28 January 2022

By Maynard Paton

Results summary for Tasty (TAST):

- A predictably poor performance due to the pandemic, albeit with revenue up 33% on the even worse H1 2020 following greater takeaway and delivery sales.

- Favourable changes to both the ‘going concern’ small-print and CVA commentary suggest the risk of failure has diminished.

- But underlying net cash of £4m does not leave enormous room for error given an estimated underlying cash outflow of £1m for this H1.

- IFRS 16 total lease obligations remaining at £55m looks odd given annual rents may have been reduced by 27%.

- A post-results update citing “extremely encouraging” trading plus plans to re-open the remaining closed restaurants provide hope of a recovery. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TAST

- Results summary

- Revenue and losses

- Revenue per restaurant

- Financials: going concern and cash flow

- Financials: landlords and leases

- Financials: cost analysis

- Immediate prospects and new menu

- Valuation

News links, share data and disclosure

News: Interim results for the 26 weeks to 27 June 2021 published 27 September 2021 and trading update published 04 January 2022

Price: 5p

Shares in issue: 141,089,758

Market capitalisation: £7.1m

Disclosure: Maynard owns shares in Tasty. This blog post contains SharePad affiliate links.

Why I own TAST

- Disastrous ‘legacy’ shareholding bought initially due to experienced family management building and selling two quoted restaurant chains for £200m-plus.

- Changes to the ‘going concern’ text, talk of “extremely encouraging” trading plus plans to re-open all closed outlets suggest the worst may now have passed.

- Bombed-out share price might provide substantial recovery upside… assuming sales can rebound to pre-pandemic levels and return the group to profit.

Further reading: My TAST Buy report | All my TAST posts | TAST website

Results summary

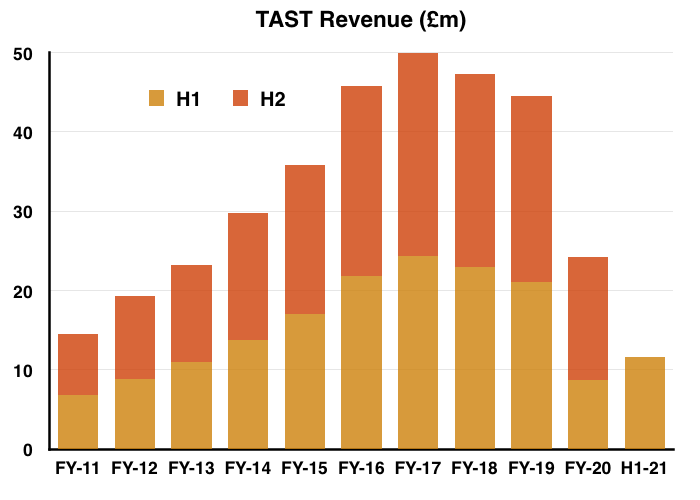

Revenue and losses

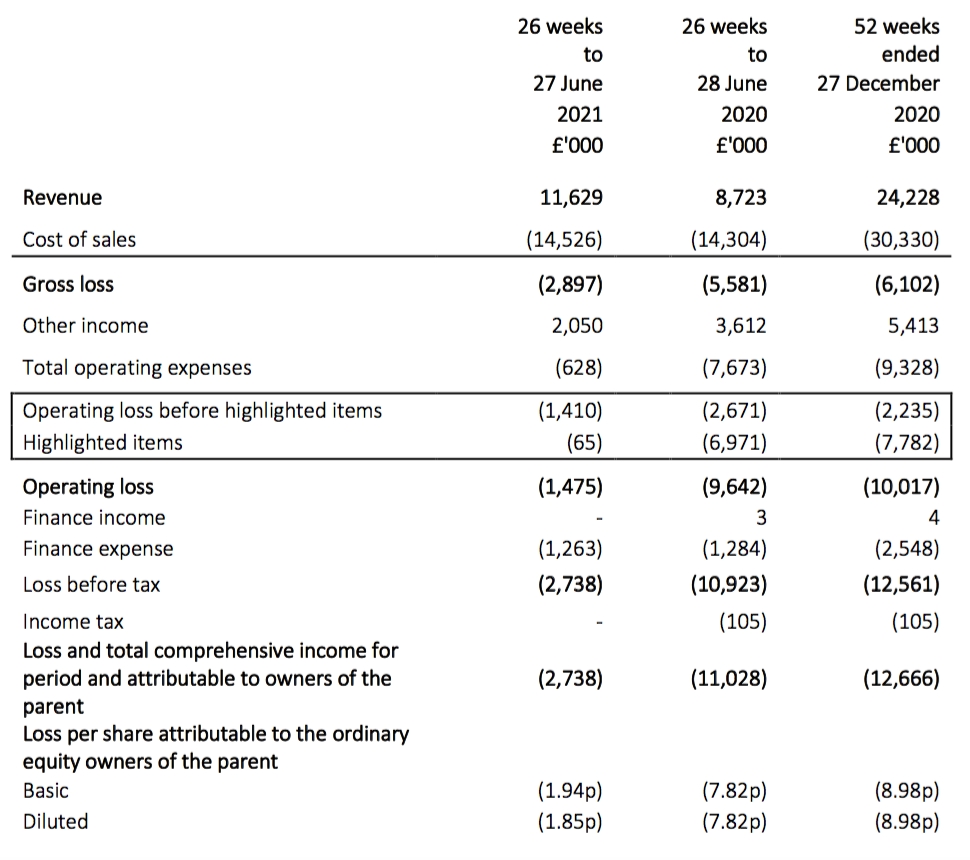

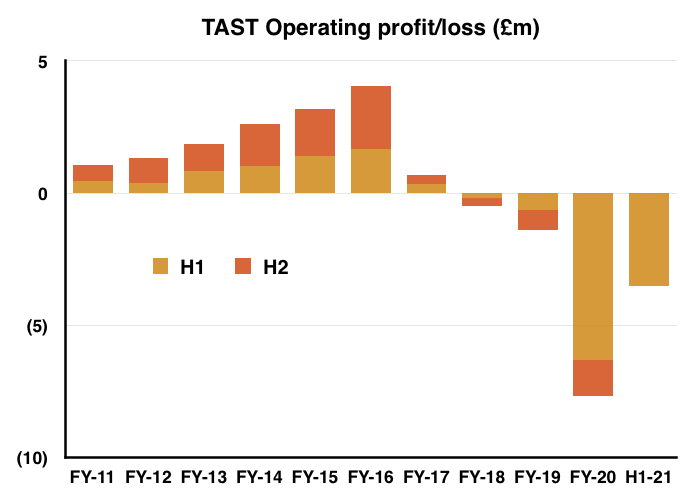

- Ongoing pandemic disruption ensured this H1 2021 performance would be poor.

- Revenue was 45% lower than the level reported during the pre-pandemic (and woeful) H1 2019. The operating loss would have been £3.4m were government support of £1.9m not received (and recognised):

- This H1 was not as bad as H1 2020. Revenue versus the comparable six months was 33% higher as TAST sold more meals through takeaways and deliveries:

“In H1 2021 even though the lockdown restrictions unexpectedly lasted longer than H1 2020, we were better positioned to take greater advantage of the takeaway and delivery market which has grown significantly throughout the pandemic and continues to remain strong after the re-opening of dine-in.“

- This H1 was not a good as H2 2020, with revenue 25% lower versus the preceding six months. H2 2020 was boosted by the government’s Eat Out To Help Out (EOTHO) scheme and then TAST’s own follow-up version.

- TAST’s reported profit for this H1 was thankfully not blighted by any further ‘highlighted’ items. Covid-related impairments of more than £11m were reported for FY 2020.

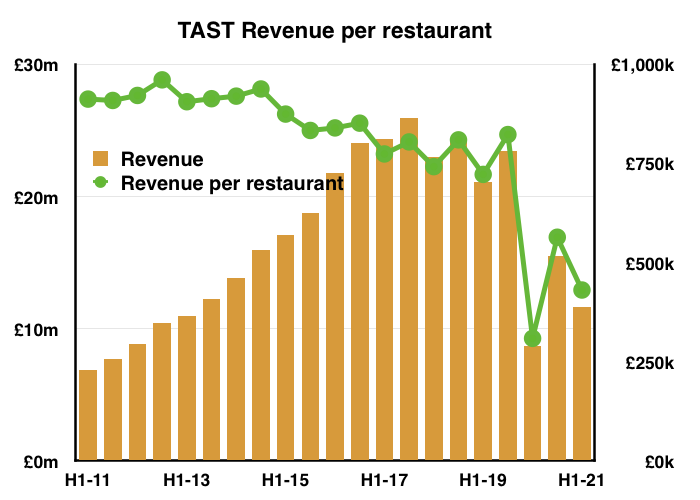

Revenue per restaurant

- TAST started and ended the half owning 54 restaurants. Annualised revenue per restaurant was £431k:

- But just 38 sites operated (on a takeaway/delivery-only basis) between January and April, while 49 operated (without any restriction) at the end of June.

- The average number of restaurants actually trading during the half could therefore have been (38+49)/2 = 43.5.

- Annualised revenue per that 43.5 average is £535k. My sums for FY 2020 on a similar restaurants-actually-trading basis came to £515k, suggesting this H1 was better than FY 2020 as a whole, but probably not as good as the preceding EOTHO-assisted H2.

Financials: going concern and cash flow

- My analysis of TAST’s financials continues to focus on whether the group can recover from the pandemic.

- The ‘going concern’ small-print looks to have improved.

- Such text noted a “material uncertainty” within the statements for H1 2020…

“However, the circumstances represent a material uncertainty which may cast significant doubt on the Group’s ability to continue as a going concern and, therefore, to continue realising their assets and discharging their liabilities in the normal course of business.“

- …and FY 2020:

“However, the combined circumstances and risk that the mitigating actions available to the Directors are not sufficient represent a material uncertainty which may cast significant doubt on the Group’s ability to continue as a going concern and, therefore, to continue realising their assets and discharging their liabilities in the normal course of business.“

- But the going-concern text for this H1 did not feature a “material uncertainty” and instead appeared reasonably normal:

“The Directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. In reaching this conclusion the Directors have considered the financial position of the Group, together with its forecasts for the next 12 months from the date of approval of these interim accounts and taking into account possible changes in trading performance should Government restrictions be reintroduced. The Group monitors cash balances closely to ensure there is sufficient liquidity. Accordingly, the Directors believe that it remains appropriate to prepare the financial statements on a going concern basis.“

- Talk of a Creditors Voluntary Arrangement (CVA) seems to have moderated, too.

- The FY 2020 statement implied a CVA remained an option:

“With the progress made on consensual negotiations with landlords and other creditors, the Group has to date managed to prevent a CVA. However, with dine-in restrictions in place until May 2021, there is additional pressure on cash reserves. The Board will continue to explore all options but are hopeful that with continued creditor assistance, a more formal procedure may be avoidable.“

- But this H1 statement did not imply a CVA was an option, and instead said one had been avoided:

“With the support of the majority of our landlords we have managed to avoid a Creditors Voluntary Arrangement (CVA) within the Group. However, with the potential of rising infections as we head into the colder months, we will continue to monitor the situation closely in the coming months.“

- The welcome receipt of a £1.3m bank loan from Barclays supported an overall cash inflow of £1.9m.

- Adjust for the Barclays cash injection and TAST’s cash inflow was £0.6m. Then subtracting recognised furlough income of £1.9m gave a £1.3m outflow.

- The £1.3m outflow was influenced by TAST paying off “aged creditors“.

- This H1 statement said:

“Overall, the net cash inflow for the period was £1.8m (2020: outflow £1.4m). As at 27 June 2021, the Group had net cash after bank loan of £8.6m (28 June 2020: net cash of £3.2m). After allowing for aged creditors net cash was £4.2m (28 June 2020: net debt of £0.4m).“

- Aged creditors were therefore £8.6m less £4.2m = £4.4m.

- The preceding FY 2020 said:

“Net cash before outstanding bank loan at the balance sheet date was £8.0m (2019 – net cash £2.9m)… The cash balance at year-end reflects our cash preservation strategy and deferring payments due to landlords, HMRC, and other trade creditors. After reflecting these outstanding payments, our net cash at year-end is approximately £1.5m.”

- Deferred payments due to landlords, HMRC and other trade creditors for FY 2020 were therefore £8.0m less £1.5m = £6.5m.

- Assuming the aged creditors for this H1 and deferred payments for the preceding FY 2020 both cover the same overdue bills, TAST looks to have paid £2.1m during this H1 to clear some of those very old invoices.

- The results small-print also revealed TAST collecting further government money of £1.8m that was not recognised as income:

“Other income includes Government Coronavirus Job Retention Scheme (“CJRS”) (£1.9m) and sub-let property income (£0.1m). The Group has also received £1.8m of Government Grants which at the present time have not been recognised in other income while Group assesses when the recognition conditions are met in full.”

- I think(!) all this means that cash flow before the Barclays loan (£1.3m), recognised furlough (£1.9m), aged creditors (£2.1m) and unrecognised grants (£1.8m) was £1.9m less £1.3m less £1.9m plus £2.1m less £1.8m = a £1m outflow.

- A £1m outflow does not feel too horrendous for this H1 given TAST spent three months selling meals only via takeaway and delivery. But net cash of £4.2m (after aged creditors) does not leave enormous room for error if cash flow remains negative.

Financials: landlords and leases

- This H1 statement gave a short update on rent negotiations:

“The Group has been successful in achieving rent reductions and lease concessions across most of the estate. Landlords have, in the main, been extremely understanding and supportive.“

- The use of the past tense suggests these negotiations have now been completed.

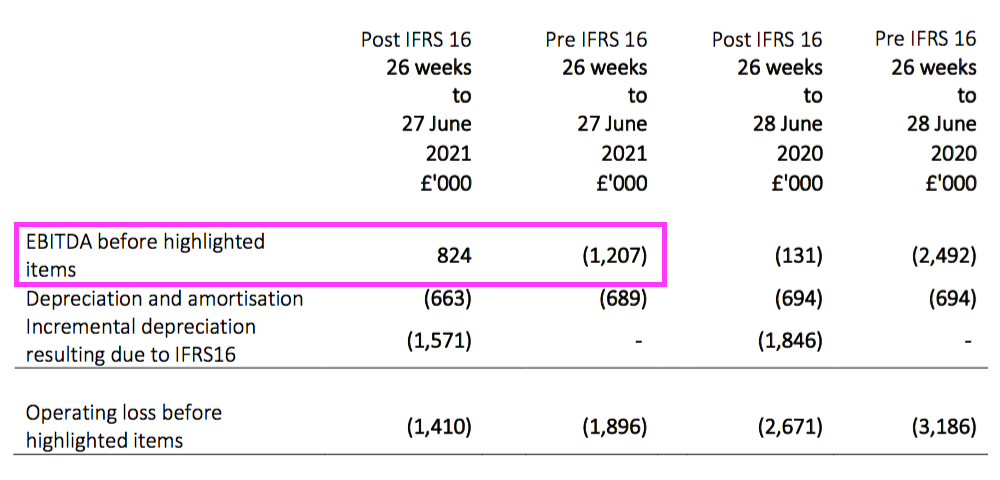

- TAST commendably published pre- and post-IFRS 16 versions of the headline performance, from which lease costs could be deduced:

- The £2.0m difference between the Ebitda numbers represents the pre-IFRS 16 lease cost that, post-IFRS 16, is now reflected within the depreciation expense and financing charge.

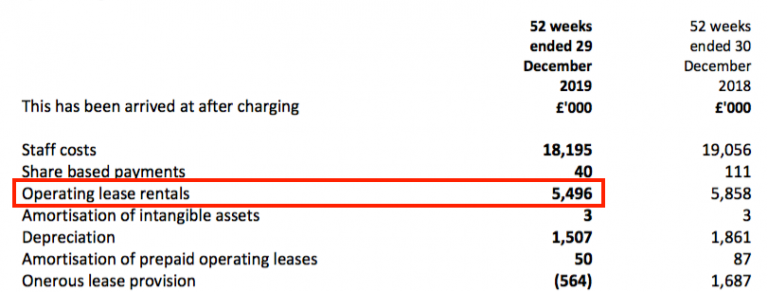

- Annualising the £2m difference gives £4m, and compares to the pre-IFRS 16 lease cost of £5.5m for FY 2019:

- £4m versus £5.5m implies rent costs being cut by 27%.

- Cash lease payments were £1.5m during this H1, which annualised gives £3m and is £1m less than the £4m pre-IFRS 16 lease cost calculated above.

- I am not sure why the cash lease expense is less than my calculated pre-IFRS 16 accounting expense. But this mismatch is better than the cash expense being greater than the accounting expense.

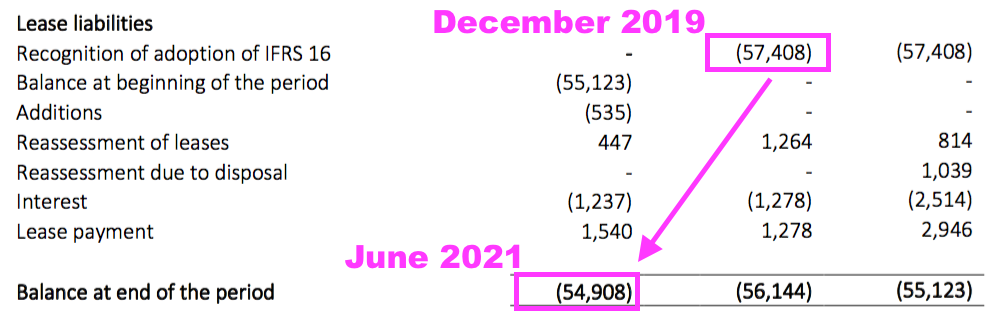

- Total lease obligations remain £55m on a net present value basis:

- But total lease obligations at the end of FY 2019 — i.e. 18 months beforehand — were £57m on a net present value basis:

- Total lease obligations reducing by just £2m to £55m during a period when TAST was busy negotiating lower rents does not feel quite right.

- Possible explanations for this small, £2m reduction include:

- The lower rents are temporary;

- My 27% reduction calculation is wrong, and;

- I have misunderstood IFRS 16.

- TAST’s total lease obligations staying close to £55m requires further investigation and I trust the upcoming FY 2021 results will shed further light on this matter.

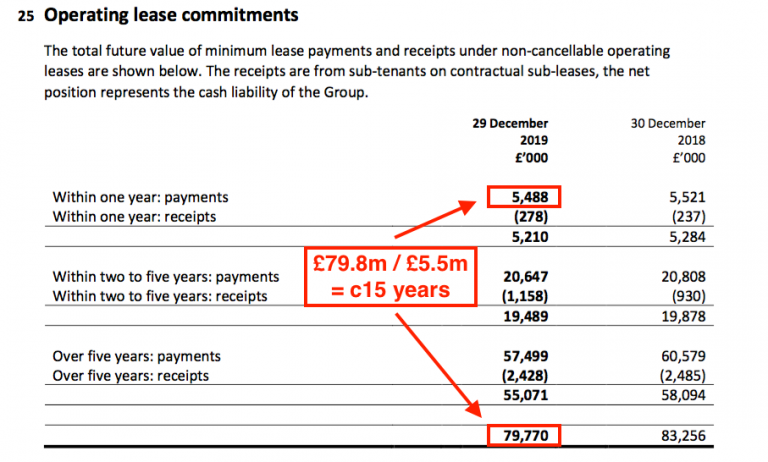

- The accompanying right-of-use lease asset was £38m, which arguably suggests TAST would pay £17m (£55m minus £38m) less to rent its properties were it to commence the same leases today.

- The (pre-IFRS 16) FY 2019 figures suggested TAST’s leases ran for an average of approximately 15 years:

Financials: cost analysis

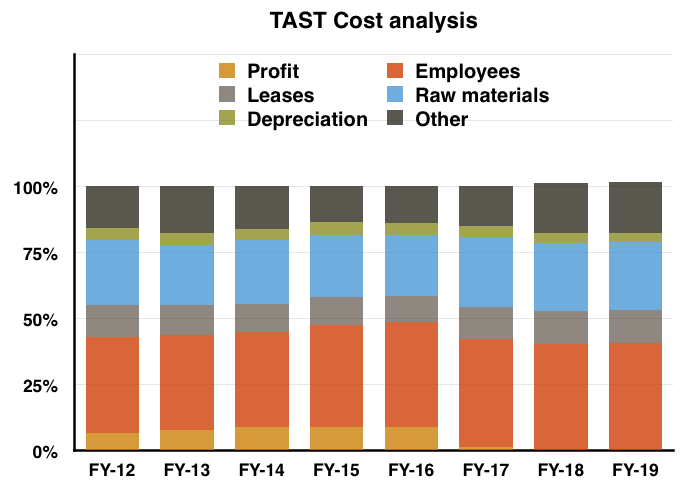

- TAST has in the past kept lease costs under control.

- Lease costs stayed between 10% and 12% of revenue between FY 2012 and FY 2019:

- In contrast, Employee costs increased from 36% to 41% while Other costs increased from 16% to 19%.

- The increases to Employee and Other costs took an extra 8% of revenue that squeezed TAST’s 7% margin for FY 2012 to less than zero for FY 2019.

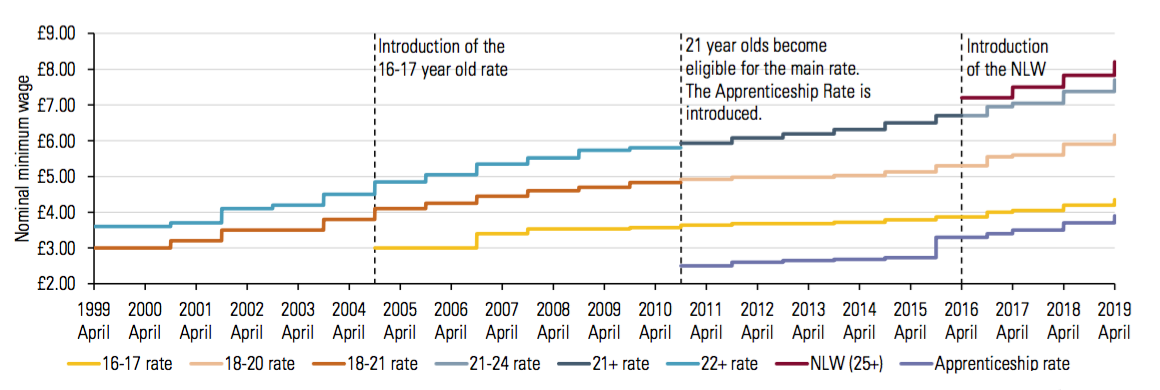

- TAST’s employs mostly lower-paid staff, and past increases to the minimum wage and the introduction of the national living wage would therefore appear the likely causes of Employee costs out-pacing revenue:

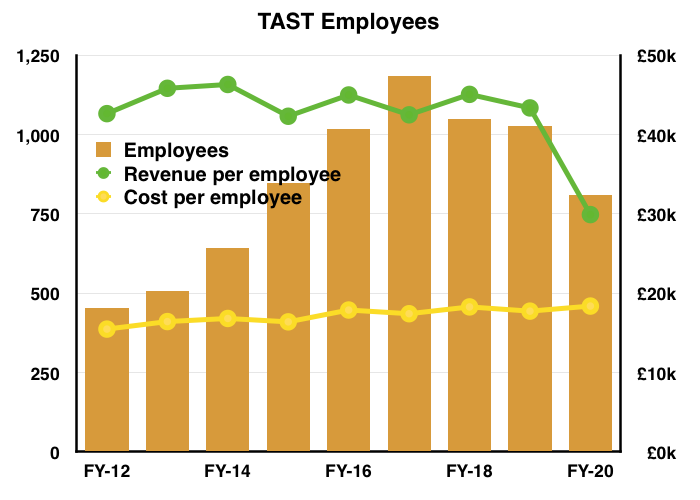

- TAST’s revenue per employee has bobbed between £42k and £46k a year since FY 2012:

- But the annual cost per employee has increased from £15k to £18k during the same time.

- The upshot is TAST failed to enjoy productivity improvements (i.e. greater sales) from employees in exchange for paying higher wages.

- My hope is TAST’s greater revenue from takeaways and deliveries can enhance the employee economics at the group’s restaurants.

- For perspective, Restaurant Group (RTN) says takeaways and deliveries have grown to represent 16% of sales at its ‘Leisure’ brands (mostly Franky & Benny’s and Chiquito):

Immediate prospects and new menu

- TAST’s remarks about early H2 trading were positive:

“Trading since re-opening for dine-in in May 2021 has been encouraging and exceeded the Board’s expectations.”

- The group was also confident enough to use the words “viable” and “growth“:

“[W]e now have a viable platform on which to build a successful business…“

“Despite [the pandemic] uncertainties the Board remains optimistic as to the outlook for the Group and expects to keep under review future opportunities for growth.“

- But TAST did admit that early H2 trading had been assisted by “VAT and rate support, staycations, pent-up demand and a higher level of disposable income“.

- A statement earlier this month confirmed good trading between July and November:

“Trading across the Group for the second half of the year up until December 2021 was extremely encouraging.“

- But further Covid restrictions led to a difficult December:

“The rising infection rates of the latest Omicron Covid-19 variant and in particular the reinstatement of working from home advice by the UK Government, significantly reduced the number of customers eating out and specifically deterred the larger Christmas bookings. As a consequence, trading for the peak December trading period was considerably weaker than anticipated.“

- At least festive customers included my son and his housemates at TAST’s York restaurant. They ordered three-course Christmas meals for £19.95 a pop:

- Due in March or April, the FY 2021 results should outline the impact of December’s weak performance on the overall H2 effort.

- The FY 2021 results should also provide a comment on Q1 2022 trading, which will be supported by a revised menu:

- The revised menu has introduced various new dishes, but remains based on a broad mix of pizzas, pastas and burgers.

- The pandemic could have been an opportunity for a radical menu overhaul.

- After all, a broad mix of pizza, pastas and burgers did not attract hoards of diners during the difficult (pre-pandemic) FYs of 2018 and 2019.

- The aforementioned “extremely encouraging” trading cited within this month’s update nonetheless gives hope that TAST’s pizzas, pastas and burgers have regained some popularity.

- Maybe pizzas, pastas and burgers are very suitable for takeaways and deliveries. The latest update described takeaways and deliveries as a “strong revenue stream“.

- The following 15 dishes featured on the November 2019 menu and remain on the latest menu:

- Starters:

- Baked mushrooms: were £5.95 now £6.40

- Garlic tiger prawns: were £7.25 now £7.75

- Calamari: was £6.95 now £7.15

- Pizza:

- Margherita: was £8.95 now £9.10

- Double pepperoni: was £10.95 now £11.25

- Hoi Sin duck: was £11.25 now £12.20

- Pasta:

- Traditional bolognese: still £10.75

- Oven-baked lasagne: was £11.65 now £12.15

- Peri-peri chicken penne: was £11.95 now £12.25

- Grill:

- Buttermilk chicken burger: was £11.55 now £12.35

- 10oz sirloin steak: was £17.95 now £18.95

- Classic cheeseburger: was £11.75 now £12.35

- Other:

- Seafood risotto: was £12.95 now £13.45

- Cobb salad: was £11.75 now £12.95

- Fries: still £3.95

- Price increases during the two intervening years range from 0% to 10% and average 5%.

- TAST’s January update said 50 out of the group’s 54 sites were open, although encouragingly the four closed outlets “should re-open later in the year“.

- Operating all 54 restaurants would suggest TAST is confident each outlet has the prospect of profitability (or at least not heavy losses).

Valuation

- 54 restaurants operating normally and returning to FY 2018/2019 sales of £750k each would generate group revenue of £40m.

- Revenue of £40m does not require a huge operating margin to leave a profit that would make the £7m market cap appear remarkably cheap.

- A margin of 3.5% on £40m for example leads to a £1.4m operating profit and a mid-single-digit P/E.

- You never know, lower rents, “reduced competition” and the potential for fewer problem sites could one day generate a 3.5% margin.

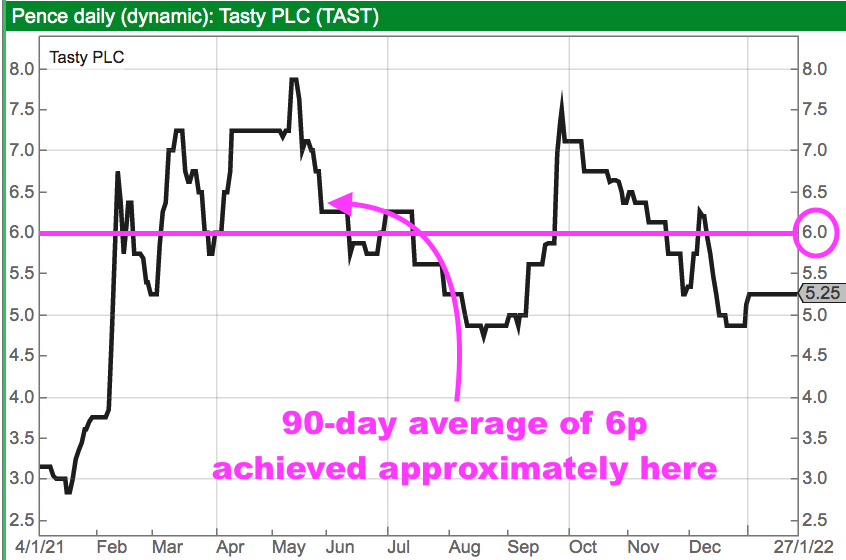

- Options awarded to the chief exec at the start of FY 2021 reveal what the board thinks could be possible with the share price.

- The scheme pays out:

- 3.3% of the current share count if the share price has traded at a 90-day average of 6p by the start of FY 2022;

- 6.7% of the current share count if the share price has traded at a 90-day average of 8p by the start of FY 2023, and;

- 10% of the current share count if the share price has traded at a 90-day average of 16p by the start of FY 2025.

- While the 16p target is tantalising given the 5p share price, do note the total option payout is limited to 10% of the share count.

- This 10% dilution limit means the 16p target becomes redundant if the 6p and 8p targets are met beforehand.

- I calculate the share price traded at a 90-day average of 6p during FY 2021 and therefore the chief exec is now entitled to options representing 3.3% of the share count:

- Should the shares trade at a 90-day average of 8p during the next year or so, the scheme payout will reach the maximum 10% and the chief exec may no longer strive for the 16p target.

- The shares reaching 8p from 5p gives a 60% gain.

- The shares reaching 16p from 5p gives a 220% gain, albeit spread over the remaining three years of the option scheme’s life.

- I would prefer the shares to advance 220% to 16p over three years, rather than climb 60% to 8p within one year and possibly stagnate thereafter.

- But I would also prefer the shares to climb 60% to 8p within one year rather than never advance 220% to 16p.

- The 8p option target will have been reached or missed by this time next year. At that point shareholders will have a better view on whether the chief exec could still be aiming for the 16p.

- Fingers crossed, by this time next year TAST may be operating with all 54 restaurants trading normally and the prospect perhaps of the group breaking even or recording some sort of profit.

- For the time being I am minded to retain my TAST shares because the worst now seems to have passed.

- Management’s commentary appears to have turned from ‘survival’ to ‘recovery’, and even claimed trading was “extremely encouraging” before the December disruption. The possible upside from 5p could be significant if a full recovery is ever achieved.

- But the longer-term economics of TAST’s restaurants remain very unclear, and the group is never likely to enjoy an obvious niche with its middle-of-the-road menu.

- I am therefore hoping one day for a suitable exit rather than opportunities to buy more.

- I also recognise the time dedicated to TAST could be better spent on portfolio holdings in which I have a greater conviction to buy if the price was right.

Maynard Paton

Tasty (TAST)

Trading update published 08 March 2022

A promising update. Here is the full text interspersed with my comments:

——————————————————————————————————————

Tasty (AIM: TAST), the owner and operator of restaurants in the casual dining sector, announces the following unaudited trading update for the 52 week period ended 26 December 2021.

* Revenue of £34.9m (2020: £24.2m), an increase of 44% year-on-year with 33 weeks dine-in trading, driven by strong sales post re-opening despite weaker trading for the peak December period than anticipated, due to the onset of the Omicron variant

* 2021 revenue represented 78% of the Company’s 2019 revenues of £44.6m despite fewer operating sites

* Adjusted EBITDA(1) is expected to be approximately £8.0m (2020: £2.7m)

* Pre IFRS 16 adjusted EBITDA(1) is expected to be approximately £3.9m (2020: £1.5m loss)

* Cash at the year-end was £11.0m. After allowing for deferred HMRC payments, creditors and bank loan our net cash position was approximately £6.8m

Tasty is now trading out of 50 venues, with four restaurants currently closed but at different stages of re-opening planning. There are still ongoing negotiations to dispose of, or re-gear, two or three of the restaurant leases within the Group.

(1) Adjusted for depreciation, amortisation and highlighted items including share-based payments and impairments. Note the adjusted EBITDA figure includes £1.9m of exceptional Government grant income.

——————————————————————————————————————

Full-year revenue at £34.9m means H2 revenue of £23.3m — and on a par with pre-pandemic H2 2019 (£23.4m) and not far from the record H2 of 2017 (£25.9m). Bear in mind TAST suffered during December (peak trading month) because of the Omicron Covid outbreak, so H2 2021 could have actually been a record H2 for revenue.

Taking the 54 total restaurants, sales per restaurant were an impressive £862k during H2 — better than the £833k, £851k, £804k, £809k and £823k seen during the H2s between 2015 and 2019. Using the 50 open restaurants, H2 sales per restaurant reached £931k and at a level seen back in TAST’s 2013/2014 heyday.

Adjusted Ebitda looks to have been £7.2m for H2 versus £0.8m for H1, while pre-IFRS 16 adjusted Ebitda looks to have been £5.1m for H2 versus (£1.2m) for H1. So a decent profit for this bumper H2. The difference between the two adjusted Ebitda numbers is £4.1m, which confirms my calculations in the blog post above about lease charges now running at £4m per annum.

Year-end cash of £11m means the the cash position improved by £1.1m during H2. Net cash after debt (presumably still £1.25m) and aged creditors of £6.8m means aged creditors are £2.95m. Aged creditors at the H1 stage were £4.4m, so £1.5m was spent paying off HMRC etc during H2.

Government grants of £1.9m equals what was recognised during H1, and so means nothing was claimed during H2.

——————————————————————————————————————

Since re-opening for dine-in in May 2021, the Group was EBITDA positive and cash generative for the remainder of 2021. The strong trading post full re-opening of the estate up until the outbreak of Omicron in late November 2021 was encouraging, however, this has been tempered by the challenges which the Company expects as a result of the end of Government support including VAT and business rates.

There is also an expectation of a reduction in pent-up demand, disposable income and staycations as well as a steep rise in inflation in relation to wages, utilities and input supplier costs as the UK adjusts to Brexit, the aftermath of the pandemic and the current war in Ukraine.

——————————————————————————————————————

Ok, so TAST is hinting the bumper H2 may not be repeated for 2022. Reduced lease expenditure may just be eaten up by greater wage, utility and ingredient costs. Note that TAST was barely profitable during FYs 2018 and 2019, so what is important is whether the economics of the restaurants have fundamentally improved post-pandemic. The company refers to delivery and takeaways below, which I am hopeful can enhance staff productivity and the returns from each outlet.

——————————————————————————————————————

Well publicised industry employee shortages and supply issues are being managed and will continue to be a focus for the Company. During the last twelve months, the Company has invested in refreshing some of the older sites and increasing and renewing the outside seating across the estate, and this programme will continue throughout this year.

In addition, there has been a recruitment drive to strengthen the head office team and operational structure. This increase in head count will facilitate a measured expansion plan for a pipeline of five to six new units this year and a refocus on takeaway and delivery which, following the lifting of Covid restrictions, due to employee shortages has once again become secondary to the dine-in trade.——————————————————————————————————————

Revamping old sites, recruiting more people and — most notably of all — looking at opening five or six new outlets suggests TAST is confident about the future. Net cash of £6.8m following a net cash inflow of £2.5m for H2 (before paying aged creditors) looks a good base (relatively speaking) to face any economic difficulties during FY 2022.

Maynard

Thank you for your analysis Maynard, we’ll keep our shares too.

Thanks Vic!