07 November 2018

By Maynard Paton

Update on Oleeo (OLEE).

Event: Preliminary results for the twelve months to 31 July 2018 published 02 November 2018.

Summary: Publishing results at 4:28pm on a Friday is never a good sign. And sure enough, the recruitment software outfit warned of yet another profit slump. Still, at least revenue inched to a new record as the firm enjoyed greater subscription income. Meanwhile, an anonymous tip-off has set me straight about OLEE’s contract with HMRC — the deal appears not to have been lost after all. All I can do now with this illiquid share is hope for an earnings rebound. I continue to hold.

Price: 220p

Shares in issue: 7,620,054

Market capitalisation: £16.8m

Click here to read all my OLEE posts.

Results:

My thoughts:

* No less than six excuses for a tough 2019

These results were issued at 4:28pm on a Friday — a classic City signal to brace yourself for underwhelming numbers.

Indeed, OLEE (formerly World Careers Network) has warned of tumbling earnings for at least three years now — and this statement was sadly no different.

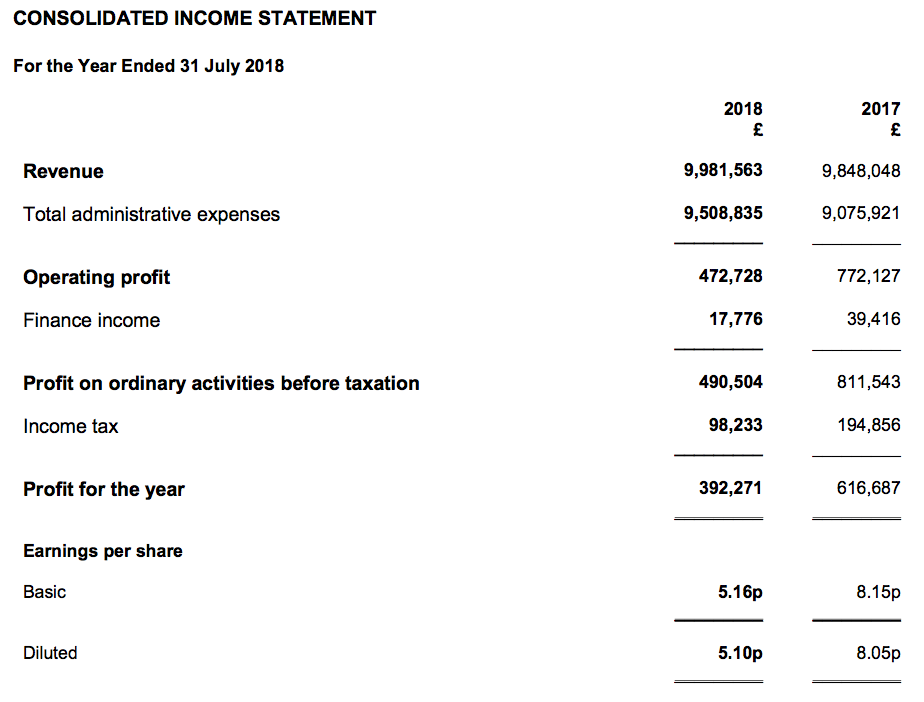

An ongoing mix of sluggish new sales alongside greater support, development and marketing costs pushed operating profit down 39% to a 14-year low:

| Year to 31 July | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (£k) | 8,584 | 7,857 | 8,457 | 9,848 | 9,982 |

| Operating profit (£k) | 2,431 | 1,155 | 1,340 | 772 | 473 |

| Other items (£k) | - | - | - | - | - |

| Finance income (£k) | 44 | 43 | 43 | 39 | 18 |

| Pre-tax profit (£k) | 2,475 | 1,198 | 1,383 | 811 | 491 |

| Earnings per share (p) | 25.25 | 12.29 | 14.62 | 8.15 | 5.16 |

| Dividend per share (p) | 3.50 | 3.50 | 3.50 | 3.50 | 3.50 |

I note operating profit during the second half was extremely weak:

| H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | ||

| Revenue (£k) | 5,104 | 4,744 | 9,848 | 5,063 | 4,918 | 9,982 | |

| Costs (£k) | (4,434) | (4,642) | (9,076) | (4,674) | (4,835) | (9,509) | |

| Operating profit (£k) | 670 | 102 | 772 | 389 | 83 | 473 |

At least revenue continues to grow — just.

The full-year top line inched 1% higher to set a new all-time record. In addition, the 4% improvement during the second half was better than I had expected — and better than the small decline witnessed at the interim stage.

The following extract was the most encouraging remark within the RNS:

“The slight increase in revenues was underpinned by an increase in ongoing subscription revenues counteracted by lower implementation revenues.”

I have my fingers crossed that OLEE’s software revenue is becoming more predictable following the higher level of ongoing subscription income.

The management narrative revealed no less than six excuses for a tough 2019:

* an uncertain general economic outlook;

* a tough environment for our clients and prospects;

* an extremely competitive market;

* lower than expected new sales;

* known reductions in revenues from the existing clients this year and next, and;

* upward pressure on costs as we seek to grow through additional investments in customer success, marketing and product development;

The long list will mean profits are “expected to be substantially lower in the current year than in the year which has just closed”.

I dare say there is the chance OLEE could report a break-even result for 2019 — or perhaps even a small loss.

Indeed, I wonder whether the firm’s chairman/founder/71% shareholder will begin to reign in the additional costs if profits ever do turn to losses.

I guess there must come a point when all this greater expenditure has to be reviewed… and a judgement call be made on whether there are alternative ways to produce additional revenue by more efficient means.

Anyway, a 3.5p per share annual dividend was declared for the thirteenth year — which might be a stock-market record for the longest standstill payout.

* Anonymous tip-off tells me to check with the Cabinet Office

I must own up to making a mistake about OLEE’s contract with HMRC — the group’s largest customer.

Back in April I ranted about OLEE seemingly losing its deal with the tax office.

You see, I kept an eye on HMRC’s monthly spreadsheets and the spreadsheets for January, February and March made no mention of OLEE.

Given OLEE’s contract with HMRC ran until 31 January 2018, I assumed the agreement had ceased.

However, an anonymous reader — who I suspect is close to OLEE — then tipped me off about a change to the government’s spreadsheets.

(Hint: I welcome all tips-offs, scuttlebutt, corrections and other help! Contact me here.)

Civil-service recruitment expenses are now handled by the Cabinet Office and, from what I can tell, its spreadsheets show £47k monthly payments to OLEE starting from July.

(I am not sure what happened to HMRC’s payments between January and June).

HMRC therefore appears to have renewed its OLEE agreement and — very surprisingly — continues to pay the same £47k monthly fee. Perhaps HMRC was persuaded to maintain its payments by OLEE’s recent rebranding.

Either way, this HMRC tip-off has left me a little more comfortable with OLEE than I was earlier this year.

* Cash flow remains sound but certain ratios are dismal

There is not much to say about OLEE’s accounts.

The greater support, development and marketing costs have left certain ratios looking very dismal:

| Year to 31 July | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating margin (%) | 28.3 | 14.7 | 15.8 | 7.8 | 4.7 |

| Return on average equity (%) | 26.2 | 11.1 | 12.1 | 6.3 | 3.9 |

At least cash flow remains sound:

| Year to 31 July | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating profit (£k) | 2,431 | 1,155 | 1,340 | 772 | 473 |

| Depreciation and amortisation (£k) | 88 | 81 | 84 | 94 | 113 |

| Cash capital expenditure (£k) | (96) | (90) | (107) | (125) | (153) |

| Working-capital movement (£k) | (196) | (346) | 1,093 | 1,161 | (465) |

| Net cash (£k) | 8,171 | 8,219 | 10,172 | 11,631 | 11,254 |

I can live with the 2018 negative working-capital movement given the positive movements during 2016 and 2017.

As always, OLEE’s annual report will reveal the amount of upfront customer payments (or ‘deferred income’) that sit on the balance sheet. This sum can in turn signal the possible trend for revenue for the current year.

Meanwhile, I am pleased OLEE’s expenditure on tangible assets remains relatively modest and that the business continues to write off all software development spend as incurred.

The year-end cash position fell a fraction to £11.3m, or 148p per share, and is equivalent to two-thirds of the market cap. The balance sheet carries no debt and no pension obligations.

(I should add that £7.8m of OLEE’s cash is now held within short-term investments — the details of which should be disclosed in the forthcoming annual report).

Valuation

With earnings currently at very depressed levels and heading towards zero, assessing OLEE’s valuation is not straightforward.

The only real yardstick is the £11.3m cash position, which adjusting for upfront customer payments is probably about £10m. With OLEE’s market cap at £17m, the underlying business could arguably be valued at £7m.

That said, I do keep wondering whether OLEE’s cash hoard is kept to reassure clients and as such should not be deemed as ‘surplus’ funds.

For long-suffering shareholders, the continuing hope of course is that OLEE’s additional costs eventually pay off, revenue regains its momentum and profitability then rebounds.

However, I have given up trying to predict when — or even if — OLEE may return to growth.

I wrote in April that OLEE has taught me a tough lesson about illiquidity — the free float has only a c£1m market value and I just can’t sell without crashing the share price.

Oh well — I remain resigned to keeping OLEE and will continue to yearn for a turnaround. At least I do not need to worry about the HMRC contract for the time being.

Maynard Paton

PS: You can receive my Blog posts through an occasional e-mail newsletter. Click here for details.

Disclosure: Maynard owns shares in Oleeo.

Oleeo (OLEE)

Publication of 2018 annual report

The most notable feature of this annual report is the new front cover (the previous seven editions had each used the same smiling lady). A bit of work has gone into the report’s fresh design.

Here are some other points of interest:

1) Corporate governance

OLEE has obeyed the new rules about corporate-governance reporting and included a handful of pages on how it meets ten different points:

The following stood out:

I attended the AGM a few years ago and I would not say then that attendance was encouraged. Perhaps I should try attending again.

2) New accounting standards

I get the impression IFRS15 could create some bookkeeping issues:

That said, OLEE’s working-capital movements over the years have generally looked fine, so I do not feel the business has been recognising revenue in an aggressive manner to date. Half-year results in April will provide the first clue to the IFRS15 impact.

Nothing much to worry about with IFRSs 9 and 16:

3) Revenue split

This is probably the most encouraging part of the whole report:

Total revenue gained 1.4%, and I see revenue from the largest customer (HMRC) dived 29% to £934k.

So… total revenue excluding the largest customer improved 6.1%. Not bad. Driving that performance has been OLEE’s oversees divisions, where sales gained a very welcome 21.3%.

In fact, if you exclude the largest customer, revenue has grown from £6.0m to £9.0m between 2014 and 2018 — which is actually quite impressive. The majority of that advance has come from the US, where sales during the same time have climbed from £760k to £3.4m.

I keep seeing the somewhat feisty Jeanette Maister, OLEE’s US boss, on social media extolling the group’s services. She seems to be doing a decent job.

4) Director pay

Another encouraging snippet:

The three execs each took a pay cut last year. Boss Charles Hipps saw his wages reduced by 14%/£41k. I guess the greater expenses that have reduced earnings for the last few years have now reached the boardroom.

Wishful thinking perhaps, but I would like to think when directors cut their own pay, a greater focus is soon applied to lifting sales and profit.

5) Employees

OLEE’s employee costs and headcount were very similar to the year before:

The average employee cost remains at £61k, the average revenue per employee remains at £87k while employee costs as a proportion of revenue remain at 70%.

6) Short-term investments

OLEE placed £7.75m into a high-interest account:

7) Trade payables

Deferred income — representing upfront customer payments — has declined by £144k:

Not a great sign, but perhaps not unexpected given OLEE’s long list of excuses for a tough 2019 given in the management narrative.

8) Trade receivables

The appearance of ‘accrued income’ is interesting:

This entry generally relates to revenue that has been recognised but not yet invoiced let alone paid. A lot of software companies that suffered huge problems in the past saw their accrued income soar well above trade receivables (which are amounts invoiced to customers and unpaid).

Right now the amount of accrued income is relatively small, but the entry is something to keep an eye on. I wonder if the appearance of accrued income relates to the upcoming IFRS15 (see above).

The ageing of outstanding trade receivables has not really changed from 2017:

Maynard

Oleeo (OLEE)

Holding(s) in Company published 29 March 2019

A collectors item — OLEE’s first Holding(s) in Company RNS since 2010, and only the fifth since the 2000 flotation.

Liontrust has reduced its stake from 12% to 9.31%. Presumably another fund has picked up the 2.69%, but no notification RNS from the buyer was required as the acquired stake was below 3% .

Anyway, somebody somewhere thinks OLEE is worth backing. Let’s hope they are right. Liontrust has owned c10% of OLEE since 2004.

OLEE’s shareholder register has the chairman and family owning 83%, Liontrust now having 9%, which leaves 8% — or c550k shares with a c£1m value — for the mystery purchaser above, me, and all other shareholders.

Maynard