22 March 2019

By Maynard Paton

Results verdict on Tasty (TAST):

- Miserable figures blighted by debts and losses that confirmed — albeit within the small-print — that an equity placing is on the way.

- The shares are now a gamble based on how much shareholders are asked to raise and at what price.

- Second-half trading offered hope through greater cash generation alongside improved sales per restaurant and per employee.

- Restaurants continue to be sold for cash although current trading was described as “slow”.

- Market cap now £4.2m for sales of £47m and 58 restaurants. I continue to hold.

Contents

- Event link and share data

- Why I own TAST

- Results summary

- Revenue, losses and the intention to raise new equity

- First half versus second half

- Restaurant disposals

- Management strategy

- Cash flow

- Debt and provisions

- Outlook

- Valuation

Event link and share data

Event: Preliminary results for the 52 weeks to 30 December 2018 published 20 March 2019

Price: 7p

Shares in issue: 59,795,496

Market capitalisation: £4.2m

Why I own TAST

- Experienced family management has already built and sold two quoted restaurant chains for £200m-plus (ASK Central and Prezzo).

- Bombed-out share price may provide vast upside if cash generation can improve to stave off a significant rescue fund-raising.

- Latest results offer glimmers of hope through greater sales per restaurant and per employee.

Further reading: My TAST Buy report |All my TAST posts

Results summary

Revenue, losses and the intention to raise new equity

- Dismal interim figures published during September had already heralded these miserable full-year numbers.

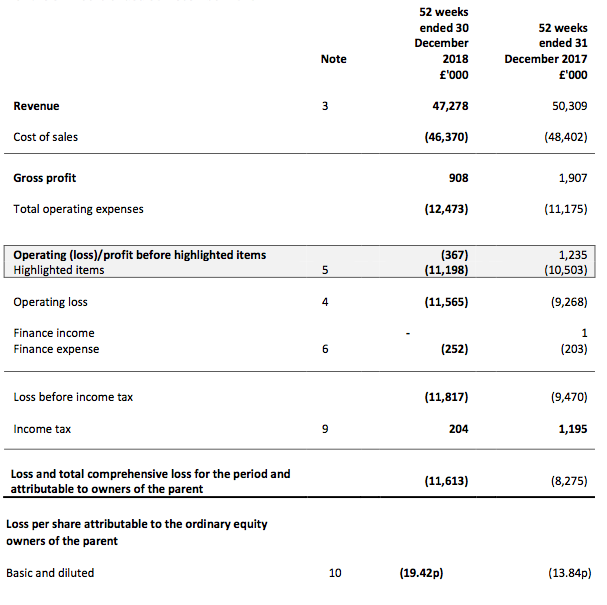

- Total revenue fell 6% while last year’s operating profit turned into an operating loss:

| Year to c31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (£k) | 29,734 | 35,794 | 45,847 | 50,309 | 47,278 |

| Operating profit before pre-opening costs (£k) | 2,986 | 3,818 | 4,692 | 1,101 | (478) |

| Pre-opening costs (£k) | (360) | (644) | (642) | (413) | - |

| Operating profit (£k) | 2,626 | 3,174 | 4,050 | 688 | (478) |

| Net finance cost (£k) | (74) | (107) | (213) | (202) | (252) |

| Other items (£k) | - | - | (3,925) | (9,956) | (11,087) |

| Pre-tax profit (£k) | 2,552 | 3,067 | (88) | (9,470) | (11,817) |

| Earnings per share (p) | 3.88 | 4.64 | (1.56) | (13.84) | (19.42) |

| Dividend per share (p) | - | - | - | - | - |

- The combination of debt and long-leasehold, loss-making restaurants prompted TAST to admit — albeit within note 21 of the accounting small-print — that “the company intends to raise new equity”.

- This new equity is in addition to the £500k the directors pledged to inject during November.

- The shares are now a gamble based on how much shareholders are asked to raise and at what price.

- The spectre of a de-listing lurks in the background. Management-connected chain Richoux gave up its AIM quotation earlier this year.

- TAST’s fundamental operational problem remains a number of under-performing restaurants due to a mix of:

- Poor locations;

- Rising labour and supply costs;

- Fixed rents;

- Middle-of-the-road menus;

- Regular discounting, and;

- Greater competition.

First half versus second half

- TAST’s second-half performance showed glimmers of hope.

- Glimmer 1: sales per average restaurant improved from £804k during H2 2017 to £809k during H2 2018:

| H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | ||

| Revenue (£k) | 24,375 | 25,934 | 50,309 | 22,997 | 24,281 | 47,278 | |

| Average number of units | 63 | 64.5 | 62.5 | 62 | 60 | 62 | |

| Average revenue per unit (£k) | 774 | 804 | 805 | 742 | 809 | 763 |

- Perhaps trading has stabilised.

- Hurt by the poor first half (deep snow, hot weather, World Cup), sales per site for the year were 18% below that achieved during 2014:

| Year to c31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (£k) | 29,734 | 35,794 | 45,847 | 50,309 | 47,278 |

| Year-end restaurants | 36 | 48 | 61 | 64 | 60 |

| Average restaurants | 32 | 42 | 54.5 | 62.5 | 62 |

| Average revenue per restaurant (£k) | 929 | 852 | 841 | 805 | 763 |

- Glimmer 2: the gross margin improved from 1.4% during H1 to 2.5% during H2:

| H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | ||

| Revenue (£k) | 24,375 | 25,934 | 50,309 | 22,997 | 24,281 | 47,278 | |

| Gross profit (£k) | 893 | 1,014 | 1,907 | 313 | 595 | 908 | |

| Operating profit*(£k) | 494 | 607 | 1,101 | (184) | (294) | (478) | |

| Gross margin (%) | 3.7 | 3.9 | 3.8 | 1.4 | 2.5 | 1.9 | |

| Operating margin* (%) | 2.0 | 2.3 | 2.2 | (0.8) | (1.2) | (1.0) |

(*before pre-opening costs and various write-offs)

- That said, the gross margin remains extremely weak and additional central costs crept into the business during H2.

- Glimmer 3: net write-offs and impairments came to only £157k during H2 following the enormous £11m figure reported during H1:

| H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | ||

| Profit on disposal (£k) | - | 1,237 | 1,237 | 1,942 | 190 | 2,132 | |

| Onerous leases (£k) | - | (1,635) | (1,635) | (1,688) | 1 | (1,687) | |

| Lease impairment (£k) | (172) | 76 | (96) | (890) | (7) | (897) | |

| Asset impairment (£k) | (9,320) | (142) | (9,462) | (10,294) | 231 | (10,063) | |

| Goodwill impairment (£k) | - | - | - | - | (115) | (115) | |

| Restructure & consultancy (£k) | - | - | - | - | (457) | (457) |

Restaurant disposals

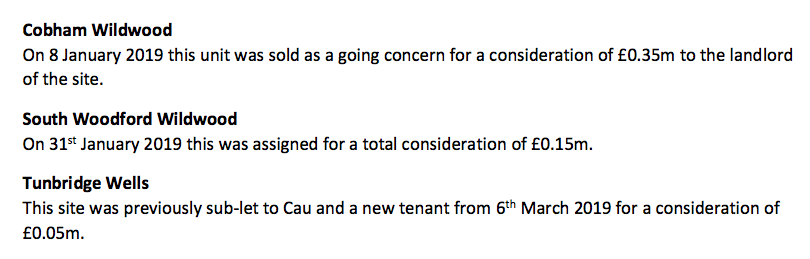

- The disposal of three sites for an aggregate £505k during early 2019 provides further hope that certain TAST outlets do have value:

- That £505k adds to the £4.1m raised during H1 following the sale of two central London sites.

- Of course, not every TAST outlet can be sold on. The balance sheet shows an ‘exit provision’ of £3m. More on that later.

- And of course, TAST may in fact be selling its very best units simply to raise much needed cash.

- At least the results small-print suggested not every TAST site is a basket-case (my bold):

“Our sites are primarily based on the high street. However, we have a number of leisure, retail and tourist locations which trade well.”

“The Group intends to dispose of underperforming sites if necessary, but has been successful with a number of turnaround plans implemented on selected restaurants.”

Management strategy

- Management reiterated its five-point plan:

- Rationalise the estate;

- [Improve the] food and drink proposition;

- Engage with our customers;

- Invest in our staff, and;

- Streamline our structure.

- Actions have included re-jigging menus, staff training, new IT and less bureaucracy.

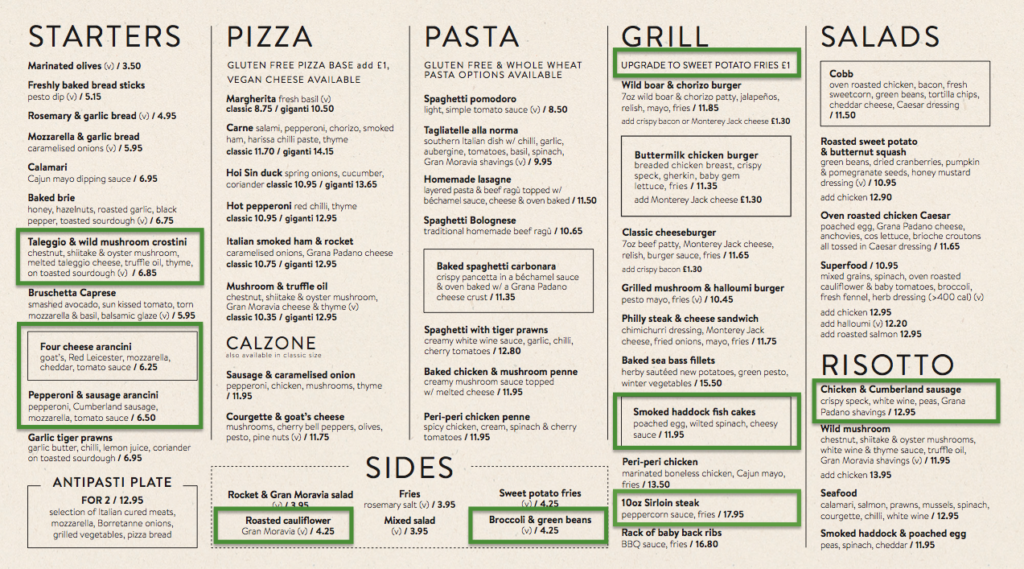

- Menu changes during October were not too radical:

- New dishes included smoked haddock fish cakes and a chicken and cumberland sausage risotto. About a third of menu items have seen their prices lifted by between 5p and 40p.

- The menu was previously changed during July, indicating management is keen to experiment with new dishes:

- Employee ratios provided further glimmers of hope.

- Staff productivity — as measured by sales per restaurant employee — has improved to its highest level since 2014:

| Year to c31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (£k) | 29,734 | 35,794 | 45,847 | 50,309 | 47,278 |

| Average restaurants | 32 | 42 | 54.5 | 62.5 | 62 |

| Restaurant employees | |||||

| Number | 634 | 836 | 1,005 | 1,169 | 1,030 |

| Cost (£k) | 10,099 | 13,028 | 17,191 | 19,716 | 18,106 |

| Revenue per employee (£) | 46,899 | 42,816 | 45,619 | 43,036 | 45,901 |

| Employees per restaurant | 19.8 | 19.9 | 18.4 | 18.7 | 16.6 |

| Cost per employee | 15,929 | 15,584 | 17,105 | 16,886 | 17,579 |

- What’s more, employees per restaurant (at 16.6) is the lowest since the 2006 flotation.

- Perhaps the greater productivity is due to a greater supply of sector talent:

“Due to restaurant closures amongst our competitors in the sector, we have been able to secure high calibre candidates that would previously have been harder to secure.”

- I should also mention that the cost per average restaurant employee has reached £17.6k — a new high.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Cash flow

- The year-end balance sheet showed cash of £4.3m and debt of £6.4m. Net debt was therefore £2.1m.

- Add on the £505k received from the aforementioned restaurant disposals during early 2019, and net debt could now arguably be £1.6m.

- TAST’s first-half statement said cash and debt at the end of June were £2.9m and £7.0m respectively following an underlying cash outflow of £3.1m.

- During the second half, TAST generated net cash of £2.0m to give an underlying cash outflow of £1.1m for the full year.

- TAST’s November update said cash and debt at the end of October were £2.1m and £6.4m respectively. During November and December, TAST therefore generated net cash of £2.2m.

- Trading during July, August, September and October therefore appears to have consumed cash of £0.2m.

- Excluding £4.1m raised from restaurant disposals, net capital expenditure came to £1.3m and was covered amply by the £1.9m depreciation charged against earnings:

| Year to c31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating profit* (£k) | 2,986 | 3,818 | 4,692 | 1,101 | (478) |

| Depreciation and amortisation (£k) | 1,312 | 1,712 | 2,045 | 2,149 | 1,864 |

| Net capital expenditure (£k) | (6,378) | (9,844) | (11,652) | (5,777) | 2,889 |

| Change in working capital (£k) | 1,215 | 67 | (883) | (319) | (731) |

| Net cash/(debt) (£k) | 1,294 | (3,529) | (1,996) | (5,157) | (2,105) |

(*before pre-opening costs and various write-offs)

Debt and provisions

- Interest paid during H2 was £133k and suggests an interest rate of approximately 4.0% on the outstanding debt.

- A 4% interest rate perhaps means the bank views a default as unlikely.

- The accounts were prepared on a ‘going concern’ basis and the banking covenants were not breached:

“The Group was covenant compliant at the 30 December 2018. Based on current and forecasted performance, the Board expect there will continue to be covenant headroom for the foreseeable future.”

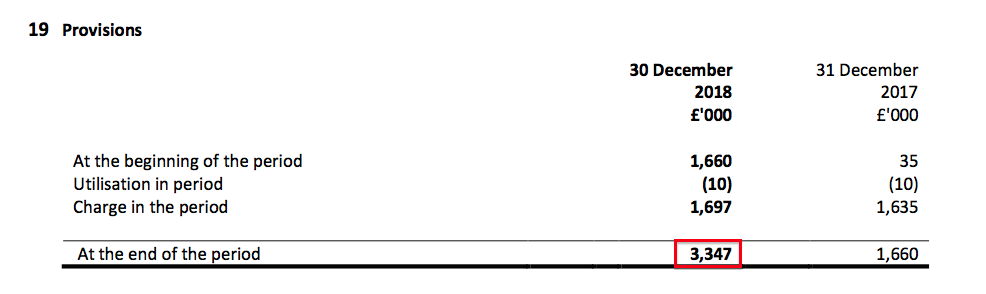

- The balance sheet carries provisions of £3.3m:

- Accounting note 19 said:

“During the period a provision for onerous leases was made of £1,687,000 (2017 – £1,625,000). This provision has been made against sites where projected future trading income is insufficient to cover the unavoidable costs under the lease. The provision is based on the expected cash out flows of these sites and the associated costs of exiting these leases. The provision covers a three year period and it is expected the majority of the provision will be utilised over the next 24 months.”

- TAST essentially took a £1.7m charge during 2018 and a £1.6m charge during 2017 as its best guess of the cash expenditure required to jettison loss-making restaurants.

- In other words, cash of up to £3.3m could be needed during the next two years to exit the problem leases.

- Some of this £3.3m may be generated by the better-performing restaurants.

- However, TAST produced an underlying £1.1m cash outflow during 2018 and continues to have debt of £6.4m to service.

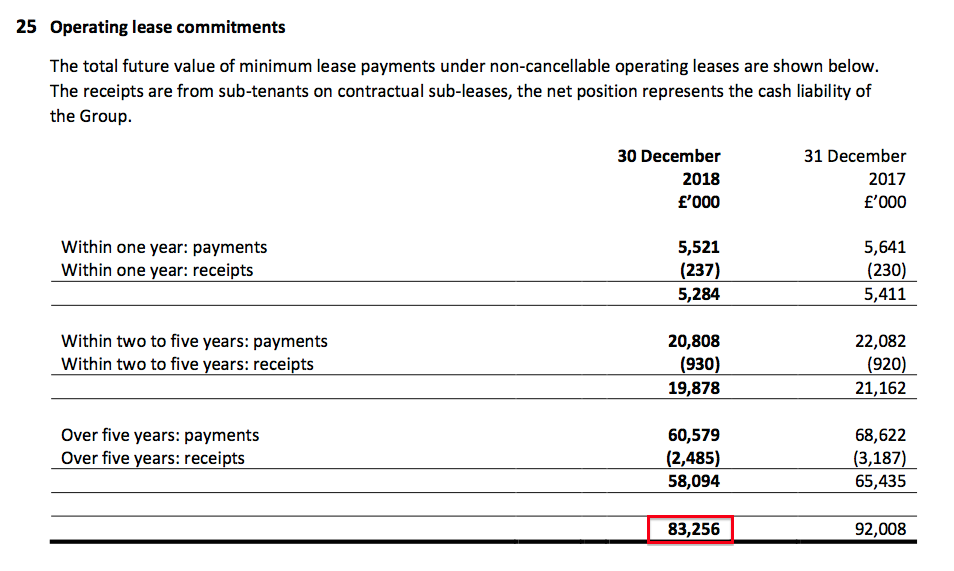

- Oh, and there are long-term lease obligations that total £83m to consider:

- As such, the aforementioned small print within note 21 — that “the company intends to raise new equity” — is perhaps not so surprising after all.

Outlook

- Management blamed politics for weak 2019 trading:

“Trading over the Christmas period was positive, though the uncertainty of Brexit has meant that 2019 has started slowly.”

“Market conditions have been increasingly challenging through 2018 and the Board’s expectation is that there will be no significant improvement in 2019. We will continue to focus on sales and cost control to ensure that the impact of the challenging economic environment is minimised.”

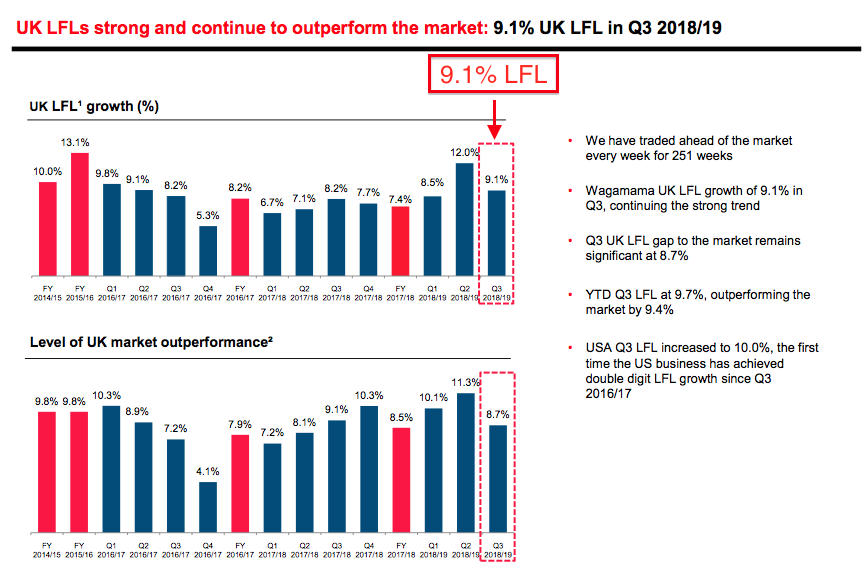

- But people are still eating out. For example, like-for-like sales at Wagamama have been running at 9%:

- Perhaps Brexit is a convenient excuse, and diners simply prefer Wagamama’s ramen dishes to TAST’s smoked haddock fish cakes.

Valuation

- The recent 7p share price supports a £4.2m market cap.

- To emphasise how badly TAST has fared, two years ago the group reported a £4.1m operating profit.

- A £4.2m market cap compares to revenue of £47m and a net book value of £11m.

- The estate currently comprises 52 Wildwood restaurants and 6 dim-t restaurants. Each site is therefore valued at £4.2m / 60 = £70k.

- Two years ago management claimed new a site fit-out would cost £650k.

- The landlord of the Cobham Wildwood restaurant recently purchased the site as a going concern for £350k — presumably no fit-out costs were required.

- The prospect of acquiring a decent restaurant well below its fit-out cost may tempt other buyers.

- Righting TAST’s balance sheet once and for all may require say, £3m, to reduce debts to a manageable level and, say, £3m, to cover the expected losses reflected by the aforementioned provision.

- TAST’s 2017 annual report reveals the company can issue an extra 11,959,100 shares — or 20% of the current share count.

- 11,959,100 shares placed at the recent 7p share price raises £837k.

- £837k plus the £500k the directors pledged to supply in November does not appear enough to resolve TAST’s plight once and for all.

- But £837k plus the £500k might be enough to provide TAST some breathing room to enable further disposals and stem current losses.

- Bear in mind the nominal price of TAST’s shares is 10p — and new shares cannot be issued below the nominal price. Any equity raise will therefore require extra paperwork to resolve this matter.

- The upside potential from a £4.2m market cap could be vast if trading ever improves and/or the underlying cash generation (a £1.1m outflow for 2018) can return to a break-even (or even positive) performance.

- I am bravely/stupidly holding on to the shares in the hope the aforementioned glimmers are evidence that TAST is not completely crippled just yet.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Tasty.

Thanks for the excellent analysis, Maynard

Thanks Kevin

Maynard,

Great work, what a comprehensive review, made me feel better for some reason!

Fingers crossed I’m with you

Thanks for sharing, very enlightening

David

Thanks David

I think the sales per restaurant and employee ratios suggest management actions have stemmed the tide (at least for now) and all is not completely lost. Shareholders could still be diluted to smithereens with an equity raising, but selling out now simply feels far too late. In my wilder dreams, management may actually raise cash to pick up site bargains from other distressed operators.

Another point I should have mentioned was debt of £1,800k was due to be repaid within 3 months after the year and (i.e. before 31 March). That TAST has not yet announced the directors injecting the pledged £500k suggests the financials haven’t deteriorated too badly so far this year.

Maynard

Tasty (TAST)

Menu changes

The Wildwood menu has been revised further.

The menu was previously changed during October 2018:

Back then, new dishes included smoked haddock fish cakes and a chicken and cumberland sausage risotto. I estimated about a third of menu items then saw their prices lifted by between 5p and 40p.

The new menu is below (now produced by TAST in an annoying jpeg format rather than a pdf):

(right-click to enlarge)

The smoked haddock fish cakes have gone and the chicken and cumberland sausage risotto is now a chicken and ‘Nduja sausage risotto.

The main additions are three gourmet pizzas, and with the other changes, there are two extra main dishes (I think). There are a net two extra sides, while both aperitifs have disappeared. The grill dishes have almost all witnessed price rises of up to 90p. A handful of rises have occurred elsewhere on the menu.

Overall, not a radical menu overhaul but at least management appears to have accelerated the menu tweaking while gourmet pizzas do not seem to be an obvious flop (on paper at least).

Maynard

Announcement today to raise funds resulting in a further dilution of the share price.

I guess it’s good that they have found investors will to part with £3.5m if I have understood the announcement correctly

Now down at 4.8p, how lower can it go….. don’t answer that one Maynard!

David

Tasty (TAST)

Firm Placing and Open Offer

A few quick bullet points on today’s statement:

* TAST’s 2018 results had already indicated — albeit within note 21 of the small print — that “the company intends to raise new equity”.

* Today’s announcement confirms up to £3.25m will be raised at 4p a share.

* The share count will increase by 136% if the fund raise is taken up entirely.

* The Kaye family (42% shareholders) has pledged to provide £800k.

* An executive director (7% shareholder) has pledged to provide £100k.

* Gresham House (17% shareholder) has pledged to provide £400k.

* The Kayes, the exec director and Gresham (then Livingbridge) bought shares at 145p during the November 2016 fund raise.

* Octopus Investments (4% shareholder) has not pledged anything.

* House broker Cenkos has agreed to “use its reasonable endeavours… to procure subscribers” for a further £1.7m.

* Ordinary shareholders can participate in a 2 for 19 open offer to provide up to £0.25m

* Assuming the full number of shares is taken up, the market cap at the 4p placing price is £5.6m.

* The proceeds will be used to reduce debt.

* Debt at the end of 2018 was £6.4m, of which £3m was repayable during 2019.

* The fund raise should leave debt of £3.4m, with a final repayment date in March 2022.

* Cash at the end of 2018 was £4.3m and assets of £550k have since been sold.

* Cash right now will undoubtedly be lower than £4.3m + £550k due to “slow” Jan/Feb trading and the business having consumed cash throughout 2018 (except during Xmas).

* However, cash post-placing should be greater than debt — which is a start.

* Provisions at the end of 2018 were £3.3m and represent future cash outflows and lease-exit costs from certain loss-making restaurants.

* Finding positive cash flow of £3.3m from profitable sites (if there are any profitable sites) to counterbalance these expected outflows could be tall order.

* As such, TAST does not seem completely out of the woods just yet.

* But breathing space with the bank should now allow management more time to deal with operational matters.

* Everything still boils down to TAST reviving its sales, lowering costs and (critically) generating cash.

* The upside potential from a £5.6m market cap could be vast if trading ever improves given revenue of £47m and 57 restaurants.

* The 2018 results showed glimmers of hope, and the menu continues to be tweaked, but obvious signs of a recovery remain elusive.

* TAST states (my bold): “Where sites are underperforming, turnaround strategies have been implemented and, in many instances, significant improvements in performance have been made.”

* The term “many instances” suggests some sites have not done as well following the turnaround strategies.

* I continue to bravely/stupidly hold on.

Maynard

Great update as always Maynard

Thanks for sharing

David

Tasty (TAST)

Results of Open Offer

Results of General Meeting

Director/PMDR Shareholding

The money has been raised. The important text is below:

————————————————————————————————————————————

The Open Offer closed for acceptances at 11.00 a.m. on 30 April 2019. The Company received valid acceptances from Qualifying Shareholders in respect of 6,580,017 Open Offer Shares including applications for 5,199,269 Open Offer Shares under the Excess Application Facility. This represents 104.5 per cent. of the maximum Open Offer Shares available under the Open Offer.

…

Tasty (AIM: TAST), the owner and operator of restaurants in the casual dining sector, is pleased to announce that at the General Meeting held earlier today, all resolutions proposed were duly passed by shareholders. Accordingly, the Company has raised £3.25 million in the Placing and Open Offer

————————————————————————————————————————————

The basic Open Offer (2 for 19) received acceptances of 1,380,748 shares, or 22% of the maximum. Thankfully the Excess Application Facility made up the remaining 78% allocation to ensure the full £0.25m Open Offer was raised. I did not participate in the Open Offer.

£3m was also raised through the Firm Placing.

The directors invested £736k — £36k more than stated in the circular. Jonny Plant spent an extra £17k and Keith Lassman spent an extra £19k.

Edit 30 May 2019:

I note no other RNSs have since come through indicating any change to notifiable holdings. Presumable a lot of different investors took up small-ish stakes.Tardy notifications have now emerged:

Islandbridge Capital now owns 4.78%.

Cannaccord Genuity now owns 16.2%.

Gresham House confirmed as owning 14.2%.

The Firm Placing involved 75 million new shares, of which 23.4 million were acquired by the Kaye family concert party/other directors, 22.8 million by Cannacord, 6.8 million by Islandbridge and 10 million by Gresham House. That leaves about 12 million shares for other institutions. A 3% disclosable holding requires about 4.2 million shares. A further 6.2 million shares were issued via the Open Offer.

End of edit

The Firm Placing and Open Offer combined to issue shares representing 57% of the enlarged share capital.

Let’s hope the money is put to good use and trading can improve.

Maynard

Tasty (TAST)

Scuttlebutt

Stockopedia blogger Paul Scott appears pleased with TAST’s Bournemouth restaurant. Screenshots of his social-media comments below:

Paul is evaluating Aim-quoted Bigdish, which is some sort of discount-meal platform, rather than TAST, but at least TAST’s food was satisfactory and the restaurant manager says “the trial is going great“. I will take any good reviews given TAST’s share price. Paul adds that Bigdish is creating “incremental business” for TAST — well, there is this meal and I think another one bought by Paul the previous week.

Maynard

Every little helps Maynard

Regards

David