01 October 2019

By Maynard Paton

Happy Tuesday! I hope you continue to find my Blog useful… and that your shares are coping well in the current market.

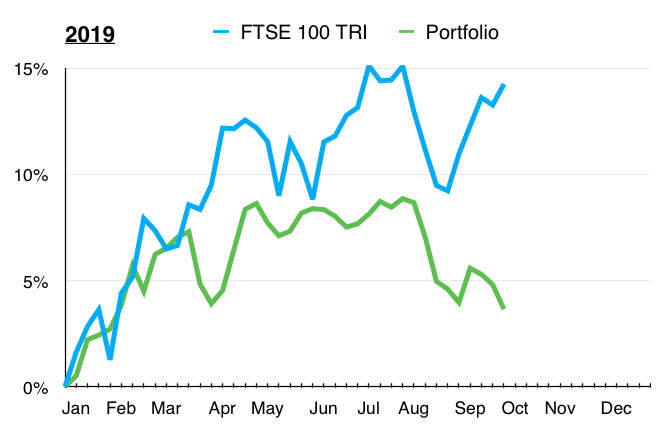

My portfolio continues to lag the FTSE 100. Since the start of the year, I am up a measly 3.6% while the index with dividends reinvested is up 14.3%.

I remain on the wrong side of what has become a two-tier market. While global ‘quality’ large-caps continue to charge higher, my portfolio is still full of smaller UK companies…

…many of which are undergoing potential recoveries (e.g. Getech, Tasty), experiencing standstill earnings (e.g. FW Thorpe, M Winkworth) or operating in an unloved sector (e.g. Daejan, Mountview Estates).

I am sure a broad earnings improvement throughout my portfolio ought to revive some very stagnant share prices. In the meantime, I remain convinced that investing in respectable businesses that offer modest valuations, decent accounts and capable managers is a sensible investing approach.

Let me now explain what has happened within my portfolio during July, August and September. (Please click here to read all of my previous quarterly round-ups)

Contents

Q3 share trade

I increased my Daejan holding by 20% at £51 including all costs. The commercial-property group revealed in July that its net asset value (NAV) had advanced to £119 per share, and yet the share price continues to drift lower (probably due to wider sector worries — my study of Hammerson revealed severe difficulties within retail property). Daejan’s price to NAV has dropped to 42% and such a valuation has typically rewarded (very) patient investors.

Q3 portfolio news

As usual I have kept an eye on all of my existing holdings. The Q3 developments are summarised below:

- Acceptable statements from City of London Investment and S&U;

- Subdued progress at FW Thorpe and M Winkworth;

- Mixed updates from Andrews Sykes and Mincon;

- Nothing from Bioventix, Mountview Estates, Oleeo and System1.

During the quarter I attended three AGMs and one company presentation. A few interesting snippets emerged:

- System1’s new AdRatings service did not entice new clients because the subscription fee was “too cheap” (read AGM report).

- Mountview Estates purchases regulated-tenancy properties at a 25% discount to their fair market value and has “enough business out there for another 15 to 20 years” (read AGM report).

- Daejan is deliberately shifting its focus towards the United States as the country offers “more opportunities and less regulation” than the UK (read AGM report).

- Tristel currently sells a new surface disinfectant in 25 UK hospitals and reckons France could become a very significant market (read presentation report).

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Q3 portfolio returns

The chart below compares my portfolio’s weekly 2019 progress (in green) to that of the FTSE 100 total return index (in blue):

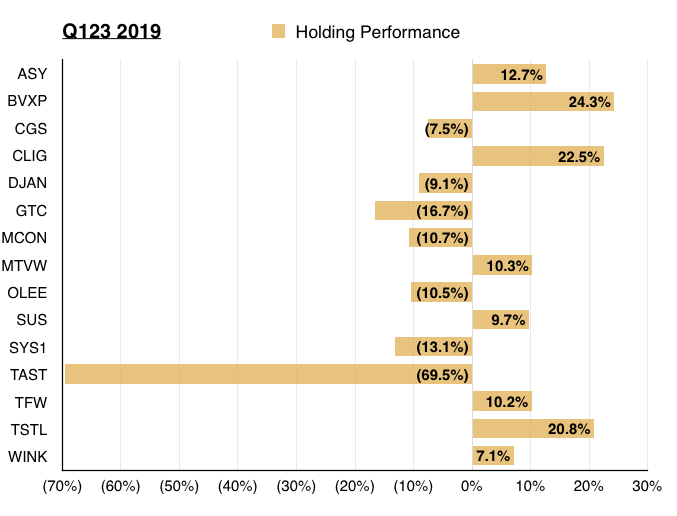

This next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me year to date:

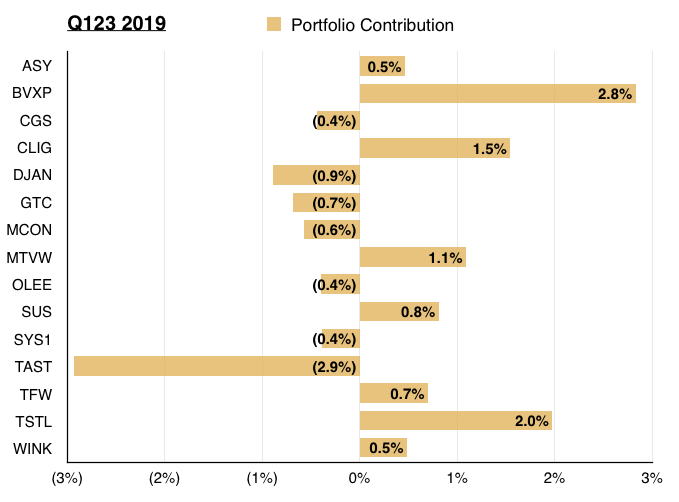

Meanwhile, this chart shows each holding’s contribution towards my overall 3.6% gain:

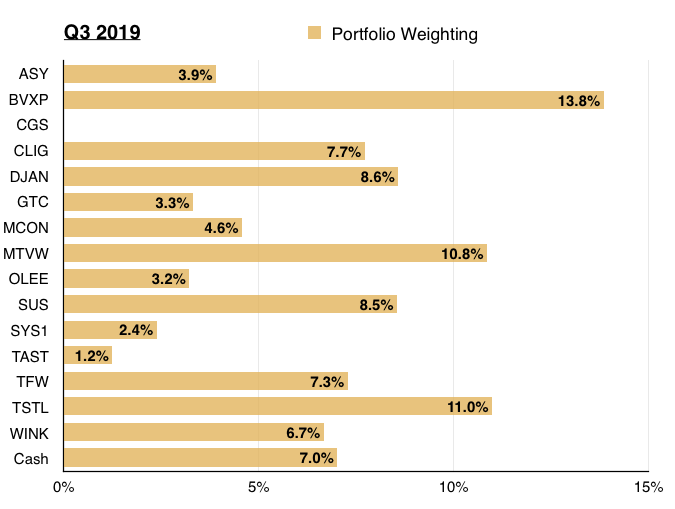

And this chart shows my portfolio’s holdings and their weightings at the end of Q3:

Obscure but important annual-report small-print

I am convinced reading annual reports can give you a stock-market advantage. You can find all sorts of obscure — but important— small-print that most other investors will skim over…

…assuming they read the reports in the first place!

Here are three examples of obscure small-print that you may wish to double-check when reading your next annual report.

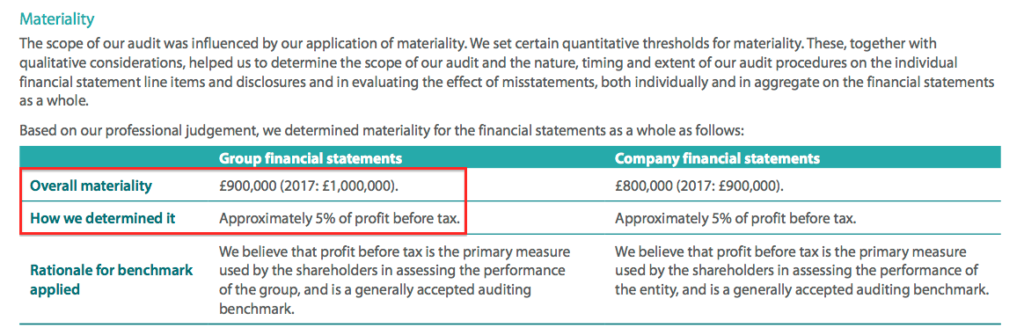

1) Audit materiality

Every annual report includes an audit report. Typically full of ‘boilerplate’ text, the audit report ought to include ‘materiality’ thresholds.

(According to the International Standards of Auditing (UK), information is considered to be ‘material’ if “its misstatement or omission individually or in aggregate could influence the economic decisions of users on the basis of the financial information provided”.)

The FW Thorpe annual report provides an example of materiality thresholds:

The overall materiality threshold for Thorpe was set at 5% of pre-tax profit — a level that has become an informal standard for quoted companies.

(Nine of my 14 shares have 5% profit materiality thresholds, with the others having thresholds based on c1% of revenue (because their profits are very low or non-existent) or c1% of gross assets (because they are property companies).)

Materiality thresholds should be checked because the higher they are, the greater the suspicion the auditor may not dig as deep to unearth ‘material’ misstatements — which perhaps has implications for the accuracy of the accounts.

For example, Keywords Studios has an overall materiality threshold of 10% of pre-tax profit:

A good question for the next Keywords AGM would be why the directors and/or the auditor — BDO Dublin — determined 10% was suitable when the level at most other companies is 5%.

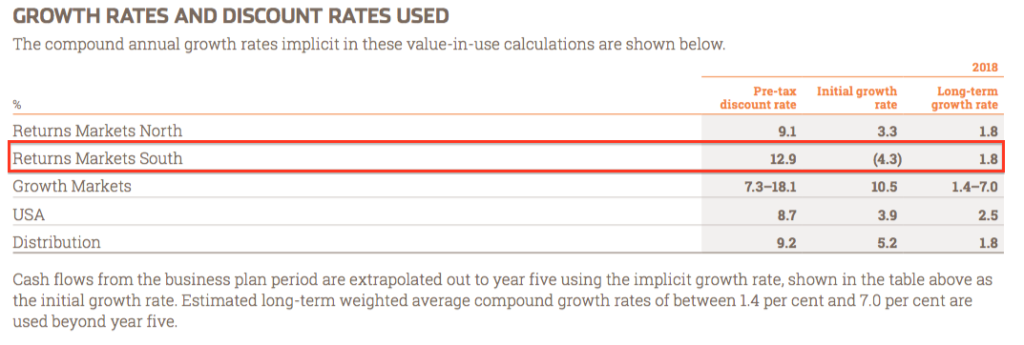

2) Goodwill projections

The accounting note covering goodwill can provide clues about a company’s future prospects — and whether the directors are being too ambitious.

(Goodwill is created when one business acquires another, is typically calculated as the difference between the purchase price and net tangible assets, and is recorded as an intangible asset.)

Companies must ‘test’ their goodwill every year to ensure the associated accounting value remains valid, and the assumptions used in these tests should be published. The following table comes from Imperial Brands:

You can see that goodwill relating to four of Imperial’s five divisions have initial growth rates greater than their respective long-term growth rates. Those differing projections make sense, as near-term growth is more likely to be greater than long-term growth as the wider business matures.

However, the odd division out — Returns Markets South — has an initial growth rate of negative 4.3%… and yet Imperial reckons the division’s long-term growth rate is a positive 1.8%.

Imperial essentially reckons the cash flows from Returns Markets South will reduce by 4.3% a year for the next five years… but suddenly grow by 1.8% a year thereafter.

The previous four annual reports show initial growth rates for Returns Markets South to be -2.1%, -0.1%, -0.8% and -2.2%.

Despite the consistently negative short-term projections, the long-term growth rate for Returns Markets South has — very oddly — always been a positive 1.8%.

I dare say the board’s £1.7 billion valuation of the Returns Markets South goodwill could be too optimistic.

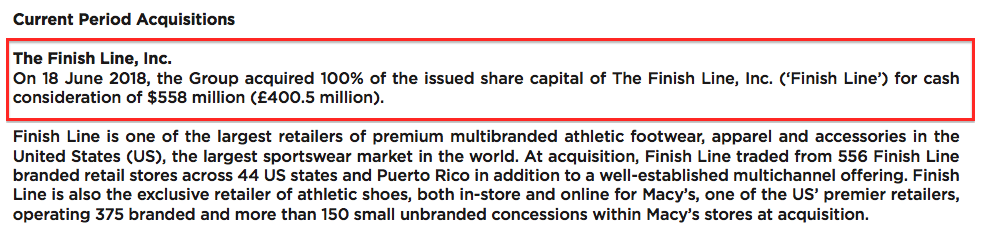

3) Acquisition details

The accounting note covering acquisitions offers useful small-print to examine the financial effect of the purchase.

In particular, companies ought to declare the additional revenue and profit derived from the acquisition, and the level of revenue and profit that would have occurred had the acquisition taken place at the start of the financial year.

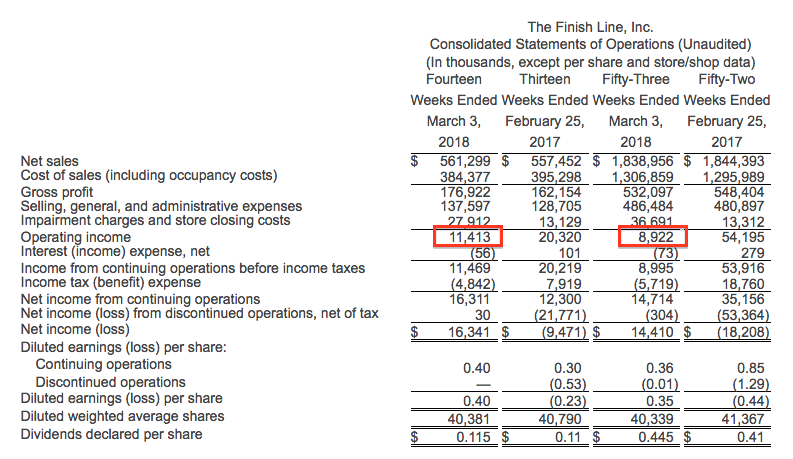

JD Sports Fashion provides a good example. The sports retailer purchased The Finish Line for £401m during 2018:

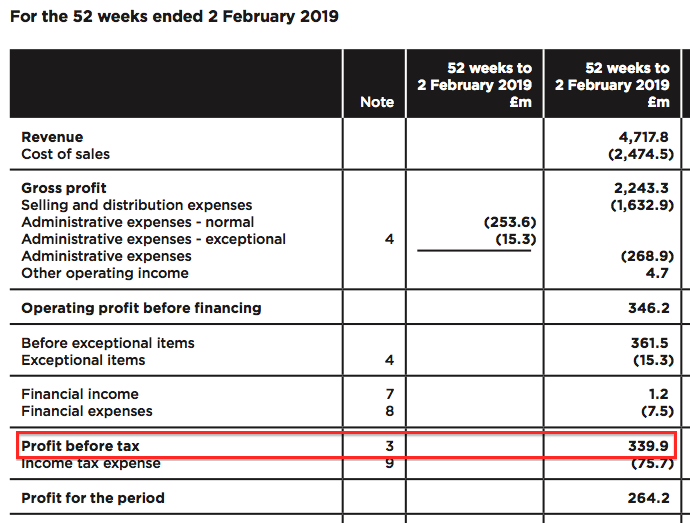

Here is The Finish Line’s financial contribution:

And here is what JD would have reported had The Finish Line been owned for the full year:

That £318.8m profit before tax figure is interesting because JD actually reported £339.9m:

How can an acquisition contribute less profit during a full year than during part of the year? Answer: when the acquisition is a retailer that makes the bulk of its money at Christmas.

You can see from The Finish Line’s results prior to the acquisition that December, January and February witnessed a greater profit than the full year:

The upshot is The Finish Line would have contributed only an extra £3.5m profit to JD for the whole year — and any valuation sums for JD really ought to have been based on the £318.8m and not the reported £339.9m.

So there you go — three examples of obscure annual-report small-print that might prompt further investigation into the shares you own. Feel free to report any untoward or unusual annual-report small-print you have discovered in the comment box below.

Until next time, I wish you happy and profitable investing.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Daejan, Getech, Mincon, Mountview Estates, Oleeo, S&U, System1, Tasty, FW Thorpe, Tristel and M Winkworth.

Hi Maynard

Thanks for sharing, as usual interesting to get your insights. Hopefully your portfolio will start to pick up soon when we get this Brexit out of the way

Looking forward to your analysis on Tasty

Best

David

Great blog as always. Love the small-print analysis, thanks Maynard.