***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

17 May 2024

By Maynard Paton

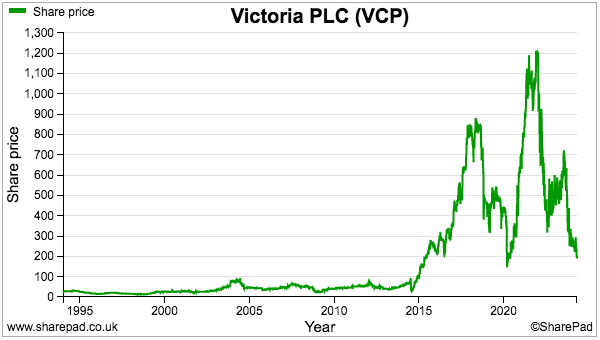

Oh dear. Today I am writing about Victoria, a £228 million carpet manufacturer that last year attracted attention following an adverse audit:

When I last looked at an adverse audit for SharePad, a commotion erupted that debated whether I was simply reporting “transcription errors” or spotlighting something more sinister.

So to be clear:

- What follows is just my interpretation from reading Victoria’s 2023 annual report and other company statements;

- I have not inspected every part of Victoria’s accounts nor considered every aspect of the wider investment case, and;

- Please do your own research and form your own conclusion.

And with that, let’s take a closer look.

Read my full VICTORIA article for SharePad >>Maynard Paton