07 September 2021

By Maynard Paton

Results summary for System1 (SYS1):

- A better-than-expected H2 accompanied some bold management commentary that cited an eventual £1 billion market cap.

- The acceleration towards ‘scalable’ data products continues, with ‘disruptive’ pricing and partnerships with ITV and LinkedIn spearheading the transition.

- Downgraded option targets and upgraded director pay looked awkward given the optimistic narrative and receipt of government pandemic support.

- Greater net cash, a mooted share buyback and a 21% adjusted H2 margin suggest the accounts have recuperated from their pandemic nadir.

- Despite extra growth investment limiting near-term earnings progress, long-term multi-bagger upside may still be obtainable. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own SYS1

- Results summary

- Revenue, profit and management optimism

- Business strategy

- Test Your Ad

- ITV and LinkedIn

- A new book, dull films and Mark Ritson

- Financials

- Options and AGM voting

- Valuation

Event links, share data and disclosure

Events: Annual report for the twelve months to 31 March 2021 published 14 July 2021 and AGM statement published 13 August 2021

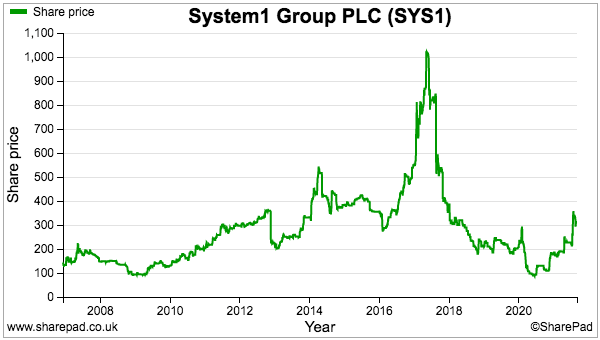

Price: 310p

Shares in issue: 12,898,296

Market capitalisation: £40.0m

Disclosure: Maynard owns shares in System1. This blog post contains SharePad affiliate links.

Why I own SYS1

- Advertising ‘effectiveness’ agency that predicts and improves the success of television adverts through the industry’s “most accurate, cheapest and quickest” data and guidance.

- Boasts founder/entrepreneurial executive leader who has overseen acquisition-free growth, retains a 23%/£9m shareholding and has declared five special dividends.

- Transition from consultancy work towards ‘scalable’ data products, partnerships with ITV and LinkedIn plus bold management ambitions lead to tantalising multi-bagger possibilities.

Further reading: My SYS1 Buy report | All my SYS1 posts | SYS1 website

Results summary

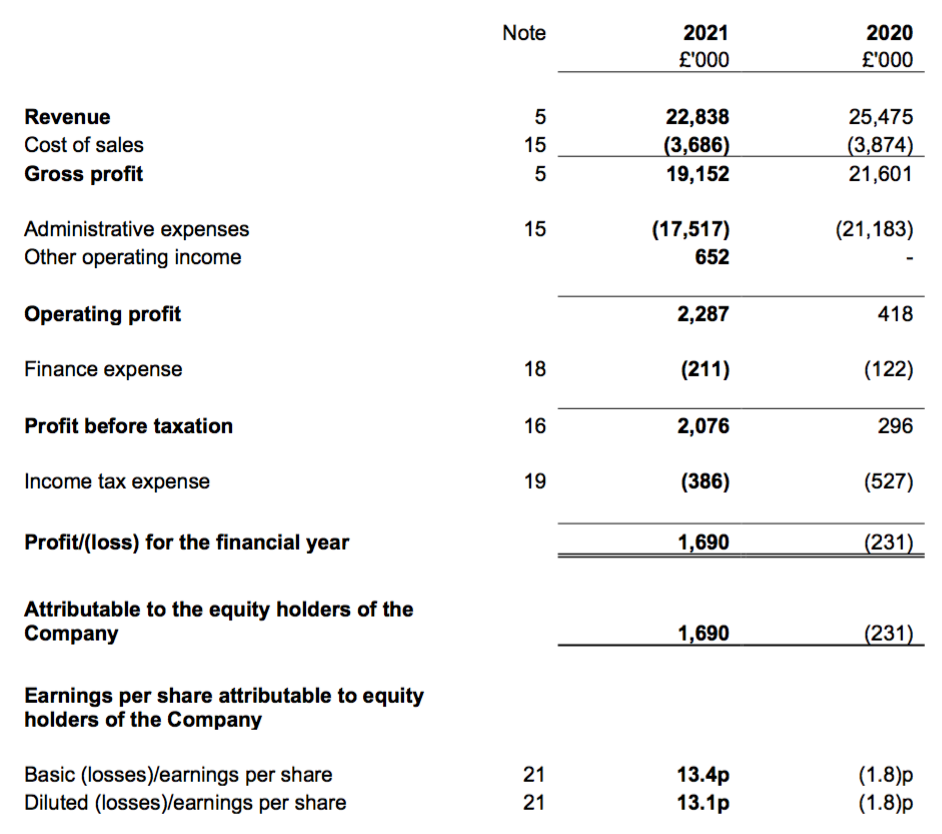

Revenue, profit and management optimism

- A favourable update during April had already confirmed these FY 2021 results would show the remarkable H1 turnaround continuing throughout H2.

- H2 revenue did indeed increase by 8%, to £12.7m, to give annual revenue of £22.8m.

- The adjusted pre-tax profit was indeed £2.9m, which meant the H2 adjusted pre-tax profit of £2.5m was significantly greater than the £0.4m reported for H1.

- The H2 adjusted pre-tax profit of £2.5m was also greater than the £1.8m I had extrapolated at the interim stage.

- Pandemic disruption during H1 meant total annual revenue was the weakest since FY 2012:

| Year to 31 March | 2017 | 2018 | 2019 | 2020 | 2021 |

| Revenue (£k) | 32,801 | 26,939 | 26,899 | 25,475 | 22,838 |

| Operating profit (£k) | 6,308 | 1,985 | 2,056 | 418 | 1,635 |

| Other items (£k) | - | - | - | - | 652 |

| Finance income (£k) | (29) | 7 | (135) | (122) | (211) |

| Pre-tax profit (£k) | 6,279 | 1,992 | 1,921 | 296 | 2,076 |

| Earnings per share (p) | 32.7 | 9.9 | 10.1 | (1.8) | 13.4 |

| Dividend per share (p) | 7.5 | 7.5 | 7.5 | 1.1 | - |

| Special dividend per share (p) | 38.1 | - | - | - | - |

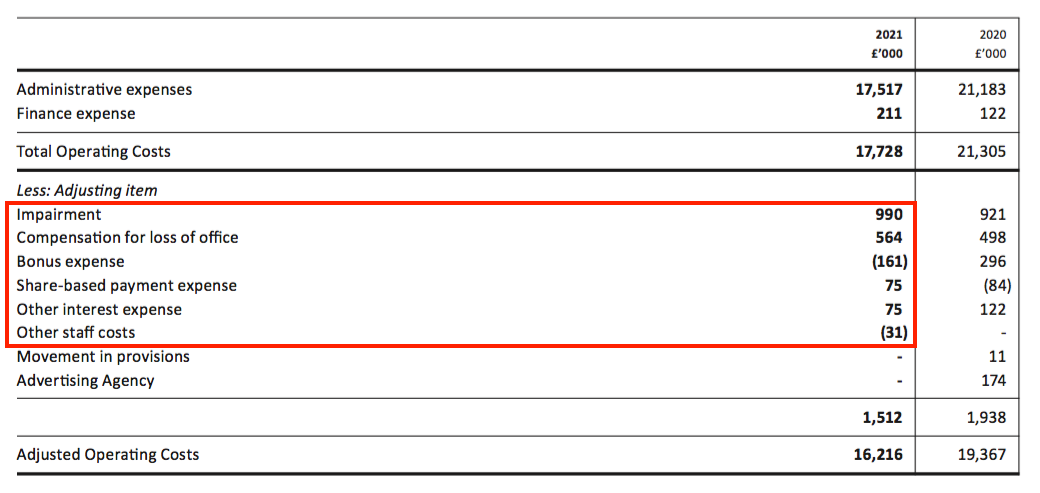

- Profit was shored up by various Covid-prompted cost savings and complicated by a number of adjustments:

- The £1m impairment followed office closures and is arguably a one-off charge.

- “Compensation for loss of office” of £0.6m could also be deemed one-off, although SYS1 has recorded such costs every year since FY 2012 that have totalled £2.5m.

- Reversing the (unusual) bonus credit also seems sensible to arrive at an adjusted figure.

- Government support of £0.7m to navigate the pandemic bolstered the performance as well.

- The government support alongside greater current-year costs (see Valuation below) probably explained why the dividend was not reinstated.

- SYS1’s financial performance was rather overshadowed by some very bullish management commentary.

- Bold projections included:

1) Increasing market share from less than 1% to 10% during the next decade:

“Currently at less than 1% share, we believe that System1 can gain 10% global market share in the next decade-a lower share than the current market leaders“.

2) Setting a medium-term revenue target of £100m-plus (versus £22.8m for this FY 2021):

“We take every decision with our medium term £100m+ Revenue milestone in mind.“

3) Stating the market cap could eventually become £1 billion (versus £40m now):

“We believe that System1 could be worth £1 billion eventually.”

- The finer points of this FY 2021 statement will be quickly forgotten if SYS1 achieves any of those ambitions.

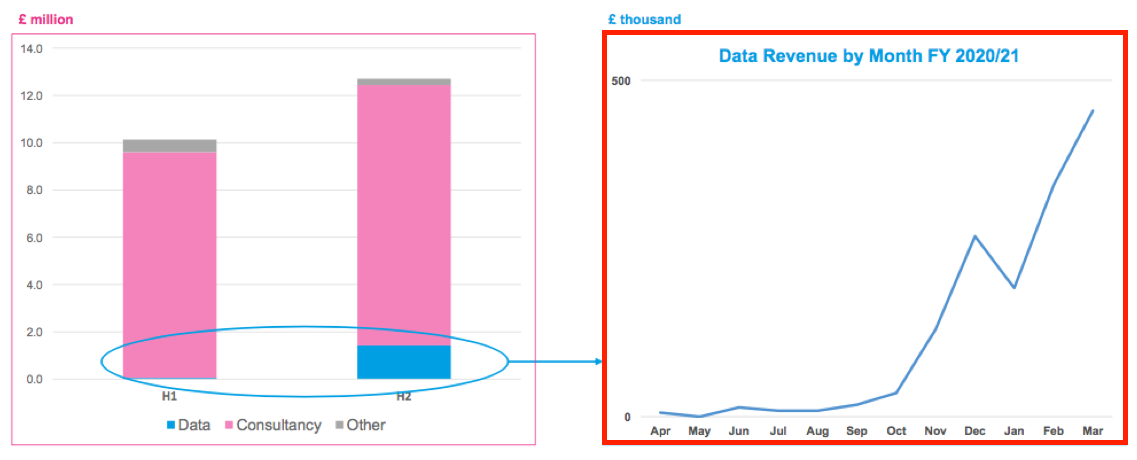

- Supporting management’s optimism was an accelerating shift from consultancy work towards the more predictable data-related revenue:

“Our automated prediction products represented 1% of Revenue at the half-year, 7% in the December quarter and 15% in the final quarter… and are on track to continue growing in the coming months.”

- This right-hand chart from the results presentation was particularly impressive:

- The AGM statement subsequently revealed data-related revenue was likely to rise to 33% of total revenue for the current H1.

- Propelling the greater data revenue were important partnerships with ITV and LinkedIn (see ITV and LinkedIn below).

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Business strategy

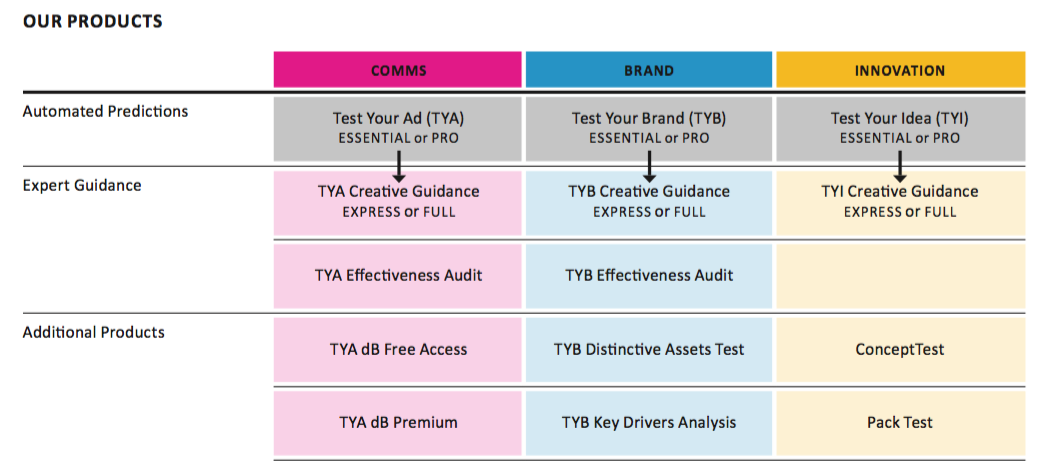

- This FY 2021 statement was notable for management’s clear description of SYS1’s business and strategy.

- SYS1 presented this simple table to outline its products and services:

- SYS1 operates three divisions:

- Communications, which measures and predicts the effectiveness of a client’s broadcast advertising;

- Brand, which measures and predicts the effectiveness of a client’s brands through market-share tracking and product recognition, and;

- Innovation, which measures and predicts the effectiveness of a client’s potential new product or idea.

- SYS1 supplies three services for each division:

- ‘Automated Predictions‘, which are low-cost, automated services that summarise verdicts derived from SYS1’s online-panel surveys.

- ‘Expert Guidance‘, which are SYS1’s consultancy insights into how the advert, brand or new product can be enhanced. This work includes “rapid-turnaround” assignments as well as “higher value-add consultancy” services that include the large, bespoke projects that once dominated SYS1’s top line.

- Various ‘Additional Products‘, which include the AdRatings database that allows clients to access SYS1’s verdict on 50,000-plus televised adverts.

- SYS1 plans to use a disruptive, too-cheap-to-ignore, Amazon-style approach to drive a high volume of advert/brand/innovation testing through Automated Predictions:

“Today many of our Advertising predictions are automated, and we have challenged ourselves to deliver them at 1/100th the cost and 100x faster than traditional methods.“

- SYS1 will then sell the follow-on Expert Guidance consultancy services to improve the advert, brand or innovation.

- SYS1 implied its revamped business was “scalable“:

“Data and production economics point to industry value accruing disproportionately to a small number of scalable players. We are laser focussed on becoming one of them.“

- But SYS1 did not really explain how its follow-on Expert Guidance consultancy services could be as scalable as its Automated Predictions data products.

- I presume some employee thinking and skill must be involved in every Expert Guidance consultancy assignment. How many assignments can then be undertaken will therefore be determined (at least in part) by the productivity of the consultancy employees.

- Automated Predictions for the Communications division (‘Test Your Ad’) is up and running and supported the H2 profit recovery.

- Automated Predictions for the Brand division (‘Test Your Brand’) was launched last week and for the Innovations division (‘Test Your Idea’) will be revamped within the next twelve months.

- Revenue from the ad-testing Communications division has grown from approximately 30% to 46% of total revenue between FY 2016 and FY 2021….

- …and reached 52% during H2:

- I am guessing Communications will remain the largest division over time, as the number of ads a customer creates will probably exceed the number of brands the customer owns and the number of new products it will develop.

Test Your Ad

- SYS1 continues to claim its services outclass those of the competition:

“We maintain that our predictions are the most accurate, cheapest and quickest (24-hour turnaround), and that our guidance to improve our customers’ marketing is the best in the industry. This is the heart of our sales pitch. “

“We believe we are far ahead of traditional competitors in automated predictions and indeed that some of our competitors’ legacy economics will make it difficult for them to catch up with us.”

- Other ‘moat’-type remarks included:

“We are now a product-focussed seller of marketing predictions and improvements – we believe the best in the world“

“our pioneering framework”

“our proprietary databases”

“Our products are difficult to copy“

“world-leading intellectual property”

“helping us build unique relationships with key global customers”

“the largest dataset of advertising predictions in the US and UK“

- SYS1 commendably provides example reports (example pdf here) from the flagship Test Your Ad service that has supported the greater Communications revenue:

- SYS1 said the Test Your Ad service conducted 2,471 tests during the year. Clients included adidas, Sky, Carlsberg and Kellogg’s.

- Total Data revenue was £1,480k, suggesting the average Test Your Ad test cost £600 (assuming no other source of Data income).

- £600 compares with the £2k headline price for Test Your Ad, although discounts for volume testing are available:

- SYS1 claimed 30 companies took out a subscription to the AdRatings database, which has a minimum headline charge of £12k a year, contains verdicts on 50,000-plus adverts and cost at least £5m to develop.

- A potential £360k (30*£12k) income from AdRatings compares to the £53k the service earned during FY 2020.

ITV and LinkedIn

- I remain convinced a partnership with ITV has helped spur greater demand for SYS1’s services.

- To recap, SYS1 announced a tie-up with ITV at the start of 2020 that appeared to validate the philosophy, data and conclusions of SYS1’s advert testing.

- ITV serves many deep-pocketed advertisers and, encouragingly for SYS1, the broadcaster’s new desire to show more effective ads should have some bearing within the industry.

- The pandemic unfortunately delayed any immediate progress, but ITV’s competition for the best Euro 2020 advert — with SYS1 assisting the judging — was run this summer:

- A SYS1-ITV Diversity/Inclusion webinar was hosted the other month as well.

- These results said ITV was “promoting and recommending” SYS1’s Test Your Ad service, which sounds extremely promising although the exact financial arrangements are unclear.

- Perhaps emphasising the ITV impact:

- UK revenue climbed 25% during the year versus non-UK revenue declining 20%, and;

- UK revenue represented 30% of total revenue — the highest proportion since FY 2015.

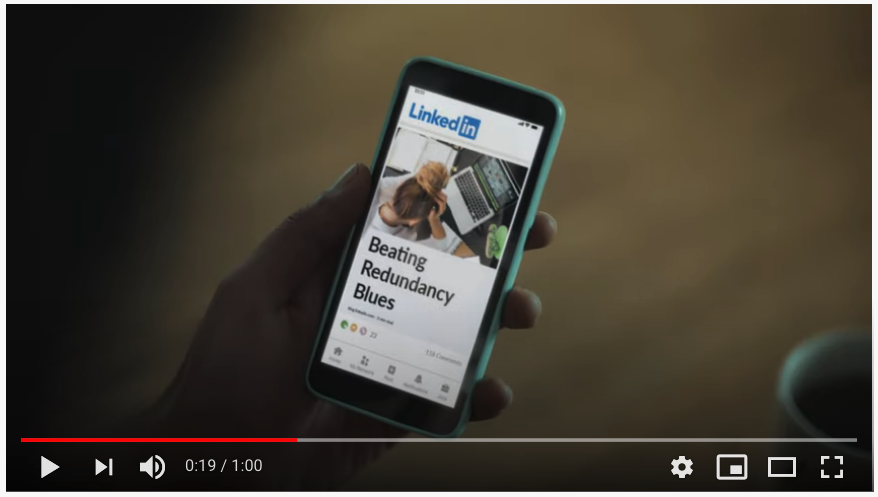

- These results revealed LinkedIn had become the second partner to offer SYS1’s services to advertisers.

- SYS1 claimed its services would allow LinkedIn’s advertisers to “refine and improve” their adverts.

- SYS1 also claimed LinkedIn was “on a mission to do for online B2B advertising what Facebook and Google have done for online consumer advertising“.

- Earlier this year LinkedIn said its advertising revenue had surpassed $3 billion and was “growing nearly three times faster than the B2B digital advertising market overall“.

- SYS1 has helped LinkedIn test and optimise the advert below:

- LinkedIn said the ad was shown in the UK, United States, Australia and Germany and had “delivered strong results for short-term sales activation and long-term market share growth”.

- The growing importance of online video advertising has prompted SYS1 to commission a new book…

A new book, dull films and Mark Ritson

- SYS1 announced Orlando Wood, the company’s chief innovation officer, will write a book about online adverts:

“Orlando Wood is currently using the database in his work with The Institute of Practitioners in Advertising (IPA) on Lemon II, the working title of a follow-up publication to the critically acclaimed Lemon (the IPA’s biggest ever selling book), showing how the principles of the most effective advertising apply as much, if not more, to online video, as they do in TV advertising.“

- I am pleased Mr Wood is back to writing books and not making films.

- As you may recall, Mr Wood’s films “Where the Lemons Bloom”…

- …and Achtung!…

- …were not exactly the riveting works that captured the true System 1 automatic/intuitive/emotional/reactive way of thinking.

- Last year I complained:

“I would recommend Mr Wood keeps to the spreadsheets and German literature. SYS1’s chief marketing officer should step up — or appoint someone else — to do the much-needed System 1 promotional work instead.

Mark Ritson would be ideal: “

- Although Mr Ritson has not become SYS1’s video presenter, his testimonial now adorns the SYS1 home page:

- References to Mr Wood’s films have meanwhile been demoted from the home page to a drop-down menu.

- I am pleased SYS1 has eventually realised Mr Ritson’s fame, feeling and fluency could offer significant appeal to potential clients.

Quality UK investment discussion at Quidisq. Visit forum.

Financials

- SYS1’s main accounting attraction is the cash-flush balance sheet.

- Cash finished the year at £9.0m, up £2.3m over the twelve months and up £1.0m from H1.

- Bank debt of £2.5m matched that of six months ago and twelve months ago.

- Year-end net cash was therefore £6.5m.

- A proportion of the cash appears to be surplus to requirements. Both April’s update and these results signalled a possible share buyback later this year.

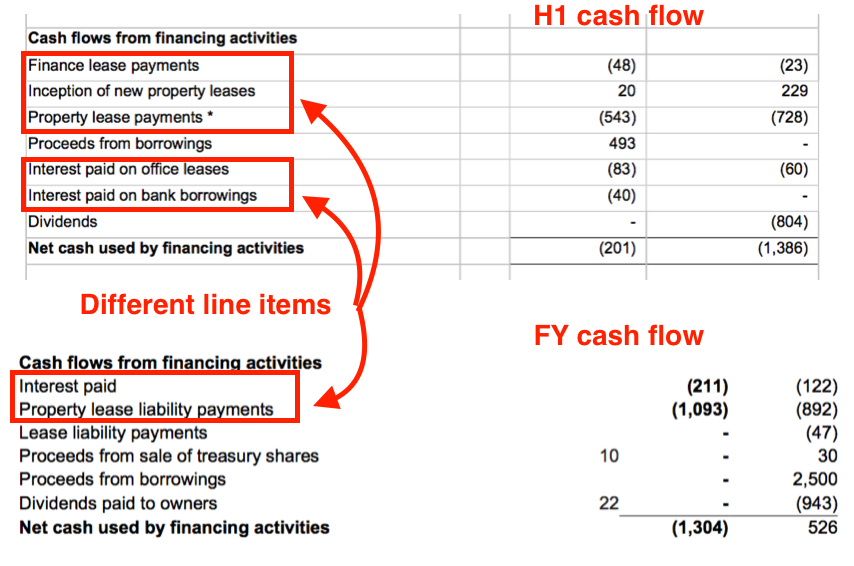

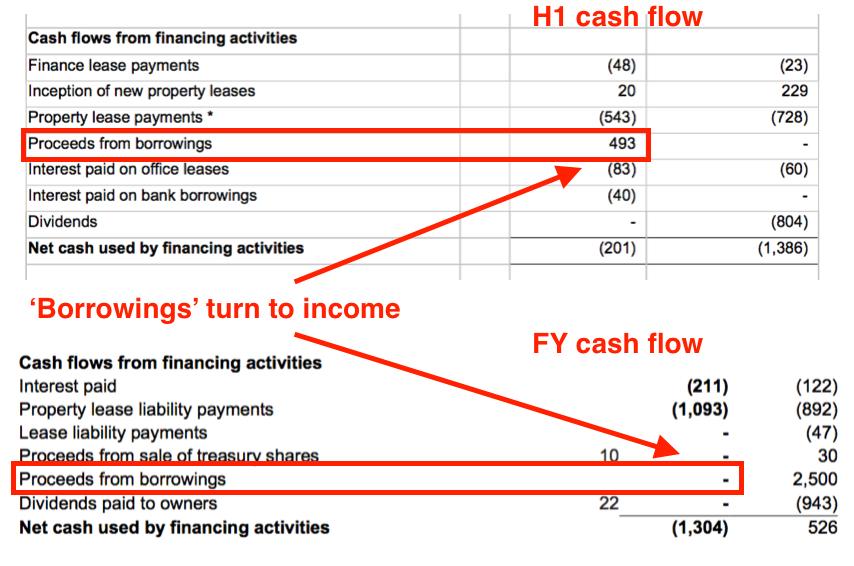

- Evaluating SYS1’s cash flow was not straightforward. H1 cash flow included different entries to this FY 2021 cash flow:

- The £0.5m “proceeds from borrowings” reported during H1 were in fact US government pandemic benefits that were waived during H2 and so recognised as income as part of that aforementioned £0.7m support:

- Free cash flow before tax credits was £2.3m and compared to a £3.1m profit before tax and the aforementioned impairment.

- The £0.8m difference between the two figures was due mostly to an extra £0.5m invested into working capital:

| Year to 31st March | 2017* | 2018 | 2019 | 2020 | 2021 |

| Operating profit (£k) | 7,260 | 1,985 | 2,056 | 418 | 1,635 |

| Depreciation and amortisation (£k) | 556 | 374 | 286** | 494** | 157** |

| Net capital expenditure (£k) | (290) | (113) | (1,030) | (916) | (198) |

| Working-capital movement (£k) | 767 | 775 | (910) | 348 | (499) |

| Net cash (£k) | 8,266 | 5,784 | 4,315 | 4,150 | 6,508 |

(*15 months **excludes IFRS16 depreciation)

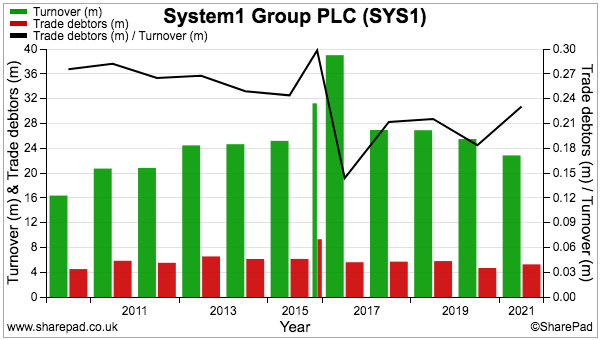

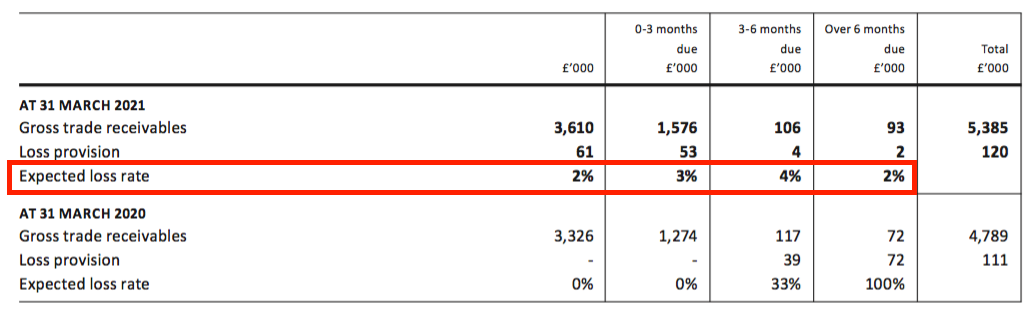

- The extra working-capital funded trade receivables, which grew by £0.6m to represent 23% of revenue:

- Significant trade receivables compared to revenue could mean customers are very late payers and lead to questions about the quality of the company’s sales.

- Trade receivables equivalent to approximately 23% of revenue is about the limit for my shares. Only Andrews Sykes within my portfolio has a similar percentage to SYS1, with FW Thorpe, Mincon and Tristel within the 15% to 17% range and the rest well below 10%.

- Mind you, SYS1’s greater year-end trade receivables will reflect the trading improvement experienced during H2. Doubling up H2 revenue to £25.4m would result in a 21% calculation.

- SYS1’s transition towards high-volume, low-price data services and away from low-volume, high-price consultancy work should mean a lower prevalence of outstanding customer invoices. I can’t recall SYS1 suffering material bad debts in the past and the associated provision rates are low single digits:

- Interest paid of £75k on the £2.5m bank loan implies a 3% interest cost and SYS1 being a lower-risk borrower.

- SYS1’s headline operating margin has improved to 7%:

| Year to 31st March | 2017* | 2018 | 2019 | 2020 | 2021 |

| Operating margin (%) | 18.6 | 7.4 | 7.6 | 1.6 | 7.2 |

| Return on average equity (%) | 47.9 | 14.0 | 18.0 | (3.6) | 26.0 |

(*15 months)

- Excluding SYS1’s adjusting items of £1.5m would give a full-year margin of 14% (£3.1m/£22.8m).

- Notably, for H2, excluding SYS1’s adjusting items would give a margin of 21% (£2.6m/£12.7m).

- A 21% adjusted H2 margin may well be an early indication of SYS’1s scalable ambitions and provide support for all those moat-type remarks. That said, greater costs are on the way that could hinder near-term profitability (see Valuation below).

- My return on equity calculations in the table above have not been altered for numerous profit adjustments and, in light of SYS1’s haphazard five-year progress, remain academic at present.

- Property lease obligations on the balance sheet came to £2.6m versus an associated right-of-use asset of £1.3m.

- The £1.3m difference arguably reflects the sum SYS1 will pay in excess of the cost of leasing the same properties today.

Options and AGM voting

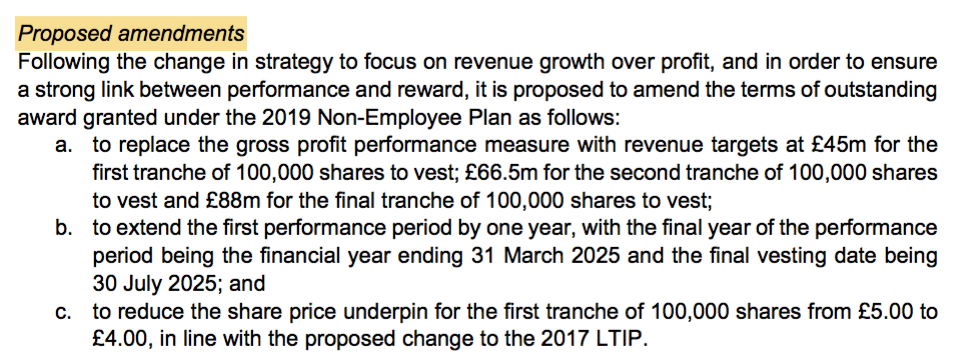

- The results small-print revealed changes to SYS1’s 2019 LTIP plan.

- Changes included:

- Extending the scheme for one year to 2025 due in part to Covid-19, and;

- Replacing a minimum £39.5m gross-profit performance target (up 106% from FY 2021) with a minimum £45m revenue performance target (up 97% from FY 2021).

- Some of the changes were more contentious, not least:

- Reducing the minimum share-price performance target from £10 to £4, and;

- Replacing the minimum earnings performance target of £7m with “the requirement for the Company to be profitable after tax and the Remuneration Committee considering the level of profitability in the year of vesting and the overall corporate and share price performance over the period.”

- The AGM notification small-print — but not the annual report small-print! — revealed changes to the 2019 Non-Employee Plan. This plan’s sole participant is chief executive Stefan Barden:

- Contentious changes to the 2019 Non-Employee Plan included:

- Replacing the minimum gross-profit performance target of £45m with a minimum revenue performance target of £45m, and;

- Reducing the minimum share-price performance target from £5 to £4;

- SYS1 explained:

“We believe we could disincentivise the management team and participants due to the fact that the performance criteria are set at a level that is almost impossible to achieve given the Company’s current strategy, performance and planned growth.”

- Shareholders can presumably now scrap hopes of earnings reaching £7m and the share price hitting £5 (or even £10) by 2025.

- SYS1 sadly did not explain why the performance targets were downgraded while at the same time issuing upbeat remarks about £100m-plus revenue “milestones” and £1 billion market caps.

- Perhaps the follow-up 2026 LTIP will include a £1 billion market cap performance target.

- Shareholders were unimpressed with the option re-jig. The AGM voting showed 27% and 35% protest votes against the 2019 LTIP changes and Non-Employee Plan changes respectively.

- 1,623k (mostly nil-cost) options were outstanding at the year end, while the 2019 LTIP scheme presently has scope to issue another 198k.

- The maximum dilution is therefore 14% with 13,227k shares in issue and 328k shares in treasury.

- The potential dilution is not ideal, but at least the changed options do require revenue to double to £45m during the next four years to come good. Note SYS1 does not expect growth to be assisted by acquisitions:

“The Committee has based the Executive reward structure on the long-term organic growth strategy of the business“

- But whether profit will follow revenue higher is not clear. The AGM notification small-print did state:

“Following the change in strategy to focus on revenue growth over profit…”

- I can only trust the near-term revenue emphasis will eventually pay off and create a significant level of long-term profit.

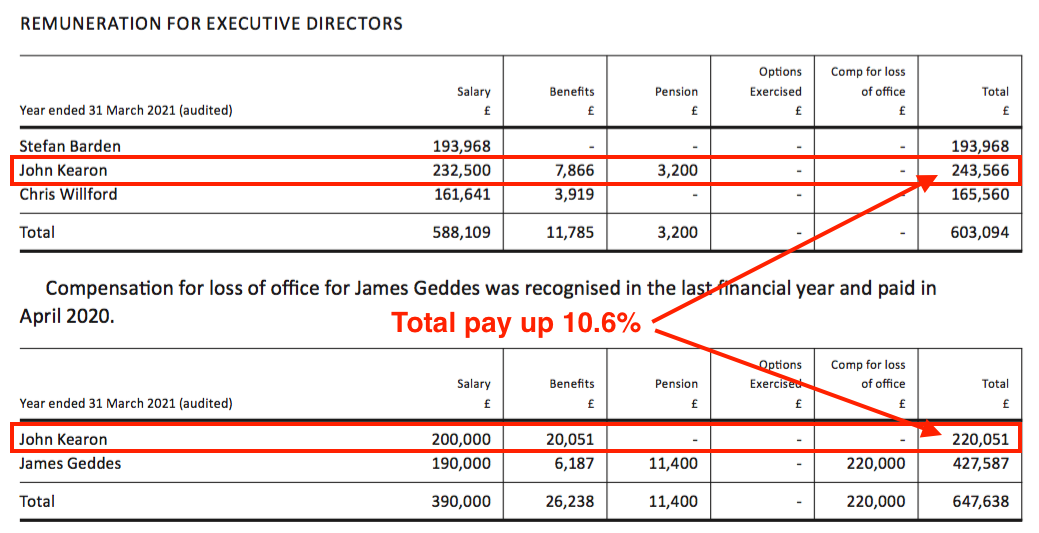

- The AGM voting also protested against the directors’ remuneration with a 24% objection.

- SYS1 did not explain why founder John Kearon saw his total pay and benefits increase 11% during a year when the company:

- Received £0.7m government pandemic support;

- Implemented temporary salary deferrals and reduced staffing levels, and;

- Did not declare a dividend.

- In addition, Mr Kearon arguably delegated some of his executive duties to the new chief executive.

- No wonder SYS1 held its AGM online and did not allow attendees to vote or ask questions during the event.

- While the option revisions and dubious pay rise are not endearing, I have become more pragmatic when assessing suspect remuneration arrangements.

- Five years ago I criticised Tristel (at 130p) and City of London Investment (at 360p) for their option/incentive schemes, but both companies have since performed positively and both share prices have gained.

- I have also criticised the executive pay at Mountview Estates, but that has not stopped those shares from tripling since I first bought (at £41).

- Perhaps SYS1 will become another portfolio holding with unfortunate remuneration arrangements that goes on to perform well.

- Whether the revised options create genuine shareholder value will only be known when (or if) revenue surpasses the minimum £45m performance threshold.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- SYS1 (rather awkwardly once again) indicated near-term profit might not rise in line with revenue as the company invests for growth:

“We plan to remain profitable and to continue to generate cash in the 2021/22 financial year, as we prioritise scaling our automated prediction products. Notwithstanding that, we are targeting revenue growth to be at least matched by the rate of cost growth, due to the pandemic-related cost reductions in the year just ended.“

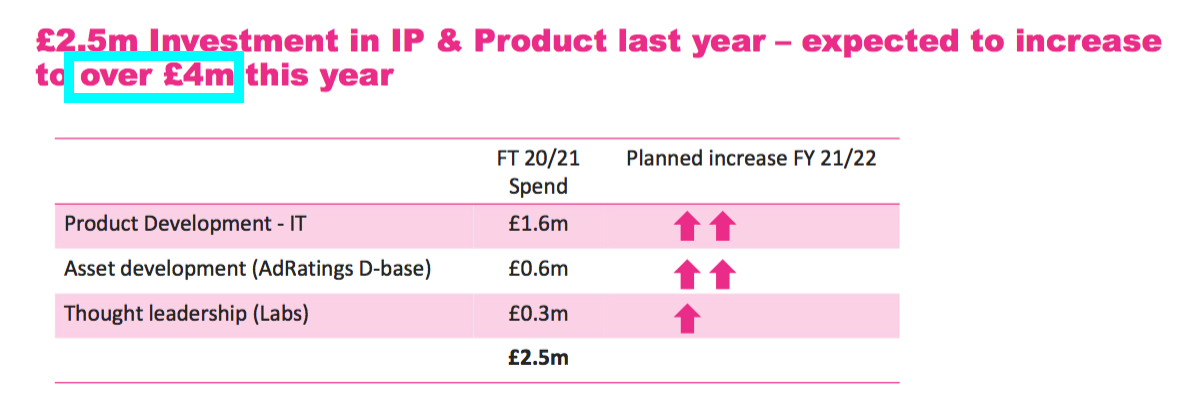

- The results presentation said investment should increase by a minimum £1.5m for FY 2022:

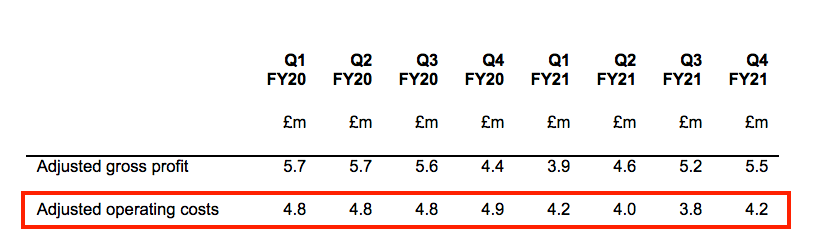

- SYS1 commendably provided the following quarterly breakdown of adjusted costs:

- SYS1’s AGM statement then supplied information on the current-year Q1, the previous Q4 and the previous Q1:

“Total revenue in the quarter ended 30 June was £6.5m, broadly in line with the previous quarter and 38% higher than the equivalent Covid-affected period last year. Data products represented 28% of revenue in Q1, compared with 15% in Q4… The proportion of revenue from our data products continues to rise and will likely represent a third of the Company’s revenues in H1.”

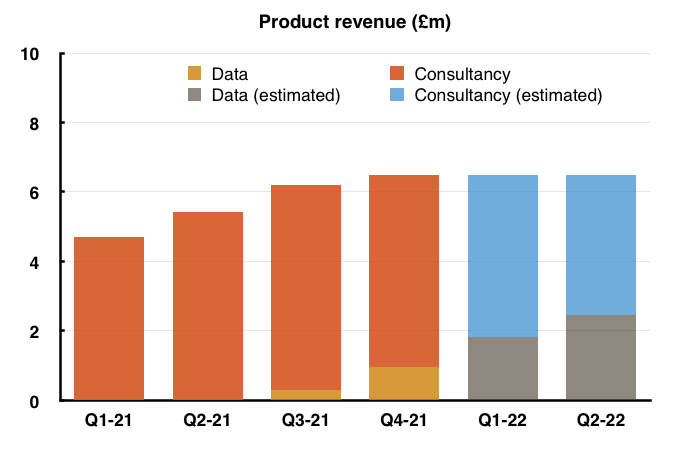

- Amalgamating all the quarterly information and assuming revenue for the current-year Q2 replicates the £6.5m from the current-year Q1, I estimate Data revenue could presently be running at £2.5m a quarter (or 38% of total revenue):

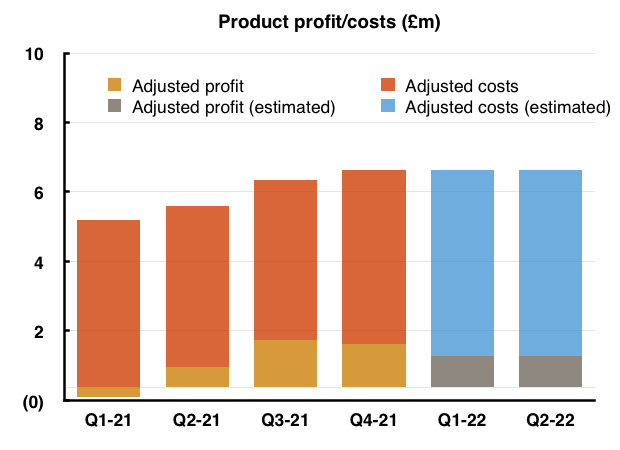

- Assuming adjusted costs increase by the minimum £1.5m SYS1 expects for FY 2022, I estimate adjusted operating profit could be presently running at £0.9m a quarter:

- £0.9m * 4 = a £3.6m annual pre-tax profit, which after standard 19% UK tax would give earnings of £2.9m or 22.6p per share.

- The 310p share price could therefore reflect a multiple of 13-14x based on that extrapolation.

- The AGM statement also confirmed the cash balance had advanced £1.1m to £10.1m during Q1 2022.

- Increasing cash by £1.1m during Q1 supports my estimate of pre-tax profit running at £0.9m a quarter.

- Cash of £10.1m less debt of £2.5m gives net cash of £7.6m — equivalent to 19% of the £40m market cap.

- The sums could be fine-tuned further for SYS1’s mooted buyback.

- SYS1 has approval to repurchase up to 15% of its shares, which if used in full would cost £6.2m at 310p and lift my earnings guess from 22.6p to 26.7p per share and support a possible 11-12x rating.

- Regardless of whether the mooted buyback occurs or not, today’s ratings are not as obviously inexpensive as last year when the share price was 185p, the P/E could have been 8 and net cash represented 25% of the market cap.

- That said, the £40m market cap may be extraordinarily cheap if SYS1’s £1 billion market cap projection is actually met.

- SYS1 believes its market share can surge from less than 1% to 10% during the next decade…

- …which if accomplished would presumably lift revenue from the present £23m to at least £230m (assuming the value of SYS1’s market remains the same).

- Apply a 25% operating margin to that £230m to reflect SYS1’s industry-leading data and scalable business model, and earnings would then be approximately £40m and a 25x multiple would support that £1 billion valuation.

- Alternatively, earnings may be £5m and the medium-term P/E could be 9 were SYS1 to achieve that £45m LTIP revenue target and enjoy a 15% margin.

- While the share price is no longer the obvious bargain it was last year, it may still offer long-term multi-bagger upside should SYS1 one day realise its growth ambitions.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Hi Maynard,

Excellent work as always.

Regards valuation I think you can argue that whilst the the SP was materially lower last year validation of the data products has only more recently occurred – I’d imagine no one who followed the non take up of ad-ratings could have predicted the success of Test my Ad. I’ve been astounded by the data products growth rate – 1%, 7%, 15%, 28%, 38% of rev is staggering QonQ growth imo.

Thanks Patrick.

Yes, I would agree the growth of Data revenue has been astounding following the AdRatings disappointment.

I think there were signs the business had turned a corner (at least profit wise) and things were moving in the right direction (with ITV/Test Your Ad/UK revenue) within the November interims (and perhaps even in the October update just before). Also, the directorspeak back then was rather bullish for a business that had suffered several mishaps in the prior years. While I did not foresee the rate of Data growth, the valuation last year did not really reflect any potential growth anyway, and the risk/reward situation appeared favourable at the time if you believed trading would one day pick up.

Maynard

Well played on upping your stake so early in the Test My Ad progression.

I’d held relatively briefly on Ad Ratings potential Nov 18 to Feb 20 selling when it appeared to be gaining no traction.

Started taking an interest again after the 21st April TS highlighted Test My Ad growth and took a stake when there was a seller in the market in early July (at 225 & 226 with a tiny sliver at 214).

I’d be interested in how you see the more traditional consultancy business progressing. It appears that whilst the data product is incremental, the consultancy business is declining? Or do you see a churn of consultancy customers moving from consultancy to self serve platform customers?

In an ideal world I’d like to see the successful data products business driving customers to Sys1 consultancy services but perhaps that’s too much to ask for and Sys1 will evolve to an almost exclusively platform business in time.

Be interested in your views?

Patrick

Hi Patrick

I am going on the results narrative, which said:

“The products shown in the third layer are higher value-add consultancy ‘Improve’ products, which are more standardised than our previous consultancy services. We continue to undertake large, bespoke consulting assignments for a small number of major customers but anticipate that this type of offering will decline in significance for System1 as customers convert to the faster, cheaper standard products

So revenue per Consultancy assignment will decline as customers convert to the cheaper option. But how much extra Consultancy work will be generated via the lower pricing remains to be seen. The lower charge per assignment could be offset by a much higher volume.

The plan is indeed to drive greater volume of testing via automated products, which then ought to drive greater Consultancy activity for the follow-up advice. So SYS1 could well evolve into an almost exclusively platform business.

The question I have is just how ‘scalable’ are the Consultancy products, as some human skill/intervention is needed to give some advice and the associated revenue will to a certain extent be determined by employee productivity.

I trust your past success with JDG and GAW will now rub off on SYS1 :-)

Maynard

Whilst it’s impossible to accurately predict the future, of my 20 odd stock portfolio SYS1 does seem to have the most obvious attributes of a potential multibagger.

Scalable platform model, respected operator within their industry and plenty of cash to internally fund development. If it emulates JDG and GAW then we’ll both be in clover :-)

Another stock I feel is really interesting currently is GDWN. It’s one you’ve previously covered in 2015 & 2017. I visited the company in early September and feel their multi year transformation from reliance on O&G is about to bear fruit.

Their legacy businesses in Casting and Engineering have secured very long term (multi decade) contracts in nuclear decommissioning and US naval forgings which will ramp up over the next couple of years which have necessitated an expansion of facilities and at Goodwin International O&G valve sales declining from 43% of revenue to less than 33% this year (with valve sales budgeted to be static).

The refractory business is emerging from covid softness in it’s end markets and has a potential new driver in a silica free casting powders which will allow it to target US casting customers. This business also has 2 new patent protected products that are growing from a low base – SoluForm https://www.soluform.co.uk/about-soluform/ and Lithium Battery Fire Extinguishers https://www.avdfire.com/.

Management have high hopes for Easat Radar Systems which has evolved from providing components for Radar systems to providing complete systems which they believe will transform it’s prospects.

Long term perhaps the most exciting business is an internal startup Duvelco which is a company formed to manufacture a polyimide polymer targeting high value components in demanding end markets – aviation etc.

The most recent results highlight an virtual doubling of EPS in H2 over H1 which I believe could well be set to continue into the forthcoming year as the new contracts continue to ramp up. No forecasts out there to provide guidance but I think they’re probably on a forward PE of <15 with excellent prospects of growth over the next couple of years.

Perhaps this post shouldn't be residing on the SYS1 report as I seem to have gone off topic …….sorry :-)

Thanks for the info Patrick. Will probably have to catch up with Goodwin at some point. Lots has happened since I last looked. Could well be a company for a SharePad write-up.

(EDIT 20 Oct 2021: And here is the SharePad write-up)

Maynard

Back to SYS1:

I recently downloaded their Streaming and Entertainment Test Your Brand report for research purposes.

Anyway today received an email from a Client Development Manager suggesting how SYS1 could help me with my brand recognition :-)

Suggests they’re being pretty proactive chasing sales leads.

Hi Maynard

Interesting company and their claim to be a future $1b company does make you sit up and take notice.

Where do come out on the strength of their moat? I have difficulty figuring it out. Is it their predictive power, the speed of analysis or cost advantage? Kantar seems to offer similar products, citing 200k case studies and a similar turnaround time, and they also claim to analyse emotional response, and Kantar is of course bigger. S1 also draws a comparison with Yougov’s business model, but their products seems to be very different. Unlike yougov, What S1 calls ‘Data’ is not really data at all but ad testing. Its data subscription product – Adratings – doesn’t seem to have worked for S1 and I can sort of see why as for an ad, it’s probably more useful to receive tailored feedback than to pick through competitors’ ads, so the recurring high margin subscription revenue may prove elusive.

Regards,

Jerry

Hi Jerry,

Ultimately the competitive advantage will boil down to the predictive power of the testing service. The hard part in all of this is correlating the prediction with subsequent changes to brand recognition, market share etc.

Kantar does offer a very similar service. Kantar interestingly states: “Understand instinctive responses with facial coding (partnering with Affectiva)”

Which leads on to this:

“Affectiva, the global leader in Emotion AI, today announced findings on consumers’ emotional engagement with ad content over the last eight years, which show that advertisers are increasingly pulling on people’s heartstrings to generate a response.”

“This first-of-its-kind emotion database consists of data on 10 million consumer responses to more than 53,000 ads in 90 countries, collected over the last eight years. The data was collected through Affectiva’s Media Analytics software, which uses artificial intelligence to detect nuanced emotional reactions and complex cognitive states from the facial expressions of market research participants when they view ad content.”

Affectiva uses facial recognition, unlike SYS1, which uses simple user responses. I don’t know which is the more accurate option. Other competition will exist, too.

Although SYS1 claims its services are better, cheaper and faster, I recognise the company may not (and never will) have a Google-type dominance. That perhaps has been reflected in the past valuation. If/when the rating starts to rise to premium levels, the size of the moat will become more important to investors.

SYS1’s founder remarked at the AGM the other year of wanting AdRatings to become the “Yougov of advertising data“. The AdRatings database has not worked out as a standalone product and I doubt subscription revenue will ever be material. But the data helps put new predictions into context for the client, and can be used for the all-important correlation between past adverts and subsequent market-share gains.

Maynard

PS I am hopeful the ITV partnership validates SYS1’s standing among effective ad testers.

System1 (SYS1)

Trading update published 20 October 2021

An encouraging update. Here is the full text interspersed with my comments:

——————————————————————————————————————

System1 Group issues the following update on trading for the six months to 30 September 2021. The Company will announce its interim results on 30 November 2021.

The first half of the current year (H1) saw a marked increase in sales of automated data products including Test Your Ad. Data products represented 45% of Revenue in Q2, growing from 28% in Q1. Data Revenue in Q2 exceeded Q1 despite a quarter-on-quarter reduction in total Group Revenue. The Group’s H1 Revenue grew 22% on last year to £12.3m.

——————————————————————————————————————

Q2 Data revenue was better than the Q1/AGM statement had indicated.

Total H1 revenue of £12.3m less £6.5m for Q1 gives £5.8m for total Q2 revenue. 45% of that £5.8m gives Q2 Data revenue of £2.6m and H1 Data revenue of £4.4m — representing 36% of total H1 revenue. SYS1 had previously indicated Data would represent a third of H1 revenue.

Total Q2 revenue of £5.8m is not great given the previous two quarters each registered £6.5m total revenue. But SYS1 is transitioning from bespoke consultancy work to automated Data income and I guess the revenue cross-over will not always balance out. What is important is the more attractive Data revenue is growing quickly:

Consultancy revenue was only £3.2m during Q2 versus £4.7m during Q1 and £5m-plus for Q3 and Q4 of FY 2021. That reduction has meant current profit is running below what I had calculated in the blog post above.

——————————————————————————————————————

Adjusted Operating Costs* grew as planned as the Group continued to invest in automated products, technology and business development, increasing by 10% over the comparable period to £9.0m.

Adjusted Pre-tax Profits are expected to be some £1.3m in H1, approximately £0.9m higher than in the comparable period. Statutory Pre-tax Profits are expected to be £1.3m compared with a loss of £0.4m in the first half of last financial year.

Period end cash, net of borrowings, was £7.3m, compared with £6.5m at end-March 2021.

——————————————————————————————————————

Adjusted operating costs of £9.0m for this H1 is a little better than I had predicted. My sums in the blog post above predicted nearly £9.2m.

Pre-tax profit of £1.3m for this H1 looks about right assuming an 85% gross margin (as per Q4 FY 2021) on the £12.3m H1 revenue (=£10.5m gross profit) less £9.0m of adjusted costs.

But H1 pre-tax profit of £1.3m, or £2.6m annualised, is below my £3.6m full-year guess within the blog post above:

I am hopeful this Q2 is SYS1’s profit low point as Data revenue continues to grow and replace the old-style Consultancy work. H2 could provide some clues as to the possible economics of the Data operation, as any incremental revenue/profit during Q3 and Q4 can be compared to that of Q2.

Net cash of £7.3m is up only £0.8m on the year end, which seems a tad light given H1 pre-tax profit of £1.3m. But the Q1 update implied net cash was £7.6m, which we now know to be £0.3m higher than Q2, so SYS1’s cash movements appear significant from quarter to quarter.

——————————————————————————————————————

We have been delighted by the continuing adoption by both new and existing customers of System1’s repeatable, fast-turnaround and scalable data products as they displace the historic large bespoke consultancy projects that dominated the Group’s activity until H2 last year. We believe that the growth in data revenues signals tangible progress towards our strategic goals, and that these revenues will in due course more than offset the reduction in bespoke consultancy projects as more customers switch to using our automated data products.

In line with previous communications, the Group intends after the interim results announcement to initiate a share buyback programme to repurchase its shares over an extended period, in order to enhance shareholder returns and to satisfy obligations in relation to employee share schemes.

* Adjusted Operating Costs exclude impairment, interest, share based payments, bonuses, severance costs and government support related to the Covid pandemic. Adjusted figures exclude items, positive and negative, that impede easy understanding of underlying performance.

——————————————————————————————————————

Ah, so SYS1 is indeed expecting Data revenue to “more than offset” Consultancy work, albeit “in due course“.

The mooted buyback is still on, although SYS1 is now mentioning an “extended period” and “obligations” to share schemes. So not quite the ‘pure’ buyback I had hoped for.

(There are of course no buyback “obligations” with share schemes; companies do not have to operate such schemes and do not have to buy back the shares to offset the resultant dilution.)

I am now reluctant to consider the buyback for valuation purposes as the text reads as if the money will be spent over many years to keep a lid on share dilution. Mind you, significant option vesting will only occur if revenue doubles to £45m during the next four years — which if it does ought to support a higher share price anyway.

Maynard

Agree with that Maynard, encouraging progress with Data Products (still presumably only Test my Ad with the remaining 2 pillars still to be reflected in the numbers) offset by alarger than hoped reduction in Q2 consultancy revenue.

He’s an example of their work with GSK which I thought quite interesting as it highlights the iterative creative process that SYS1 can assist with.

https://www.adweek.com/performance-marketing/how-glaxosmithklein-used-emotion-tracking-to-hone-its-marketing-for-arthritis-drug/

System1 (SYS1)

US trade name legal dispute

I have been tipped off about a legal dispute:

A US company called System1 Inc is about to float on the NYSE. Here is the S-4 flotation prospectus.

The relevant legal text:

“We have received correspondence from counsel for a United Kingdom-based marketing research company and its United States subsidiary (collectively, the “Demanding Group”) alleging trademark infringement based on our use of the “SYSTEM1” trade name and mark in the United States, and alleged use of the “SYSTEM1” trade name and mark in the United Kingdom.

The correspondence demanded that we cease and desist from using the “SYSTEM1” name and mark, and made reference to potential legal action if we do not comply with that demand.

While we were engaged in active discussions and correspondence with the Demanding Group to resolve the matter, the Demanding Group filed a lawsuit in the United States District Court for the Southern District of New York on September 27, 2021 (the “Infringement Suit”) alleging (i) trademark infringement, (ii) false designation of origin, (iii) unfair competition and (iv) certain violations of New York business laws, seeking, among other things, an injunction, disgorgement of profits, actual damages and attorneys’ fees and costs.

We believe that the Demanding Group’s infringement and other allegations and claims set forth in the Infringement Suit may be subject to a laches defense, among other defenses, and we intend to vigorously defend our rights in the Infringement Suit.

No lawsuit has been filed in the United Kingdom, and we do not believe that our activities infringe any rights of the Demanding Group in the United Kingdom because, among other defenses, we do not offer services to customers using the SYSTEM1 name and mark in the United Kingdom.”

I am not a legal expert, but SYS1 may well have a good case having operated under the System1 brand (in the US and globally) since 2017.

Although System1 Inc does own the https://system1.com/ domain, and I am pretty sure SYS1 would have noted the ownership of that domain before plumping for https://system1group.com/.

System1 Inc will not be short of funds following is US flotation (presentation here). The company has already paid $55m to cover transaction fees and expenses:

So perhaps System1 Inc will pay a handsome amount to SYS1 to settle the case?

Although that outcome may not be ideal if two ‘System1’ companies exist in the States involved in digital marketing in some way. System1’s business model is very different to that of SYS1 though:

The flipside is System1 Inc has a lot more money than SYS1 to contest a protracted legal battle.

Another issue is whether ‘System1’ is actually SYS1’s to own, as the term was devised/popularised by Daniel Kahneman.

Maynard

System1 (SYS1)

Complaint for trademark infringement published 09 November 2021

SYS1 claims the case mentioned in the comment above is “compelling“. Here is the full text:

——————————————————————————————————-

“System1 announces that on 27 September 2021 its US and UK subsidiaries, System1 Research Inc. and System1 Research Limited, filed a complaint for trademark infringement, unfair competition and deceptive trade practices at the United States District Court Southern District of New York against System1 LLC (“the Opposing Party”) over their infringing use of the mark “SYSTEM1”. The Company is being advised in this matter by Norton Rose Fulbright, an international law firm.

The Opposing Party continues to use the “SYSTEM1” name and mark and has announced that it proposes to expand such use by becoming a NYSE-listed company through a business combination with Trebia Acquisition Corp.

The Company takes the protection of its unique intellectual property very seriously and believes such ongoing and expanding use by the Opposing Party is likely to cause significant confusion with System1 Group PLC and its registered marks and, moreover, constitutes intentional infringement, in violation of relevant US federal and state trademark laws as well as trademark laws in the UK, the EU and other countries.

The Board believes that the Company’s case against the Opposing Party is compelling and will issue further updates in due course. A summary of the Company’s registered trademarks is attached to this release.”

——————————————————————————————————-

Here are the trademarks registered in the US:

U.S. Registration No. 5,362,152 for “SYSTEM1 RESEARCH”

U.S. Registration No. 5,488,953 for “SYSTEM1 GROUP”

U.S. Registration No. 5,870,379 for “SYSTEM1 MARKETING”

U.S. Registration No. 5,870,950 for “SYSTEM1 AD RATINGS”

So nothing for “SYSTEM1” in the US, even though SYS1 does have such trademarks in the UK and EU:

EU Registration No. 018400922 for “SYSTEM1”

UK Registration No. 00003596520 for “SYSTEM1”

The obvious question then is who owns the “SYSTEM1” trademark in the US?

I can’t quite see the “compelling” case myself, and perhaps the best outcome for SYS1 is System1 Inc pays off SYS1 handsomely to go away.

Maynard

System1 (SYS1)

Publication of 2021 annual report

1) Section 172

New for the 2021 report is a full Section 172. The s172 for the previous year just referred readers to other parts of the report. Within this year’s s172…

A nice pyramid reiterating the company’s bold market-leading ambition:

Reiterating “better, faster and cheaper“:

Useful snippets about LinkedIn and how to devise an advert, with a start, middle and end:

‘Truth’ and ‘trust’ is important to the company:

‘Truth’ always helpful when adverse trading updates are published! Interesting to see the company applies its own service for employee surveys. Presumably the results are accurate.

Snippets about shareholder alignment:

Contrary perhaps to the text, the online 2021 AGM did not allow investor participation on the day (questions had to be submitted in advance). Whether the AGM had to be online was questionable, too. The event was hosted in August, the same month I attended a physical AGM for a different company.

Useful to know there are no plans to raise extra cash!

Interesting insights about the suppliers:

All seem to be on-board for helping SYS1 disrupt the industry.

2) Risks

No major changes and only the one extra ‘sub-risk’.

A few bits of revised text for this year, including:

For 2020 the mitigation text for losing a significant customer included: “We therefore go to considerable lengths to monitor service quality and seek client feedback.” Now SYS1 just “works hard to earn their loyalty“.

Revenue from the largest customer at 8.1% equates to £1,861k, versus £2,596k for 2020. Never clear whether SYS1’s largest customer is always the same client. But the contribution has bobbed up and down over the years, ranging from £1,476k for 2012 to £3,402k for 2017.

The extra sub-risk relates to the company’s transition to automated products:

3) Corporate governance

Looks like the directors all attended their relevant meetings:

Mr Barden and Mr Willford attended two main board meetings before becoming formal executives in June. Also, the three executives sat in on the rem-com meetings, which is notable because Mr Kearon enjoyed a useful 11% pay hike despite the company collecting furlough payments and him delegating some duties to Mr Barden (see blog post above).

I recall the 2020 report had confirmed no execs were involved with their own remuneration:

But this 2021 report removed all that text:

Not sure why somebody removed that text. Surely Mr Kearon did not have a say in deciding his extra 11% pay hike?!

A review of the board and chairman (new for 2021) did not reveal anything untoward:

4) Audit and audit report

The non-exec in charge of the audit committee is in fact in charge of three other audit committees, so not unfamiliar with auditors:

The new FD decided to change the accounting software:

No audit problems:

Slight change to key audit matters. Just the sabbatical provision looked at this year (and not intangible asset valuation as well). The impairment of the intercompany receivable was added for 2021, but is somewhat academic from a group perspective:

Going-concern audit text all revamped for 2021, including notes on worst-case scenarios and covenant breaches:

Reads as is SYS1 would still be able to pay back the bank loan if big trouble strikes.

Standard 5% of pre-tax profit for audit materiality:

100% audit coverage, but a full audit was performed only in the UK — which represents just 30% of revenue:

Mind you, the previous auditor performed only audit ‘procedures’ on the subsidiaries for 2019, so a full audit at the UK subsidiary is an improvement on that.

New standard audit text for 2021 covering fraud:

5) Director remuneration

A reminder that the LTIP participants do not receive an annual bonus:

The remuneration policy says revisions should happen every four years…

…but then lists a load of revisions for the LTIP (see blog post above):

“Implementation of the new strategy is unlikely to be linear…” has (sadly!) been confirmed by subsequent trading statements:

The LTIP was changed because management could have been “disincentivised“:

Reads as if management would have actually been discouraged to perform without the revised LTIP, which does not sound great.

06) Going concern

Revamped text for 2021:

“the Group is a lot more confident about how to respond to an abrupt negative situation” should be useful given subsequent trading updates!

07) Revenue recognition

Nothing untoward. Revenue booked when the consultancy report is delivered:

08) Customer and supplier payments

Useful snippets on payment terms. Customers should pay within 60 days of delivery, and some customers pay upfront:

Trade receivables were £5.3m, which versus revenue of £22.8m suggests payments take (5.3/22.8*365) = 85 days:

Doubling up the stronger H2 gives revenue of £25.4m and implies payment terms of 76 days. So customers are can be tardy payers.

Footnotes indicate 33% of trade receivables were overdue (£1.7m/£5.3m), which is not ideal but not out of keeping with previous years:

Overdue trade receivables were 29%, 36% and 34% of total trade receivables for 2020, 2019 and 2018 respectively.

Working-capital cash movements have never really appeared untoward, so I guess SYS1 eventually collects these payments.

The largest customer is a slow payer:

Largest customer represented revenue of £1,861k, and receivables of £666k indicate payment terms of 666/1861*365 = 131 days.

Trade payables remain relatively small at £845k, with terms quoted at 30-45 days:

The level of trade payables is not great when trade receivables are 4-5x larger (i.e. SYS1 pays suppliers much earlier than customers pay SYS1).

But SYS1 does carry notable accruals and deferred income, which I suspect are mostly expenses recognised but not yet invoiced by the supplier. So the overall receivable/payable cash flow movement may not be so pronounced.

Also, SYS1 does benefit from contract liabilities, which reflect upfront customer payments and are double the size of ‘contract assets’ (external costs capitalised for project work not yet completed):

09) Borrowings

Interest charged on the £2.5m loan is a reasonable LIBOR+2.5%:

Finance lease IFRS 16 obligations reduced to £2.6m from £4.3m for the previous year after office closures:

The associated right-of-use asset of £1.3m implies SYS1’s obligation of £2.6m is twice as much as would be the case if the remaining lease agreements were started today.

10) Options

Confirmation of the option count being 12.8% of the year-end share count (adjusted for treasury shares). Most options concern the LTIP:

11) Employees

New for 2021 are helpful entries concerning R&D:

Total R&D up 20%.

Staff numbers down in all areas save for IT, which understandably increased given the shift towards Data revenue:

The lower headcount led to lower employee costs:

Nothing truly shining through on the workforce productivity front to emphasise the Data transition. Revenue per employee was £170k, a fraction below the average of the preceding five years of £177k. Total cost per employee was £79k, just about matching the preceding five-year average of £80k.

Not something awarded at every company: staff earn an extra 20 days holiday after serving for six years:

12) Tax

Confirmation of R&D tax credits, which if continued may prove helpful for cash flow purposes:

Maynard