Event: Preliminary results and presentation for the twelve months to 31 January 2019 published 26 March 2019. Price: 1,900p Shares in issue: 12,011,426 Market capitalisation: £228m

Why I own SUS

Provides ‘non-prime’ credit to car buyers and property developers, where disciplined lending and reliable service have supported an enviable company record.

Boasts veteran family management with 40-year-plus tenure, 44%-plus/£102m-plus shareholding and a “steady, sustainable” approach to organic, long-term growth.

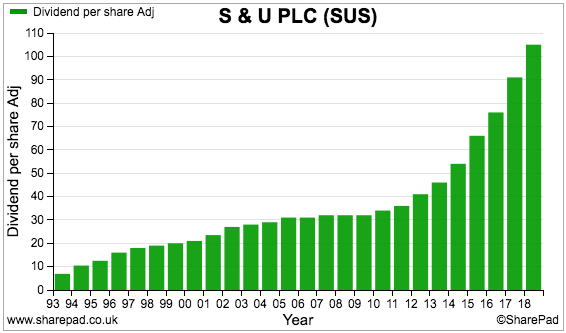

Illustrious dividend has not been cut since at least 1987 and presently supports a 6%-plus income.

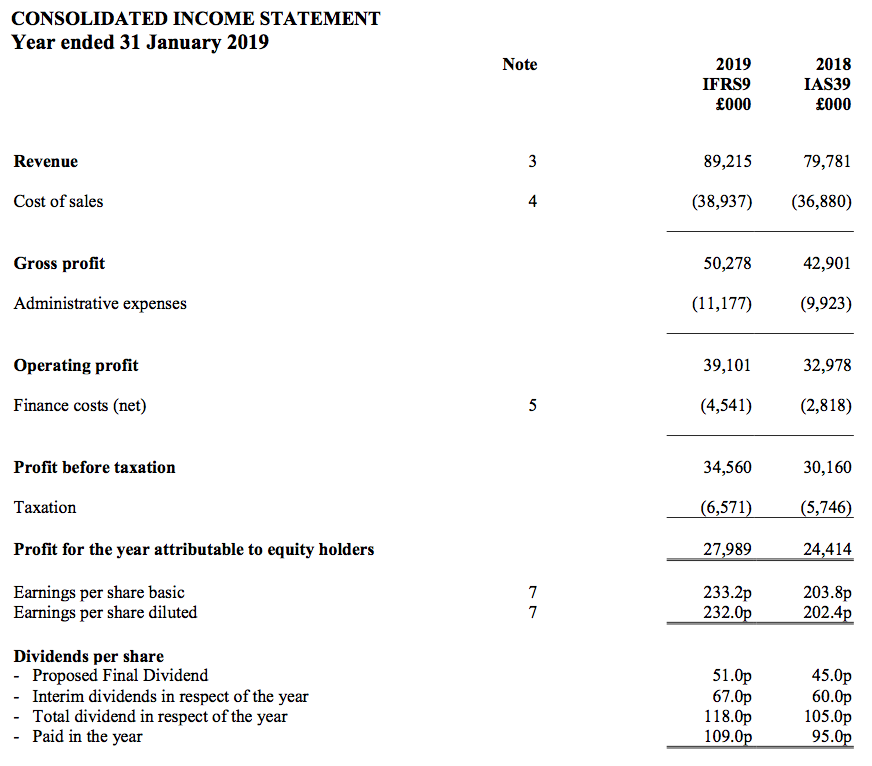

The results revealed revenue up 12%, operating profit up 19% and the dividend up 12%:

Year to 31 January

2015

2016

2017

2018

2019

Revenue (£k)

36,102

45,182

60,521

79,781

89,215

Operating profit (£k)

18,922

23,643

26,871

32,978

39,101

Other items (£k)

-

-

-

-

-

Finance cost (£k)

(2,207)

(3,243)

(1,668)

(2,818)

(4,541)

Pre-tax profit (£k)

16,715

20,400

25,203

30,160

34,560

Earnings per share (p)

100.1

133.6

170.7

203.8

233.2

Dividend per share (p)

66.0

76.0

91.0

105.0

118.0

Revenue, profit and the dividend all reached new highs.

The results extended SUS’s run of impressive growth following the sale of the group’s home-credit business during 2015.

The introduction of IFRS 9 for 2019 reduced both revenue and the group’s bad-debt impairment charge by £2.4m.

The new accounting rule prevents the “grossing up of revenue and impairment for uncharged interest on arrears”.

SUS’s prior-year figures were not restated under IFRS 9. Revenue would have advanced 15% (vs 12% reported) and impairments would have advanced 31% (vs 18% reported) on a like-for-like accounting basis.

IFRS 9 had no effect on reported profit or cash flow.

Advantage Finance, SUS’s car-loan division, delivered its 19th consecutive year of record pre-tax profit.

Aspen Bridging, SUS’s fledgling property-loan division, became profitable following last year’s start-up loss.

Management said: “The long-term outlook for responsible and good-quality used-car finance, at affordable monthly repayments provided by Advantage is strong.”

Management added that its “prognosis” for the next twelve months was “realistic, but optimistic”.

Reading between the lines — and studying the numbers (see below) — the pace of growth is likely to subside during the next year or two.

Motor-finance bad debts

Bad debts continue to represent a greater proportion of revenue and outstanding loans within Advantage Finance:

Year to 31 January

2015

2016

2017

2018

2019

Motor

Loan provision (£k)

5,863

7,611

12,194

19,434

22,980

Revenue (£k)

36,102

45,182

60,521

78,882

86,372

Average customer loans (£k)

89,678

125,764

169,335

222,372

255,013

Loan provision/Revenue (%)

16.2

16.8

20.1

24.6

26.6

Loan provision/Average customer loans (%)

6.5

6.1

7.2

8.7

9.0

Revenue/Average customer loans (%)

40.3

35.9

35.7

35.5

33.9

'Risk-adjusted yield' (%)*

33.7

29.9

28.5

26.7

24.9

During the last five years, Advantage’s bad-debt ‘loan provision’ has increased from 16.2% to 26.6% of divisional revenue.

For 2019, Advantage’s £23m loan provision was equivalent to 9.0% of the division’s £255m average customer loans, versus 6.5% back in 2015.

Meanwhile, revenue earned from Advantage’s customer loans has dropped from 40.3% to 33.9% a year since 2015.

Lower revenue from loans alongside greater bad-debt provisions has meant SUS’s own ‘risk-adjusted yield’* for Advantage has fallen from 33.7% to 24.9% since 2015.

*risk-adjusted yield is a KPI used by SUS and is calculated as: (revenue - loan provision) / average customer loans

Advantage’s bad-loan ratios all deteriorated during the second half:

H1 2018

H2 2018

FY 2018

H1 2019

H2 2019

FY 2019

Motor

Loan provision (£k)

8,573

10,843

19,434

11,320

11,660

22,980

Revenue (£k)

37,470

41,412

78,882

43,270

43,102

86,372

Average customer loans (£k)

210,168

239,011

222,372

257,335

261,113

255,013

Loan provision/Revenue (%)

22.9

26.2

24.6

26.2

27.1

26.6

Loan provision/Average customer loans (%)

8.2

9.1

8.7

8.8

8.9

9.0

Revenue/Average customer loans (%)

35.7

34.7

35.5

33.6

33.0

33.9

'Risk-adjusted yield' (%)*

27.5

25.6

26.7

24.8

24.1

24.9

The same bad-loan ratios had already deteriorated during the previous 18 months.

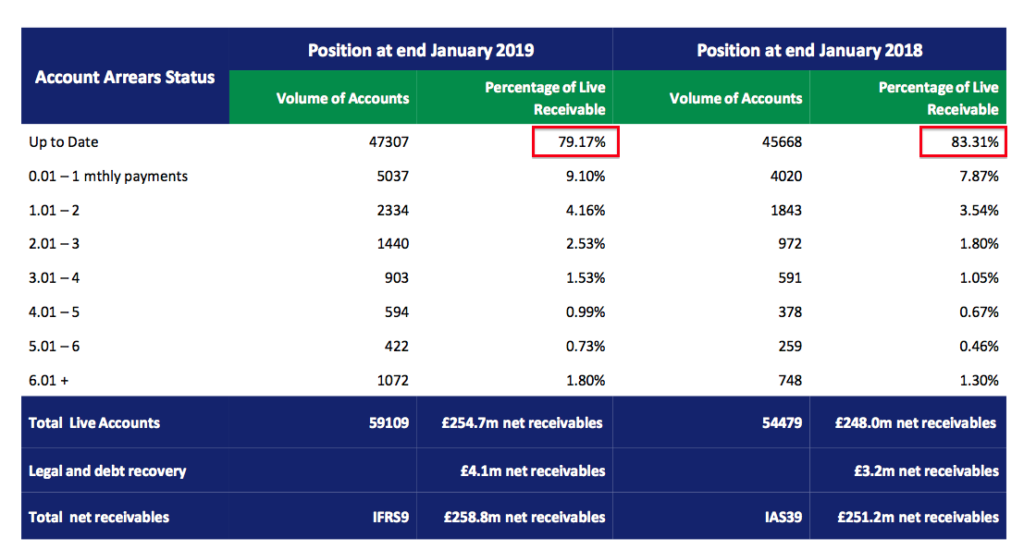

The proportion of up-to-date car-loan accounts declined once again:

The proportion of overdue car-loan accounts has actually doubled from 9.6% to 20% since 2016:

Year to 31 January

2016

2017

2018

2019

Motor

Up to date accounts

29,460

37,447

45,668

47,307

Overdue accounts

3,144

5,620

8,811

11,802

Total accounts

32,604

43,067

54,479

59,109

Up to date/Total (%)

90.4

87.0

83.8

80.0

Overdue/Total (%)

9.6

13.0

16.2

20.0

All this number-crunching clearly shows Advantage’s customers are no longer as profitable or reliable as they once were.

SUS admitted: “[The pressure on] working people’s average real incomes… persuaded some customers to take on newer forms of high cost credit financial obligations which resulted in slightly less consistent repayments to Advantage this year than we anticipated”.

At least SUS continues to tweak its loan-approval processes:

“Further underwriting changes, which clearly recognise these high-cost credit obligations, and marketing improvements to attract a better product mix, are designed to maintain returns and gradually return impairment levels to those of the past five years.”

This time last year SUS was performing “sensible gear changes” to moderate bad debts.

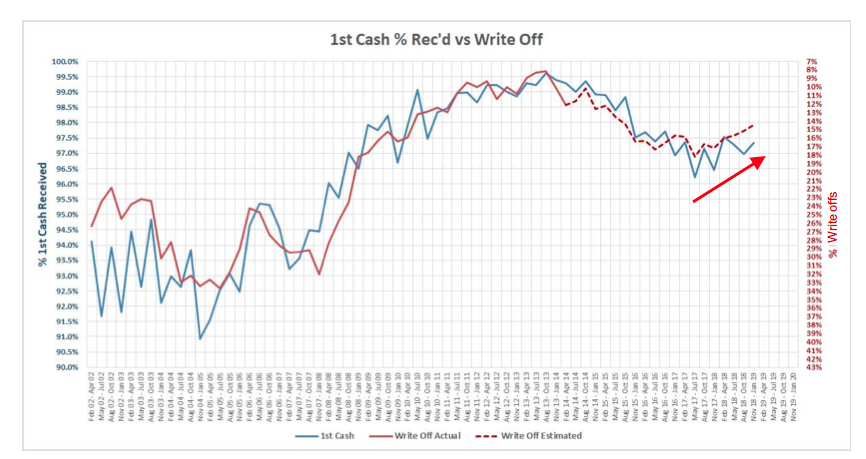

Reflecting the tweaks and changes, the proportion of new accounts that make their first payment on time has improved during the last 18 months (blue line, left axis):

SUS believes this first-payment improvement should lead to lower write-offs (dotted red line, right axis).

Also reflecting the tweaks and changes, the proportion of approved car-loan applicants has dropped from 32% to 23% during the last two years:

Year to 31 January

2017

2018

2019

Motor

Applications

over 750,000

over 860,00

over 1,000,000

Approvals (%)

c32%

c29%

c23%

Approvals

c240,000

c250,000

c230,000

Loans issued

20,042

24,518

21,053

Only 9% of approved applicants go on to accept their new car loan.

SUS has never really explained why the remaining 91% of approved applicants do not collect their loan.

Presumably the 91% have applied for multiple loans (usually through a broker) and then choose a cheaper lender — which would suggest Advantage has the best rates for only a small proportion of qualified borrowers.

The typical Advantage customer has a patchy credit history, borrows £6.2k and pays back £11.1k over 51 months — equivalent to a flat c18% interest rate:

Motor-finance customer numbers and loans outstanding

The tightened application criteria implemented by Advantage has reduced the rate of customer growth:

H1 2018

H2 2018

FY 2018

H1 2019

H2 2019

FY 2019

Motor

New agreements

12,542

11,976

11,412

11,822

9,231

21,053

Active customers

49,000*

-

54,479

58,008

-

59,109

Net customer increase

5,933

5,479

11,412

3,529

1,101

4,630

Customer loans (£k)

226,807

-

251,215

263,455

-

258,810

Change to customer loans (£k)

33,278

24,408

57,686

12,240

(4,645)

7,595

(*rounded by SUS)

New car-loan agreements had been running at c12k every six months. During the second half of 2019, the number fell to c9k.

SUS does not disclose the number of car-loan customers lost every year due to non-payment or full repayment.

However, my sums suggest the net increase to car-loan customers had been running at somewhere between 5k and 6k every six months during 2018.

During 2019, the net increase to car-loan customers fell to 3.5k during the first half and then to just 1k during the second (at least according to my sums).

Total outstanding car loans dropped by £5m to £259m during the second half of 2019.

December’s update reported total outstanding car loans were £276m. Total outstanding car loans therefore dropped by £9m during the final two months of the financial year.

As such, the effect of the aforementioned application tightening and/or the greater loan write-offs appears to have recently accelerated.

Aspen Bridging

Established two years ago, Aspen offers property bridging loans aimed at small/individual property developers/investors with awkward financial circumstances.

The average bridging loan is £375k with a monthly interest rate of “just over” 1% and a term of between 6 and 14 months. These case studies give a flavour of the borrowers involved:

The half-year split shows Aspen making very encouraging progress, with start-up losses having now turned into profit:

H1 2018

H2 2018

FY 2018

H1 2019

H2 2019

FY 2019

Revenue (£k)

86

813

899

1,190

1,653

2,843

Pre-tax profit (£k)

(280)

(18)

(298)

279

559

838

Bridging loans generate lower annual revenue (i.e. interest) than car loans for every £1 lent (19.5p vs. 33.9p):

H1 2018

H2 2018

FY 2018

H1 2019

H2 2019

FY 2019

Property

Loan provision (£k)

19

143

162

98

108

206

Revenue (£k)

86

813

899

1,190

1,653

2,843

Average customer loans (£k)

899

6,320

5,421

13,584

17,290

14,547

Loan provision/Revenue (%)

22.1

17.6

18.0

8.2

6.5

7.2

Loan provision/Average customer loans (%)

4.2

4.5

3.0

1.4

1.2

1.4

Revenue/Average customer loans (%)

19.1

25.7

16.6

17.5

19.1

19.5

'Risk-adjusted yield' (%)*

14.9

21.2

13.6

16.1

17.9

18.1

But bridging loans do enjoy lower rates of bad debts (7.2% vs. 26.6% of revenue).

The loans are secured on the property involved and repaid through the property’s onward sale or by re-mortgage. Every property is visited by Aspen before a loan is granted.

Aspen’s 18.1% ‘risk-adjusted yield’ compares to 24.9% at Advantage.

I suppose further expansion at Aspen and greater bad debts at Advantage could see their risk-adjusted yields meet in the middle.

For now at least, Aspen remains a small part of SUS. Outstanding bridging loans total £18m versus £259m for car loans.

SUS has high hopes for Aspen. Management anticipates “controlled revenue growth at Aspen of at least 50% per year over the next two years.”

50% revenue growth for two years equates to 125% growth.

Could Aspen become another Advantage — and go from start-up to an annual £30m-plus profit within 19 years?

SUS cites research that claims the property-bridging market could grow from £7.5 billion to £10 billion by 2021.

In comparison, the market for used cars bought on finance is £12 billion (point 1).

Margin and ROE

The 2018 annual report (point 11) says SUS borrows money from mainstream banks at 4% to then lend out at 31%.

The wide net interest margin is required to cover debt impairments and operating costs, but still led to a high 43.8% operating margin for 2019:

Year to 31 January

2015*

2016

2017

2018

2019

Operating margin (%)

45.6

47.0

44.4

41.3

43.8

Return on average equity (£k)

-

15.1

15.2

16.7

17.6

Return on average equity (£k)**

-

12.6

13.2

12.0

11.9

(*ROE figures not shown due to distortion following demerger of home-credit subsidiary **adjusted for debt and interest payments)

SUS requires a high level of profit to generate a respectable return on the equity that supports the business.

Since 2015, SUS’s shareholder equity has advanced by £84m to £165m while earnings have advanced by £16m to £28m.

The resultant incremental return on equity (ROE) during that period was an attractive £16m/£84m = 19%.

Note that SUS’s ROE is assisted by significant levels of debt.

Year-end net debt was £108m — more than 3x 2019 earnings of £28m.

Adjusted for debt and interest payments, the 2019 ROE falls to around 12%.

Adjusted for debt and interest payments, the incremental ROE for 2015 to 2019 falls to around 13%.

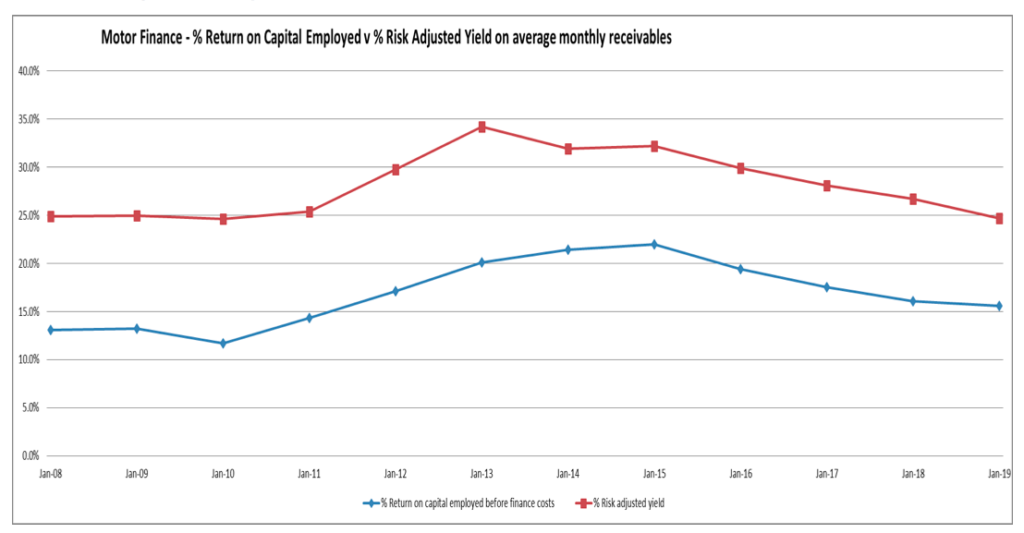

SUS calculates the return on capital employed (ROCE) within Advantage to be 15% for 2019 (red line):

The 3% difference between my ROE calculation and SUS’s ROCE calculation is due mostly to my calculation including tax.

Borrowings

SUS’s net debt has increased over time as cash flow was reinvested heavily into working capital (essentially new customer loans):

Year to 31 January

2015

2016

2017

2018

2019

Operating profit (£k)

16,445

21,251

26,871

32,978

39,101

Depreciation (£k)

129

426

253

294

414

Net capital expenditure (£k)

(601)

(396)

(308)

(1,040)

(785)

Working-capital movement (£k)

(8,576)

(6,057)

(48,488)

(68,881)

(19,041)

Net debt (£k)

(53,565)

(11,901)

(49,167)

(104,990)

(108,037)

The £19m absorbed into working capital for 2019 was split as a £21m outflowduring H1 and a £2m inflow during H2:

H1 2018

H2 2018

FY 2018

H1 2019

H2 2019

FY 2019

Operating profit (£k)

15,427

17,551

32,978

18,813

20,288

39,101

Working-capital movement (£k)

(34,725)

(34,156)

(68,881)

(21,056)

2,015

(19,041)

Other cash-flow movements (£k)

(3,373)

(4,142)

(7,515)

(4,649)

(4,881)

(9,530)

Operating cash flow (£k)

(22,671)

(20,747)

(43,418)

(6,892)

17,422

10,530

That H2 £2m inflow presumably followed the aforementioned tightening of Advantage’s application criteria — and reflected car-loan repayments exceeding new car-loans issued.

As such, operating cash flow during H2 was £17m — of which £13m was used to reduce debt.

The moderation of new car loans being issued could lead to further surplus cash generation and reduce debt during the current year.

Interest payments of £4.4m were covered a healthy 9x by operating profit during 2019.

SUS maintains a tiny defined-benefit pension scheme that last reported a surplus.

Valuation

SUS ended the year with total outstanding customer loans of £277m.

During H2, SUS earned revenue equivalent to 32.1% of outstanding customer loans.

Multiplying £277m by 32.1% gives possible revenue of £89m for the current year.

Also during H2, SUS recorded:

a bad-debt impairment equivalent to 26.3% of revenue;

other cost of sales equivalent to 17.7% of revenue, and;

administrative expenses equivalent to 12.5% of revenue.

Potential revenue of £89m less those percentage charges would leave a potential £39m operating profit.

Applying the 19% tax used in these results to a potential £39m operating profit delivers possible earnings of £31m or 261p per share.

Adding the £108m debt to the current £228m market cap gives an enterprise value (EV) of £336m or £28 per share

Dividing the £28 EV per share by my 261p EPS guess leads to a multiple of 10.7x.

The 118p per share dividend supports an appealing 6.2% income.

I bought SUS shares two years ago, since when the price has fallen 10% while earnings have gained 37% and the divided has advanced 30%.

Assuming the seasoned family management can continue to deliver its mantra of “steady, sustainable growth”, the shares do not appear expensive for patient investors.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

6 thoughts on “S & U: Record FY Results Show Dividend Up 12% But Management Hints Of Slowing Growth Leave Yield At 6%-Plus”

Hi Maynard

I’ve not studied S&U – just your (excellent) write up.

My work background was reinsurance underwriting – not a million miles from assessing the risks for lending money.

I imagine that the published figures are on an accounted during the report year basis? ie interest received & bad debts provisioned from all loans current – irrespective of when they were made?

Do they make “loan year” figs available? ie figures showing the loans made, flow of interest received, debt provisions over time in respect of all loans made during a particular year? This would be especially interesting to show how bad debt provisions evolve – I imagine these evolve from initially being anticipated default rates to actual experience over a number of years and it would show how good they are at estimating.

With accounted year figs and, especially, with a growing account, it’s very difficult to take a view on how adequately reserved they might be. In insurance, fast growth and under-reserving always ends in tears…. Independent Insurance being a classic example.

Personally, I’d be a bit jittery looking at your table under Motor-finance bad debts – bad debts up nearly fourfold on income just over double. How much (if any) of the later year bad debts relate to loans made in earlier years, but falling outside the provisions made then?

BUT – Accounting may be v different from insurance……

Hope these comments are of some interest!

Andy

Hello Andy

Thanks for the comment and apologies for the tardy reply.

Funny you should mention Independent Insurance — I had a near miss with IIG back in the day. I thankfully spotted the awful cash movements well before the share suspension.

Yes, the published figures are on an accounted-during-the-report-year basis — so from all loans current irrespective of when they were made.

“Loan year” figures are not published. So you can’t track back to an earlier year and compare the initial estimate to how much was eventually written off.

So there is a certain amount of trust given to the board, which has treated shareholders well over time.

I have done my best to study the latest figures (see my comment on the 2019 report below), and nothing strikes me as obviously untoward in terms of past provisioning. But the sharp rise in provisions may well come from under-provisioning from prior years — I don’t know.

This paragraph is published within each annual report and is a reminder of the importance of family management:

2) Industry stats

The report says the used-car finance market is worth £17bn and 900k used cars are purchased on HP:

The 2018 report said the market was £12bn and 700k used cars were purchased.

3) Complaints

94 complaints from 21k new accounts and 59k total accounts seems commendably low:

Most complaints concern the quality of the car, for which I assume SUS is not liable.

4) Testimonials

SUS included a customer testimonial that referred to an employee called ‘Natalie’:

‘Natalie’ must be an impressive employee, as she was also cited within the 2018 report:

5) Improvements within Advantage

SUS reckons changes made at Advantage can “reverse the marginal reduction… in both risk-adjusted yield and return on capital employed”:

The same wording was used within the 2018 annual report, yet both measures declined during 2019.

6) Risks

The only updated risk concerns Brexit:

7) Director pay

The executives received basic-pay rises of £10k or less during 2019:

Bonuses to the executive Coombs twins were modest:

Advantage Finance boss Guy Thompson remains the highest-paid executive (justifiably so), but notably did not collect a deferred bonus from 2018:

Not all of Mr Thompson’s shadow options vested as well.

I am encouraged SUS could perform well during 2019 and not every incentive was collected by Mr Thompson — his full targets would therefore appear reasonably stretching.

The board is due pay rises for 2020, to match the rise for the wider workforce:

8) Auditor

I see Deloitte has audited SUS for 21 years — a long time to engage the same auditor and probably in excess of quoted-company best practice.

9) Employees

The average cost per employee has declined during 2017, 2018 and 2019 (from £55k to £54k to £52k to £45k):

The total cost of the workforce as a proportion of total revenue has dropped from 13.6% to 11.2% to 9.6% to 9.0% during the same three years.

I am pleased SUS appears to be making employee savings in light of the rising bad-debt charge.

On the downside, revenue per Advantage Finance employee dropped from £540k to £498k during 2018, although the figure is still up on the £484k for 2017.

10) Loan loss provision

SUS adopted IFRS 9 for 2019 and presented its loan-loss provision (i.e. bad debt charge) slightly different to last year.

For background, this note explains Stages 1 and 3 (Stage 2 is not significant):

This next note tells us £23,186k was charged to earnings as a loan-loss provision, and £12,647k was actually written off:

The £58,213k figure is the net loan-loss provision accumulated over the years — i.e. the amount charged to earnings to date as a best guess of future write offs.

The 2018 annual report showed a £3,298k write-off (under IAS38)…

…a lot smaller than the £12,647k charged for 2019 (under IFRS 9).

Determining exactly whether SUS’s provisioning is conservative or not is difficult.

There is sadly no way to match up the loan loss provision of any one year to the subsequent write-offs — which may occur in any future year — to gauge how accurate the provisioning is.

Under the previous (IAS38) rules, some £12,322k was formally written off as bad (motor finance) debt during the five years 2014-2018.

That £12,322k does not seem too great much given net customer loans advanced from £53m to £251m during the same time.

Also, the representative APR on an Advantage loan is 29%:

But (motor finance) revenue as a proportion of average net customer (motor finance) loans was 34% during 2019 — the book-value of those loans would have to be c17% greater to arrive at 29%. As such, perhaps the provisioning and associated bookkeeping is adequate.

11) Interest rates

SUS says it lends out money at 30% (not the 29% quoted APR) and borrows at 4%:

12) Pension scheme

SUS’s final-salary pension scheme continues to carry a tiny surplus that is not displayed on the main balance sheet due to certain accounting rules:

13) Options

134k options represent a modest 1.1% of the share count:

A reassuring update that showed loan impairments starting to reduce. Here is the full text:

—————————————————————————————————————————— S&U, the motor finance and bridging lender, issues a trading update for the period 1 February 2019 to 22 May 2019, prior to its AGM being held today.

Advantage Finance, S&U’s motor finance business, continues to trade well with profits up on last year, whilst customer numbers now exceed 60,000 for the first time. Advantage’s continuing policy of focussing on debt quality is proving its worth in light of current economic uncertainty, with current collections up 6% compared to net receivables, at £263m, up 3% against last year. Similarly, impairment has shown recent improvement and rolling 12-month risk adjusted yield is now slightly improved at just over 25% (31 January 2019: 24.6%).

These healthy indicators are also reflected in the record number of applications for finance that Advantage is currently receiving, averaging over 108,000 per month. This has meant that, even within the tightened under-writing regime, recent transaction volumes and quality as recorded in tiered tranches are showing improvement.

Aspen Finance, S&U’s new property bridging lender, continues to make impressive progress. Its loan book now stands at £22m against £18m at year end, as its product range, introducer network and reputation continue to grow. This is evidenced in both the number of its recent illustrations and, most importantly, in its active deal pipeline, which is at a record level and has doubled over the period.

The Group’s current progress has been reflected since year-end in an increase in Group borrowing from £108m to nearly £114m. This is well within our budgeted requirements and within our recently increased £160m medium term facilities, providing ample headroom for our anticipated growth.

Commenting on S&U’s trading and outlook, Anthony Coombs, S&U Chairman, said:

“Recent trends in our business are encouraging, particularly in transaction growth, debt and new customer quality. Together with our tried and tested traditional emphasis on continuous process refinements and improvements for our customers, these give us confidence of further steady and sustainable growth and a successful year ahead.”

——————————————————————————————————————————

Here is the important line: “Similarly, impairment has shown recent improvement and rolling 12-month risk adjusted yield is now slightly improved at just over 25% (31 January 2019: 24.6%).”

The risk-adjusted yield is a group KPI that is calculated as (revenue less loan provision) divided by average customer loans. The red line within the chart below shows the figure has come in at 25% or more during the last ten years — apart from at the end of the 2019 financial year.

At least the ratio is back above 25%, which means the tweaks the group recently applied to its lending criteria may have taken effect. I have to admit I did not think the result of the lending tweaks would come though until next year.

Lending applications now run at 108k a month, up from 80k (+35%) from this time last year. So there is no shortage of people looking for a used car on finance.

With only minor movements to customer loans and debt, I am not minded to change my valuation sums from the blog post above.

I should add that I doubled my SUS holding during early April at £18.57 including all costs following my sale of Castings.

The informative event focused on the Advantage car-loan division, and allowed me to discuss the accounts at length with the finance director. A few interesting snippets were revealed during the presentation, too.

In attendance were the three group executives, plus two directors of Advantage plus the chief of the Finance Lease Association. The latter gave a presentation about the FLA which did not reveal anything too ground-breaking. Absent was Guy Thompson, the managing director of Advantage, due to illness.

Presenting for Advantage were i) Keith Charlton, deputy managing director and someone who was “very much involved” in founding the business with Guy Thompson, and ii) Alan Tuplin, credit risk director and an Advantage board member since 2008.

Here is my best recollection of what was said (mostly paraphrased):

1) Growth history

* Illustrious track record based on having “never deviated from quality service and product, and continual improvement”.

* Cost of sales increased during recent years due to increasing competition and higher processing costs.

* Profit per employee “very efficient”. 150 staff at Advantage in Grimsby.

* Employee culture has a “long-term over short-term mindset”

* Low staff turnover — 30% of Advantage staff have 10-plus years of service.

2) Regulation

* Advantage is fully compliant with current FCA regulation — long before the FCA became the regulator.

* Recent FCA investigation into non-prime lending led to “zero remedies” for Advantage,

3) Customer application

* Most customers now apply for car finance online first, then find their car.

* Applications received by Advantage are almost always through loan brokers or car dealers.

* During April 2019, 112k applications were received, 26k then approved and 2k then completed.

* Completed applications fall into 5 tiers: A, B, C, D and E.

* Tier A contains lower-risk customers paying lower interest rates. Tier E contains higher-risk customers paying higher interest rates.

* The tiers are split: A: 28%, B: 19%, C: 19%, D: 21% and E: 13%.

* The split between tiers has not changed much over the years. Tier A has fluctuated between high 20s and low 20s. More competition within Tier A than Tier E.

* Of the 26k approved in April, 24k did not complete due to a mix of i) customers deciding not to buy a car, ii) the chosen car not being acceptable to Advantage (e.g. too old, high mileage etc), or iii) more usually, a cheaper loan is found elsewhere.

* On ii), Advantage is legally responsible for the quality of the car. Hire-purchase rules dictate the dealer sells the car to Advantage, which in turn hires out the car to the customer. Advantage has to consider likelihood of the car going wrong. (I guess this liability explains why Advantage may have lost some complaints taken to the Financial Ombudsman — the quality of the car was poor.)

* On iii) rival lenders are taking on risks Advantage would not (i.e. Advantage strongly implied these rivals are likely to lose money).

* Advantage customers are not that price sensitive. They simply decide whether they can afford, say, £200 a month rather than look at the interest rate.

* The loan brokers and introducers are price sensitive. Brokers/introducers generally receive a flat fee from Advantage for a completed lead.

* Customers are deemed to be ‘non-prime’, but not ‘sub-prime’. ‘Non-prime’ and ‘sub-prime’ have different meanings depending on the financial institution. Advantage caters for borrowers that have “had a problem in the past but are on an upward trend”

* Example situation given was a borrower that is two months behind on a loan. Has the loan gone from zero to one to two months behind, or from four to three to two months behind? The latter shows the borrower intending to make up the shortfall — an improving trend. Intent of the customer and past behaviour are important when evaluating applications.

* Shareholders must remember that Advantage “sells to people, not algorithms” — so manual processing and employee judgement still involved.

4) Credit scores

* “Uniquely in financial services”, Advantage creates its own credit file based on credit agencies (Experian, TransUnion), Gov.uk, ONS, Zoopla (rent data).

* Algorithm then creates in-house scorecard result to judge credit-worthiness within 10 seconds of online application.

* Years of past borrower behaviour and previous customer records help the algorithm .

* Conversation with Zoopla suggested Advantage could sell on its in-house credit scores to others — though SUS not sure of that suggestion due to giving valuable information to competitors.

5) Technology

* Advantage started in 1999 — division decided to build own tech and focus on online (no call centres etc). Decision has been crucial in Advantage’s success. Company employs own programmers and built own CRM — which allows firm to control development. No tech outsourcing.

* Firm will soon revamp its own website in the hope of gaining direct custom — should not affect leads from dealers/brokers etc.

6) Loan provisions

* The recent rise to loan provisions was caused by borrowers finding alternatives to payday loans, the lending rules for which were tightened a few years ago.

* The effect of the alternatives had slipped through Advantage’s processing until the number of defaults increased from borrowers possessing such alternatives.

* The oversight occurred mostly during the year to January 2018.

* No questions about loan provisions were asked during the presentation Q&A.

* I now understand why some loans appear ‘impaired’ in this note:

* The ‘impaired’ loans (in the red box) are those where part of their value has been reduced by the likelihood of non payment.

* The impaired loans reflect the residual value of the loan Advantage still expects to collect — discounted back to today’s money.

* When a loan goes from ‘not impaired’ to ‘impaired’ (and moves into the red box), Advantage re-calculates the loan’s book value given the greater likelihood that part of the loan will never be repaid.

* The difference between the non-impaired and impaired value of the loan (i.e. the impairment) is taken to the income statement as a loan loss provision (i.e. a bad debt).

* Further impairments of impaired loans will also be taken as a provision through the income statement.

* The annual report note explaining impairments is here:

* As well as the impairments arising from individual loans, a collective loan loss provision is also charged to the income statement based on loans issued during the previous 12 months:

* This note shows the impairments of older loans (‘net transfers and changes in credit risk’) and later loans (‘new loans originated’).

* The IFRS 9 note format above was new for 2019. The note suggests Advantage under-estimated the impairment of older loans by £11,402k.

* However, loan provisions are guesswork until the amount is formally written off a few years down the line.

* This chart from the 2019 annual results presentation is useful:

* Ignoring the banking crash year of 2008, loans issued between 2009 and 2014 — where repayments are now all but completed — were reasonably consistent for both collections after 30 months and total collections.

* The chart suggests the capital of a typical Advantage loan is repaid after almost 30 months (when repayments equal 100% of the loan capital), and interest representing approximately 50% of the original loan capital is eventually paid to arrive at the 150% collection figure (the average loan lasts for 4 years 4 months).

* Future editions of this chart ought to show similar-ish 110% and 150% figures. But I suspect the growing impairment charge of the last few years could mean the figures are closer to 100% and 140%.

This update did not read too badly. Here is the full text:

————————————————————————————————————

S&U PLC, the motor finance and property bridging specialist, today issues a trading update for the period from its AGM statement of the 23rd May to the 31st July 2019. It will announce half year results on the 24th September 2019.

Trading

Both our motor finance, Advantage Finance, and our property bridging, Aspen, companies continue to trade well and in line with our expectations. In contrast with the current low levels of consumer confidence in the UK, demand for Advantage’s motor finance is healthy and transactions are ahead of last year. Indeed, despite a recent downturn in the new car market, the used car market remains robust and is likely to continue to do so, even assuming a “no-deal” Brexit.

Whilst activity in the housing market remains subdued, valuations continue to be steady and profitable growth at Aspen continues, albeit at a slightly slower pace than anticipated.

Advantage Finance

During the period, the pace of growth in both applications and transactions continue to accelerate . Advantage now receives over 110,000 applications per month and new transactions are ahead of last year. Customer numbers now stand at a record 62,000, up 7% on last year.

Following the reported tightening of underwriting last year, collections for the half year are up by 7% on the same period last year, and early repayment indicators on new business continue to show improvement.

In a competitive and evolving market, Advantage’s relationships with its introducer partners continue to grow and deepen and recent reward and IT platform changes are consolidating this.

Aspen

The property bridging market depends principally on values and activity within the housing market. Whilst the former has been firm, the latter has slowed, partly due to uncertainty around Brexit and around Government stability. Aspen therefore continues to gradually build its bridging book and net amounts receivable at half year stand at over £24m (2018: £16.3m).

Recent improvements to Aspen’s loan products, a wider product range and closer alignment of its IT platform with its large introducers are expected to help continue increasing our bridging receivables during H2.

Funding

At the period end Group borrowing stood at just over £125m, well within our medium-term facilities of £160m.

Commenting on the Group’s trading and outlook, Anthony Coombs, S&U chairman, said:

“Trading in the first half of the year reflects continued and consistent growth in profitability which has been the S&U hallmark over the past 10 years. Transaction volumes and quality improvement, particularly in our motor finance business, are expected to be reflected in the pace of profits growth over the full year.”

————————————————————————————————————

More than 110,000 motor-finance applications a month compare with more than 80,000 this time last year, up c37%. So, not shortage of demand.

Since May’s trading update, customer numbers have advanced by 2,000 to 62,000 and by 3,000 since the January year end (i.e. during the first half of the current year). The second half of the previous year saw ‘active’ customer numbers increase by only c1,000, so perhaps competition among other lenders may have reduced of late to SUS’s benefit.

Reflecting the additional customers, debt has grown from £108m at the year-end to £114m during May and £125m now. No mention of customer receivables was made, so I will revisit my valuations after September’s half-year results.

Aspen’s loan book has advanced by £6m since the year end and £2m since May to stand at over £24m. The reference to “improvements” to Aspen’s loan products could mean the scale of the loan size. I understand Aspen was initially viewed by intermediaries as ‘not being serious’ due to the initial small-ish size of the loans available.

Rhys Thomas: “Maynard, I have really enjoyed reading your column, and your original contributions back in the TMF days. Many thanks for…” 30 Mar 2026

Roger: “I’m late to the party with my comments – apologies. I’m sorry that you have to stop and enjoyed reading…” 27 Mar 2026

Johnny boy: “Maynard, I have really enjoyed reading you write-ups over the years. Please don’t lose your passion for individual stock picking.…” 16 Mar 2026

NIGEL: “Maynard I would also like to thank you for all the work you have done over the years. I have…” 25 Feb 2026

James H: “Hi Maynard, I’d like to put on record my thanks to you for all of the content over recent years.…” 14 Jan 2026

Zach: “Hello Maynard, You may or may not remember me. I joined the company you retired from just a month or…” 09 Jan 2026

Simon Brenncke: “Thanks for this instructive summary of your portfolio developments, and all the best!” 09 Jan 2026

Anonymous: “Thank you for such meticulous and fascinating insight over the years. I’ve only followed your output relating to one company…” 07 Jan 2026

Hi Maynard

I’ve not studied S&U – just your (excellent) write up.

My work background was reinsurance underwriting – not a million miles from assessing the risks for lending money.

I imagine that the published figures are on an accounted during the report year basis? ie interest received & bad debts provisioned from all loans current – irrespective of when they were made?

Do they make “loan year” figs available? ie figures showing the loans made, flow of interest received, debt provisions over time in respect of all loans made during a particular year? This would be especially interesting to show how bad debt provisions evolve – I imagine these evolve from initially being anticipated default rates to actual experience over a number of years and it would show how good they are at estimating.

With accounted year figs and, especially, with a growing account, it’s very difficult to take a view on how adequately reserved they might be. In insurance, fast growth and under-reserving always ends in tears…. Independent Insurance being a classic example.

Personally, I’d be a bit jittery looking at your table under Motor-finance bad debts – bad debts up nearly fourfold on income just over double. How much (if any) of the later year bad debts relate to loans made in earlier years, but falling outside the provisions made then?

BUT – Accounting may be v different from insurance……

Hope these comments are of some interest!

Andy

Hello Andy

Thanks for the comment and apologies for the tardy reply.

Funny you should mention Independent Insurance — I had a near miss with IIG back in the day. I thankfully spotted the awful cash movements well before the share suspension.

Yes, the published figures are on an accounted-during-the-report-year basis — so from all loans current irrespective of when they were made.

“Loan year” figures are not published. So you can’t track back to an earlier year and compare the initial estimate to how much was eventually written off.

So there is a certain amount of trust given to the board, which has treated shareholders well over time.

I have done my best to study the latest figures (see my comment on the 2019 report below), and nothing strikes me as obviously untoward in terms of past provisioning. But the sharp rise in provisions may well come from under-provisioning from prior years — I don’t know.

The subject requires further investigation.

Maynard

S & U (SUS)

Publication of 2019 annual report

Here are the snippets of interest:

1) Business philosophy

This paragraph is published within each annual report and is a reminder of the importance of family management:

2) Industry stats

The report says the used-car finance market is worth £17bn and 900k used cars are purchased on HP:

The 2018 report said the market was £12bn and 700k used cars were purchased.

3) Complaints

94 complaints from 21k new accounts and 59k total accounts seems commendably low:

Most complaints concern the quality of the car, for which I assume SUS is not liable.

4) Testimonials

SUS included a customer testimonial that referred to an employee called ‘Natalie’:

‘Natalie’ must be an impressive employee, as she was also cited within the 2018 report:

5) Improvements within Advantage

SUS reckons changes made at Advantage can “reverse the marginal reduction… in both risk-adjusted yield and return on capital employed”:

The same wording was used within the 2018 annual report, yet both measures declined during 2019.

6) Risks

The only updated risk concerns Brexit:

7) Director pay

The executives received basic-pay rises of £10k or less during 2019:

Bonuses to the executive Coombs twins were modest:

Advantage Finance boss Guy Thompson remains the highest-paid executive (justifiably so), but notably did not collect a deferred bonus from 2018:

Not all of Mr Thompson’s shadow options vested as well.

I am encouraged SUS could perform well during 2019 and not every incentive was collected by Mr Thompson — his full targets would therefore appear reasonably stretching.

The board is due pay rises for 2020, to match the rise for the wider workforce:

8) Auditor

I see Deloitte has audited SUS for 21 years — a long time to engage the same auditor and probably in excess of quoted-company best practice.

9) Employees

The average cost per employee has declined during 2017, 2018 and 2019 (from £55k to £54k to £52k to £45k):

The total cost of the workforce as a proportion of total revenue has dropped from 13.6% to 11.2% to 9.6% to 9.0% during the same three years.

I am pleased SUS appears to be making employee savings in light of the rising bad-debt charge.

On the downside, revenue per Advantage Finance employee dropped from £540k to £498k during 2018, although the figure is still up on the £484k for 2017.

10) Loan loss provision

SUS adopted IFRS 9 for 2019 and presented its loan-loss provision (i.e. bad debt charge) slightly different to last year.

For background, this note explains Stages 1 and 3 (Stage 2 is not significant):

This next note tells us £23,186k was charged to earnings as a loan-loss provision, and £12,647k was actually written off:

The £58,213k figure is the net loan-loss provision accumulated over the years — i.e. the amount charged to earnings to date as a best guess of future write offs.

The 2018 annual report showed a £3,298k write-off (under IAS38)…

…a lot smaller than the £12,647k charged for 2019 (under IFRS 9).

Determining exactly whether SUS’s provisioning is conservative or not is difficult.

There is sadly no way to match up the loan loss provision of any one year to the subsequent write-offs — which may occur in any future year — to gauge how accurate the provisioning is.

Under the previous (IAS38) rules, some £12,322k was formally written off as bad (motor finance) debt during the five years 2014-2018.

That £12,322k does not seem too great much given net customer loans advanced from £53m to £251m during the same time.

Also, the representative APR on an Advantage loan is 29%:

But (motor finance) revenue as a proportion of average net customer (motor finance) loans was 34% during 2019 — the book-value of those loans would have to be c17% greater to arrive at 29%. As such, perhaps the provisioning and associated bookkeeping is adequate.

11) Interest rates

SUS says it lends out money at 30% (not the 29% quoted APR) and borrows at 4%:

12) Pension scheme

SUS’s final-salary pension scheme continues to carry a tiny surplus that is not displayed on the main balance sheet due to certain accounting rules:

13) Options

134k options represent a modest 1.1% of the share count:

Maynard

S & U (SUS)

AGM Statement and Trading Update

A reassuring update that showed loan impairments starting to reduce. Here is the full text:

——————————————————————————————————————————

S&U, the motor finance and bridging lender, issues a trading update for the period 1 February 2019 to 22 May 2019, prior to its AGM being held today.

Advantage Finance, S&U’s motor finance business, continues to trade well with profits up on last year, whilst customer numbers now exceed 60,000 for the first time. Advantage’s continuing policy of focussing on debt quality is proving its worth in light of current economic uncertainty, with current collections up 6% compared to net receivables, at £263m, up 3% against last year. Similarly, impairment has shown recent improvement and rolling 12-month risk adjusted yield is now slightly improved at just over 25% (31 January 2019: 24.6%).

These healthy indicators are also reflected in the record number of applications for finance that Advantage is currently receiving, averaging over 108,000 per month. This has meant that, even within the tightened under-writing regime, recent transaction volumes and quality as recorded in tiered tranches are showing improvement.

Aspen Finance, S&U’s new property bridging lender, continues to make impressive progress. Its loan book now stands at £22m against £18m at year end, as its product range, introducer network and reputation continue to grow. This is evidenced in both the number of its recent illustrations and, most importantly, in its active deal pipeline, which is at a record level and has doubled over the period.

The Group’s current progress has been reflected since year-end in an increase in Group borrowing from £108m to nearly £114m. This is well within our budgeted requirements and within our recently increased £160m medium term facilities, providing ample headroom for our anticipated growth.

Commenting on S&U’s trading and outlook, Anthony Coombs, S&U Chairman, said:

“Recent trends in our business are encouraging, particularly in transaction growth, debt and new customer quality. Together with our tried and tested traditional emphasis on continuous process refinements and improvements for our customers, these give us confidence of further steady and sustainable growth and a successful year ahead.”

——————————————————————————————————————————

Here is the important line: “Similarly, impairment has shown recent improvement and rolling 12-month risk adjusted yield is now slightly improved at just over 25% (31 January 2019: 24.6%).”

The risk-adjusted yield is a group KPI that is calculated as (revenue less loan provision) divided by average customer loans. The red line within the chart below shows the figure has come in at 25% or more during the last ten years — apart from at the end of the 2019 financial year.

At least the ratio is back above 25%, which means the tweaks the group recently applied to its lending criteria may have taken effect. I have to admit I did not think the result of the lending tweaks would come though until next year.

Lending applications now run at 108k a month, up from 80k (+35%) from this time last year. So there is no shortage of people looking for a used car on finance.

With only minor movements to customer loans and debt, I am not minded to change my valuation sums from the blog post above.

I should add that I doubled my SUS holding during early April at £18.57 including all costs following my sale of Castings.

Maynard

S & U

Capital Markets Day

I attended SUS’s capital markets day event on 15 May. Here are the presentation slides.

The informative event focused on the Advantage car-loan division, and allowed me to discuss the accounts at length with the finance director. A few interesting snippets were revealed during the presentation, too.

In attendance were the three group executives, plus two directors of Advantage plus the chief of the Finance Lease Association. The latter gave a presentation about the FLA which did not reveal anything too ground-breaking. Absent was Guy Thompson, the managing director of Advantage, due to illness.

Presenting for Advantage were i) Keith Charlton, deputy managing director and someone who was “very much involved” in founding the business with Guy Thompson, and ii) Alan Tuplin, credit risk director and an Advantage board member since 2008.

Here is my best recollection of what was said (mostly paraphrased):

1) Growth history

* Illustrious track record based on having “never deviated from quality service and product, and continual improvement”.

* Cost of sales increased during recent years due to increasing competition and higher processing costs.

* Profit per employee “very efficient”. 150 staff at Advantage in Grimsby.

* Employee culture has a “long-term over short-term mindset”

* Low staff turnover — 30% of Advantage staff have 10-plus years of service.

2) Regulation

* Advantage is fully compliant with current FCA regulation — long before the FCA became the regulator.

* Recent FCA investigation into non-prime lending led to “zero remedies” for Advantage,

3) Customer application

* Most customers now apply for car finance online first, then find their car.

* Applications received by Advantage are almost always through loan brokers or car dealers.

* During April 2019, 112k applications were received, 26k then approved and 2k then completed.

* Completed applications fall into 5 tiers: A, B, C, D and E.

* Tier A contains lower-risk customers paying lower interest rates. Tier E contains higher-risk customers paying higher interest rates.

* The tiers are split: A: 28%, B: 19%, C: 19%, D: 21% and E: 13%.

* The split between tiers has not changed much over the years. Tier A has fluctuated between high 20s and low 20s. More competition within Tier A than Tier E.

* Of the 26k approved in April, 24k did not complete due to a mix of i) customers deciding not to buy a car, ii) the chosen car not being acceptable to Advantage (e.g. too old, high mileage etc), or iii) more usually, a cheaper loan is found elsewhere.

* On ii), Advantage is legally responsible for the quality of the car. Hire-purchase rules dictate the dealer sells the car to Advantage, which in turn hires out the car to the customer. Advantage has to consider likelihood of the car going wrong. (I guess this liability explains why Advantage may have lost some complaints taken to the Financial Ombudsman — the quality of the car was poor.)

* On iii) rival lenders are taking on risks Advantage would not (i.e. Advantage strongly implied these rivals are likely to lose money).

* Advantage customers are not that price sensitive. They simply decide whether they can afford, say, £200 a month rather than look at the interest rate.

* The loan brokers and introducers are price sensitive. Brokers/introducers generally receive a flat fee from Advantage for a completed lead.

* Customers are deemed to be ‘non-prime’, but not ‘sub-prime’. ‘Non-prime’ and ‘sub-prime’ have different meanings depending on the financial institution. Advantage caters for borrowers that have “had a problem in the past but are on an upward trend”

* Example situation given was a borrower that is two months behind on a loan. Has the loan gone from zero to one to two months behind, or from four to three to two months behind? The latter shows the borrower intending to make up the shortfall — an improving trend. Intent of the customer and past behaviour are important when evaluating applications.

* Shareholders must remember that Advantage “sells to people, not algorithms” — so manual processing and employee judgement still involved.

4) Credit scores

* “Uniquely in financial services”, Advantage creates its own credit file based on credit agencies (Experian, TransUnion), Gov.uk, ONS, Zoopla (rent data).

* Algorithm then creates in-house scorecard result to judge credit-worthiness within 10 seconds of online application.

* Years of past borrower behaviour and previous customer records help the algorithm .

* Conversation with Zoopla suggested Advantage could sell on its in-house credit scores to others — though SUS not sure of that suggestion due to giving valuable information to competitors.

5) Technology

* Advantage started in 1999 — division decided to build own tech and focus on online (no call centres etc). Decision has been crucial in Advantage’s success. Company employs own programmers and built own CRM — which allows firm to control development. No tech outsourcing.

* Firm will soon revamp its own website in the hope of gaining direct custom — should not affect leads from dealers/brokers etc.

6) Loan provisions

* The recent rise to loan provisions was caused by borrowers finding alternatives to payday loans, the lending rules for which were tightened a few years ago.

* The effect of the alternatives had slipped through Advantage’s processing until the number of defaults increased from borrowers possessing such alternatives.

* The oversight occurred mostly during the year to January 2018.

* No questions about loan provisions were asked during the presentation Q&A.

* I now understand why some loans appear ‘impaired’ in this note:

* The ‘impaired’ loans (in the red box) are those where part of their value has been reduced by the likelihood of non payment.

* The impaired loans reflect the residual value of the loan Advantage still expects to collect — discounted back to today’s money.

* When a loan goes from ‘not impaired’ to ‘impaired’ (and moves into the red box), Advantage re-calculates the loan’s book value given the greater likelihood that part of the loan will never be repaid.

* The difference between the non-impaired and impaired value of the loan (i.e. the impairment) is taken to the income statement as a loan loss provision (i.e. a bad debt).

* Further impairments of impaired loans will also be taken as a provision through the income statement.

* The annual report note explaining impairments is here:

* As well as the impairments arising from individual loans, a collective loan loss provision is also charged to the income statement based on loans issued during the previous 12 months:

* This note shows the impairments of older loans (‘net transfers and changes in credit risk’) and later loans (‘new loans originated’).

* The IFRS 9 note format above was new for 2019. The note suggests Advantage under-estimated the impairment of older loans by £11,402k.

* However, loan provisions are guesswork until the amount is formally written off a few years down the line.

* This chart from the 2019 annual results presentation is useful:

* Ignoring the banking crash year of 2008, loans issued between 2009 and 2014 — where repayments are now all but completed — were reasonably consistent for both collections after 30 months and total collections.

* The chart suggests the capital of a typical Advantage loan is repaid after almost 30 months (when repayments equal 100% of the loan capital), and interest representing approximately 50% of the original loan capital is eventually paid to arrive at the 150% collection figure (the average loan lasts for 4 years 4 months).

* Future editions of this chart ought to show similar-ish 110% and 150% figures. But I suspect the growing impairment charge of the last few years could mean the figures are closer to 100% and 140%.

Maynard

S & U (SUS)

Trading update

This update did not read too badly. Here is the full text:

————————————————————————————————————

S&U PLC, the motor finance and property bridging specialist, today issues a trading update for the period from its AGM statement of the 23rd May to the 31st July 2019. It will announce half year results on the 24th September 2019.

Trading

Both our motor finance, Advantage Finance, and our property bridging, Aspen, companies continue to trade well and in line with our expectations. In contrast with the current low levels of consumer confidence in the UK, demand for Advantage’s motor finance is healthy and transactions are ahead of last year. Indeed, despite a recent downturn in the new car market, the used car market remains robust and is likely to continue to do so, even assuming a “no-deal” Brexit.

Whilst activity in the housing market remains subdued, valuations continue to be steady and profitable growth at Aspen continues, albeit at a slightly slower pace than anticipated.

Advantage Finance

During the period, the pace of growth in both applications and transactions continue to accelerate . Advantage now receives over 110,000 applications per month and new transactions are ahead of last year. Customer numbers now stand at a record 62,000, up 7% on last year.

Following the reported tightening of underwriting last year, collections for the half year are up by 7% on the same period last year, and early repayment indicators on new business continue to show improvement.

In a competitive and evolving market, Advantage’s relationships with its introducer partners continue to grow and deepen and recent reward and IT platform changes are consolidating this.

Aspen

The property bridging market depends principally on values and activity within the housing market. Whilst the former has been firm, the latter has slowed, partly due to uncertainty around Brexit and around Government stability. Aspen therefore continues to gradually build its bridging book and net amounts receivable at half year stand at over £24m (2018: £16.3m).

Recent improvements to Aspen’s loan products, a wider product range and closer alignment of its IT platform with its large introducers are expected to help continue increasing our bridging receivables during H2.

Funding

At the period end Group borrowing stood at just over £125m, well within our medium-term facilities of £160m.

Commenting on the Group’s trading and outlook, Anthony Coombs, S&U chairman, said:

“Trading in the first half of the year reflects continued and consistent growth in profitability which has been the S&U hallmark over the past 10 years. Transaction volumes and quality improvement, particularly in our motor finance business, are expected to be reflected in the pace of profits growth over the full year.”

————————————————————————————————————

More than 110,000 motor-finance applications a month compare with more than 80,000 this time last year, up c37%. So, not shortage of demand.

Since May’s trading update, customer numbers have advanced by 2,000 to 62,000 and by 3,000 since the January year end (i.e. during the first half of the current year). The second half of the previous year saw ‘active’ customer numbers increase by only c1,000, so perhaps competition among other lenders may have reduced of late to SUS’s benefit.

Reflecting the additional customers, debt has grown from £108m at the year-end to £114m during May and £125m now. No mention of customer receivables was made, so I will revisit my valuations after September’s half-year results.

Aspen’s loan book has advanced by £6m since the year end and £2m since May to stand at over £24m. The reference to “improvements” to Aspen’s loan products could mean the scale of the loan size. I understand Aspen was initially viewed by intermediaries as ‘not being serious’ due to the initial small-ish size of the loans available.

Maynard