23 December 2019

By Maynard Paton

Results summary for Oleeo (OLEE):

- A bombshell tender offer and delisting proposal overshadowed details of the 2019 results.

- I have tendered my full holding and recorded a 30% loss after owning the shares for four years.

- The tender offer was not exactly generous, given OLEE’s net cash represented 93% of the tender valuation.

- A delisting was always a risk when the executive chairman (and related parties) owned 84% of the business.

- Full-year revenue climbed 7% to reach a new high, although the significant development expenditure seen since 2015 is set to depress profit for at least another year.

Contents

- Event links and share data

- Why I sold OLEE

- Why I had owned OLEE

- Tender offer and delisting proposal

- Results summary

- Revenue, profit and dividend

- Financials

- Valuation

- Portfolio sale

Event links and share data

Event: Final results for the twelve months to 31 July 2019 and tender offer and delisting proposal published 07 November 2019.

Price: 165p

Shares in issue: 7,651,404

Market capitalisation: £12.6m

Why I sold OLEE

- A tender offer at 165p per share provided the only exit to avoid a proposed delisting and holding shares in a private company.

Why I had owned OLEE

- Developed recruitment software with an emphasis on customer support that landed blue-chip clients such as Marks & Spencer, WPP, Morgan Stanley and 60%-plus of UK police forces.

- Founder/executive chairman boasted a 71%/£9m shareholding, had ensured long-term management consistency and seemed to possess the “capacity to suffer” to deliver long-term returns.

- A £13m market cap had looked inexpensive given the £11m net cash position and any forthcoming recovery to current minimal earnings.

Further reading: My OLEE Buy report | All my OLEE posts | OLEE website

Results summary

Tender offer and delisting proposal

- OLEE accompanied its 2019 annual results with a bombshell tender offer and delisting proposal.

- Shareholders could either accept the 165p per share tender offer or remain invested in what would become a private company.

- OLEE said the decision to delist was due to:

- The “considerable costs, management time and the legal and regulatory burden” associated with maintaining an AIM quote;

- The potential to “better utilise” the savings;

- The company’s minimal share-trading volumes;

- The executive chairman (and related parties) owning 84% of the shares;

- The market cap being £12.6m;

- The lack of raising extra equity capital since the March 2000 flotation, and;

- Being “unlikely to benefit from any new institutional investors or additional analyst interest in the secondary market”.

- Apart from point 5 — the market cap has bobbed between £4m and £30m since the flotation — the other points could have been cited at any time during the last 19 years.

- OLEE has only itself to blame for points 3 and 7.

- Terse results statements and an absence of City engagement did not endear many conventional investors to the company.

- In fact, OLEE’s own announcement about the “corporate privatisation” ironically revealed more about the business than any previous RNS (my bold):

“Oleeo, the pioneer in artificial intelligence-enabled recruiting technology solutions, today announced its corporate privatization from the London Stock Exchange. The change enables Oleeo to accelerate its artificial intelligence (AI) technology innovations and market expansion, while also increasing its investments in customer success.

Oleeo counts many of the world’s top employers among its customers, including leaders in finance and banking, retail, technology, e-commerce, professional services, manufacturing, recruitment process outsourcing, travel, and entertainment.

In the US Oleeo experienced over 40 percent sales growth from 2016 to 2018, with plans to increase investments to accelerate growth in that market.

In the UK Oleeo is already the leading talent acquisition technology provider, where the company counts some of the UK’s most notable brands as its customers, as well as many branches of public service, including healthcare, central government (covering half a million civil service employees), and over 60% of the police forces.”

- Mentioning:

- Artificial intelligence-enabled recruiting technology;

- Plans to accelerate growth in the US, and;

- A 60%-plus share of UK police-recruitment systems…

…in RNSs may well have created more City attention.

- Given OLEE’s executive chairman (and related parties) owned 84% of the shares, other investors could not prevent the delisting.

- I suppose investors should be pleased a 165p tender price was provided. Not all companies that delist offer to buy out exiting shareholders.

- The prospect of owning shares in a private company was not appealing (at least for me).

- The 165p per share tender offer was not generous (see Valuation below).

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Revenue, profit and dividend

- April’s first-half statement had already suggested full-year revenue would surpass £10m and that the low point for earnings may have now passed.

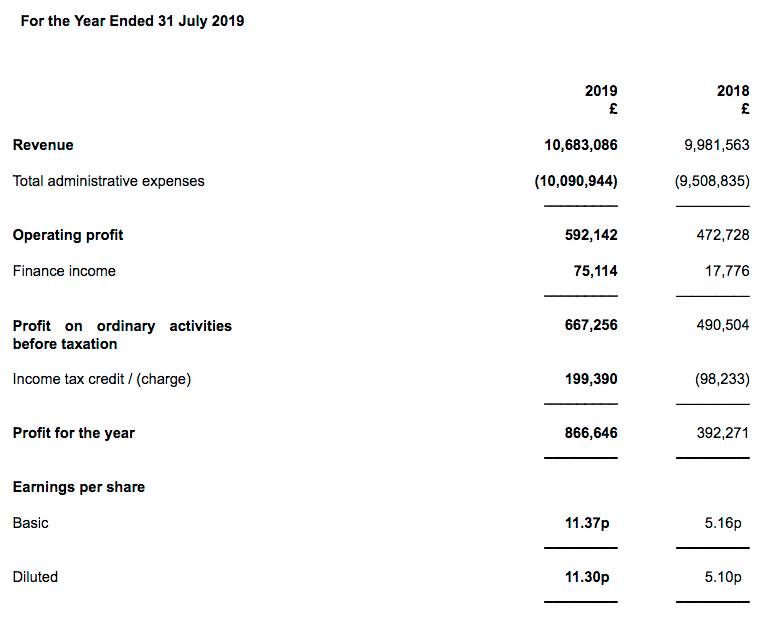

- In the event, revenue advanced 7% to indeed surpass £10m at £10.7m — a new record.

- “Like-for-like” operating profit climbed 15% to £546k.

- OLEE’s reported operating profit of £592k was influenced by the adoption of IFRS 15, a new accounting standard that dictates how revenue and profit should be recognised:

| Year to 31 July | 2015 | 2016 | 2017 | 2018 | 2019 |

| Revenue (£k) | 7,857 | 8,457 | 9,848 | 9,982 | 10,683 |

| Operating profit (£k) | 1,155 | 1,340 | 772 | 473 | 592 |

| Other items (£k) | - | - | - | - | - |

| Finance income (£k) | 43 | 43 | 39 | 18 | 75 |

| Pre-tax profit (£k) | 1,198 | 1,383 | 811 | 491 | 667 |

| Earnings per share (p) | 12.29 | 14.62 | 8.15 | 5.16 | 11.37 |

| Dividend per share (p) | 3.50 | 3.50 | 3.50 | 3.50 | 3.50 |

- Earnings were bolstered by tax refunds following the submission of R&D claims to HMRC.

- OLEE simply said the revenue increase reflected “growth in new and ongoing contracts offset by known terminations, supplemented by higher change requests and online test revenues”.

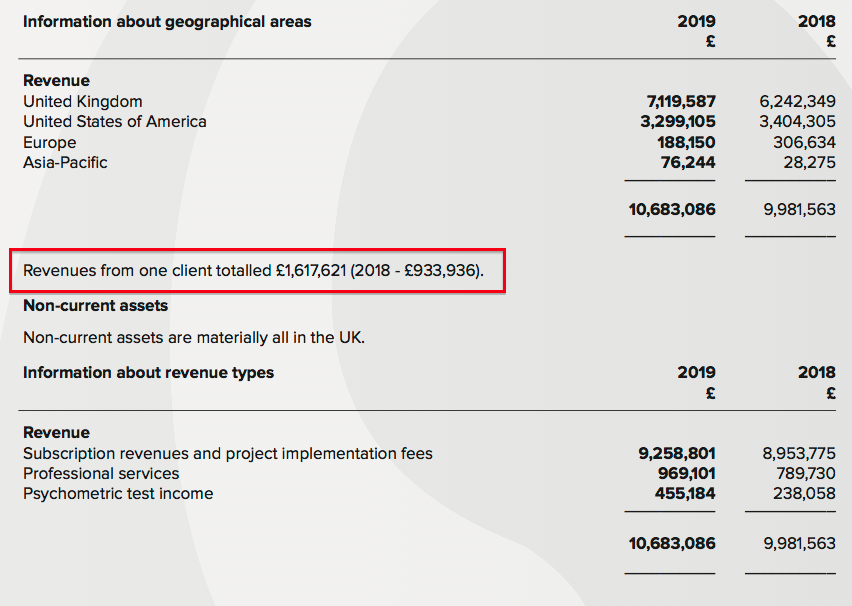

- The 2019 annual report revealed the group’s largest client represented £1.6m — or 16% — of total revenue:

- The figures for 2018 were £0.9m and 9%.

- Whether the largest client for 2019 was also the largest client for 2018 is not clear.

- If the client is the same — then almost all of the extra revenue for 2019 came from that particular customer.

- The half-year split showed an encouraging improvement to second-half profit:

| H1 2018 | H2 2018 | FY 2018 | H1 2019 | H2 2019 | FY 2019 | ||

| Revenue (£k) | 5,063 | 4,918 | 9,982 | 5,139 | 5,544 | 10,683 | |

| Costs (£k) | (4,674) | (4,835) | (9,509) | (4,945) | (5,146) | (10,091) | |

| Operating profit (£k) | 389 | 83 | 473 | 194 | 398 | 592 |

- April’s interim results had not provided any guidance for the full year.

- The absence of guidance was promising — the previous four results (November 2018, April 2018, November 2017 and April 2017) had all warned of lower profits.

- Alas, the profit improvement for 2019 may not be sustained for 2020 (my bold):

“Costs are expected to grow putting continued downward pressure on profitability. The new business team are buoyed by some new business success at the turn of the new financial year and positive prospects for the first half, however known reductions and an extremely competitive environment mean that the outlook for both sales and profits remain uncertain.”

- Of course, OLEE may have talked down the prospects for 2020 to minimise the level of the tender.

- OLEE’s operating profit topped £2.4m during 2014, since when heavy expenditure to bolster products, marketing and service has depressed profit to minimal levels.

- I had described this investment phase as management’s “capacity to suffer” — a tolerance of significant expenditure with no near-term return but the potential for high long-term rewards.

- OLEE has never said when the current rate of expenditure will recede (if ever).

- A cynic might suggest that — given the tender offer has followed five years of falling/minimal earnings — the end of this investment phase is now a lot closer than the start.

- A 3.5p per share dividend was declared for the fourteenth consecutive year.

Financials

- OLEE’s accounts remain simple and cash-rich.

- Cash in the bank is still the leading attraction at £11.7m or 153p per share — equivalent to 93% of the 165p per share tender offer.

- Cash increased by £418k during the year, with earnings of £867k funding dividends of £267k, extra working capital of £160k and other cash movements of a net £22k:

| Year to 31 July | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating profit (£k) | 1,155 | 1,340 | 772 | 473 | 592 |

| Depreciation and amortisation (£k) | 81 | 84 | 94 | 113 | 128 |

| Cash capital expenditure (£k) | (90) | (107) | (125) | (153) | (164) |

| Working-capital movement (£k) | (346) | 1,093 | 1,161 | (465) | (160) |

| Net cash (£k) | 8,219 | 10,172 | 11,631 | 11,254 | 11,672 |

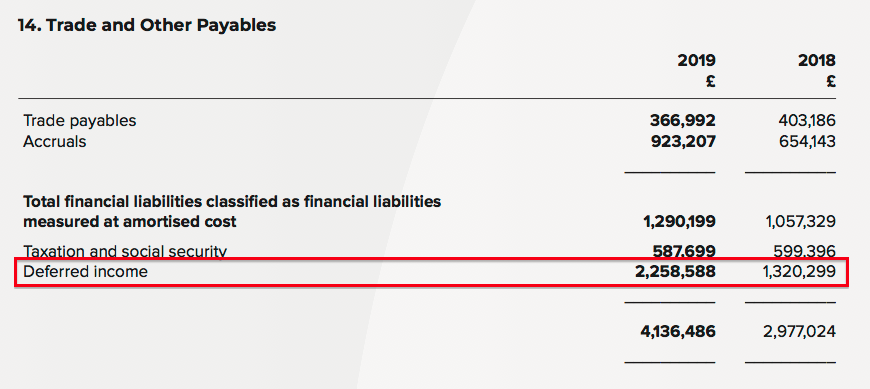

- The cash position is bolstered by deferred income — essentially upfront customer payments that are yet to be recognised as revenue.

- The 2019 annual report showed deferred income advancing £0.9m to £2.3m:

- The increase to deferred income was due mostly to IFRS 15, and the deferral of revenue that had been previously recognised.

- Account for deferred income, which could perhaps be refunded to customers, and OLEE’s ‘surplus’ cash position is arguably £11.7m less £2.3m = £9.4m.

- The balance sheet carries no debt and no pension complications.

- The greater expenditure on support, development and marketing has left certain ratios at dismal levels:

| Year to 31 July | 2015 | 2016 | 2017 | 2018 | 2019 |

| Operating margin (%) | 14.7 | 15.8 | 7.8 | 4.7 | 5.5 |

| Return on average equity (%) | 11.1 | 12.1 | 6.3 | 3.9 | 8.5 |

- All development expenditure is commendably expensed as incurred and not capitalised onto the balance sheet.

- Finance income during the year came to £75k — a notable 11% of pre-tax profit.

Valuation

- The 165p per share tender offer valued OLEE at £12.6m.

- The aforementioned £9.4m ‘surplus’ cash position implied the tender offer valued the underlying business at just £3m.

- OLEE has always operated with significant net cash and maybe the presence of such cash is required to keep clients happy — and is therefore not really ‘surplus’ to requirements.

- Nonetheless, the substantial cash position does make the tender offer look rather ungenerous.

- OLEE reported earnings of £1.9m during 2014. A return to that level of profitability would make the tender offer appear extremely meagre.

- The 3.5p per share dividend supported a 2.1% yield on the 165p tender price.

Portfolio sale

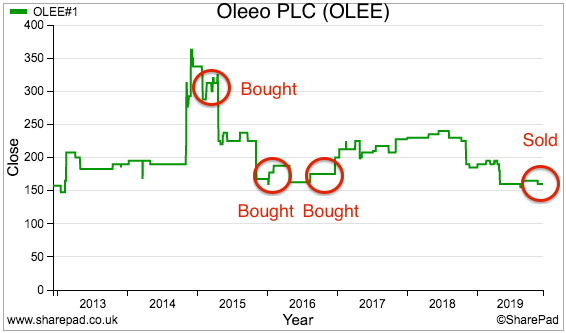

- I tendered my entire OLEE position and received the 165p per share proceeds earlier this month.

- I first purchased OLEE (then known as World Career Networks) during 2015 at 320p.

- I bought more during 2016 at 182p.

- All told, I paid an average of 260p, collected dividends equivalent to 16p along the way and ended up selling at 165p to register a 30% loss:

- OLEE had initially offered many attractive traits. In my original Buy report I wrote:

“When I bought, I was convinced this £24m firm offered all the hallmarks of a successful investment.

Alongside claims of supplying “world-class technology”, other attractions included a blue-chip client list, generous margins, a cash-flush balance sheet, respectable sales growth and a long-time founder/entrepreneur at the helm. Furthermore, a possible P/E of just 7 suggested the shares were a bargain.”

- But I was aware of the illiquidity of the shares and the chance of a delisting:

“I guess the other risk with [OLEE] is dominant executive Charles Hipps turns the business into a personal fiefdom that one day leads to a delisting.

I suppose I am more relaxed about this risk than most other investors. For a start, [OLEE] has already been quoted for 15 years and I feel if the boss was ever going to do the dirty on shareholders, he’d have done so by now.

I don’t know for sure with [OLEE], but my research into family-dominated firms suggests a stock-market quotation offers:

* Greater transparency and reassurance for customers and suppliers;

* Operational benefits and greater financial discipline from the additional reporting;

* The opportunity for smaller family shareholders to dispose of their investments, and;

* The ability to raise funds through further share issues or to motivate staff with share options (although many family firms I have come across do neither!)

I trust one of those reasons will keep [OLEE] on the stock market for some time to come.”

- Those reasons kept OLEE on the market for a further four years.

- In retrospect, I was unfortunate to invest right at the start of OLEE’s multi-year phase of heightened expenditure…

- ….which made the obscure, illiquid shares even less attractive to the wider market, and in turn gave the executive chairman more reason to propose the delisting.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard no longer owns shares in Oleeo.

Hi Maynard ,

Sorry to hear this .

I have a small holding ASY just wondered your thoughts on them as very much family owned. Although I note it has a market cap of more than 20x Olee.

I like ASY but do wonder sometimes whether I have fallen in love with the company too much !!! there is always a risk of delisting , but seems to have looked after shareholder thus far.

Hi Tony

ASY is family owned, but not family run. According to ASY’s MD and FD at an AGM a few years back:

“Listing — board owns 90% of the shares while the company has no option scheme nor has issued any shares to raise money (at least for a decade). So why have a quote? Governance — quoted firms are tightly regulated and controlling family, who are not involved in the operation of the business, like the higher levels of management governance a stock-market listing can provide. Question has been asked for at least the last ten years.”

I went to the OLEE AGM in (I think) 2015 and asked the same question and the exec chairman said the delisting subject had been discussed occasionally at board meetings — which in hindsight was a warning I guess. OLEE’s exec chairman is involved in running the business and a relation of the chairman also has a hand in preparing the accounts (see related party transactions in the annual report), so going private for them may have been an easier decision.

I suspect had OLEE been able to prosper without the heavy expenditure, the delisting may not have occurred.

I reckon 7 of my 12 shares have families/concert parties owning 50%-plus of the shares. The flipside to having dominant ‘owner managers’ is that ordinary investors are ultimately passengers on the share register.

Maynard