28 December 2019

By Maynard Paton

Results summary for Mountview Estates (MTVW):

- Brexit “uncertainties” led to a dull performance, with revenue falling 1%, underlying operating profit improving 1% and an unchanged dividend.

- An improved gross margin and the disposal of four investment properties for prices well above book were encouraging.

- Debt represents a modest 10% of the group’s property estate — which continues to be accounted for at cost.

- This year’s AGM witnessed further protest votes against the independent non-executives, the board’s pay and the auditors.

- MTVW’s book value increased by 4% to £96 per share, although the balance sheet could inherently be worth £200-plus per share. I continue to hold.

Contents

- Event link and share data

- Why I own MTVW

- Results summary

- Revenue, profit, dividend and net asset value

- Gross margin

- Allsop valuation

- Financials

- Corporate governance

- Valuation

Event link and share data

Event: Interim results for the six months to 30 September 2019 published 21 November 2019

Price: £118

Shares in issue: 3,899,014

Market capitalisation: £460m

Why I own MTVW

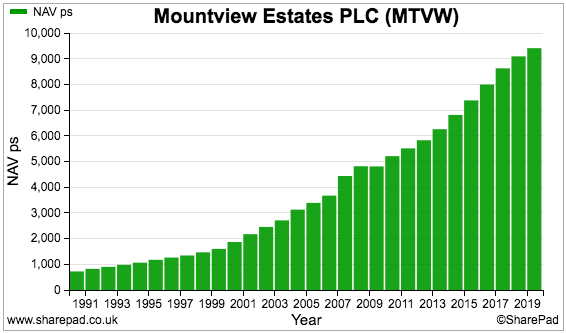

- Buys, holds and sells regulated-tenancy properties and boasts an illustrious, 30-year-plus history of net asset value and dividend advances.

- Board led by veteran family management that continues to control an aggregate 51%/£235m shareholding.

- Simple accounts carry properties at cost, which if sold at their current market values may be worth significantly in excess of the recent market cap.

Further reading: My MTVW Buy report | All my MTVW posts | MTVW website

Results summary

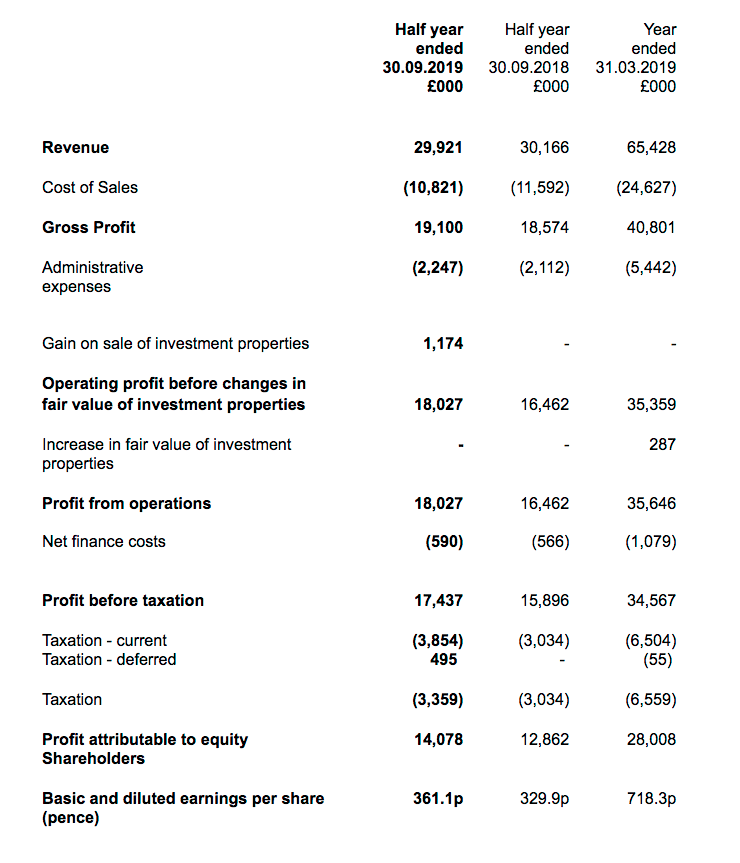

Revenue, profit, dividend and net asset value

- The four-paragraph, 222-word statement left the accounts to do all of the talking.

- Revenue fell 1% to the lowest H1 level for six years. Operating profit before investment-property gains climbed 1%.

- The revenue decline was due to MTVW selling regulated-tenancy properties at a lower average price (£269k vs. £283k):

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| Property sales revenue (£k) | 23,953 | 27,887 | 20,656 | 25,774 | 20,199 | ||

| Properties sold | 84 | 86 | 73 | 81 | 75 | ||

| Average selling price (£k) | 285 | 324 | 283 | 318 | 269 |

- Not selling a property for more than £1m caused the lower average price. MTVW sold a single £1m-plus property during the comparable half.

- Profit improved because the gross margin achieved on property sales increased from 57% to 61% (see Gross margin below).

- Rental income increased 2% to £9.7m — equivalent to 32% of total revenue.

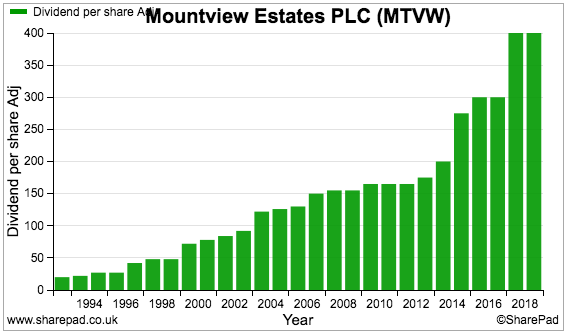

- A 200p per share interim dividend was declared for the fifth consecutive year.

- Net asset value (NAV) advanced by £14m to £373m — equivalent to £95.70 per share and a fresh NAV record:

Gross margin

- MTVW’s balance sheet is dominated by 2,000 or so regulated-tenancy (and similar) properties that boasted an aggregate £317m book value within the 2019 annual report.

- Assured-/life-tenancy properties plus freehold/leasehold ground-rent properties represent a further £75m.

- MTVW sells its regulated-tenancy properties only when the tenancy ends — which typically occurs when the tenant dies.

- The number of properties becoming available for sale — and the total proceeds MTVW earns from one set of results to the next — can therefore be unpredictable.

- The group’s properties are held on the balance sheet at their cost price.

- The percentage gain from a sold property is largely correlated to how long the property has been owned by MTVW.

- Management comments at the AGM during August indicated MTVW likes to purchase regulated-tenancy properties at a 25% discount to the property’s ‘unregulated’ state.

- The table below shows the gross margin achieved from selling properties during 2018, 2019 and this H1:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| Property sales revenue (£k) | 23,953 | 27,887 | 20,656 | 25,774 | 20,199 | ||

| Property sales gross profit (£k) | 14,297 | 15,721 | 11,706 | 15,751 | 12,271 | ||

| Property sales gross margin (%) | 59.7 | 56.4 | 56.7 | 61.1 | 60.8 |

- The 60.8% gross margin for this H1 is equivalent to MTVW selling a property for a 155% gain. MTVW’s five- and ten-year averages are 171% and 163% respectively.

- The health of the housing market — which management claims has been stifled by Brexit of late — can effect the gains MTVW reports.

- During 2015, 2016 and 2017, MTVW reported gains of approximately 185% from property sales — with bumper 245% gains achieved during the six months to September 2016.

- I remain hopeful MTVW’s property gains can gradually return to their 185% pre-Brexit level.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Allsop valuation

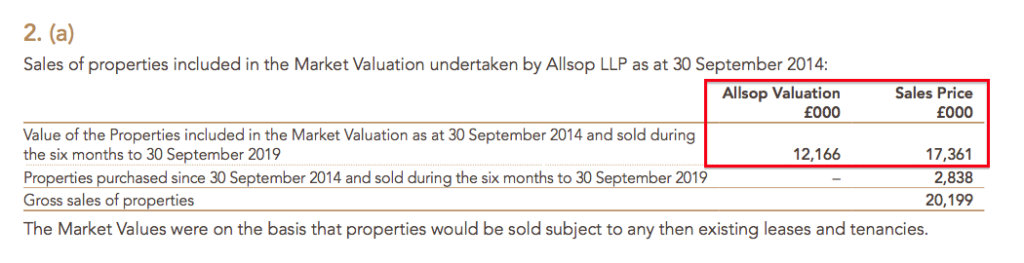

- MTVW commissioned property agent Allsop to value the group’s estate during September 2014.

- Allsop returned a £666m valuation — some 2.1x the £318m book value of the properties carried at the time.

- The Allsop calculation was based on MTVW’s properties remaining in their regulated-tenancy state.

- Following the Allsop valuation, MTVW reveals the proceeds from sold properties versus their stated Allsop value:

| H1 2018 | H2 2018 | H1 2019 | H2 2019 | H1 2020 | |||

| Property sales revenue (£k) | 22,496 | 22,660 | 17,363 | 23,910 | 17,361 | ||

| Allsop valuation (£k) | 14,767 | 15,827 | 12,226 | 16,501 | 12,166 | ||

| Sold-vs-Allsop multiple (%) | 1.52 | 1.43 | 1.42 | 1.45 | 1.43 |

- Sale proceeds have in the past been 1.5x or more than the associated Allsop valuation.

- These results showed the ‘sold-vs-Allsop’ multiple at 1.43x — in keeping with the previous 18 months.

- The Allsop valuation is now five years old and has become rather stale.

- Management claimed at the AGM in August that it was “premature to conduct another valuation in the current uncertain times”.

- The “uncertain times” related to Brexit.

- I see no shame in the Board committing to valuations every (say) five years and simply saying a valuation is taking place and nothing can be done about any “uncertain times”. Shareholders can then adjust the valuation for any uncertainties themselves.

- MTVW said in this H1 RNS:

“With continuing good purchases and sound financial planning the Company is well placed to take advantage when the country’s economic strategy can be planned with greater certainty.”

- Maybe the outcome of the recent general election can now lead to “greater certainty” and another Allsop valuation.

Financials

- MTVW’s accounts remain very straightforward.

- Some £8m was spent during the six months acquiring 28 additional properties (average cost: £286k), which MTVW described as “good purchases”.

- The disposal of four investment properties raised a useful £4.2m.

- The investment properties had a combined £3.0m book value, which might suggest the remaining investment properties (book value: £25m) are undervalued in the accounts.

- Earnings of £14m plus the investment-property disposals funded a £9m debt repayment and an £8m dividend.

- Net debt dropped by £7m during the six months to £39m — equivalent to 10% of the group’s £392m property estate.

- In the past, net debt has at times represented 30% or more of MTVW’s property stock.

- The group could therefore have the capacity to borrow another £78m.

- Annualised interest costs of £1.2m were equivalent to a reasonable 2.7% of average H1 debt of £44m.

- MTVW’s books are free of pension obligations.

Corporate governance

- Despite MTVW’s illustrious, 30-year-plus history of NAV and dividend advances, not every shareholder is happy.

- Recent AGMs have seen c30% protest votes against re-electing the independent non-executives, the approval of the board’s remuneration and the re-appointment of the auditors.

- MTVW shareholders can be dividend into three groups:

- The Sinclair family concert party, which is led by chief executive Duncan Sinclair and represents 51% of the share count;

- The Murphy family and connected parties, who own 24% of the share count and whose largest shareholder is the chief executive’s sister, and;

- Everybody else, who control 25% of the share count.

- The protest votes come almost entirely from group 2.

- I attended the AGM in August and, from what I could tell, the Murphy family is broadly happy with the running of the business, but:

- Is aggrieved about the board’s pay;

- Has lost the trust of the non-execs to act on the views of shareholders, and;

- Is frustrated about a general lack of influence at board level.

- Last year the chief executive took home a total £975k while the finance director received £692k (point 3).

- Some could argue those payments are extremely generous for simply collecting rent and putting properties into auction. Bonuses were paid for 2019 despite a reduced profit and an unchanged dividend.

- Some could argue those bonuses should instead be used to fund another Allsop valuation.

- Dissident shareholders have actually prevented the re-election of certain non-executives at the last three AGMs.

- These re-elections were prevented because the resolutions were deemed to be ‘independent’ and the Sinclair family concert party could therefore not vote.

- However, the FCA’s listing rules allow MTVW to hold a subsequent general meeting, whereby the non-exec re-elections can be proposed again — but this time with the Sinclair family concert party allowed to vote.

- The rejected non-execs have always been re-appointed at these subsequent general meetings:

| 2017 | 2018 | 2019 | |

| AGM | |||

| Votes FOR | 126k (13%) | 220k (19%) | 179k (16%) |

| Votes AGAINST | 827k (87%) | 927k (81%) | 938k (84%) |

| Subsequent GM | |||

| Votes FOR | 2,361k (74%) | 1,504k (62%) | 2,094k (69%) |

| Votes AGAINST | 826k (26%) | 941k (38%) | 939k (31%) |

- When announcing the AGM result in August, MTVW said:

“The Directors will engage with shareholders to obtain feedback on their concerns and will publish an update on that engagement within six months of the date of the Annual General Meeting. “

- When announcing the result of the subsequent general meeting in November, MTVW said:

“As communicated at the General Meeting today, since the Annual General Meeting the Company has sought to engage with shareholders as to their views on the above re-appointments. The Company is disappointed, that there was a significant minority vote (being more than 20 per cent) against each of the Resolutions. As we have done previously, we will continue to seek to engage with independent shareholders to take into account their concerns and considerations in the future.”

- I am not sure whether this second statement counts as the “update on that engagement” mentioned after the AGM.

- 7 February 2020 marks six months from the AGM when the “update on that engagement” has to be published.

- An interesting footnote to the Sinclair family concert party is this announcement from October:

“In September 2013, the Concert Party entered into a revised agreement (the “Concert Party Agreement”) setting out certain terms of conduct between members of the Concert Party including the event of an offer being made for the Company. The concert party members are not bound under the terms of the Concert Party Agreement to vote together at a general meeting of the Company. In October 2016, the Concert Party Agreement was extended for a period of three years; this extension came to an end, in accordance with its terms, at 5.00pm on 30 September 2019.

The Concert Party is in discussions to extend the Concert Party Agreement for a period of three years, until 30 September 2022. A further announcement will be made once this has been completed.”

- An extension to the concert agreement has yet to be announced, which may suggest the discussions have not been straightforward.

Valuation

- MTVW could be worth more than £200 per share — assuming all of the group’s regulated tenancies were to end immediately and the properties were then all sold at a fair market value.

- The following table outlines my latest sums:

| Property stock Sept 2014 (£k) | 317,651 |

| Less property stock sold since Sept 2014 (£k) | (99,098) |

| 218,553 | |

| Allsop-vs-book multiple | 2.10 |

| Sold-vs-Allsop multiple | 1.43 |

| 655,133 | |

| Property stock purchased since Sept 2014 | 173,902 |

| Sold-vs-Allsop multiple | 1.43 |

| 248,680 | |

| Possible property stock value (£k) | 903,813 |

- I have taken the original September 2014 portfolio value of £318m and subtracted the £99m book value of properties sold since that date.

- I have then multiplied the £219m remainder by my 2.1x ‘Allsop-vs-book’ multiple and then by the 1.43x ‘sold-vs-Allsop’ multiple witnessed during this first half.

- I arrived at a £655m estimated value for all of MTVW’s properties that were owned at September 2014 but have yet to be sold.

- Since September 2014, MTVW has spent £174m buying additional properties.

- I have assumed all of these additional properties can be sold one day for £249m based on my 1.43x ‘sold-to-Allsop’ multiple.

- Adding the £655m and the £249m together gives £904m.

- This next table adjusts that £904m for 19% taxation, other investments, net debt and other liabilities to give a possible book value of £787m or £202 per share:

| Possible property stock value (£k) | 903,813 |

| Less tax at 19% (£k) | (97,158) |

| Plus other investments (£k) | 25,091 |

| Less net debt (£k) | (39,955) |

| Less other liabilities (£k) | (4,366) |

| Possible NAV (£k) | 787,425 |

| Possible NAV per share (£) | 201.95 |

- These sums are not perfect. In particular, no allowance has been made for properties purchased and sold after September 2014.

- In addition, the September 2014 valuation— and Allsop’s original £666m verdict — is now very stale.

- The major question of course remains how long MTVW will take to sell all of its properties to realise my potential £202 per share NAV guess.

- At the August AGM, management claimed there was “still enough business out there for another 15 to 20 years.”

- Patience will undoubtedly be required for the underlying value of the property portfolio to be realised.

- Mind you, the longer the disposals take, the higher house prices should rise and the greater proceeds MTVW ought to eventually achieve from its future sales.

- MTVW’s £96 per share book value — calculated with the properties accounted for at cost — covers 81% of the £118 share price.

- The trailing 400p per share dividend supplies a 3.5% income at £118.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in Mountview Estates.

Dear Maynard

I enjoy very much your annual report. I have always liked Mountview, but it is one of several companies where the “family” have a controlling stake. Compare say North Midland Construction. But if they keep the div up I will keep buying.

I, being cautious, tend to split the portfolios I advise on to go say 80/20 on 80 being bog standard FTSE and 20 punting.

I quite like Breedon as a punt, went and had a look at some of the quarries, they have obviously spent a lot of money on the infrastructure, and should have a stranglehold on these products, which I guess will flow as the new government start spending.

No dividend as yet, but capital growth interesting.

Also punted Strix and Forterra.

Hmm

As explained earlier, I am not much of a number cruncher.

Best wishes for 2020 and keep up your great emails.

best wishes

Bertie

Hi Bertie,

Thanks for the comment. Always good to know people like the emails! I hope your portfolio fares well this year and your 20% punts come good!

Maynard

Mountview Estates (MTVW)

The Sinclair Family Concert Party and Update on 2019 AGM voting outcome

Just catching up with these statements from January and Feburary.

I wrote in the blog post above:

An extension to the concert agreement has yet to be announced, which may suggest the discussions have not been straightforward.

MTVW stated in January:

“The Company had previously notified its shareholders of the existence of a concert party consisting of certain members of the Sinclair family, related Sinclair family trusts and companies under the control of certain Sinclair family members (the “Concert Party”), as more particularly set out in the Appendix to this announcement.

On 2 October 2019 an announcement stated that the Concert Party were in discussions to extend the concert party agreement for a further three years to 30 September 2022. The Company now announce that all the members of the Concert Party have entered into a new agreement containing an extension of the period to 30 September 2022 as well as acknowledgment between the members of the Concert Party of the regulatory obligations arising from the existence of the Concert Party.

The Concert Party have control of voting rights over 1,995,075 ordinary shares representing 51.17 per cent of the Company’s share capital.”

So no change there.

I also wrote in the blog post above:

7 February 2020 marks six months from the AGM when the “update on that engagement” has to be published.

The engagement update was published on 10 February. Here is the text (my bold):

In accordance with Provision 4 of the UK Corporate Governance Code, the Company is providing the following update to the 2019 AGM voting results made on 8 August 2019 regarding the significant vote against a number of resolutions:

Resolution 5: re-election of Mrs M.L. Jarvis as a director of the Company

Resolution 6: re-election of Mr A. W. Powell as a director of the Company

Resolution 8: to approve the Directors’ Remuneration Report

Resolution 9: to re-appoint Messrs BSG Valentine as auditors of the Company

In addition, Resolutions 11 and 12, to re-elect Mrs M.L Jarvis and Mr A.W. Powell as directors of the Company, were not approved by a majority of the Company’s independent shareholders. At a subsequent general meeting held on 19 November 2019, as the Company was entitled to convene in accordance with the FCA’s Listing Rules, both Mrs M.L. Jarvis and Mr A.W. Powell were re-elected as directors of the Company.

Following the 2019 AGM in August and prior to the general meeting held on 18 November 2019, the Company identified as far as possible those shareholders who did not support the various resolutions and attempted to engage with them to seek their views. They declined to meet or engage. The Company remains committed to shareholder engagement and we will continue to offer to meet with shareholders to take into account their concerns and considerations in the future.

Not sure why the dissident shareholders — the Murphy family with a 24% stake and few others — declined to meet the board. From my AGM notes, I recall Craig Murphy and the chairman both referring to a meeting last year between the parties, but a difference of opinion was given by each as to what was actually said.

Maynard