***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

17 May 2026

By Maynard Paton

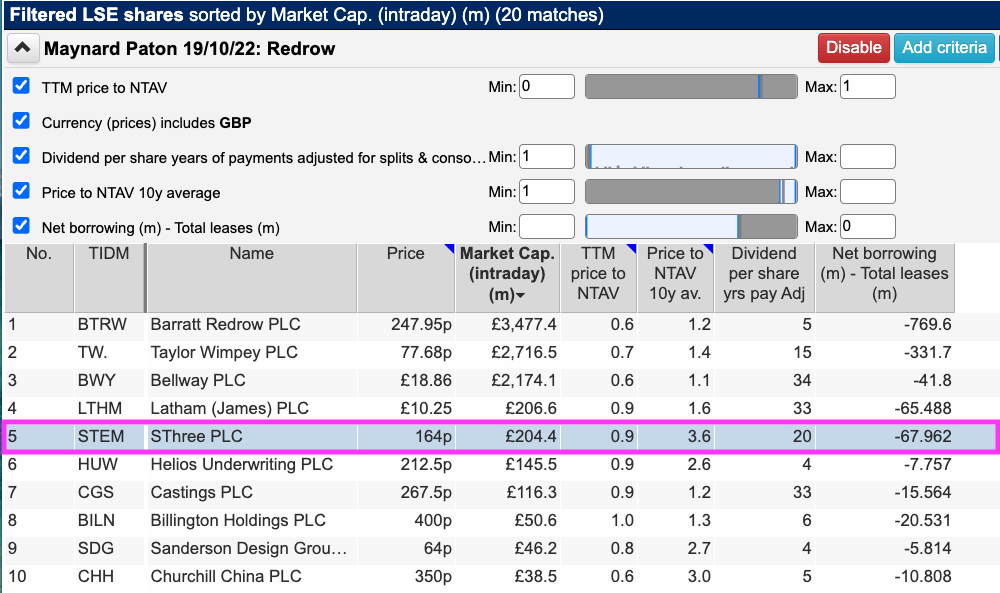

I am once again looking for ‘value bargains’ and revisiting a screen that identifies companies trading at less than book value.

Importantly, this screen attempts to avoid ‘value traps’ by demanding the shares offer net cash, dividend payments and a history of trading above book value.

The exact filter criteria I redeployed were:

- A price to net tangible assets of no more than 1;

- A dividend being paid during the most recent year;

- A 10-year average price to net tangible assets of at least 1;

- Net borrowings less total leases of no more than 0 (i.e. a net cash position excluding IFRS 16 lease obligations), and;

- A share price denominated in pounds sterling.

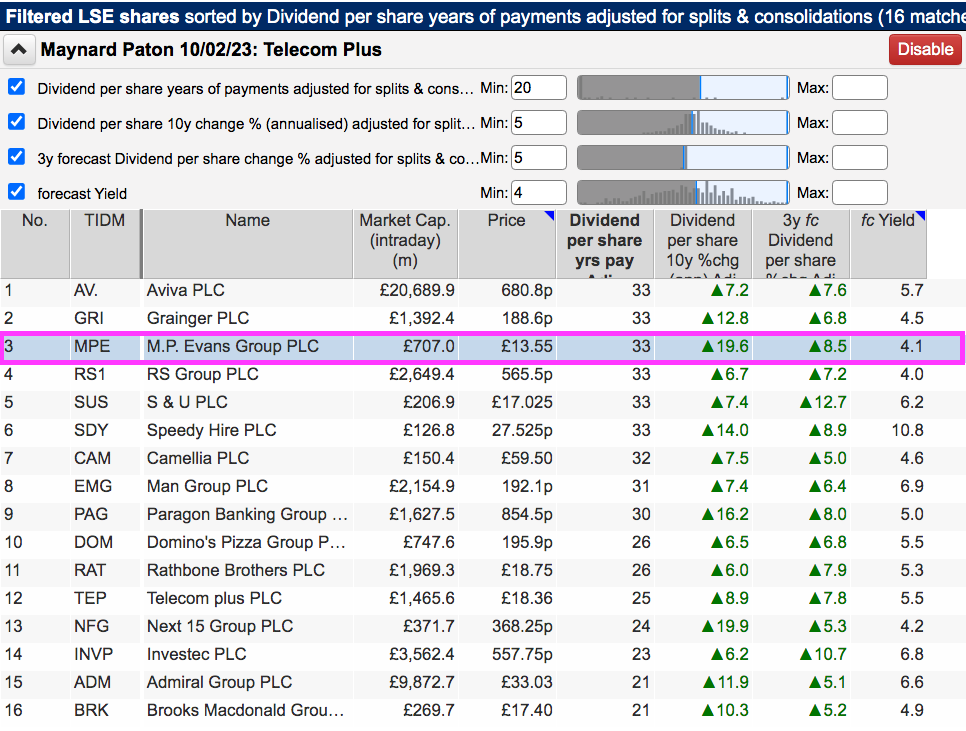

This time ShareScope returned 20 companies:

I selected SThree because I was very surprised to discover this recruitment agency was trading below book value alongside asset-heavy shares such as house builders.

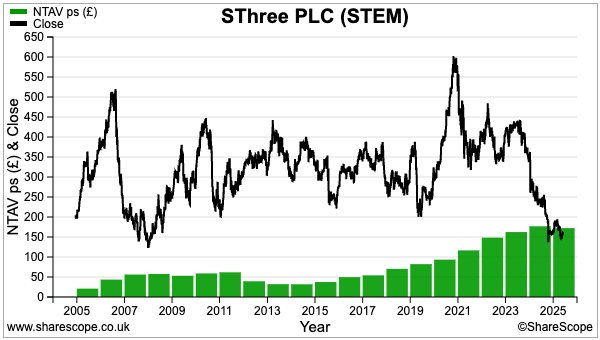

But sure enough, SThree’s 164p shares were priced a fraction less than the group’s 172p per share net tangible asset value:

I see the shares have in the past traded at beyond 5x net tangible value.

Let’s take a closer look.

Read my full STHREE article for ShareScope >>Maynard Paton