***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

21 November 2021

By Maynard Paton

Investors love ‘disruptors’. Find a pioneering upstart that is stealing market share from industry dinosaurs, and your portfolio may enjoy a huge stock-market winner. Amazon of course is the textbook example.

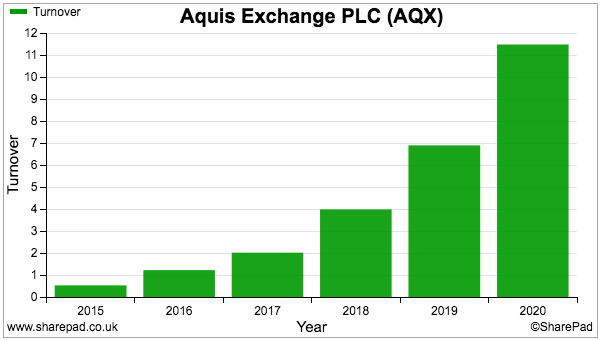

One company that could be a genuine disruptor is Aquis Exchange, a £180 million small-cap trying to revolutionise share trading and taking on the likes of the London Stock Exchange and Euronext.

Let’s take a closer look.

Read my full Aquis Exchange article for SharePad.

Maynard Paton