01 May 2018

By Maynard Paton

Update on World Careers Network (WOR).

Event: Interim results for the six months to 31 January 2018 published 30 April 2018

Summary: Yet again the recruitment software developer delivered results that warned of greater costs and lower client fees. However, this statement was also accompanied by details of a company rebranding — which seems a complete joke project to me. Instead, management really should be addressing why the firm looks to have lost its largest customer. I have sat on a 35% loss here for three years now, and have been taught a tough lesson about illiquidity. Sadly I continue to hold.

Price: 235p

Shares in issue: 7,610,304

Market capitalisation: £17.9m

Click here to read all my WOR posts

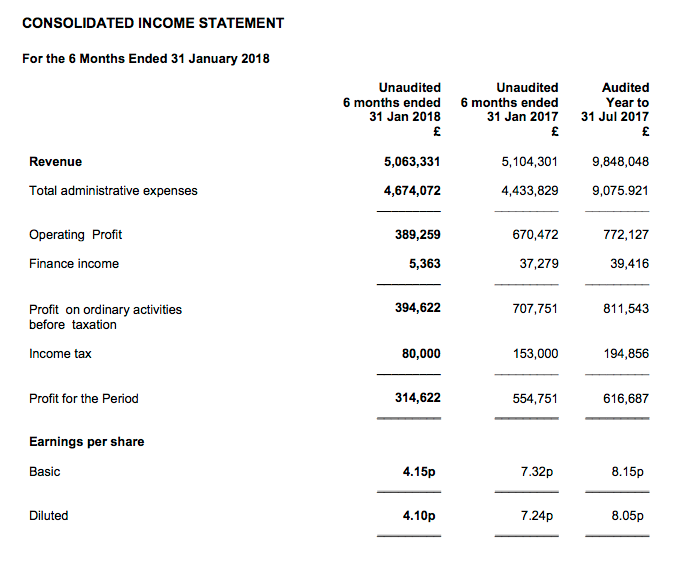

Results:

My thoughts:

* He did say there would be a “material adverse impact”

This time last year, WOR admitted its 2018 earnings would experience a “material adverse impact” due to a mix of slow sales to new clients and greater operating costs.

As such, these results were never going to be spectacular.

In the event, revenue dropped 1% while operating profit dived 42%. The sole positive from this H1 performance was that it was not as bad as H2 2017, when operating profit collapsed to £102k.

That said, the prospect of another woeful H2 seems high. WOR’s executive chairman, Charles Hipps, confessed:

“Low new sales in the first half of the year, and known reductions in subscription revenues from the existing client base, mean that we expect profits for the second half of the year to be lower than the first half and for this to be reflected in a lower profit for the full year than we achieved in 2017.”

Perhaps if WOR held its seminars away from converted bunkers…

…then new sales would not be so elusive.

* Substantial HMRC contract looks to have been lost

When I studied November’s annual figures, I wrote:

“I note the term “known reductions in revenue from the existing client base”.

I bet that concerns HMRC, which is WOR’s largest customer and represents about 12% of group revenue.

My investigation back in 2015 revealed that HMRC’s standard monthly payment to WOR had dropped by a massive 66%.

The HMRC contract is up for renewal in early 2018 and I dare say WOR has again pitched a lower fee to keep the business. “

Well, it seems WOR has lost its HMRC contract — at least judging by HMRC’s monthly spreadsheets.

The spreadsheets for January, February and March made no mention of WOR. HMRC produced approximately 14% of WOR’s 2017 revenue and would be a significant client loss.

* Stupid name change could disguise a more pressing problem

I had to snigger at this remark from the aforementioned Mr Hipps:

“As we continue to grow the business, we want our brand to best reflect why we exist, what we believe in, and where we are heading. In order to achieve this we intend to change our logo, our visual identity and the branding of our products and services and, alongside this, the name of the company.”

Continue to grow the business!? Excuse me Mr Hipps, but operating profit currently runs 80% below the level reported for 2014.

The company name will be changed to Oleeo plc.

No, I am not sure how exactly Oleeo reflects why the company exists, what it believes in and where it is heading either.

I also doubt this rebranding exercise will disguise what could be a more fundamental problem — that the products just aren’t good enough — and why perhaps HMRC has jumped ship.

I can only trust Mr Hipps spent a few minutes on Domainhole rather than employ costly consultants for this joke project.

Valuation

With earnings continuing at a very depressed level and no sign of any imminent improvement, gauging WOR’s valuation remains tricky.

The only real yardstick is the £11.0m net cash position, which adjusting for likely upfront customer payments is probably about £9.5m. With a market cap of £17.9m, the underlying business could arguably be valued at £8.4m.

However, that £8.4m figure does not appear to be an obvious bargain given the £491k trailing operating profit.

The straw to clutch, of course, is that WOR’s investment in marketing and so on eventually pays off, revenue then advances, and profitability in time rebounds to the previous heights of £2m-plus. (I acknowledge this projection could be wishful thinking.)

I have held this share for three years now and have been stuck with a 35% loss for almost all of that time.

While I am a patient investor, the (likely) loss of the HMRC contract alongside the stupid name change has left me somewhat uncomfortable with the business.

Indeed, I am beginning to sense the group’s extra costs are to help its products catch up with the competition, rather than to extend their prominence.

Normally I would be selling out here, but WOR has taught me a tough lesson about illiquidity — the free float has only a c£1m market value and I just can’t sell without crashing the share price.

As such, I have to resign myself to keeping WOR on and hoping I do not face another three years of holding ‘dead money’.

Maynard Paton

PS: You can now receive my Blog posts through an occasional e-mail newsletter. Click here for details.

Disclosure: Maynard owns shares in World Careers Network.

World Careers Network (WOR)

HMRC payments update:

I continue to monitor the monthly expenditure updates from HMRC, what was WOR’s largest customer (but may be no longer).

HMRC’s data now covers March 2018:

https://www.gov.uk/government/publications/hmrc-spending-over-25000-march-2018

No reference to WOR again this month. Three consecutive months without payment has never happened before — and feels ominous.

Here is that HMRC contract again.

The contract ran until 31 January 2018.

Maynard

Dear Maynard

Just a style point. You’r blog is a really nicely measured and elegant thing,

The tone speaks of calmness and care in your investing. Recent posts use more intemperate words – bullshit, complete joke. You sold one holding and would sell the other. Not sure what to make of the language shift. It’s not typical.

We all have an interest in psychology and investing. Language gives us clues as to our state of mind.

Best wishes

Dan

Hello Dan

Thanks for the comment. I guess I have become too frustrated with developments at certain companies, and do not wish to ‘beat around the bush’ with my view. Sorry if the language has offended.

Maynard

(EDIT 06 May: PS I thought about this overnight, and decided to change the wording within the Record post)

Hello Maynard – Recruitment activities for Civil Service now fall under Cabinet Office, not HMRC. This may help inform your view.

World Careers Network/Oleeo (OLEE)

Change of name

So my vote against the name-change resolution was not enough, and World Careers Network has rebranded itself Oleeo.

Here is the company’s PR announcement:

————————————————————————————————————

Global recruitment technology leader unveils new brand identity after two decades of improving hiring for the likes of Morgan Stanley and NBC Universal

NEW YORK and LONDON (June 5, 2018) — World Careers Network (WCN), the talent acquisition pioneer first established in 1995, is today announcing a new brand identity, Oleeo, launched to coincide with new offerings designed to let recruiters reclaim time for talent engagement.

Effective immediately, Oleeo – which has offices in London, New York and Vietnam – will offer a machine learning and big data based suite of talent acquisition tools including a multiple award-winning Applicant Tracking System and a refreshed Candidate Relationship Management platform.

Oleeo’s recruitment technology offerings will help employers radically reduce unconscious biases and enhance diversity by uncovering strong candidates who may go unnoticed in a manual process. The new offerings provide recruiters with robust prescriptive analytics informed by 120 data points, helping them to make better informed decisions in a fraction of the time.

The world of work has transformed significantly since we first launched more than two decades ago. Our new name, Oleeo, stems from the mid century term Olio, which means a diverse collection of things that together make something extraordinary. Like this word, through our prescriptive analytics and intelligent automation, we help employers easily draw on the biggest possible pool of talent to create brilliant teams

“The world of work has transformed significantly since we first launched more than two decades ago. Our new name, Oleeo, stems from the mid century term Olio, which means a diverse collection of things that together make something extraordinary. Like this word, through our prescriptive analytics and intelligent automation, we help employers easily draw on the biggest possible pool of talent to create brilliant teams,” commented Charles Hipps, founder and CEO, Oleeo. “With us, the efficiency of our technology and the predictive power of data work hand in hand to meet the hiring challenges of today. The result is more effective hiring for companies and a more engaging experience for candidates.”

Frequently leveraged for high-volume recruiting, Oleeo’s intelligent suite of solutions immediately identifies the top third of candidates from an applicant pool, highlighting the most qualified candidates who should be invited for interview. Hiring improvements achieved as a result include:

* Time to hire: moving talent from application to interview in as little as 35 minutes in some cases, and from application to hire as rapid as three days, freeing an estimated 156 days each year for recruiters

* Diversity: Oleeo has helped to improve the diversity of overall hires by up to 30% across its customer base

* Cost: Oleeo customers report that intelligent automation has helped to deliver savings as high as $1.2 million/£800,000 a year

Stephanie Ahrens, Head of Talent Acquisition at Morgan Stanley, remarks: “Working with the Oleeo team has been fundamental to ensuring that Morgan Stanley continues to hire the best quality candidates. The tools we harness mean we can run end-to-end hiring, including strengths based interviewing, without having to juggle systems in the process and can be assured of watertight security and robust compliance measures. This brand evolution will help continue transforming our talent acquisition processes moving forward.”

The company’s award-winning suite — recently hailed by IDC, Aragon Research and Constellation Research — has driven measurable hiring improvements for more than 400 companies globally, including Morgan Stanley, WPP, Marks & Spencer, the UK Civil Service and NBCUniversal.

“The role of data in successful hiring is undeniable today. Solutions such as Oleeo — backed by a solid understanding of HR and shepherded by seasoned leadership — will play an increasingly critical role in helping companies of all sizes navigate the pace and complexity of hiring today,” shared Kyle Lagunas, research manager, IDC.

————————————————————————————————————

Certainly the new oleeo.com website is a more lively affair than the old WCN effort. I also note the references to “machine learning” and “big data” in the above release. Hopefully these mentions are heralding bold new products that many new clients will gladly pay handsomely for.

Sadly Oleeo’s social-media feed sadly is full of launch parties and ‘beer pong’, and not a lot about revamped products to reflect the new brand.

Maynard