02 March 2022

By Maynard Paton

Results summary for System1 (SYS1):

- An acceptable H1 performance, albeit with profit lower than I had anticipated due to greater costs associated with the transition to Data services.

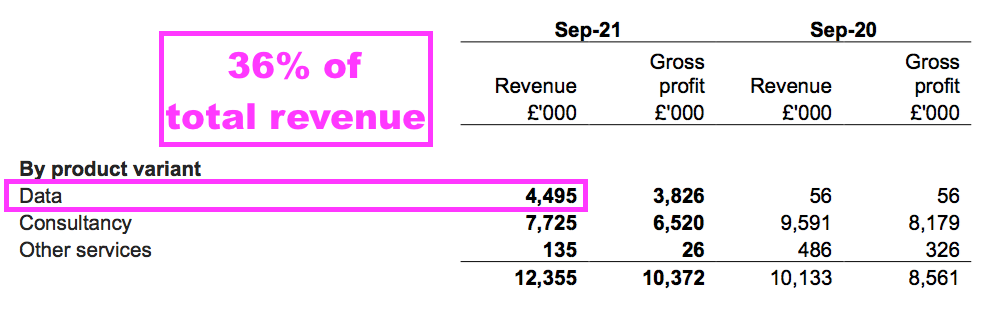

- Data services continue to advance, representing 36% of total revenue for H1 and reaching 43% for the subsequent Q3.

- UK revenue jumping 33% in part through an influx of new Data clients suggests the partnership with ITV is working.

- A Q4 sales warning relating to old-style Consultancy activities emphasised management’s upbeat ambitions are susceptible to mishaps.

- Net cash now represents 25% of the market cap, with long-term multi-bagger upside still obtainable if LTIP revenue targets are met and healthy ‘platform’ margins are delivered. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own SYS1

- Results summary

- Revenue and profit

- Data versus Consultancy

- Communications and UK revenue

- Revenue per employee

- Look out.

- Financials

- February 2022 trading updates

- Valuation

News links, share data and disclosure

News: Interim results and presentation for the six months to 30 September 2021 published 30 November 2021, directorate change announced 04 January 2022, share buyback programme announced 07 January 2022, trading update published 09 February 2022 and trading update published 22 February 2022

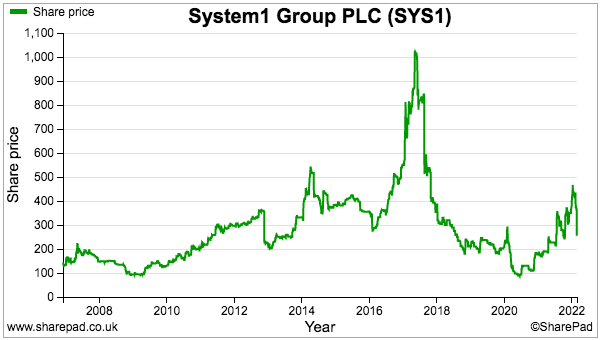

Price: 270p

Shares in issue: 12,767,802

Market capitalisation: £34.5m

Disclosure: Maynard owns shares in System1. This blog post contains SharePad affiliate links.

Why I own SYS1

- Advertising data specialist wishing to become the “world’s marketing decision-making platform” by serving “world-beating prediction and improvement methodologies” for television adverts.

- Boasts founder/entrepreneurial executive leader who has overseen acquisition-free growth, retains a 22%/£8m shareholding and has declared five special dividends.

- Transition from bespoke consultancy work towards ‘scalable’ data products, partnerships with ITV and LinkedIn plus bold management ambitions lead to tantalising multi-bagger possibilities.

Further reading: My SYS1 Buy report | All my SYS1 posts | SYS1 website

Results summary

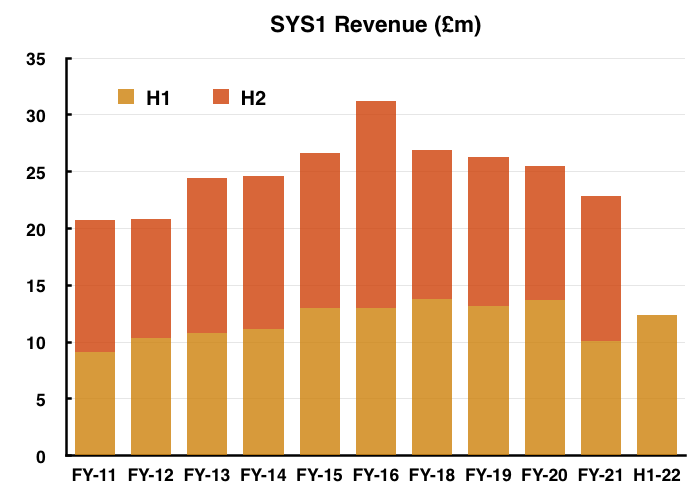

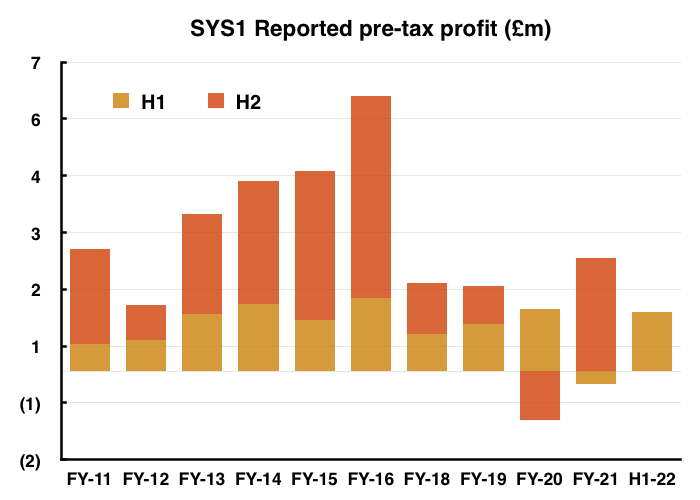

Revenue and profit

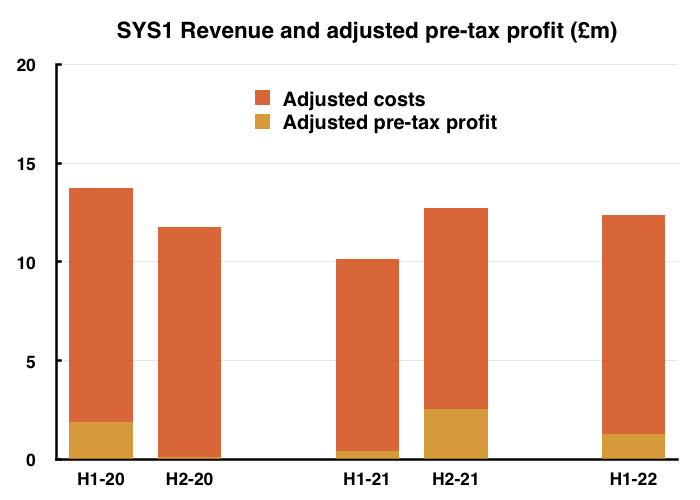

- An update during October had already signalled this acceptable H1 performance.

- H1 revenue did indeed increase by 22%, to £12.4m, while H1 adjusted pre-tax profit did indeed more than triple to £1.3m.

- But the £1.3m H1 adjusted profit was lower than the preceding £2.5m H2 adjusted profit, and also below what I had anticipated after the preceding FY 2021 results:

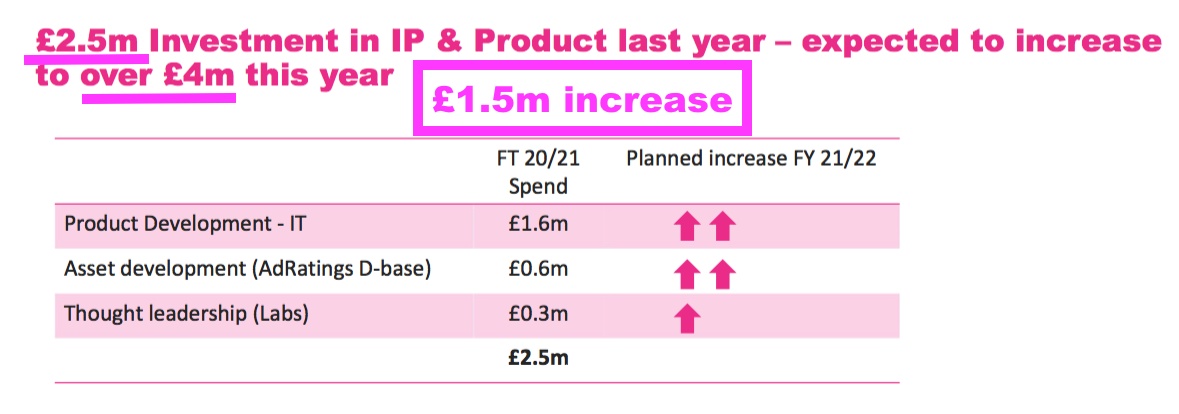

- The FY 2021 statement showed adjusted operating costs of £16.2m and indicated an increase to those adjusted costs of at least £1.5m for FY 2022:

- I had (optimistically) hoped FY 2022 adjusted operating costs would increase by the minimum £1.5m to £17.7m.

- But this H1 statement disclosed adjusted operating costs of £9.1m, which annualised implies FY 2022 adjusted operating costs will be £18.2m.

- SYS1 reiterated what the adjustments cover:

“Adjusted Operating Costs exclude impairment, interest, share based payments, bonuses, severance costs, and government support related to the Covid pandemic. Adjusted figures exclude items, positive and negative, that impede easy understanding of underlying performance.“

- SYS1 did not provide a formal reconciliation between statutory H1 profit and adjusted H1 profit, which is bad form and did not really support an “easy understanding of underlying performance“.

- The adjustments for this H1 were simply cited in the text, and were a £0.2m reversal of an earlier lease write-down and a £0.2m legal charge relating to a trademark dispute.

- SYS1’s results from FY 2018 onwards have not offered an “easy understanding of underlying performance” due to the business:

- Spending a hefty £5m to develop the AdRatings database;

- Transitioning from providing consultancy work to supplying data services, and;

- Experiencing weaker sales during the pandemic.

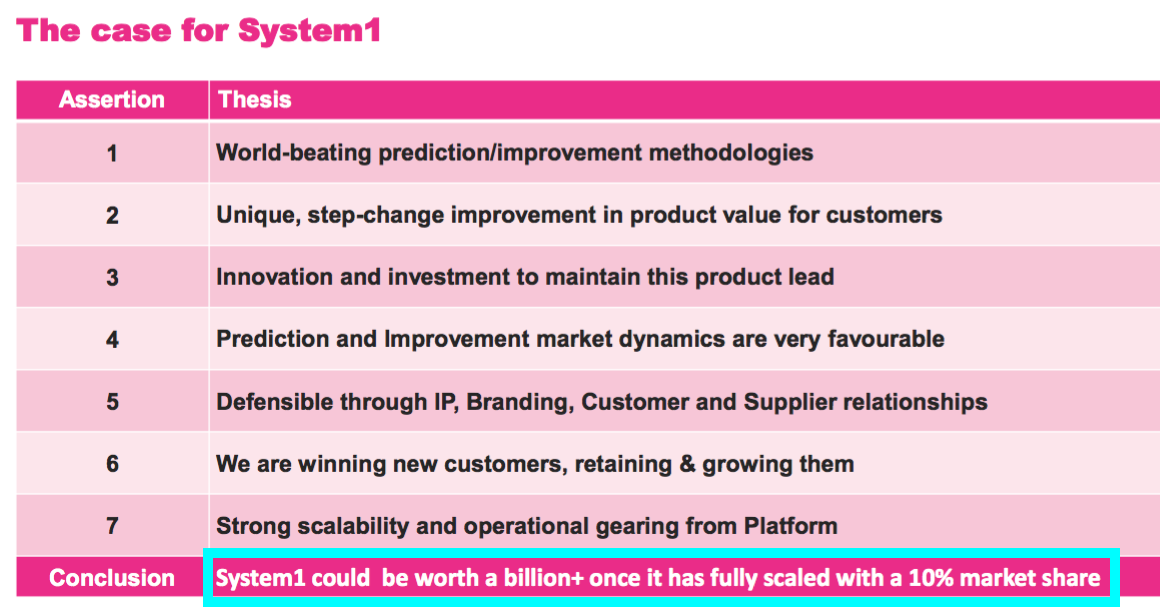

- At least SYS1 reiterated the very bullish management commentary from the preceding FY 2021 results. Bold projections had included:

1) Increasing market share from less than 1% to 10% during the next decade:

“Currently at less than 1% share, we believe that System1 can gain 10% global market share in the next decade — a lower share than the current market leaders“.

2) Setting a medium-term revenue milestone of £100m-plus (versus £22.8m for FY 2021):

“We take every decision with our medium term £100m+ Revenue milestone in mind.“

3) Stating the market cap could eventually become £1 billion (versus £40m now):

“We believe that System1 could be worth £1 billion eventually.”

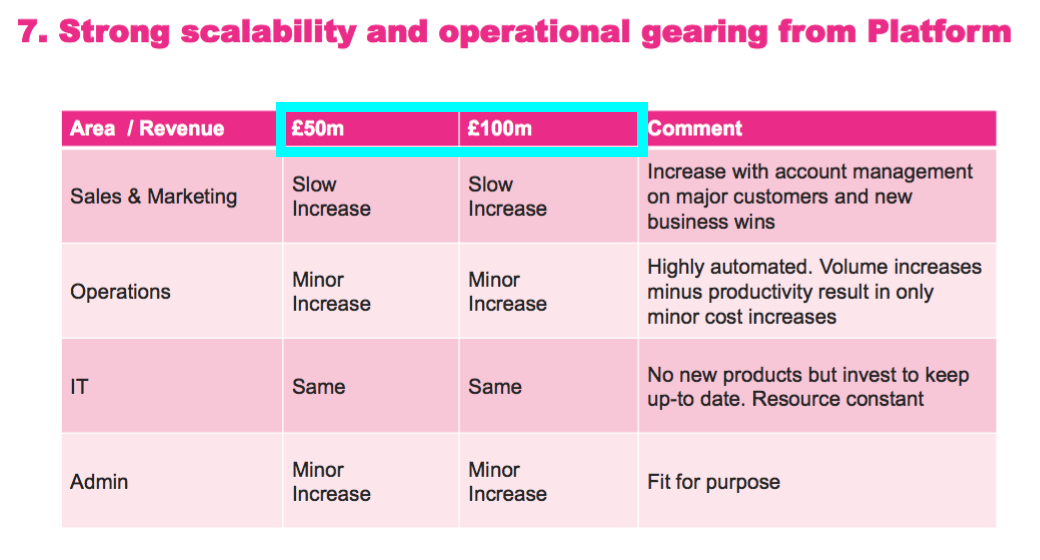

- The H1 presentation slides repeated those ambitions:

- The H1 text also revealed a new company description. “Advertising effectiveness agency” has now been replaced by “marketing decision-making platform“:

“Our mission is to be the world’s marketing decision-making platform“

- The H1 text contained terms such as “global winner“, “world-beating“, “unique“, “step-change“, “protected through IP” and “market dynamics are favourable” to support the investment case.

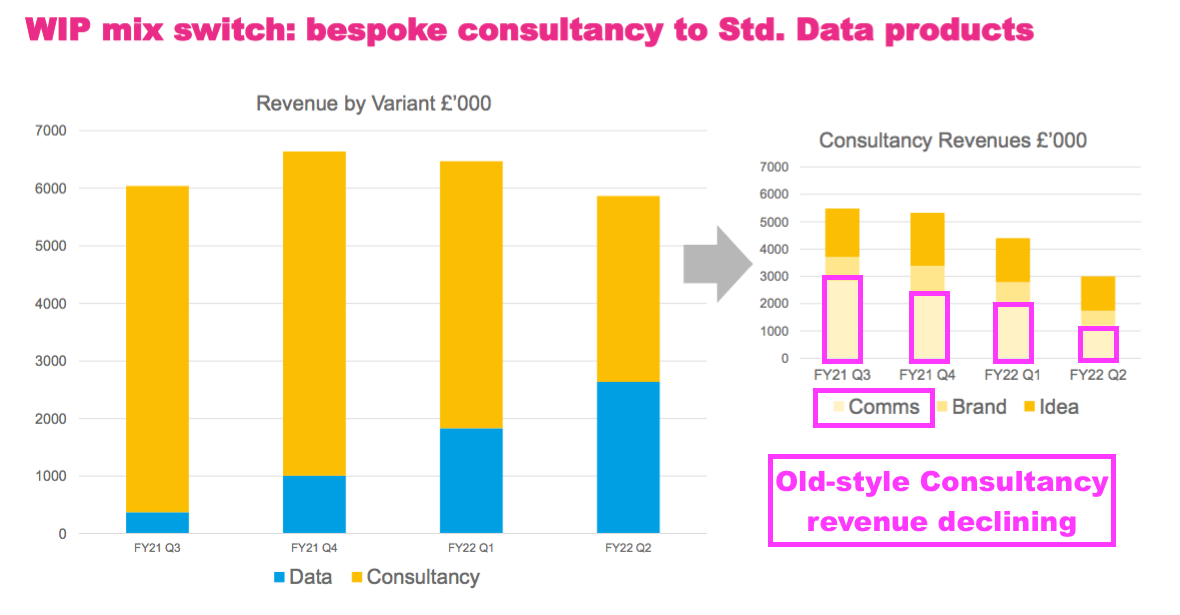

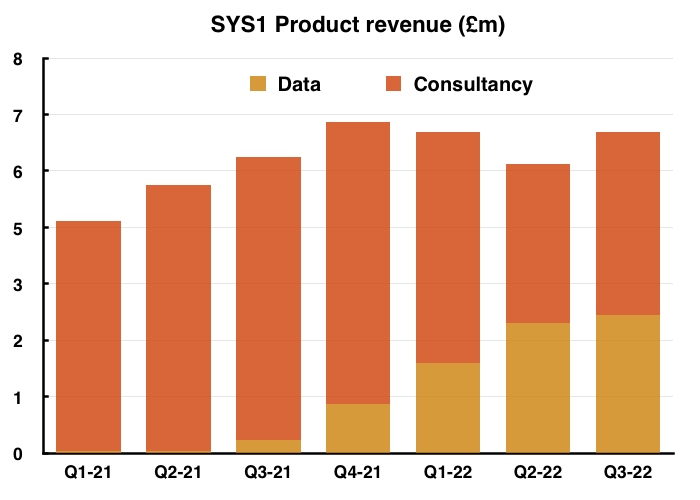

Data versus Consultancy

- The use of “marketing decision-making platform” reflects SYS1’s ongoing transition from supplying bespoke consultancy work to providing automated data services.

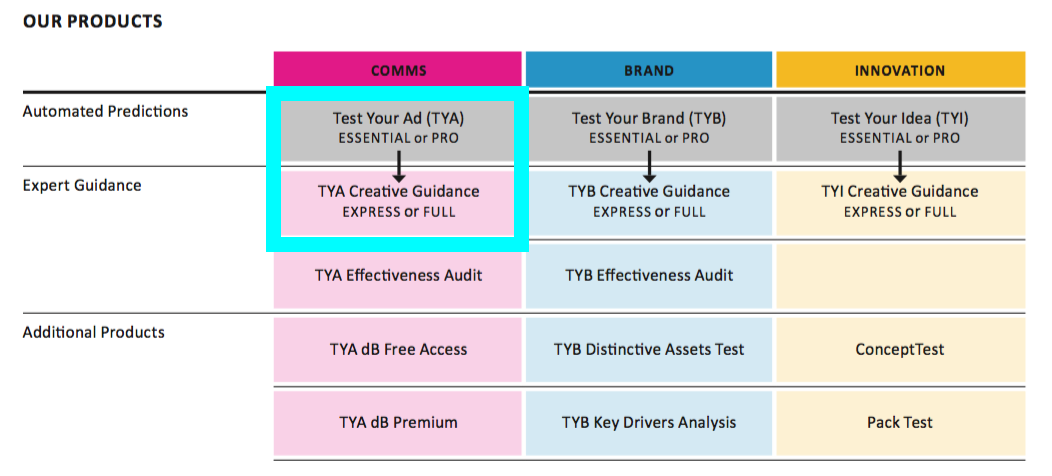

- Data products include Test Your Ad…

- …which allows clients to upload their television adverts to SYS1’s ‘platform’ and receive a report based upon the verdict of an online panel (example pdf here):

- Data revenue is also supported by Test Your Brand and Test Your Idea, which perform the same online-panel function for a company’s brand and marketing idea:

- SYS1 was pleased with the rate of transition to Data services:

“We have been delighted by the continuing adoption by both new and existing customers of System1’s repeatable, fast-turnaround and scalable data products as they displace the historic large bespoke consultancy projects that dominated the Group’s activity until H2 last year.“

- An update during August had expected Data products to “likely represent” a third of H1 revenue.

- This H1 statement in fact revealed Data revenue at 36% of total H1 revenue:

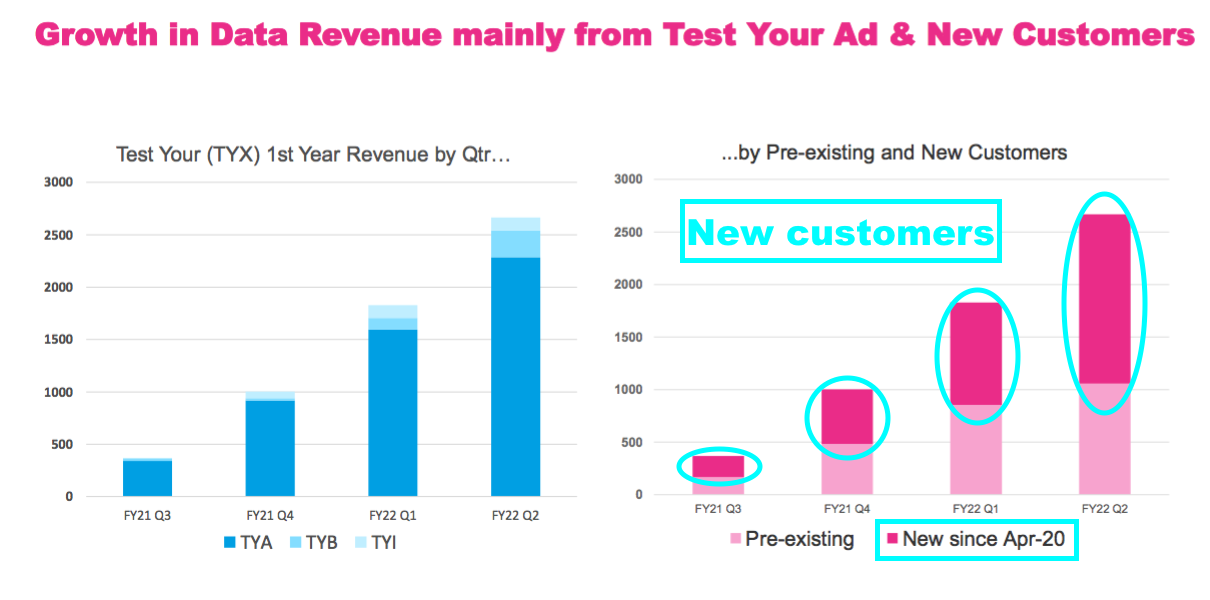

- The presentation slides provided useful progress charts:

- Launched during Q3 2021, Test Your Ad is the predominant Data service and, through partnerships with ITV and more recently LinkedIn, has led to an influx of new customers to SYS1.

- The reduction to the old-style bespoke Consultancy revenue relates to the Test Your Ad growth:

- A follow-on to the Test Your Ad service is Creative Guidance, which provides insights as to how the advert could be enhanced through “data-enabled, rapid-turnaround… assignments“:

- The H1 presentation revealed old-style Consultancy revenue for advert testing (within ‘Comms’) had halved during the last twelve months, as clients switched to the cheaper Creative Guidance service:

- SYS1 acknowledged that further switching from bespoke consultancy to Creative Guidance consultancy would occur as the shift to Data services continued:

“The rapid adoption of our automated data products by existing and new customers in the first half of the year augurs well for the future of our platform strategy and is expected to be partially offset in the near term by the continuing reduction in our legacy bespoke consultancy assignments that previously formed the core of our historic BrainJuicer business.“

- SYS1 will in future commendably disclose old-style and new-style consultancy revenue separately:

“In future reporting periods we will report the revenue from standard consultancy separately from the complex bespoke projects.”

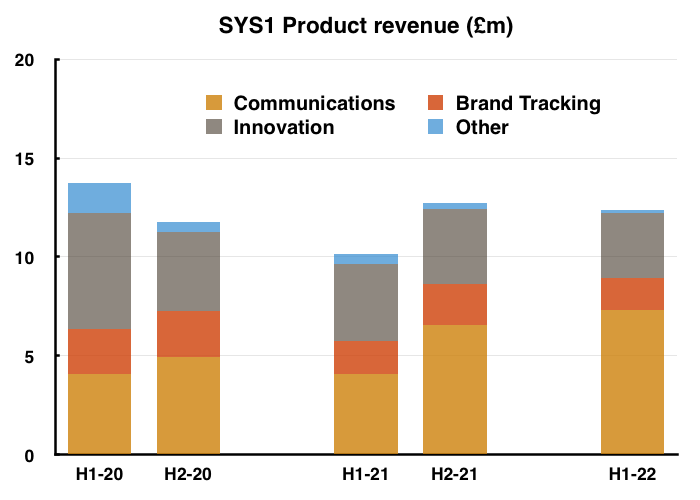

Communications and UK revenue

- The preceding FY 2021 statement had hinted SYS1’s past reporting of product “area” — defined as Communications, Brand and Innovation — may not be continued:

“[W]e now segment our revenue primarily by product variant rather than product area (Comms, Brand, Innovation)”

- But revenue (for now) continues to be reported by Communications, Brand and Innovation.

- Emphasising the growing demand for Test Your Ad, SYS1’s Communications revenue (which covers all advert-testing services) recorded its best-ever six-month level of £7.3m:

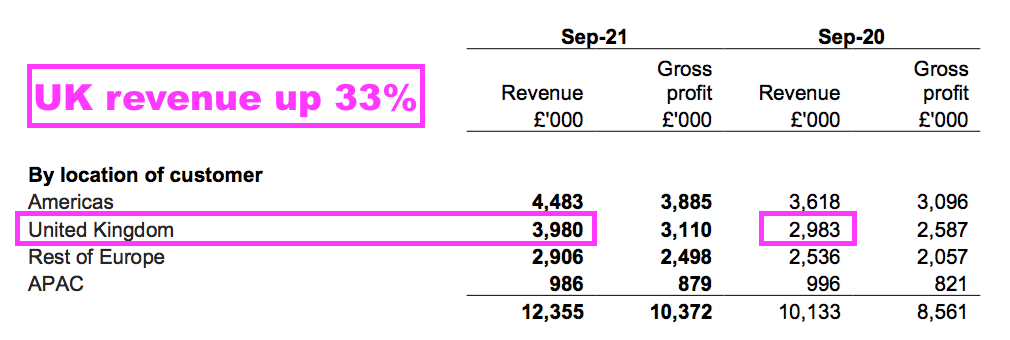

- Also of note was a strong UK performance:

- The UK has outpaced SYS1’s overseas divisions ever since the company announced a tie-up with ITV at the start of 2020.

- The ITV partnership was prompted by the broadcaster’s new desire to show more engaging adverts, and the agreement appeared to validate the philosophy, data and conclusions of SYS1’s advert testing.

- The preceding FY 2021 results had said ITV was “promoting and recommending” SYS1’s Test Your Ad service, in part through a Euro 2020 advert competition.

- Perhaps emphasising the ITV impact during this H1:

- H1 UK revenue climbed 33% versus non-UK revenue gaining 17%;

- H1 UK revenue represented 32% of total H1 revenue — the highest proportion since FY 2015, and;

- H1 UK revenue of £4.0m was the best six-month UK performance since H2 2016.

- This H1 statement mentioned ITV only very briefly:

“Our commercial strategy is also working well. Partnerships with broadcasters and platform owners including LinkedIn and ITV are bearing fruit, bringing our decision-making platform to a wider international customer base.“

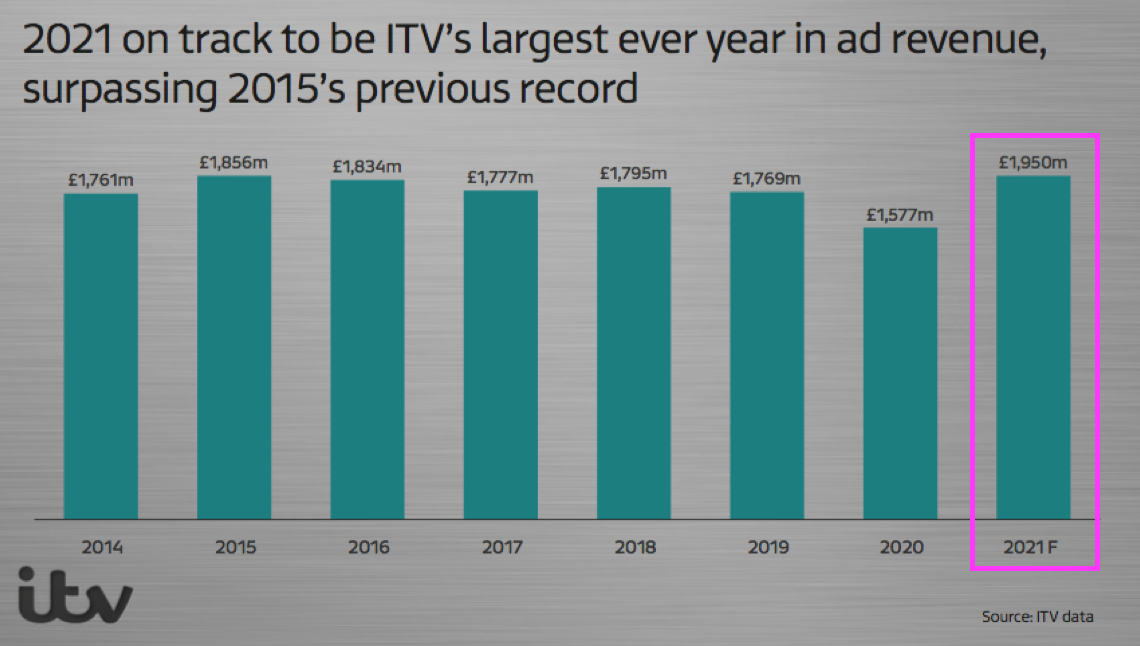

- ITV is already preparing for this year’s World Cup, although a follow-up ad competition with SYS1 has not been mentioned.

- No mention either of SYS1 within ITV’s 2021 investor presentations.

- But a November ITV presentation did reveal the broadcaster’s advert revenue was set to reach an all-time high:

- SYS1’s H1 text hinted that partnerships extended beyond ITV and LinkedIn…

“Our commercial strategy is also working well. Partnerships with broadcasters and platform owners including LinkedIn and ITV are bearing fruit, bringing our decision-making platform to a wider international customer base.“

- …and a recent SYS1 job advert refers to “Globo in Brazil and ThinkTV in Canada“:

Revenue per employee

- The aforementioned increase to adjusted operating costs reflected extra employees:

“Adjusted Operating Costs increased by 10% compared with H1 2020/21, broadly in line with the year-on-year growth in average employee numbers (H1 2021/22: 146; H1 2020/21: 128). Growth in employee numbers resulted from investment in sales and marketing (headcount +37%) and IT (headcount +27%) to accelerate the development of our automated data products and their commercialisation through partnerships and platform.“

- To date the extra employees have not improved SYS1’s workforce ‘productivity’.

- Revenue per employee for this H1 was £169k, below the £170k reported for FY 2021 (point 11) and below the £178k average for the five years to FY 2020:

- When additional income from Data services more than offsets declining sales from the old-style Consultancy work, revenue per employee should advance well beyond that historical £178k average as the ‘scalable’ nature of SYS1’s new ‘platform’ emerges.

Look out.

- The H1 text referred to a new book by Orlando Wood, SYS1’s chief innovation officer:

“Earlier this month we launched our Chief Innovation Officer Orlando Wood’s latest book on advertising effectiveness, Look out., which was published by the Institute of Practitioners in Advertising.

Look out. argues that to create effective and memorable advertising that builds brands, the advertising industry must capture the ‘broad-beam’ attention of audiences; to achieve this the industry must shift its attentional plane — it must look out.

The new book explains the behavioural science that underpins the methodology behind Test Your Ad and has been hailed by CMOs and advertising industry leaders.“

- Mr Wood spoke to SYS1’s chief marketing officer about the book during this November webinar:

- If the webinar is anything to go by, the book requires some deep System 2-type thinking. Lots of parallels were drawn between early 16th century paintings and modern advertising:

- Mr Wood’s previous books and films were not exactly the riveting works that harnessed the true System 1 way of thinking (i.e. automatic, intuitive and emotional).

- But at least his latest publication has been “hailed by CMOs and advertising industry leaders“. SYS1 commendably provides a downloadable ‘glimpse’ pdf of the book.

- I note SYS1’s results presentation gave a passing reference to the new book…

- …but dedicated a full slide to a testimonial from marketing expert Mark Ritson:

- I maintain SYS1 should employ a Mark Ritson-type presenter to showcase the group’s research in a more System 1-type manner:

Financials

- SYS1’s primary accounting attraction remains the cash-flush balance sheet.

- The cash position improved by £1.0m during the half to £10.0m.

- Bank debt of £2.5m matched that of six months ago.

- H1 net cash was therefore £7.5m.

- The £1.0m cash inflow included a £0.4m tax receipt following a successful £0.5m R&D tax-credit claim. The tax credit received during this H1 related to FY 2020 and a claim has been submitted for FY 2021 (point 12).

- A further £0.4m was absorbed into working capital during the half. SYS1 generally pays its suppliers (e.g. online panel organisers) faster than payments are collected from customers (point 8).

- I am hopeful the transition towards high-volume, low-price Data services and away from low-volume, high-price Consultancy work can lead to a more favourable working-capital profile.

- The aforementioned extra employees reduced SYS1’s adjusted pre-tax margin to 11% from the 20% reported for the preceding H2.

- The share buyback mooted within the FY 2021 results was confirmed during January.

- Buyback details include:

- Up to £0.75m will be spent repurchasing shares until the 31 March 2022 year-end;

- To date £430k has been spent buying shares at an average 358p, and;

- Repurchased shares will be used to satisfy LTIP obligations.

- SYS1 said initially during February 2020 the buyback programme would cost up to £1.5m.

- SYS1 will “formally review the effectiveness” of the buyback programme after the 31 March 2022 year-end.

February 2022 trading updates

- SYS1 issued two trading updates last month.

- The first update revealed further progress with Data services during Q3:

“Revenue in Q3 rose 8% on the comparable period last year to £6.5m, and Data products represented 43% of the quarter’s revenue.

Year-to-date revenue to the end of Q3 was 17% higher than the prior year at £18.9m, and Data revenue represented 39% of the year-to-date total (H1: 36%).

Period-end cash, net of borrowings, was £8.1m, compared with £6.5m at end-March 2021.

Profitability was in line with management’s expectations and reflected an increase in expenditure on people and platform as highlighted in the interim results announcement.”

- I calculate Data revenue for Q3 was £2.8m versus £2.6m for Q2 and £1.8m for Q1:

- I also calculate the Q3 cash inflow was £0.6m, which appeared better than the aforementioned £1.0m H1 inflow that was bolstered by the £0.4m tax receipt (see Financials).

- Two weeks later, the second update disclosed:

“Despite substantial progress in the development of new revenue streams from automated prediction products (Data) since their introduction in 2020, and satisfactory performance in the first 9 months of the current financial year, total revenues in the final quarter ending 31 March 2022 are now expected to be over £1m short of management’s previous expectations. This is due to a sudden and unanticipated reduction in the forecast for bespoke consultancy project sales in the US.

Management is taking rapid action to address the consultancy sales performance in the US. As a consequence of the lower consultancy revenues, we now expect profit before tax for the final quarter and the year as a whole to be about £1m below the current market expectations.

The Company is now well into its transition from a marketing agency to a decision-making platform. Automated Data products in the US region, and overall, continue to perform well, attracting over 200 new customers since launching in 2020. In the nine months to 31 December 2021, 39% of revenue came from Data and 60% of that revenue originated from those new customers.

Cash net of borrowings remained strong at the end of January at £9m, compared with £6.5m at end-March 2021.

- SYS1 admitted the old-style Consultancy revenue had fallen at least £1m short of expectations for Q4.

- Previous SYS1 profit warnings implied the old-style Consultancy work had little revenue predictability:

January 2018: “Q3 trading continued to be worse than anticipated and, subject to its normal lack of revenue visibility, the Company now anticipates Gross Profit for the year to 31 March 2018 will be around 20% less than the prior year.“

August 2017: “The slower than expected start to our financial year which we noted at the time of the announcement of our 2016/17 results on 15 June 2017 has continued since then… This is mainly due to non-recurrence of large one-off Innovation projects as a result of some significant client spending deferrals and a more competitive market, although there have been some more encouraging signs recently.“

March 2013: “Every year, some clients spend unused budget in November and December, but in 2012 many big companies decided instead to cut back, and this had a material effect on our profits. As a result, we reduced costs and we’ll be less reliant on clients releasing spare budgets at the end of the year going forward.“

- The shift to Data services ought to limit future Consultancy upsets, but in retrospect a Consultancy mishap was always a danger.

- At least the annual-report small-print (point 6) claimed…

“the Group is a lot more confident about how to respond to an abrupt negative situation”

- …and maybe the sudden profit warning reflected a “team behaviour” (point 1):

“Truth — always tell the truth… and tell it early“

- Assuming SYS1 was expecting Data and Consultancy revenue for Q4 to match that of Q3, then a £1m Consultancy revenue shortfall could look like this:

- Assuming also that gross margins and adjusted operating costs for H2 match those witnessed during H1, Q3 and Q4 adjusted profit may look like this:

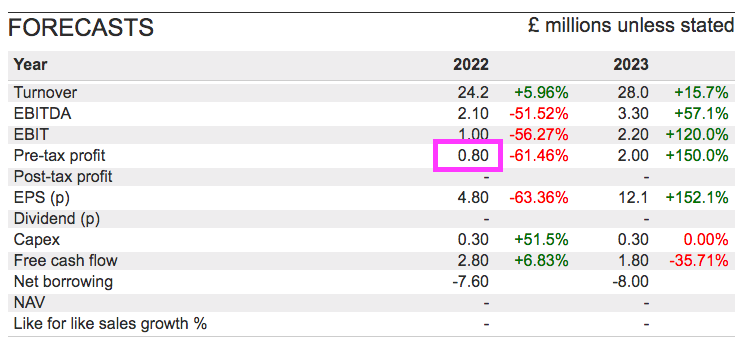

- My profit calculations are more optimistic than the broker forecast shown in SharePad:

- The SharePad forecast of a £0.8m pre-tax profit for FY 2022 implies a H2 pre-tax loss of £0.5m.

- The second trading update also disclosed:

- Net cash of £9m, which represents 25% of the market cap and implied January witnessed a remarkable cash inflow of £0.9m, and;

- 60% of Q123 Data revenue was generated by new customers, which my rough sums translate into Q3 Data revenue from new customers of £1.75m versus £1.6m for Q2 and £1.0m for Q1.

- The second trading update followed this management change during January:

“System1 Group plc (AIM: SYS1) today announces that, as planned, Stefan Barden will step down as CEO and from the board of directors on 31 January and revert to his previous role as an adviser to the board of directors on strategy and technology. System1’s founder, John Kearon, will return to the CEO role.”

- The wording “as planned, Stefan Barden will step down as CEO” contradicted the statement from March 2021 that announced Mr Barden’s as chief executive:

“System1 Group plc, the advertising effectiveness agency, (AIM: SYS1) announces that, in line with the continued evolution of the Company, John Kearon, previously Chief Executive Officer, has today assumed the title of ‘Founder and Executive President’ and Stefan Barden, previously Chief Operating Officer, the title of ‘Chief Executive Officer’.

Stefan will remain an executive director rather than reverting to the purely advisory role indicated last year.“

- Although when Mr Barden was first appointed to the board as chief operating officer during June 2020, he was expected to return to an advisory role:

System1 Group plc (AIM: SYS1) today announces that it has appointed Stefan Barden to the board of directors of the Company as an executive director with immediate effect. From November 2018, Stefan has been an adviser to the board of directors on strategy and technology, and has recently taken on the executive role of chief operating officer to assist the Company through its next phase of development. He will return to the advisory role when this is complete, expected to be in around a year.“

- Mr Barden has led the ‘hands-on’ implementation of Data services, and I had interpreted his return to the advisory role as positive:

“Not sure what to make of this. Mr Barden was set to have a year-long stint as a board exec, then became CEO and a permanent executive, but now has decided to return to the advisory role. I get the impression Mr Barden was required to push through some tough changes, so had been appointed a board exec.

I suppose the bull case from this latest RNS is the hard transitional work has now been completed and, nine months after saying Mr Barden would remain an exec, the company has transitioned so well that actually Mr Barden can return to being an advisor.”

- Perhaps the Consultancy shortfall shows Mr Barden should have stayed on as an executive for a little longer.

Valuation

- Doubling up the H1 adjusted performance and applying 19% standard UK tax gives earnings of £2.1m.

- A market cap of £35m less the £9m net cash position gives an enterprise value of £26m, which is 12-13 times that £2.1m earnings extrapolation.

- But the Q4 profit setback raises questions about the future of SYS1’s old-style Consultancy work.

- Will such Consultancy revenue bounce back? Or is Consultancy revenue now withering as SYS1 focuses on Data services?

- I get the impression Consultancy might be withering. After all, that earlier presentation slide did show old-style Consultancy revenue within the ‘Comms’ segment halving as clients shifted to the cheaper Creative Guidance service (see Communications and UK revenue).

- Perhaps SYS1 may now accelerate the transition to Data as Consultancy efforts are wound down.

- The longer-term investment case remains based on the transition to Data — and Consultancy profits were never likely to support SYS1’s market-share ambitions (from sub-1% to 10%) and talk of that £1 billion market-cap.

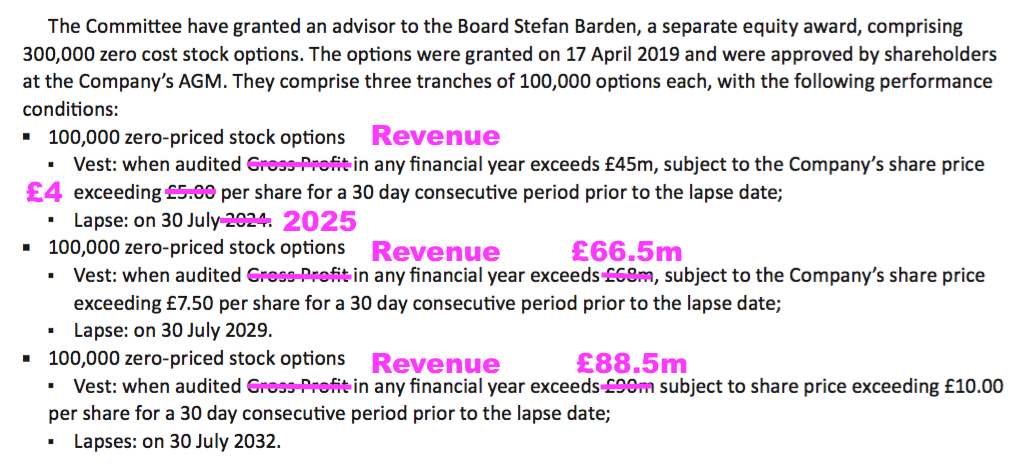

- SYS1’s (contentious) LTIP scheme may indicate what the board thinks is financially possible:

- The lowest revenue target of £45m compares to my best guess of £24m for FY 2022. Data revenue is presently running at an annualised £11m.

- Assume revenue does reach £45m and SYS1’s ‘platform’ ambition translates into a 20% operating margin, then earnings could be close to £7m after 25% tax (from FY23).

- Earnings close to £7m could make the £35m market cap very cheap regardless of the £9m net cash position.

- Mind you, SYS1’s current LTIP scheme was first introduced during 2017, was extended during 2019 and then (contentiously) changed during 2021. Option targets are therefore not guaranteed to be met in a timely fashion.

- The intriguing investment prospect of course remains SYS1’s talk of advancing its market share from less than 1% to 10%, and that growth then supporting a possible £1 billion market cap.

- But whether such upbeat projections are truly realistic or just plain reckless is impossible to determine right now.

- I am guessing the long-term investment outcome will be somewhere in between truly realistic and plain reckless.

- After all, the clear business strategy, the product validation from ITV alongside the rapid take-up of Data services all provide optimism…

- …but the Q4 Consultancy warning underlines management’s ambitions being susceptible to setbacks.

Maynard Paton

System1 (SYS1)

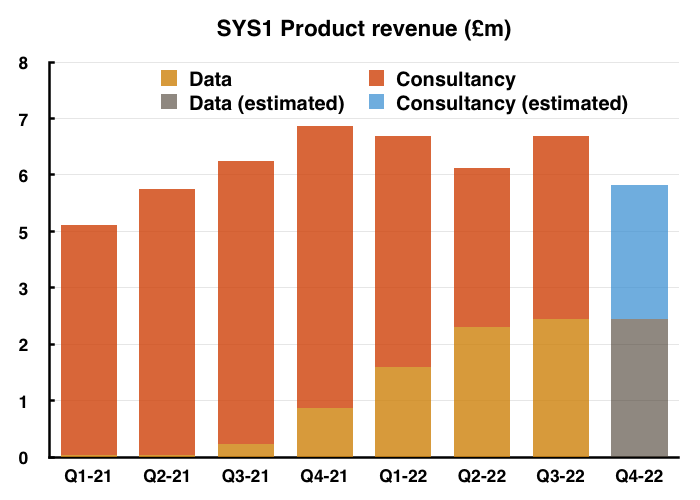

Trading update published 27 April 2022

A mixed update that did not quite match my expectations following February’s trading statement. In particular, Data revenue dropping from £2.8m for Q3 to £2.4m for Q4 was not ideal given SYS1’s transition is dependent on Data revenue expanding.

A small H2 loss was also signalled, although cash generation during H1 appeared sound. Management meanwhile seems upbeat and is even hosting a presentation.

Here is the full text interspersed with my comments:

——————————————————————————————————————

Revenue for the year rose by 6% to £24.1m (H1: +22%, H2: -8%). Data Revenue increased by £8.4m year on year to £9.7m (H2: £5.3m), representing 40% of the total (H2: 45%). As indicated in the interim statement and the February trading updates, adjusted operating expenditure, principally employee-related costs, rose 18% year on year (H2: 26%) reflecting the planned investment in people, partnerships and platform.

——————————————————————————————————————

Full-year revenue at £24.1m matches my £24m projection in the blog post above.

Full-year Data revenue was stated as £9.7m with H2 Data revenue stated as £5.3m. But the H1 figures showed Data revenue of £4.5m, so H2 Data may be £9.7m less £4.5m = £5.2m or £0.1m lower than stated. I suspect a rounding error explains the difference.

Q3 Data revenue was 43% of £6.5m = £2.8m, which means Q4 Data revenue was £5.2m (my H2 total) less £2.8m = £2.4m.

Quarterly Data revenue had previously grown from £1.0m to £1.4m to £1.8m to £2.7m to £2.8m, so a drop to £2.4m is not ideal. I am not sure whether this Q4 drop is due to the weak Q4 consultancy performance (as per the February trading statement) or other factors.

I calculate Q4 consultancy revenue to be £2.8m, versus £3.7m for Q3, £3.2m for Q2 and £4.7m for Q1.

——————————————————————————————————————

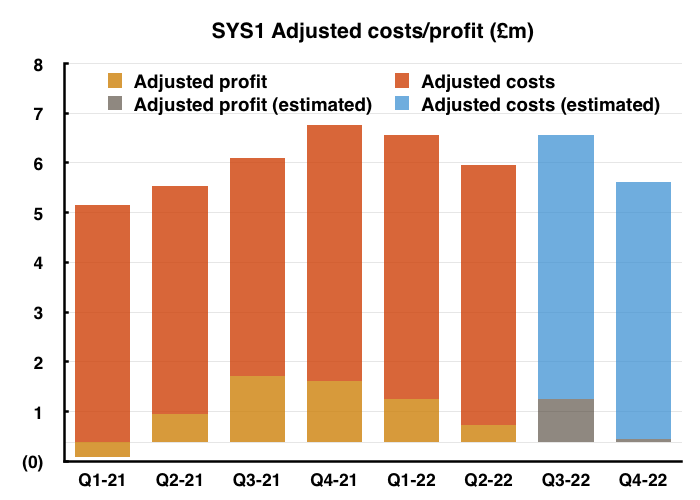

Profitability was stronger in H1 than H2 as the planned increase in H2 operating costs coincided with a reduction in revenue during the final quarter. We expect to report an adjusted profit before taxation (which excludes impairment, share-based payments, government support, bonuses, loan interest and certain provisions) of some £1.1m for the full year (FY21: £3.0m). Statutory profit before taxation is expected to be ca £0.8m, £1.1m before share-based payments. (FY21: £2.1m, £2.2m).

The business continued to generate cash, ending the period with £8.7m cash net of borrowing versus £6.5m at the previous year end. During the final quarter of the year the Company spent £0.6m repurchasing 158,674 ordinary shares. No dividends were declared or paid during the financial year.

——————————————————————————————————————

A full-year adjusted profit before tax of £1.1m compares to £1.3m reported for H1, so a £0.2m loss for H2. I had been expecting a profit for H2 in my blog post above, although the broker forecasts I referred to in my blog expected a £0.5m H2 loss.

Net cash of £8.7m compares with £8.1m at the end of Q3 and £7.5m at the end of H1. So adjusted for the £0.6m buyback (conducted entirely during Q4), H2 saw a cash inflow of (£8.7m+£0.6m-£7.5m) = £1.8m and Q4 saw a cash inflow of (£8.7m+£0.6m-£8.1m) = £1.2m.

No doubt July’s full-year results will explain how a £0.2m H2 pre-tax loss translated into extra H2 cash of £1.8m. Part of the difference relates to share-based payments, which were £17k during H1 but seemingly £0.3m for H2. Tax credits could also be involved.

——————————————————————————————————————

OUTLOOK

System1 remains focused on achieving revenue growth over the short and medium term. Having stepped up our investment in people, partnerships and platform to develop and commercialise our automated marketing predictions last year, we are convinced that it is right to keep those resources and infrastructure in place despite the fall off in revenue performance in the last quarter.

We intend to grow revenue and profits in the course of the new financial year and anticipate that the growth will be weighted to the second half of the year as expenditure flattens versus last year. The launch of Test Your Idea and further development of our commercial partnerships are expected to promote revenue growth, particularly in the second half of the financial year.

System1 Founder and CEO John Kearon said:

“System1 has rapidly addressed the issues that led to the reduction in sales last quarter by injecting fresh talent in the USA and unifying our sales and marketing activities under the chief growth officer. The executive leadership group is focused on delighting customers with the speed of our decision-making platform and the clarity of our creative guidance.”

——————————————————————————————————————

An upbeat narrative — as you might expect from a management team that has mentioned a potential £1 billion market cap! Although progress for the forthcoming H1 is not expected to be spectacular.

The notable text is “expenditure flattens versus last year“, which I trust signals the emergence of higher profits — and the ‘scalability’ of SYS1’s Data services — as revenue grows while costs can be kept steady.

——————————————————————————————————————

CAPITAL MARKETS DAY

System1 will be holding a Capital Markets Day for investors and analysts at 14:00 BST today. This virtual event will be an opportunity for to learn more about the Company’s operating model, prediction methodologies and growth strategy.

Speakers will include John Kearon (CEO), Chris Willford (CFO), Jon Evans (Chief Growth Officer) and James Gregory (COO).

The Capital Markets Day is expected to last from 14:00 – 15:30 BST. To register for the event, please email investorrelations at system1group dot com .

A copy of the presentation materials and a video replay will be available on the Company’s website.

Other than as set out in today’s announcement, no new material information regarding current trading will be disclosed at the Capital Markets Day.

——————————————————————————————————————

I can’t recall SYS1 ever hosting a CMD before, or at least one open to the wider investing public. Management presumably has a positive story to tell. I have registered to attend.

Maynard

hi Maynard

I’ve just watched a recording of the Capital Markets Day.

I found the demonstration of the data platform useful in enabling me to better understand how it all works so from that perspective it was useful.

It was the first time I had seen John Kearon in action. He initially came across as a bit of a mad professor with the start of the presentation being quite amateurish. Fortunately it improved with the other presenters, in particular with Jon Evans (Chief Growth Officer) who came across very well.

What did you make of the CMD? I thought the combined response to the question you submitted rather muddled and unsatisfactory.

Kind regards

Peter

Hi Peter

Thanks for the comment. CMD recording is here: https://vimeo.com/704128612

‘Mad professor’ is a good description :-) I have not re-watched the CMD, but I did not find the answers unsatisfactory at the time. The stumbling block for years has been SYS1 not getting the attention of CMOs, and instead facing resistance from CMO underlings. But I think JK said SYS1 is now getting that attention and claimed SYS1 is the only marketing research business to have such CMO audiences. I went to a SYS1 industry event the other month and spoke to Adam Zavalis, marketing director at Aldi UK, and he said Aldi was putting more business SYS1’s way because the research turnaround was next day versus a few weeks for an existing supplier.

By the way, Jon Evans hosts a podcast called Uncensored CMO, which is worth a listen as he talks with other CMOs. The CMOs of Direct Line and Yorkshire Tea were guests a while ago. Interesting stuff! https://uncensoredcmo.com/

Maynard

Regarding your question and their response.

You asked 1) What % of the old consultancy users had moved to the new Data Platform and 2) What prevented those who didn’t move from making the move.

Their combined (eventual) response was that virtually everyone using Test Your Ad had stayed with them. I thought that Test Your Ad was only part of the new Data Platform and not related to the old consultancy users, in which case your question was misunderstood / incorrectly answered.

Or maybe it is me that misunderstood?

As for now engaging directly with CMO’s this is clearly the way to go and it will be interesting to see how new contract wins pick up as a result.

Peter

Hi Peter

Ah, ok, I had two questions answered. The other concerned the scalability of the follow-on creative-guidance service.

Test Your Ad is indeed part of the Data Platform, but the customers using Test Your Ad were previously old-style consultancy users. This slide…

…shows the elements in blue that are now automated that were all manual processes before (an earlier slide showed those blue processes in grey).

This next slide compares data sales from ‘pre-existing’ clients to new clients, and sales from pre-existing clients for FY22 being the same as FY21:

It looks as if the pre-existing clients that wanted to move to Test Your Ad have now done so, which ties up with what management said during the webinar, i.e. that most have moved to the new automated process.

There will be some users sticking with the old-style consultancy because they have bespoke needs beyond what the automated Test Your Ad can provide. I got the impression from the webinar these particular clients are large spenders and are few in number, which means old-style consultancy revenue could remain difficult to predict when some of these clients do not require any bespoke work (as per the Q4 sales warning).

Maynard

System1 (SYS1)

Distribution policy published 22 June 2022

Here is the full text interspersed with my comments:

——————————————————————————————————————

System1 Group plc (AIM: SYS1) today announces an update on its distribution policy to shareholders.

Prior to the outbreak of Covid in early 2020, System1 had a policy of paying dividends to shareholders, and dividends for the year ended 31 March 2019 totalled 7.5 pence per share (£0.9m).

In April 2020, in response to the outbreak of Covid-19 the Company suspended both a proposed buyback programme for £1.5m of System1 shares as well as a final dividend for the year ended 31 March 2020 after having paid a 1.1p interim dividend totalling £0.1m.

During the Covid period the Company maintained a strong balance sheet with significant levels of cash to enable the business to weather the impact of Covid on the business and to continue to invest as required. No dividends were paid for the year ended 31 March 2021.

During the first quarter of 2022, with Covid in the rear-view mirror, the Company spent £0.6m undertaking a share buyback programme and the net cash balance at end March 2022 was a healthy £8.7m.

——————————————————————————————————————

Useful background. On to the important bit…

——————————————————————————————————————

The Board has now conducted a wider review of its capital allocation priorities and considered the Company’s near-term cash needs and its dividend policy.

Following this review, and taking into consideration feedback from certain shareholders, the Board has decided to pay annual distributions to shareholders by way of on market share buyback or tender offer, rather than by way of a dividend.

The Board has concluded that the distribution policy will be progressive, taking into account underlying business performance. It is expected that the absolute level of distribution for the year end 31 March 2023 will be between 30 – 40% of through-the-cycle profit after tax.

The Board is comfortable that this policy will support continued investment in the business, provide funds for potential in-fill acquisitions to supplement organic growth and will deliver returns to shareholders.

——————————————————————————————————————

I suppose SYS1 considering returning more money to shareholders is encouraging as the decision signals the business is generating surplus cash. But buybacks and tender offers are not the same as cash dividends, and their effectiveness is determined by the price at which they are conducted. The £0.6m buyback conducted during Q1 at an average 348p has not yet shown to have created much value.

“Certain shareholders” does not mean “all shareholders” and I wonder if the shareholders that did provide feedback included chief exec John Kearon, who owns 22%. Using company money to buy back management’s shares seems to create a conflict of interest — the management selling could set the buy price!

For example, Best of the Best announced a tender offer at a 52% premium to the prevailing price — which when the management is selling its full allotment does not feel quite right.

True, “underlying business performance” and “through-the-cycle” profit provides lots of wiggle room to determine how much is returned, but nothing is ever certain with dividends as well.

“In-fill acquisitions” is interesting. SYS1 has not acquired anything before and I wonder if a particularly important supplier (a panel supplier perhaps?) could be purchased.

——————————————————————————————————————

In addition to the above distribution policy, reflecting the strong cash position of the Group, the Board has decided to undertake an additional return of capital.

The Board believes that a strong balance sheet and positive net cash are appropriate for the Company. At the same time, the Board considers that the Company has cash at levels above its through-the-cycle and near-term requirements and will therefore seek to return up to £1.5m of excess cash by way of a tender offer at the earliest opportunity after the Company has published its report and accounts for the year ended 31 March 2022 on 12 July.

Further information will be provided in due course.

——————————————————————————————————————

Note that the tender offer will be performed “at the earliest opportunity after the results. Typically the final dividend is approved at the AGM — but no such democracy is happening with the tender offer. Hopefully the tender price will make sense for the company. £1.5m equates to 11-12p per share, so the amount existing shareholders will be able to sell through the tender will be small given the 300p mid-price.

Maynard

Hi Maynard –

Thank you for doing so much analysis and thinking about System 1.

I had a look at the System 1 website and the video.

The product looks good.

But I wondered how significantly their online testing platform is different / better / cheaper than those offered by the big guys like Kantar and IPSOS and other competitors.

From a quick look, it seems their database contains many more TV ads and their predictability claim based on the relationship with the IPA is impressive.

When YouGov was growing rapidly in the early days of web based research I remember their product was better, faster and cheaper than the big guys. It was easy to give them business.

Do you feel the SYS1 product is significantly better than those of competitors?

Best, Tim

Hi Tim

SYS1’s FY 2021 presentation contained the slide below to outline the group’s ‘value proposition’:

One important differentiator is speed. The customer gets a basic report within 24 hours, whereas other suppliers take much longer. I went to a SYS1 industry presentation earlier this year and spoke briefly to Aldi UK’s marketing boss, and the first point he mentioned about SYS1 was the quick service and how that can help his team ‘react faster’. I suppose when you have ad slots already booked, you don’t want to discover you have a dud ad just before the ad is broadcast. John Kearon (CEO) did say at an AGM he wanted SYS1 to become the ‘YouGov of ad testing’. Ultimately the advertisers will decide whether SYS1 has a better product, but if there is belt-tightening within the industry then perhaps that may prompt a few advertisers to test through SYS1 rather than the costlier traditional alternatives.

Maynard

hi Maynard

Publication of the 2021/22 Annual Report seems to be delayed. The results were announced on 12th July, nearly 6 weeks ago. In the past 2 years the Annual Report has been produced within 7 days of the results announcement.

Perhaps the delay is connected to the £1.5m return of cash return to shareholders by way of tender offer, announced on 22nd June. Nothing more has been heard about this so maybe there are some complications?

Nothing sinister going on here I hope.

Peter

Hi Peter

Yes, I noticed the full-year results contained the abridged version of accounts as opposed to the full version as seen during previous years. Annual reports must now include extra disclosures, such as carbon emissions etc, and I wonder if SYS1 has been lacking in that department.

But yes, the £1.5m buyback/tender offer situation could be the delay, too, and is all a bit strange. The company initially proposed a tender offer during June, then at the results said a buyback would be undertaken and then what is left of the £1.5m after the buyback would fund the tender offer. The buyback has until 31 August to run, so possibly the tender offer ought to be announced soon after. I suspect the tender offer needs the annual report published before it can go ahead. I have heard on the grapevine the tender offer has been pushed by an external shareholder, who seemingly wants out of the company. I am not sure management is truly keen on the tender offer, so maybe there are indeed complications (probably about the tender price). I would prefer SYS1 retain the cash and only consider handbacks to shareholders when the new Data division has truly established itself.

Maynard

What to make of today’s announcement of a strategic review / cancellation of the tender offer and share buybacks / appointment of new NED?

I sense much internal disagreement behind the scenes and a high degree of CEO frustration (his desire to become a £1b company now seems rather distant). When I viewed the recent Capital Markets day I did comment that I felt the Founder / CEO John Keaton came across as a rather haphazard mad professor. Today’s announcement hints at a level of desperation and fumbling in the dark so perhaps only serves to re-inforce my initial view.

Clearly the new NED is being onboarded to drive the strategic review. He is described as an investor, entrepreneur and consultant with Law and Economics degrees and ‘……he also periodically advises companies on a wide range of commercial, financial and business matters…….’. There is no mention of any advertising industry experience so it’s hard to have a view on whether he is an appropriate appointment. Perhaps he has had previous business dealings / connections with the CEO?

I’ll wait to see the outcome of the strategic review (due by end of November) before forming an opinion but my initial impressions are not very positive.

Would welcome your views.

Kind regards

Peter