), with an average of 11%.

- I do wonder whether SYS1’s notable ‘other expenses’ provide scope for cost reductions. My question on this matter was not answered at the Capital Markets Day (see Capital Markets Day: other Q&A).

Capital Markets Day: strategic optimism

- Hosted last month, SYS1’s Capital Markets Day (CMD) reiterated the conclusions of the strategic review and included slides ‘missing’ from the H1 2023 presentation.

- The “System1 could be worth a billion+ once it has fully scaled with a 10% market share” ambition returned…

- …as did the market sizes of SYS1’s different industry applications:

- Management did not explain why those slides were excluded from the strategic-review conclusion within the H1 2023 presentation.

- Nor did management really comment on the “billion+ once it has fully scaled with a 10% market share” ambition during the CMD…

- …which was surprising, as the recent £24m market cap offers significant shareholder upside were the ambition to become reality.

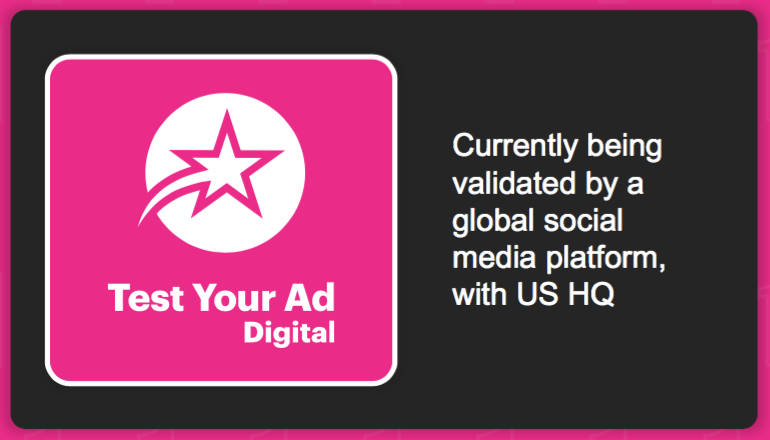

- Other encouraging CMD slides included talk of Test Your Ad “being validated by a global social media platform“…

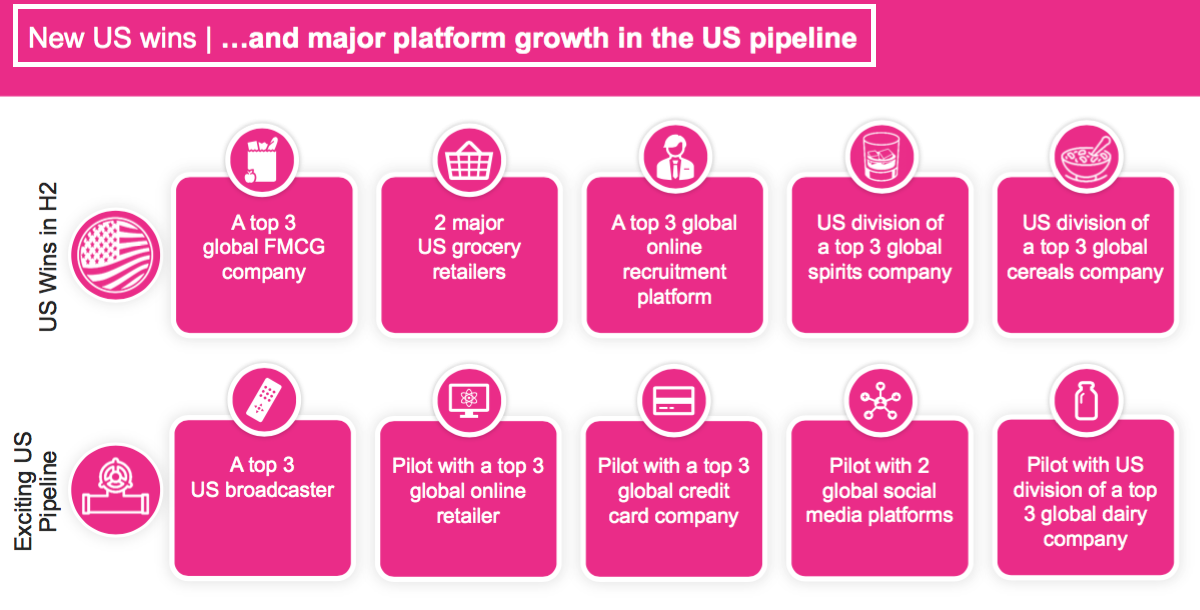

- …and various “new US wins” during the current H2 2023:

- The US division now employs Jason Chebib, who might be a good recruit given he was previously head of market research at Diageo:

- Management’s CMD commentary was very bullish on the US salesforce:

“We have rebuilt the team [in the US], we did not have a full complement but now we have a full team and they are firing on all cylinders let’s say.”

- Management also claimed its “fame-building” activities through podcasts, books and emails had lifted inbound sales enquiries by 28% year-on-year, with a 78% improvement enjoyed during January and February:

- Also of note were management remarks about partners paying for promotional activities:

“Wise Up is funded by our partners, so what’s lovely is our customers are actually paying us to do the kind of research that they then want to talk about.”

- The FY 2022 statement previously revealed such promotional work had contributed to greater expenses:

“Of the £3.0m cost increase year on year about a half was people costs and the other half external spend such as fame building activities including Ad of the Week and the launch of Look Out and Feeling Seen.“

Capital Markets Day: strategic confusion

- The CMD presentation contained some confusing remarks and slides.

- The chairman claimed he “instigated” the strategic review when he took on his current role:

“I was delighted to be asked to join System1 Group in 2021 as a non-executive director, but did find them somewhat lacking strategic clarity and in particular how to execute it commercially with a resultant lack of overall growth. So on becoming chairman late last year, I immediately instigated a full strategic review which frankly was overdue, and we appointed two excellent new NEDs, Conrad Bona and Phillip Machray, to take major roles in that review.“

- The strategic review was in fact launched at the end of August while the chairman was appointed to his role a month later at the conclusion of the 2022 AGM.

- Furthermore, when the board was asked at the 2022 AGM about the progress of the strategic review, the previous chairman and another non-exec did all of the talking while the current chairman — who claimed to have “instigated” the review — said nothing.

- Oh, and the aforementioned 2022 AGM comments suggested “institutional shareholders” who were “obviously very concerned about capital allocation” actually did a lot of the instigating of the strategic review (see Strategic review)!

- The CMD presentation confirmed a dependence on old-style Consultancy work that appeared to counter the “transformation to a digital/data-led business” cited within the H1 2023 statement.

- Management CMD’s commentary acknowledged the “world’s largest advertisers” required old-style bespoke consultancy to get started with SYS1:

“We want to retain the ability to deliver bespoke consultancy, because it is very, very valuable in how we onboard the world’s largest advertisers.They often need specific support while they transition into our methodology, so what we know is that… we want to retain the specific original consultancy business only to allow us to grow the future of [Data] predictions and improvements going forward.”

- Given one of SYS1’s goals is to attract the “world’s biggest advertisers“…

- …old-style Consultancy revenue will therefore remain important to SYS1…

- …which in turn suggests the group will not become entirely dependent on ‘scalable’ Data income within the foreseeable future.

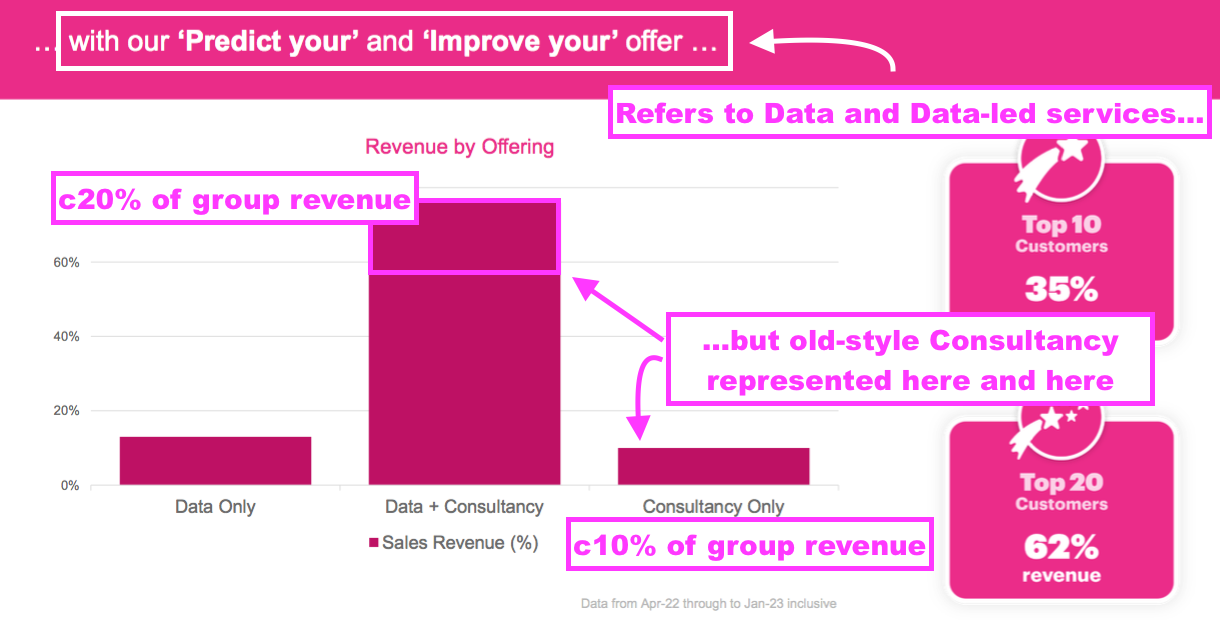

- SYS1 confirmed my aforementioned sums that Data and Data-led consultancy represented more than 70% of total revenue:

“The standard Predict and Improve products represent just over 70% of Group revenue in the current financial year to date.“

- Old-style Consultancy therefore supported almost 30% of total revenue…

- …although the CMD presentation may have given the impression old-style Consultancy represented only 10% of revenue:

- The need to supply old-style Consultancy for the world’s largest advertisers explains why SYS1 must employ 47 sales and marketing people; lots of bespoke ‘hand holding’ is required to turn a sales pitch into a pilot test into a happy Data customer.

- Management’s CMD commentary seemed to admit only three people had previously worked full time on recruiting new customers:

“It is incredibly important in a growing business… you have to have a dedicated resource focused on winning new customers and I am delighted to say we have increased our headcount from three to thirteen in pursuit of that goal. The majority of those heads have only joined in the second half, so the impact has still yet to be seen. But we are committed to focusing the resource on where it makes the biggest difference.“

- No wonder the chief exec acknowledged his days are spent mostly on sales:

“The majority of my time is focused on the commercial side of the business. What is really clear is that our product and platform have been built to an absolutely brilliant standard…but where we will be judged will be the success of our commercial space so I am working really closely with… our customer-facing and revenue-driving side to really help drive forward that part of the business.”

- The CMD was the ideal opportunity for SYS1 to expand upon the ‘Rule of 40’ financial ambition declared within the strategic review.

- But SYS1 instead said:

“The Company re-emphasises its intention to become a Rule of 40 business, balancing growth in its standard, repeatable Predict and Improve products with return measured by Adjusted Group EBITDA as a % of Group Revenue. Supporting goals, measures and targets that support the Rule of 40 objective will be communicated at future full-year and interim results announcements.“

- A protracted absence of the “supporting goals, measures and targets” might suggest the ‘Rule of 40’ objective was set originally without the “supporting goals, measures and targets” actually in place.

- At least management’s CMD commentary revealed the yardsticks that would be monitored:

“The topics we have covered are essentially where we would like those [supporting Rule of 40] measures to be. So we have talked about US revenue growth, we have talked about our customers, so customer churn for example, we have talked about the number of top advertisers and the number of partners that we onboard, and we also want to talk about recurring and repeatable revenue as well going forward.“

Capital Markets Day: new information

- The CMD presentation provided various new snippets of customer information.

- Extra stats included these percentages:

“Over three quarters of our revenue (calculated for the period from April 2022 to January 2023 inclusive) comes from customers that purchase both Data and Consultancy from System1. Over the same period, the 10 largest customers accounted for 35% of revenue, the 20 largest, 62%.“

- After applying those percentages to the total revenue of £22.0m achieved during the twelve months to December 2022:

- Customers 1-10 spent £7.7m collectively, or £770k each on average, and;

- Customers 11-20 spent £5.9m collectively, or £590k each on average.

- Versus my aforementioned £51k per Data customer, larger customers might appear to spend much more on old-style Consultancy than on the new-style Data services.

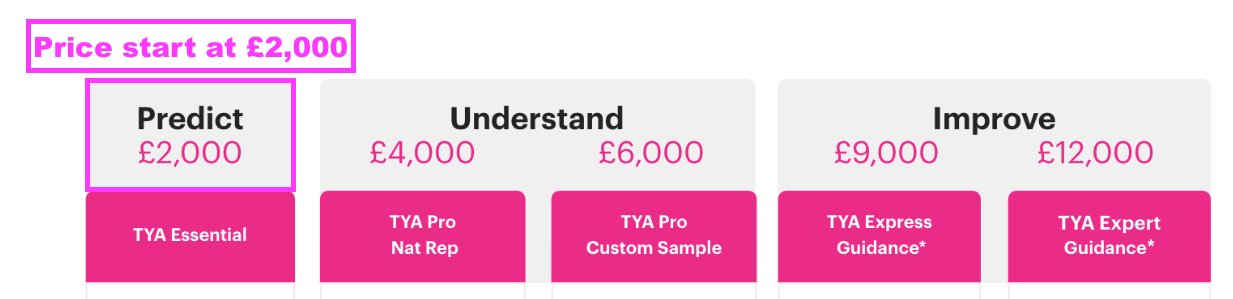

- Such a large difference should not be surprising, given the new-style Data services are deliberately offered with “market beating… value” and prices starting at just £2k:

- But SYS1 did say…

“Customers that purchased only Data products this financial year spent significantly less on average than our 20 largest customers.”

- …which could mean Data revenue per customer may be skewed by the top 20 customers spending lots on Data (and Consultancy) alongside numerous smaller customers spending very little on Data only.

- Indeed, the CMD revealing old-style Consultancy representing almost 30% of revenue could mean old-style Consultancy income was £6.6m (£22m * 30%) during the twelve months to December 2022…

- …and if that £6.6m was attributable entirely to the top 20 customers, then those top 20 customers would have also spent £7.0m (£22m * 62% less £6.6m) on new-style Data services… or £350k each.

- SYS1 also said:

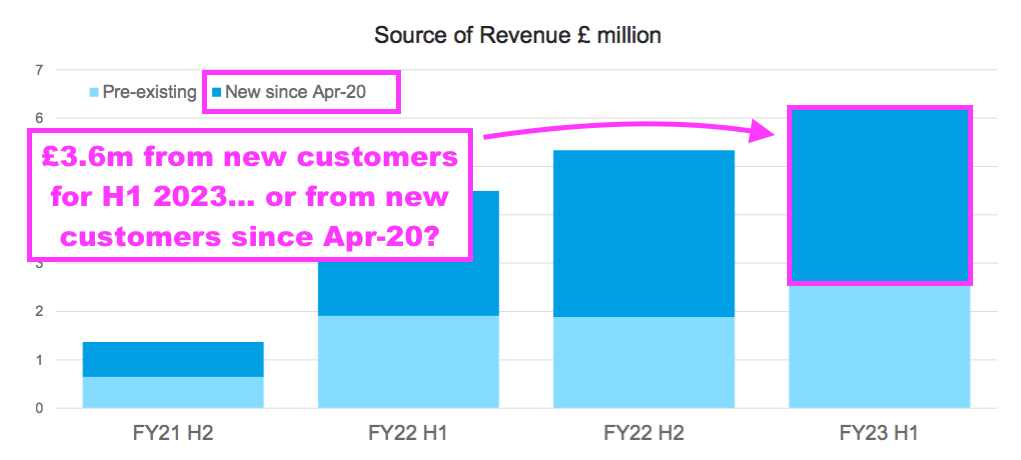

“£3.6 million of the £6.2 million Data revenue we reported in H1 of the current financial year came from customers that did not purchase from System1 in the preceding financial year.“

- £3.6m from the 85 new Data customers during H1 gives annualised average Data revenue of £85k per new Data customer.

- £2.6m (£6.2m less £3.6m) from the 155 existing Data customers during this H1 gives annualised average Data revenue of £34k per existing Data customer.

- Spend per Data customer therefore appears to have increased significantly, at least according to the limited CMD information about Data customer numbers:

- Given the unsatisfactory profit performance during this H1 and the preceding H2 2022, the obvious question is how SYS1 can persuade customers to spend much more than £34k/£85k/£350k a year on the new-style Data services?

- Questions on this matter were asked during the CMD Q&A, but were not addressed properly (see Capital Markets Day: other Q&A).

- Suffice to say (again!), SYS1’s inconsistent reporting of customer numbers (total for FY 2022 versus Data-only for H1 2023) does not help shareholders understand the progress the business is making.

Capital Markets Day: other Q&A

- The CMD’s Q&A session was frustrating. I submitted multiple questions and the following were not asked:

Q) Annualised revenue per new Data customer during H1 2023 was £3.6m*2/85 = £85k each, which does not appear huge given Data customers include big names such as Sky, Intel and Aldi.

How does management view this £85k average and what is management’s ambition with this figure following the strategic review? How much more than £85k/year could new Data customers pay and the company still maintain its ‘disruptive’ pricing?

Q) The company’s FY 2022 presentation said Test Your Ad revenue through partnerships was £3.9m during FY 2022, and was the “most significant source of new business.”

The strategic-review conclusion then said: “These platforms (ITV and LinkedIn) provide the Company with access to multiple advertisers at significantly reduced customer acquisition costs.”

Why then does the business remain unprofitable when the ‘most significant source of new business’ during FY 2022 were the media platforms, which *already* provide access to customers at a ‘significantly reduced cost’?

Q) The greater focus on testing digital ad formats suggests the partnership with LinkedIn will become of greater significance.

What details can management provide to highlight the positive progress of this particular partnership, such as the number of customers acquired through LinkedIn versus this time last year? And what details can be provided about ITV and the progress made there?

Q) ‘Other expenses’ were £9m in FY 2022. Assuming £4m of the £9m reflected cost of sales (panel costs etc), £5m is left undefined (representing c26% of all administrative costs). Given the company’s lack of profitability, can management explain the nature of these undefined ‘other’ costs and their necessity to the business?

Q) The strategic review concluded with a single financial goal of becoming a ‘Rule of 40’ company, although that goal could be achieved at the expense of cash flow and further reductions to the net cash position. Following the strategic review, what then is management’s cash flow ambition for the next 1-2 years?

- Other questions I submitted were amalgamated with others into broader questions about the sales team, the ‘Rule of 40’ and US revenue.

- The CMD was billed as a 90-minute event but finished after 80 minutes, so questions were not overlooked because of a lack of time.

- My questions at the 2022 AGM did not appear to be welcomed either.

- At least this question of mine was asked and answered during the CMD:

Q) What consideration was given to undertaking a formal sales process during the strategic review? Given the ongoing lack of profitability, the company would appear to be better suited within a larger organisation — whereby an acquirer could remove duplicate/extraneous expenses and deliver a (long-awaited) return to System1 shareholders.

A) “[A formal sale process] was something we looked at in the strategic review but we were very clear that this was the wrong time for this business to consider a sale, and that when you are doing well and you are seen to be successful and seem to be growing, then people tend to come and talk to you and then that’s the time when you can consider whether any of those [people] are suitable to turbocharge your growth.”

Valuation

- SYS1’s recent losses and negative cash flow does not make assessing its £24m market cap straightforward.

- Management confirmed during the CMD that greater revenue was required to return the group to profit:

“We will become profitable when we move out of the current revenue range given that we’re marginally profitable today… it’s that simple.“

- Gross margin during H1 2023 and the subsequent Q3 was approximately 82%, while total adjusted operating costs are approximately £19m per annum.

- Applying an 82% gross margin to potential revenue of £25m then subtracting adjusted costs of £19m gives an adjusted operating profit of £1.5m — which could be the minimum required to ensure positive cash flow to cover future capitalised IT costs.

- Potential revenue of £25m compares to actual revenue of £22m for the twelve months to December 2022.

- Applying an 82% gross margin to potential revenue of £30m then subtracting adjusted costs of £19m gives an adjusted operating profit of £5.6m — which should generate meaningful positive cash flow after future capitalised IT costs.

- Assuming old-style Consultancy revenue remains unchanged, Data and Data-led revenue may have to increase by 50% to almost £24m for total revenue to reach £30m… which seems unlikely to happen overnight when Q3 2023 Data revenue advanced by 18%.

- And could revenue increase to £30m with adjusted operating costs remaining at £19m?

- The H1 statement admitted costs were increasing:

“Whilst the second half of the year has started well, and we expect H2 revenue to exceed H1, the Board is mindful of the current economic backdrop particularly in Europe. The higher H1 exit run-rate for expenditure, combined with exchange rate and inflationary pressures are likely to increase expenditure and erode profitability in H2. We now have the platform and human capital to serve a significantly bigger revenue base and are focused on growing from this point to deliver superior returns to our shareholders.”

- The worry of course is costs will continue to increase and the superior ‘platform’ economics of the Data activities will in turn struggle to emerge.

- After all, the CMD confirmed almost 30% of revenue remains old-style Consultancy work while management’s CMD commentary highlighted the need to retain such bespoke skills to win the very largest customers.

- A more pressing concern is understanding why SYS1 is unprofitable despite operating as a “global industry thought leader with a superb, proven suite of products” that “outperforms… competitors on the key measure of ‘predictiveness’ as well as on speed and cost“.

- ‘Market leader’ SYS1 ought to be very successful, but instead:

- Current revenue is lower than FY 2013 revenue;

- Underlying cash losses are running at £2m-plus;

- The dividend went missing more than three years ago, and;

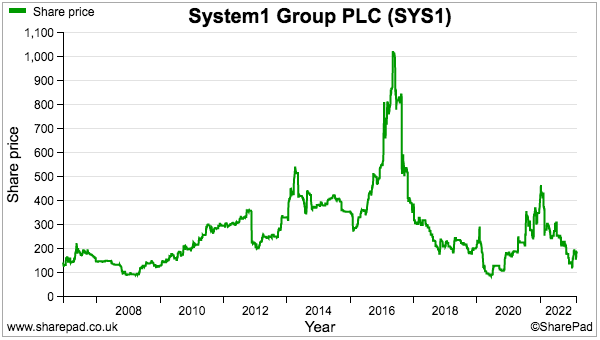

- The 190p share price is at a level first achieved during 2007:

- The lack of real progress remains frustrating, not least because SYS1’s Data transition essentially started five years ago by developing AdRatings to “create new scalable revenue streams“.

- Partnerships with ITV and LinkedIn — which should open the door to numerous new customers at “significantly” lower cost — have meanwhile not delivered an obvious profit boost.

- Not for the first time I am left to ponder whether SYS1 really offers services of interest to the general marketing industry (from FY 2019):

“The lack of AdRatings revenue raises a wider doubt about the whole business — are SYS1’s services actually of any interest to the majority of marketing departments?“

- Maybe SYS1’s products are actually nothing special?

- Or maybe the products are great, but the marketing is poor? (Remember the indulgent Where the Lemons Bloom?)

- Or maybe the products and marketing are great, but the ‘disruptive’ Data pricing is too low to cover the necessary costs?

- Or maybe the products and marketing and Data pricing are great, but SYS1’s operations are simply riddled with needless expenses?

- SYS1 meanwhile does itself no favours through:

- Inconsistent reporting of customer numbers and adjusting items;

- Once again capitalising IT costs;

- Incurring significant undefined ‘other expenses’;

- Delaying details of the “supporting goals” to the ‘Rule of 40’ ambition;

- Hesitantly citing ambitions about market cap, market share and market revenue, and;

- Appearing not to welcome all questions in a public forum.

- For now I must trust the strategic review pays off and SYS1 eventually hits the big time through digital ads, the world’s largest advertisers, extra partnerships, the United States and the minor boardroom re-jig…

- …

and look back at the 2022 AGM protest votes and speculate whether the strategic review will increase or decrease shareholder dissatisfaction at the 2023 AGM.

- …although shareholders suddenly look set to be rescued by the welcome receipt of a requisition notice.

Receipt of requisition notice

- This week SYS1 revealed two former executives had requisitioned a general meeting to implement various board changes:

“System1 announces that it has received an email dated 3 March 2023 from Stefan Barden (former System1 chief executive officer and Board adviser) and James Geddes (former System1 chief financial officer) seeking to requisition a general meeting of the Company (the “Requisition”) unless certain board changes were agreed to by the Company’s board of directors (the “Board”), as set out below.“

The board changes proposed by Stefan Barden and James Geddes are to:

(i) retire Rupert Howell as Chairman and a Non-Executive Director of the Company;

(ii) elect Stefan Barden as Executive Chairman and a Director of the Company;

(iii) retire Philip Machray as a Non-Executive Director of the Company; and

(iv) re-elect John Kearon as a Director of the Company but moving into a Non-Executive capacity.

- SYS1 rejected the proposed changes:

“Certain members of the Board have met with Stefan Barden and James Geddes on 6 March and have communicated that the Board is firmly of the view that changes proposed by the Requisition are not in the best interests of the Company or its shareholders.“

- Meeting requisitioners Stefan Barden and James Geddes clearly felt SYS1’s plans following the strategic review and subsequent Capital Markets Day were not sufficient to return the group to worthwhile levels of profit.

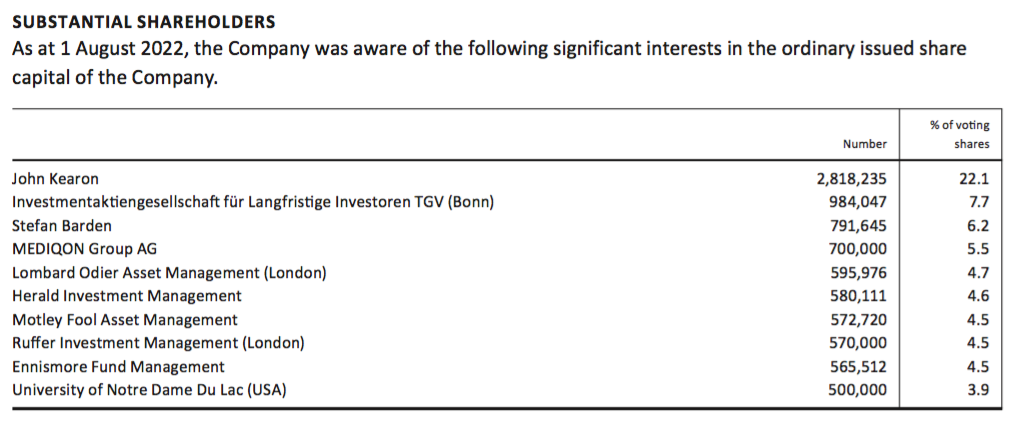

- The 30%-plus protest votes at the 2022 AGM suggest the proposed board changes are likely to attract significant support.

- Mr Barden is a 6% shareholder while Mr Geddes (according to the 2020 annual report) owns approximately 2%.

- SYS1 founder and executive John Kearon owns 22%, who will certainly vote against being demoted to a non-exec and the other proposed changes. Other board members own approximately 0.9%.

- Matters will almost certainly be decided by the eight top institutional shareholders, who collectively own another 40%:

- The general meeting may well provide shareholders with the very welcome/radical/intriguing outcome that I had thought possible through the strategic review.

- Mr Barden could in fact be the new executive chairman SYS1 desperately needs…

Stefan Barden

- Stefan Barden became a SYS1 board executive during June 2020 following more than 18 months as a board “adviser“:

“System1… today announces that it has appointed Stefan Barden to the board of directors of the Company as an executive director with immediate effect.

From November 2018, Stefan has been an adviser to the board of directors on strategy and technology, and has recently taken on the executive role of chief operating officer to assist the Company through its next phase of development. He will return to the advisory role when this is complete, expected to be in around a year.“

- Mr Barden then became chief executive during March 2021:

“System1… announces that, in line with the continued evolution of the Company, John Kearon, previously Chief Executive Officer, has today assumed the title of ‘Founder and Executive President’ and Stefan Barden, previously Chief Operating Officer, the title of ‘Chief Executive Officer‘.

Their internal responsibilities are unaffected, with John leading the Company direction, product development and external facing parts of the business, and Stefan leading the Company’s organisation, technical development and operational parts of the business. No board changes are expected to arise as a result of this development. Stefan will remain an executive director rather than reverting to the purely advisory role indicated last year.“

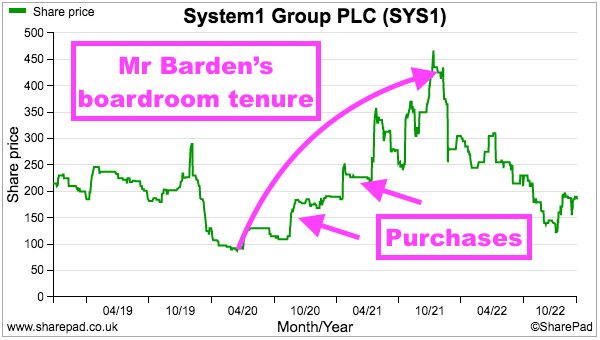

- The promotion seemed prompted by a sudden return to quarterly profitability during the early stages of the pandemic.

- When Mr Barden was first appointed as a board executive, quarterly losses were running at £0.5m…

- …which remarkably transformed into a £0.9m profit by the next quarter and eventually led to a £2m-plus H2 2021 profit and a better-than-expected FY 2021.

- Mr Barden returned to his original adviser role during January 2022…

“System1… announces that, as planned, Stefan Barden will step down as CEO and from the board of directors on 31 January and revert to his previous role as an adviser to the board of directors on strategy and technology. System1’s founder, John Kearon, will return to the CEO role.”

- …and one month later SYS1 issued that Q4 2022 profit warning and the group has not made money since.

- This may be very simplistic, but a pattern seems to have emerged:

- Mr Barden takes on executive board duties, and SYS1 turns from loss to profit, and;

- Mr Barden relinquishes executive board duties, and SYS1 turns from profit to loss.

- Mr Barden left SYS1 during March 2022…

“System1…announces that further to the announcement on 4th January 2022, Stefan Barden has today informed the System1 board of directors (the “Board”) that he will be stepping down as an adviser to the Board with effect from 31st March 2022.”

- … and I am hopeful his (proposed) return to executive duties will herald SYS1 turning losses into profit once again.

- SYS1’s progress during Mr Barden’s boardroom tenure prompted me to more than quadruple my shareholding (Q4 2020, Q2 2021):

- The share price during Mr Barden’s boardroom tenure increased from approximately 100p to more than 400p.

- Mr Barden’s 6% shareholding provides a good incentive for him to take charge of SYS1.

- He bought his shares between September 2018 and January 2021 at prices ranging from 92.5p to 210p (here, here, here, here, here), with his average cost at 181p. None of his 6% shareholding was acquired through options or similar.

- I assume his share buying was, like mine, prompted by believing SYS1 had significant upside potential.

- After all, the FY 2021 results contained those bullish ‘Reasons to Believe’… under which Mr Barden was a signatory:

- Maybe Mr Barden was in fact the architect of that £1 billion market-cap ambition…

- …which may explain why the ‘Reasons to Believe’ were published only after he became chief executive…

- ….and then watered down after he departed SYS1.

- Perhaps Mr Barden has genuine plans for SYS1’s market cap to reach £1 billion…

- …and garnering support for a shareholder vote would be a lot easier if he — unlike SYS1 with its ‘Rule of 40’ ambition — already has the “supporting goals, measures and targets” in place.

- Mr Barden’s initial SYS1 appointment gave a short CV:

“Stefan has over 20 years of General Manager, Managing Director and CEO experience after graduating from McKinsey Management Consultancy and Unilever’s fast-track management development programme. These include CEO of Northern Foods, CEO Heinz UK and Ireland, as well more latterly CEO of the internet business Wiggle which he took from £140m to £360m in sales in 3 years. Semi-retired, he also supports several CEOs, often founders, in developing high growth businesses. System1 is one of these companies.”

- Online trawling finds Mr Barden’s career has involved marketing salad cream, terminating a contract with Marks and Spencer and conducting a significant sports-retail merger.

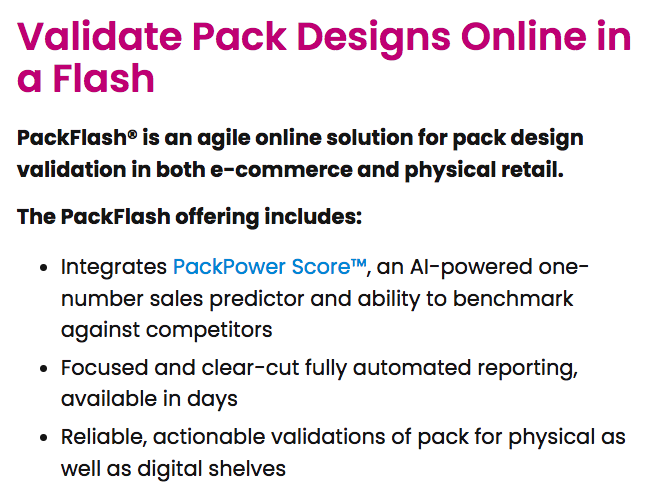

- Further online trawling reveals Mr Barden to be non-exec chairman of Behaviorally, a US business that helps brands “create more valuable transactions as leaders in applying behavioural principles to successful retail marketing“.

- Behaviorally uses a mix of software, data and behavioural science to improve retail packaging for marketing purposes…

- …and has even developed an AdRatings-type service for e-commerce images:

- Acting as Behaviourally’s chairman presumably makes Mr Barden well versed in US marketing, which coupled with high praise from SYS1 founder Mr Kearon a year ago…

“John Kearon said: “ I would like to express the whole Company’s gratitude to Stefan for his immeasurable executive contribution over the past 18 months. Including playing a leading role implementing the new strategy centred around our Marketing Predictions platform, rebuilding our ‘back-office’ from first principles to support it, and reinforcing our Executive Team with key hires to add to our own home-grown talent, including the appointment of a chief operating officer. I’m very pleased Stefan will continue with us in his original advisory role. Thank you, Stefan“. “

- …plus his various mid-cap CEO roles underline some very suitable qualifications for leading SYS1 outright.

- Possibly not a coincidence, but Behaviourally’s chief exec is former SYS1 director Alex Hunt:

- Mr Hunt joined SYS1 during 2009, became co-head of its US business during 2012, was appointed to the board during 2017 and left during 2018.

- SYS1’s US division reported notable growth under Mr Hunt. Between 2012 and 2018, SYS1’s US revenue and US profit (before central costs) improved 72% to £10.3m and 94% to £4.4m respectively.

Verdict on proposed board changes

- I have held SYS1 shares since March 2016 and the subsequent seven years have witnessed SYS1 deliver occasional bursts of very positive progress counter-acted by prolonged periods of setbacks and disappointment.

- True, the pandemic has not helped while the transition from old-style Consultancy to automated Data services was never going to be entirely smooth.

- Mind you, SYS1 was already warning of weaker trading just before the pandemic…

“After H1 single-digit growth, followed by modest further progress in Q3, trading in Q4 to date has been disappointing, due in the main to the ongoing transition of sales talent, and subsequent disruption and decline in adhoc revenue from smaller clients.“

- …while commentary from FY 2019 suggests a general transition to automated services has been underway now for at least five years:

“During 2017/18, our first year as System1, we re-engineered our IP into a highly automated, value-enhancing ‘Ad System’, providing next day predictions, at a fraction of the previous cost, creating more consultancy time for profit-enhancing improvements of good ideas. Clients get a faster-cheaper-better ‘System’ to predict and maximise their advertising investment and we’re better placed to win larger-scale, longer-term contracts and drive the business towards our long-term commercial leadership goal.“

- The fundamental issue remains why SYS1 has failed to thrive long-term despite offering the advertising industry “superior predictiveness… at market-beating speed and price“…

- …and the aforementioned ‘Reasons to Believe’ including numerous ‘moat’-type remarks:

“our pioneering framework”

“our proprietary databases”

“Our products are difficult to copy“

“world-leading intellectual property”

“helping us build unique relationships with key global customers”

“the largest dataset of advertising predictions in the US and UK“

- The unsatisfactory H1 2023 performance, frustrating CMD Q&A plus the various reporting niggles have created growing doubts about SYS1’s stewardship…

- …while the messy AdRatings implementation for example is evidence of sub-par operations occurring well before the pandemic and its aftermath.

- Founder Mr Kearon has been the common executive denominator throughout SYS1’s mostly underwhelming quoted history, and I can only conclude fresh boardroom leadership is required to maximise the group’s “superb, proven suite of products” and re-establish worthwhile levels of profit.

- I will therefore support the proposed board changes at the forthcoming general meeting.

- My contact form is open for anyone wishing to share their views on the proposed board changes and SYS1’s products, marketing, profitability and potential.

Maynard Paton

The article is too long for me Maynard. I got bored before halfway. Others may think differently!

You miss the all important point with SYS1. I looked up what their competitors are doing a couple of years ago. Test Your Ad is very much not unique or ahead of competition. From memory the giant Kantar had something that looked better. I dare say there are dozens of similar things around….

Hi Brian

Thanks for the message. Other companies have TYA-type services, but where SYS1 claims to stand out is through its ‘predictiveness’ accuracy and pricing versus the rest. But the competition is catching up. Note that the service has been validated by partnerships with ITV and LinkedIn, who presumably thought TYA was of use to their own advertisers. You would have thought ITV and LinkedIn would have chosen Kantar etc if TYA was not very good.

Maynard

Maynard,

Not too long for me :-)

I’ve been contemplating the choices we have at the GM and:

I’m not sure Stefan’s tenure at Wiggle is as clear cut as your quote suggests. Companies House suggests revenue was £167m FYE Jan 14 after he joined in Sept 13 rising nicely to £205m in FYE Jan 17, before he then left in April 17. The business was though profitable when he joined and loss making when he departed with losses accelerating in the following year! Chain Reaction appears to have been actually purchased after he resigned but he may have been involved prior to leaving. Stefans website certainly suggests he was instrumental in the deal.

John Kearon is though certainly glowing in his testimonial to Stefan on his website.

Patrick

Hi Patrick

Good point on Wiggle. I could not reconcile the sales figures from Companies House for Wiggle to those quoted by Stefan Barden either. I wondered if there were other (overseas?) group businesses under Mr Barden’s watch that accounted for the difference. Wiggle’s 2017 annual report says “during the previous period Chain Reaction Cycles Limited was acquired by the Group, during the current year the trade and assets of Chain Reaction Cycles Limited was hived up into Wiggle Limited”, which I guess translates as CRC being acquired by Wiggle’s parent first (2016), then transferred into Wiggle later (2017).

John K’s testimonials maybe be the best argument for Mr Barden to take charge!

Maynard

What would it take for you to sell up? Hard to phrase such a question without inferring criticism, there is none. I am a fan of your work. Interested in your process is reason for asking.

Hi Michael

Probably the product really losing its edge and/or the Data strategy falling apart. All the large shareholders find themselves trapped in this illiquid share, which I suspect is why a few have persuaded Stefan Barden to take action. Mr Barden is a large shareholder as well, so if his proposed board changes fail and he sells out (but to whom?), then that would create a serious dilemma for me. All the time there are unhappy large shareholders on the register and the product remains validated by ITV, LinkedIn etc, then there is hope.

Maynard

Maynard,

Yes you’re correct , Stefan became a director of CRC in August 2016 and CRC actually had turnover of £167m in FYE Jan 17 so I think probably Stefan’s revenue claims probably stack up although I can understand why he doesn’t highlight turning 2 profitable businesses into 1 larger unprofitable one on his CV :-).

Any info on his sudden departure in April 17? Seems a strange time whilst the consolidation of the businesses was ongoing.

Patrick

Hi Patrick

Sadly no info on his departure, which occurred c18 months before his appearance at SYS1.

Maynard

Hi Patrick,

Mr Barden has sent in the following chart to clarify the story at Wiggle:

He said the performance of Wiggle under his leadership, when it faced “very severe market-contraction headwinds“, enabled it to become “the undisputed European #1 and consolidator“. He also noted i) Wiggle was profitable and CRC was unprofitable at the time of the CRC purchase; ii) approximately £20m of annual EBITDA synergies were created through the purchase for his successor before he stepped back, and; iii) almost all of his hand-picked team left within 9 months of the new leadership taking charge (which I presume explains why the enlarged group may have then struggled).

Maynard

Thank you for setting the record straight Maynard.

Patrick, I appreciate that Wigggle information at companies house is not the easiest to read. (Strange time periods, need to track two companies, etc), hence I understand your questions. I’m always happy to catch up directly if you have more questions.

Kind regards, Stefan Barden

PS. I stepped back after a bit more than the three years I agreed to come out of retirement for. Job complete I thought. However, performance deteriorated as new management changed the winning strategy. I worry that the same is happening at System1 today.

Thanks for the interesting write up.

I sold SYS1 in Oct 22 for a c. 20% loss after a poor investor presentation from the major shareholder, who appeared smug and out of control of the US (and more generally). I also think AI developments may well undermine their product – again, the major shareholder appeared out of touch on this point.

Barden was one of the reasons I invested and I should have sold when he stood down as CEO for all the reasons you point out above. As I recall, he was successful and made money from Wiggle.

Good luck.

MTIOC