03 January 2025

By Maynard Paton

Happy New Year!

I trust you enjoyed the festive break and are now ready to battle the market for another twelve months!

This post provides a ‘year in review’ of my current holdings. I recap how each business performed during 2024 as well as provide a few remarks about their attractions, drawbacks and valuations.

These reviews are very useful to write, not least because they help ensure I am still invested for the right reasons. I also hope the reviews help me avoid disappointing returns during the year ahead! I undertook the same review process at the start of 2015, 2016, 2017, 2018, 2019, 2020, 2021, 2022, 2023 and 2024.

My portfolio gained 22.4% during 2024 and this other post explains that performance in more detail.

I have covered each of my holdings below in order of size within my portfolio. I have accompanied each write-up with a ShareScope chart to show how each company has progressed over the longer term.

Of course my calculations, logic, assumptions and charts may have little bearing on the future… so please do your own research and derive your own conclusions!

Contents

- System1

- Mountview Estates

- Tristel

- City of London Investment

- M Winkworth

- Bioventix

- S & U

- FW Thorpe

- Andrews Sykes

- Mincon

- Summary

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, FW Thorpe, Tristel and M Winkworth. This blog post contains ShareScope affiliate links.

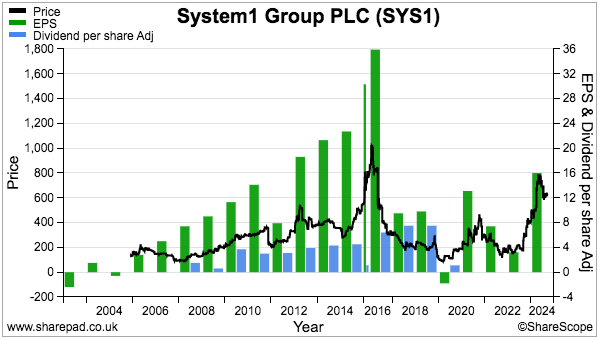

1) System1 (SYS1)

- Bid-price: 610p

- Market cap: £81m

- Portfolio weighting: 38.2%

SYS1’s transition from bespoke consultancy towards automated ‘platform’ services accelerated during 2024.

The ad-testing specialist started the year announcing a better-than-expected Q3 that was followed by a better-than-expected Q4. July’s FY results confirmed annual revenue gained 28% to £30m and pre-tax profit to be £3.1m — well ahead of the £2.8m anticipated after the Q4 upgrade. The first dividend for more than four years was even declared.

Then came July’s Q1 update that reported revenue up 53% driven by platform revenue surging an astonishing 74%. The shares had started the year at 295p but touched almost 800p during the summer.

The share-price enthusiasm was supported by a growing belief that SYS1 was finally exploiting its “unique” way of translating human emotions into accurate predictions of marketing success.

In fact, industry guru Mark Ritson now claims SYS1 has “come to dominate the field of pre-testing in a remarkable short period of time”. Stuart McGurk at the FT has meanwhile reported: “Every retail brand I spoke to for this story tests its advertising with System1.”

Less than two years after facing a shareholder revolt, SYS1 is now confident enough to include tantalising ‘illustrative scenarios’ within its presentations.

SYS1 at first illustrated revenue doubling and Ebitda margins scaling to 30% over the “medium term“, which I believed could support a £16 share price. An updated scenario now suggests revenue could quadruple over the “long term” to reach the same margin, which might support £30-plus.

Future growth is based upon winning large customers in the United States (which appears increasingly plausible with US H1 revenue up 79%), and revitalising the group’s innovation-testing service (which appears less plausible). Holding back the innovation service is a lack of relevant “thought leadership” and confidentiality limitations to publicising client-innovation info.

The accounts do not yet exhibit true ‘quality’, but record revenue per employee underpins the workforce’s new “performance culture” while £9m net cash allowed December’s H1 statement to unveil a £2m “discretionary” investment. Margins and the share price will suffer if ‘discretionary’ actually means ‘mandatory’ and the extra ‘illustrative’ revenue proves elusive.

SYS1’s founder retains his 22% holding and, fortunately, now acts as a background “mad inventor“. I meanwhile trust the other executives will demonstrate strong ambition through a challenging new LTIP.

I bought SYS1 at 325p (2016), 238p (2018), 183p (2020) and 242p (2021), and despite my hefty weighting have never top-sliced.

My SYS1 buy report | All my SYS1 posts

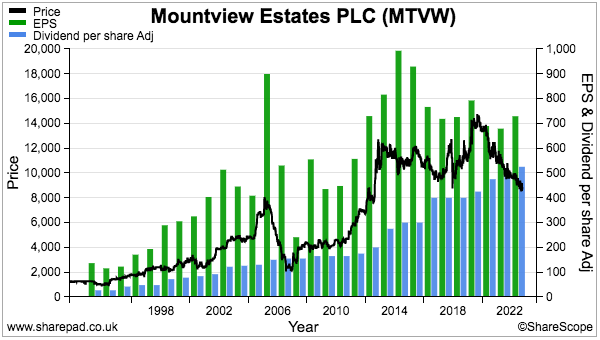

2) Mountview Estates (MTVW)

- Bid-price: £86

- Market cap: £335m

- Portfolio weighting: 10.6%

MTVW was my top top-up idea of 2024. I elevated the regulated-tenancy landlord into second place within my portfolio after almost doubling my holding (Q2, Q4) at a £96 average. I first bought during 2011 at £42 and acquired more at £98 (2018 and 2019).

The valuation theory is relatively simple: MTVW’s trading properties are carried at cost and I estimate the £103 per share NAV — up 42x since 1985 — could eventually realise approximately £180 per share versus a bid-price of £86. The dividend — up 117x since 1985 — meanwhile supports a 6% income. The discount to book is the widest for eleven years and the yield the highest for 15.

I believe today’s lowly rating is due mostly to doubts over whether MTVW still generates adequate property gains. My calculations indicate properties bought and then sold since 2014 have realised proceeds of only £69m versus their £64m purchase cost.

The board has repeatedly said MTVW aims to buy regulated tenancies at 75% of vacant possession value, which should in theory lead to 33% profits on disposal.

Group debt costs advancing beyond 6%, the prospect of (further) unfavourable landlord legislation alongside a consistent “difficult times” narrative are other explanations why the stock market remains wary.

MTVW’s ownership structure creates a very fine line between ‘value bargain’ and ‘value trap’.

The chief executive’s 50% family concert party dictates proceedings and overlooks regular AGM protest votes from his sister (15% ownership and speaks for 24%) and (I understand) property tycoon David Pears (7% ownership). The 2024 AGM was another lively event, with trenchant questions about corporate governance, non-executive independence and the lack of another estate valuation.

Still, a new non-executive provides hope that outside shareholders might one day influence the board; her 25-year property background includes a “keen focus on governance, risk, and compliance, ensuring best practices are followed across all levels of operations“.

MTVW remains a share only for the extremely patient. But the chief executive is 77 and other concert-party stalwarts are at least 69… and I would like to think their beneficiaries may not be such die-hard MTVW investors.

Indeed, the chief executive did not rule out a group sale at the AGM: “There may be another company that… is very capable of taking the rump of our portfolio, who may come in and buy that rump.” Although he did add: “We’re not very near that date yet.”

My MTVW buy report | All my MTVW posts

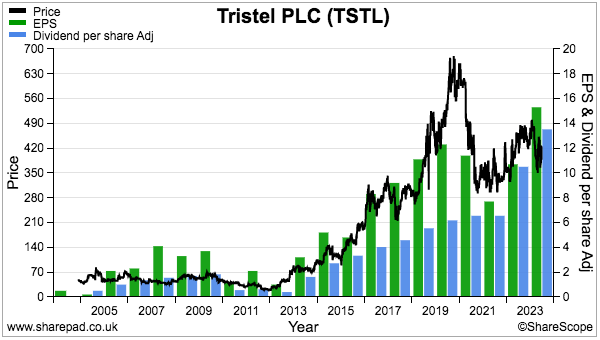

3) Tristel (TSTL)

- Bid-price: 420p

- Market cap: £200m

- Portfolio weighting: 9.3%

Twelve months ago I was left wondering why TSTL’s chief executive had suddenly decided to retire.

All became clear during 2024 after the new chief executive informed shareholders of “purchasing bureaucracy” within the United States.

TSTL had finally achieved FDA approval for its ultrasound-disinfection foam during 2023, but those tasked with selling the product in the US — which ought to become the group’s most lucrative market — were simply not prepared for ‘sales cycles’ of up to 18 months.

The leadership change ought to end TSTL’s persistent over-promising and under-delivery of the US programme. The CV of the new boss ticks a lot of US/marketing/healthcare boxes, and I trust he can in time fully exploit TSTL’s unique disinfection chemistry in what is now deemed a “$100m opportunity” for the group and its US partner.

Certainly TSTL’s range of hospital disinfectants continue to sell well around the world. Both February’s H1 results and October’s FY results set new records for revenue and profit, helped in part by overseas sales gaining 8% to £25m from 61 countries. Demand for proper disinfection plus deft purchases of three distributors have advanced overseas revenue five-fold in ten years.

TSTL’s UK progress remains very impressive, too. Domestic sales last year gained a remarkable 32% to £16m, supported by 9% greater volumes alongside higher prices included within a new NHS supply agreement.

TSTL’s accounts reflect an attractive industry position, with the top-selling wipes and foams earning an 83% gross margin that perhaps persuaded the new chief executive to retain the group’s appealing 25% Ebitda-margin target.

The new boss should reveal his medium-term financial goals during 2025, although the board’s ‘boilerplate’ LTIP — seeking only 5.5% minimum EPS growth — is a concerning omen for management ambition.

At least the board has kept its bold commitment to lifting the annual dividend by a 5% minimum, while last year’s 29% payout advance plus lowly c1.1x dividend cover emphasise TSTL’s inherent cash generation and lack of significant capital requirements. Net cash at the last count was a healthy £12m.

These shares currently trade at a level first achieved almost five years ago, although the 25x P/E understandably still reflects the group’s superior growth history and expansion possibilities. I bought at a 46p average during 2013 and 2014, and sadly top-sliced at 79p (2014), 100p (2015), 123p (2016) and 289p (2017) to retain just 25% of my original holding.

My TSTL buy report | All my TSTL posts

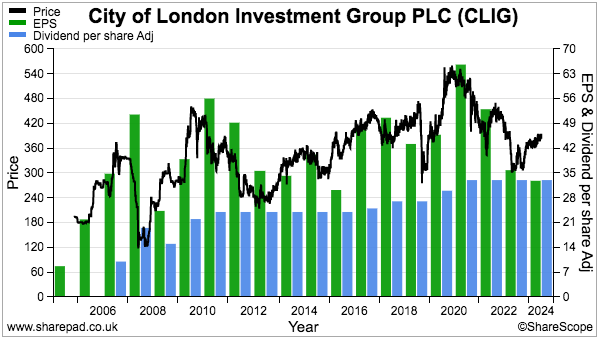

4) City of London Investment (CLIG)

- Bid-price: 381p

- Market cap: £193m

- Portfolio weighting: 9.1%

Another year, another CLIG purchase.

I topped-up my holding in the fund manager at 332p during 2024 (Q2) after previously adding at 320p (2023) and 350p (2022). I invested initially at a 281p average between 2011 and 2013, but did sell 42% of those shares at 335p (2015).

The close proximity of my buy and sell prices do tell a story… that capital gains here are hard to come by.

Returns are typically delivered by the dividend, which last year remained at 33p per share to support a scarcely believable 10% yield on my 2024 purchase. The income is so high because FY 2024 earnings of 33.5p per share barely covered the payout while the business generally struggles to attract new clients and grow.

Sad to say, but October’s Q1 2025 update announced the eleventh quarterly outflow of client money from the last 16 quarters. Total funds under management at $10.7b are meanwhile less than the $11.0b witnessed at the end of 2020.

Although CLIG’s investment strategy — buying investment trusts at attractive discounts and occasionally taking an activist stance — is eminently very sensible, the predominantly US client base just seems reluctant to hand over extra money. CLIG delivering mid-single-digit returns for a c0.7% fee when the S&P 500 is rocketing 20% per annum for a c0.1% fee probably explains why.

The saving grace here is the group’s largest shareholder, George Karpus. At the 2023 AGM, Mr Karpus issued a scathing statement that demanded the board “be replaced with a seasoned group of directors that understand the enormous potential of CLIG“.

Mr Karpus founded Karpus Investment Management during the 1980s and knows how to run a lucrative money manager. His firm attracted client money of $3b that paid him a $15m salary before merging with CLIG during FY 2021.

Mr Karpus now heads a 38% concert-party stake and his influence persuaded two non-executives to step down last year. A series of “constructive meetings” with CLIG also appears to have appeased his anger, and board comments at the 2024 AGM revealed Mr Karpus having “high hopes and high expectations” — especially on the matter of generating new business.

Despite clients chipping away at fees and employees enjoying greater pay, CLIG’s margin — although not as high as it once was — remains a useful 38%. Net cash of $34m could also shore up the all-important dividend if/when markets tumble and/or new clients remain evasive.

My CLIG buy report | All my CLIG posts

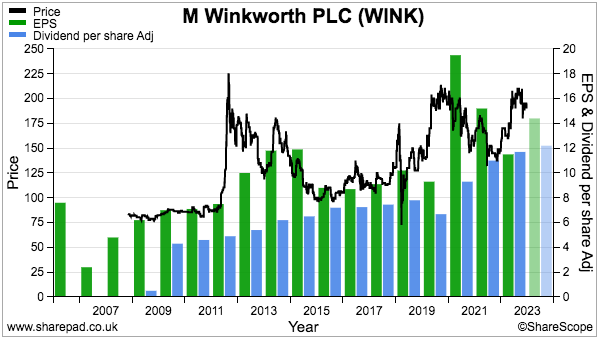

5) M Winkworth (WINK)

- Bid-price: 190p

- Market cap: £25m

- Portfolio weighting: 7.4%

Has WINK put itself up for sale?

The appointment last year of two non-executives with extensive corporate-finance backgrounds certainly suggested the estate-agency franchisor was at least contemplating some M&A activity.

During September’s H1 webinar, WINK claimed the appointments were “part of the natural evolution of the board as we bring in new talent to ensure that we can do our best to push the company forward, aligned with the vision and values we hold dear.” Press rumours were also dismissed: “The Negotiator is wrong to suggest that Winkworth is putting itself up for sale.”

The sector nonetheless continues to consolidate, not least because UK housing transactions have stagnated since 2007 and ‘growth’ therefore depends entirely on wining market share and higher property prices. Maybe the non-executives were recruited because the merger between quoted peers Property Franchise and Belvoir prompted a fresh bout of tentative bid enquiries.

The decision to sell out or not will be taken by WINK’s chairman, who boasts a 41% shareholding and is now 82 years old. The chairman’s son is WINK’s chief executive and owns a further 6%.

WINK’s trading improved during 2024. Interest rates reaching 5.25% during 2023 led to fewer property transactions, with April’s FY results revealing a 25% profit decline after sales commissions dropped 20%.

But September’s H1 statement announced sales commissions up 9% and profit up 24% after additional sellers returned to the market. Sales activity apparently accelerated during H2.

Bid or no bid, WINK should navigate today’s property market better than most. In particular, the group’s franchising structure — 100 of the 103 branches are operated by franchisees — provides greater flexibility to revitalise locations “where our standards are not met”. WINK’s three in-house offices meanwhile create a “training ground” for up-and-coming agents with ambitions to run their own WINK franchise.

The aforementioned chairman likes his dividends, as they are paid quarterly, have doubled during the last ten years and included a number of specials. The shares yield 6%, but dividend cover is a tight-ish c1.2x because profit currently runs at the same c£2m as 2014/2015. The accounts remain in good shape, with margins close to 20% and the balance sheet carrying £4m net cash.

My initial WINK buy occurred at 90p during 2011 and I sold 70% at 173p (2013 and 2014). I then topped up at 116p (2016 and 2017) and 178p (2021).

My WINK buy report | All my WINK posts

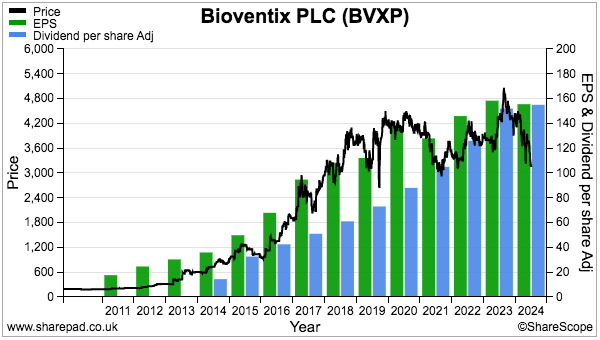

6) Bioventix (BVXP)

- Bid-price: £31

- Market cap: £162m

- Portfolio weighting: 6.7%

Could the next twelve months prove pivotal for BVXP?

I attended the 2024 AGM (notes coming soon!) and the board suggested by “this time next year“, the diagnostic-antibody developer ought to have discovered whether its Alzheimer’s R&D has progressed to the final stages of customer testing.

If BVXP does progress, then shareholders are one step closer to possibly participating in what the board described as a “blockbuster era of human-neurology diagnostics during the 2030s“.

October’s FY results revealed a £155k income from the Alzheimer’s R&D, which implies BVXP’s customers have enjoyed some prototyping success to date. Purchase orders are apparently “encouraging“, as are very tentative conversations about royalty rates.

I am pretty sure the Alzheimer’s potential depends mostly upon the brain-derived tau test that measures neuro-degeneration. I get the impression the research-based revenue from the Alzheimer’s work has far exceeded any other research-based revenue BVXP has earned.

The Alzheimer’s R&D was the highlight of a relatively subdued year. Both FY revenue and profit gained 6% after BVXP admitted income from its top-selling vitamin D antibody advanced only 1%.

Rather embarrassingly, past royalties from the troponin antibody — once expected to become the next big seller — had been overstated by a major customer. The final dividend was unfortunately reduced by 3p to 87p per share.

The 4.8% dividend yield has today become the principal source of returns as the shares revisit levels first achieved more than six years ago. But BVXP’s wonderful business model — customers undertake a lot of the antibody manufacturing and pay BVXP usage royalties — continues to lead to super economics.

A stratospheric 78% of revenue was converted into profit last year, partly because BVXP’s physical antibodies sell for up to £210k a gram and only 17 people are employed in the company’s small lab. Earnings since FY 2016 have meanwhile more than doubled despite being distributed entirely as dividends during the same time. Net cash is £6m, too.

I bought BVXP during 2016 at £11 and have never top-sliced. I must admit the 21x trailing P/E is not an obvious bargain, but then again seems not to anticipate much Alzheimer’s R&D hitting the big time.

The chief executive founded BVXP, still owns 6% and seems enthused by Alzheimer’s research generally and what he claimed to be “one of the most remarkable changes that I’ve seen downstream amongst our customers in the last 20 years”.

My BVXP buy report | All my BVXP posts

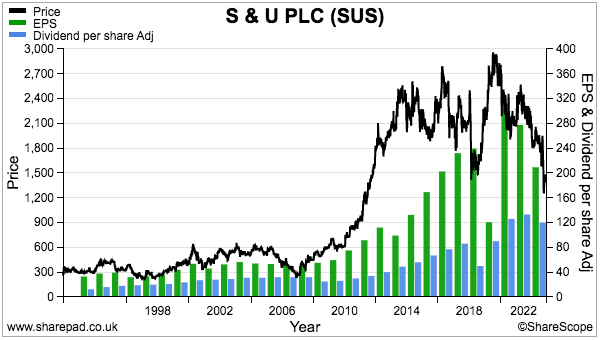

7) S & U (SUS)

- Bid-price: £14

- Market cap: £171m

- Portfolio weighting: 6.1%

I wrote last year: “I am hopeful 2024 sees resilient trading and an opportunity to invest very close to (or even below) NAV.”

I took the opportunity to invest below NAV during 2024 after buying more at £18.62 versus a £19.27 per share NAV (Q2).

Since 1994, SUS has only briefly traded below NAV during 2000, 2008/9 and 2020 — and the 2024 ‘bargain’ rating therefore appeared too good to miss.

After all, the specialist lender’s veteran executives boast a 44%-plus shareholding, enjoy 40-year tenures and have successfully handled previous difficulties by always demanding careful underwriting and prudent borrowing. Proof of management’s success is NAV advancing 38x and the dividend expanding 48x since 1987.

Trading last year was sadly not exactly “resilient“. April’s FY results admitted H2 profit had dropped 41% following an extra £10m impairment on suspected bad loans within SUS’s car-loan division. An “upsurge” in regulatory activity led to SUS agreeing to “specific limitations on its repayment processes” as the wider motor-finance industry acclimatised to the FCA’s new Consumer Duty regime.

October’s H1 results then showed profit down 40% and the interim payout cut 14% as SUS’s ‘voluntary’ adherence to FCA collection restrictions prompted a further £11m write-off. The proportion of up-to-date car loans slid to a pandemic-like 69%.

Shareholders did enjoy some respite last year, when SUS confirmed the FCA had lifted its restrictions and the motor-loan division could presumably re-engage with late-paying customers.

But that respite lasted just two weeks, as a bombshell legal case then ruled car dealers could not receive commissions from motor-finance lenders unless customers had provided their “informed consent“. The ruling effectively deemed the FCA’s commission-disclosure rules as unlawful and leaves SUS — as well as the entire motor-finance sector — open to compensation claims.

While the bombshell case heads to a final judgement this year, even consumer champion Martin Lewis is unsure whether motor-finance lenders should have to reimburse customers: “I find it difficult to believe that retrospective redress is due from car-finance firms with fixed commissions, as they were following regulator’s guidelines.” SUS has always paid fixed-fee commissions.

For now the £14 shares trade at 0.74x NAV and yield a trailing 8%. The upside could be considerable if the bombshell ruling is overturned and SUS then captures market share as rivals succumb to (the separate) DCA compensation. I first bought SUS during 2017 at £21 and bought more at £19 (2019) and £17 (2020). I have never top-sliced.

My SUS buy report | All my SUS posts

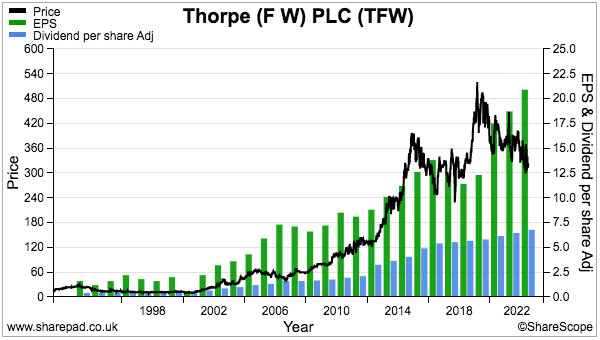

8) FW Thorpe (TFW)

- Bid-price: 306p

- Market cap: £364m

- Portfolio weighting: 4.7%

Combining the roles of chief executive and finance director was the most notable event at TFW last year. I can’t recall another quoted business the size of TFW — revenue of £176m and operating profit of £33m — undertaking such an unusual board structure.

The lighting manufacturer said the combined role followed the “strengthening [of] the subsidiary boards at the operating companies and promoting a focused group of managers from within that can support Group activities when called on”.

TFW shed more light on the matter during the 2024 AGM. Attendees were told managing the overseas operations at board level had become “quite difficult” and that the combined CEO/FD role was “not going to be the same forever”. Furthermore, a new-ish “group innovation team” reports directly to the board to offset the current lack of ‘lighting’ board executives.

Outside shareholders must for now trust the dual CEO/FD role does not inhibit TFW’s progress — and its wonderful run of 22 consecutive annual dividend advances.

The board remains reassuringly staffed by two Thorpe-family non-executives, who spent their careers at TFW, have (presumably) accrued plenty of knowledge about management appointments and risk an aggregate 43% shareholding if the board reshuffle is mis-judged.

A standstill H1 effort was followed by a stronger H2 that helped FY 2024 profit to gain 9% and allowed a small special dividend — the third in four years — to be declared.

TFW’s margin last year returned to a welcome 18% — the highest since FY 2015 — with the group’s main Thorlux division now boasting 20%. Cash control remained very satisfactory and pushed net cash to a mighty £50m.

I speculate a large portion of that £50m will eventually be spent on European acquisitions. The last decade has witnessed TFW spend c£80m in the Netherlands, Spain and Germany in order to, as AGM attendees were told, “de-risk” the group from the UK. Although no purchase blunders have so far emerged, the board does not publish return on capital measures to assess its investments.

TFW’s immediate outlook is not incredible, with November’s AGM indicating “marginally ahead” progress. But long-term demand for the group’s energy-efficient lighting — one customer last year enjoyed an energy saving of 94%! — ought not to diminish.

The share price is back to levels first reached eight years ago while the 14x P/E is the lowest for ten years. I first bought TFW during 2010 at 69p, added more at 80p (2011) and 89p (2012), and sold 25% at 234p (2016).

My TFW buy report | All my TFW posts

9) Andrews Sykes (ASY)

- Bid-price: 488p

- Market cap: £204m

- Portfolio weighting: 2.1%

I am convinced employee productivity is linked to investment success and therefore any business that publishes a “staff absenteeism” KPI should deserve greater attention.

Say hello then to ASY, whose absenteeism KPI declined from 1.67% to 1.01% between 2020 and 2023. The equipment-hire group seemingly weeded out unreliable workers after the pandemic and, remarkably, May’s FY results showed the headcount reduced by 13% to the lowest level since 2013…

…and yet revenue per employee — also a published KPI — is now 20% higher than the pre-pandemic peak.

A tip-top workforce underpins ASY’s “premium level of service 24 hours per day, 365 days per year” that in turn allows the group to become “the preferred supplier to many major businesses and operations spanning a huge range of industries and geographic locations“. The hire equipment supplied is predominantly water pumps, air conditioners and heaters — demand for which is prompted by heavy rain, heatwaves and cold snaps respectively.

The weather during the last year or two has not been too favourable for ASY. The UK did not experience another 2022 40-degree summer during 2023 or 2024, while September’s H1 statement admitted to a milder winter that left both revenue and profit unchanged. May’s FY figures were actually quite similar to those reported for 2018.

Mind you, ASY’s accounts are still pristine, wth highlights including net cash last seen at £21m and a conventional return on equity of 34%. And the employee efficiency has pushed annual margins to a super 29% — the highest for at least 15 years.

But one drawback is the unchanged productivity of the hire equipment. For some years now, £1 invested in new equipment continues to earn £1 of annual revenue.

Growth is most likely to be driven by extra depots within ASY’s European operations, revenue from which has tripled since 2009 to support a third of the top line. But the group’s overseas progress has not been straightforward, with the French subsidiary now closed and losses suffered in the Middle East.

The shares trade at levels first achieved seven years ago and do not seem extravagantly valued at 12x earnings plus a 5% yield. I purchased at 233p during 2013 and have never top-sliced.

ASY is 91% owned by the Murray family, who do like their dividends; the last ten years have witnessed earnings distributed entirely through a mix of ordinary and special payouts. The Murrays have controlled ASY for approximately 30 years and I vaguely speculate they may one day wish to sell.

My ASY buy report | All my ASY posts

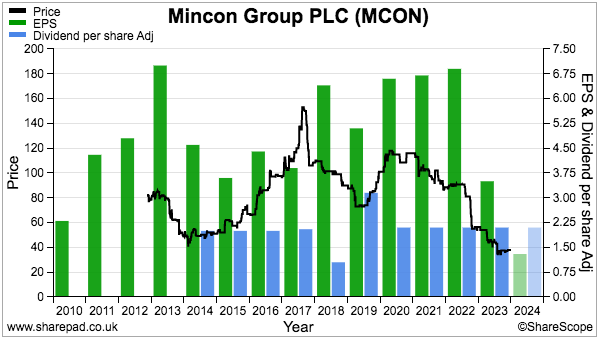

10) Mincon (MCON)

- Bid-price: 37p

- Market cap: £79m

- Portfolio weighting: 1.1%

‘Life events’ sadly prevented me from evaluating results from MCON last year. Maybe overlooking the industrial-drill manufacturer was for the best, as progress went from bad to worse.

FY figures published during March revealed revenue down 8% and profit slumping 38% after mining customers bought fewer drills due to lower commodity prices and post-pandemic “destocking“.

Alarmingly, MCON essentially admitted its technical-innovation ‘moat’ had been breached by low-cost pricing:

“We found also that the competition in standard, unpatented drilling tools was increasing with products manufactured in low-cost economies in particular undercutting our products by a margin significant enough in the eyes of the clients to counterweigh the lower technical performance of those products. It is our job to confront this situation and to take steps to retain and grow our market.”

H1 results issued during August were terrible. Revenue slid 16% as this time construction customers reigned in their spending after higher interest rates curtailed building activity. H1 profit came in at just €249k and the directors could not even acknowledge they suspended the dividend.

A “root and branch” cost-cutting review has been initiated, but I am convinced MCON’s “one-stop-shop” strategy is the fundamental problem. Supplying large customers directly with an extended product range has over time lumbered the group with stock of €69m — equivalent to an enormous 48% of revenue — and net debt of €17m.

To make matters worse, I am unsure whether MCON is adhering to its debt agreements. Trailing twelve-month Ebitda is €14m while the annual-report covenant small-print says “Ebitda to be no less than €18 million“.

MCON is 56% owned by the founding Purcell family, which goes to show significant insider ownership does not always lead to investment success. A new formal risk for the group cited “management burnout“, and I believe an outside chief executive is now required to reshape the business and allow the family directors to revert to their past technical and sales roles.

The stock market has understandably given up on the business, as the 37p shares now trade below the 43p per share net tangible asset value. However, October’s Q3 update did indicate a stronger H2 versus H1 and even declared the missing H1 dividend. Various R&D projects that offer “transformational” potential may prove valuable during the next few years, too.

I paid 45p for MCON during 2015 and for now my regular blog coverage has ceased.

My MCON buy report | All my MCON posts

Summary

Last year I stuck with all ten of my shares and the holdings mostly exhibit the traits outlined in How I Invest:

- Capable, owner-aligned management;

- Attractive accounts;

- Respectable track records, and;

- Reasonable prospects.

The plan for 2025?

I am hopeful my returns can remain positive as a mix of savvy boardrooms, market-leading products and conservative balance sheets help my portfolio cope with a UK economy saddled with profligate public spending, a ballooning regulatory burden, flat-lining labour productivity and now last year’s Budget.

Seven of my ten holdings earn considerable revenue from overseas, which may — or may not! — prove useful during the coming year and beyond.

My portfolio is presently 95% invested, and the potential top-up candidates for the remaining 5% are ASY, BVXP, CLIG, MTVW, SUS, TFW and WINK. Given my relatively small cash position, I would ideally like to buy at bargain prices to make my final purchases really count.

My ShareScope articles could of course identify a suitable alternative, but I have not bought a new share since 2017 and now far prefer to buy more of the companies I already own.

I trust you found this annual review informative. I certainly found it useful to write.

Please click here to examine my portfolio’s 2024 performance in more detail.

Until next time, I wish you safe and healthy investing!

Maynard Paton

Hi Maynard, thanks for an informative write up as ever and well done on an excellent performance. Just curious on why you will look to add to existing positons rather than add new ones. Is it a lack of the type of small owner operated company you like on the UK market, a lack of time to research, a lack of funds to make a meaningful opening position or some combination of the above?

Also sorry to hear about your health concerns. As ever I’m reminded that ‘your health is your wealth’. Hope it is manageable for you at this stage.

Hi Paul

Thanks for the message. Preferring to add to existing positions has been prompted by my liking to go a bit deeper with my research, which helps me build conviction to hold larger positions but also creates a lack of time looking at different shares. To diverge from the market (both ways!) I believe larger positions are the way to go. The theory is I should be able to spot better buying opportunities in the shares I already hold (after following them for years) versus new shares. I have held all my shares for 8 years now and I continue to discover things I did not know about them. But I do have a few decent names on the watch list that I may one day introduce to my portfolio. One difficulty is buying some of them in any great size — I don’t want new positions to be small and not have any real influence on my overall return. I appreciate your ‘health is your wealth’ comment — my wife’s health is not great, but thankfully is manageable.

Maynard