22 September 2021

By Maynard Paton

Results summary for Mincon (MCON):

- A very mixed H1 performance, as record €67m six-month revenue contrasted with profit down as much as 13% due to general pandemic disruption.

- European construction revenue encouragingly climbed 50% supported by numerous smaller projects and innovative sector products.

- Customer testing of the “disruptive” Greenhammer system remains on hold, although other developments are now “poised to deliver“.

- The move to selling a wider range of equipment direct to customers continues to limit margins/returns on equity/cash flow and raise doubts about an indisputable competitive ‘moat’.

- While a P/E of 20 is not a clear bargain, the long-time family management expects a stronger H2 and claims to have established a “platform for future growth“. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own MCON

- Results summary

- Revenue, profit and dividend

- Revenue split: Geography and sector

- Greenhammer and other development projects

- Financials: Margins and returns on equity

- Financials: Stock

- Financials: Cash flow

- Valuation

Event links, share data and disclosure

Event: Interim results and presentation for the six months to 30 June 2021 published 09 August 2021

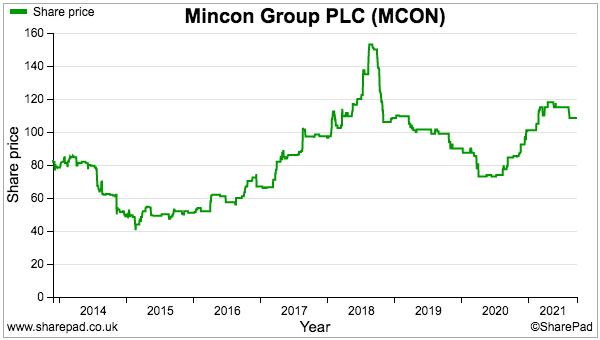

Price: 110p

Shares in issue: 212,472,413

Market capitalisation: £234m

Disclosure: Maynard owns shares in Mincon. This blog post contains SharePad affiliate links.

Why I own MCON

- Designs and manufactures industrial drills and bits, with sales supported by established reputation, engineering excellence, product patents and technical innovation.

- Boasts veteran family management with 44-year tenure, 56%/£132m shareholding and long-term business perspective.

- Offers higher earnings potential through pandemic recovery, greater direct sales, construction market entry and “disruptive” new products.

Further reading: My MCON Buy report | All my MCON posts | MCON website

Results summary

Revenue, profit and dividend

- These H1 2021 figures were not quite at the level I was expecting.

- An update during May had said revenue between January and April was “ahead” of last year and that the start of 2021 was “challenging for production in our key hammer facility in Shannon, as we endeavoured to ensure we remained Covid-free.“

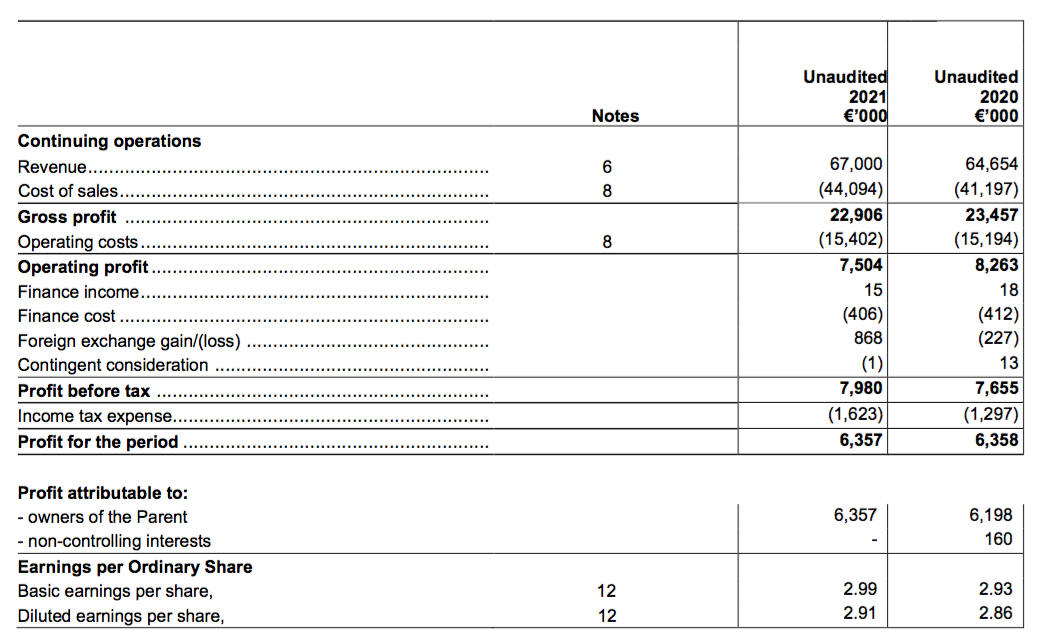

- This H1 statement revealed revenue up 4% but operating profit down 9%.

- MCON blamed the profit shortfall on pandemic disruption:

“At the beginning of the year, including all of January and most of February, we experienced interruption in our manufacturing in some of our plants due to the pandemic. The largest impact was at our hammer factory in Shannon. Our capacity in the Shannon plant was severely disrupted, with a 35% reduced manufacturing workforce during those initial months of this year.”

- May’s update did not suggest the main Shannon factory had reduced its workforce (and perhaps its output) by 35%.

- But these results did imply the Shannon factory was now operating at record productivity:

“However, during March the Covid situation improved in Shannon, and by Q2 2021 the plant was manufacturing at a much higher monthly run-rate than had been achieved in the past and this should help to improve gross margin in the second half of the year.“

- Higher material costs, surging shipping rates and the use of “expensive” air freight were also cited for the lower profit.

- H1 revenue of €67m set a new six-month record and MCON did not say the performance was bolstered by currency movements or acquisitions.

- Sales of MCON’s own-brand equipment gained 3% and continue to represent 86% of total revenue.

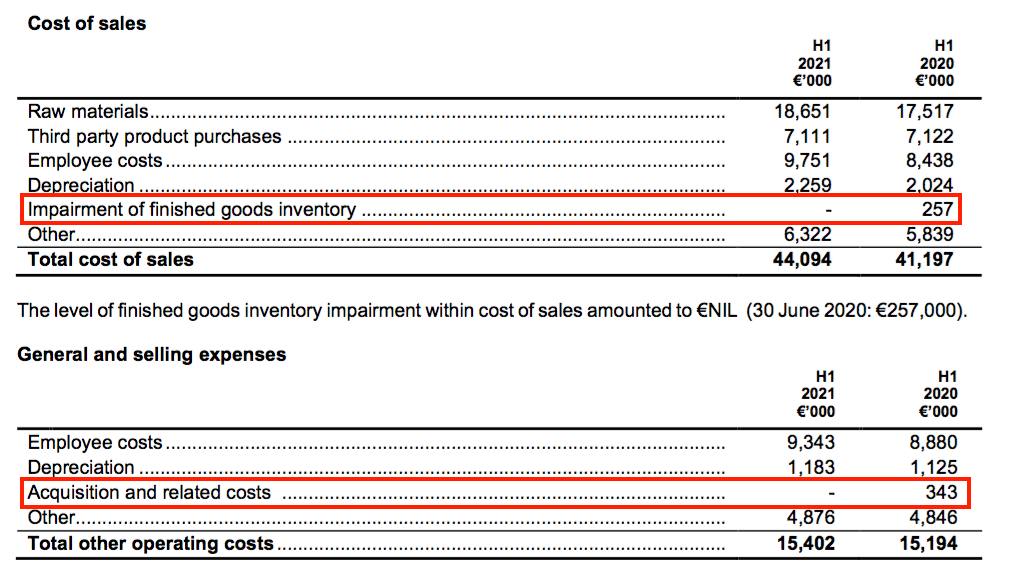

- The comparable H1 2020 operating profit was taken after impairments and acquisition costs of €0.6m:

- Adjust for that €0.6m and arguably the comparable H1 2020 profit was €8.9m and this H1’s profit shortfall was not 9% but in fact 13%.

- MCON’s reported profit could be fine-tuned further for capitalised R&D spend without an associated amortisation charge (see Greenhammer and other development projects below).

- The ongoing concerns following these H1 results are:

- A further deterioration to margins and the continuing absence of indisputable ‘moat’-like profitability, and;

- A further sizeable increase to working capital and resultant lack of free cash generation.

- True, the pandemic influenced this H1 and talk of “strong” order books ought to support a better H2.

- But MCON’s past commentary (point 1) of “products that are best-in-class” and “continuous excellence in technical innovation” has never really been apparent within the financials during the last five years (see Financials: Margins and returns on equity below).

- At least the H1 dividend was set at 1.05 eurocents a share, which matched the payments for H1s 2018, 2019 and 2020.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

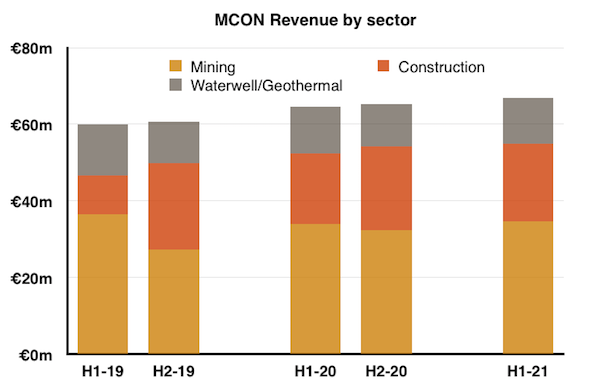

Revenue split: Geography and sector

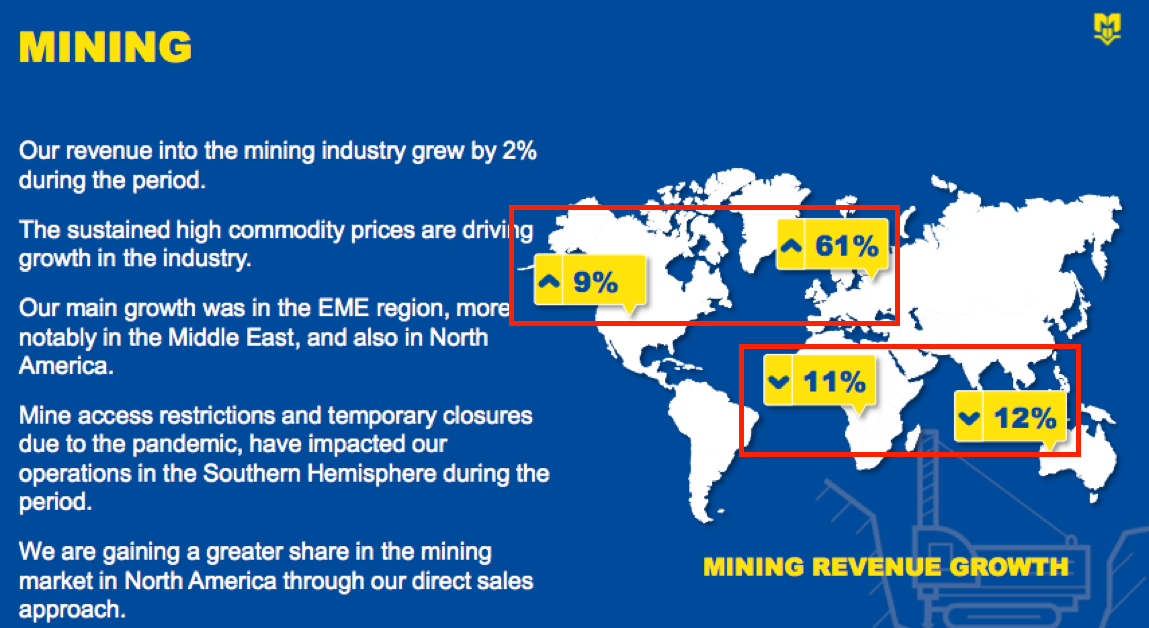

- MCON experienced a revenue ‘north-south divide’ during this H1.

- Greater revenue was earned from mining customers located within Europe, the Middle East and North America as Covid restrictions eased and MCON gained greater access to client sites:

- Lower revenue was meanwhile earned from mining customers operating in Southern Africa, South America and Australasia as pandemic restrictions remained in place.

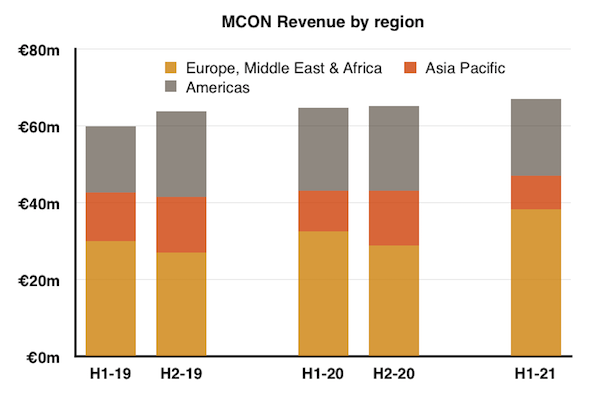

- Revenue from all customers within Europe, the Middle East and Africa in fact gained almost 18% to represent 57% of group revenue — the highest proportion for ‘EMEA’ since flotation save for H2 2018 (61%):

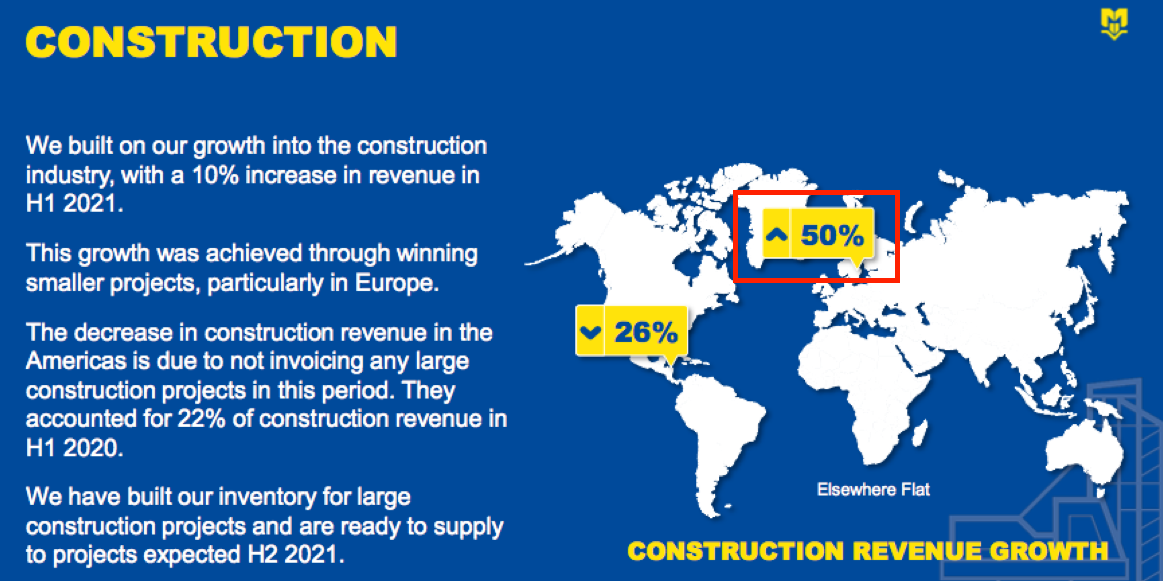

- Construction was MCON’s best performing sector, with H1 revenue up 10%:

- MCON’s construction division was effectively formed during FY 2017 following the purchase of Finnish operator PPV.

- Since then acquisitions and innovative products have helped construction revenue grow to represent 30% of group sales.

- Construction products include the Spiral Flush…

- …the Rock Drill R142…

- …and the M Wall:

- Europe in particular witnessed greater construction activity, with revenue up 50%:

- MCON reassuringly said its H1 construction revenue was supported by smaller projects and did not include any large contracts.

- Last year’s construction progress was dominated by large North American projects, and I had wondered whether the timing and frequency of such work would mean construction income would be unpredictable.

- MCON also noted its large construction projects earn the group a “much higher operating margin” than its other activities.

- MCON does not disclose the profitability of its three product divisions (mining, construction and waterwell/geothermal). But maybe one day construction-related profit could surpass profit earned from MCON’s traditional mining customers.

- Two years ago MCON embarked on selling equipment direct to its end customers rather than through intermediaries:

“We are differentiating ourselves from the less developed businesses in low margin activities in the sector, and we are positioning ourselves to deal directly with end customers and to win large contracts.”

“Going forward we plan to… seek long-term partnerships and multi-year contracts with end customers incorporating direct delivery to their sites.”

- The FY 2020 statement was the first to reveal the extent of direct sales at 77%:

“Our involvement in full-service mining and large geotechnical contracts has led to an increase in direct end user revenue, the direct approach now accounts for 77% of total turnover.“

- Direct sales should benefit MCON by cutting out the intermediary margin and providing greater insight into future customer requirements.

- No mention was made of revenue earned from direct customer sales within this H1. I trust the trend towards direct sales remains positive.

Quality UK investment discussion at Quidisq. Visit forum.

Greenhammer and other development projects

- MCON admitted its Greenhammer project had made no further progress due to Covid-19 restrictions:

“Our Greenhammer system is still waiting to get onsite in Australia“.

- The FY 2018 statement described this new hydraulic drilling system as:

“[A] disruptive technology, offering tremendous savings in fuel, with an ambitious planned partnership programme in our customer base”.

- MCON added:

“This is not a small system or easily replicable, and we have placed patents around the system to protect it. The system is more than just the hydraulic hammer; it includes all the drill string and the supporting on-rig infrastructure and handling.”

- The project appears to have commenced ten years ago. It was first mentioned within the FY 2016 results while the FY 2018 results said development had started seven years beforehand.

- MCON nonetheless remains optimistic. My question to management about Greenhammer’s prospects at the (online) AGM elicited the following (paraphrased) response:

“Greenhammer is being tested and currently showing 2-3x improvements on penetration times. Such performance should lead to a decrease of rig requirements for customers, perhaps needing only half the expenditure on labour and fuel as now based on the cost-per-metre of drilling. Greenhammer is being trialled in Western Australia, where there is a large opportunity. Further development is required before the system can be rolled out elsewhere.

Greenhammer could produce significant incremental profitability and there remains a very big market opportunity for other MCON products.”

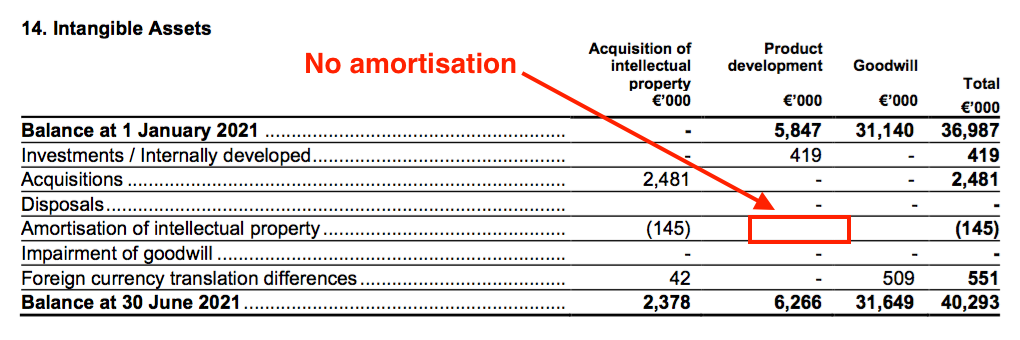

- MCON capitalised Greenhammer development costs of €0.4m during this H1 to take the project total to €6.3m since FY 2016:

- Not a eurocent of that €6.3m expenditure has been charged against earnings. Amortisation will commence only when the system enters commercial use.

- The €6.3m expense represents 8% of the €78m aggregate operating profit before exceptional items reported during the same 5.5 years.

- If the entire Greenhammer project is written off, arguably past profits since FY 2016 were overstated by 8%.

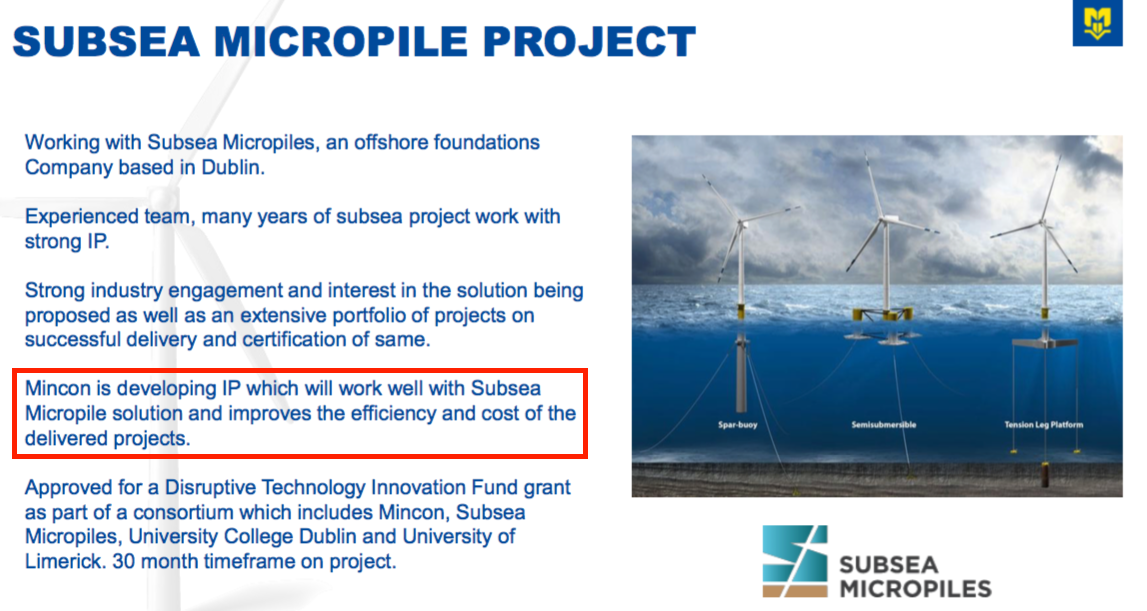

- Beyond Greenhammer, MCON claimed its “ambitious and challenging product development projects” were now “poised to deliver“. The presentation indicated customer testing of “large hammers” was about to start:

- The presentation also showed MCON’s involvement in robotic seabed drilling:

- This video has more:

Quality UK investment discussion at Quidisq. Visit forum.

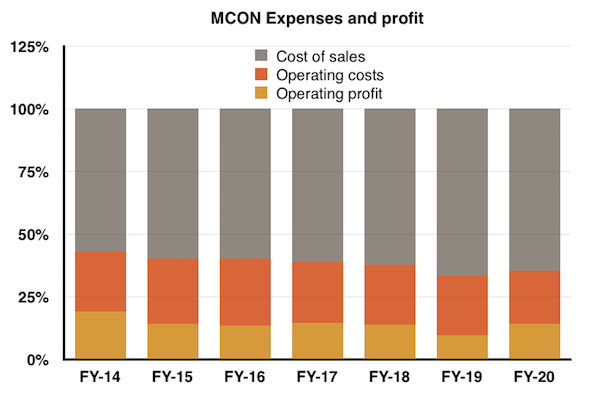

Financials: Margins and returns on equity

- I bought MCON shares during 2015 partly because of the company’s then attractive margins:

“[H]igh margins underpin the notion that MCON has a respectable competitive advantage. The group converted 19% of revenues into profit during 2014 and above 20% during 2011, 2012 and 2013.”

- I wrote when reviewing the FY 2020 statement:

“A 14% margin is reasonable, but not overwhelming evidence of a competitive ‘moat’ and customers having few viable alternatives.”

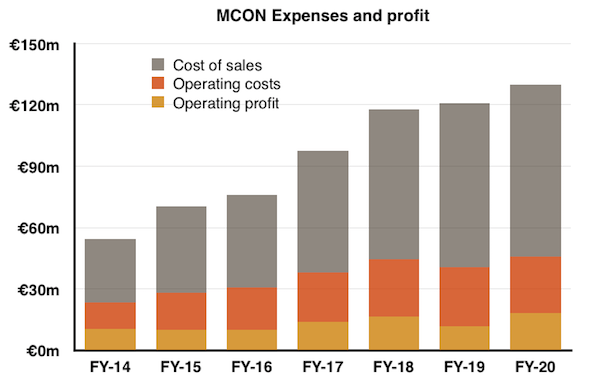

- The operating margin for this H1 was 11%.

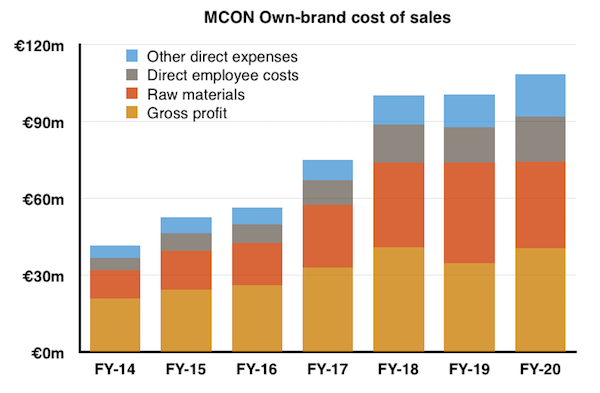

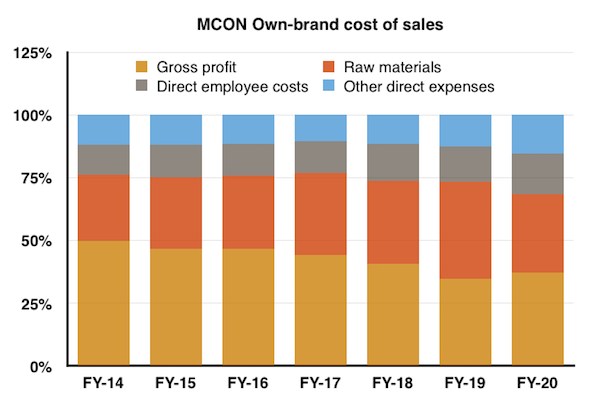

- The long-term margin decrease has been due to greater cost of sales:

- Raw materials and direct employee costs have represented a growing part of own-brand revenue since FY 2014 (from a combined 38% to 47%):

- My question to management about MCON’s margin at the (online) AGM elicited the following (paraphrased) response:

“The 20% margin of the past was achieved on much lower revenue when the company was manufacturing only part of the drill string and the more profitable DTH [down-the-hole] drills represented a greater part of the business.

Today the company manufacturers the full drill string, and as such has been able to win large direct contracts and therefore increase profit. That said, 14% is not our level of ambition.”

- In other words, MCON has evolved from a niche, high-margin drill supplier with perhaps modest growth prospects to a wider, middle-margin drill supplier with possibly better growth prospects.

- The reduced margin feels contrary to some of the ‘margin improvement’ hints following recent acquisitions.

- These H1 results said:

“Prior to acquisition of Hammer Drilling Rigs, all the rig manufacturing was outsourced. That has now been integrated with our plant in Benton, Illinois bringing the manufacturing margin inhouse.“

- The comparable H1 2020 results said:

“In January we completed the substantial acquisition of Lehti Group to bring the manufacturing margin for our Geotech products inhouse.“

- Mind you, these H1 results also claimed:

“We are also passing on price increases where we can and that will have a positive result on our margins in H2 2021″.

- The margin-growth trade-off cited at the AGM has indeed resulted in higher absolute profit, although ‘growth’ is only one part of the investment equation.

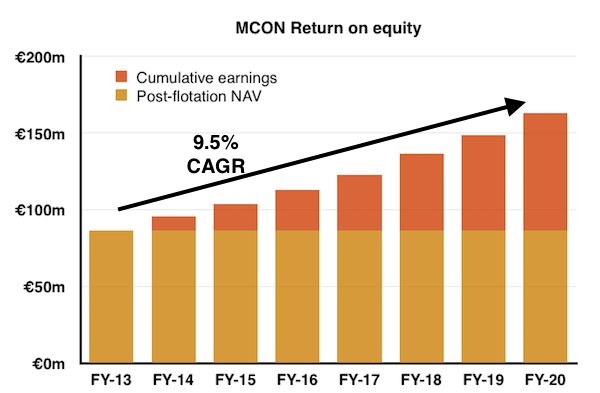

- How much shareholder money has been used to generate the extra profit?

- Since the 2013 flotation when shareholder equity was €86m, subsequent reported earnings have totalled €77m:

- Effectively investing €86m to earn an aggregate €77m over seven years equates to a 9.5% annual average compound return.

- Earning 9.5% a year on shareholders’ equity is not awful but is not exceptional either.

- For perspective, the same seven-year calculation for fellow portfolio member — and another commercial-equipment manufacturer — FW Thorpe is 12.7%.

- Maybe lifting margins and returns on equity to ‘moat’-type levels requires new products such as Greenhammer, which could/should attract customers willing to pay a premium for more cost-effective drilling.

- Revenue per employee during this H1 was €236k and gave no hints of any operational improvement either. During the seven years since flotation, revenue per employee has averaged €262k and has reached €300k only once (FY 2017).

Financials: Stock

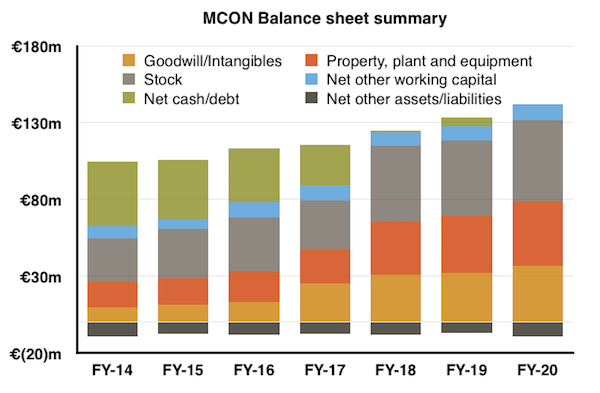

- Significant levels of stock remain an unfortunate balance-sheet feature.

- Stock levels have grown from 29% (€28m) to 40% (€53m) of net asset value between FYs 2014 and 2020:

- The proportion increased to 43% (€58m) for this H1 after MCON responded to shipping delays:

“We continue to see longer shipping times from our factories to our customer centres or customers due to vessel capacity and congestion at seaports and, in some cases, shipping times have doubled over the past twelve months. This has had a direct impact on our inventory, as we have witnessed a significant increase of inventory in transit from our factories to our customer centres and unreliable dates of seaport arrivals.

During the period, we decided to invest cash into holding larger stocks of finished goods at our customer centres to ensure supply to local customers.”

- Other companies in my portfolio typically operate with stock levels representing less than 20% of their balance sheets (vs the 40%-plus for MCON).

- Large amounts of stock could mean a company:

- Owns slow-moving items that carry greater risk of obsolescence;

- Applies inefficient working practices, and/or;

- Requires greater cash investment into extra stock to support future growth.

- On the subject of requiring greater cash investment into extra stock to support future growth, my question to management at the (online) AGM elicited the following (paraphrased) response:

“We consider inventory levels to be high, but that does reflect the wide geographical footprint the company serves. We measure stock levels by days in hand and if sales did double, then inventory would increase, but we’d expect it to reduce as measured by days in hand.“

- I am resigned to MCON operating permanently with high stock levels that are unlikely to lead to exceptional returns on equity.

Financials: Cash flow

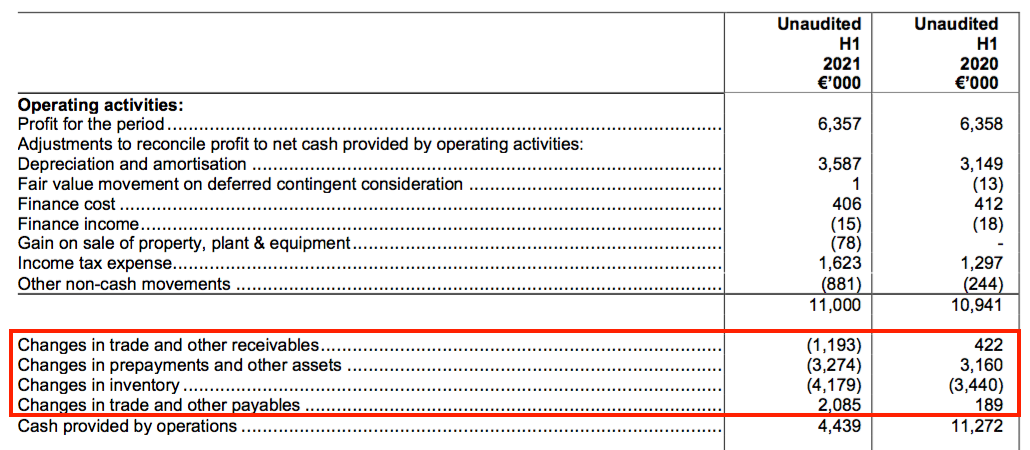

- The extra stock investment during this H1 meant cash conversion was poor.

- Net cash invested into working capital came to €6.6m, including €4.2m for extra stock and €3.3m funding prepayments for manufacturing equipment:

- Reported earnings of €6.3m eventually converted into negative free cash flow of €1.0m.

- A further €2.2m spent on acquisitions/earn-outs and €4.5m spent on dividends led to a total H1 cash outflow of €7.6m.

- This H1’s cash conversion was disappointing when last year MCON reported its best free cash flow (of €11m) since at least 2011.

- But this H1’s cash absorption was typical of MCON’s general appetite for investment, whereby significant capital expenditure, extra working capital and various acquisitions have reduced net cash of €49m at the 2013 flotation to net debt currently at €8m.

- Total gross bank loans/finance leases stand at €20m and do not appear too alarming versus earnings of approximately €12m and my FY 2020 calculation of a 3.8% interest rate.

- Note that MCON is also on the hook for contingent acquisition earn-outs of €5.7m.

- MCON’s cash flow may improve during the second half following the aforementioned:

- Management talk of “strong” order books;

- The “passing on [of] price increases“, and;

- Improved productivity at the Shannon plant.

- At least MCON’s books are not complicated by pension obligations.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- MCON’s shares do not appear obviously cheap given the very mixed H1 progress and unspectacular financial ratios.

- The reported €17.5m trailing twelve-month operating profit less:

- €0.8m for debt/lease costs, and;

- The 16% average tax applied between FYs 2016 and 2020s…

- …gives earnings of £12.0m or 5.6p per share with GBP:EUR at 1.17.

- Dividing the 110p share price by my 5.6p per share earnings guess gives a possible P/E of 20x.

- Further small adjustments could be made for the earn-outs and Greenhammer expense.

- The optimistic rating may be supported by hopes of:

- A general revenue/profit/margin recovery following the pandemic;

- Further construction-market opportunities;

- Greater direct sales of larger mining contracts;

- Greenhammer and other development projects bearing fruit, and/or;

- Management’s commitment to product quality ensuring one day a ‘moat’ is (re)built.

- MCON for now remains in a protracted ‘moat-(re)building’ phase — the eventual duration and future cost of which is still unknown.

- The share price should be somewhat higher than it is now if/when a moat is (re)built and becomes very obvious.

- The chief executive is in his mid-50s and presumably will see his “platform for future growth” deliver that future growth before retiring.

- The chief exec’s father started MCON during 1977 and remains a non-executive in his 80s, so therefore long-term thinking at this business is not new.

- Such long-term thinking is underpinned by an absence of management share dealing.

- The chief exec, his father and other family members own a collective 56%/£132m shareholding. No family member sold a share at the 2013 flotation, and none has sold a share thereafter.

- Patient investors can only trust management’s plan and the group’s expenditure will one day lead to enhanced equity returns.

- A trailing 2.1 eurocents, or 1.8p, per share dividend meanwhile supports a modest 1.6% income (before Irish withholding taxes for UK-resident investors).

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Mincon (MCON)

Q3 Trading Update 01 November 2021

A mixed update. Here is the full text interspersed with my comments:

——————————————————————————————————————

Trading

We have sustained the sales growth experienced in the first half of the year during the past quarter, with revenue for the nine months to September 2021 up 6% on the first nine months of 2020. Our order levels increased strongly during Q3 2021, and our production levels were increased to enable us to fulfil orders for the final quarter of the year.

——————————————————————————————————————

Sounds promising. H1 sales gained 4%, so 6% for Q123 suggests an acceleration during Q3. Production increasing for Q4 seems encouraging.

——————————————————————————————————————

As noted at the time of the Group’s interim results, across the Group we continue to experience delays in the delivery of raw materials to our factories and the delivery of manufactured products from our factories to our customer centres as a result of increased sea freight transit times.

As such we have decided to maintain our raw material inventories at higher levels in our factories, and we have increased inventories in our customer centres to ensure customer supply. In line with other industries, we have continued to experience higher freight and raw material costs. Arising from these issues we have experienced some pressure on margins and we are passing on increased costs when we can in an equitable and sustainable manner.

——————————————————————————————————————

Not ideal news, but perhaps not surprising given the current circumstances. Further increases to inventory levels just underline my belief that MCON must fundamentally operate with a lot of warehouse stock. Margins and RoE look likely to remain modest for the time being.

——————————————————————————————————————

Investments

During the past quarter we invested in our sales footprint to reach new customers and to gain future market share. We have hired new salespeople, opened new warehouse points in key locations and acquired AttakRoc, a distributor in Quebec City in July of this year.

We have also invested in our factories during the past quarter to improve efficiency and add capacity with new and more environmentally friendly production methods. We expect that the commissioning of the new equipment from this investment will take place in Q4 2021 and Q1 2022.

——————————————————————————————————————

Reaching new customers always sounds good, although determining how effective MCON’s past investments have fared has never been straightforward.

Maynard