02 December 2019

By Maynard Paton

Results summary for Andrews Sykes (ASY):

- Revenue dropped 8% and operating profit dived 25% following lower demand for ASY’s heaters and boilers.

- European operations continue to represent almost a quarter of the business, with new depots opened recently in France.

- Accounts now affected by IFRS 16, although the fundamental attractions of decent margins (19%) and net cash (£20m) remain in place.

- Outlook comments appeared encouraging, with the company blog suggesting busy demand for pumps to combat flooding.

- The underlying P/E could be 16 and the yield is 3.9%. I continue to hold.

Contents

- Event link and share data

- Why I own ASY

- Results summary

- Revenue, profit and dividend

- IFRS 16

- Financials

- Valuation

Event link and share data

Event: Interim results for the six months to 30 June 2019 published 27 September 2019

Price: 620p

Shares in issue: 42,174,359

Market capitalisation: £261m

Why I own ASY

- Supplies air conditioners, portable heaters and industrial pumps for hire, with success based on a prompt 24/7 service, high-quality rental fleet and commercial-only customer base.

- Accounts regularly showcase high margins, generous cash flow, net cash and attractive returns on equity.

- Chairman and family are 90%/£234m shareholders and ensure management focuses on “long-term shareholder value creation”.

Further reading: My ASY Buy report | All my ASY posts | ASY website

Results summary

Revenue, profit and dividend

- ASY’s 2018 annual results had already hinted these first-half figures would not be that spectacular.

- The 2018 statement said: “The Board remains mindful of the favourable or adverse impact that the weather can have on our business.”

- However, the previous six annual statements had said (my bold): “The Board is therefore cautiously optimistic for further success in [the next year], always being mindful of the favourable or adverse impact that the weather can have on our business.”

- Management had deliberately removed the “cautiously optimistic for further success” part from the 2019 outlook.

- The absence of those words implied “further success” would be hard to achieve during 2019.

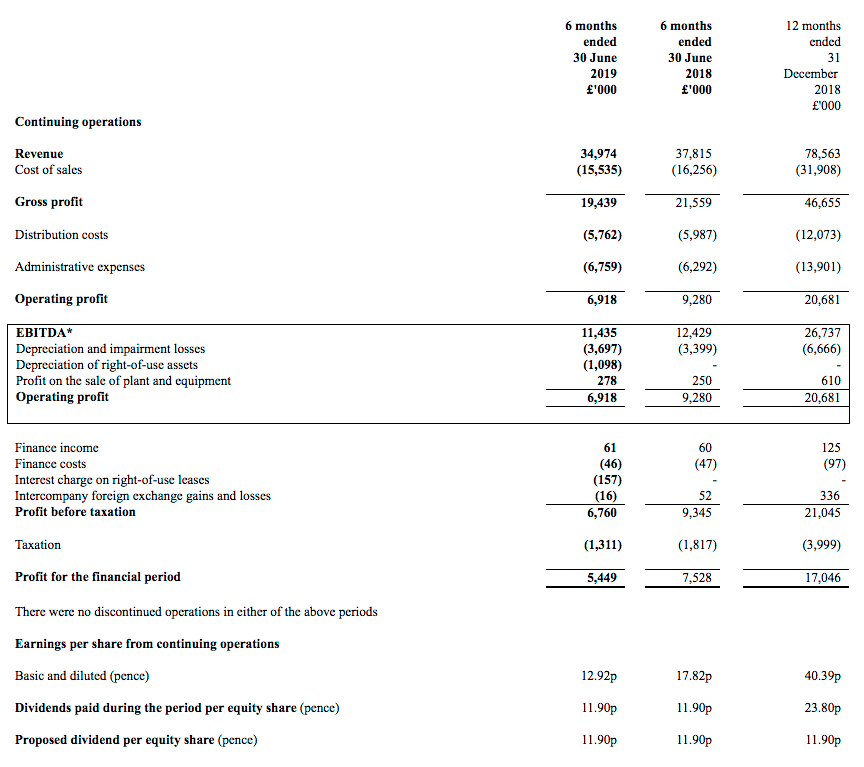

- Sure enough, this H1 witnessed revenue drop 8% and operating profit dive 25%:

| H1 2017 | H2 2017 | H1 2018 | H2 2018 | H1 2019 | |||

| Revenue (£k) | 35,334 | 35,966 | 37,815 | 40,748 | 34,974 | ||

| Operating profit (£k) | 8,171 | 9,418 | 9,280 | 11,401 | 6,918 |

- The shortfall was blamed on a milder winter that led to “less opportunities for… heating and boiler hire products”.

- I felt last year that the comparable H1 2018 figures were not that impressive, given the apparent scramble for portable heaters during the heavy snow and then for air conditioners during the subsequent heatwave.

- Following this H1 2019 performance, the comparable H1 2018 figures now appear much more impressive!

- This H1 performance was in fact the weakest since 2016.

- ASY revealed that UK sales of fuel for heaters and boilers plunged 40%. Total UK revenue slid 13%.

- The drier weather also meant lower demand for ASY’s pumps.

- The group’s European revenue fell 6% after mixed performances in Benelux, France, Italy and Switzerland.

- ASY reiterated that “start-up costs of the new businesses… continue to be expensed as incurred”.

- European depots still represent 23% of group revenue. The Middle East and Africa represent a further 17%.

- The profit slide did not lead to a divided cut. The 11.9p per share first-half payout has now been unchanged since 2014.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

IFRS 16

- ASY’s financials were affected by the introduction of IFRS 16.

- IFRS 16 dictates how companies should now recognise, measure, present and disclose operating leases within their accounts.

- Before IFRS 16, lease costs were identified as an individual operating expense.

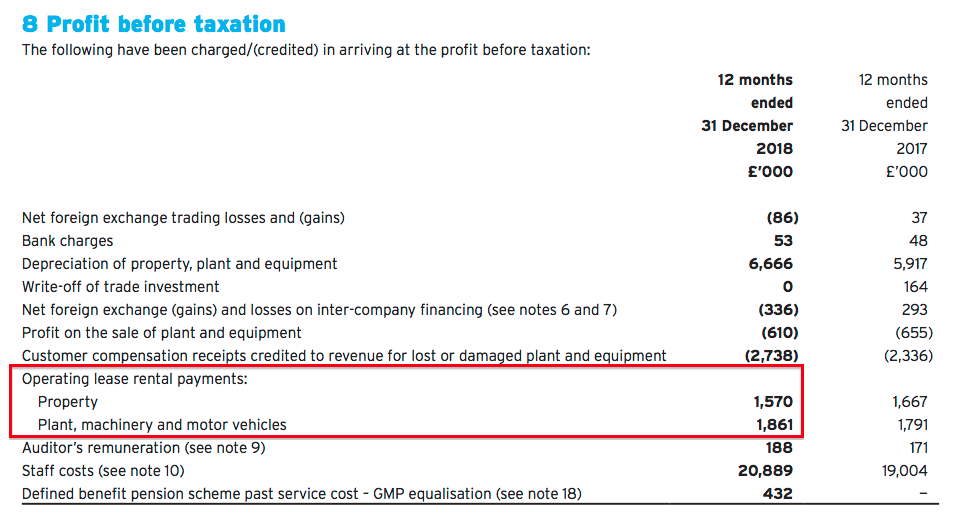

- For example, the 2018 annual report shows ASY spent £3.4m on property, plant and other operating leases:

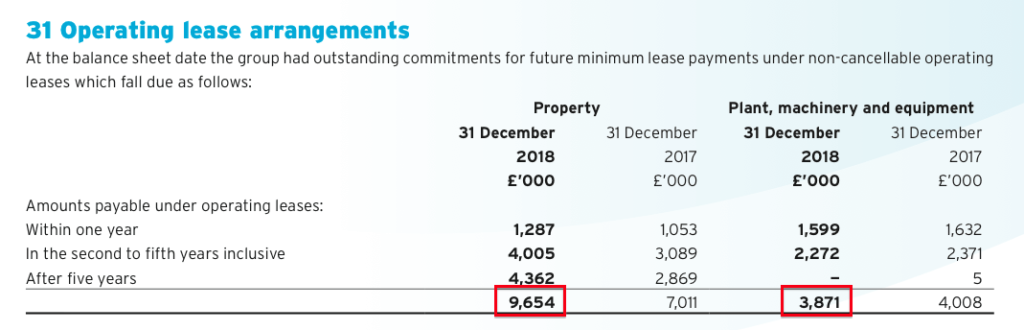

- And at the end of 2018, ASY had total minimum lease obligations of £13.5m:

- Under IFRS 16, lease costs are now charged through a mix of depreciation on ‘right-of-use’ assets and interest on ‘right-of-use’ leases.

- The ‘right-of-use’ assets initially reflect the value of the ‘right-of-use’ leases — which represent the total obligation of future leases discounted back into today’s money.

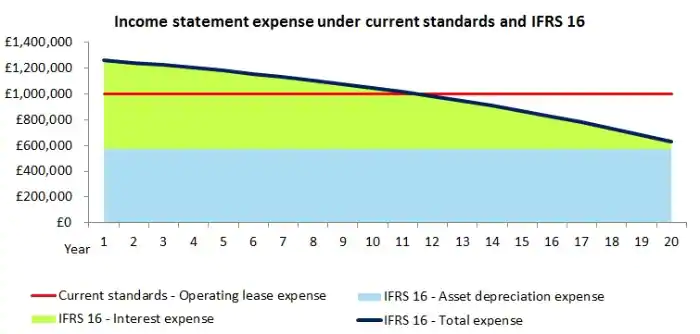

- A simple example of pre- and post-IFRS 16 accounting is provided by Deloitte. The chart below compares paying £1m a year on a 20-year lease before IFRS 16 (red line) and under IFRS 16 (dark blue line).

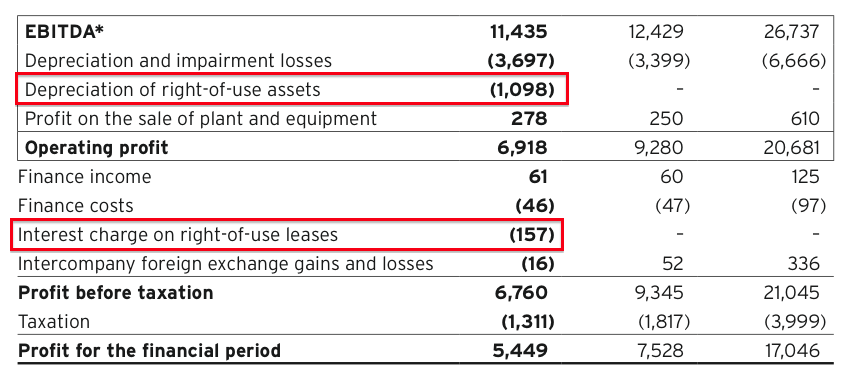

- For ASY, this H1 witnessed a combined lease cost of £1.3m:

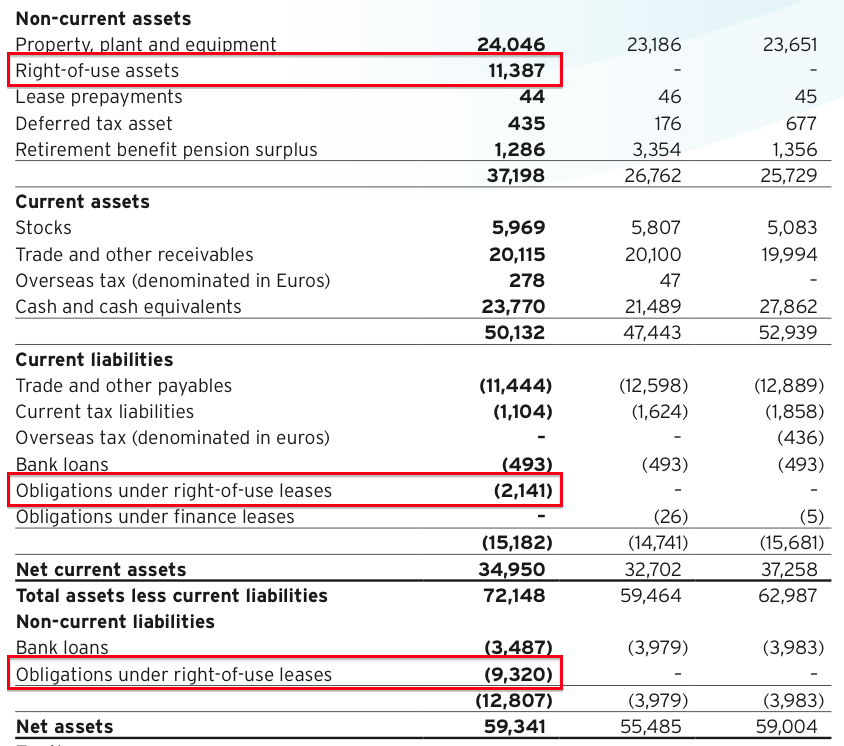

- ASY’s balance sheet shows right-of-use assets of £11.4m and ‘right-of-use’ leases of £11.5m:

- If lease costs were £3.4m during full-year 2018, the IFRS 16 lease cost of £1.3m for this H1 would appear low.

- That said, ASY claimed IFRS 16 had reduced pre-tax profit by only £50k during this H1 (my bold):

“As at 1 January 2019, the date of transition to IFRS 16, the group recognised additional right-of-use assets and liabilities of £11.4 million. An additional £1.1 million of new leases were capitalised and a depreciation expense of £1.1 million was recognised in the period. EBITDA was improved by approximately £1.2 million due to the removal of operating lease payments of this amount that would have been charged in accordance with the previous standards, and operating profit for the current period was improved by approximately £0.1 million. Overall profit before tax was reduced by approximately £0.05 million primarily due to the effect of charging more interest at the beginning of the lease term.”

- Perhaps the bulk of ASY’s lease costs will be recognised during the second half.

- The ‘right-of-use’ leases are classified as financial obligations.

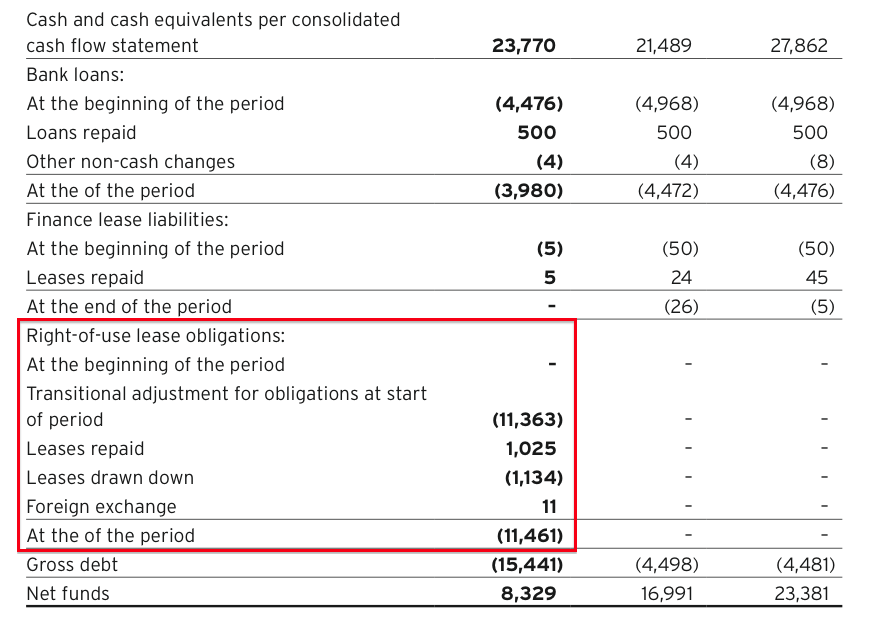

- As such, ASY now subtracts lease obligations when calculating net funds:

Financials

- ASY’s accounts remain in good shape.

- Despite the profit setback, the H1 operating margin (including ‘right-of-use’ lease interest) was a worthwhile 19%.

- ASY’s full-year operating margin has impressively topped 20% since at least 2008.

- The second-half margin is almost always higher than the first-half margin due to the greater profitability of air conditioners hired during the summer.

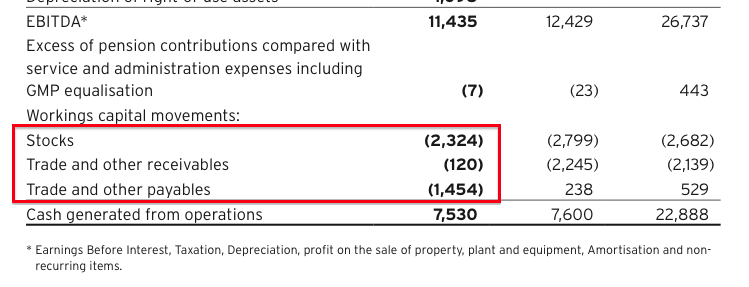

- Earnings of £5.4m during this H1 converted into free cash flow of £2.4m. The main use of cash during the half was £3.9m invested into extra working capital:

- The working-capital investments typically reverse during the second half.

- ASY’s working capital has absorbed £12m between 2014 and 2018. Buying extra equipment to sell (rather than hire) has been the main working-capital demand:

| 2014 | 2015 | 2016 | 2017 | 2018 | H1 2019 | |

| Operating profit (£k) | 11,311 | 13,208 | 15,816 | 17,589 | 20,681 | 6,918 |

| Working-capital movements | ||||||

| Stocks (£k) | (2,527) | (1,024) | (2,251) | (1,022) | (2,682) | (2,324) |

| Trade and other receivables (£k) | 284 | (2,196) | (1,876) | 563 | (2,139) | (120) |

| Trade and other payables (£k) | 686 | 139 | 1,970 | (696) | 529 | (1,454) |

| Total (£k) | (1,557) | (3,081) | (2,157) | (1,155) | (4,292) | (3,898) |

- The working-capital movements do not seem that untoward given the profit advance achieved during the same time.

- During this H1, free cash flow of £2.4m as well as £4.1m taken from existing cash resources funded dividends of £5.0m, reduced debt by £0.5m and reduced lease obligations by £1.0m.

- Cash finished the half at £23.8m, while bank debt was £4.0m.

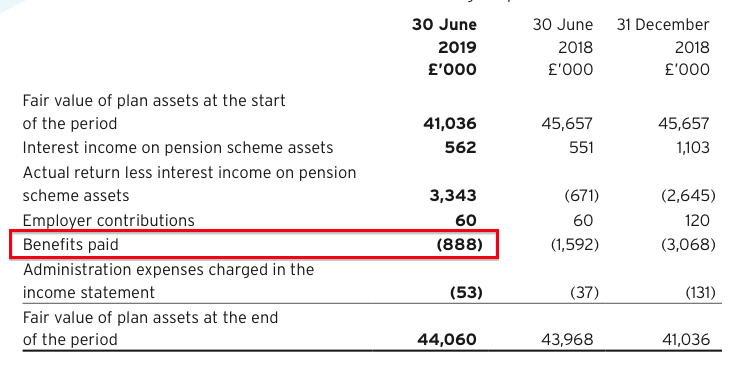

- ASY’s defined-benefit pension scheme continues to enjoy an accounting surplus.

- The 2018 annual report showed benefits paid to the scheme’s members had jumped to £3.1m.

- At the end of 2018, scheme assets of £41.0m required a very ambitious 7.5% return to sustain paying benefits of £3.1m a year without eroding the capital. (How To Evaluate Pension Deficits outlines the theory behind these sums).

- However, the scheme’s benefits have now reduced to an annualised £1.7m:

- Paying benefits of £1.7m from scheme assets of £44.0m requires a more achievable investment return of 4.0%.

- ASY’s pension-fund contributions remain low at £120k.

Valuation

- ASY appeared reasonably optimistic about the second half (my bold):

“Trading in the third quarter has started slightly more positively. In the UK the Pump hire revenue has shown a steady improvement and air conditioning hire revenue in mainland Europe has been strong, this has been driven by some extreme temperatures across the region, however the UK has not reached the very high levels we saw during the long hot summer of 2018. Once again activity in the Middle East has remained consistent through the summer period.”

- Since this H1 statement was announced, ASY has supplied pumps to flooded parts of South Yorkshire (my bold):

“It has been a particularly busy time for Sykes Pumps with businesses desperate to safeguard their premises and restrict the impact of flooding wherever possible. Our engineers have been working with a multinational infrastructural group by installing pump hire solutions to prevent further flooding in nearby locations that have been identified as high risk.”

- Management comments at the 2016 AGM indicated hiring out pumps was not as lucrative as hiring out air conditioners or heaters.

- ASY’s blog also reveals a “sizeable increase in the number of enquiries relating to heater hire for temporary storage applications”.

- ASY remains a tightly held share with a minimal free float and wide bid-offer spread.

- The 99-year-old chairman and his family own almost 90%, leaving approximately 10% for everybody else.

- A 620p mid-price values ASY at £261m and the free float at £27m.

- Subtract the £20m net cash position from the market cap and the underlying business could arguably be valued at approximately £232m or 573p per share.

- ASY has operated with net cash since 2010, and perhaps such cash is required to keep the business on a stable footing.

- Dividends before 2010 had been rather haphazard, due in part to significant levels of debt combining with the banking crash.

- My net cash figure excludes IFRS 16 lease obligations. However, my profit sums below are taken after the cost of the ‘right-of-use’ lease interest

- The trailing twelve-month operating profit is £18.2m. Bear in mind this £18.2m was buoyed by last year’s bumper H2 profit.

- Adding back a one-off £0.4m pension charge and applying tax at 19% gives earnings of 35.8p per share.

- The underlying P/E could therefore be 573p/35.8p = 16.0.

- The trailing 23.9p per share dividend supplies a 3.9% income at 620p.

- ASY’s valuation does not appear an obvious bargain. My sums (here and here) have pointed to a cash-adjusted P/E of 16 since at least October last year.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Andrews Sykes.

Andrews Sykes (ASY)

Trading update and impact of Covid-19

Just catching up with ASY and a statement published on 27 March 2020.

Here is the full text:

———————————————————————————————

Andrews Sykes, a market leader in specialist hire solutions, provides an update on trading in the period since the announcement of its half year results on 27 September 2019.

Trading in the second half of the year ended 31 December 2019 was strong and this is likely to produce a result that, although below the Company’s record year of 2018, will still be its second-best result on record.

The Company’s operations in mainland Europe enjoyed a good summer period, enhancing its overall air conditioning business revenues and the main UK subsidiary benefited from the very wet weather towards the end of the year, with pump hire performing particularly well.

The audit process for the 2019 results is well underway. The Board is awaiting feedback from the Company’s auditors with regards the timing of the completion of the process and will notify the market of the publication date of its 2019 Annual Results in due course. A decision with regards the payment of a final dividend with regards the 2019 financial year will be taken at that time. The Board notes the ability of AIM quoted companies with year ends between 30 September 2019 and 30 June 2020 to apply to AIM Regulation for an extension of up to three months to the reporting deadline for the publication of their audited accounts.

The first quarter of 2020 started positively – especially in the UK where the pump hire business continued to perform at high levels – with overall trading in the year to date marginally ahead of the same period in 2019.

However, like so many businesses, the Company is now facing challenges as a result of the global COVID-19 pandemic. The Board is continually assessing the potential disruption caused by COVID-19 and has put measures in place to provide protection to the Company’s staff and customers and to protect its cash position. The Board recognises that further actions are likely to become necessary as this unpredictable situation evolves.

Our smaller operations in Italy and France have been fully compliant with local directives in relation to the restriction of movement and this has had a negative impact on our operations in those countries. Since the Prime Minister’s address on Monday, 23 March 2020, the UK business has also faced similar restrictions, and these will continue to impact our results. The Company provides services to many essential industries, such as the Department of Health and Social Care, and will do its upmost to continue to support these industries.

Compared to many sectors of the economy, such as hospitality and retail, the impact on the Company to date has not been severe, but we are mindful that this situation could change very quickly. The Company’s capacity for sustained cash generation and its long-term strategy of maintaining good levels of cash reserves will help support it during the coming months. As at 26 March 2020, the Company has net cash reserves of £28m.

———————————————————————————————

I wrote in my Q1 2020 review that “I expect near-term earnings to be reduced but I hope most of the £10m a year dividend can be sustained.” That seems to be the case given the subsequent 2019 results. An upcoming blog post will look at those figures in more detail.

Maynard