22 May 2019

By Maynard Paton

Results verdict on Andrews Sykes (ASY):

- Very favourable weather helped revenue gain 10% and profit jump 18% to set new records.

- European sales soared 24% to represent almost a quarter of the business, and continue to offer further potential.

- Accounts showcased wonderful margins, robust returns on equity, reassuring cash levels and respectable cash flow.

- Absence of “cautiously optimistic for further success” within management’s outlook hinted that 2019 may not be as buoyant as 2018.

- The underlying P/E could be 16 while the yield is 3.3%. I continue to hold.

Contents

- Event links and share data

- Why I own ASY

- Results summary

- Revenue, profit and dividend

- Balance sheet and cash flow

- Valuation

Event link and share data

Event: Final results for the twelve months to 31 December 2018 published 10 May 2019

Price: 720p

Shares in issue: 42,174,359

Market capitalisation: £304m

Why I own ASY

- Supplies air conditioners, portable heaters and industrial pumps for hire, with success based on a prompt 24/7 service, high-quality rental fleet and commercial-only customer base.

- Accounts regularly display high margins, generous cash flow, net cash and attractive returns on equity.

- Chairman and family enjoy a 90%/£272m shareholding and ensure management focuses on “long-term shareholder value creation”.

Further reading: My ASY Buy report |All my ASY posts | ASY website

Results summary

Revenue, profit and dividend

- Widespread snow followed by a long heatwave were always going to prompt extra demand for ASY’s heaters and air conditioners during 2018.

- ASY’s first-half statement had already revealed record figures, with the most severe winter since 2010 helping profit advance 14%.

- The glorious summer — apparently the joint warmest since records began — then ensured bumper numbers for the second half.

- ASY said: “During the first quarter a period of very cold weather created good opportunities for our heating and boiler hire activities and this was followed by a long hot summer which provided excellent opportunities for our air conditioning and chiller products.”

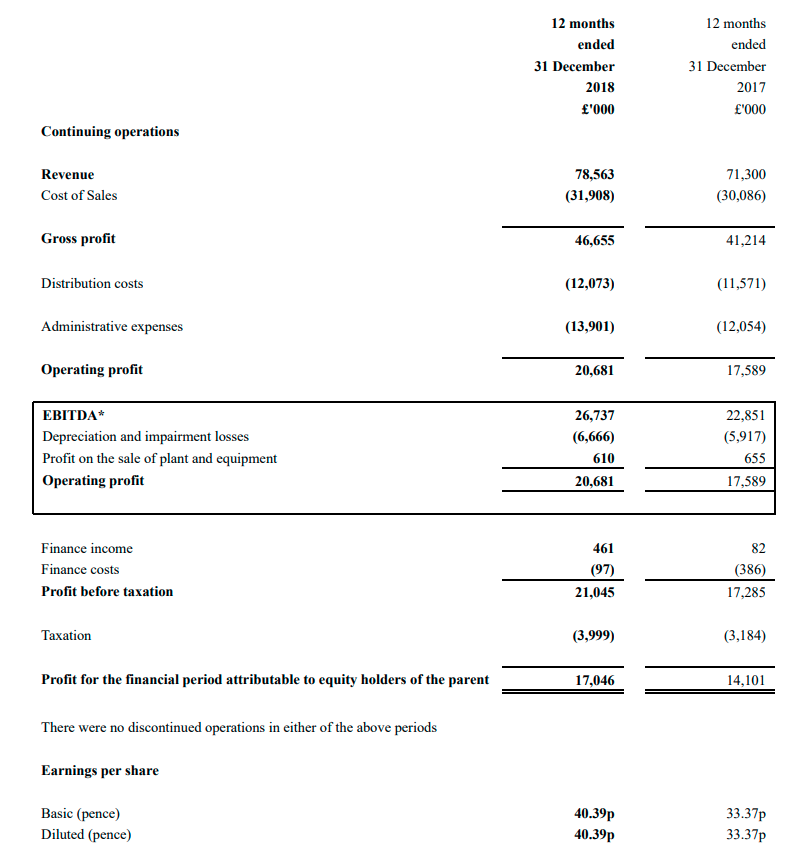

- For the full year, revenue gained 10% while operating profit climbed 18%. Both measures set fresh annual highs:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (£k) | 56,400 | 60,058 | 65,389 | 71,300 | 78,563 |

| Operating profit (£k) | 11,311 | 13,208 | 15,816 | 17,589 | 20,681 |

| Finance income (£k) | (72) | 159 | 1,725 | (304) | 364 |

| Other items (£k) | 517 | - | - | - | - |

| Pre-tax profit (£k) | 11,756 | 13,367 | 17,541 | 17,285 | 21,045 |

| Earnings per share (p) | 22.0 | 25.6 | 34.3 | 33.4 | 40.4 |

| Dividend per share (p) | 23.8 | 23.8 | 23.8 | 23.8 | 23.8 |

- ASY’s UK revenue improved 10% to £49m while the group’s European revenue jumped 24% to £18m. Middle Eastern revenue remained at £11m.

- All six of ASY’s European operations appeared to do well (point 1):

- Netherlands: “strong growth”

- Belgium: “year-on-year growth”

- Luxembourg: “significant growth”

- Italy: “additional revenue and profit”

- France: “further growth”

- Switzerland: “a successful year”

- ASY’s European depots now produce 23% of group revenue versus 17% five years ago and 10% ten years ago.

- The relocation of ASY’s main Dutch and Italian depots to “much larger” facilities that can “support further growth” underpins the prospect of additional European progress.

- ASY also plans to open more depots to serve the whole of France.

- The second-half figures showed revenue up 13% and profit up 21%:

| H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | ||

| Revenue (£k) | 35,334 | 35,966 | 71,300 | 37,815 | 40,748 | 78,563 | |

| Operating profit (£k) | 8,171 | 9,418 | 17,589 | 9,280 | 11,401 | 20,681 |

- ASY stated: “Traditionally, the group makes more profit in the second half year due to the higher profit margins on its air conditioning products which are hired predominantly in the second half of the year. The effect this year was even more pronounced than normal due to the long and hot summer throughout Northern Europe providing excellent opportunities for this area of our business.”

- Management comments at the 2016 AGM indicated i) additional demand for air conditioners starts if temperatures hit 27-28 degrees for a couple of weeks, and; ii) an extended heatwave could produce £4-5m of extra revenue.

- ASY’s robust profit growth did not lead to a divided lift. The payout has now been unchanged for four years.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Balance sheet and cash flow

- ASY’s accounts are still in excellent health.

- Margins and returns on equity continue to be attractive:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating margin (%) | 20.1 | 22.0 | 24.2 | 24.7 | 26.3 |

| Return on average equity (%) | 21.7 | 25.2 | 31.5 | 27.8 | 30.3 |

- The main UK and European divisions reported a combined 30% operating margin for 2018. The Middle Eastern operation delivered a 22% margin.

- My return on equity calculation in the table above does not adjust for ASY’s net £23m cash position.

- During the five years to 2018, ASY has lifted earnings by £5.5m and increased its shareholder equity by £15.1m. The resultant incremental return on equity is a super 36%.

- Earnings of £17m during 2018 converted into free cash flow of £13m following £4m invested into extra working capital:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating profit (£k) | 11,311 | 13,208 | 15,816 | 17,589 | 20,681 |

| Depreciation and amortisation (£k) | 4,563 | 4,959 | 5,310 | 5,917 | 6,666 |

| Net capital expenditure (£k) | (3,216) | (4,523) | (4,719) | (4,929) | (6,198) |

| Working-capital movement (£k) | (1,569) | (3,090) | (2,157) | (1,155) | (4,292) |

| Net cash (£k) | 16,846 | 14,558 | 17,673 | 20,293 | 23,381 |

- Net capital expenditure continues to be covered by the depreciation charged against earnings.

- ASY’s working capital has absorbed £12m since 2014. Buying extra equipment to hold as stock and then sell (rather than hire) has been the main working-capital demand:

| Year to 31 December | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating profit (£k) | 11,311 | 13,208 | 15,816 | 17,589 | 20,681 |

| Working-capital movements | |||||

| Stocks (£k) | (2,527) | (1,024) | (2,251) | (1,022) | (2,682) |

| Trade and other receivables (£k) | 284 | (2,196) | (1,876) | 563 | (2,139) |

| Trade and other payables (£k) | 686 | 139 | 1,970 | (696) | 529 |

| Total (£k) | (1,557) | (3,081) | (2,157) | (1,155) | (4,292) |

- Extended credit terms in the Middle East explain the increase to receivables last year (point 11).

- The working-capital movements do not seem that untoward given the group’s profit advances of late.

- Free cash flow of £13m for 2018 funded dividends of £10m, reduced debt by £0.5m and left £2.5m to add to the bank balance.

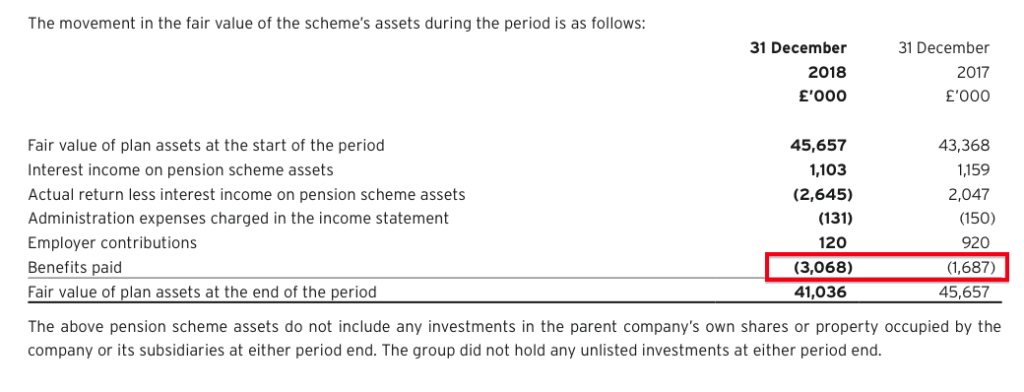

- ASY’s defined-benefit pension scheme continues to enjoy an accounting surplus. A deficit was last reported in 2007.

- However, benefits paid to the scheme’s members have jumped to £3m:

- ASY did not indicate whether this increase was a one-off or permanent change.

- Scheme assets of £41m and employer contributions of £120k do not look sufficient to sustain paying benefits of £3m a year without eroding the capital. Greater contributions could therefore be required, which would hit cash flow. (How To Evaluate Pension Deficits explains my reasoning.)

Valuation

- ASY remains a tightly held share with a small free float and wide bid-offer spread.

- The 99-year-old chairman and his family own 90%, leaving 10% for everybody else.

- The 2018 annual report states: “The Board believes that the presence and requirements of a long-standing controlling shareholder helps focus the company’s strategy on long-term shareholder value creation.” (point 3)

- A 720p offer price values ASY at £304m and the free float at £31m.

- Subtract the £23m net cash position from the market cap and the underlying business could arguably be valued at approximately £280m or 665p per share.

- ASY has operated with net cash since 2010, and perhaps the presence of such cash is required to keep the business on a more stable footing.

- Dividends before 2010 had been rather haphazard, due in part to significant levels of debt combining with the banking crash.

- Taking the 2018 operating profit of £20.7m, adding back a one-off £0.4m pension charge and applying tax at 19% gives earnings of 40.6p per share.

- The underlying P/E could therefore be 665p/40.6p = 16.4.

- ASY’s outlook comments hinted that 2019 may not be as buoyant as 2018. The company stated:

“The group’s policy to increase investments in new technologically advanced and environmentally friendly non-seasonal products will be continued into 2019. Investments will also continue in our traditional businesses to ensure we are ready to support our customers in times of extreme weather conditions.

The group continues to face both challenges and opportunities in all of its geographical markets but our business remains strong, cash generative and well developed, with positive net funds. The Board remains mindful of the favourable or adverse impact that the weather can have on our business.

- Within the six previous annual results, ASY said (my bold):

“The Board is therefore cautiously optimistic for further success in [the next year], always being mindful of the favourable or adverse impact that the weather can have on our business.”

- Somebody deliberately removed the “cautiously optimistic for further success” part from this latest RNS. The rest of the 2018 outlook text has been repeated for many years.

- This financial year is already almost five months old and experienced winter conditions milder than last year. If 2019 earnings are indeed running behind those of 2018, ASY must already know.

- The static 23.9p per share dividend supplies a 3.3% income at 720p.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Andrews Sykes.

Andrews Sykes (ASY)

Publication of 2018 annual report

Here are the points of interest:

1) Additional management narrative

The annual report contained additional management remarks about the performance of the business. The most enlightening comments concerned the European operations. As noted in the blog post above, all six European divisions reported positive progress:

2) Strategy and risks

New for 2018 were the following useful paragraphs:

They explain the group’s competitive advantage — essentially owning a fleet of modern equipment to hire and tip-top customer service.

Brexit and other risks have not changed:

3) Corporate governance

New for 2018 also was ASY’s corporate governance statement:

The most interesting parts are below:

I liked this bit: “The presence and requirements of a longstanding majority shareholder has resulted in a strategy with the key aim of creating long-term shareholder value”

Strong supplier relationships and a flat management structure also help win/keep business.

This next bit confirms the 99-year-old chairman is chairman by title only and one of his sons leads the board:

The FD is an unofficial board member.

4) Key audit matters

Always worth checking to see what audit risks have changed

From 2017:

From 2018:

“Management override of controls” has become a “significant” risk, while “existence and valuation of stocks” is not longer seen as a risk worthy of the chart.

I dare say “management override of controls” is always a significant risk at any business. ASY’s decent accounts suggest the controls in place are good.

5) New accounting standard

The upcoming implementation of IFRS 16 (Leases) provides no worries:

6) Business and geographic segments

ASY split its Hire, Sales, Installation and Maintenance revenue for 2018:

Previously Hire and Sales were lumped together, as were Installation and Maintenance.

Hire revenue in UK/Europe jumped 16% to £58.8m — versus total revenue gaining 10%. Installation sales fell 20%, while other revenue segments were +/- 5%. So the UK/European Hire performance was a little obscured by the other departments.

European revenue has now become 23% of total revenue:

7) Employees

ASY commendably uses sales per employee as a KPI:

£137k sales per employee is a new record for ASY, beating the £135k set in 2008. Since then the figure has bobbed between £110k and £130k.

In a bumper year for the business, employee costs were kept under good control. Average staff cost was £36k, versus £35k for 2016 and 2017. Staff costs as a proportion of revenue was 26.6%, the lowest since 2013.

8) Director pay

I can live with the managing director’s hefty pay given the group’s performance:

The chairman must be the oldest director of a quoted company:

The chairman collects no board fees.

9) Plant and equipment

This note underlines the high returns ASY enjoys from its hire business:

“Equipment for hire” is in the books at £17m. And yet earnings for the year were £17m, too.

10) Stock

A confusing note this:

Finished goods stated as £4.8m — which I presume relates to equipment for sale rather than hire.

“Cost of stock recognised as an expense” was £10m — so double the year-end stock value, and suggests very slow-moving equipment for sale.

Also odd is that non-Hire revenue for the year was £11m, so subtracting the £10m “cost of stock recognised as an expense” suggests equipment sales, installation and maintenance combined are not very profitable (if at all).

11) Trade receivables

No real issues here:

Net trade debtors of £17.5m represent 22% of revenue, within the 21%-26% range seen during the previous ten years.

The £8.7m overdue trade debtors represent 50% of total trade debtors:

The percentage has been between 48% and 50% for the previous five years. Trading in the Middle East often leads to payment delays:

12) Pension fund

The pension fund shows a £1.3m accounting surplus:

Contributions are set to stay at £120k a year:

ASY was previously injecting £1m a year.

Unusually, ASY charged a greater pension contribution to the income statement than the actual cash contribution. Most companies charge less to the P&L and contribute a greater cash sum. The £443k difference is noted below, and does make me wonder whether cash contributions will increase at some point:

As noted in the blog post above, pension benefits have risen to £3m:

Confirmation of a one-off £432k pension charge (not deemed to be ‘exceptional’ by ASY):

Maynard

Thanks for posting. With the weaker pound, the UK is becoming more attractive for me. A 99 yo chairman is heartening to see. Seeing the relatively low proportion of ‘sales’ compared with ‘hire’ is a good sign. A bit cheaper now :) too as I tend to ‘bookmark’ your tweets to read later. Ashamed to say that in this case it’s taken me almost 4 weeks to get around to it. Is there any reason why the company would not go completely private, given the large family ownership ? Or perhaps a question is, do you think they might want to buy out the remaining shareholders at some stage ?

Hi Christian,

No problem with the delayed reading. I am just the same with other blogs. Some thoughts on ASY’s ownership and potential for delisting here:

https://maynardpaton.com/2018/10/01/andrews-sykes-i-had-expected-h1-sales-to-grow-by-more-than-7-following-the-heavy-snow-and-extended-heatwave/#comment-12515

Maynard

Thanks for that, appreciate the reply. What you wrote makes sense. I guess a public market is a good way of selling down if they need to.

Hi again, pretty sure you are right about this half not being as good as last year but hopefully the steady organic growth will help alleviate the ups and downs due to the weather. However, getting back to the weather and unlike the UK, Europe has been pretty warm over the last month culminating in the well publicised and unprecedented heatwave. If, as you say, Europe is accounting for 25% of trade and growing, that is no bad thing. The opening of the Marseilles depot in May was a masterstroke as it is pretty well at the epicentre of the heatwave. Their latest blog confirms what I would have thought looking at the weather. They say ‘engineers working around the clock to help beat the heat’ and in the past few days we have delivered and installed hundreds of units, which is set to continue’.

Looking ahead and Europe, particularly northern Italy and the southern half of France look set to stay hot for weeks with the heat moving north at times. Once they get their units out they are probably going to stay out for the rest of the summer so things are looking good for European operations at least. There are signs that the warm weather will affect the UK at times too so the second half is starting to look good. Hope you don’t mind me waffling on about the weather, but ASY and the weather has been one of my projects for the last 20 years!

Hi Keith,

No problem with any weather waffle! Yes, Europe certainly should be busy right now and the French depots should be off to a flying start. When I went to the AGM a few years ago, management said what was important was the duration of any heatwave (clients hire for longer) rather than the absolute temperature. So hopefully the scorching Euro summer is here for a few weeks. That said, I am sure 40-plus-degree heat will prompt demand from customers that have never bothered with a/c before. When I looked at the annual report, the group’s European operations had all become profitable and certainly this part of the group ought to become greater than 25% over time. The overseas operations have been on a ‘slow burn’, but I get the impression the start-up costs have now been expensed and the growing economies of scale ought now to feed through and contribute more significantly to the group.

Maynard

Hi Maynard,

Ouch!

Thoughts on the crash in sp today?

Cheers,

NJC