28 June 2019

By Maynard Paton

Happy Friday! I hope you continue to find my Blog useful… and that your shares are performing well in the current market.

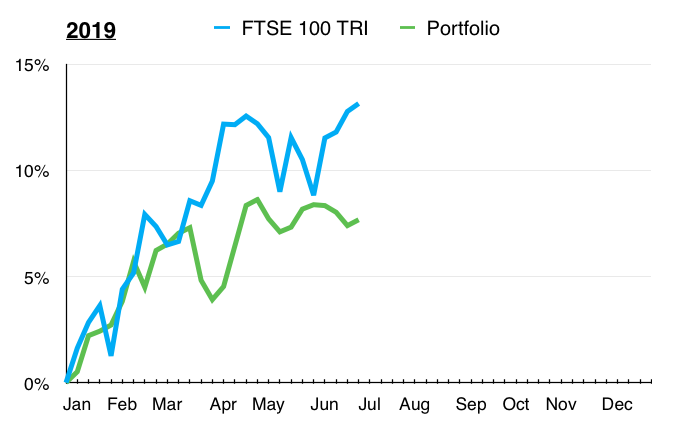

I am pleased my portfolio remains in positive territory this year — although I am still trailing the FTSE 100. So far during 2019, I am up 7.7% while the index is up 13.1%.

My underperformance is due in part to owning companies that are:

- undergoing potential recoveries (Getech, Oleeo, System1 and Tasty);

- experiencing flat earnings (Mincon and M Winkworth), or;

- operating in an unloved sector (Daejan and Mountview Estates).

Those eight shares represent approximately 40% of my portfolio. Add in cash of 7.5% as well, and almost half of my portfolio is marooned far away from the high-flying ‘quality’ growth shares that (seemingly) keep leading the market higher.

Anyway, let me now explain what has happened within my portfolio during April, May and June. (Please click here to read all of my previous quarterly round-ups.)

Contents

Q2 share trades

I made four share trades during the second quarter. I sold my entire Castings stake and bought more Daejan, Mountview Estates and S&U.

Castings

I sold my entire Castings holding during early April at 343p including all costs. My 2018 portfolio review mentioned a desire to shift to higher-conviction positions and Castings was simply a casualty of wanting to own fewer shares.

True, Castings offers a long dividend history, an LTIP-free board and cash-flush accounts. But so do other shares in my portfolio — and those alternatives boast long-haul family managers, too.

Furthermore, Castings remains dependent on three large customers, has re-jigged its depreciation charge to improve profits, and has suffered machining-division problems that may require another few years to properly resolve.

A trading statement issued after I sold revealed the engineer had (frustratingly!) enjoyed “strong demand” during the second half and that the firm’s 2019 results would come in ahead of expectations. However, Brexit-related stock-building accounted for some of the out-performance.

I bought Castings during September 2015 at 426p, then collected dividends of 76p per share and sold at 343p — leading to a 1.6% loss over three-and-a-half years. I will endeavour to recount this underwhelming investment in more detail later this year.

I should add that Castings is only the fifth share since 2004 on which I have suffered a loss after completely selling out.

The proceeds from Castings were reinvested in the following shares:

Daejan

I increased my Daejan holding by 20% at £56 including all costs. The commercial-property group revealed in November its net asset value (NAV) had climbed to £116 per share, and yet the share price has drifted lower (due in part to boardroom diversity issues) and allowed the discount to NAV to widen to 50%. Such a valuation has typically rewarded (very) patient investors.

Mountview Estates

I increased my Mountview Estates holding by 10% at £99 including all costs. At the time of my purchase, the regulated-tenancy landlord sported an NAV of £92 per share (since lifted to £94 per share) — although my sums suggest the firm’s properties could be worth more than £200 per share. A yield of 4% also seems attractive based on historical valuations — albeit again for (very) patient investors.

S&U

I increased my S&U holding by 100% at £19 including all costs. The motor-finance specialist issued satisfactory annual figures during March, although the double-digit earnings and dividend advances were counterbalanced by a greater increase to bad loans. My calculations at the time of purchase signalled a P/E of less than 11 and a yield greater than 6%

A subsequent trading statement then suggested the increasing bad loans had started to moderate.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Q2 portfolio news

As usual I have studied all the statements issued by my holdings. The Q2 developments are summarised below:

- Satisfactory progress at Andrews Sykes;

- Acceptable figures from Mountview Estates and M Winkworth;

- Reassuring news from S&U;

- Mixed updates from City of London Investment, Mincon and System1;

- Confirmation of a £3.25m rescue fund raising at Tasty.

As well as evaluate RNSs, I always review the latest annual reports of my holdings — just in case some nasty small-print was not published within the initial results announcement.

I have not unearthed anything too sinister during the last three months, but a few interesting snippets did emerge:

- A 90% shareholder may not be so bad for Andrews Sykes: “The presence and requirements of a longstanding majority shareholder has resulted in a strategy with the key aim of creating long-term shareholder value.”

- A stirring ‘only-the-paranoid-survive’-type message from Mincon: “If we do not work to make our current range of products redundant by developing new, better products, we can rely on our competitors to do this.”

- A six-month 41% loss on quoted investments at M Winkworth:

- A 21-year stint for Deloitte as auditor of S&U:

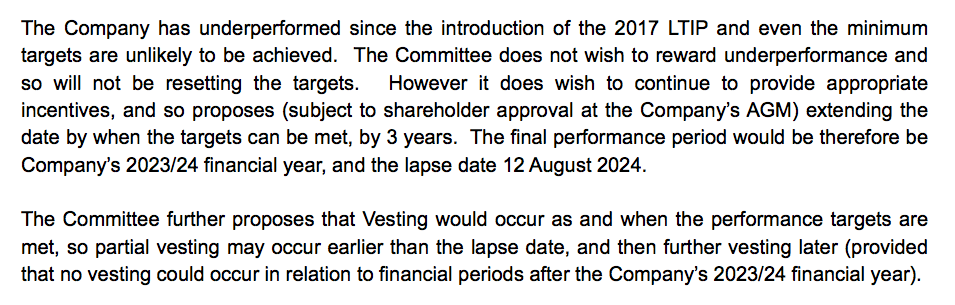

- System1 admitting it had “underperformed” and therefore would extend its 2017 LTIP scheme by three years:

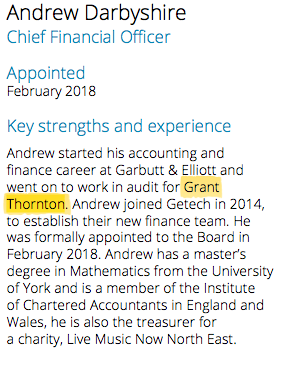

- The finance director of Getech being revealed as having worked in audit for Grant Thornton (of Patisserie Valerie fame):

Q2 portfolio returns

The chart below compares my portfolio’s weekly 2019 progress (in green) to that of the FTSE 100 total return index (in blue):

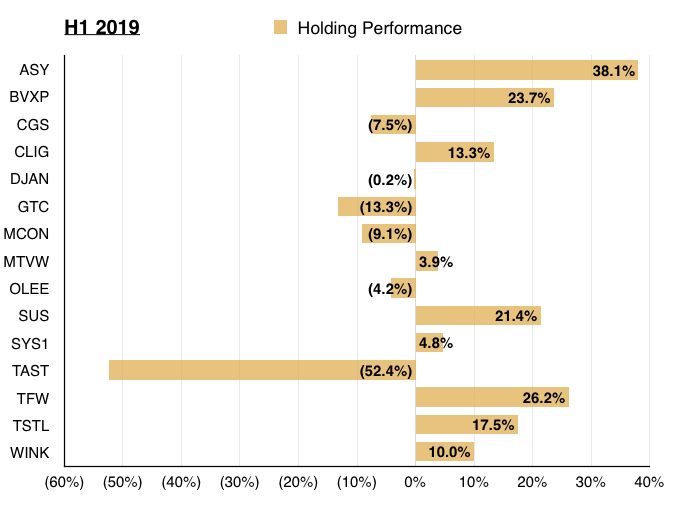

This next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me year to date:

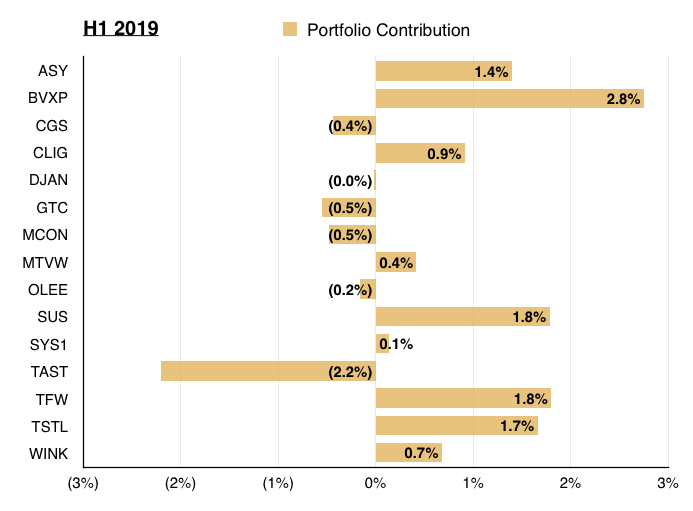

Meanwhile, this chart shows each holding’s contribution towards my overall 7.7% gain:

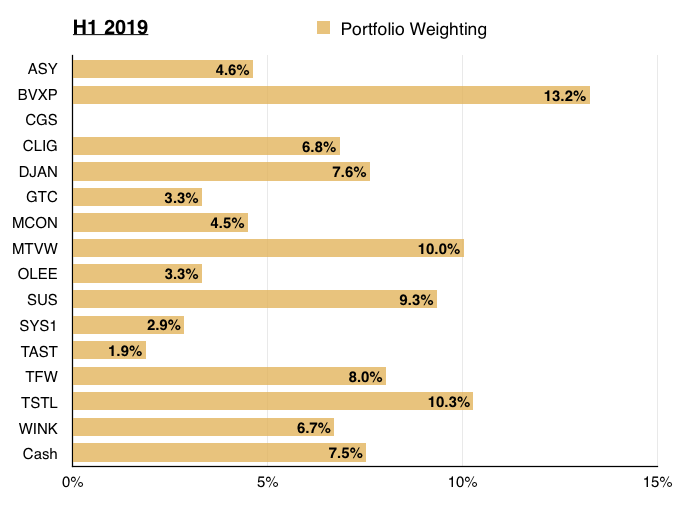

And this chart shows my portfolio’s holdings and their weightings at the end of Q2:

Portfolio analysis the Fundsmith way

If I ever become fed up with picking shares, Terry Smith may well receive my money. His Fundsmith portfolio offers a simple three-step investing strategy:

- buy good companies;

- don’t overpay, and;

- do nothing.

Successful investing can be that easy — Mr Smith’s fund has trounced the FTSE 100 (blue line) since its launch during 2010:

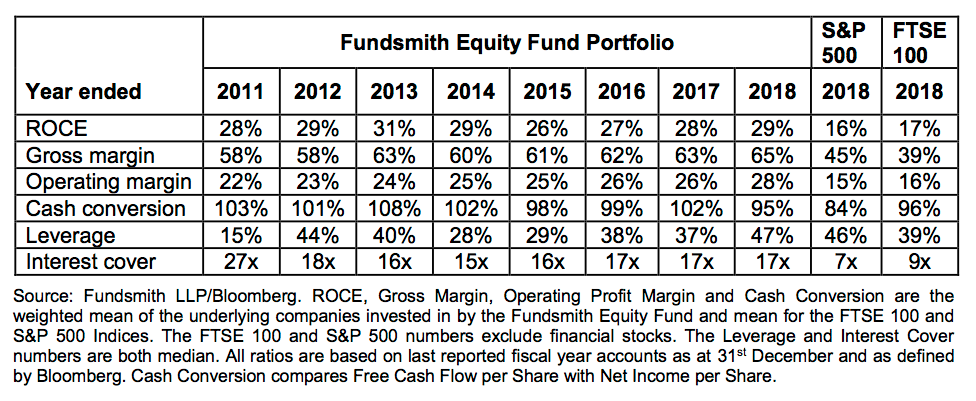

Mr Smith includes some fascinating statistics within his annual fundholder letters. In particular, he compares the operating/accounting quality of his Fundsmith portfolio to that of two popular indices:

Mr Smith analyses his portfolio as if it were a single company. He believes Fundsmith ought to perform well if its holdings collectively offer better quality — and perhaps a cheaper valuation — than the wider markets.

Ace SharePad writer Richard Beddard has already measured his Share Sleuth portfolio against Mr Smith’s theory — and scored very well. Let’s see how my portfolio shapes up.

The middle-ground between Fundsmith and the FTSE

This first table shows the Fundsmith ratios for each of my shares.

| Share | ROCE (%) | Gross margin (%) | Operating margin (%) | Cash conversion (%) | P/E | Yield (%) |

| Andrews Sykes | 34.7 | 59.4 | 26.3 | 70.4 | 16.3 | 3.6 |

| Bioventix | 64.8 | 93.4 | 78.9 | 103.3 | 34.3 | 1.6 |

| City of London Inv | 63.5 | 93.2 | 36.9 | 120.7 | 10.7 | 6.5 |

| Daejan | 8.9 | 46.5 | 37.2 | 17.7 | 4.6 | 1.8 |

| Getech | 3.3 | 47.2 | 5.6 | (199.0) | 15.9 | - |

| M Winkworth | 26.5 | 74.1 | 22.9 | 134.8 | 13.2 | 6.2 |

| Mincon | 13.3 | 38.6 | 13.9 | (81.6) | 18.0 | 0.9 |

| Mountview Estates | 9.6 | 61.7 | 53.9 | (9.3) | 12.6 | 4.1 |

| Oleeo | 4.7 | 100.0 | 4.7 | (39.0) | 31.4 | 2.2 |

| S & U | 14.3 | 56.4 | 43.8 | 34.8 | 10.2 | 5.0 |

| System1 | 21.6 | 82.5 | 7.4 | 152.2 | 24.9 | 3.2 |

| Tasty | (2.2) | 1.9 | (0.8) | 88.4 | - | - |

| FW Thorpe | 17.3 | 46.8 | 17.8 | 79.5 | 22.2 | 1.7 |

| Tristel | 23.2 | 77.3 | 17.9 | 72.7 | 32.6 | 1.5 |

| Cash | - | - | - | - | - | - |

(Note: Data as at 31 May 2019. All ratios extracted from SharePad except S&U, the ratios for which were calculated from the 2019 annual report.)

I have ignored Fundsmith’s Leverage and Interest Cover ratios because ten of my fourteen companies last reported net cash positions. I am therefore confident my portfolio is more conservatively financed than the wider market (and probably Fundsmith, too).

I have also replaced FundSmith’s free cash flow yield with dividend yield. Four of my shares last reported negative free cash flow, and I am not convinced about the arithmetic when determining my portfolio’s overall free cash figure. Dividend yield is far more straightforward in this respect. I have added the trailing P/E measure, too.

This next table compares my portfolio to Fundsmith and the FTSE 100:

| Share | ROCE (%) | Gross margin (%) | Operating margin (%) | Cash conversion (%) | P/E | Yield (%) |

| My portfolio | 25 | 62 | 32 | 47 | 17.8 | 2.75 |

| Fundsmith | 29 | 65 | 28 | 95 | 23.8 | 1.57 |

| FTSE 100 | 17 | 39 | 16 | 96 | 15.5 | 4.52 |

(Note: Fundsmith and FTSE 100 data from Fundsmith as at 31 December 2018.)

My portfolio’s return on capital employed (ROCE), gross margin and operating margin are all greater than that of the FTSE 100.

However, my portfolio’s cash conversion is well below that of the index. I am not sure whether my free cash ‘absorbers’ have skewed this calculation disproportionately.

Mind you, Getech, Mincon, Mountview Estates and Oleeo did indeed produce negative cash flow last year, and improvements are certainly required at Getech and Mincon.

I am not too surprised my portfolio lags behind Fundsmith on ROCE.

Suffice to say, Mr Smith has been much happier than me to pay higher valuations for top-quality businesses such as Microsoft and Facebook. In contrast, I have tried to pay modest valuations for respectable — but not truly outstanding — companies.

I should add that my portfolio’s 32% operating margin — which is four percentage points higher than that of Fundsmith — is due mostly to the stratospheric profitability of Bioventix. I estimate the 32% would be 22% without the antibody group.

Turning to valuation, my portfolio is rated less highly than Fundsmith but is more expensive than the FTSE 100. That middle-ground rating seems about right given my portfolio sits in the ‘quality’ middle-ground between Fundsmith and the market.

By striking a balance between quality and valuation, I am hopeful my portfolio can outrun the FTSE index. To outrun Fundsmith, I perhaps need to invest in higher-quality businesses — but pay less for them than Mr Smith does. That may be tough going when ‘quality’ growth shares continue to attract premium valuations.

Until next time, I wish you happy and profitable investing.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Daejan, Getech, Mincon, Mountview Estates, Oleeo, S&U, System1, Tasty, FW Thorpe, Tristel and M Winkworth.

Really thoughtful honest and transparent report

Thanks very much for your latest portfolio update Maynard. I was interested to hear your comment that if you ever became fed up with picking shares then Terry Smith might end up managing your money as I would agree that he is one of the best fund managers around. I never became fed up of picking shares but I did realise that it was difficult for me to beat the very best fund managers. I would describe the best fund managers as those with clearly stated philosophies which are rational and easy to understand and which have, to a greater or lesser extend, a formulaic (and therefore reproducible) approach to selecting shares and with performance records which suggests that their approaches works. In my opinion, Terry Smith, Nick Train and Keith Ashworth-Lord are such fund managers and there are of course similarities in their approaches. I use a hybrid approach to managing my money by using the stock picks, ideas and philosophies of these managers to buy companies directly thereby avoiding the management/admin fees and giving me the satisfaction of running my own portfolio. Importantly, I also use their philosophies to buy some shares which are too small, too illiquid or otherwise beyond the remit of these fund managers. For example, like you, I have owned Andrew Sykes for a number of years. I also have personal experience of the biotech sector and have combined this with the ideas of these fund managers to select a few companies in this sector (yes there are a few companies like this in the US!). I also invest directly in the flagship funds run by these managers not only because they fairly deserve some fees but also to get exposure to their foreign non-US investments which would be more expensive for me to hold directly because of the foreign exchange cost and witholding taxes if dividends are paid. However, I do hold some of their US companies directly in my SIPP because of the remarkable fact that the US IRS allows tax benefits on dividends even for foreign investors. As you might imagine, this approach, which I started around 2010 (adding the Fundsmith and Buffetology philosophies later) has produced a decent return. I hope you don’t ever get fed up of picking shares yourself as I find your insights interesting and valuable but if you do, I would certainly recommend considering the above approach.

Hi John

Thanks for the comment.

I don’t think I will ever become fed up with picking shares, but sometimes I do wonder whether the effort is worth it when hands-off investors in Fundsmith etc have done so well. One day the current tide may turn. I have avoided paying high-ish multiples for ‘quality’ shares as I have always felt investment gains are often supercharged by P/E re-ratings, and a P/E expanding from 10 to 15 is more likely than a P/E expanding from 20 to 30, or from 30 to 45. At least that’s what I thought. I bought Bioventix on a P/E of 17 a few years ago, and that sort of mix of business quality/valuation is hard to find at present.

I use a hybrid approach to managing my money by using the stock picks, ideas and philosophies of these managers to buy companies directly thereby avoiding the management/admin fees and giving me the satisfaction of running my own portfolio.

Yes, this is a good approach — cherry-picking your favourite ideas. I do occasionally look at what Fundsmith etc has bought. The ace fundhunter.co website keeps me informed of what Smith, Buffettology etc are buying. I have to admit I like to dig for my own independent ideas rather than coat-tail other people.

Maynard

Hi Maynard

Always a pleasure to read your updates. What’s your outlook on Tasty after the rescue fund raising? Lost cause or do you think there are any silver linings?

Eric

Hi Eric

Tasty — could very well be a lost cause. But I recall from the results that silver linings included better staff productivity, so management has made some changes that may one day lead to profitable margins. So perhaps all is not lost. Company appeared to say a recovery was dependent on the sector/economy improving, which is not great. At least the balance sheet is shored up for now. Likely outcome in the foreseeable future is the share being ‘dead money’ until a decisive change in trading occurs (hopefully positive).

Maynard