14 December 2021

By Maynard Paton

Results summary for FW Thorpe (TFW):

- A remarkable recovery following a factory fire ensured a satisfactory FY 2021, which included a record H2 and a special payout to complement the 19th consecutive annual dividend lift.

- Customers seeking “tried and tested” manufactures alongside ongoing demand for SmartScan counterbalanced component shortages, the pandemic and Brexit.

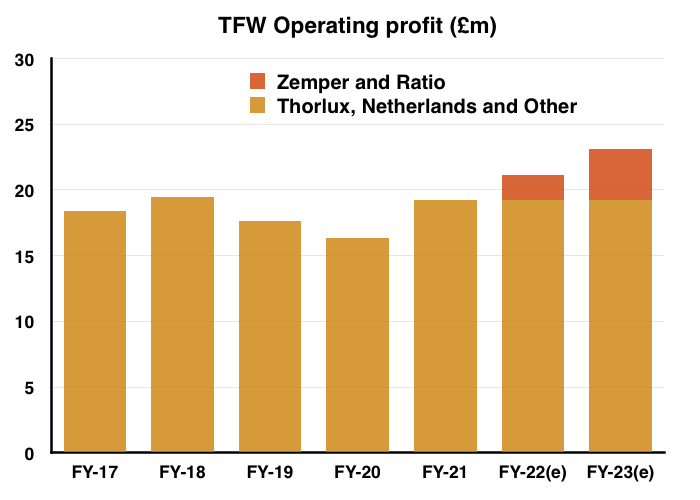

- £27m spent on new acquisitions has underlined TFW’s expansion ambitions and signals a firm desire to earn greater returns on the group’s £76m cash hoard.

- The accounts remains in good shape, although the record 47% gross margin may be short lived if supply difficulties and rising costs continue.

- A P/E of 30 feels generous, but might reflect operational reliability, a positive ‘buy and build’ strategy, significant ‘ESG’ attractions and/or potential growth beyond lighting systems. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own TFW

- Results summary

- Revenue, profit and dividend

- Thorlux and Smartscan

- Netherlands

- Recent acquisitions

- Other companies

- Financials

- Valuation

Event links, share data and disclosure

Events: Annual report for the twelve months to 30 June 2021 published 05 October 2021, Zemper acquisition published 04 October 2021, AGM statement published 18 November 2021 and Ratio acquisition published 02 December 2021

Price: 450p

Shares in issue: 117,004,508

Market capitalisation: £527m

Disclosure: Maynard owns shares in FW Thorpe. This blog post contains SharePad affiliate links.

Why I own TFW

- Manufactures commercial lighting systems with a long-established reputation for high product quality, leading technical innovation and first-class customer service.

- Board led by a veteran executive and assisted by family non-execs who steward a 45%-plus/£239m-plus shareholding.

- Conservative accounts showcase enormous cash reserves, zero bank debt, substantial freehold property, consistent working-capital management and illustrious dividend.

Further reading: My TFW Buy report | All my TFW posts | TFW website

Results summary

Revenue, profit and dividend

- A “resilient” H1 performance that was disrupted by Covid-19, Brexit and a factory fire but also carried this optimistic outlook…

“Supported by the Group’s healthy order book, I foresee a steady second-half performance better than expected at the start of the pandemic.“

- …had already suggested TFW’s FY 2021 outcome would be satisfactory in the circumstances.

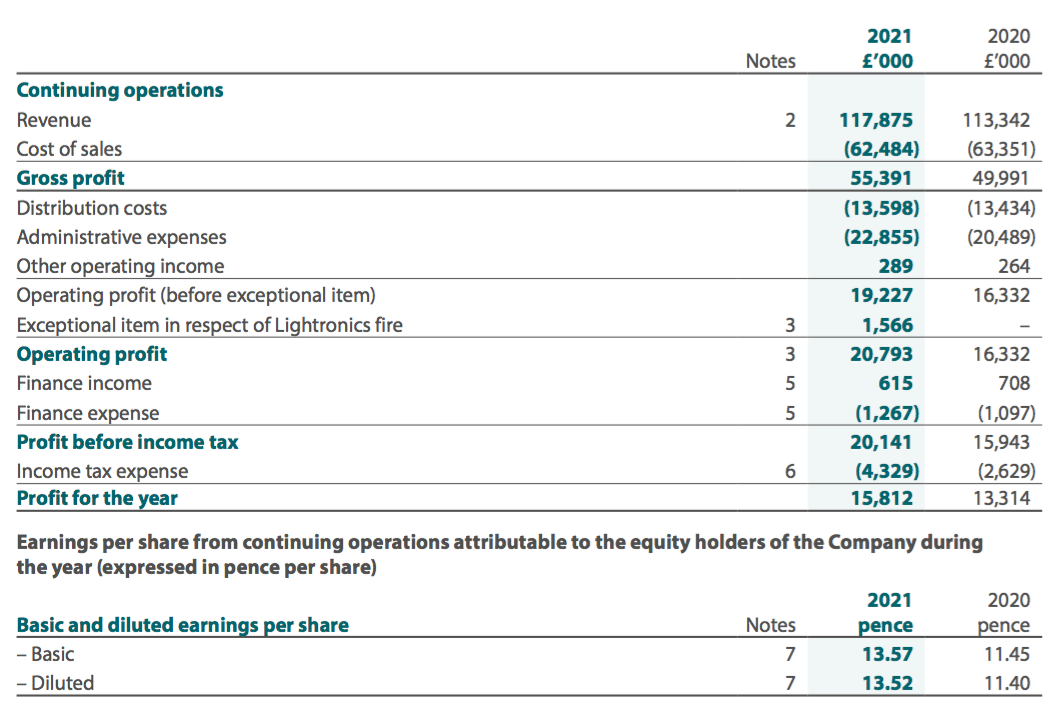

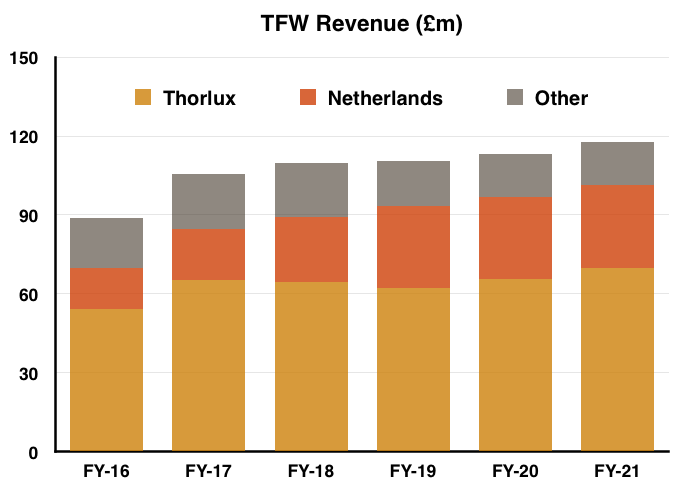

- Full-year revenue gained 4% to £118m and set a new all-time high for the eighth consecutive year:

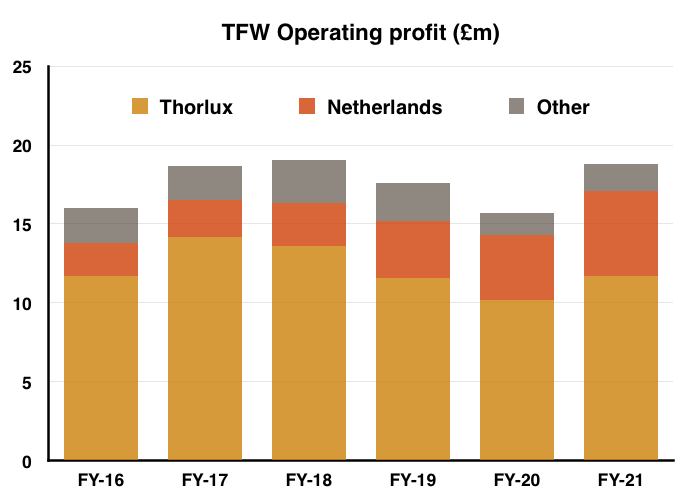

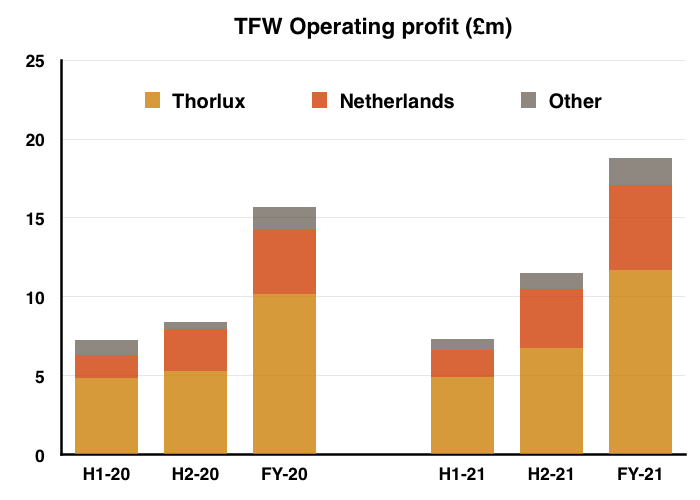

- Assisted by a remarkable performance from the group’s Netherlands division (see Netherlands), full-year operating profit rebounded 18% to £19m to almost surpass the record set during FY 2018:

- TFW believed the positive trading was supported in part by the group’s product quality:

“Orders have certainly held up better than expected; within the Group, we believe that during uncertainty customers have been less inclined to take chances with lesser known brands and have stuck with tried and tested and more local manufacturers.“

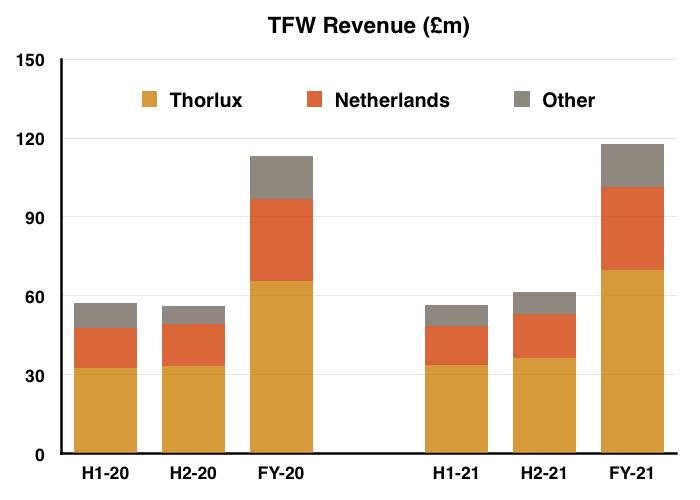

- The H2 performance was in fact TFW’s best ever, with H2 revenue up 10% on H2 2020 (and up 6% on H2 2019)…

- …and H2 operating profit up 31% on H2 2020 (and up 9% on H2 2019):

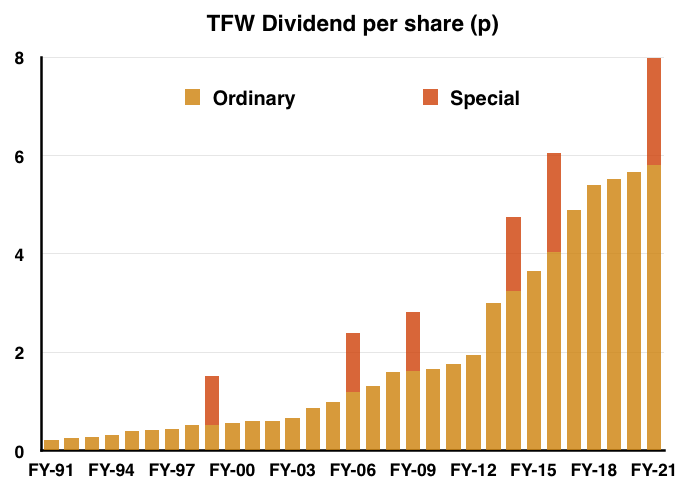

- TFW once again said its “robust” balance sheet and “strong” cash flow justified a dividend improvement, with the final payout lifted 2.6% versus 2.0% for H1.

- TFW has now raised its annual dividend for 19 consecutive years:

- The payout has not been cut since at least 1991.

- A results highlight was the declaration of a special dividend, the sixth such one-off payout since FY 1999, and which amounted to 2.2p per share.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

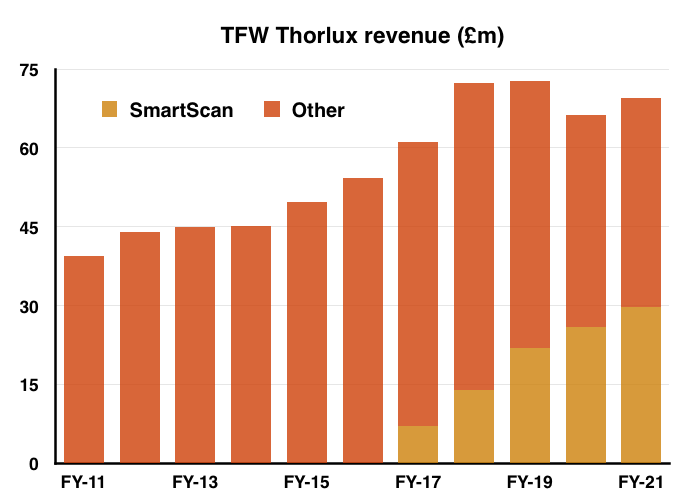

Thorlux and Smartscan

- Thorlux is TFW’s largest division and represents approximately 60% of the group.

- Thorlux manufactures a wide range of commercial lighting equipment:

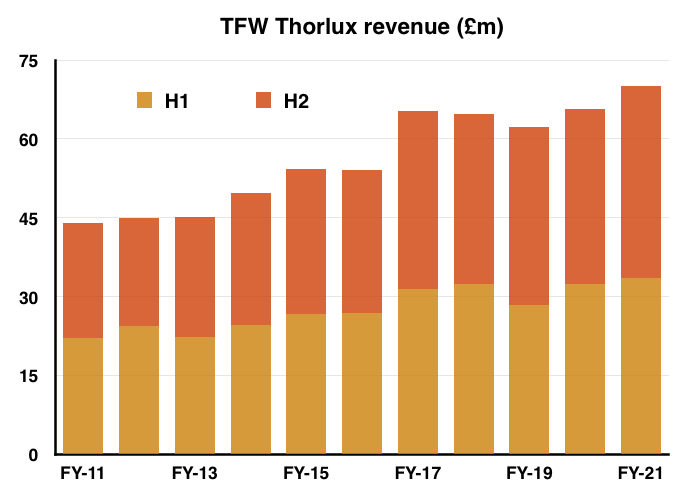

- Thorlux reported full-year revenue up 7%, with H2 revenue up 10%:

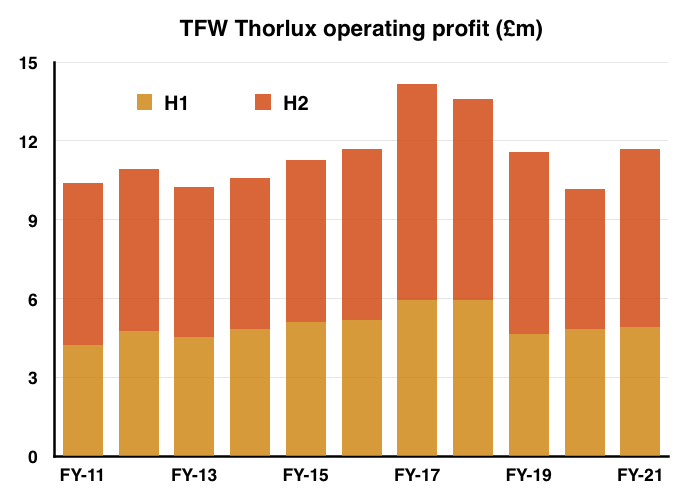

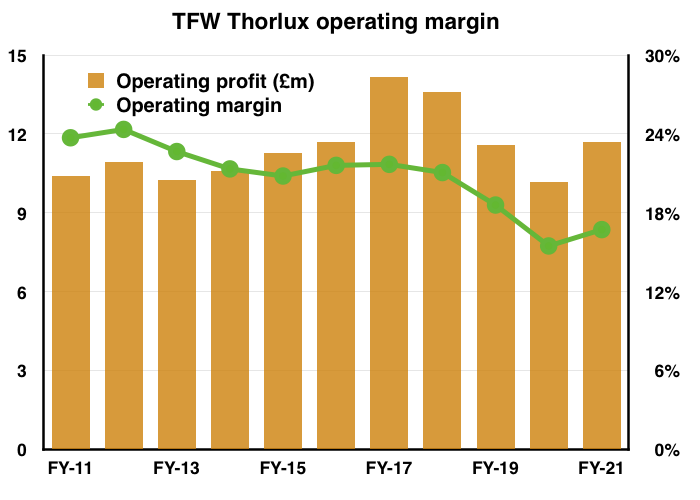

- Full-year profit gained 15%, with H2 profit advancing 28%:

- The profit chart above shows mixed longer-term progress.

- Divisional profit has not recovered to the level enjoyed during the LED boom a few years ago, and is only 10% higher than the level witnessed a decade ago.

- …but the SmartScan product is by far the division’s largest recent success.

- Launched during FY 2016, SmartScan is described as a “revolutionary wireless lighting control system” and provides customers with energy reports, emergency lighting tests, “occupancy profiling” information and even air-quality data:

- The United Lincolnshire Hospitals NHS Trust is a SmartScan customer. The 2021 annual report disclosed the Trust enjoying a 91% energy saving after installation:

“This recommendation was based on installing the Thorlux SmartScan monitoring and management system, which incorporates Smart intelligent lighting control. Integral Smart sensors monitor ambient light and presence, and control output to the correct level; they dim and switch when there is sufficient daylight, and illuminate only when the area is occupied.

Thorlux SmartScan luminaires have delivered a 91% energy saving compared withthe previous lighting installation, resulting in electrical operating savings of £398,570 per annum.“

- The case study also implied the cost of installation may have been £2.6m:

“The Trust received a grant from the National Energy Efficiency Fund for £2.6 million, enabling the replacement of around 12,000 light fittings with modern LED fittings with smart technology that means lights turn off after a period of inactivity, saving energy and money for the Trust.”

- Saving £400k annually from an initial £2.6m investment equates to a 6.5-year payback.

- TFW is upgrading the SmartScan system to shorten the payback time:

“Later in the year, Thorlux will release the second generation of SmartScan… will be faster and smarter, and importantly will provide more data and analytics for customers to use in new ways to help streamline their operations, using the Group’s luminaires as a method of collecting and transporting information.

Investments this year in new improved electronics, especially but not limited to those for outdoor areas, have brought cost downs, enabling customers to achieve paybacks in shorter times.“

- Revenue from SmartScan has soared since the product was launched during FY 2016:

- Note that the chart above may not be entirely accurate.

- SmartScan systems are now sold through TFW’s Dutch division (see Netherlands) and, unlike previous years, TFW did not disclose a specific Smartscan revenue figure for FY 2021. TFW instead stated:

“SmartScan continues to deliver, with revenues growing significantly again this year. “

- My chart above assumes SmartScan replicated the £3.9m revenue increase reported for FY 2020 for FY 2021, which would take annual SmartScan revenue to almost £30m.

- Also consider how revenue now attributed to SmartScan may have otherwise been attributed to other products. Non-SmartScan revenue within Thorlux during FY 2021 was lower than Thorlux’s pre-SmartScan revenue between FYs 2012 and 2016.

- The greater popularity of SmartScan has coincided with Thorlux’s margin declining:

- Thorlux’s margin has reduced from 24% to 17% during the last ten years and whether that decline is due to SmartScan development costs, pressure on pricing or something else has not really been made clear.

- TFW has cited Thorlux’s lighting “services” for lower margins…

“Revenue continues to be supported by growth in services; however, £2.2m of revenue from services earned lower margins than lighting sales and had a dilutive impact on operating results. Providing surveying, project management and installation services does, however, augment the ability of Thorlux to secure significant-value product orders which in turn provide characteristic margin levels. “

- …although the small revenue involved does not quite explain the longer-term margin reduction.

- At least Thorlux’s immediate outlook seemed positive:

“Thorlux starts 2021/22 with a significant order book and the opportunity to secure further large scale orders. Continuing to target specific sectors and territories will be crucial to ongoing success.“

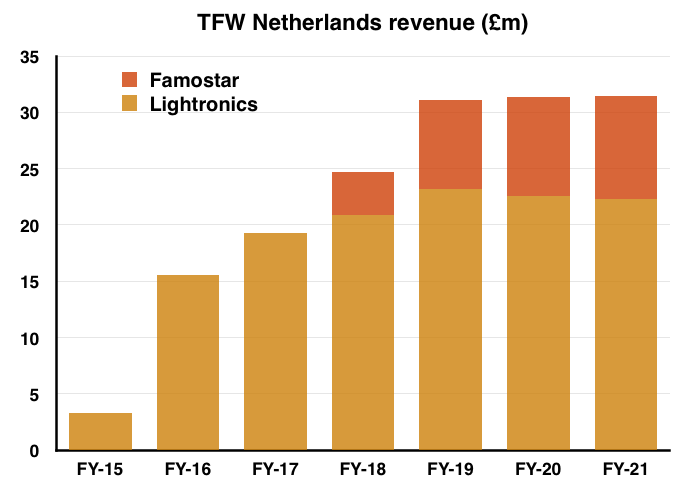

Netherlands

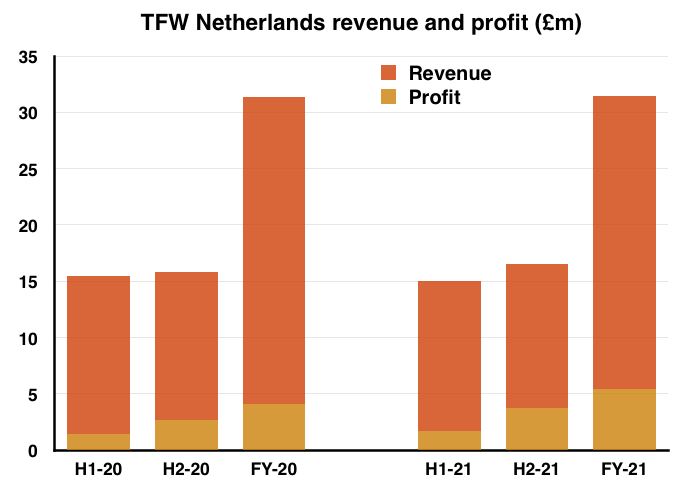

- TFW’s Dutch businesses — Lightronics and Famostar — represent approximately 27% of the group.

- Lightronics was acquired during FY 2015 for an initial £8.3m that included a £1.9m debt repayment. Lightronics manufactures mostly street lighting, and annual sales were £10.9m and profit was £1.2m at the time of purchase.

- Famostar was acquired during FY 2018 for an initial £6.3m. Famostar manufactures mostly emergency lighting, and annual sales were approximately £6.7m and profit was approximately £1.1m at the time of purchase.

- The charts below show their collective revenue and profit contributions to the group:

- Both Lightronics and Famostar appear to have flourished under TFW’s ownership.

- Aggregate Lightronics/Famostar revenue reached £31m for FY 2021 versus less than a combined £18m at the time of their purchases.

- Aggregate Lightronics/Famostar operating profit meanwhile reached £5.4m for FY 2021 versus a combined £2.3m at the time of their purchases.

- TFW has enjoyed a very satisfactory return from its Dutch operations.

- TFW effectively bought an initial 65% of both Lightronics and Famostar and these FY 2021 results confirmed the earn-out for the 35% balances would total £16.6m:

- The overall amount to acquire Lightronics and Famostar is therefore £8.3m + £6.3m + £16.6m = £31.2m.

- Dutch FY 2021 operating profit of £5.4m less 25% standard Dutch tax gives Dutch earnings of approximately £4m.

- Earnings of £4m from a total £31.2m investment gives a 13% return.

- However, the initial 65% Lightronics and Famostar stakes purchased for a combined £14.6m would now be returning £2.6m (65% of £4m earnings), or 18% of that £14.6m.

- What’s more, TFW has paid total dividends of £4.9m on the 35% balances between FYs 2016 and 2021…

- …which implies TFW has retained Dutch dividends of approximately £9.1m from its 65% stakes.

- Account for these dividends of £9m that TFW received before paying the 35% earn-outs, and the net Dutch investment would be £8.3m + £6.3m – £9.1m + £16.6m = £22.1m.

- Overall FY 2021 Dutch earnings of £4m on a net £22.1m investment = 18%.

- Enjoying a return of 13%, 18% or somewhere in between has prompted further European purchases (see Recent acquisitions)

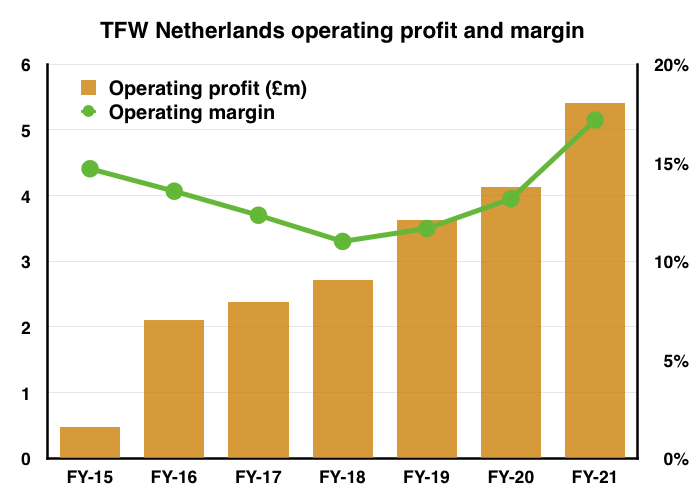

- The FY 2021 performance of the Netherlands division was extremely impressive given Lightronics suffered a fire during H1:

- The 2021 annual report disclosed operations resumed in temporary facilities the next day:

“Fortunately, there was a limited impact on stock, which enabled the rapid resumption of production. With the support of the Group, Lightronics secured a temporary facility and assembly began within 24 hours of the fire, with production lines set up for street and area luminaires as well as tunnel lighting. The sales team contacted customers regarding the status of current orders, the majority of which were still delivered on time.“

- The 2021 annual report also quoted Jos Spapens, managing director of Lightronics:

“The fire at Lightronics on 23 September was, of course, a terrible disaster. At that moment we could have done one of two things: either sat down and done nothing or put our shoulders to the wheel and given it 100%. We did the latter.

We no longer looked back at what had been, but forward to the future. Thanks to this spirit from the entire team we were back to full production by the beginning of November and all the backlog was cleared by the end of November. We did all this during a coronavirus crisis, and I am incredibly proud of my team.”

“I am surprised a Dutch managing director has not been appointed to the main board (point 14).”

- The size of the Dutch division alongside the extremely commendable post-fire recovery surely merit Mr Spapens a promotion to the group board.

- Although Dutch revenue for the year remained flat, operating profit jumped a super 31% with a 40% surge reported for H2.

- The profit gain led to the division’s operating margin rising from 13% to 17% for the year, with a lovely 22% reported for H2.

- TFW did not really explain the division’s margin improvement other than to state “material cost reductions“.

- The divisional outlook appears bright, with expansion plans at both subsidiaries:

“Plans for the new [Lightronics] building, which will have around 75% more manufacturing space than the previous unit, have received planning consent, and construction will commence shortly…

Famostar, too, is actively developing its site for future expansion, with a greater warehouse area planned and plans generally for a larger operation in the future.”

Quality UK investment discussion at Quidisq. Visit forum.

Recent acquisitions

- The apparent success of TFW’s Lightronics and Famostar purchases has prompted two further European deals.

- TFW announced the purchase of Spanish lighting group Zemper during October and then announced the purchase of Dutch firm Ratio, which develops electric-vehicle charging systems, during December.

- The Zemper deal is by far TFW’s largest, with €24.5m (£21.1m) spent to acquire a 63% share that included certain additional assets worth €4.2m (£3.6m).

- For perspective, the initial £21.1m payment exceeded TFW’s entire FY 2021 operating profit of £19.2m.

- TFW said:

“Zemper has a complete range of emergency lighting, an area of business well liked by FW Thorpe for being somewhat niche and specialised.”

- The “somewhat niche and specialised” business is reflected by Zemper being able to convert its FY 2021 revenue of €20.3m into operating profit of €3.8m — a margin of 19%.

- The deal terms appear to value 100% of Zemper at approximately €36m (£31m), which is equivalent to 10x Zemper’s operating profit.

- TFW also paid an initial c10x operating profit multiple for the combined Lightronics and Famostar.

- Zemper employs 120 people, which equates to c€169k revenue per head and compares with €250k-300k at Lightronics and Famostar at their respective times of purchase.

- I get the impression Zemper’s 19% margin is due in part to employing many lower-paid staff, who I suppose could be called upon to reduce the costs of TFW’s other divisions. TFW’s revenue per employee was £169k (c€200k) for FY 2021.

- The operating logic behind the Zemper deal — to extend the group’s emergency-lighting offering — is more straightforward than the rationale for the Ratio acquisition.

- Ratio will widen TFW’s product range beyond lighting into electric-vehicle charging:

“FW Thorpe’s know-how in electrical engineering, manufacturing and lighting, combined with Ratio’s experience in electrical vehicle charging will allow the introduction of new products into the UK market as well as supporting growth in Ratio’s existing markets.

We see similarities in technology and engineering skills, giving the Group the opportunity to diversify into new areas of engineering with high growth potential.“

- TFW has paid €6.8m (£5.8m) for a 50% share of Ratio. TFW expects Ratio to deliver 2021 revenue of €8m and a profit “in keeping with Group operating profit levels”.

- The absence of a specific profit figure for Ratio contrasts with profit figures disclosed when TFW announced the purchases of Lightronics, Famostar and Zemper .

- TFW said the Ratio acquisition was “expected to enhance earnings per share in the financial year ending 30 June 2023“.

- However, TFW said the Zemper acquisition was “expected to enhance earnings per share in the financial year ending 30 June 2022“.

- I therefore get the impression Ratio may not be that profitable during the current FY 2022.

- Whether the move into electric-vehicle charging generates returns akin to those sported by Lightronics and Famostar remains to be seen.

- But what is becoming clear is TFW’s desire to expand beyond the UK through notable acquisitions.

- During the 20 or so years prior to buying Lightronics, TFW’s acquisition accomplishments were limited to purchasing a handful of smaller UK lighting firms for an approximate £5m total.

- In contrast, total expenditure acquiring 100% of Lightronics, Famostar, Zemper and Ratio seems set to approach £75m.

- The acquisition strategy certainly explains how TFW will use its sizeable cash position (see Financials).

- I have typically viewed acquisitive companies with suspicion. Common growth-by-acquisition risks include overpaying, integration problems and ‘diworsification’.

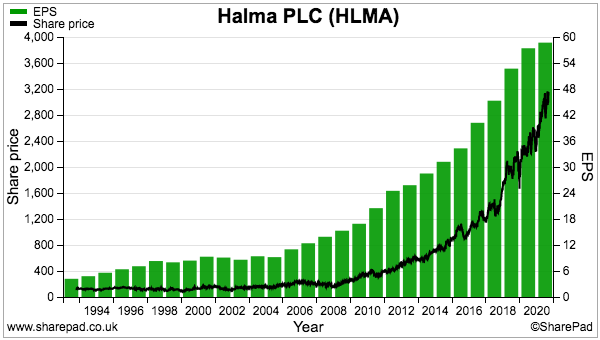

- But some companies can make acquisitions really work. Halma (HLMA) is the textbook example, where acquisitive success over 50 years has boiled down to the acquired companies being:

- Paid for by internally generated cash;

- A replica of a subsidiary already owned by the group;

- A bolt-on or quasi-bolt-on (i.e. a purchase that can operate on a standalone basis), and;

- Likely to improve the quality as well as the quantity of earnings.

- I am hopeful TFW can follow HLMA’s growth-by-acquisition template for creating shareholder value:

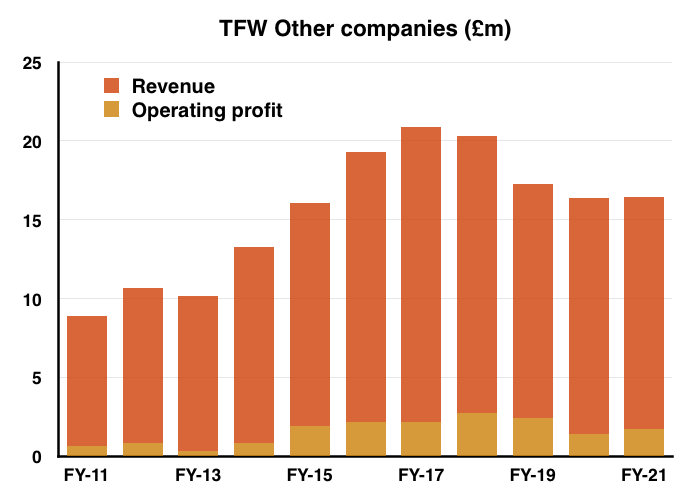

Other companies

- The European acquisition strategy will diminish the influence of TFW’s Other companies within the group.

- TFW’s Other companies consist of:

- TRT Lighting, which was launched during FY 2012 and supplies lighting for road tunnels;

- Philip Payne, Solite and Portland, which supply emergency lighting, cleanroom lighting and shop lighting respectively, and;

- A trio of overseas Thorlux offices.

- Together they represented 14% of group revenue and 9% of group profit during FY 2021.

- The collective long-term performance of the Other companies has been mixed.

- By far the best performing Other company is TRT Lighting, which has gone from nothing to sales of £10m during the last nine years.

- Philip Payne, Solite, Portland and the overseas Thorlux offices therefore look to have — at best — collectively stagnated during the same nine years.

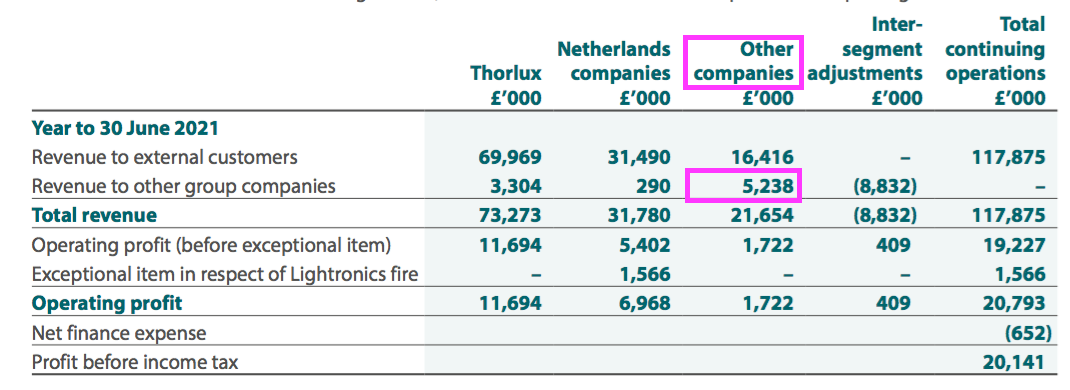

- However, the 2021 annual report reveals the Other companies do support the main Thorlux and Dutch divisions. Products from TRT and the rest worth £5m were sold onto other parts of the group during FY 2021:

Financials

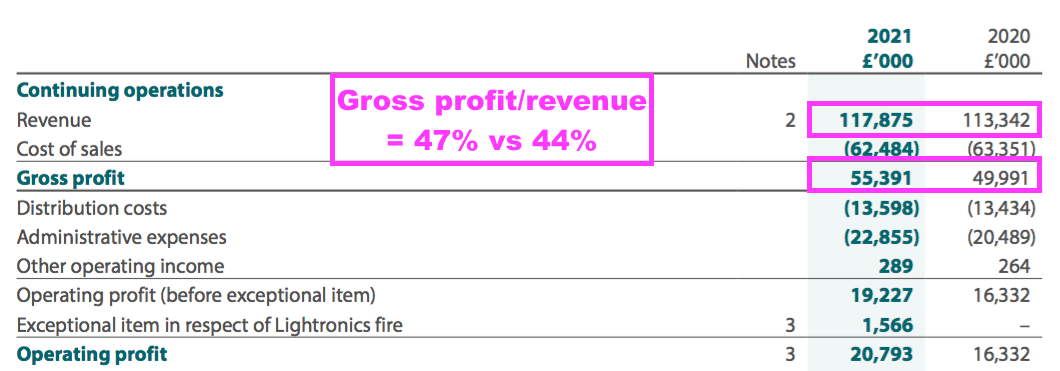

- TFW’s accounts remain in good shape.

- The aforementioned operating margin improvement was achieved by lifting the gross margin from 44% to a new 47% record:

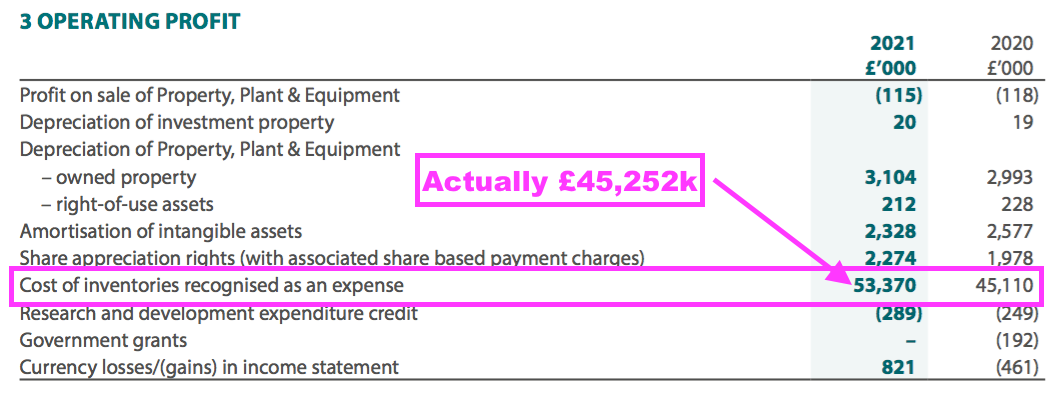

- A higher gross margin can be achieved by selling lower-cost stock, although very oddly the accounts showed the cost of the stock sold was up 18% to £53,370k when revenue was up only 4%:

- TFW has confirmed to me the £53,370k includes inter-company transactions and the correct figure for FY 2021 (i.e. net of inter-company transactions) is in fact £45,252k.

- The £45,252k cost of stock sold represents 38.4% of revenue, the lowest proportion for at least ten years.

- I get the impression TFW acquired cheap stock during the early stages of the pandemic, although sourcing cheap stock at present may not be as easy (see below).

- The group’s operating margin has not quite recovered to the 17-18% level of a few years ago and the 20%-plus level enjoyed between FYs 2008 and 2012.

| Year to 30 June | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating margin (%) | 17.2 | 17.5 | 15.7 | 14.2 | 16.1 |

| Return on average equity (%) | 15.1 | 15.1 | 13.8 | 10.6 | 11.9 |

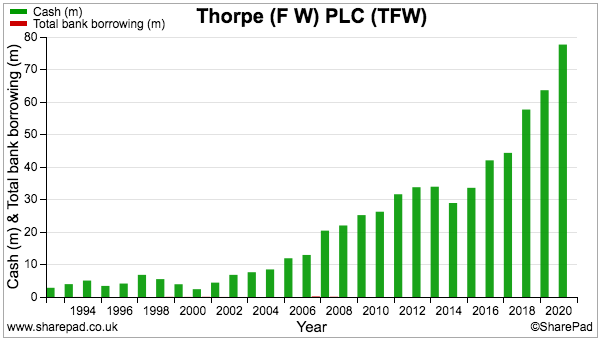

- Return on average equity remains at modest levels, although influencing the calculation is TFW’s surging cash pile on which trivial interest is earned:

- The £76m year-end cash position represented a hefty 55% of TFW’s £137m net asset value.

- The £76m has since been reduced to approximately £33m after paying:

- £16.6m to settle the Lightronics/Famostar earn-out;

- £21.1m for 63% of Zemper, and;

- £5.8m for 50% of Ratio.

- The earnings to be generated from the £27m spent on Zemper and Ratio ought to improve the group’s return on equity for FY 2022 and beyond.

- Given the size of the Zemper and Ratio deals and TFW seemingly committing to a European acquisition strategy, corporate activity will most likely dictate future returns on retained profit.

- Demands on cash flow remain very acceptable:

| Year to 30 June | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating profit (£k) | 18,422 | 19,466 | 17,649 | 16,332 | 19,227 |

| Depreciation and amortisation (£k) | 3,999 | 4,595 | 5,022 | 5,817 | 5,664 |

| Cash capital expenditure (£k) | (7,286) | (7,819) | (5,473) | (8,495) | (4,398) |

| Working-capital movement (£k) | 1 | (241) | 2,234 | 627 | (1,445) |

| Cash (£k) | 41,659 | 43,958 | 57,290 | 63,002 | 75,871 |

- The £8m difference between five-year net capital expenditure of £33m and five-year depreciation and amortisation of £25m can be explained by TFW’s purchases of extra freehold property.

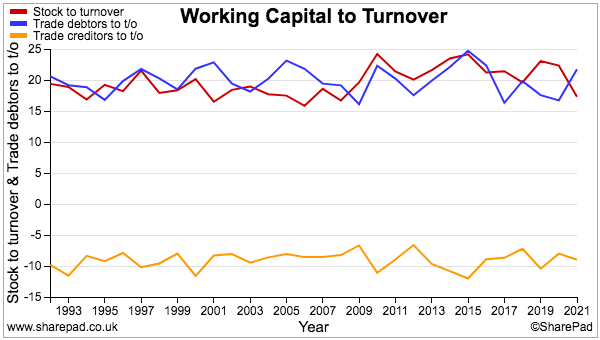

- Working-capital movements look under good control, with a net £1m extracted from stock, debtors and creditors since FY 2017.

- FY 2021 cash flow was in part bolstered by reduced stock buying caused by component shortages:

“All companies are dealing with severe shortages and rising costs for many of the basic components necessary for making Group luminaires, such as steel, plastics, cardboard, electronic components and microchips. Although the Group has a strong cash position and can afford to stock up, the reality is that this has not been possible and stocks have reduced“

- Component shortages and rising costs could mean the aforementioned gross-margin improvement to 47% is short lived.

- Stock levels at £20.4m were the lowest since FY 2016 and, at 17.3%, were the lowest proportion of revenue since FY 2008 (16.7%).

- The stock situation may in time prove to be a blip. Longer-term working-capital management has been reasonably consistent:

- Cash flow was assisted by a net £1.8m insurance payment relating to the Lightronics fire.

- Free cash flow of nearly £21m funded dividends of almost £7m and left approximately £13m to be added to the cash position.

- Other balance-sheet assets include investment property of £2m, loan notes of more than £2m plus an equity portfolio and associate investment with a combined £4m value.

- Bank debt remains at zero.

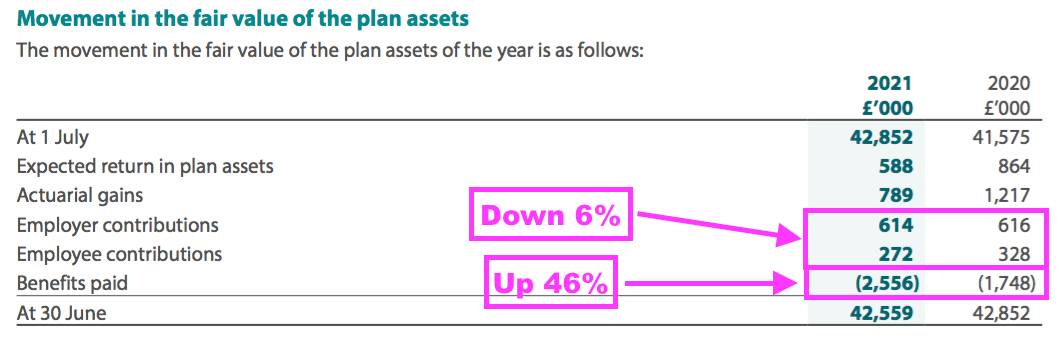

- A pension surplus of £2m does not appear troublesome, although scheme benefits jumped 46% while contributions dropped 6%:

- If the cash position does fall to my estimated £33m following all the acquisition expenditure, it will represent approximately 28% of FY 2021 revenue — the lowest cash-to-revenue proportion since FY 2007.

- TFW operates with a high cash balance in part to reassure customers that help will always be forthcoming if product problems arise. The 2021 annual report states:

“Customers come to us for peace of mind. They want the correct technical solution, professional service, sustainability of products/services and the ability to provide support during a product’s warrantable life and beyond.

Our business model is focused on the needs of customers and the marketplace, with a robust capital structure that underpins our ability to deliver sustainable growth, innovative products and excellent customer service.“

- The 2.2p per share special dividend will cost £2.6m and will not make a great dent in the cash position.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- TFW’s outlook felt positive, albeit with acknowledgement of the present trading environment:

“Within the Group we have once again started the new financial year with a very strong order book, exceeding our expectations in most companies, especially Thorlux Lighting, and we look forward to more normal trading conditions returning soon.”

“Whilst still carrying some increased manufacturing costs, all companies are capable of producing increased revenue in the coming year.

There remain some difficulties, though, caused by component supply shortages, some capacity restraints and ongoing COVID-related disruption.”

- Last month’s AGM reiterated the mix of good customer demand and limited component supplies:

“Since the beginning of the new financial year the Group has experienced the usual ups and downs across its different businesses. Overall, revenue is marginally ahead with orders up more significantly compared to the same period last year.

Our manufacturing continues to suffer from supply shortages and logistical complications, especially related to electronic components and LED drivers. These shortages are currently hampering our ability to lift revenues to a higher level with some factories not able to operate at optimum output.

The sales order performance suggests our Group as a whole, and the market, is in good shape. We need to see material supply conditions stabilise to enable further improvement on last year’s financial achievements.“

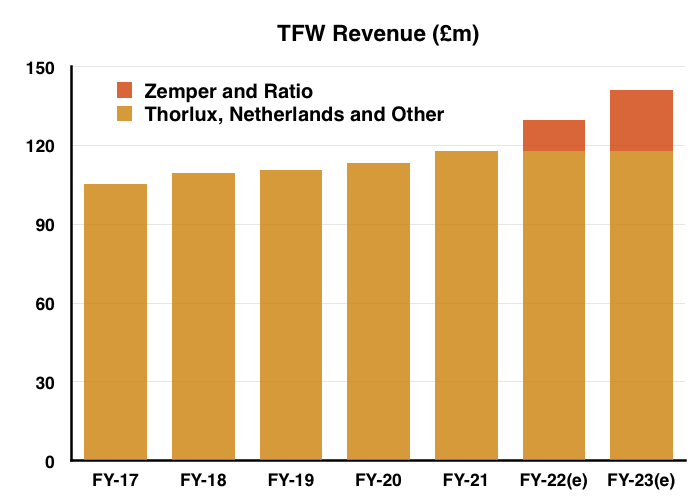

- Assuming the FY 2021 performance is sustained, 100% ownership of the Zemper and Ratio acquisitions ought to support group revenue of £141 million…

- …and a group operating profit of £23m by FY 2023 (assuming a 10% margin for Ratio):

- Applying the forthcoming 25% UK tax rate then gives earnings of £17m or 14.8p per share.

- The implied 30x rating at 450p appears generous given the modest progress during recent years.

- Perhaps investors are willing to apply a premium multiple because of TFW’s:

- Operating resilience displayed during the pandemic;

- Positive comments about current trading, and/or;

- Fast-growing SmartScan service and the revenue opportunity beyond traditional lighting systems.

- Another reason could be the European acquisition strategy and some sort of HLMA-type ‘buy and build’ ambition.

- Then there is also the environmental angle. TFW said:

“More and more of the Group’s customers demand solutions that are kind to the environment – good news for local manufacturing wherever possible.”

- TFW customers may even include fellow portfolio members Andrews Sykes (point 12) and Mountview Estates (point 5), which have both cited plans to use energy-efficient lighting.

- TFW has arguably been an environmental pioneer. In particular, Thorlux devised a carbon-offsetting scheme during 2009 that has since involved planting approximately 150,000 trees in Monmouthshire.

- TFW showcased the tree scheme on the front and back cover of its 2021 annual report:

- Such ‘green’ credentials and the present enthusiasm for ‘ESG’ investing may have therefore put TFW on many investors’ radars.

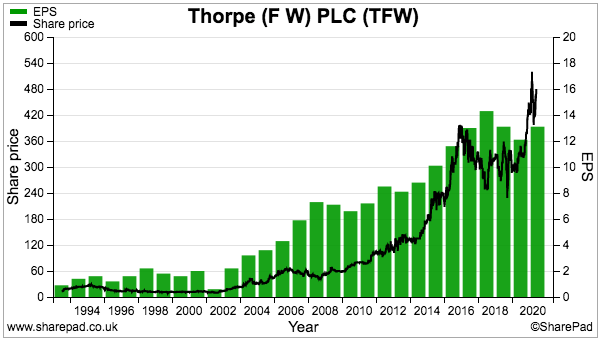

- The present rating contrasts starkly to that seen when I started buying TFW during 2010 at 68p. Back then the £81m market cap traded at 10x earnings of £8m and was 30% supported by net cash of £25m.

- The dividend yield back in 2010 was 2.4%, but the current 5.8p per share ordinary payout provides a 1.3% income at 450p.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Thx for another enjoyable article. Focusing just on the negatives for the sake of brevity; after reading I have a feeling of FW buying growth. Halma, Judges, Bunzl etc have excelled in doing just this, but they are exceptions rather than the rule, I am also wary of acquisitions outside a field of competence. Ratio 50% purchase is thematic (energy ESG) and related (electronics) but the overlaps are loose with lighting. Further, lack of earnings data and FY23 to be eps accretive suggest that this is unlike FW’s previous, slim acquisition record. Electric charging is zeitgeisty too, but margins are relatively unknown.

FW kind of stagnating since end of 2017 while generating lots of cash, the temptation to spend to grow is there, I feel that they are giving in to that temptation but have yet to articulate the strategy re management structure to accommodate a larger, increasingly european business which will span, what I imagine to be, two very different sectors. The other options are buybacks (less attractive given liquidity and large family holding), larger special divs and/or foothold acquisitions. Zemper fits the fill, Ratio less so, neither are large purchases but acquisitions have been much more rapid than in previous years.

Thx again for your articles, some of the best content on investing around imo.

Hi Michael,

Thanks for the message and I am glad you found the blog useful. All good points on the acquisitions, and Halma etc are indeed exceptions. You are right that management structure will have to be looked at; the current executives include the MD for one of the smaller ‘Other’ UK businesses, the board relevance of whom is not obvious to me. Buybacks are very unlikely as the DTR rules (I think) instruct any 30%+ holders to table a bid if their percentage holding increases (the Thorpe family concert party own 30%+). TFW struggled to grow overseas sales organically, so purchased the two Dutch businesses a few years ago and they seemed to do well. So at present I am minded to give the acquisition strategy the benefit of the doubt. The shift into electric-car charging offers the risk of pumping a lot of extra cash into a product development race in which TFW does not succeed, but also the reward of success and the growth opportunities that should follow. We can only wait and see what occurs.

Maynard

FW Thorpe (TFW)

Publication of 2021 annual report

Here are the points of interest:

1) MARKETPLACE

The same five questions were asked within this 2021 report as the 2020 annual report, but slightly different answers were given this time with less conviction about particular sectors.

For example:

“Q: Which market sectors are growing?

A: There is growth in a number of areas that continues to justify our investment in business development.”

But for 2020:

“Q: Which market sectors are growing?

A: The main growth areas have been healthcare and rail. This continues to justify our investment in business development for these areas.”

Another example:

“Q: Which sectors are you focusing on?

A: Our product and solution portfolio continues to evolve and can cater for a variety of different sectors. We continue to focus on specific sectors that are investing but with some renewed endeavour on those that have reduced in previous years.”

But for 2020:

“Q: Which sectors are you focusing on?

A: Our product and solution portfolio continues to evolve and can cater for a variety of different sectors. We continue to focus on the healthcare, logistics and retail sectors but with some renewed endeavour on education.”

Also, further text changes within the “International economic conditions” section no longer referred to specific sectors:

For 2021:

* Certain sectors will continue or potentially increase investment

* Governments have indicated the intention to invest to support economies

* Potential to win market share from competitors who struggle to recover

But for 2020:

* Certain sectors will continue to invest or potentially increase investment – healthcare, logistics are examples

* Government has indicated the intention to invest to support economy – more projects to be given the “green light”

* Potential to acquire competitors who struggle to recover as economies restart

2) BUSINESS MODEL

A repeat of last year’s approach towards product quality, service and longevity:

“Customers come to us for peace of mind. They want the correct technical solution, professional service, sustainability of products/services and the ability to provide support during a product’s warrantable life and beyond.”

TFW’s report commendably provides multiple case studies to underline the qualities of the products and the company.

Following the trend towards greater ESG reporting, this year saw new text concerning the “value generated” for the environment and communities:

Environment

Short-term: Build on the work of many years, delivering energy saving products and continuing our carbon offset programme

Long-term: Develop and implement our sustainability strategy

Communities

Short-term: Employment opportunities and supporting local charities

Long-term: Providing sustainable employment in the local areas where our businesses are located

3) OPERATING PERFORMANCE

A few extra snippets from the divisions.

a) Thorlux

Owning electric vehicles ought to give some insight into the vehicle-charging products developed by recent acquisition Ratio:

“Thorlux has continued its investment in green technologies – for example, in electric vehicles to replace traditional or hybrid technologies and improve the company’s carbon footprint – and this will continue into the next financial year. “

b) TRT Lighting

TRT was the only division among TFW’s Other divisions to record sales growth during 2020 (+14%) and 2021 (+8%), and the omens seem positive for 2023:

“Revenue has been boosted by a large scale tunnel refurbishment project on the M25 motorway and the company’s continued support of large scale rail projects in conjunction with Thorlux. TRT expects further tunnel projects to be given the go- ahead in 2021/22 and demand in street lighting to be maintained.”

4) KEY PERFORMANCE INDICATORS

A new KPI for 2021 befitting the ESG trend: Renewable energy usage:

5) PRINCIPAL RISKS AND UNCERTAINTIES

Nothing of major significance here.

Unlike the 2020 report, the 2021 report did not contain an extensive review of the impact of Covid-19 on the group.

The nine principal risks were not changed from 2020, but two risks — price changes and cyber security — were increased during the year:

The same two risks were increased during 2020, too.

The three risks cited as having a ‘high’ impact on the business remain adverse economic conditions, operational continuity and Covid-19.

6) SUSTAINABILITY

New for the 2021 report are four pages dedicated to sustainability:

Lots of ‘green’ actions were listed, such as “Thorlux has moved from paper to digital installation guides, saving over 1.3 million sheets of paper per annum.

The financial benefits were cited only for solar panels:

“This investment in solar PV panels will enable the Group to generate 40 to 50% of its own electricity usage when the project is completed.

The Group has now installed solar PV units on the roofs of most of its UK manufacturing facilities, as well as at Lightronics in the Netherlands. Further investment will be made in both the UK and Netherlands facilities to reduce consumption from traditional electricity sources.

Any remaining consumption will be delivered from renewal sources from 2022 onwards. Over their operational lifetimes, the installations are expected to deliver a total CO2 reduction of 6,113 tonnes and financial savings of over £2,600,000.”

7) PATENTS

Another 11 patents granted or pending during 2021:

The figure was 11 for 2020 and 12 for 2019.

8) CORPORATE GOVERNANCE

a) Board of directors

The all-male, all-white board may one day require some extra explanation text should new FCA diversity rules ever extend to AIM-traded shares:

As mentioned within the blog post above, I remain baffled as to why there is no Dutch manager on the board (especially when the MD of Philip Payne with sales of just £3m is a board member). And the new MD of Thorlux, TFW’s largest division, is not a board member either.

b) Adherence to QCA code

No changes from 2020, with TFW partially compliant with two of the ten principles. There is no audit committee and no formal board evaluation process. And directors at many other companies retire every year for re-election, too.

“Maintain the Board as a well-functioning, balanced team led by the Chair

The non-executives are not considered fully independent. The Board considers that the non-executive directors are appropriate as they bring significant experience and expertise in the sector. In addition, as the directors retire on a three-year rotation, shareholders have a regular opportunity to ensure that the composition of the Board is in line with their interests.

There is a Remuneration Committee but no Audit Committee, with matters that would normally be tabled at an Audit Committee put to the full Board.”

“Evaluate Board performance based on clear and relevant objectives, seeking continuous improvement

There is no formal evaluation process; however, the Chairman is responsible for Board performance and accordingly actively encourages feedback on the content and function of board meetings.

The composition and succession of the Board are subject to constant review, considering the ever-changing needs of the Group. In addition, the directors retire by rotation every three years giving shareholders the opportunity to ensure that the Board is aligned with their interests.”

Other explanatory text for the partial compliance says:

”The Company continues to be proprietorial in nature and the directors act as a unitary Board and as a consequence are unable to see the benefits of splitting the Board into sub-committees and in particular of constituting audit and nomination committees as matters that would normally be considered by an audit or nomination committee are addressed by the full Board with the non- executive directors present and the auditors attending as appropriate.”

TFW’s track record of dividend increases and resilience during the pandemic suggest the board set-up works relatively well.

c) Director remuneration

No major changes from 2020:

Only JE Thorpe saw his salary increase (from £118k to £140k). Bonuses seem under control, with total bonuses this year at 75% of total salaries versus 65% for 2020.

The report says “The directors’ emoluments exclude contributions to the pension scheme.”

I believe that means the following “pension compensation” is also omitted from the table of emoluments:

“M Allcock, D Taylor and A M Cooper have ceased being active members of the FW Thorpe Retirement Benefits Scheme and C Muncaster has ceased being an active member of his personal pension scheme due to HMRC limits on lifetime allowances and annual contributions.

Subsequently the Company has entered into pension compensation arrangements with these four directors and J E Thorpe to compensate them for the loss of these employer pension contributions. During the financial year the Company paid pension compensation to M Allcock of £169,410 (2020: £167,942), A M Cooper £nil (2020: £7,414), C Muncaster £40,790 (2020: £40,724), D Taylor £19,163 (2020: £19,132) and to J E Thorpe £10,500 (2020: £9,290).”

The executive chairman enjoys a hefty pension compensation package, which when added to his basic salary takes him to £382k a year (albeit unchanged from 2019 and 2020). Note also the executive chairman can receive a two-year payoff rather than the standard one-year payment: “M Allcock has a service contract terminable on two years’ notice.”

And note pensionable pay includes bonuses, which feels generous and not I believe to be standard practice:

“The defined benefit section aims to provide a maximum pension of two-thirds of pensionable salary at normal retirement date. M Allcock’s and D Taylor’s pensionable salary includes an average of the previous three years’ profit bonus. Defined contribution members contribute up to 5% of basic salary and the Company contributes up to 17%.

Director options do not look troublesome at 315,000 with a share count of 119 million. The last options were granted during 2014 and of the five directors to receive options back then, two have since become non-execs and two have since exercised all their options. Another options batch may therefore be forthcoming.

Two-thirds of the remuneration committee is represented by Thorpe family members, who oversee a c45%-plus family shareholding and ought to possess a sensible view on value-for-money executives.

9) INDEPENDENT AUDITORS’ REPORT

Nothing untoward here. A full-scope audit was again undertaken within the three main divisions covering c90% of the wider group. Profit materiality for 2021 was 5% of the year’s profit, rather than taking a three-year average due to Covid:

“An audit was conducted of the complete financial information of the three financially significant reporting units: Thorlux Lighting (the Company, located in the UK), Lightronics and Famostar (both located in the Netherlands). This provided coverage of 89% (2020: 91%) of profit before tax.

Overall group materiality: £929,000 (2020: £860,000) based on 5% of profit before tax excluding the impact of exceptional items.”

Among key audit matters, double-checking the earn-out for the Dutch divisions has been dropped due to the earn-out being calculated formally shortly after year-end:

“Valuation of the share appreciation rights repurchase obligation , which was a key audit matter last year, is no longer included because of the settlement position reached subsequent to the balance sheet date removing the estimation uncertainty over this item. Otherwise, the key audit matters below are consistent with last year.

The remaining key matters — warranty provisions, capitalised development costs and Covid-19 impairments — remained the same.

10) GOING CONCERN

Confirmation TFW could survive a 33% sales drop:

“The directors confirm they are satisfied that the Group and Company have adequate resources, with £52.3m cash and £23.6m short term deposits, to continue in business for the foreseeable future factoring in the expected impact of COVID-19.

They have also produced an analysis that demonstrates that the Group could cover its cash commitments even if there was a reduction of 33% in sales over the following year from approving these accounts. For this reason, they continue to adopt the going concern basis in preparing the accounts.

Mind you, the 2020 accounts said sales could go to zero and the group’s cash commitments would be covered — despite the group having less resources then (£63m) than now (£76m).

11) ACCOUNTING POLICIES

A few reassuring snippets on capital structure:

“The Group’s policy has been to maintain a strong capital basis in order to maintain investor, customer, creditor and market confidence. This sustains future development of the business, safeguarding the Group’s ability to continue as a going concern in order to provide returns for shareholders and benefits for other stakeholders.

The Group has a long-standing policy not to utilise debt within the business, providing a robust capital structure even within the toughest economic conditions.

12) GEOGRAPHIC REVENUE

The UK was the better performer last year:

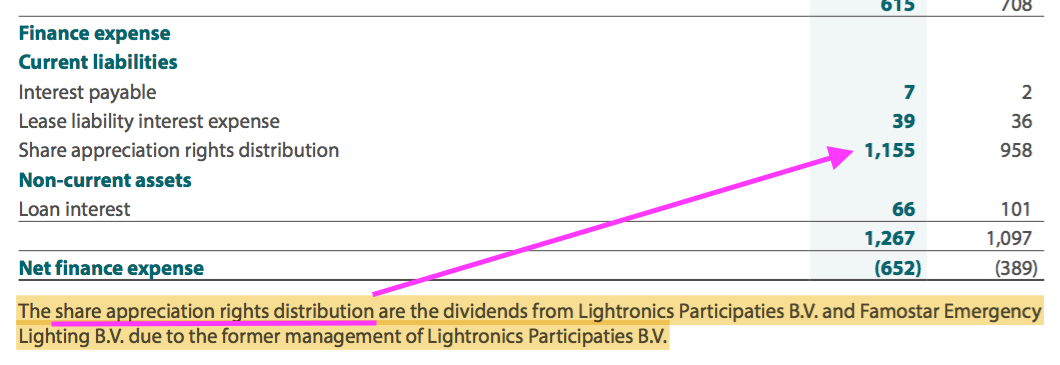

13) SHARE APPRECIATION RIGHTS

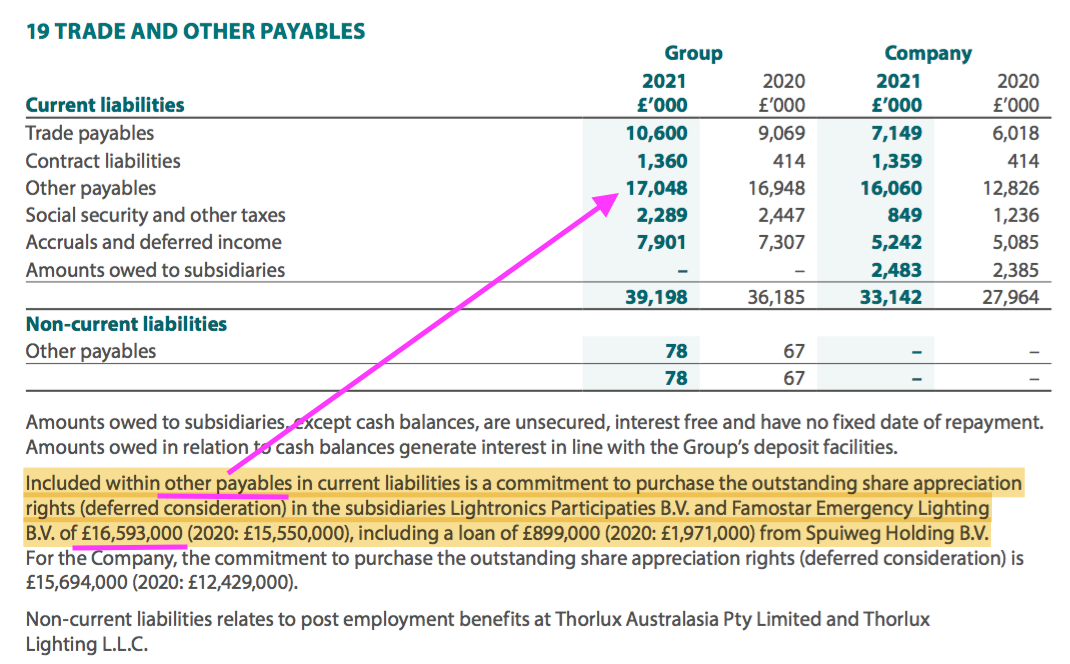

The earn-out relating to the Lightronics and Famostar purchases was paid post year-end:

The earn-out due was approximately £17m:

The earn-out payment will mean no further dividends to the minority owners…

…and no further charge to the income statement due to changes to the amount owed:

14) INSURANCE PROCEEDS

A breakdown as to how the £1.6m insurance proceeds profit was derived:

The replacement cost of assets notably exceeded the associated book values, which has implications for ROCE and similar calculations (i.e the denominator has been diminished over time by depreciation etc, and may not reflect the potential ROCE on newly purchased assets).

15) EMPLOYEES

Nothing too untoward here:

Revenue per employee gained almost £5k to £169k to a new high with total employee costs staying at 29% of revenue. The average employee cost climbed £1k to £49k to a new high.

TFW’s employee ratios have been quite consistent, with employee costs steady at between 27-30% of revenue since 2006. Revenue per employee was £151k in 2016, £119k in 2011 and £84k in 2006, which is evidence of useful productivity improvements over time.

16) TANGIBLE ASSETS

Spending on plant and equipment last year matched the depreciation expensed through the income statement:

Note how freehold assets that cost £22m are in the books for £17m after years of modest depreciation. The market value of TFW’s freeholds is in fact “significantly greater” than £22m, given text elsewhere in the report states:

“While it is considered that the market value is significantly greater than the net book value for many of the Group’s properties as a result of being acquired between one and over 20 years ago, management considers that undertaking formal valuation exercises would be costly for limited value…”

17) INTANGIBLE ASSETS

TFW has never shown any cavalier capitalisation of development costs:

Capitalised costs and the amortisation expensed through the income statement were almost identical last year. Capitalised development costs have an acceptable three-year useful life.

Fishing rights meanwhile remain one of the stock market’s more unusual intangibles (in this case created years ago through the purchase of a riverside property that is used (as I understand) for customer entertainment purposes).

Various small numerical changes were contained in the small-print below:

The Portland discount rates were 6.3% and 11.7% for 2020, so the increases to 7.6% and 15.4% suggest a lower NPV for the subsidiary.

The Lightronics and Famostar ‘headroom’ of £20m was previously £16m, which suggests the NPV of the Dutch divisions has improved by £4m.

The 6x and 5.5x EBITDA multiples cited remain the same and perhaps provide some indication of future acquisition multiples.

18) INVESTMENT PROPERTY

TFW’s investment properties have a £2m book value and include woodland in Wales for tree planting and the riverside property for customer entertainment.

I am probably missing something obvious, but the net rental income in this note was £32k…

…but in this note is £52k:

19) LOAN NOTES

Among TFW’s assets are various loan notes. The main IOU relates to a subsidiary disposal from 2011:

Repayment of this loan has been slow going, but £377k was repaid last year to leave £1.8m outstanding. TFW made a £177k provision against this loan for 2020 (i.e. TFW expected £177k not to be repaid), but that provision has been encouragingly reversed following the £377k payment.

A small Spanish investment required a £746k loan:

This £746k loan could be signalling trouble (see point 20).

Good to see Famostar reducing its loan to zero:

Total loans outstanding are £2.5m.

20) FINANCIAL ASSETS

An impairment of £529k at TFW’s small Spanish investment follows a £407k impairment during 2020:

The carrying value of Luxintec could well be zero.

21) INVENTORY

As mentioned in the blog post above, TFW’s stock reduction was due to component shortages and the associated (and favourable) cash movement may be short lived (i.e. TFW now has to pay much more for new stock to service orders):

Average stock at c£22m and the (corrected) stock expense at £45m indicates stock having a 6-month warehouse life before customer delivery. 6 months is also the average for the last 10 years, which suggests TFW likes to keep stock levels high to ensure reliable customer service.

The £3m stock provision equates to 12-13% of the year-end stock balance and indicates TFW’s products are at some risk of obsolescence while waiting in the warehouse.

22) TRADE AND OTHER RECEIVABLES

The record H2 could explain the much higher trade receivables balance:

Year-end trade receivables represented 21.7% of revenue, up from 16.7% for 2020 and the highest since 2016 (22.3%). This percentage can fluctuate (e.g. 24.7% for 2015), but ideally customers ought to pay sooner (a low percentage) rather than later (a high percentage). Past receivable levels suggest 60-90 day payment terms, which correlates with text elsewhere in the report:

“The normal credit terms are 30 to 90 days from delivery, or completion of the service provided.

However, receivables past due but not written down increased significantly to more than £3m — to represent the highest level (13%) of trade receivables since the figure was first disclosed during 2007.

This £3m past-due figure is certainly something to monitor, although difficult to say at the moment whether customers generally are becoming tardier with payments

At least actual bad debts remain minimal:

23) PENSION SCHEME

As mentioned in the blog post above, TFW’s defined-benefit scheme does not appear too troublesome:

Scheme assets of £42.6m require a generous 6% return to cover annual benefits of £2.6m, although contributions of £0.9m reduce that to 4%. The majority of scheme assets are invested in bonds.

Benefits paid increased by 46% last year, which may be due to one-off factors or maybe a permanent step-change.

Between 2010 and 2013, TFW pumped in c£1.3m a year into the scheme and a return that level of company contributions cannot be ruled out if benefits remain at £2.6m and asset returns are poor.

Any extra contributions to the scheme effectively bypass the income statement but are shown in the cash flow statement:

24) OPTIONS

TFW has three times as many shares in treasury than options:

The imbalance may be further evidence for scope to grant more options. The shares held in treasury seem purely for option-satisfaction purposes and perhaps ought to be counted as normal shares for valuation sums.

Maynard