25 June 2019

By Maynard Paton

Results verdict on System1 (SYS1):

- An unspectacular performance with gross profit unchanged and profit rebounding due only to cost cuts.

- The new AdRatings service suffered a woeful start after generating revenue of just £3k.

- The lack of all-round progress prompts awkward questions as to whether the group’s advert-analysis services are actually of much interest to the marketing industry.

- The accounts remain cash rich and would exhibit respectable ratios were it not for the chunky AdRatings start-up costs.

- The P/E could be somewhere between 10 and 15 assuming AdRatings one day breaks even (or is scrapped). I continue to hold.

Contents

- Event links and share data

- Why I own SYS1

- Results summary

- Revenue, profit and dividend

- AdRatings

- A wider doubt

- Balance sheet and cash flow

- Valuation

Event links and share data

Event: Final results and presentation for the twelve months to 31 March 2019 published 6 June 2019

Price: 230p

Shares in issue: 12,576,619

Market capitalisation: £28.9m

Why I own SYS1

- Market-research agency that predicts the long-term effectiveness of client adverts, with success built upon a “difficult-to-replicate” history of advert assessments created over 20 years.

- Boasts founder/entrepreneurial/owner-friendly chief exec who has overseen an acquisition-free growth record, retains a 23%/£7m shareholding and has declared five special dividends.

- Offers cash-rich accounts, decent underlying margins and a potentially modest valuation — assuming the new AdRatings division can one day break even.

Further reading: My SYS1 Buy report | All my SYS1 posts | SYS1 website

Results summary

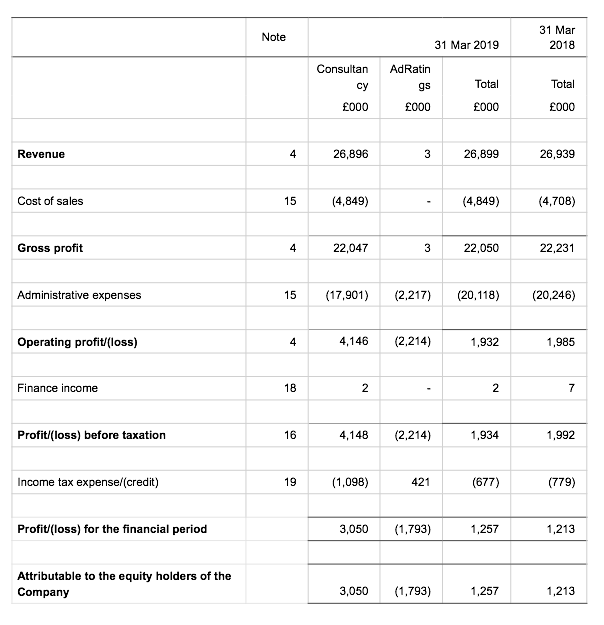

Revenue, profit and dividend

- A trading statement issued during April had already indicated these results would not be spectacular.

- Gross profit — SYS1’s main top-line performance measure — was indeed the £22m cited in April.

- Reported profit was affected by AdRatings start-up costs of £2,214k, a one-off gain of £251k and a share-based payment credit of £196k.

- Pre-tax profit before the AdRatings start-up costs, the one-off gain and the share-based payment credit was indeed the £3.7m cited in April.

- Progress was made only by reducing expenses following the “miserable” preceding year. Gross profit fell 1% while operating profit (before AdRatings start-up costs, the one-off gain and share-based payments) rebounded by 80%.

| Year to 31st | Dec 2014 | Dec 2014 | Dec 2014 | Mar 2016 | Mar 2017 | Mar 2018 | Mar 2019 | |

| Revenue (£k) | 24,645 | 25,184 | 31,236 | 25,917 | 32,801 | 26,939 | 26,899 | |

| Gross profit (£k) | 19,410 | 20,250 | 25,643 | 20,989 | 26,984 | 22,231 | 22,050 | |

| Operating profit (£k) | 4,301 | 4,546 | 6,229 | 5,052 | 6,308 | 1,985 | 1,932 | |

| Other items (£k) | - | - | - | - | - | - | - | |

| Finance income (£k) | (15) | (45) | (29) | (21) | (29) | 7 | 2 | |

| Pre-tax profit (£k) | 4,286 | 4,501 | 6,200 | 5,031 | 6,279 | 1,992 | 1,934 | |

| Earnings per share (p) | 23.0 | 24.0 | 31.9 | 26.7 | 32.7 | 9.9 | 10.0 | |

| Dividend per share (p) | 4.3 | 4.5 | 1.1 | 4.5 | 7.5 | 7.5 | 7.5 | |

| Special dividend per share (p) | 12.0 | - | 12.0 | - | 38.1 | - | - |

- A notable development was the maintained dividend.

- SYS1’s interim statement had said: “Final dividend may be reduced, depending principally on the scale of further investment in AdRatings and on opportunities to repurchase shares at an attractive valuation.”

- These results then stated:

“Given the investment opportunities with AdRatings, and a share price which some consider depressed, the decision to maintain the dividend was considered carefully.

This level of dividend will not impair the Company’s plans for AdRatings, as we have sufficient liquidity to cover planned investment including that relating to AdRatings.”

- However, the door was seemingly left ajar for a future dividend cut:

“Whilst the Board is prepared to consider reducing the dividend (as flagged in our Interim Statement), it views maintenance of the dividend as a useful discipline which it seeks to adhere to unless there is sufficiently clear-cut reason otherwise (which, in the Board’s view, is not the case at this time).

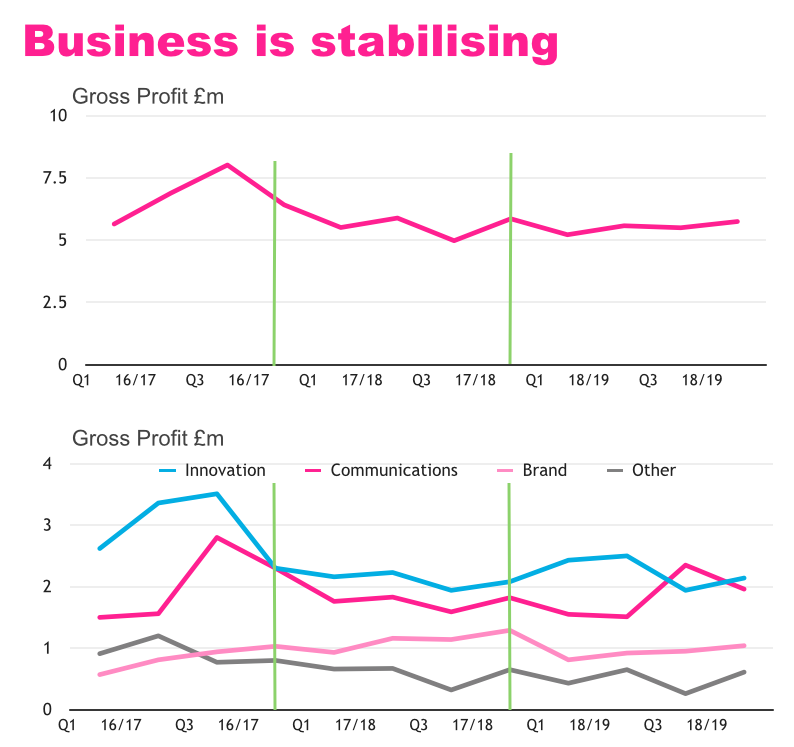

- The charts below from the results presentation show the gross-profit performance and the divisional gross-profit performances for the last twelve quarters:

- SYS1 claims its “main competitive strength” lies within its Communications division.

- The group says the Communications division has “developed market research techniques which we believe are better able to predict the long-term effectiveness of advertising than anyone else’s.”

- The Communications division offers “the most potential”, too:

- Meanwhile, the Brand division is said to be the most stable, and the Innovation division to be the most unpredictable.

- SYS1’s half-year split showed second-half gross profit up 3-4% versus the preceding first half and versus the comparable second half of 2018:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Revenue (£k) | 13,822 | 13,117 | 26,939 | 13,182 | 13,717 | 26,899 | |

| Gross profit (£k) | 11,394 | 10,837 | 22,231 | 10,802 | 11,248 | 22,050 | |

| Admin costs* (£k) | (10,554) | (9,692) | (20,246) | (9,133) | (9,022) | (18,155) | |

| Operating profit (£k) | 840 | 1,145 | 1,985 | 1,669 | 2,226 | 3,895 |

(*excludes AdRatings costs and £251k one-off gain for 2019)

- Last year’s introduction of a ‘Creative Guidance System’ — a plan to split certain work to provide cheaper, automated services and eventually win larger contracts — has yet to bear fruit.

- SYS1 says its pricing competitiveness has been restored, but admits the large-scale programmes are a “work-in-progress”.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

AdRatings

- The new AdRatings service has suffered a woeful start.

- SYS1 recapped what this product offers:

“AdRatings is a large database showing ‘ratings’ or ‘scores’, of adverts in the market as a whole. It allows clients to assess the effectiveness of their historical advertising and benchmark it against peer companies, competitor categories and the industry as a whole.”

- This time last year, SYS1 said AdRatings would be “dramatically better, cheaper and faster than any existing provider.”

- The service launched during November and generated revenue of only £3k during the subsequent four or so months.

- If the service was indeed “dramatically better, cheaper and faster than any existing provider”, then surely many clients would have signed up straight away and paid SYS1 a lot more than £3k.

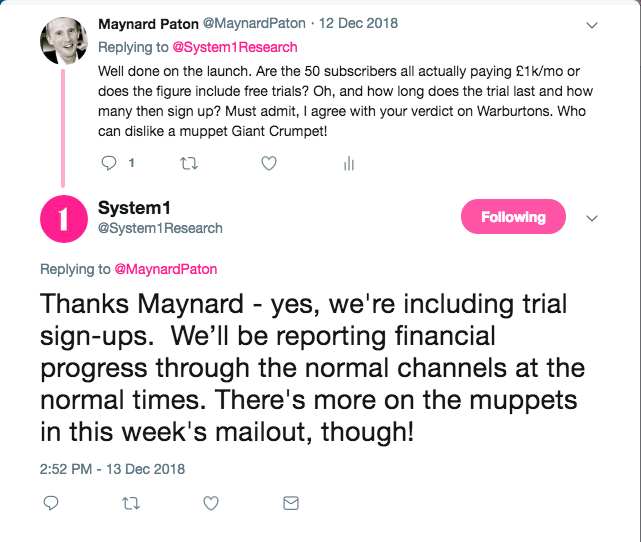

- A now-deleted tweet from @System1Research claimed AdRatings had gained 50 “subscribers” soon after launch.

- My enquiries revealed those 50 subscribers included free trials:

- Free trials for AdRatings are (supposedly) limited to 14 days (clause 3).

- At launch, AdRatings asked customers to pay £1k/$2k a month. The AdRatings website now shows the price has doubled to £2k/$4k a month.

- Revenue of £3k during four months suggests the service has captured only one paying customer.

- SYS1 said in this results statement: “We are piloting ways both to enhance and commercialise this [AdRatings] database with a small number of clients, prior to an expected further roll out later in the current financial year.”

- SYS1 said in the accompanying results presentation: “AdRatings is still in the Beta testing and development phases, with a limited number of clients. We are developing the functionality and commercial offering and expect sales to accelerate once it begins to catch on, but cannot predict when.”

- AdRatings was seemingly never ‘launched’ at all. Instead, the service remains as a pilot project in beta testing.

- The distinct lack of AdRatings progress prompts some awkward questions.

- In particular, exactly what extra functionality does AdRatings require? The service already contains data for 34,000-plus adverts and offers the fundamental advert-comparison feature.

- Why have SYS1’s existing clients not subscribed?

- SYS1 serviced 251 clients during 2019, and earned an average £88k gross profit from each one. The client base includes multinationals that could easily afford the initial £12k (or the current £24k) a year subscription.

- Indeed, price cannot be a dissuasive factor — because SYS1 said AdRatings would be “dramatically… cheaper” than the alternatives. Management comments at the 2018 AGM suggested “ultra-low pricing ought to encourage subscribers”.

- I can only conclude the lack of uptake must be due to clients just not being interested in what AdRatings has to offer.

- When I studied the AdRatings website back in November, two thoughts struck me:

- Thought 1) Numerous categories cover only a handful of advertisers. Potential subscribers may therefore already have a good idea of who is performing well in their sector — and not require SYS1’s data.

- Thought 2) Certain categories — such as finance and medical — are hamstrung by various advertising regulations. Such adverts are generally deemed by SYS1 to be 1-star money-wasters, which begs the question why anyone would pay to discover how much money everybody else serving the category is (apparently) wasting.

- SYS1 remains optimistic about the start-up service:

“We view the risk/reward profile of AdRatings as attractive. The investment has limited downside risk and high upside potential, both in terms of helping propel our existing Communications business and in creating a new scalable revenue stream.”

- £3m was spent on AdRatings last year and £2.5m is budgeted for the current year. I suppose the “limited downside risk” is the service being culled and at least £5.5m (43p per share) being wasted.

- Some 105 AdRatings subscribers paying £2k a month are required to cover costs of £2.5m a year.

A wider doubt

- The lack of AdRatings revenue raises a wider doubt about the whole business — are SYS1’s services actually of any interest to the majority of marketing departments?

- The “miserable” results for the preceding year were blamed on cutbacks at multinationals following a mooted bid for Unilever.

- However, client cutbacks can only be blamed for so long.

- SYS1 admits its gross profit has grown at 5% per annum since 2012 — a modest performance that suggests the group’s marketplace may not offer wonderful potential.

- That 5% growth history even comes with the effective backing of industry gurus Les Binet and Peter Field — high-profile experts that praise the long-term, brand-building adverts that SYS1 champions.

- Perhaps the brutal reality is that most marketing departments neither care about SYS1’s services, nor care about the style of advertising that SYS1 claims should lead to “profitable growth”.

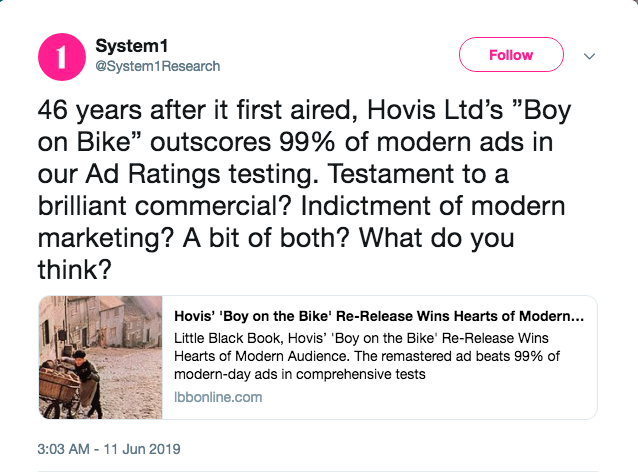

- SYS1 appears frustrated by the industry’s general direction. The group asks: “Who Killed Effective Advertising?” Clive Clickthrough? Ingid Investor? Brandon Blockchain?

- Further frustration: SYS1 points to a 46-year-old advert that resonates more with today’s viewers than 99% of modern adverts:

- The irony of course is that SYS1 informs companies whether their marketing is effective — but appears to be not so effective when marketing its own services.

Balance sheet and cash flow

- SYS1’s books remain reasonably straightforward. The results RNS was commendably published with the full accounts.

- The AdRatings expenditure continues to leave SYS1’s accounting ratios less attractive than before.

| Year to 31st | Dec 2014 | Dec 2015 | Mar 2017* | Mar 2018 | Mar 2019 |

| Operating margin (%)** | 22.2 | 22.4 | 22.6 | 8.9 | 8.8 |

| Return on average equity (%) | 36.6 | 35.8 | 47.9 | 14.9 | 14.4 |

(*15 months **operating profit as a proportion of gross profit)

- Exclude the AdRatings expense, one-off gain and share-based payment credit, and operating profit as a proportion of gross profit would have been a worthy 17% for 2019.

- Cash conversion was not great:

| Year to 31st | Dec 2014 | Dec 2015 | Mar 2017* | Mar 2018 | Mar 2019 |

| Operating profit (£k) | 4,301 | 4,546 | 7,260 | 1,985 | 1,932 |

| Depreciation and amortisation (£k) | 425 | 459 | 556 | 374 | 287 |

| Net capital expenditure (£k) | (273) | (322) | (290) | (113) | (1,030) |

| Working-capital movement (£k) | (89) | (1,053) | 767 | 832 | (858) |

| Net cash (£k) | 5,347 | 6,365 | 8,266 | 5,784 | 4,315 |

(*15 months)

- The increase to net capital expenditure was due to £923k spent on AdRatings that was capitalised on to the balance sheet and mostly avoided the income statement. (This expenditure will be amortised fully through the income statement during the next three years.)

- Prior to 2019, net capex had been prudently covered by the depreciation and amortisation charged against earnings.

- The adverse working-capital movement was due to higher trade receivables, which perhaps reversed the favourable movement of the prior year.

- SYS1 has tended to manage its working capital well — the multinational client base could easily be very slow payers to such a small supplier.

- Free cash flow for the year was a negative £463k, which after £940k paid as dividends left the bank balance £1.4m lighter at £4.3m (34p per share).

- SYS1’s books remain free of debt and free of pension obligations.

Valuation

- Assessing SYS1’s valuation requires a view on the prospects of AdRatings.

- Assume the net present value of AdRatings is zero, and SYS1’s £29m market cap is simply 11 times my £2.7m (or 21p per share) earnings estimate for the other parts of the group (before the one-off gain and share-based payment credit).

- Assume the £4.3m cash position is surplus to requirements, too, and the rating is less than 10 times.

- Assume instead that SYS1 will plough on with AdRatings losing £2m a year forever, and 2019’s reported earnings of £1.3m support a multiple of 22x.

- A potential outcome for AdRatings is significant losses occurring for the next year or two, followed by minimal profit contributions thereafter.

- Let’s say a further £5m is pumped into AdRatings before the division breaks even. A £29m market cap plus £5m gives £34m, which divided by my £2.7m earnings estimate leads to a 13x rating.

- Assume £10m is pumped into AdRatings before the division breaks even, and the multiple becomes 15x.

- My sums suggest the share price is expecting AdRatings to absorb a substantial amount of money before the new service eventually covers its costs.

- My estimated multiples of between 10x and 15x look about right for a business that has expanded at a 5% per annum average since 2012.

- SYS1 claimed its “[i]nvestment in AdRatings, while significant, will not strain the balance sheet, is discretionary, and is being managed dynamically as we learn from initial client feedback.”

- During 2019, the main parts of the group delivered an underlying £3.7m operating profit — which would just about cover the £2.5m projected current-year spend on AdRatings and another £940k as dividends.

- SYS1’s outlook comments did not hint at imminent growth fireworks:

“Although we have limited short-term revenue visibility, we believe that the core business can return to steady long-term growth, and that in addition the Company has upside potential with AdRatings.”

- A repeat of the 7.5p per share dividend supplies a 3.3% income at 230p.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in System1.

System1 (SYS1)

Publication of 2019 annual accounts

SYS1 commendably published its full annual accounts within its full-year results RNS. Here are the points of interest.

1) Corporate governance

SYS1 has followed the new AIM rules by declaring a corporate governance statement:

The statement contained nothing too out of the ordinary. The directors think for the medium-to-long term:

2) Brexit risk

The report added a new risk for Brexit:

3) Auditor

Grant Thronton — auditor of Patisserie Valerie — has been swapped for RSM:

4) Stefan Barden

Confirmation that 6% shareholder Stefan Barden is advising the board on strategy and technology:

Would be useful to know what strategies Mr Barden has suggested to the directors.

5) Director pay

The chief exec’s pay has been held at £200k (or just below) for five years now:

This next note reminded me that 2018 incurred a (sort of one-off) £215k loss-of-office charge, which would have flattered year-on-year profit comparisons:

6) LTIPs

The 2017 LTIP scheme has been modified because SYS1 admits the minimum targets are now unlikely to be met by the original 2021 deadline:

The options holders receive another three years to 2024 for SYS1 to hit certain profit measures and the share price to reach 994.5p.

The chief exec has now joined the 2017 LTIP after initially hoping for annual bonuses instead:

Confirmation of Stefan Barden’s LTIP scheme:

Would be useful to understand why Mr Barden has different targets and timescales to the 2017 LTIP plan.

Confirmation of the 11.3% LTIP dilution:

The 11.3% dilution can only occur if the share price breaches £10. I will take that dilution.

7) IFRS 16

No problems with the upcoming new rule for lease accounting:

8) Largest client

This is interesting.

SYS1’s largest client represented 6% of revenue for 2019 (5% for 2018 from the same client):

However, a different note says the largest client represented 6% of revenue for 2019 but 10% (i.e. not 5% as per the note above) for 2018:

I can only conclude the largest client of 2019 was not the largest client of 2018. Other figures suggest revenue from the 2018 largest client fell from £2.6m to at most £1.5m.

Perhaps the group’s wider standstill performance was due to this particular large client spending £1.1m less during 2019.

£1.1m of lost client revenue might equate to £0.9m of lost gross profit, which could have added 4% to the £22m gross profit actually reported for 2019.

Disclosed for the first time was SYS1’s largest 10 clients representing 35% of revenue.

9) Employees

Good progress here:

The headcount fell by 20, leaving gross profit per employee up from £134k to £152k — second only to the £169k for 2017. Pre 2017, gross profit per employee was below £140k — so productivity has generally improved (I suspect due to the greater ‘automation’ of in-house processes).

Perhaps not surprisingly, cost per employee increased, by £5k to £82k. The high was £87k during 2017.

Total employee costs represented 54% of gross profit, versus 57% for 2018 and 65% for 2017. The low was 51% during 2008.

Note that (sort of one-off) redundancy costs (see note above) were £424k less during 2019 than 2018 — which would have flattered year-on-year profit comparisons.

10) Share-based payment

Not often a share-based payment *credit* is recorded within the books. But SYS1 enjoyed a total £196k credit during 2019:

I guess the credit is due to the 2017 LTIP scheme becoming very unlikely to produce any vested options, and so the credit reverses part of the initial share-based payment charge. I would not count this credit as part of an underlying profit.

11) AdRatings

Confirmation of AdRatings absorbing £923k of cash expenditure that was capitalised on the balance sheet, of which £110k was subsequent amortised through the income statement:

This next note is interesting. Management reckons AdRatings could receive 50% fewer subscriptions than planned, but the expenditure would not be impaired:

Confirmation of the three-year amortisation period:

12) Advertising agency

SYS1’s fledgling advertising agency remains a loss-maker:

However, my sums suggest the agency did record a small profit during H2.

13) Trade receivables

SYS1’s clients continue to pay their bills, but slightly slower than before:

Outstanding invoices represented 22% of revenue for 2019, versus 19% for 2018 and 18% for 2017 (albeit under slightly different accounting rules).

Meanwhile, trade receivables ‘not past due’ were 64% versus 66% for 2018 and 69% for 2017. I note SYS1 has for the first time introduced a 6-plus months past-due category, which cover 2% of all trade receivables.

14) Exceptional credit

Confirmation of the £251k one-off gain:

15) Net cash from operations error

I reckon the 4244 shown in the note below should be 423 to allow the reconciliation to add up correctly:

Maynard

Hi Maynard,

Excellent write up as always but does not make me regret selling out my holding the day before your article was published. After holding for many years I have too much doubt in this company’s offering so sold at a 20% capital loss. I now think there are better opportunities for this cash though not sure where yet!

Good luck with your ongoing holding.

Tricky.

Thanks Tricky. I hope to make the AGM to find out more. Hope you find a good opportunity!

Maynard

System1 (SYS1)

AGM attendance

I attended yesterday’s SYS1 AGM. The following is my best recollection of what was said during the Q&A and pre- and post-meeting chit-chat (mostly paraphrased).

All board members were present and chief executive John Kearon (JK) kindly provided a short presentation before the formal business and the wider Q&A. Four private investors attended including me.

————-

JK claimed AdRatings was the world’s biggest (and most accurate) database for predicting the success of adverts. A “goldmine” of information, with 68,000 ads tested. Project aims to become the “Yougov of advertising data”.

Presentation slides included a demo of AdRatings, showing lots of stats, charts, advert comparisons, etc. Notably the user could play the advert and watch a ‘trace’ showing at what point within the ad the test panel clicked their emotional responses and brand recognitions.

Board would not give any hints as to the timeline for AdRatings success or costs beyond that already disclosed (£2.5m for the current year). I asked JK whether he would be happy if AdRatings was still losing £2m/year in five years’ time — answer: no. So the board does have some sort of ‘success’ timescale in mind (i.e. less than 5 years).

Finance director James Geddes (JG) said the AdRatings ‘investment’ — SYS1’s chairman emphasised the AdRatings expense was an ‘investment’ — was being monitored and decisions would be made as the project progressed and more became known. No pre-defined timescale was set for the project and its assessment.

(My impression: hazy replies from the board suggest AdRatings is taking much longer and costing much more than initially expected.)

Some free trial users of the AdRatings service have become paying subscribers since the year end, but numbers were not revealed and the impression given was the numbers were very low.

JK said AdRatings costs will be covered by a mix of subscriptions and — notably — new business won on the back of Ad Ratings.

(My impression: AdRatings is therefore not a standalone project and could well become another ‘valuable showcase’ (like the Agency division) that loses money for the ‘greater good’ of the group)

JK said the new business wins via AdRatings would be greater initially than the service’s subscription revenue. AdRatings “adds credibility” to SYS1’s services and will be “hugely powerful” in helping convert potential clients into paying customers. Non-exec Jane Wakely (JW) described Ad Ratings as a “door opener” into further client conversations.

JK admitted AdRatings requires further improvements. In particular, interested clients require “validation” — they want to see that market-share changes in their particular advertising category correlate to changes to SYS1’s star ratings for the relevant adverts. SYS1 only has correlation evidence in certain advertising categories. Work is underway to ensure all categories have such validation.

JK claims no-one else has done this correlation within the industry. This correlation should become a crucial selling point to potential clients. The correlation period covers the last two years.

JK claimed AdRatings progress would be “slow, slow, slow, pop” — when things would suddenly take off. Company has to “build up momentum” with client wins.

JK cited AdRatings pricing as a challenge. Potential clients were apparently not interested in the service as the price was “too cheap” — with the implication that the service would be poor.

(My impression: I am not sure this ‘too cheap’ explanation stacks up — many clients have explored the service through a free trial, yet have not paid for a subscription. Perhaps they did not pay because the service was simply not required or not good enough.)

JG claimed the low cost of AdRatings meant the service did not reach the attention of chief marketing officers (CMOs) — who could not justify their time evaluating a £12k/year service. “Needs to be £50k/year to be credible”. Problems with client procurement procedures were also cited as a reason for low trials.

Attracting attention of CMOs appears important. JK explained part of SYS1’s challenge is to change the attitudes of client Insight teams. These teams handle advertising data and (generally) report to the CMO on the effectiveness of their company’s adverts.

JK said CMOs generally accept the benefits of the System1-style of advertising and are open to experiment. Trouble is, their Insights teams are risk-averse and wish to keep using existing suppliers/methods/data rather than throw away years of work and start again using other supplier/methods/data — even though SYS1’s services are simpler.

JK claimed Insights teams typically argue for no change (i.e. an easier life) — which is good news for incumbent ad-services suppliers such as Kantar. SYS1’s chairman mentioned many large organisations suffer from “large inertia” when it comes to marketing change.

Upshot is SYS1 has to make a “compelling case” to CMOs to get them to change the habits of their Insights teams. SYS1 has previously targeted (change-resistant) Insights teams, but is now talking more directly to CMOs.

JW (a Mars CMO) has helped SYS1 put together a “pitch deck” to win over CMOs. JW made the point that analysing System1-type adverts with System2-type data tools (e.g. Kantar) would be ineffective.

(Note: This tweet featuring JW is very enlightening. JW says: “We [Mars] had to very scarily throw out years and years of brand equity research that the organisation was hooked on…” to properly adopt System1-type advertising. To therefore win new clients, SYS1 has to persuade these new clients to “very scarily throw out years and years of brand equity research”. Not easy.)

JW admitted Mars, her employer, did not use SYS1 services due to a “conflict of interest”. JW claimed she applies the System1 philosophy with her Mars work. On reflection I should have asked who Mars used for its ad-testing services.

JK said a golden opportunity to approach a CMO is just after their appointment when they are more open to new ideas. SYS1’s chairman hoped that as younger marketing execs rose through the ranks, old-style methods and incumbents would be more likely to be dislodged as new bosses would look at marketing differently. However, dislodging the likes of Kantar, which apparently are entrenched throughout the marketing departments of many large businesses, would be slow.

I was pleased that JK admitted SYS1 needed to raise its own “fame, feeling and fluency” in winning clients. The company has historically concentrated on research development, and is now “learning on commercialisation”.

The appointment of Stefan Barden (SB) has helped. SB works only two days a week but JK said he is a “machine” (SB is an accomplished triathlete) and is “brilliant”. SB works on the company’s “process, structure and rhythm” — making sure everything works like clockwork. I had no time to ask about SB’s LTIP.

JK said the cost of testing an ad:

* Adhoc client: £3k, then £6k for further creative guidance.

* Regular client: £1k, then £4k for further creative guidance.

Margins on ad testing/guidance are apparently “on the up” despite lower prices because the associated testing costs have reduced.

(Note: I did not realise the testing could cover scripts and early-stage animations/versions of adverts. Adjustments are made to the star ratings if the advert is not the final broadcast version.)

150 people per test are used to form a “nationally representative” sample. Products purchased by a particular gender still have a mixed male/female panel. The results are more predictive with mixed panels.

AdRatings could soon offer clients the ability to upload an advert and pay for a test — with the results received a day later including a full comparison to other ads in the same category. JK hoped this upload facility could become very popular.

JK hoped ad agencies could help SYS1 win business. Ad agencies “hate” old-style ad-testing services such as Kantar, as their research/conclusions never seem to value the creativity of the ad and just pick faults (e.g. logo is too small). Agencies are beginning to recognise SYS1’s research places greater value on the ad’s creativity and SYS1 hopes the agencies can now recommend SYS1 to clients.

Summary

A useful meeting with no ground-breaking developments revealed.

From what I can tell, SYS1 needs the following to progress:

* hope new CMOs are open to change;

* approach CMOs directly with a more compelling pitch that can persuade their Insights teams to accept new data/tools etc;

* Develop the validation data within AdRatings that proves industry market-share changes correlate to SYS1 ratings verdicts, and;

* Perhaps work more with ad agencies to encourage referrals.

Plus, the AdRatings project is an investment to grow the wider business rather than a standalone operation that (in theory) could be scrapped. The associated costs should therefore not be ignored.

Maynard

System1 (SYS1)

Trading Update

This update was issued during October:

——————————————————————————————————————

System1, the marketing services group, issues the following update on trading for the six months to end-September 2019. The Company will announce its interim results on 7 November 2019.

The first half of the current year (H1) saw Gross Profit (our main top-line performance indicator) growing modestly. Gross Profit for the half-year is expected to be some 7% above the comparable 2018/19 period (4% at constant exchange rates).

Operating Costs were well controlled, benefiting from our ongoing drive to increase efficiency across the business. Excluding investment in AdRatings (the Company’s database of advert ratings), Operating Cost growth was some 3%.

Normalised H1 Pre-tax profits, excluding AdRatings and share based payments, are expected to be some £2.4m, approximately 24% higher than in the comparable period.

A total of £1.2m, modestly below budget, was invested in further expanding our AdRatings asset during H1. System1’s financial position remains strong. Despite continued relatively high levels of investment and the payment of the 2018/19 final dividend during H1, the period-end cash balance was £4.1m, compared with a cash balance of £4.3m at the end of March 2019. System1 has no debt.

As well as ongoing investment in AdRatings, the Company continues to invest in its IT infrastructure and data capability. System1 also strengthened its senior management team during the first half. Key new hires include a Chief Commercial Officer (Karen Wolfe, formerly at Nielsen) and a Chief Marketing Officer (Jon Evans, formerly at Lucozade Ribena Suntory), both of whom joined System1 towards the end of the half year.

——————————————————————————————————————

Maynard