07 May 2019

By Maynard Paton

Results verdict on Oleeo (OLEE):

- A terse 155-word statement revealed an unsurprising 50% profit plunge as OLEE extends its “capacity to suffer” to four years.

- At least revenue continues to inch ahead and might even be growing at a reasonable pace if the largest customer is excluded.

- Recent client installations include all four Welsh police forces — cementing OLEE’s 50%-plus share of supplying UK police recruitment IT.

- A lack of guidance for the full-year could strangely mark the low point for earnings.

- A £13m market cap is almost entirely supported by the £11m net cash position. I continue to hold.

Contents

Event link and share data

Why I own OLEE

Results summary

Revenue and profit

Financials

Valuation

Event link and share data

Event: Interim results for the six months to 31 January 2019 published 30 April 2019

Price: 170p

Shares in issue: 7,628,054

Market capitalisation: £12.9m

Why I own OLEE

- Develops recruitment software with an emphasis on customer support that has landed blue-chip clients such as Marks & Spencer, WPP, Morgan Stanley and 50%-plus of UK police forces.

- Founder/executive chairman enjoys 71%/£9m shareholding, ought to ensure long-term management consistency and may have the “capacity to suffer” to deliver long-term returns.

- A £13m market cap could be very inexpensive given the £11m net cash position and any forthcoming improvement to current minimal earnings.

Further reading: My OLEE Buy report | All my OLEE posts | OLEE website

Results summary

Revenue and profit

- Oleeo took the maximum three months (AIM Rule 18) to publish these results and a terse 155-word management narrative.

- November’s annual statement had already warned shareholders to expect profit to be “substantially lower in the current year”.

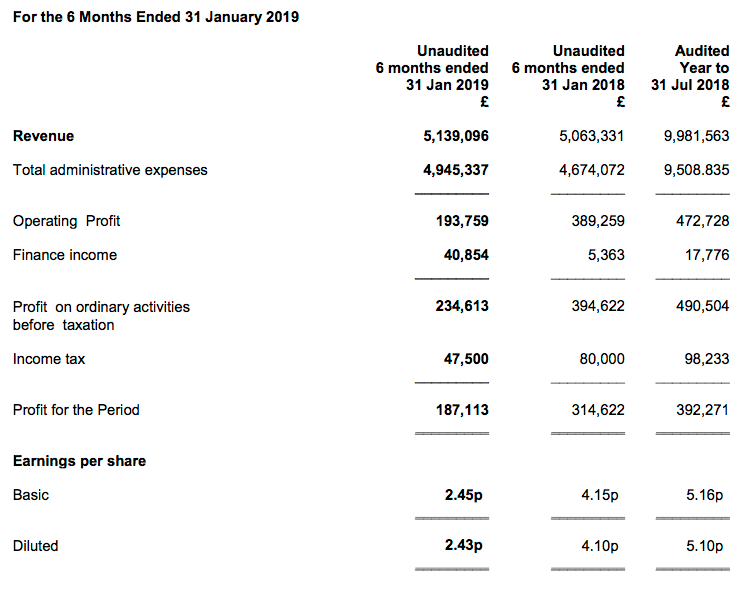

- Revenue gained 1% while operating profit dived 50%:

| H1 2017 | H2 2017 | H1 2018 | H2 2018 | H1 2019 | |||

| Revenue (£k) | 5,104 | 4,744 | 5,063 | 4,918 | 5,139 | ||

| Costs (£k) | (4,434) | (4,642) | (4,674) | (4,835) | (4,945) | ||

| Operating profit (£k) | 670 | 102 | 389 | 83 | 194 |

- Revenue set a new first-half record and management “expected to see some improvement in sales during the second half”.

- Turnover for the full year is therefore very likely to top £10m for the first time.

- Total revenue progress could have been hindered by lower income from HRMC, Oleeo’s largest customer.

- The 2018 annual report (point 3) revealed sales excluding the group’s largest customer gained 6% last year (versus a 1% overall advance).

- A contract with Welsh police forces and the introduction of product algorithms may have enhanced revenue during the half year.

- The £194k operating profit for the half compares relatively well to the £83k profit registered during the preceding second half.

- During 2012, 2013 and 2014, first-half operating profit actually surpassed £1m.

- Subsequent heavy expenditure to bolster products, marketing and staff has since depressed earnings to minimal levels.

- Optimistic shareholders may view this investment phase as management’s “capacity to suffer” — a tolerance of significant expenditure with no near-term return but the potential for high long-term rewards.

- OLEE has not said when the current rate of expenditure will recede (if ever).

- A possible straw to clutch: OLEE did not provide any guidance (woeful or otherwise) for the full year.

- In contrast, the previous four results statements issued the following gloomy forecasts:

- November 2018: “…a highly challenging and uncertain outlook for sales and, more particularly, profits, which are expected to be substantially lower in the current year than in the year which has just closed”.

- April 2018: “[W]e expect profits for the second half of the year to be lower than the first half and for this to be reflected in a lower profit for the full year than we achieved in 2017”.

- November 2017: “[W]e expect to see a further significant fall in profits.”

- April 2017: “I expect the profit for the full year to be significantly reduced compared to last year and for our investments to have a material adverse impact on our results for 2018.”

- The absence of further bad news this time around could mean the £83k generated during the preceding second-half marked the low point for profit.

- The 2018 annual report revealed the board taking a pay cut (point 4). I wrote at the time: “Wishful thinking perhaps, but I would like to think when directors cut their own pay, a greater focus is soon applied to lifting sales and profit.”

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Financials

- OLEE’s accounts are still in acceptable shape.

- Cash in the bank remains the leading attraction at £10.9m or 143p per share.

- The balance sheet carries no debt and no pension complications.

- Cash flow consumed £115k during the six months, due entirely to working-capital movements that are typically reversed during the second half.

- Margins, return on equity and other ratios remain at pitiful levels due to the depressed level of profit.

- All development expenditure is expensed as incurred and not capitalised onto the balance sheet (other software companies should take note).

- Finance income during the half came to £41k — a significant 17% of pre-tax profit.

- The 2018 annual report (point 6) showed OLEE utilising short-term deposit accounts earning between 0.75% and 1% for part of the company’s cash position.

Valuation

- OLEE remains a tightly held share with a minimal free float and wide bid-offer spread.

- The executive chairman owns 71%, his wider family control 13% and a managed fund holds 9%.

- Everyone else therefore owns 8%.

- A 170p offer price values OLEE at £13m and the free float at £1m.

- Subtract the £10.9m cash position from the market cap and the underlying business could arguably be valued at approximately £2m.

- OLEE has always operated with significant net cash, and perhaps the presence of such cash is required to keep clients happy and therefore is not really ‘surplus to requirements’.

- OLEE reported earnings of £1.9m during 2014. A return to that level of profitability could make the present valuation very inexpensive.

- Mind you, OLEE’s shares have always seemed cheap.

- My initial investment was influenced by an apparent P/E of 7 — and the shares have halved since then.

- Earnings for 2015, 2016, 2017 and 2018 were lower than those reported for 2014.

- Profit retained by the business since 2014 has therefore not created any value to date.

- May be one day OLEE’s software products could re-exhibit the attractive returns of yesteryear — or at least something close to them.

- Between 2011 and 2014 for instance, the operating margin topped 21% and return on equity topped 23%.

- Shareholders can only hope OLEE’s significant expenditure since 2014 will eventually pay off.

- Shareholders have been waiting for four years now.

- OLEE has never declared an interim dividend. The annual payout is likely to remain at 3.5p per share for the fourteenth consecutive year.

- The yield at 170p is 2%.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Oleeo.