15 July 2019

By Maynard Paton

Results summary for Mountview Estates (MTVW):

- Brexit “uncertainties” led to MTVW’s lowest annual revenue and earnings since 2013.

- At least the dividend was held and net asset value reached a fresh £94 per share high.

- A higher gross margin during the second half was encouraging and may indicate MTVW is enjoying slightly stronger sale prices.

- Debt represents a low 12% of the group’s property estate — which continues to be accounted for at cost.

- My sums suggest MTVW’s balance sheet could actually be worth £200-plus per share — more than double the recent share price. I continue to hold.

Contents

- Event link and share data

- Why I own MTVW

- Results summary

- Revenue, profit, dividend and net asset value

- Gross margin

- Allsop valuation

- Balance sheet and cash flow

- Valuation

Event link and share data

Event: Preliminary results for the twelve months to 31 March 2019 published 13 June 2019

Price: £97

Shares in issue: 3,899,014

Market capitalisation: £378m

Why I own MTVW

- Buys, holds and sells regulated-tenancy properties and boasts an illustrious, 40-year-plus history of net asset value and dividend advances.

- Board led by veteran family management that continues to enjoy an aggregate 51%/£193m shareholding.

- Simple accounts carry properties at cost, which if sold at their fair market value may be worth double the recent share price.

Further reading: My MTVW Buy report |All my MTVW posts | MTVW website

Results summary

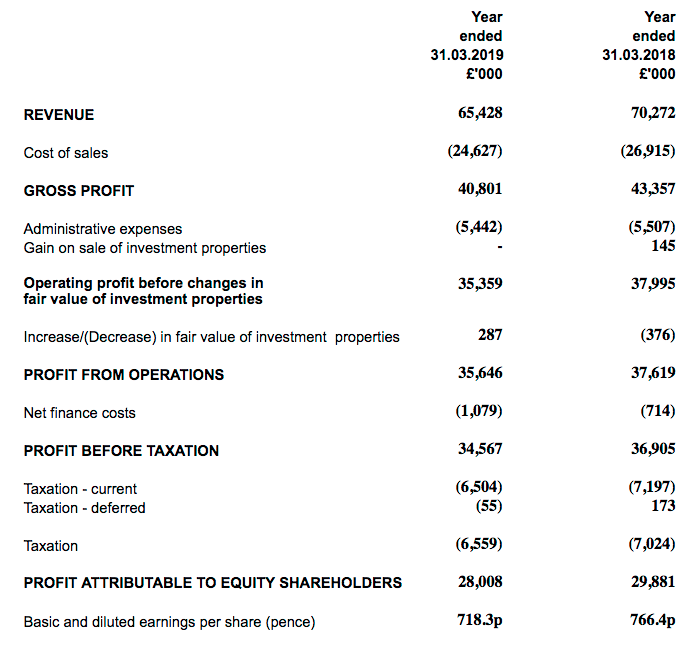

Revenue, profit, dividend and net asset value

- November’s interim results — the weakest for five years — had already suggested these 2019 figures would not be spectacular.

- The chief exec’s terse statement blamed Brexit “uncertainties” for the group’s lowest annual revenue and earnings since 2013:

| Year to 31 March | 2015 | 2016 | 2017 | 2018 | 2019 |

| Net asset value (£k) | 287,661 | 311,752 | 336,279 | 354,462 | 366,874 |

| Net asset value per share (p) | 7,378 | 7,996 | 8,625 | 9,091 | 9,409 |

| Revenue (£k) | 71,331 | 79,765 | 78,232 | 70,272 | 65,428 |

| Gross profit (£k) | 46,710 | 53,014 | 52,056 | 43,357 | 40,801 |

| Operating profit (£k) | 41,655 | 47,866 | 46,825 | 37,850 | 35,359 |

| Net valuation gain (£k) | 57 | 1,504 | (1,020) | (376) | 287 |

| Finance income (£k) | (1,736) | (1,179) | (819) | (714) | (1,079) |

| Other items (£k) | - | 197 | - | 145 | - |

| Pre-tax profit (£k) | 39,976 | 48,388 | 44,986 | 36,905 | 34,576 |

| Earnings per share (p) | 816 | 993 | 929 | 766 | 718 |

| Dividend per share (p) | 275 | 300 | 300 | 400 | 400 |

- Revenue and operating profit both fell 7% after MTVW sold 16 fewer properties at £4k less than last year:

| Year to 31 March | 2015 | 2016 | 2017 | 2018 | 2019 |

| Properties sold | 192 | 209 | 182 | 170 | 154 |

| Average price (£k) | 278 | 294 | 331 | 305 | 301 |

- At least rental income increased 3% to £19m — equivalent to 29% of total revenue.

- The dividend was held at 400p per share.

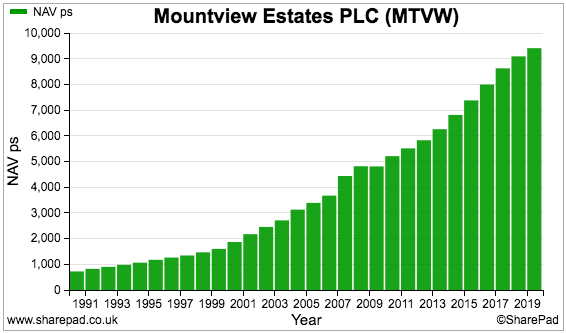

- Net asset value (NAV) improved by £12m to £376m — equivalent to £94.09 per share and a fresh NAV record:

- The 4% NAV advance was the lowest annual percentage gain since NAV dipped slightly during 2009.

- NAV per share growth has slowed over time.

- NAV per share has compounded at a 7% average during the last 10 years, 9% during the last 20 years, 11% during the last 30 years and 13% during the last 40 years.

Gross margin

- MTVW’s balance sheet is dominated by 2,000 or so regulated-tenancy (and similar) properties that boast an aggregate £392m book value.

- MTVW sells these properties only when the regulated tenancy ends — which typically occurs when the tenant dies.

- The number of group properties becoming available for sale — and the total proceeds MTVW earns from one year to the next — can therefore be unpredictable.

- The group’s properties are held on the balance sheet at their cost price.

- The percentage gain on each property sold is largely correlated to how long the property has been owned by MTVW — and can vary somewhat in any particular year.

- The table below shows the gross margin achieved from selling properties during the last five years:

| Year to 31 March | 2015 | 2016 | 2017 | 2018 | 2019 |

| Group gross margin (%) | 65.5 | 66.5 | 66.5 | 61.7 | 62.4 |

| Property sales gross margin (%) | 65.0 | 65.8 | 66.3 | 57.9 | 59.1 |

- The 59.1% gross margin for 2019 is equivalent to MTVW selling a property for a 145% gain. The five-year average is 171% and the ten-year average is 163%.

- Lower house prices can affect the gross margin MTVW enjoys.

- Before the Brexit vote, MTVW had enjoyed a gross margin of approximately 65% from property sales — with a record 71% gross margin achieved during the six months to September 2016:

| H1 2017 | H2 2017 | H1 2018 | H2 2018 | H1 2019 | H2 2019 | |||

| Property sales revenue (£k) | 25,133 | 35,021 | 23,953 | 27,887 | 20,656 | 25,774 | ||

| Property sales gross profit (£k) | 17,843 | 22,024 | 14,297 | 15,721 | 11,706 | 15,571 | ||

| Property sales gross margin (%) | 71.0 | 62.9 | 59.7 | 56.4 | 56.7 | 61.1 |

- These results encouragingly showed the gross margin from property sales improving during the second half to 61.1% — equivalent to selling a property for a 151% gain.

- I am hopeful this gross-margin improvement can be sustained — and that gross margins can perhaps gradually return to their 65% pre-Brexit level.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Allsop valuation

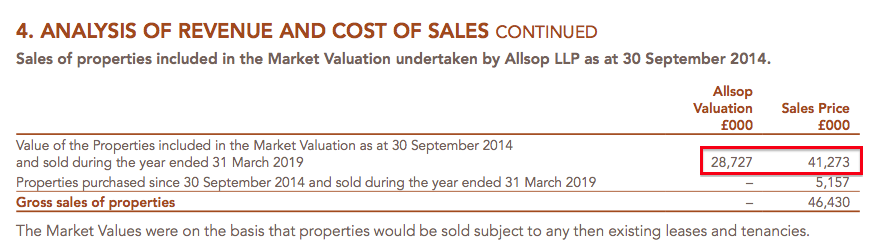

- MTVW commissioned property agents Allsop during September 2014 to value the group’s estate.

- Allsop returned a £666m valuation — some 2.1x the £318m book value of the properties carried at the time.

- The Allsop calculation was based on MTVW’s properties remaining in their regulated-tenancy state.

- The Allsop valuation was not formally applied to the accounts. MTVW’s properties remain on the balance sheet at their cost price.

- However, MTVW does reveal the proceeds from sold properties versus their Allsop value:

| FY 2016 | FY 2017 | H1 2018 | H2 2018 | H1 2019 | H2 2019 | |||

| Property sales revenue (£k) | 61,442 | 57,174 | 22,496 | 22,660 | 17,363 | 23,910 | ||

| Allsop valuation (£k) | 42,600 | 38,505 | 14,767 | 15,827 | 12,226 | 16,501 | ||

| Sold-to-Allsop multplier(%) | 1.44 | 1.48 | 1.52 | 1.43 | 1.42 | 1.45 |

- These results encouragingly showed the ‘sold-vs-Allsop’ multiplier improving slightly to 1.45x during the second half.

- The multiplier was 1.44x for 2019 as a whole.

- The second-half improvement to both the ‘sold-vs-Allsop’ multiplier and the gross margin suggests the group may now be enjoying slightly stronger sale prices.

Balance sheet and cash flow

- Some £31m was spent acquiring 105 additional properties during the year (average cost: £299k), which MTVW described as “good purchases”.

- Exclude two purchases that totalled close to £4m, and the average price paid was £268k.

- A £2m debt repayment plus a £16m dividend left net debt £2m heavier at £47m.

- Net debt represents 12% of the group’s £392m property estate:

| Year to 31 March | 2015 | 2016 | 2017 | 2018 | 2019 |

| Trading properties (£k) | 323,020 | 334,108 | 347,380 | 376,879 | 392,384 |

| Net debt (£k) | (59,538) | (41,619) | (31,217) | (44,995) | (46,519) |

- Net debt has at times represented 30% or more of MTVW’s property stock.

- The firm could therefore have the capacity to borrow another £70m.

- MTVW’s books remain free of pension obligations.

Valuation

- MTVW’s balance sheet could be worth more than £200 per share — assuming all of the group’s regulated tenancies were to end immediately and the properties were then all sold at a fair market value.

- The following table outlines my sums:

| Property stock Sept 2014 (£k) | 317,651 |

| Less property stock sold since Sept 2014 (£k) | (91,170) |

| 226,481 | |

| Allsop-vs-book multiple | 2.10 |

| Sold-vs-Allsop multiple | 1.44 |

| 683,646 | |

| Property stock purchased since Sept 2014 | 165,904 |

| Sold-vs-Allsop multiple | 1.44 |

| 238,902 | |

| Possible property stock value (£k) | 922,547 |

- I have taken the original September 2014 portfolio value of £318m and subtracted the £91m book value of properties sold since that date.

- I have then multiplied the £226m remainder by my 2.1x ‘Allsop-vs-book’ multiple and then by the 1.44x ‘sold-vs-Allsop’ multiple witnessed during 2019.

- I arrived at a £684m estimated value for all of MTVW’s properties that were owned at September 2014 but have yet to be sold.

- Since September 2014, MTVW has spent £166m buying additional properties.

- I have assumed all of these additional properties can be sold one day for £239m based on my 1.44x ‘sold-vs-Allsop’ multiple.

- Adding the £684m and the £239m together gives £923m.

- This next table adjusts that £923m for 19% taxation, other investments, net debt and other liabilities to give a possible balance-sheet value of £796m or £204 per share:

| Possible property stock value (£k) | 922,547 |

| Less tax at 19% (£k) | (100,721) |

| Plus other investments (£k) | 28,112 |

| Less net debt (£k) | (46,519) |

| Less other liabilities (£k) | (7,103) |

| Possible NAV (£k) | 796,307 |

| Possible NAV per share (£) | 204.23 |

- These sums are not perfect, but should give a reasonable idea of the group’s inherent value.

- The Allsop valuation was commissioned almost five years ago — and the original £666m verdict may now be very stale.

- The great unknown of course remains how long MTVW will take to sell all of its properties to realise my potential £204 per share NAV guess.

- Patience will undoubtedly be required for the underlying value of the property portfolio to be realised.

- Mind you, the longer the disposals take, the higher house prices should rise and the greater proceeds MTVW ought to eventually achieve from its future sales.

- MTVW’s £94 per share book value — calculated with the properties accounted for at cost — almost covers the £97 share price.

- That simple NAV valuation hardly suggests the shares are expensive.

- The 400p per share dividend supplies a 4.1% income at £97.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Mountview Estates.

Mountview Estates (MTVW)

Publication of 2019 annual report

Here are points of interest.

1) Extra management commentary

The terse management narrative within the results RNS was expanded upon with the annual report.

The chairman implied the group’s “skilled and dedicated” staff could be the group’s competitive advantage:

Shareholders can also look forward to fresh corporate-governance statements within next year’s report. (MTVW’s corporate governance does not meet many best practices).

The outlook statement below did not suggest anything too untoward:

2) Concert party shareholding

The Sinclair family concert-party shareholding is now 51%:

For years the holding was 53%. Then during 2018 the holding was trimmed to 52% and trimmed further to 51% during 2019.

Extra trimming could in theory see the concert party could lose control of the company. The concert-party shareholding is important as the shareholder register contains significant dissident investors (this write-up has more)

3) Director pay

On the subject of dissident investors, 30% of shareholders voted against the remuneration report at the AGM:

The chief exec’s basic pay increased 3% to a (hefty) £530k, but his bonus was trimmed by 4% to a (hefty) £421k:

The chief exec’s basic pay has increased at a 12% average during the last five years. In comparison, the dividend has compounded at 15% and NAV at 7% during the same time.

The executives will enjoy pay rises this year:

MTVW argues the lack of an LTIP scheme and pension contributions justifies the pay arrangements:

The company seeks views on remuneration:

I understand the chief exec’s brother-in-law regularly expresses his (dissident) views at the AGM.

4) Property details

This note reveals the majority of property sales are sub-£500k, suggesting MTVW may not be too exposed to extravagant housing valuations:

Most properties are located in London and the south east of England:

5) New accounting standards

No problems with new IFRSs:

6) Revenue split

As mentioned in the Blog post above, MTVW does receive rental income from its properties:

Such income represented 29% of total revenue during 2019.

The rental yield from the £392m book value of trading properties and £28m book value of standard investment properties is a useful 4.5%.

7) Allsop valuation

MTVW repeats its explanation as to why the Allsop valuation was so far ahead of the property estate’s reported book value:

8) Employees

MTVW’s employee ratios deteriorated during 2019:

One extra worker alongside lower group revenue meant revenue per employee fell 10% to £2.26m — the lowest since 2012. Still, £2.26m per employee remains a remarkable level of revenue. Most companies enjoy less than £200k.

The 29 staff last year handled 105 purchases and 154 sales — or approximately 9 transactions per employee. Previous years have seen employees generally handle between 10 and 12 transactions on average.

Employee costs as a proportion of revenue increased from 5.3% to 6.0% — the highest level for at least 20 years.

Average employee pay is £135k, and within the £134k-£139k range seen during the previous three years.

The (well paid) directors account for half of total staff pay. Exclude the two executives and average employee pay is £75k.

9) Bank interest

MTVW is paying greater interest on its debt:

Interest paid during the year was £1,079k versus £714k for 2018. Average debt during 2019 was £49m, so the effective interest rate paid was 2.18%. For 2018, average debt was £41m and the effective interest rate was 1.73%.

For 2014. 2015, and 2016, interest paid represented 2.50%, 2.26% and 2.17% of average debt, so the 2018 figure seems freakishly low and the 2.18% for 2019 does not appear worrying. MTVW’s main borrowings renew in 2022 and 2023.

10) Trade receivables

This note is great:

Trade receivables are tiny compared to revenue of £65m. Clearly every tenant pays on time. Even including the prepayments and accrued income, all receivables reflect just 3% of revenue. There are no ‘past due’ receivables either.

Tenants pay on time because they could otherwise forfeit their ‘cut price’ tenancy agreement:

11) Expected inventory to be settled within twelve months

For the fourth year running, MTVW expects to sell property with a book value of between £20m and £21m during the forthcoming twelve months:

The projection is simply a three-year average of previous years, but nevertheless does give investors an idea as to what management expects the business could achieve.

During 2018, MTVW sold properties with a £19m book value after predicting selling £20.5m in the 2017 annual report.

Maynard

Hi Maynard,

Thanks very much for this post.

I agree with you that the shares are undervalued.

I have a question on the cash flow statement. Given that Mountview generally buys their properties years in advance of being able to sell them I was expecting to see operating cash flows before movements in working capital to be far ahead of operating profit in the income statement. I accept that there will be some cash expense for refurbishing and selling the properties but I assumed that most of the £18,973,000 cost of properties sold in 2019 would be cash laid out in previous years to purchase the properties. Looking back at previous years this doesn’t seem to be the case either. Do you have any thoughts on why this is? What am I missing?

Thanks in advance.

Hi James

Good question. The £18,973k ‘cost of properties’ cash movement occurs within the ‘change to inventories’ item within the movements within working capital. MTVW’s properties are held as stock, so the associated cash inflows and outflows (from adding new/selling old stock) occur in that inventories movement and not before.

The (£15,505k) inventory movement for 2019 therefore reflects the +£18,973k stock reduction from the property sales less £34m invested in new stock. (This £34m includes certain buying costs such as stamp duty).

Had MTVW not purchased any new stock, the inventory movement would have been +£18,973k and cash generated from operations would have been c£54m to reflect the entire proceeds from the disposals.

Similar reinvestment of sale proceeds into new stock have occurred in previous years.

Maynard

Mountview Estates (MTVW)

AGM attendance

I attended yesterday’s MTVW AGM. The following is my best recollection of what was said during the presentation, follow-up Q&A and post-meeting chit-chat (mostly paraphrased). No proof of share ownership was needed to attend.

All board members were present and chief executive Duncan Sinclair (DS) and financial director Maria Bray (MB) kindly provided a short presentation before the wider Q&A — the answers for which were almost entirely provided by the chairman. The formal business of the AGM was conducted behind the scenes following the Q&A. More on that later.

The meeting must have attracted 50 or so attendees — a mix of family/veteran shareholders, advisors and ordinary investors. About 6-8 different (ordinary) investors asked questions. Craig Murphy (whose family control 24% of the shares) asked various pointed questions, and there were short statements from other family members, too.

The whole meeting was recorded on audio — certain family members do not get on and disagree about the group’s corporate governance and board membership. A tape recording could therefore come in useful as to who said what.

It was a pleasure to meet the three attendees who read my blog and who approached me after the meeting to say hello.

————-

DS commenced the presentation:

* MTVW started as “very simple business” and that simplicity “continues to be the case”. “No complex financing” and “do simple things well”. MTVW continues to be run as “a small company”.

* Management had studied other types of property investments in the past, but concluded regulated tenancies offer the best returns and the group’s results “bear out” the strategy.

* Revenue was lower in 2019 due to a lower number of property sales rather than lower prices. There were “less vacant possessions than might have been expected”. (Vacant possessions typically occur on the death of the tenant). The lower number of vacant possessions was a “quirk of fate” and the “law of averages will return”. The number of vacant possessions has a much greater effect on any year’s revenue/profit than variations to house prices.

* Regulated tenancy properties are purchased typically at 75% of their fair market value.

* Dividend up 35x during DS’s time as chief executive (29 years). Payout was “artificially low” in years gone by.

* Back in 2000, management felt the business had “15 to 20 years to go”. (The number of regulated tenancies are shrinking because they can no longer be created). However, the group has since recognised some tenants were in their 20s when taking their regulated tenancies back in the 80s, so “there is still enough business out there for another 15 to 20 years.”

* MTVW “not obliged” to revalue its trading stock. “Can be argued it is premature to conduct another valuation in the current uncertain times”. The “appropriate announcements will be made when discussions have taken place.”

(I was surprised by these comments, and on reflection the comments did not make clear whether another valuation would actually be forthcoming. The comments certainly felt as if the management were not committed to another valuation.

I made the point in the Q&A that management appeared “indecisive” about the valuation — and the excuse of “uncertainty” seemed odd given MTVW has experienced all sorts of “uncertain” economic and political times over the years.

DS replied by repeating his earlier statement. The chairman effectively admitted that conducting a valuation before the Brexit outcome is known would be a waste of money given the property market could change notably thereafter.

My view: The previous valuation took place in Sept 2014 and there would be no shame in the Board committing to a fresh valuation every five years starting from Sept 2019, and simply saying a valuation is taking place and nothing can be done about the Brexit uncertainty.

By committing to regular valuations, the Board will benefit from having a lot less awkward questions on the subject and shareholders can happily adjust the valuation for any Brexit uncertainties themselves. DS admitted the Board did not see the valuation as a useful tool for managing the business day-to-day, so I remain confused why — when shareholders continue to ask about the valuation — the Board is non-committal and provided waffly answers.)

* MB outlined the £3.74m purchase of two leasehold ground rents in Kensington Court, Kensington, W8. The two leases run for 999 years, but are subject to short sub-leases of 10 and 11 years. Lease extensions could lead to an estimated profit of £2.5m (I am not sure if that is total profit or on each lease). If the leases revert back to MTVW, then the valuation could be £4m per lease.

On to the Q&A:

* Q: Possibility of buybacks given the share-price valuation? Board has spoken to shareholders (presumably other family members) and there has been “no appetite for buybacks”. Management happy to continue to reinvest in regulated properties.

* Q: Craig Murphy asked about the rationale for the service payment for the previous chairman beyond his departure.

(For background, the previous chairman left the board on 31 March 2019 and his departure was announced on 25 February 2019. The annual report indicates he was paid up to 30 June 2019. The previous chairman’s pay was £99k a year, he collected £124k up to June, so he apparently enjoyed a £25k ‘bonus’).

Did the ex-chairman have a legal entitlement to the ‘extra’ payment? The payment was a “fair and reasonable thing to do”.

When did the board know of the ex-chairman’s intentions to leave? The AGM/EGM votes of last year (August and November) apparently prompted his decision. Nominations committee meetings were held in November 2018 and the following February.

The chairman then explained he had met with Craig Murphy between the AGM and EGM, and that Mr Murphy had been “supportive of the strategy” and that he “recognised the skills and value of the executives”. The chairman said his “door was open” to further conversations.

Mr Murphy then claimed he “broadly supported the business model” but that a “very good proportion” of the meeting with the chairman concerned “corporate governance failings” and that he had lost the “trust and confidence in the non-execs to act on the views of shareholders”.

Mr Murphy asked why, as a representative of a collective 24% shareholding, he could not obtain a seat on the board? (Mr Murphy claimed the previous chairman had told him he would not get a seat on the board even with 30% or 40%, but at 51% it would be “difficult to resist”.) The appointment of directors was “a decision for the nominations committee”.

* One investor said he was “fed up with the Murphys” and their “particularly nasty guerrilla campaign to drive someone out”.

* Another investor said “a 24% shareholder ought to have representation on the board”.

* James Langrish-Smith said his family — 12.5% shareholders — were “very supportive of the board”.

* A good question was asked about the £5.157m proceeds from properties bought after the 2014 Allsop valuation — what was the margin on those sales? Similar to a lot of questions during the meeting, the answer was waffly and gave no specifics. The chairman claimed MTVW had “never sold a property at a loss” during his time at the firm (since 1 April 2018).

* Q: There is no obvious family successor to DS, so what are MTVW’s succession plans? Chairman said the plans would “kick into gear big time” when DS signals his retirement. DS set to “continue for many years yet”. Did not want to go into details on “hypothetical” situations.

* Q: What is the hurdle rate on new purchases? The chairman did not give specifics but DS did admit the discount paid for new purchasers was calculated on “getting the keys tomorrow morning” and did not involve property price “speculation”. Staff provide DS with a “thorough dossier” on each proposed purchase, who then (seemingly) approves each transaction. Price of 75% of fair market value is a “fair assessment” of the current market. DS was vague as to how that 75% figure had changed over time.

DS added: Life tenancies — “where rental income can be as low as £10 a year” but occupants are responsible for repairs — are typically bought at 50% below fair value. Some of the larger £3m-plus properties bought of late are life tenancies , but they are not typical purchases and were bought at more than 50% of fair market value.

Q: How long typically does MTVW own a regulated property for? Not worked out the figures.

Q: How old is the average tenant? Don’t know.

(I asked those two questions and I can’t say I was impressed. The eventual rate of return is likely to be guided mostly by the length of time of ownership. The longer the ownership, the less effect the original purchase discount will have on the eventual return.)

Q: Something the chairman was happy to disclose was that most properties (by number) are sold through auction.

Q: Will MTVW sell properties in a housing downturn or hold on for prices to recover? Will sell in a downturn, because the opportunity to reinvest at attractive prices — and likelihood of attractive future returns — is likely to be good.

Q: Any worries about tenancy regulations being changed? No sign of anything affecting MTVW.

On to the formal business of the meeting, whereby Craig Murphy requested polls for various resolutions instead of a show of hands. The request meant the resolutions were not discussed in the meeting and the voting was done on cards behind the scenes.

One attendee made the valid point that the polls should have been conducted before the Q&A, and the result announced to the meeting after the Q&A.

Anyway, the result of the AGM was confirmed through the RNS.

The (non-family) non-execs have been voted off once again (as per 2017 and 2018). The votes ‘against’ this year increased by about 10k versus a 60k loss of votes for the ‘for’ camp. So the dissident Murphys appear to be enjoying slightly greater support, although the eventual outcome — an EGM in November which will hold another vote that will recognise the 51% concert-party shareholding — should see the non-execs formally reappointed.

Of some significance is this line: “The Directors will engage with shareholders to obtain feedback on their concerns and will publish an update on that engagement within six months of the date of the Annual General Meeting.“

MTVW has not previously published any engagement feedback. I look forward to the disclosure of the discussion. MB said in the meeting the cost of an EGM was £40-50k (expensive legal paperwork).

According to the post-meeting grapevine…

* the Murphys (24% shareholders) are broadly happy with the running of the business, but are aggrieved about the board’s pay and general lack of influence at board level. The execs are paid well for “just collecting rent and putting houses in auctions”.

(I attended the 2014 AGM and Graham Murphy complained about board pay (among other things) then. At this meeting, I was not clear whether the Murphys want to sell up. I think they just want a seat on the board — which they were refused despite MTVW appointing a new non-exec in 2018 (who is now acting chairman). I am not clear what the Murphys would do differently operationally if they were in charge.)

* An industry insider claimed DS does a good job and was a “good buyer” of property given competition with Pears, Dorringtons, etc.

Maynard

Thanks for the update, gives quite a bit of colour. Appreciate it, I’m a tiny holder (living in Australia), so happy to wait and collect 4 %. I’ve not looked particularly closely at DJAN, but recognise that their discount to to book is far greater, presumably because they conduct valuations more frequently. Is the discount to book quite a rarity ?

Hi Christian,

For DJAN, the shares have always traded at a discount to NAV due to the ‘unconventional’ corporate governance, low free float, lack of City engagement and so on. Whether the discount will ever disappear is debatable. MTVW’s shares did trade below book for years, but then came the Allsop valuation that shone a more realistic figure on the property estate.

Thanks

Maynard

Useful AGM update, thanks Maynard.

Regarding deaths, it might be interesting to correlate the results of Dignity, which can be hit by lower deaths, and the sales of regulated tenancies from Mountview (I presume the latter would a lagging indicator, though probably not by much since MTVW presumably actions a sale quickly on vacancy).

The lower death rate seen by Dignity hit the headlines in May:

“Funeral firm Dignity says its profits are likely to be lower this year because fewer people have died in 2019 so far.

Dignity said the absolute number of deaths in the first three months of 2019 fell by about 12% to 159,000, compared with 181,000 in the same period last year.”

https://www.bbc.co.uk/news/business-48252127

Cheers!

Hi Owain,

Yes, good point. I shall keep an eye on DTY’s statements!

Maynard

official death details!

https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/deaths