18 April 2019

By Maynard Paton

Results verdict on M Winkworth (WINK):

- Collecting a greater proportion of franchisee estate-agent income supported an acceptable rate of growth.

- Subdued sector conditions likely to persist until “relative [political] stability” emerges.

- Further market-share gains won from London rival Foxtons, while threat of online competition continues to subside.

- Accounts still exhibit high margins, a cash-flush balance sheet and appealing returns on equity.

- P/E of 11 and yield of 6% do not appear expensive should earnings resume their momentum. I continue to hold.

Contents

- Event links and share data

- Why I own WINK

- Results summary

- Revenue, profit and dividend

- First half versus second half

- Foxtons comparison

- Online competition

- Financials

- Valuation

Event links and share data

Event: Final results and annual report for the twelve months to 31 December 2018 published 03 April 2019.

Price: 125p

Shares in issue: 12,733,328

Market capitalisation: £15.9m

Why I own WINK

- Operates a London estate-agency franchising business, where progress is dependent on experienced, entrepreneurial and motivated franchisee owner-managers.

- Franchising model leads to high margins, attractive equity returns, low capital requirements and generous cash flow.

- Seasoned family management boasts £6m/50% shareholding and rewards shareholders through resilient quarterly dividends and occasional special handouts.

Further reading: My WINK Buy report |All my WINK posts | WINK website

Results summary

Revenue, profit and dividend

- September’s satisfactory interims and January’s trading statement had already indicated these full-year numbers would reveal acceptable progress.

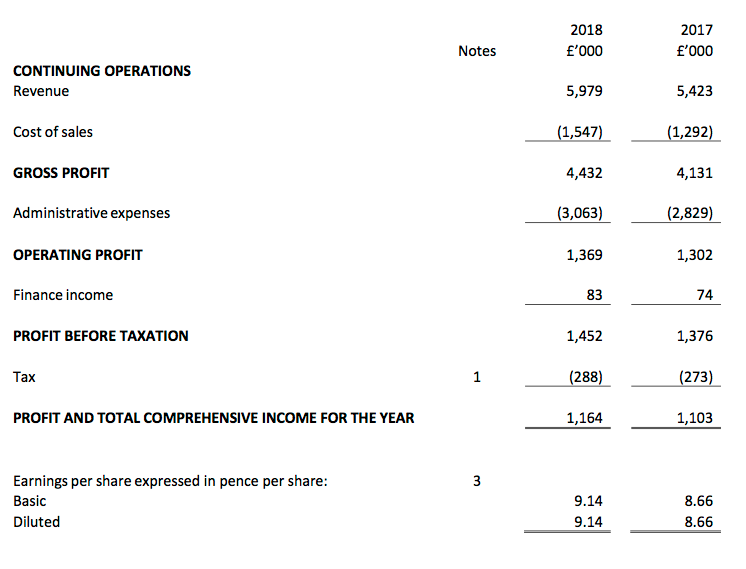

- Revenue gained 10% while operating profit advanced 5%:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Gross Franchisee Sales & Lettings (£k) | 50,100 | 49,010 | 46,120 | 46,200 | 46,500 |

| Revenue (£k) | 5,495 | 5,865 | 5,566 | 5,423 | 5,979 |

| Operating profit (£k) | 1,840 | 1,817 | 1,346 | 1,302 | 1,369 |

| Finance income (£k) | 86 | 90 | 71 | 74 | 83 |

| Other items (£k) | - | - | - | - | - |

| Pre-tax profit (£k) | 1,926 | 1,907 | 1,417 | 1,376 | 1,452 |

| Earnings per share (p) | 11.83 | 11.95 | 8.84 | 8.66 | 9.14 |

| Dividend per share (p) | 6.20 | 6.50 | 7.20 | 7.25 | 7.45 |

| Special dividend per share (p) | - | 1.80 | - | - | - |

| Return of capital per share (p) | - | - | - | - | 9.00 |

- Revenue reached a new record although operating profit was well below the £1.8m level of 2014 and 2015.

- Revenue improved mostly because WINK took a greater share of the income earned by its network of franchisee estate agents.

- WINK’s network of franchisees generated gross sales of £46.5m, of which 12.9% went to WINK:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Gross Franchisee Sales & Lettings (£k) | 50,100 | 49,010 | 46,120 | 46,200 | 46,500 |

| Revenue (£k) | 5,496 | 5,865 | 5,566 | 5,423 | 5,979 |

| Revenue/Gross Franchisee Sales & Lettings (%) | 11.0 | 12.0 | 12.1 | 11.7 | 12.9 |

- Franchisees pay WINK 8% of all commissions/letting income received as well as variable contributions towards advertising and IT services. Franchisees also pay WINK for any landlords and tenants introduced by the company.

- WINK’s management cited the “uncertainties brought about by various stamp duty changes, Brexit, pending withdrawal of tenant fees, and changes in taxation in the rental market” as continuing to stifle London’s property market.

- 81% of revenue from WINK’s franchisees is through London-based branches.

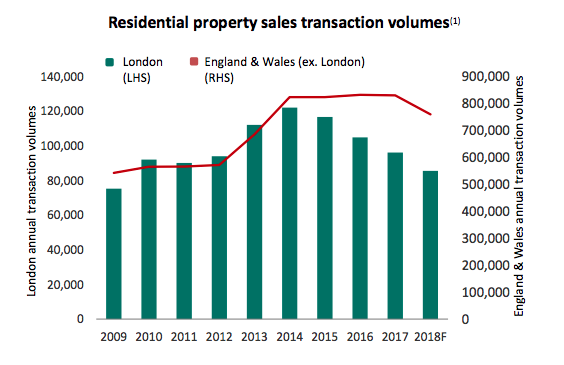

- According to rival Foxtons (FOXT), the number of property transactions in the capital has declined during the last four years (green bars, left axis) and is now at half the level seen during 2007:

- WINK’s quarterly dividend declarations had already signalled a record 7.45p per share payout for 2018.

- The Q1 2019 payout announcement of 1.9p per share suggests the dividend will advance at least 2% to 7.6p per share during the current year.

First half versus second half

- These results showed WINK achieving a long-held target of increasing lettings-related income to match the income earned through property sales.

- During the second half, lettings-related income from franchisees exceeded property-sales income for the very first time:

| Gross Franchisee Revenue | H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | |

| Sales (£m) | 11.7 | 13.1 | 24.8 | 10.8 | 12.6 | 23.4 | |

| Lettings (£m) | 9.7 | 11.6 | 21.3 | 10.3 | 12.8 | 23.1 | |

| Total (£m) | 21.4 | 24.7 | 46.2 | 21.1 | 25.4 | 46.5 |

- Although WINK’s H2 revenue gained 10%, H2 profit advanced only 3%:

| H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | ||

| Revenue (£k) | 2,544 | 2,879 | 5,423 | 2,798 | 3,181 | 5,979 | |

| Operating profit (£k) | 507 | 795 | 1,302 | 551 | 818 | 1,369 |

- The accounting small-print revealed a minor £32k write-off (point 10) that would otherwise have seen H2 profit gain 7%.

Foxtons comparison

- WINK said: “In this low transactional market we outperformed our peers and grew market share, improving our ranking to second for properties exchanged in London and third in listings, a reflection of our efficiency at selling the properties we list.”

- WINK continues to outperform London-rival FOXT, which claims to enjoy the “Number 1 market position and brand awareness in London estate agency”:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Winkworth | |||||

| Gross Franchisee Sales Revenue (£m) | 32.6 | 30.1 | 26.0 | 24.8 | 23.4 |

| Gross Franchisee Lettings Revenue (£m) | 17.5 | 18.8 | 20.1 | 21.3 | 23.1 |

| Total Gross Franchisee Revenue (£m) | 50.1 | 49.0 | 46.1 | 46.2 | 46.5 |

| Foxtons | |||||

| Sales Revenue (£m) | 69.8 | 72.5 | 55.5 | 42.6 | 36.2 |

| Lettings Revenue (£m) | 67.4 | 69.0 | 68.3 | 66.3 | 67.0 |

| Total Sales & Lettings Revenue (£m) | 137.2 | 141.5 | 123.8 | 108.9 | 103.2 |

| Winkworth / Foxtons | |||||

| Sales Revenue (%) | 46.7 | 41.5 | 46.8 | 58.2 | 64.6 |

| Lettings Revenue (%) | 26.0 | 27.2 | 29.4 | 32.1 | 34.5 |

| Total Revenue (%) | 36.5 | 34.6 | 37.3 | 42.3 | 45.1 |

- During 2014, WINK’s total franchisee revenue represented 36.5% of FOXT’s property sales and lettings revenue.

- Last year, the proportion had increased to 45.1% — with 46.6% witnessed during H2.

- The FOXT comparison is not strictly like-for-like, as FOXT generates almost all of its revenue from branches within London while WINK generates 81%.

- Still, WINK’s self-employed franchisees appear to be handling London’s stagnant property market better than FOXT’s conventional employees.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Online competition

- Recent industry developments suggest the threat of online disruption is receding.

- The informative Property Industry Eye has recently published the following articles:

- High street agents seeing off online rivals in battle for market share

- I was wrong: Russell Quirk admits online agency is ‘too cheap’ to work

- Online agent House Network ceases trading

- Former Local Property Expert spills the beans on his time with Purplebricks

- Online agents commanding under 5% of market – and Purplebricks way out in front

- That final article refers to this LinkedIn blog by Gavin Brazg and contains this chart:

- According to Mr Brazg, new listings on Zoopla from online estate agents (OEAs) have consistently represented a fraction of new listings from high street estate agents (HSEAs).

- Not exactly ‘disruption’ just yet.

- Almost three years ago I pondered: “It is not clear to me whether an online agent or a hybrid agent such as Purplebricks (PURP) will sell your home more conveniently, efficiently and quickly than a traditional agent. Selling your house of course means having the buyer’s cash in the bank, not just a verbal offer at your asking price.”

- I remain generally sceptical of the online/hybrid approaches employed by Purplebricks and other estate agents.

Financials

- WINK’s accounts remain in good shape.

- Margins and returns on equity have been kept high:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating margin (%) | 33.5 | 31.0 | 24.2 | 24.0 | 22.9 |

| Return on average equity (%)* | 87.0 | 71.2 | 49.5 | 48.5 | 62.2 |

(*adjusted for net cash and investments)

- WINK’s operating margin has declined during the last few years, due mostly to the additional cost of extra employees:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (£k) | 5,496 | 5,865 | 5,666 | 5,423 | 5,979 |

| Employee costs (£k) | 1,295 | 1,528 | 1,492 | 1,600 | 1,784 |

| Employees | 27 | 34 | 32 | 33 | 33 |

| Employee costs/Revenue (%) | 23.6 | 26.1 | 26.8 | 29.5 | 29.8 |

- The extra staff investment helped fund new departments that introduce landlords and tenants to franchisees.

- During 2018 these departments generated the participating franchisees revenue of £1m — although the proportion of that £1m WINK took as commission was not disclosed.

- Management told me at the 2016 AGM that WINK would charge “15%/20% plus the standard 8% fee” on business delivered through the new departments.

- So maybe WINK collected c£250k from the £1m, which spread over perhaps six staff does not leave much room for any profit.

- The group’s lower operating margin supports the notion that the profitability of the new departments is small.

- WINK reckoned margins could improve: “Even a modest upturn in sales volume, or increased market share following competitors’ closures, will feed through to increased profits. Our cost base is closely contained, which means that top line improvements feed straight through to the bottom line.”

- However, revenue climbed 10% during 2018 but the operating margin decreased — suggesting top-line improvements may not always feed entirely to the bottom line.

- WINK added: “For our shareholders, our priority is to increase the dividend steadily and maintain a strong balance sheet.”

- The balance sheet is indeed strong.

- Cash and investments finished 2018 at £3.0m (23p per share). Start-up loans to franchisees were £1.0m (8p per share).

- The balance sheet carries no debt and no pension obligations.

- Finance income during 2018 came to £83k — a notable 6% of pre-tax profit.

- Assuming cash in the bank earned 1%, the interest rate on the start-up money lent to franchisees was 5%.

- Cash flow appeared sound:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating profit (£k) | 1,840 | 1,817 | 1,346 | 1,302 | 1,369 |

| Depreciation and amortisation (£k) | 244 | 275 | 368 | 246 | 270 |

| Net capital expenditure (£k) | (237) | (108) | (250) | (247) | (189) |

| Working-capital movement (£k) | (878) | (195) | (145) | 567 | (56) |

| Net cash and investments (£k) | 2,513 | 3,175 | 2,979 | 3,586 | 2,988 |

- Expenditure on tangible and intangible items continues to be covered by the depreciation and amortisation charged against earnings.

- Working-capital movements were favourable during H2 and reversed the significant unfavourable movement of H1.

- Additional cash absorbed by WINK’s working capital often represents start-up loans to new franchisees.

Valuation

- WINK presented a mixed 2019 outlook.

- Any increase to London property transactions is apparently dependent on a period of “relative [political] stability”.

- However, “strong levels of demand” are expected for lettings.

- WINK added that its lettings division will this year see “a minor negative impact from the well-publicised change in tenant fees”.

- The 2018 operating profit of £1.4m less tax at the standard 19% gives earnings of £1.1m or 8.7p per share.

- A market cap of £15.9m less cash/investments of £3.0m and franchisee loans of £1.0m gives an enterprise value of £11.9m, or 94p per share.

- Dividing the 94p per share enterprise value by the 8.7p per share earnings guess gives an underlying multiple of 11.

- The 11x rating does not look expensive, but earnings for 2016, 2017 and 2018 were lower than those reported for 2013, 2014 and 2015.

- Profit retained by the business since 2015 has therefore not created any obvious value to date.

- But WINK has reinvested at high rates in the past.

- During the five years to 2015 for example, earnings improved by £0.7m after £3.3m was added to the equity base. The resultant incremental return on equity was £0.7m / £3.3m = 22%.

- Were WINK to ever repeat such reinvestment returns, the present P/E offers scope for a positive re-rating.

- In the meantime, the prospective 7.6p per share dividend is covered 1.2x by 2018 earnings and offers a 6% yield.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in M Winkworth.

M Winkworth (WINK)

Publication of 2018 annual report

Full marks for WINK for publishing its annual report alongside the results RNS.

Here are the snippets of interest:

1) Corporate governance

New AIM rules introduced during 2018 have prompted WINK to beef up its corporate-governance reporting:

The annual report refers readers to the group’s website: http://www.winkworthplc.com/corporate-governance

Some titbits of website info that reveal:

* WINK’s plans to remain competitive:

* a competitive advantage essentially based on a reputation for high-quality service:

Plus this on the AGM:

I attended the 2016 AGM and was not made to feel entirely welcome.

2) Directors’ report

The directors’ report has also been enhanced.

Shareholders are now told how many board meetings the directors attend (which is standard for companies on the main market):

The non-execs work 15 days a year:

3) Risks

WINK has recognised three additional risks:

Brexit goes without saying.

Risks involving franchisee recruitment and brand reputation underline the corporate-governance notes (point 1 above) that tip-top service is vital for the business.

4) Audit

A new note within the Audit section:

See point 8 below.

5) IFRS 16

Credit to WINK for providing some figures for the impending introduction of IFRS 16 and changes to the reporting of lease commitments:

The overall effect is immaterial.

6) Employees

As noted in the Blog post above, additional employees and associated costs have reduced the group’s operating margin during the last few years.

During 2018, the average employee cost £54k (vs £48k for 2017), the highest since 2013.

Revenue per employee was a useful £181k (vs £164k for 2017), the highest since 2014.

7) Director pay

The chief exec’s total pay dropped by £25k — he appears not to have collected as large a bonus this time:

Board pay overall does not look ridiculous.

8) Trade receivables

This note is worth monitoring following the extra audit note (see point 4 above):

For 2018, trade receivables of £591k represented 9.9% of revenue — in line with the 9.1%-11.5% seen during the prior five years.

However, the £301k of not-due receivables represented only 50.9% of all receivables — the lowest proportion bar 2013 (54%) since 2008.

In other words, 49.1% of all (year-end) receivables for 2018 were overdue. The corresponding figure for 2017 was 37.3%.

WINK has historically not suffered significant bad debts, but I would understand if some of the smaller franchisees are finding the going tough at present.

9) Franchisee loans

The same receivables note shows the loans issued to franchisees:

The total outstanding comes to just over £1m.

10) Investments

WINK appears to have dabbled in some shares during H2 2018:

£78k was invested and £32k (41%) has already been written off.

The cash flow statement confirms the £32k was expensed against profits:

What were the chosen shares? Purplebricks? Countrywide?

11) Subsidiaries

The Blog post above mentions new departments for introducing tenants and landlords to franchisees. The new departments are managed within a subsidiary business:

I under-estimated the revenue earned from these new departments in the Blog post above. The 2017 accounts for the relevant subsidiary shows revenue of c£300k:

I was right to assume profit from these new departments was small.

12) Options

Oh dear — what has happened here.

The annual report claims 163,400 plus 360,000 = 523,400 options have been granted to date:

Yet the 2017 annual report claims the number was 300,200 plus 360,000 = 660,200:

Therefore 136,800 granted options went missing during 2018.

Within the 2017 annual report, 603,200 options were said to have been outstanding:

The 2017 figures within the 2018 report have been restated to show 523,400:

Therefore 79,800 outstanding options went missing during 2018.

WINK has some form with mis-reporting options.

The 2016 annual report (point 5) owned up to the board effectively changing its mind about an option grant confirmed in an earlier RNS.

Anyway, the directors own 455,000 options (unchanged from that reported within the 2017 annual report):

I suspect the mis-reporting is due to an employee leaving and his/her options lapsing.

The majority of options are exercisable at 150p, which right now does not cause a great problem with potential dilution.

Maynard

M Winkworth (WINK)

Dividend declaration:

Here is the full text:

————————————————————————————————————————

The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 1.9p per ordinary share for the first quarter of 2019 to shareholders. The timetable is as follows:

Ex-Dividend Date * 25/04/19

Record Date ** 26/04/19

Expected Payment Date 23/05/19

* Shares bought on or after the ex-dividend date will not qualify for the dividend

** Shareholders must be on the Winkworth share register on this date to receive this dividend.

————————————————————————————————————————

Going on WINK’s previous dividend history, a 1.9p per share Q1 dividend suggests the full-year payout will be at least 1.9p*4 = 7.6p per share.

Maynard

M Winkworth (WINK)

Dividend declaration:

This statement was issued in July. Here is the full text:

————————————————————————————————————————

The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 1.9p per ordinary share for the second quarter of 2019 to shareholders. The timetable is as follows:

Ex-Dividend Date * 25/07/19

Record Date ** 26/07/19

Expected Payment Date 22/08/19

* Shares bought on or after the ex-dividend date will not qualify for the dividend

** Shareholders must be on the Winkworth share register on this date to receive this dividend.

————————————————————————————————————————

This 1.9p per share Q2 dividend matches the Q1 payout and continues to suggest the full-year payment will be at least 1.9p*4 = 7.6p per share.

Maynard