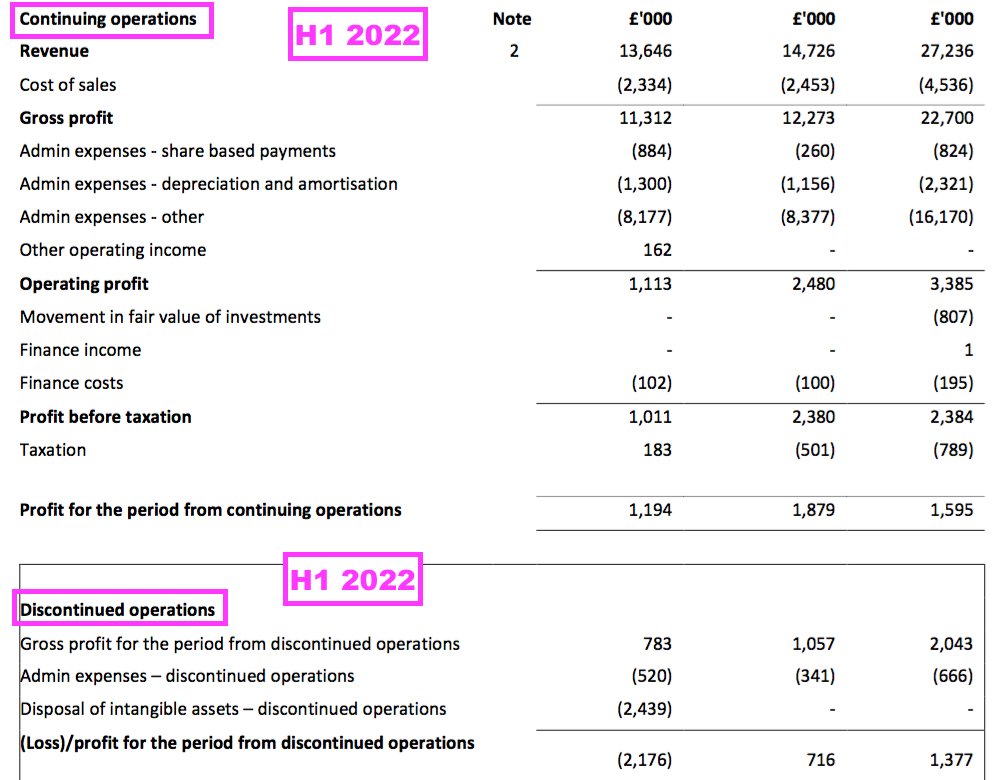

12 January 2023

By Maynard Paton

Results summary for Tristel (TSTL):

- Another pandemic-disrupted performance, although 10-15% per annum sales-growth guidance suggests hospital customers will soon resume normal purchasing activity.

- Progress was complicated by an accounting U-turn, with Brexit stock-piling, share options, US costs and write-offs creating a wide range of profit outcomes.

- Management webinar comments suggested a positive US regulatory verdict is dependent on a “negotiation” with the FDA concerning data tests using different product batches.

- A useful 17% operating margin, net cash of £10m, worthwhile cash conversion and low capital requirements imply the group’s disinfectants still enjoy favourable economics.

- An estimated 24x P/E for FY 2025 is not an obvious bargain, but a premium rating may be justified by a US product approval and hefty royalties appearing soon thereafter. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TSTL

- Results summary

- Revenue, profit and dividend

- Discontinued operations and accounting U-turn

- Presentation disclosure

- Product categories

- UK versus overseas

- United States: FDA submission

- United States: FDA Predicate and De Novo guidance

- United States: costs and potential

- Patents and chemistry

- Share options

- Financials

- Valuation

News links, share data and disclosure

News: Annual report, presentation and webinar for the twelve months to 30 June 2022 published/hosted 25 October 2022 and AGM statement published 12 December 2022

Share price: 350p

Share count: 47,233,493

Market capitalisation: £165m

Disclosure: Maynard owns shares in Tristel. This blog post contains SharePad affiliate links.

Why I own TSTL

- Develops medical-device disinfectants that face limited direct competition due to proprietary chemistry, instrument-manufacturer approvals, scientific testimonies and regulatory hurdles.

- Enjoys a sizeable and resilient UK market position alongside worthwhile expansion opportunities abroad — most notably within the United States.

- Boasts financials that, pandemic-disruption aside, showcase high margins, low capital requirements, decent cash conversion and no debt.

Further reading: My TSTL Buy report | All my TSTL posts | TSTL website

Results summary

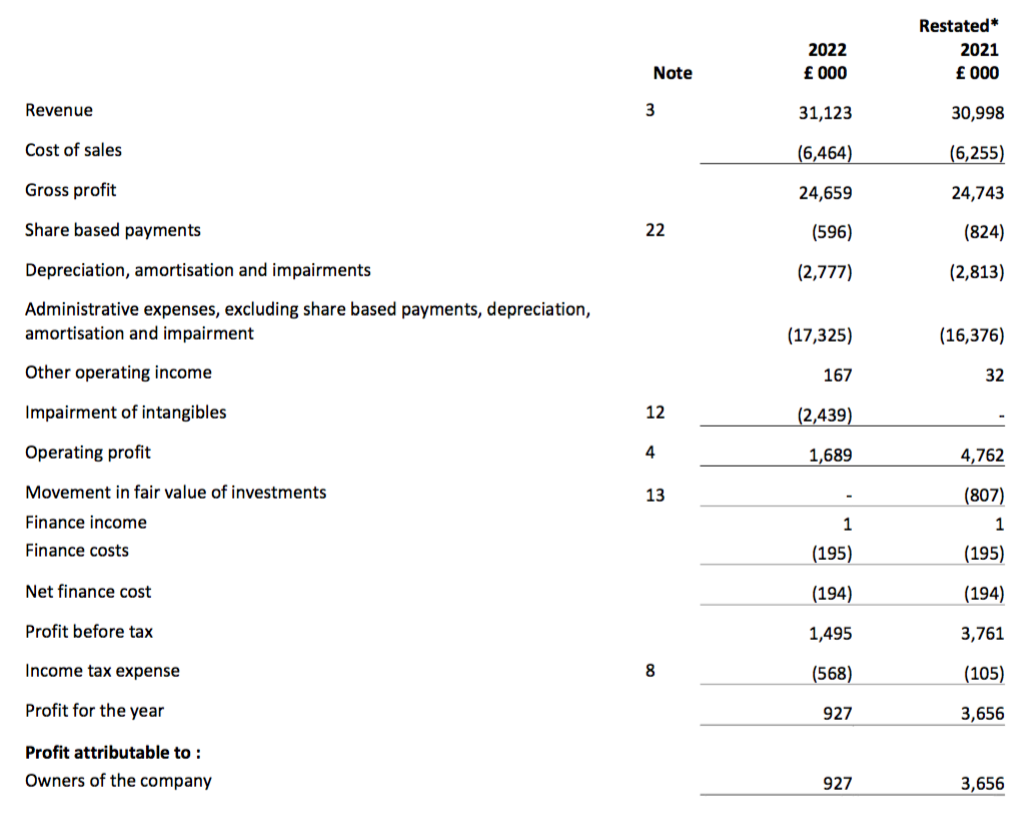

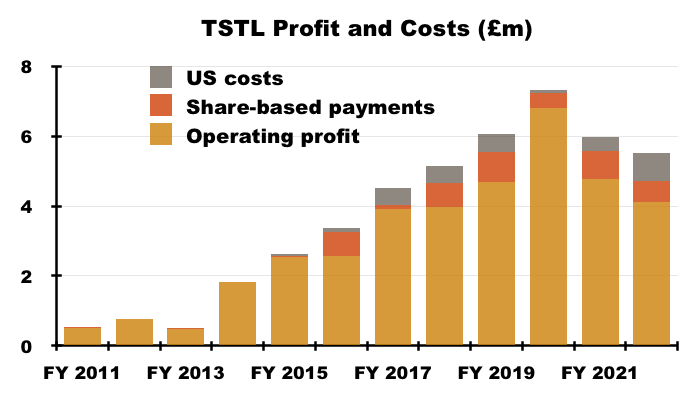

Revenue, profit and dividend

- July’s trading update had already signalled the headline performance for FY 2022:

“Revenue and adjusted profit before tax* for the year from the continuing operations will be in line with consensus forecasts of £28.4m and £4.5m respectively.

*adjusted for share-based payments“

- Revenue from ‘continuing’ operations was £1.2m higher than predicted at £29.6m, while adjusted ‘continuing’ profit before tax seemed to match the predicted £4.5m.

- Correlating July’s update to these FY figures was unfortunately complicated by TSTL reversing the accounting re-jig applied during the preceding H1.

- The preceding H1 witnessed TSTL announce a culling of ‘non-core’ products that led to revenue and profit being classified as either ‘continuing’ or ‘discontinued’.

- But management admitted during the FY webinar that the auditor had disagreed with the H1 ‘continuing’ and ‘discontinued’ interpretation, and had instructed TSTL to revert back to its previous accounting policy.

- The auditor’s instruction meant these FY 2022 results were compiled on the same basis as the FY 2021 results, but on a different basis to the preceding H1 statement (see Discontinued operations and accounting U-turn).

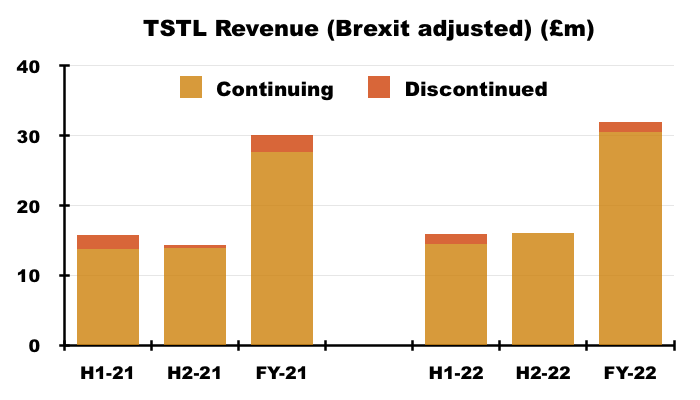

- Interpreting this FY 2022 statement was complicated further by Brexit stock-piling, which generated extra revenue of £0.9m during the prior-year H1 2021 that would have otherwise been earned during H1 2022.

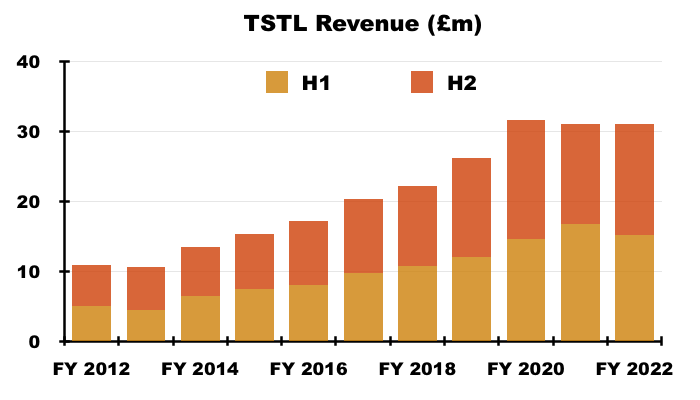

- Total FY revenue including all discontinued products and not adjusted for Brexit stock-piling inched 0.4% higher to £31.1m:

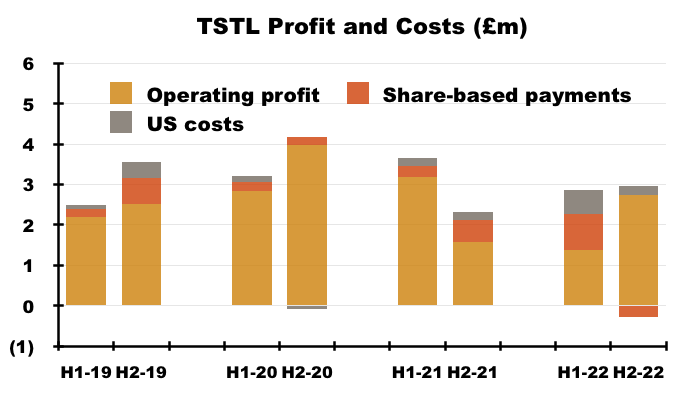

- But FY revenue excluding ‘discontinued’ products and adjusted for the Brexit stock-piling gained 10% to £30.5m, with H2 revenue on the same basis climbing 15% to £16.0m:

- H2 revenue of £16m exceeded the £14-15m six-month revenue reported before the pandemic ‘panic buying’ of H2 2020 and the Brexit stock-piling of H1 2021:

- TSTL’s FY profit progress was also difficult to analyse.

- As well as the Brexit stock-piling and an exceptional £2.4m H1 discontinued-product write-off, reported profit was complicated by TSTL’s usual:

- Share-based payments (see Share options), and;

- Costs associated with the US regulatory programme (see United States: costs and potential).

- Other operating income of £167k (relating to chemical-data fees and formulation transfers) also influenced reported profit.

- Including every operating charge, FY operating profit fell 65% from £4.8m to £1.7m.

- Excluding share-based payments, US costs and the discontinued-product write-off, FY operating profit declined 8% from £6.0m to £5.5m:

- Adjust for the Brexit stock-piling as well, and the FY operating profit perhaps climbed 17% from £5.3m to £6.2m.

- Excluding share-based payments and US costs, H2 operating profit climbed 14% from £2.3m to £2.7m:

- Although all the adjustments and guesswork with these FY 2022 figures suggest an ‘underlying’ profit improvement versus FY 2021, ‘underlying’ profit looks to have only matched that of (pre-pandemic) FY 2019 and fallen £1m short of (pandemic-boosted) FY 2020.

- The subdued profit progress reflects the impact of the pandemic.

- TSTL develops wipes and foams that decontaminate diagnostic medical instruments such as nasendoscopes, cardio echo probes and tonometers, and the number of procedures involving such instruments reduced as hospitals became overwhelmed by Covid-19 matters.

- July’s update had provided earlier encouragement as the pandemic receded…

“Hospitals worldwide are gradually returning to normal levels of service, which for Tristel means an increasing number of diagnostic procedures, each requiring a disinfection event“

- …while this FY statement claimed the recovery was “far from complete“…

“We are confident that there is still a significant improvement in demand ahead of us as the global recovery in the provision of diagnostic services is far from complete.“

- …and reassuringly confirmed FY 2023 had started positively:

“The new financial year has started strongly with first quarter sales up 20% on the prior year — a sales run rate of £34m.“

- A sales run-rate of £34m compares to revenue of £31m reported for this FY.

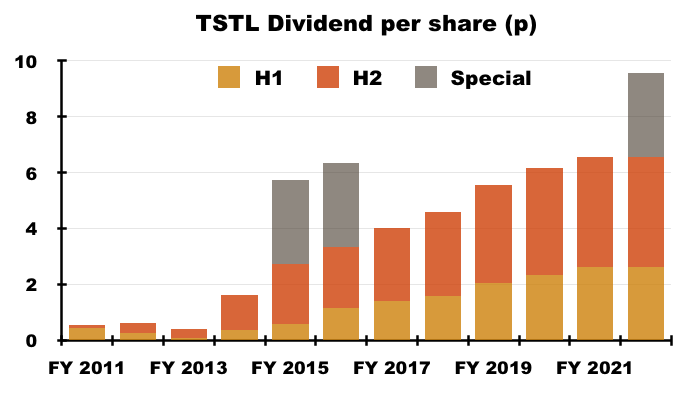

- TSTL held its H1 dividend and this FY 2022 statement announced an unchanged final dividend — the first occasion the full-year payout has not been lifted since FY 2013:

- Dividend cover was 1.3x based on adjusted earnings of 8.4p per share and management said during the webinar the payout would be held until dividend cover reached 2x (equivalent to adjusted earnings reaching 13.1p per share).

- The year’s dividend highlight was revealed within July’s update — a 3p per share special payout.

- The special was TSTL’s third since FY 2015 and — alongside some confident three-year guidance (see Valuation) — suggests the worst of the pandemic disruption has now passed.

Discontinued operations and accounting U-turn

- The preceding H1 2022 statement announced a welcome culling of legacy products that suffered unfavourable economics:

“During the period the Company refocused the business to accelerate top-line growth and increase profitability as it exits the pandemic. This focus is on Tristel’s proprietary chlorine dioxide technology and the hospital market. These represent “Continuing operations”.

The Company has discontinued the manufacture and sale of most products in its Anistel and Crystel product ranges and these represent “Discontinued operations”. The Discontinued operations command substantially lower margins, and the Board considers that they will not contribute to future revenue growth without significant investment.“

- The H1 rationalisation was accompanied by an accounting change that divided the group’s revenue and profit into ‘Continuing’ and ‘Discontinued’:

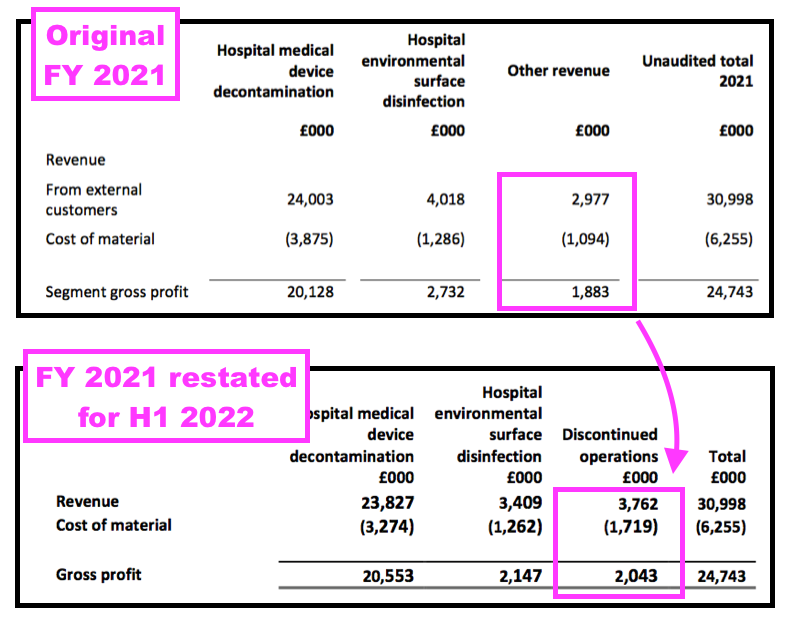

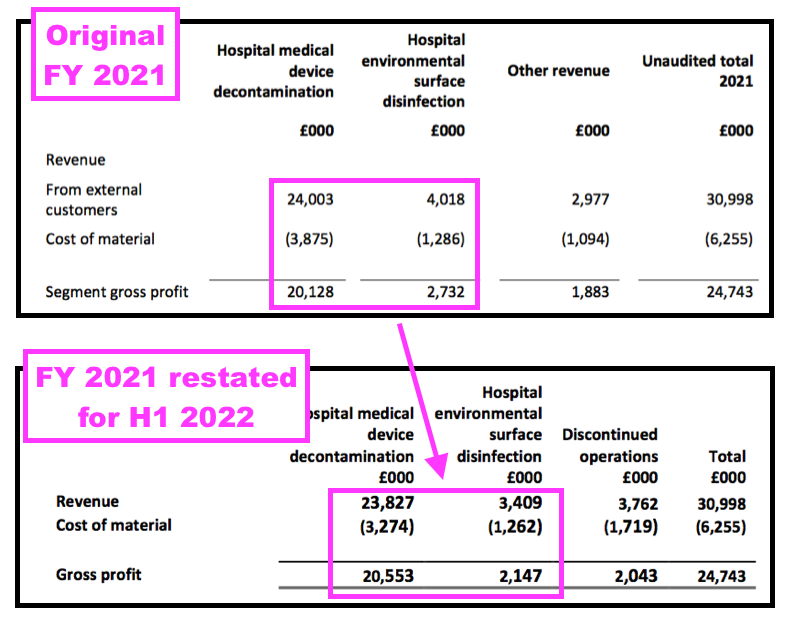

- The H1 re-jig restated certain FY 2021 disclosures and created some confusion.

- For instance, the FY 2021 results had originally declared Other revenue of £3.0m, while the H1 2022 results showed Discontinued revenue for FY 2021 at £3.8m:

- In other words, some products shareholders previously believed generated ‘core’ revenue did in fact generate ‘non-core’ revenue.

- More worrying was the FY 2021 results originally showed a gross profit of £2.7m from surface disinfectants… but the H1 2022 results restated that £2.7m to £2.1m:

- In other words, the surface-disinfectant division was less lucrative than shareholders had previously thought.

- Management explained the accounting U-turn during the FY webinar:

“We believed in February that we were reporting a discontinued operation and the accounting policy around it we thought we satisfied, which was that… there was a whole division… that we were ceasing. But our auditors have told us they viewed it differently, so it’s not appropriate. It’s a pure accounting decision by KPMG… which I’m actually really disappointed about, because I thought it was really simple and straightforward to restate… It was a huge blow. We were very disappointed not to be able to demonstrate it in that way.“

- Management explained after the webinar that the auditors determined the ceased products were not a discontinued operation because the products did not form a “stand alone” unit (the ceased products in fact shared premises and other services with the rest of the group).

- TSTL confirmed the discontinued products “made a neutral profit contribution” for FY 2022:

“The rationalisation was committed to at the end of FY21, largely completed by 31 December 2021, and wrapped up in the second half of FY22. The discontinued products generated revenue in FY22 of £1.5m and after all associated overheads, write-off of redundant inventory and internal reorganisation costs, they made a neutral profit contribution to the year. An impairment charge of £2.4m was recorded as all license rights, IP, and intangibles associated with the products were written down in their entirety.“

- The discontinued products generated a £263k operating profit during H1, and the “neutral profit contribution” for FY 2022 implies H2 closure costs were a matching £263k.

- The £2.4m discontinued-product write-off recorded during H1 was not changed for this FY.

- The accounting U-turn unfortunately makes a fully accurate comparison between H1 2022 and H2 2022 impossible.

- But next month’s H1 2023 announcement should include revised H1 2022 figures that will be directly comparable to all other TSTL results.

- The auditor’s statement within TSTL’s 2022 annual report did not mention the accounting U-turn. Total audit fees for FY 2022 advanced 19% to £331k.

Presentation disclosure

- TSTL’s presentation for this FY 2022 was thankfully more informative than the preceding H1 2022 presentation.

- The H1 powerpoint disclosed revenue only by region:

- But the FY powerpoint disclosed revenue by region in more detail…

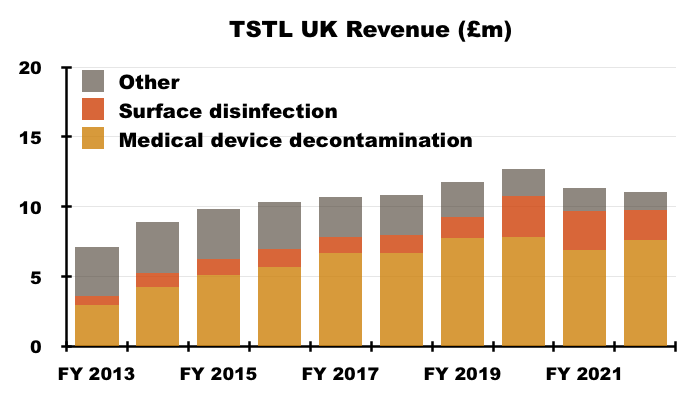

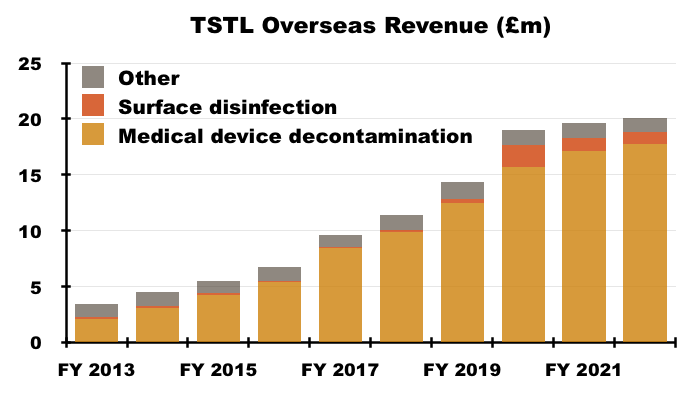

- …as well as disclose revenue by product type:

- As such, determining the sales progress of TSTL’s most profitable products (the medical-device wipes and foams) within its largest market (the UK) has once again become possible.

- I trust UK revenue will continue to be disclosed separately from other regions. The UK is by far TSTL’s most mature market and therefore serves as a guide for the sales potential of other countries.

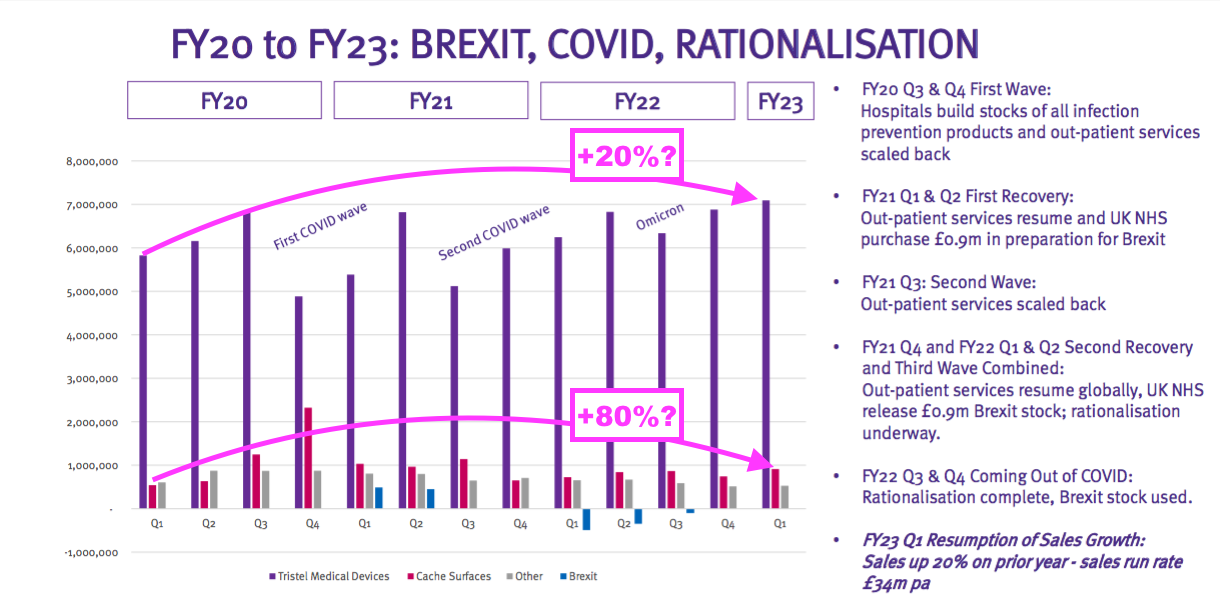

- The original H1 presentation did not include a Pandemic Impact slide.

- But this FY presentation commendably did:

- The Pandemic Impact slide reveals the quarterly revenue ups and downs as Covid-19 disrupted TSTL’s hospital customers.

- Between Q1 2020 and Q1 2023, revenue from medical-device wipes and foams looks to have advanced by approximately 20%, while revenue from surface disinfectants seems to have increased by approximately 80%.

Product categories

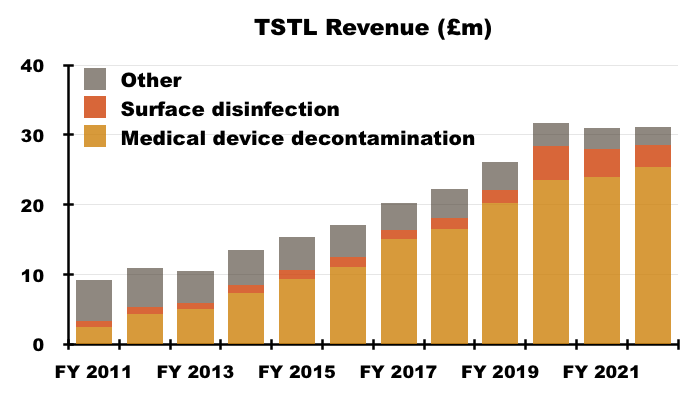

- TSTL’s wipes and foams that decontaminate medical devices remain by far the group’s largest division:

- TSTL divulged an interesting statistic within its July update:

“During the year 15.7 million disinfection events took place with a Tristel medical device disinfectant, which is 31% higher than in the year ended 30 June 2019, before the pandemic struck.“

- Revenue from the medical-device wipes and foams was £20.3m during FY 2019 and £25.4m during FY 2022.

- As such, revenue per medical-device “disinfection event” has declined only a fraction during the last three years, from £1.69 for FY 2019 to £1.62 for FY 2022.

- Cleaning ultrasound probes appears to be TSTL’s primary money-spinner. A statement during June said:

“Ultrasound probe disinfection is one of Tristel’s most important areas of focus within the hospital infection prevention market and accounts for approximately 40% of the Company’s global revenue which analysts forecast at £28 million for the current financial year.

Duo ULT is widely used throughout Europe, the Middle East, Asia, and Australasia and during the Company’s current financial year the product will have been used in over 8 million disinfection procedures of ultrasound probes worldwide.“

- Representing more than 50% of disinfection procedures during FY 2022 (8-plus million out of 15.7 million) but supporting (at most) 40% of revenue implies the Duo ultrasound foam has a lower price point than the typical group wipe or foam.

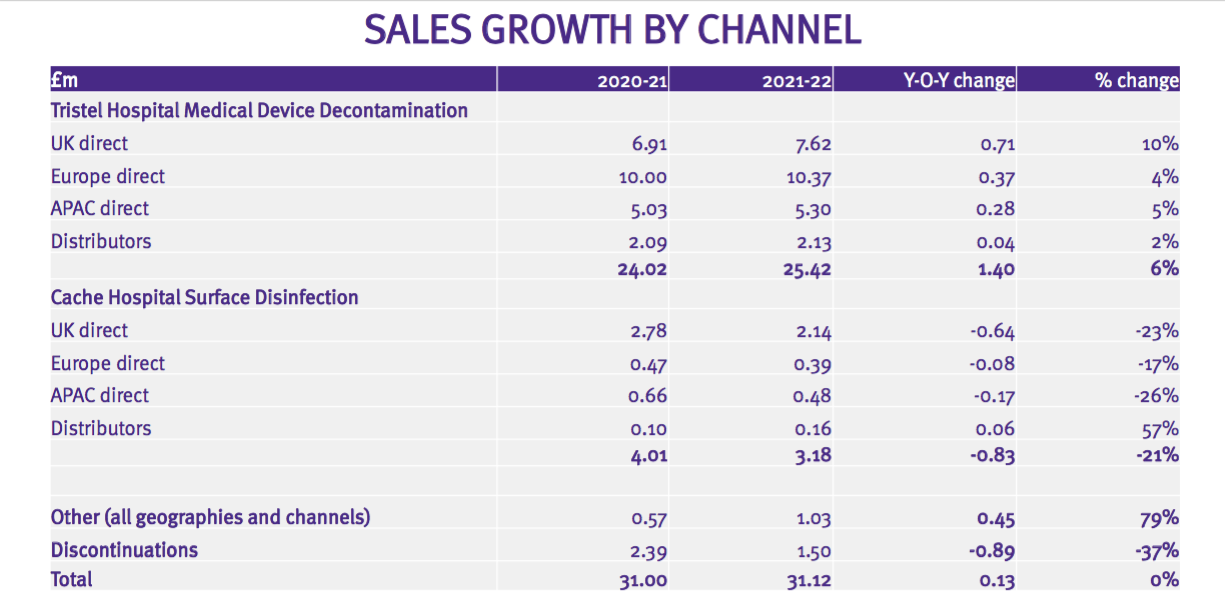

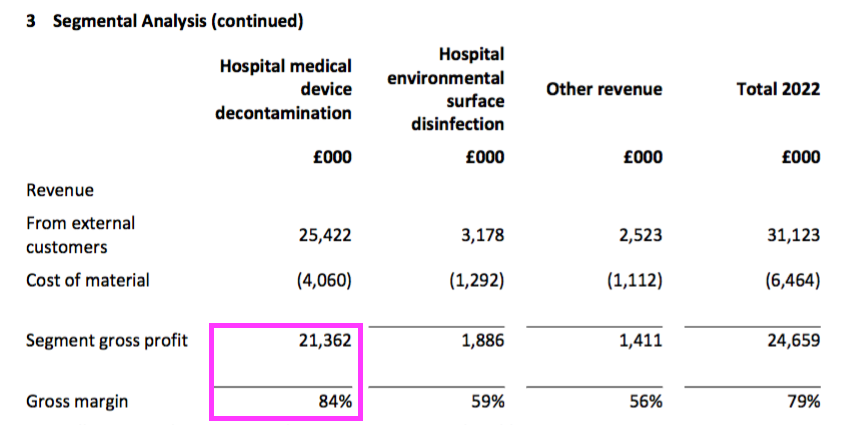

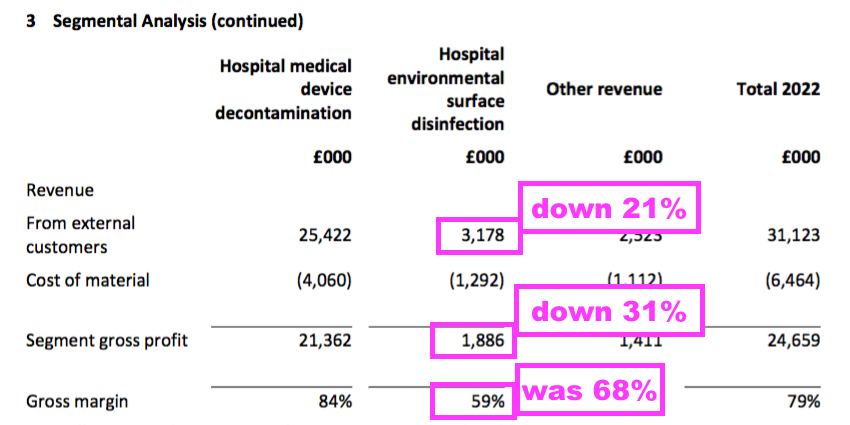

- The medical-device wipes and foams retained an impressive 84% gross margin and represented 87% of group gross profit:

- TSTL’s surface disinfectants — used for cleaning hospital surfaces such as floors, mattresses and bedside tables — displayed lower revenue, lower gross profit and a lower gross margin:

- The weaker surface-disinfectant performance seemed due to the aforementioned discontinued products; the preceding H1 acknowledged some discontinued products had previously contributed to the surface-disinfectant division.

- TSTL was optimistic about the prospects for Cache, its surface-disinfectant brand:

“Our objective is to create a clearly identifiable segment within surface disinfection for sporicidal products and to be the global market leader in this segment.

…

The cleaning and disinfection of environmental surfaces in hospitals is ubiquitous and the global expenditure by hospitals on surface disinfection is far greater than the expenditure on decontaminating medical devices. The capability of a disinfectant to kill bacterial spores is the defining hallmark of the best-performing biocides, and chlorine dioxide is one of the elite chemistries that can kill spores.

We expect a legacy of COVID-19 will be that hospitals will be more rigorous in their selection of the best performing and most scientifically validated disinfectant products, which will benefit Cache.”

- Conversations with TSTL’s staff during July’s open day revealed the surface disinfectants “cannot compete on efficacy alone“, and a product revamp now made “routine” surface disinfection as cheap (if not cheaper) than the ubiquitous (but less effective) pre-wetted plastic wipes.

- However, management revealed during the FY webinar the surface-product revamp had not yet been launched…

“[Cache] does have a big future. The year was an anomaly, sales have fallen in the UK and that is due to the mix of products within there, the new products we are launching, the capsules, the Tank, they are not launched yet, they are not available and legal to sell, because we have been advised by our hospital market that they need to have the UK CA mark applied to them… So that’s another hurdle for us to jump to obtain regulatory approval for those products as medical devices, even though they are surface disinfectants.”

- Management added during the webinar that surface disinfectants were being given away to help create awareness:

“The gross margin has fallen as a consequence of sampling and giveaways, in order to get the product moving.”

- Management told webinar attendees to take the long-term view with the surface division:

“You’ve got to take a long-term view, we have a big ambition [with surface disinfectants], it’s not going to happen in anything other than many years.”

- I have been a TSTL shareholder for nine years, during which time revenue from the medical-device wipes and foams has quintupled to £25m and revenue from surface disinfects has quadrupled to £3m.

- In theory at least, a much more effective surface cleaner that is cheaper than the ubiquitous pre-wetted plastic wipe — as well as being much more environmentally friendly — ought to have a big future.

- The downside with surface disinfectants may not be their future growth rate, but their significantly lower price point compared to the wipes and foams.

- Management presentation comments from FY 2018 suggested the NHS was purchasing low-grade surface wipes at 2p a pop.

- Assuming TSTL effectively price matches that 2p, enormous volumes will therefore be needed if surface disinfectants are ever to represent a notable proportion of TSTL’s profit.

- TSTL promoting the environmental benefits of its surface disinfectants against pre-wetted wipes does raise the question about the environmental impact of its own Trio wipes product.

- Do note that Other revenue of £2.5m included ‘discontinued’ revenue of £1.5m, which still leaves revenue of £1m earned beyond hospital wipes, foams and surface disinfectants.

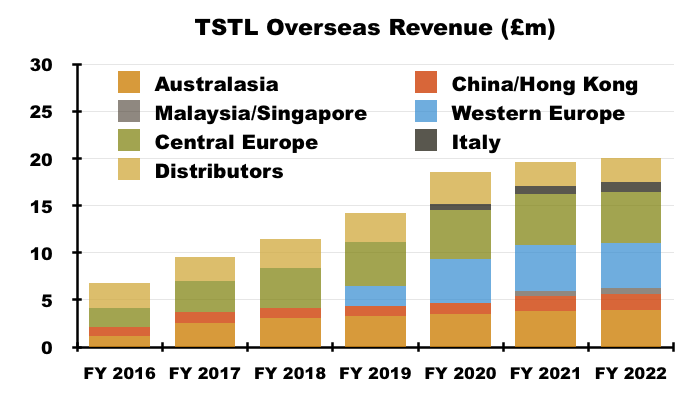

UK versus overseas

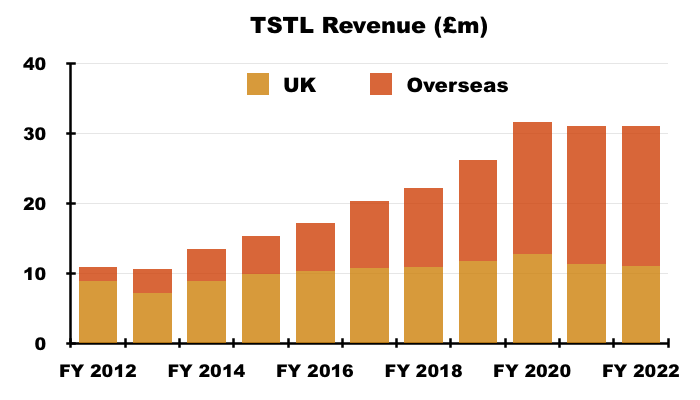

- UK revenue represented 35% of total revenue, the lowest full-year proportion in TSTL’s history:

- UK revenue has stagnated somewhat since (pre-pandemic) FY 2019…

- …while overseas revenue has advanced higher:

- Reasons for the diverging performances may include:

- Tighter pandemic restrictions within the NHS than overseas;

- Greater ‘discontinued’ products sold within the UK;

- TSTL acquiring distributors within markets such as Benelux, France, Italy and Malaysia, and;

- Favourable currency fluctuations.

- But perhaps the fundamental reason for the diverging performances is TSTL’s much greater UK market share. The group started to experience slower domestic progress way back in H1 2016:

“Slowing growth in the United Kingdom is due to the very high levels of market penetration that we have achieved in the clinical areas of the hospital that we target.“

- TSTL’s largest overseas region, central Europe (Germany, Poland and Switzerland), has in contrast witnessed its revenue more than double since FY 2016:

- Furthermore, the subsequent performances of overseas distributors acquired by TSTL have been particularly impressive.

- TSTL acquired its Australian distributor for £1.1m during FY 2017.

- Australasian sales (i.e. Australia and New Zealand) have since climbed 87% from approximately AU$3.9m to approximately AU$7.3m (six-year CAGR: 11%).

- TSTL acquired its Benelux/French distributor for £6.4m during FY 2018.

- Western Europe sales (i.e. Benelux and France) have since climbed approximately 86% from €3.1m to approximately €5.7m (four-year CAGR: 17%).

- TSTL acquired the outstanding 80% of its Italian distributor for £0.6m during FY 2020.

- Italian sales have since climbed 70% from €700k to approximately €1.2m (three-year CAGR: 19%).

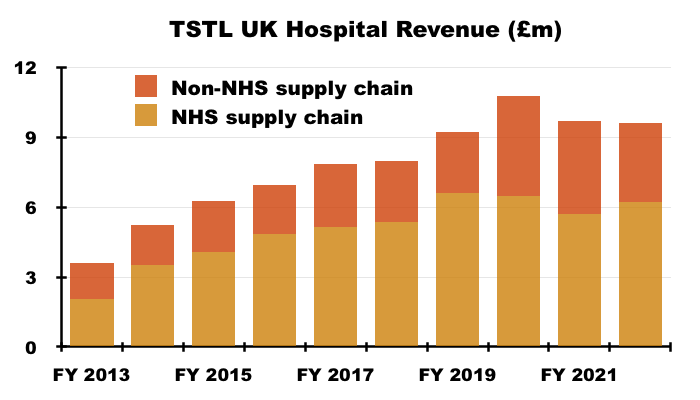

- TSTL’s UK progress can be influenced by revenue fluctuations created by the NHS Supply Chain (the group’s largest customer):

“Hospital medical device decontamination revenues were derived from a large number of customers but include £4.572m from a single customer which makes up 18% of this segment’s revenue (2021: £5.727m, being 24%). Hospital environmental surface disinfection revenues were derived from a number of customers but include £1.636m from a single customer which makes up 51% of this segment’s revenue (£0.930, being 23%).”

- Revenue earned from the NHS Supply Chain was £6.2m for FY 2022, but adjusted for Brexit stock-piling would have been £7.1m — and in excess of the record £6.6m earned from the Supply Chain during FY 2019.

- TSTL’s UK revenue remains dominated by the Supply Chain:

- Prior to the recent Brexit stock-piling, TSTL previously cited the Supply Chain’s unpredictable buying patterns and bulk purchases for some inconsistent UK performances.

- TSTL did not appear concerned about any NHS budget pressures, with the presentation slides confirming “an actual price increase of 6-8% being implemented during the course of H1 [2023] in all geographical markets.”

- The proportion of total revenue derived from the NHS Supply Chain has reduced from 26% during FY 2017 to 20% during FY 2022.

United States: FDA submission

- The preceding H1 statement had reiterated TSTL would submit its application for FDA product approval by 30 June 2022:

“In the USA we have re-commenced state-by-state registration of Duo Ultrasound under our EPA approval and are confident we will complete the FDA De Novo submission for Duo by June this year“

- An update on 30 June 2022 confirmed the submission had occurred…

“Tristel… the manufacturer of infection prevention products, reports that it has submitted its De Novo request for approval to the FDA, the United States regulatory body responsible for medical device disinfectants. Tristel Duo ULT is used for the disinfection of ultrasound probes.“

- …and expressed confidence about the impact an FDA approval would have on the group:

“The United States is the largest ultrasound market in the world.. .Duo ULT is recognised as a leading high-level disinfectant throughout the rest of the world, and our entry into the United States market will be a significant inflection point for the Company.“

- June’s update also noted additional data requests from the FDA were “commonplace“…

“The FDA’s De Novo review and approval process stipulates a 150-day decision timeframe. Additional data requests are commonplace, and the FDA website states that the average duration for review and approval is approximately 11 months.“

- …and sure enough, an update during September revealed the FDA had requested additional data:

“In June Tristel achieved a major milestone event by making its De Novo submission to the USA Food and Drug Administration (FDA) for its Tristel DUO ULT product which is used as a high-level disinfectant for ultrasound intra-cavity probes. Following the FDA’s complete review of the submission, it has provided the Company with an Additional Information request.

As previously outlined to shareholders, Additional Information requests are commonplace within the De Novo submission process, and therefore the previous guidance on the average duration for review and approval of approximately 11 months remains accurate for this submission. The Company and its advisors are confident that the 180-day timeline set by the FDA to return the information will be met. The overall expected timescale for the process is unchanged.“

- These FY 2022 results confirmed the FDA’s decision should be published by June 2023:

“After more than five years of data generation, we lodged our De Novo submission for the high-level disinfectant Duo ULT with the FDA in June 2022. Our best intelligence is that De Novo submissions are typically decided upon by the Agency within twelve months.“

- The results RNS did not shed any light as to what additional information the FDA required.

- But management did reveal during the webinar the request for additional information was “pretty extensive“:

“The submission was extensive, it ran to many hundreds of pages, it underwent a successful completeness check by the agency, and then they completed their review… and as a consequence of completing that review provided us with a detailed and pretty extensive request for supplemental additional information and clarification on many points, a lot of the data they want clarification, some challenges as to the methods we had used to generate that data and we are now in the process of discussing and negotiating with the FDA, so we really do understand with our advisors what they want, and the detail and the protocols and the methodologies they want us to employ and then we will go off and get that additional data generated.”

- Management also said during the webinar the additional request involved applying the same batch of product for all three categories of testing:

“So they [the FDA] ideally want [us] to use the same batch of product across all three categories of testing. We couldn’t, because what was used in the potency testing in 2015, 2016, was out of date, and so you can’t work with it. So you can see some of the practical difficulties that we have encountered.

But they have rules and guidelines and so the guideline says that we should use the same batch that’s used across all three tiers [of categories], so a bit of negotiation and… we will go back as far as we can with the batches that we still have in storage, and use that on at least two of those categories.”

- The saving grace is the usage of “ideally“, “guideline” and “negotiation“, which implies TSTL may persuade the FDA the whole testing process does not have to be repeated with the same batch of product.

- TSTL has already taken five years to undertake the tests to support this FDA submission.

- Management said during the webinar it was confident of a “successful outcome”:

“Nothing that they [the FDA] have presented us with causes us any great concern. It’s well within our gift to generate the responses that they are looking for. It’s important there is no ambiguity about what we do because we have to get it all done within the 180-day period, but we are confident we will. And we have to remain confident that we will get a successful outcome from the FDA.”

- And that confidence was repeated within December’s AGM statement:

“…[W]e are preparing the additional data requested by the FDA in September. We expect to submit it in March next year, meeting the FDA’s deadline and facilitating a decision from the agency around our year-end in June. We remain confident of a successful outcome.”

- The risk of course is the FDA ‘negotiations’ do not go well, TSTL can’t generate the necessary additional information by March and the FDA approval timetable slips further…

- …or even worse, the FDA demands a fresh submission with completely new data based on a single product batch.

United States: FDA Predicate and De Novo guidance

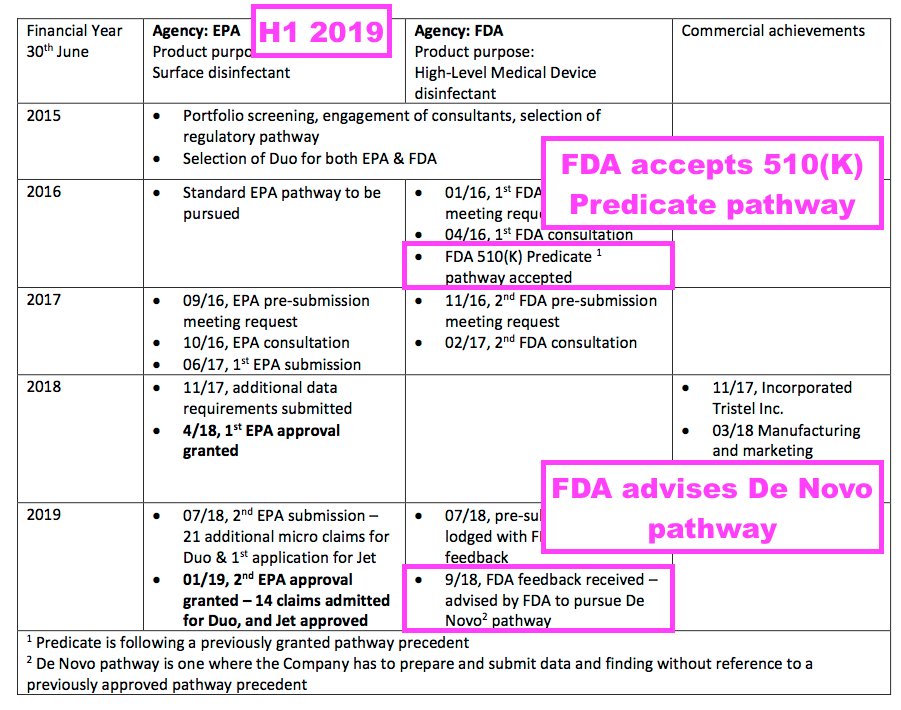

- TSTL has been consistently optimistic about FDA submissions and timetables.

- My notes from 2015 recall management initially hoping FDA regulatory approval would be received by June 2017.

- By October 2016, the directors were forecasting US revenue being earned during the year to June 2019.

- By October 2018, the directors were expecting the FDA submission would be completed by June 2019.

- And by February 2019, TSTL had withdrawn all FDA guidance after receiving feedback from the agency during the preceding September:

“We received the FDA’s feedback on 25 September 2018 to the pre-submission written review which we lodged in July 2018. Their feedback was to follow a De Novo pathway rather than the Predicate pathway.“

- Back in February 2019, TSTL noted the FDA had already accepted the group using (the less demanding) 510(K) Predicate route for regulatory approval:

- The FDA’s change of mind to a (more demanding) De Novo application meant TSTL required far more testing and data for its regulatory submission.

- But TSTL remained optimistic despite the FDA’s change of mind.

- Full-year results published on 17 October 2018 — three weeks after the FDA’s revised application guidance was received on 25 September 2018 — revealed TSTL still hoping to submit an application based on the original (and less demanding) 510(K) Predicate process:

“We are preparing a submission to the FDA for Duo as a high-level disinfectant… We expect to submit the application for 510(K) approval during the financial year ending 30 June 2019.“

- An AGM update on 11 December 2018 — more than two months after the FDA’s revised application guidance was received — then stated the FDA project was “progressing as planned“:

“The Company is performing in line with management’s expectations and our United States regulatory approvals project is progressing as planned.”

- With the benefit of hindsight, TSTL ought to have formally disclosed the FDA’s revised application guidance earlier than it did.

- The FDA application process started during 2015, and the subsequent setbacks and confusion allow layman shareholders the right to doubt whether a positive FDA verdict will be received within TSTL’s current expectations.

- For what it is worth, I am quite sure TSTL’s Duo foam boasts all the scientific qualities to meet the FDA’s requirements. The same foam is after all currently used without problem in many other countries.

- But whether TSTL’s extra test data will meet the FDA’s additional-information requirements remains to be seen.

- The application setbacks of the past will be quickly forgotten if, as TSTL expects, the FDA announces an approval by June this year.

United States: costs and potential

- As the FDA decision is awaited, sales of Duo foam have begun in the States under EPA approval (for disinfecting ultrasound consoles). December’s AGM statement confirmed:

“With respect to North America, we have made our first sales in the United States and Canada…“

- Management did not suggest during the webinar the EPA approval would lead to an immediate sales bonanza:

“You can regard this as a soft market introduction with a view to gaining brand awareness, getting the product into our distribution network in the States, which has been established with our partner Parker Laboratories, all in preparation for the FDA launch, later next year, or indeed we may well find that this product approved by the EPA, as an intermediate level disinfectant… will in its own right be very successful. And that would be our hope.“

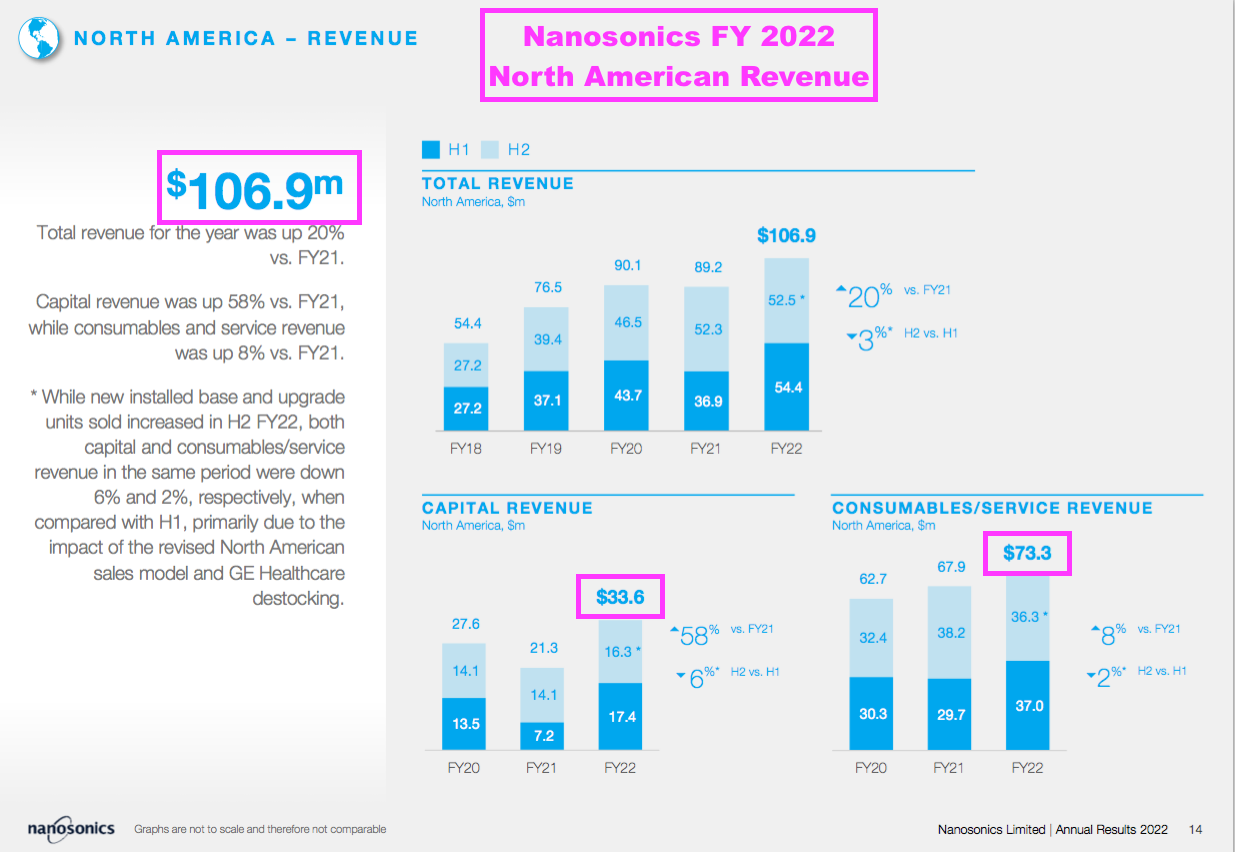

- Hints of potential long-term sales in the States were dropped during July’s open-day presentation.

- Management more than once referred to the North American ‘consumable’ revenue of £30m enjoyed by Nanosonics (NAN), the Australian manufacturer of the Trophon machine that disinfects ultrasound probes.

- NAN’s consumable revenue is generated from the sale of disinfectants used within its Trophon machines.

- Conversations with staff at July’s open day indicated TSTL plans to price its disinfectants in the States at the same level as NAN’s Trophon disinfectants.

- NAN’s FY 2022 results showed North American revenue of AU$107m (c$79m), comprising AU$34m (c$25m) from the sale of machines and AU$73m (c$53m) from consumables and servicing:

- NAN has installed 26,130 Trophons in North America and still reckons the market could sustain 60,000 Trophons.

- Wishful thinking I know, but assuming TSTL can one day achieve NAN’s £30m consumable revenue in the States, the mooted 17.5% royalty from sales handled by Parker Laboratories would lead to US royalty income exceeding £5m.

- £5m of US royalties would be very significant versus FY 2022’s operating profit (before share-based payments, US costs and discontinued-product write-downs) of approximately £6m.

- NAN’s revenue is limited to disinfecting ultrasound probes, while TSTL’s wipes and foams can disinfect ultrasound probes as well as numerous other medical devices.

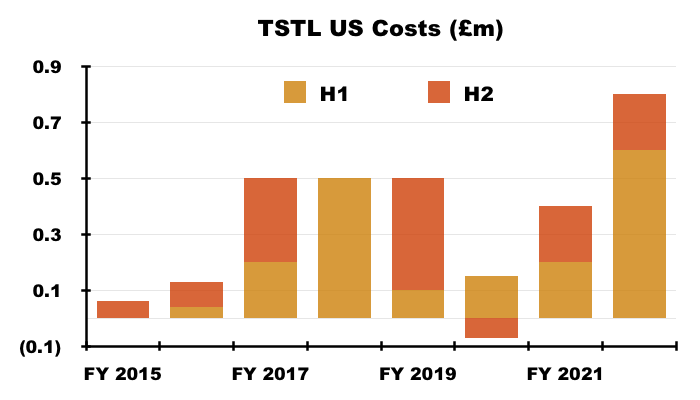

- US costs were £0.6m during H1 and £0.2m during H2, taking the aggregate US expense to £3m:

- Adjusting TSTL’s reported profit for US costs allows shareholders to better judge the group’s underlying profitability. US costs up to FY 2022 have of course been accompanied by no US revenue.

Patents and chemistry

- TSTL has regularly cited patents as part of its competitive advantage:

“In its broadest sense, our intellectual property relates to:

1. Patents, trademarks and registered designs;

2. The scientific validation of our chemistry and our products that have entered the public domain, via a number of peer‐reviewed and published papers, and;

3. The certification by medical device manufacturers that our chemistry is compatible with their products. We enjoy official compatibility with the instrumentation of 56 medical device manufacturer, with respect to 1,449 of their individual models.”

- Some of TSTL’s patents are due to expire within the next few years.

- Google Patents shows the expiry dates of TSTL’s wipe patents to be:

- UK: 7 May 2024 (GB 240 4337)

- EU: 26 July 2024 (EP 174 2672)

- US: 7 September 2024 (US 808 0216)

- Google Patents shows the expiry dates of of TSTL’s foam patents to be:

- UK: 27 January 2026 (GB 242 2545)

- EU: 27 January 2026 (EP 184 3795)

- US: 11 September 2030 (US 884 0847)

- Management said during the preceding H1 2022 webinar:

“It is more than the patent that gives us our protection. There is proprietary know-how that is in the formulation“

- I have previously concluded the “proprietary know-how that is in the formulation” — which I believe is not cited in the patent — relates to the speed of the chemical reaction.

- A short discussion with Bruce Green, the chemist who devised TSTL’s disinfectant chemistry, at July’s open day provided further insight into the group’s competitive advantage.

- According to Mr Green, the competitive advantage is not only helped by not divulging the chemistry, but also by not divulging the “manufacturing that goes into the chemistry“.

- Mr Green added that large American companies have tried to ‘reverse engineer’ TSTL’s chemistry, but had no success because they “did not know the right route to go“.

- Mr Green summarised the situation by telling me “don’t be concerned” about the patents expiring.

- Mr Green was notably bullish on the opportunity from new (but not yet approved) patents, which attempt to ensure manual cleaning is as effective as automated cleaning by filming and analysing the process.

- I believe these new patents to be GB 259 7911, GB 259 7912 and GB 259 7913, which all cover the “validation of procedures in a decontamination process” that involve “capturing a video stream of a work area… in which the… procedure is carried out by a user [and] analysing the video stream…”

- If approved, these new patents could be — at least according to Mr Green — a “game changer on a world basis”.

Share options

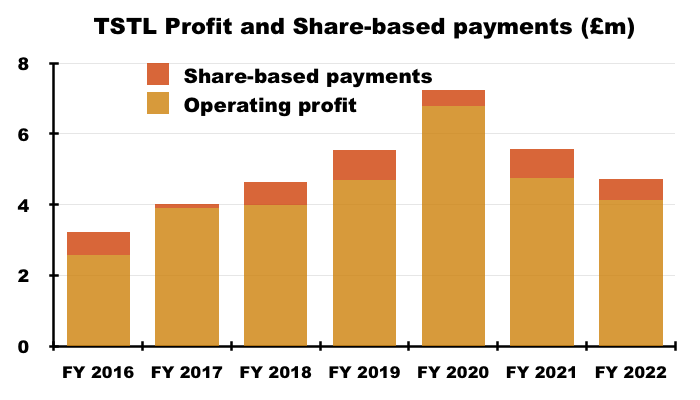

- Significant share-based payments have featured regularly within TSTL’s accounts.

- Between FY 2016 and FY 2022, share-based payments reduced the aggregate pre-exceptional operating profit by £4.2m, or 12%:

- FY 2022 witnessed share-based payments reduce pre-exceptional operating profit by £596k, or 13%.

- Note that the share-based payment charge was £884k during H1, meaning H2 incurred a £228k share-based payment credit.

- Accounting rules say companies should calculate a share-based payment charge even if the options eventually become worthless.

- TSTL’s (somewhat contentious) 2015 senior management options were granted when the shares were 96p and would vest if the price topped 134p.

- TSTL’s (less contentious) 2018 management options were granted when the shares were 275p and would vest if the price reached 350p, 425p and 500p.

- All the 2015 and 2018 options vested as the share price climbed from 96p to 500p.

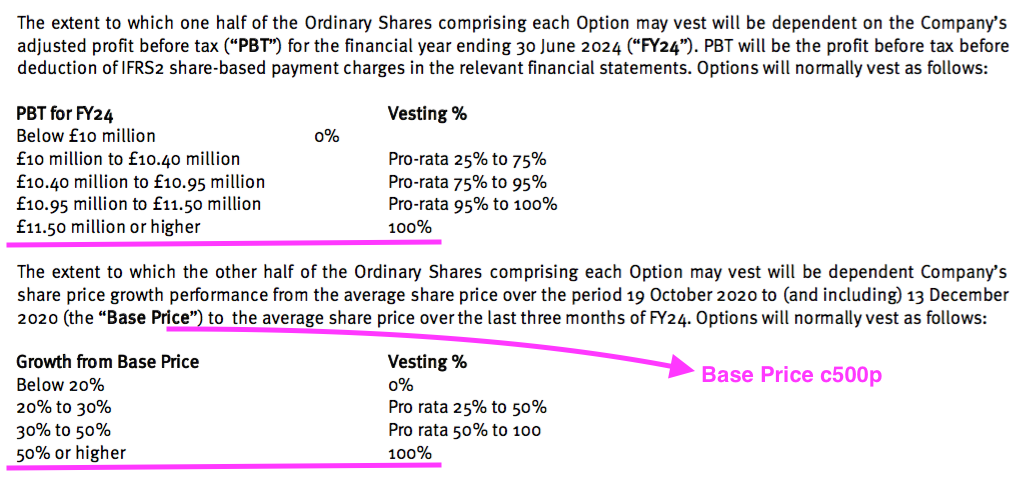

- TSTL granted 800k further executive-director options at the start of calendar 2021 when the shares were 500p.

- These 800k options will vest in full if profit before tax (and share-based payments!) surpasses £11.5m and the share price tops c750p during FY 2024:

- For any of the 800k options to pay out, profit before tax and share-based payments has to reach £10m during FY 2024 (versus £4.7m for FY 2022) or the share price has to trade at a c600p average during Q4 2024.

- TSTL’s pandemic-hindered progress during FYs 2021 and 2022 suggests profit before tax reaching £10m — let alone the maximum £11.5m threshold — by FY 2024 to be very remote.

- The present 350p share price is well below the minimum c600p requirement, too.

- This latest 800k batch of options is therefore likely to become worthless — and the year’s £596k share-based payment charge is therefore likely to become very irrelevant.

- The real cost of options to ordinary shareholders is through dilution and not accounting charges.

- TSTL’s share count has advanced 14% since the start of FY 2016, with 12% due to options and 2% due to the purchase of the Benelux/France distributor.

- The 2022 annual report showed 2,083k total options outstanding and a 47.2m share count, which indicates a maximum further dilution of 4.4%.

Financials

- TSTL’s accounts appear in adequate shape despite the pandemic hindrance and accounting U-turn.

- Excluding share-based payments, US costs, discontinued-product write-offs and other operating income, operating profit of £5.4m equated to a useful 17% operating margin:

| Year to 30 June | 2018 | 2019 | 2020 | 2021 | 2021 |

| Operating margin* (%) | 23.2 | 23.0 | 22.3 | 19.2 | 17.2 |

(*before share-based payments, US costs, write-offs and various minor items)

- The lower margin during the pandemic-disrupted years of FYs 2021 and 2022 has been due primarily to greater staff costs. TSTL said:

“Overheads (excluding share-based payments, depreciation, amortisation and impairment) rose by 6% from £16.4m to £17.4m, principally due to the increase in headcount from 189 to 199. The associated increase in wages and salaries of £0.7m (excluding share-based payments) was partially offset by a reduction in travel and the number of medical conferences at which we exhibited.“

- The extra headcount in part relates to greater compliance requirements:

“Compliance can only be achieved by increasing overhead to attract the best Quality Assurance and Regulatory Affairs people in a highly competitive market for such skills. This is one cause of the upwards pressure on our business costs.”

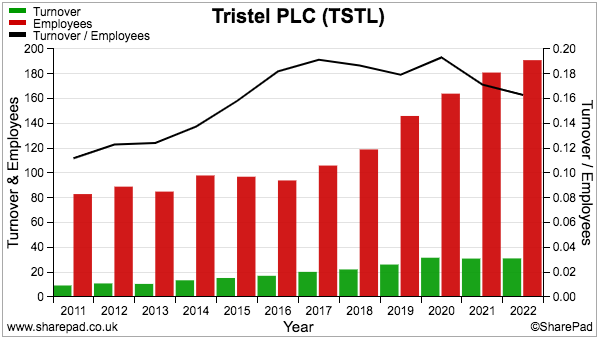

- Employee productivity has unsurprisingly declined during the pandemic:

- Revenue per employee is not unsatisfactory at approximately £160k, but is back to a level first seen during FY 2015.

- TSTL’s balance sheet implies the business remains an inherently capital-light operation.

- Net assets of £29m less intangibles (£9m) and cash (£9m) leaves £11m, represented mostly by working capital (£7m) and property, plant and equipment (£3m).

- £11m compares to FY 2022 operating profit (before share-based payments, US costs and discontinued-product write-offs) of approximately £5m, and implies TSTL may not need to reinvest huge amounts to advance profit further.

- Cash flow remains respectable.

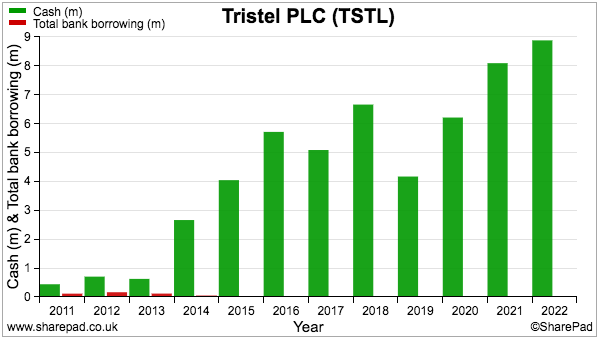

- The year ended with cash at £8.9m, up £0.8m, after £3.5m was generated by the business, £0.4m was raised through options and £3.1m was paid as dividends.

- For this FY and on aggregate during the last five years, net expenditure on tangible and intangible assets has been commendably matched by the combined depreciation and amortisation expensed against earnings:

| Year to 30 June | 2018 | 2019 | 2020 | 2021 | 2022 |

| Operating profit* (£k) | 4,645 | 5,549 | 7,240 | 5,586 | 4,724 |

| Depreciation and amortisation (£k) | 1,498 | 1,470 | 1,799 | 1,974 | 1,737 |

| Net capital expenditure (£k) | (1,450) | (1,347) | (2,380) | (1,767) | (1,203) |

| Working-capital movement (£k) | (520) | (780) | (1,453) | 324 | (1,003) |

| Net cash (£k) | 6,661 | 4,170 | 6,212 | 8,094 | 8,883 |

(*before share-based payments and write-offs)

- Working capital has absorbed an extra £3.4m during the last five years, which does not seem too horrendous given revenue during the same time has advanced by £11m, or 50%.

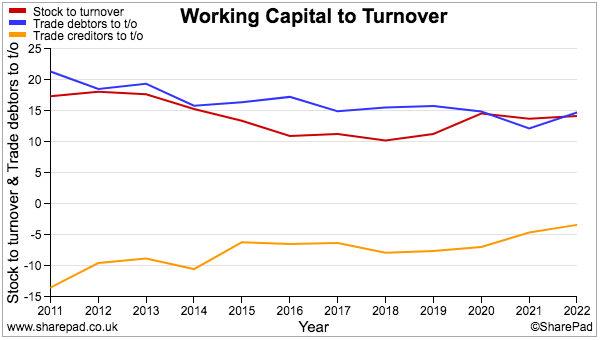

- SharePad shows stock and debtor levels versus revenue as being reasonably consistent, while decreasing creditor levels presumably reflect TSTL paying suppliers faster and does not feel too worrying:

- December’s AGM statement said cash had increased after the year-end to “approximately £10m“.

- TSTL carries no bank debt and no final-salary pension obligations:

Valuation

- December’s AGM statement implied revenue may advance at least 9% to at least £34m for FY 2023:

“The Company is returning to its pre-pandemic growth trajectory, with first half revenue expected to exceed £17m, compared to £15m in the first half of last year. Revenue growth is consistent across all our geographical markets. Gross margin is in line with expectations…

The Company is making good progress… [and] we face the prevailing economic environment with confidence“”

- FY 2023 revenue growth excluding the discontinued products should be greater than the implied 9%.

- Looking further out, this FY statement repeated the three-year guidance unveiled at July’s open day:

i) sales growth in the range of 10% to 15% per annum as an annual average over the three years;

ii) the achievement in each year of an EBITDA margin (excluding share-based payment charge) of at least 25%.

- The guidance was almost the same as that set during October 2019 for the three years to FY 2022:

“i) sales growth in the range of 10% to 15% per annum as an annual average over the three years;

ii) the achievement in each year of an EBITDA margin (excluding share-based payment charge) of at least 25%, and

iii) to increase profit before tax (excluding share-based payments) year-on-year, independently of the other two targets.

- This time the third ambition — to increase profit before tax year-on-year — has been dropped.

- TSTL commendably compared the 2019 targets to the group’s subsequent performance:

- Management confirmed during the webinar that no US sales were included in the new three-year guidance.

- Achieving the top-of-the-range 15% revenue-growth target would deliver FY 2025 revenue of £47.3m.

- Then meeting the minimum 25% Ebitda margin (before share-baed payments) would give FY 2025 Ebitda of £11.8m.

- Less FY 2022’s depreciation and amortisation of £2.7m then produces a pre-tax profit of £9.1m.

- Applying the forthcoming 25% standard UK tax rate then leaves earnings of £6.8m or 14.5p per share.

- The valuation sums could be fine-tuned further for lease costs, the cash position, depreciation/amortisation changes and tax intricacies, but the 350p share price at 24 times my 14.5p per share calculation — for FY 2025 — does not indicate an obvious bargain.

- The premium share-price rating may be justified if:

- TSTL’s secret chemistry, manufacturer agreements and regulatory approvals continue to underpin a worthwhile competitive advantage;

- The renewed focus on hospital wipes, foams and surface cleaners revives TSTL’s operating margin and employee productivity;

- TSTL proves resilient against a tricky global economy and enjoys further meaningful growth within its established markets, and;

- An FDA approval is received as expected, US sales suddenly take off and hefty royalties are quickly collected.

- June’s update was positive on that final point:

“Within the next five years we have high hopes that America will be a significant revenue and profit contributor to the Group“.

- But the likely share-price downside remains significant should TSTL fail to obtain FDA approval after taking eight years to lodge a submission.

- While shareholders await the FDA’s verdict, the trailing 6.55p per share ordinary dividend supports a modest 1.9% income.

Maynard Paton

Hi Maynard

It seems that your patience will be rewarded. I watch with interest, having bought a tiny position this morning whilst awaiting your analysis of this development….

(FWIW – like you, I have been following this firm for many many years)

Regards

Charles

Thanks Charles. Analysis due sometime before October’s FY results!

Maynard

Hi Maynard

I’m now doing my own analysis of Tristel (nothing like as thorough as yours). Whilst many things seem very good here, I’m concerned about the capital management at this company.

The ‘discontinued operations” involved a write down (or write off) of a number of assets. In particular the valuation of intangibles at £2.4m should have been a real valuation – i.e. I’d normally expect the value to be checked annually. So if they were worth £2.4m in the previous year, then that part of the business must have been profitable or at least had positive cash flow. So I’m wondering why was it not sold? (especially since they probably had some other associated costs of closure). I hope you don’t mind me asking – has this matter been raised with management by you or anyone else?

I’m also wondering how they justified the previous valuation?

Regards

Charles

Hi Charles

Thanks for the question and many apologies for the tardy reply.

My thoughts at the time of the product cull are here.

I wrote: “Despite generating that £1.4m profit during FY 2021, the terminated products were effectively valued at zero by their discontinuation.”

So yes, those products were profitable.

From my blog post notes of the time, I can’t recall me or anybody else asking about why the products were not sold to a trade buyer. I recall thinking the decision to cull those products was a bold but welcome move, and I wanted management to focus on the money-spinning wipes and foams. I was also distracted by a lot of re-jigged numbers at that time as the products were reclassified in the accounts and presentation.

The relevant website presentation recording is here. I think you can submit a fake email to watch it.

TSTL said at the time:

“Whilst the product ranges have always made a net profit contribution and have generated cash, the revenue decline could only be reversed by making a substantial and high-risk investment in bulking up our sales and marketing activities in markets which are dominated by multinationals manufacturing generic cleaning and disinfectant products at a scale which we did not believe we would be able to match.”

On reflection I should have asked why a disposal was not sought. But I would like to think the decision to cease production and not sell the products will not make much difference to shareholders over the longer term.

Maynard

Hi Maynard

Thank you very much for that detail.

FWIW, whilst the prospects for the US market are very good indeed, I’m pretty sure that I won’t make Tristel one of my main holdings. They do seem a little too easy going for me!

Regards

Charles

Tristel (TSTL)

Publication of 2022 annual report

Here are the points of interest beyond those noted in the blog post above:

1) RESTATEMENTS and ADJUSTMENTS

The FY 2022 results were difficult to analyse due to accounting U-turns, discontinued operations, write-offs, Brexit stock-piling and US costs.

I did not dare mention the tax restatement for the preceding 2021 that added 23% to 2021 earnings:

A £170k tax asset that I recall looking odd as a liability for 2021 was indeed a £170k tax asset, and the 2021 balance sheet has been restated.

The adjustments for 2022 look acceptable for the discontinued impairments and share-based payments:

I must admit the prior-year 2021 adjustments confused me as the £807k fair-value movement was EXCLUDED from the operating profit in the P&L — and therefore should not interfere with adjusted operating profit and adjusted EBITDA:

But the operating profit stated in this note (£3,955k) INCLUDES the £807k fair-value movement, which is inconsistent reporting but the adjusted figures do add up.

Note that management’s financial-target efforts for 2021 were restated for 2022:

I don’t know why annual/average revenue growth was restated slightly. Adjusted Ebitda margin was restated from 24.5% to 27.1% I think due to the £807k fair-value investment movement being incorrectly included originally within adjusted Ebitda.

All told, these restatements just do not give a good impression of TSTL’s reporting — especially given the headline numbers are already difficult to interpret. I note shareholder presentations now include the presence of the group’s financial controller, who I trust is increasingly assisting the FD with the reporting.

2) HIGHLIGHTS

A few positive quotes taken from the opening pages that I omitted from my blog post above:

“WITH BREXIT BEHIND US, THE EFFECTS OF COVID-19 RECEDING, AND THE RATIONALISATION CONCLUDED, WE ARE SET TO RESUME CONSISTENT REVENUE AND PROFITS GROWTH”

“WE HAVE ENTERED THE CURRENT FINANCIAL YEAR WITH A STABLE, PREDICTABLE ORDER PATTERN FROM OUR LARGEST UK CUSTOMER”

“WE HAVE SEEN A MARKED INCREASE IN SERVICE LEVELS IN ALL 14 COUNTRIES IN WHICH WE OPERATE DIRECTLY”

3) CHIEF EXECUTIVE’S REPORT

a) Revenue by geography

Closed Russia, while Singapore is new for 2022.

“We have 14 subsidiaries selling directly into the hospital marketplace in the United Kingdom, Belgium, the Netherlands, France, Italy, Germany, Switzerland, Poland, Hong Kong, China, Malaysia, Singapore, Australia, and New Zealand. We have subsidiaries in the US, Japan, India and Ireland, which are not yet active in terms of selling. We closed our Russian subsidiary early in the current financial year.”

b) Intellectual property protection

A few changes here:

“On 30 June 2022, we held 137 patents granted in 33 countries providing legal protection for our products. In its broadest sense, our intellectual property relates to:

1. Patents, trademarks and registered designs

2. The scientific validation of our chemistry and our products that have entered the public domain, via a number of peer-reviewed and published papers

3. The certification by medical device manufacturers that our chemistry is compatible with their products. We enjoy official compatibility with the instrumentation of 56 medical device manufacturers, with respect to 1,449 of their individual models.”

Previously held 246 patents in 38 countries. Pretty sure management has confirmed the patent reduction is due to the culling of legacy products. But patents for the main products are expiring in the next few years.

Missing for 2022 is this 2021 text: “19 guidelines have been published by professional clinical bodies, infection prevention bodies, and national healthcare institutions that reference the use of chlorine dioxide recognisable as one of our products.”

Not sure why that text has been removed.

2021 text had “55 medical device manufacturers, with respect to 1,845 their individual models“, and the 396 reduction to the number of models to 1,449 again I hope is due to the culling of legacy products.

4) FINANCIAL REPORT

Various snippets of interest:

a) Employees

A breakdown of employee location:

“Our employees are distributed around the globe as follows: 123 in the United Kingdom (2021: 117); 38 in Europe (2021: 36); and 38 in the Asia and Pacific region (2021: 36). All manufacturing takes place in the United Kingdom together with central corporate functions such as Quality Assurance, Regulatory Affairs, Product Development and Research.”

Direct European revenue was £8.6m, so £228k per head. Direct APAC revenue was £6.3m, so £166k per head. Direct UK revenue was £13.6m, so £111k per head. All these numbers make sense, given UK operations include all the manufacturing, and European healthcare markets are more likely to accept higher price points than APAC.

b) Travel and marketing

Worth monitoring these costs as they have been subdued of late (and so help to prop up earnings) and may well re-emerge in the near future. Travel and marketing were £0.8m combined for 2022.

Travel costs were £0.3m versus £0.7m in mostly pre-pandemic FY 2020:

“The pandemic continued to curtail travel between our overseas offices and our manufacturing facility in the United Kingdom, and we cancelled international conferences. Travel costs remained low at £0.3m (£0.2m in the prior year).”

Marketing costs decreased by an undisclosed amount to £0.5m:

“Presenting our products at national and international medical conferences is our principal marketing activity and COVID-19 continued to result in the cancellation of most conferences during the year. Whilst we shifted our marketing activities to other promotional and communication channels as quickly as possible, marketing expenditure decreased during the year to £0.5m.”

c) Financial key performance indicators (KPIs)

No changes to the eight financial KPIs, which commendably include ROCE:

Thankfully no repeat of the five major QA non-conformances from 2021:

“During the year, the Group underwent three audits of the Quality Managements System and two desktop reviews of device technical files, and no major non-conformances were reported.”

d) Going concern

All new text for 2022 understandably referring to inflation, energy costs etc:

“The Directors have prepared cash-flow forecasts in order to assess going concern. The forecasts take account of potential and realistic changes in trading performance, and also include severe yet plausible downside scenarios. These scenarios include modelling reductions in revenue and margins and increasing costs and considering the consequent cash outflow that could result. The Directors have also considered the current economic environment, and in particular, recent movements in foreign exchange rates, rising energy costs and inflation in these scenarios. The forecasts indicate that, taking account of severe yet plausible downside scenarios, the Group and Company are able to operate within the level of existing cash resources, which at 30 September 2022 were £9.2m for the Group.”

e) Risks

Minor changes here.

Operations, legal and supply chain risks were unchanged. Brexit risk now removed. Covid-19 and health & safety risks have been watered down. IT risks now refers to “the increased level of home working“.

Financial risks remain credit and liquidity risks, cash flow risk and exchange-rate risk, all of which were unchanged from 2021 save for a new line about inflation:

“Rising inflation impacts the business’s ability to maintain profitability levels and stakeholder goodwill. Where cost increases cannot be absorbed via efficiencies and adaptations, customer price increases will be considered.”

4) DIRECTOR BIOGRAPHIES

Just minor changes here versus 2021.

The FD now adds “straightforward communication, enthusiasm” to her skills. Her bio has never said she qualified as an accountant, which does not mean she has not qualified, but tends to be part of a typical FD bio. For example, one of the non-exec’s bio starts with “Tom qualified as a chartered accountant…“.

Bart Leemans now “co-founded” Ecomed and various other ventures, rather than “founded” them. He is also confirmed as the MD of the Belgian and French subsidiaries.

5) DIRECTOR REMUNERATION

A few changes to the text here versus 2021.

Useful clarification of bonuses, with the “in proportion… ” condition added for 2022:

“The Executive Directors’ bonus scheme pays out if pre-tax profit exceeds the Company’s budget, in proportion to the budget overage.”

Bit sad that employees are no longer guaranteed to accumulate 40,000 options after 10 years, because this text from 2021…

“In addition, the Group encourages share ownership amongst all staff. All permanent staff no matter their pay scale or job, are awarded share option grants at set intervals which accumulate to 40,000 share options after 10 completed years of employment. Executive Management also has discretion to award market priced options after 10 years of employment up to a maximum value of 100% of salary.”

…was replaced by just this text for 2022:

“In addition, the Group encourages share ownership amongst all staff. Executive Management has discretion to award share options up to a maximum value of 100% of salary.”

An email address is now provided for remuneration comments:

“The Committee seeks and takes into consideration the views of shareholders on remuneration on an ongoing basis and they are invited to make contact directly with the Chairman of the Remuneration Committee at isabelnapper at tristel dotcom”

Some commendable pay restraint for 2022:

“In light of the disruption caused by COVID-19 upon the performance of the business, the Executive Directors again volunteered not to accept any increase in salary or salary benefits for the financial year 2022.

As stated above, an important part of the Group’s remuneration policy is the alignment of Executive Directors’ salaries with those at comparable AIM companies. With this factor in mind and given that the Executive Directors have not accepted salary increases for two consecutive years, the Remuneration Committee was keen to ensure that their salaries did not fall behind those of peers. In setting the salary award for 2023 the Committee therefore took into consideration a number of benchmarking surveys available from external organisations. Those surveys highlighted the fact that the Executive Directors’ pay had fallen below the comparable AIM median.

The Committee consequently recommended an increase for the financial year 2023. However, at their own behest the CEO and CFO volunteered to defer the implementation of the increase until the second half of the financial year. Their 2023 increase will therefore not take effect until 1st January 2023, unless it is established that the Group is performing in line with its agreed internal budget, in which case the deferred amount will be paid.”

Director pay not increased for 2022 after being held also for 2021. Pay rise for 2023 will not be decided until H2 as well. Therefore difficult to argue on the pay front:

Unchanged pay and no bonuses. Pension a chunky 15% of salary though.

The chief exec and FD historically have made their money through options, with their options at 700k and ordinary shares at 981k. The latest option batch looks set to expire worthless during the current FY 2024 (see blog post above), so I would not be surprised if another batch is proposed within the next year.

Bart Leemans has 100,000 options and 954k ordinary shares, the latter number remaining largely undisturbed since he sold Ecomed to TSTL during 2018.

6) CORPORATE GOVERNANCE

Lots of text changes here versus 2021.

a) Nominations committee

New committee work for 2022 included a board effectiveness review, setting objectives for the executives and enhanced board reporting:

“The key changes that have resulted from this review are:

* An update to this Corporate Governance Report

* Consideration by the Nominations Committee of the desired make-up of the Board of Directors, ensuring a strong mix of skills, knowledge, experience and diversity; alongside a review of the members of each committee to the Board and the level of independence held, the latter resulting in changes to the Committee memberships

* A Board effectiveness review and implementation of changes

* Setting of personal objectives for Executive Management

* An update to Board reporting enabling improved insight into the business activities

* A review and update to the Executive Management succession plan”

b) Business strategy

TSTL now claims to hold “the gold standard” for manual disinfection:

“Through technological innovation maintain our position as the gold standard manual process for High Level Decontamination of medical devices”

2021 text said the company was aiming “to be recognised as a gold standard”

Encouraging talk of a “protective moat“, too:

“The management team works closely with regulators, key opinion leaders and authors of clinical guidelines in all countries, seeking counsel and working in cohort when appropriate. Effective connections and relationships are a key element of the ‘protective moat’ referred to within the Company’s strategic plan.”

c) ESG matters

Revised text about ESG reporting:

“During the year a number of activities were undertaken in this regard:

* Engagement of a sustainability and ESG consultant starting in the 2022-23 nancial year. The multi-workstream project will examine our carbon emissions and develop an ESG strategy going forward. This will include:

* Internal and external stakeholder insights • Analysis of our operating environment

* Framework and target setting

Operational review

Determination of operational boundaries

Data collection and authentication

• Carbon footprint calculation

This investment in time and resource will set a strong ESG foundation for future success and enable sustainability to sit at the heart of the company’s activities. Initiatives will include:

• A second calculation of the Company’s carbon emissions

• Continued consideration of the carbon profile of our key products and research into alternative and environmentally friendlier packaging options for the Company’s products“

TSTL’s shareholder presentations now regularly refer to ESG matters, but the annual report does not yet disclose the group’s Scope 1-2-3 emissions and other environmental measures — which is bad form compared to the vast amounts of ESG commentary supplied by other AIM companies.

d) Independent non-execs

The board is no longer deemed majority independent:

“David Orr is not considered to be independent by virtue of his directorship and shareholding in Manor packaging, a supplier of cardboard to the Company. Tom Jenkins is no longer considered to be independent by virtue of his employer, the British Growth Fund’s shareholding in Tristel plc.

The Board no longer complies with the QCA Code’s requirement that at least half of the Board should be independent Non-Executive Directors. However, it is recognised that the non-independent Directors bring great specialist, analytical and entrepreneurial attributes to the Board, adding viewpoints and competencies that further enrich it.”

e) Board assessments

New text about board assessments:

“The performance of the Chair is assessed annually by the Senior Independent Non Executive Director. The performance of the CEO and CFO is assessed annually by the Chair. The performance of other Executive Directors is assessed annually by the CEO. And the performance of the Non-Executive Directors is assessed annually by the Chair.”

Chief exec and FD are married, so the FD’s performance review is rightly conducted by the chairman.

f) More business strategy

Not new text, but some background to customer behaviour:

“Infection prevention is a vital yet complex area of healthcare, and healthcare providers can be reluctant to change and put their trust in new products. The Board feels that if an honest and straightforward approach is taken, whilst supporting customers through the process of adopting new products, the Company can best achieve its goals.

g) Extra executive reporting

New for 2022:

“During the year the monthly KPI reporting expanded to include a number of additional measures, focussing upon operational performance, financial performance and Quality Management System adherence. Periodically, normally annually, a corporate risk register is presented to the Board and mitigating actions agreed.

h) Lack of audit committee report

No mention of the accounting U-turn instructed by the auditors for these FY 2022 results. Maybe the lack of a formal audit committee report is a sign the audit committee could improve its own effectiveness.

“The Company does not comply with the QCA’s requirement to publish a separate Audit Committee Report as it believes that the information provided within this Corporate Governance Report gives shareholders adequate information on the committee’s activities.

During the 2021-22 year the Audit Committee met on two occasions to:

• Discuss findings and hear recommendations arising from the annual audit

• Discuss with the Company’s external auditors matters such as compliance with accounting standards

• Monitor the external auditor’s compliance with relevant ethical and professional guidance on the rotation of audit partners, the level of fees paid by the Company and other related requirements

• Consider the performance and value for money of the Company’s external auditors

Approve the appointment of the Company’s external auditors, including their terms of engagement and fees.”

i) Nominations committee activity

Nominations committee has now agreed a CEO succession plan:

”During the year the significant actions arising from the Committee were:

* The QCA Mazars Board effectiveness questionnaire was utilised to perform a Board evaluation process and resulting actions were put in place

* Executive Management objectives were agreed and implemented

* Plans were put in place to enable the Non-Executive Directors to continue to improve their market awareness and knowledge

* It was recognised that Tom Jenkins should step down from his SINED role and be replaced by Isabel Napper, because of Tom’s loss of independent status, resulting from his employer, British Growth Fund, holding a substantial shareholding in the Company

* It was agreed that Caroline Stephens would replace Tom Jenkins as Audit Committee Chair

* A CEO succession plan was agreed”

The chief exec turns 66 during December 2023.

j) Minimum cash balance

This text from 2021 was missing for 2022:

“The Board is risk averse when investing any surplus cash funds. It considers that a minimum cash balance of £4 million is appropriate – providing adequate protection against unexpected events – for the current size of the business and seeks to adhere to this wherever possible and practicable. Cash exceeding this level, which cannot be used for earnings enhancing investment purposes, may be returned to shareholders in the form of a special dividend.”

Bit sad the board does not want to reiterate its risk-averse nature. I trust the text omission does not mean the board no longer has a minimum cash balance.

k) Meeting attendances

Board hosted 8 ordinary meetings, although oddly two of the executives were eligible to attend only 7:

Text says board held a total of 11 meetings, but other text says the audit committee held two meetings:

“During the 2021-22 year the Audit Committee met on two occasions to:”

So out of 11 total meetings, 8 were ordinary meetings and 2 were audit meetings, meaning either the remuneration or nomination committees did not meet at all. Unless of course the meeting numbers are wrong… I suspect the board held 7 standard meetings to allow one meeting each for remuneration and nomination.

7) DIRECTORS’ REPORT

A steep increase to the cost of D&O indemnity insurance:

“The Group provides Directors and Officers indemnity insurance for the benefit of the Directors of the Group. For the year to 30 June 2022 the policy cost £67,500 (2021: £9,100).”

Don’t know why. Maybe the prospect of trading within the United States?

8) INDEPENDENT AUDITOR’S REPORT

a) Materiality

Materiality very close to the standard 5% of profit before tax:

“£194,000 (2021: £265,000) 4.9% (2021: 5%) of normalised total profit before tax from continuing operations

b) Key audit matters

Remain the same: i) Revenue recognition and ii) recovery of parent company’s investments in Tristel Belgium/France/Netherlands/Italy

Added clarity for revenue recognition within the final two weeks of the FY:

“We consider the risk in relation to inclusion of revenue in the year ended 30 June 2022 rather than the year ending 30 June 2023 relates specifically to recognition for the 2 weeks before the year end.

Revenue is the most material balance in the financial statements and there is a risk that revenue may be overstated due to increased shareholder pressure to maintain EPS, share price and ensure dividends can continue to be distributed.”

Auditor now looking only at sales invoices before year-end and not either side“:

“We selected a sample of sales invoices before the year-end to assess whether revenue has been recognised in the correct financial period, by agreeing the date, amount, description and quantity to relevant documentation, such as delivery notes or other third-party acknowledgement of receipt”

Auditor now looking only at higher-risk parent-company investments:

“This key audit matter previously included all the parent company’s investments, however in the current year the risk has been isolated to those investments we consider are at the highest risk of impairment.”

Oddly, the 2021 number (£12,661k) is greater than the actual 2021 parent-company balance sheet number (£12,288k).

“Recoverability of parent company’s investments in Tristel Belgium, Tristel France, Tristel Netherlands and Tristel Italia srl, included within investments of £13.097 million (2021: £12.661 million)”

c) Scope

Scope is not ideal. Subsidiaries representing only a low-ish 82% of revenue and 85% of profit were subjected to full-scope audits:

I do wonder if some of the reporting niggles from TSTL is due to the group operating with 17 components, of which only 6 are subject to full scope audits and the rest, presumably all overseas, are subject to less investigation. The auditor’s report also included this new line:

“The scope of the audit work performed was predominately substantive as we placed limited reliance upon the Group’s internal control over financial reporting.

Auditor included a new reference to “cost inflation“:

“The risks that we considered most likely to adversely affect the Group’s and Company’s available financial resources over this period were lower than expected trading volumes and cost inflation.”

9) ACCOUNTING POLICIES

Useful life has been changed for acquired patents, trademarks and licences. Was between 10 and a ridiculous 35 years, but now between 7 and 20 years:

“Patents, trademarks and licences that are acquired by the Group are stated at cost less accumulated amortisation and impairment losses. Amortisation is charged over the useful life of the asset, on a straight-line basis of between seven and 20 years.”

Capitalised R&D still has a useful life of between 7 and 25 years:

“The amortisation of intangible assets is charged to administrative expenses in the income statement on a straight-line basis of between seven years and 25 years.”

25 years feels aggressive to me. The core wipes system has been around only for about 20 years.

Mind you, the intangible expenditure of late has been relatively small and have been offset by larger amortisation charges (see point 16).

10) REVENUE SEGMENT

Helpful note confirming UK revenue added for this year:

“Revenues derived from the UK (the largest CGU stated above) for 2022 were £13.610m (2021: £13.906m). Revenues from all overseas subsidiaries total £17.513m (2021: £17.092m.) ”

11) OPERATING COSTS

Two points from this note:

a) Cost of inventory expensed

£5,951k equivalent to 19% of revenue and within the 18%-21% range witnessed since 2017.

£5,951k equivalent to 1.37x average stock level, which is similar to the 1.59x and 1.28x of the previous two years, but is somewhat less than 2x seen during 2019 and earlier. I guess stock-piling to counter supply-chain issues or other pandemic-type disruption has had some impact here and caused the lower stock-turn and longer times in the warehouse. I should add stock control has rarely been a problem at TSTL (see point 18)

b) Research costs expensed

£614k for 2022. Such costs accelerated during 2017 from £251k to £665k, with the yearly average now c£700k as the 6-year total is almost £4.2m. Not quite sure what exactly this £4.2m has been spent on and may have to question what returns have been and/or will be achieved.

12) STAFF COSTS

Nothing too untoward here:

As mentioned in the blog post above, revenue per employee has declined during the pandemic disruption. Figure was £156k during 2022 versus £172k-£193k between 2016 and 2020.

Average staff wage was £50k during 2022, matching 2021. But longer-term trend is up. Was £31k back in 2012, before the group really expanded overseas with direct operations. Rising wage trend saw total staff cost take 37% of revenue during 2022, versus 38% during 2021 but less than 34% during 2020 and earlier. I am hopeful greater revenue post-pandemic can reduce the staff proportion back to 34% or less.

I note change to the numbers employed within different staff categories. The 2022 split was 41% marketing, 29% admin and 30% production. For 2012, the split was 38% marketing, 19% admin and 43% production. The production workforce therefore looks to have become more efficient, but that improvement has been counterbalanced by greater admin personnel.

13) AUDITOR’S REMUNERATION

£331k feels hefty for the audit fee:

Lots of overseas components and that accounting U-turn perhaps influenced the bill. In contrast, fellow portfolio member FW Thorpe paid £289k with 3x the revenue and 5-6x the adjusted profit of TSTL. Must one day study my portfolio’s auditor fees to see whether TSTL is paying over the odds.

14) PROPERTY, PLANT AND EQUIPMENT

TSTL has never operated with huge amounts of tangible fixed assets:

PPE of less than £3m is modest given revenue of £31m and an adjusted £5.5m operating profit. Depreciation broadly matches the additions each year, save for the occasional spend on ‘improvements to property’, which ought to have a useful life of a few years before further improvements are necessary.

15) GOODWILL

New for 2022 — a goodwill headroom table:

I interpret that table as i) book value of goodwill acquired within acquired entity, ii) book value of total assets within acquired entity (tangible and intangible), iii) TSTL’s own valuation of the acquired entity, and; iv) the ‘headroom’ difference between iii) and ii).

Headrooms have increased from 2021.

For Ashmed (Australia), the 2021 headroom was £4.5m:

“The net present value of future cash flows exceeds the carrying value of £1.18m by £4.49m, as such no impairment has been recorded.”

Ashmed’s 2022 headroom jumped to £8.5m:

“Cash flows over five years were considered and beyond this period cash flows were extrapolated using a terminal growth rate of 1%, which is prudent when compared to the compound annual growth rate in the global infection control market. Based on a revenue growth rate of 5%, the net present value of future cash flows exceeds the carrying value of £1.525m by £8.474m, as such no impairment has been recorded.”

TSTL has assumed Australian revenue will grow at 5% per annum. The same assumption was not disclosed for 2021.

For Belgium, France and the Netherlands, the 2021 headroom was £14.8m:

“The net present value of future cash flows for each cash-generating unit exceeds its carrying value (Group total of £6.18m), by £14.80m as such no impairment has been recorded.”

Their combined 2022 headroom advanced to £15.9m:

“Cash flows over five years were considered, for Tristel Belgium a revenue growth rate of 7%, for Tristel France a revenue growth rate of 10% and Tristel Netherlands a revenue growth rate of 7%. Beyond this period cash flows were extrapolated using a terminal growth rate of 1%, which is prudent when compared to the compound annual growth rate in the global infection control market. The net present value of future cash flows for each cash-generating unit exceeds its carrying value (Group total of £6.747m), by £15.898m as such no impairment has been recorded.”

TSTL has assumed Belgian, French and Dutch revenue will grow at 7-10% per annum. The same assumptions were not disclosed for 2021.

Note that Belgium and the Netherlands suffered revenue declines during 2022, which prompted management to consider at what point impairments would be necessary:

“Although significant headroom is shown in all three entities based on the above extrapolated cash flows, management has considered the sales decline shown in Belgium and Netherlands in the current year and sensitised the recoverable value calculation to show zero sales growth over the five-year period and an increasing cost base of between 4% and 7%, assuming all other assumptions remain unchanged. Under these conditions, the net present value of future cash flows for Belgium exceeds its carrying value of £3.773m, by £1.478m, the net present value of future cash flows for The Netherlands exceeds its carrying value of £0.739m, by £0.412m and as such no impairment has been recorded.

Management has further sensitised the growth rates, cost base and discount rate for Tristel Belgium and Tristel Netherlands. For an impairment to be recognised in Tristel Belgium, the revenue growth would need to be zero and the cost base increasing by 11% year-on-year or alternatively, the discount rate to increase to 27%. For an impairment to be recognised in Tristel Netherlands, the revenue growth would need to be zero and the cost base increasing by 12% year-on-year or alternatively, the discount rate to increase to 33%.”

For Italy, the 2021 headroom was £2.3m:

“The net present value of future cash flows exceeds the carrying value of £0.96m by £2.27m, as such no impairment has been recorded.”

Italy’s 2022 headroom jumped to £8.7m:

“Based on a revenue growth rate of 18%, the net present value of future cash flows exceeds the carrying value of £1.1m by £8.683m, as such no impairment has been recorded.”

Italy clearly looks the best acquired division with TSTL applying annual revenue growth of 18% within its impairment-test calculations.

16) INTANGIBLE ASSETS

Nothing amiss here: