***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

13 April 2024

By Maynard Paton

Everybody loves shares that keep on rising.

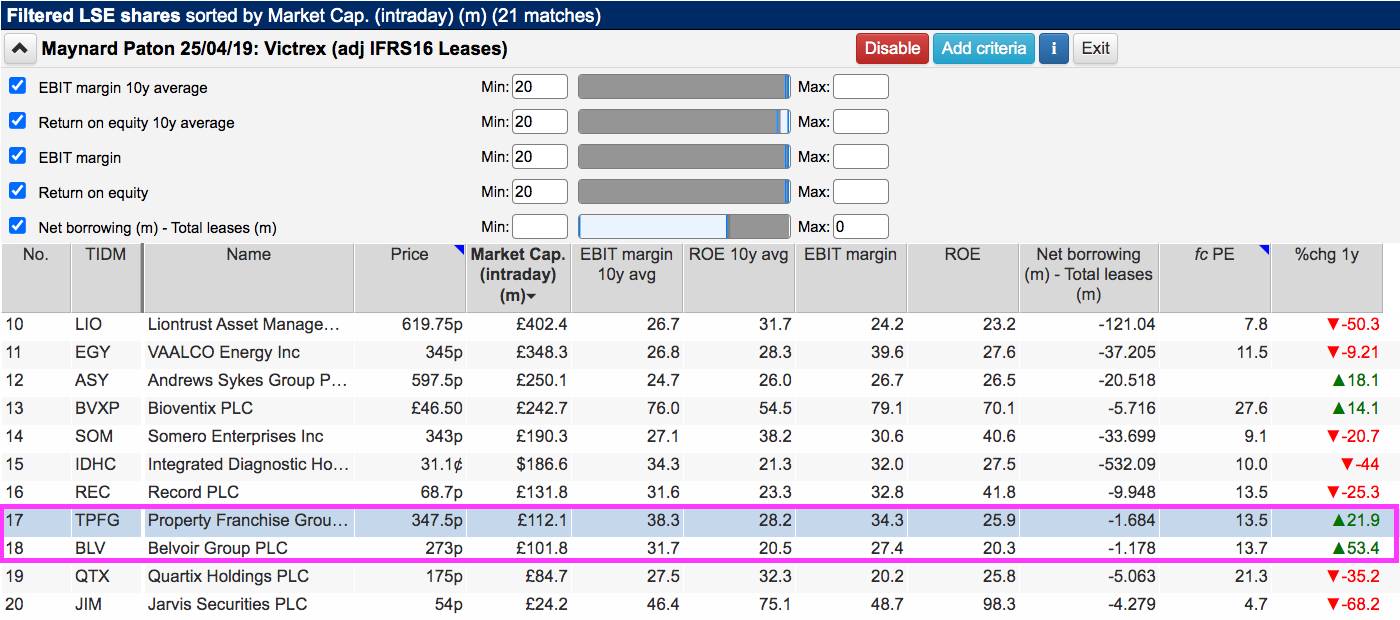

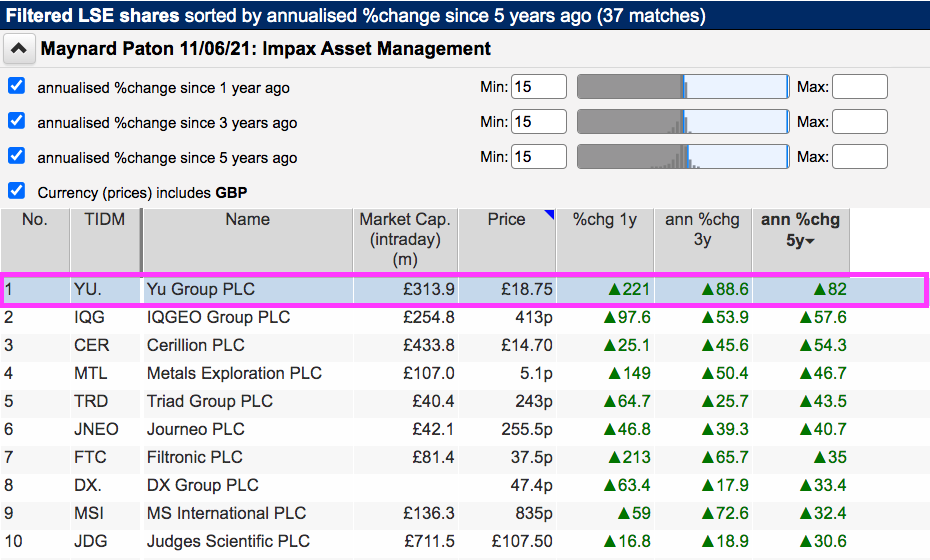

SharePad lists 37 names that have consistently delivered 15% or more annualised returns during the last one, three and five years:

The shares of independent energy supplier Yü Group have certainly kept on rising; they have more than tripled since April 2023 and have 20-bagged since early 2019.

Factors involved in this superb investment include:

- A ‘market-pariah’ valuation caused by an adverse accounting review;

- An astounding recovery buoyed by elevated energy prices;

- A ‘scalable’ business that generates extra revenue without a commensurate increase to the workforce, and;

- The entrepreneurialism and commitment of founder Bobby Kalar.

Let’s take a closer look.

Read my full YÜ GROUP article for SharePad >>Maynard Paton