02 January 2026

By Maynard Paton

This post provides a ‘year in review’ of all my portfolio holdings.

I recap how each business performed during 2025 as well as provide a few remarks about their attractions, drawbacks and valuations. I have accompanied every write-up with a ShareScope chart to show how each company has progressed over the longer term.

I undertook the same review process at the start of 2015, 2016, 2017, 2018, 2019, 2020, 2021, 2022, 2023, 2024 and 2025.

I have now decided to stop blogging about my shares and I trust you find this final annual review informative.

Maynard Paton

Contents

- S & U

- System1

- Mountview Estates

- Bioventix

- City of London Investment

- M Winkworth

- FW Thorpe

- Andrews Sykes

- Mincon

- Tristel

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, FW Thorpe and M Winkworth. This blog post contains ShareScope affiliate links.

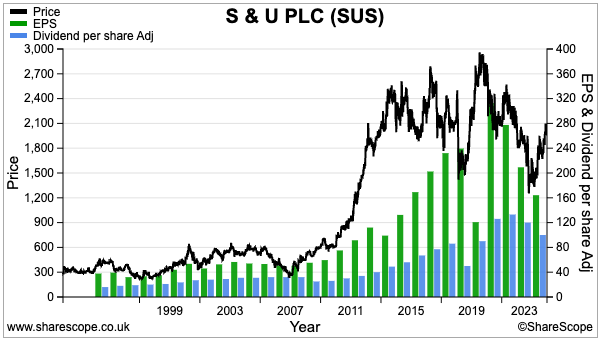

1) S & U (SUS)

- Bid-price: £20.90

- Market cap: £254m

- Portfolio weighting: 18.1%

SUS was by some distance my best performer of 2025.

The pivotal news emerged during August, when the Supreme Court overturned a previous legal judgment and ruled ‘secret’ motor-finance commissions were not in fact ‘bribes’ paid by lenders to car dealers.

Up until that verdict, SUS’s shares had been suppressed by potential compensation claims facing the group’s motor-finance division. I had estimated the total payout could have amounted to £63m or £5 a share.

The icing on the Supreme Court cake was greater clarity on what constituted an “unfair” motor-finance commission. SUS anticipates redress for such “unfair” commissions will have a “minimal” impact on its motor-finance progress.

The group’s motor-finance progress should now be free of regulatory as well as legal interventions.

For much of 2024 and 2025, SUS had been subject to an FCA section 166 investigation to ensure the motor-finance division conformed to the new Borrowers in Financial Difficulty and Consumer Duty regulations.

At times during the 166 process, I did think car-loan repayments had become optional for borrowers who did not feel like repaying and who remarkably could not be told about potential repossessions.

The combined legal and regulatory difficulties had a notable impact on SUS’s trading. April’s FY 2025 results for example showed profit down 29% following motor-finance write-downs surging 47%. The annual dividend was cut by 20p to 100p per share.

But October’s H1 2026 figures showed profit rebounding 22% after SUS shifted towards higher-quality borrowers and car-loan write-downs reduced by 56%. SUS in fact used those H1 results to announce its first dividend improvement for two years.

December’s trading update was very encouraging, showing new motor loans running close to a record 25k/year and collection rates setting a new 93.4% high. The update included particularly bullish comments on arranging “substantially larger” borrowing facilities to fund future growth.

After a year or two languishing well below the £19-£20 per share net asset value (NAV), the share price has only very recently traded above NAV following SUS’s increasingly upbeat tone. Last year I bought at £14.64 (Q2) before the Supreme Court verdict and at £18.64 (Q3) after the Supreme Court verdict.

I first invested during 2017 at £21 and bought again at £19 (2019) and £17 (2020). I have never top-sliced, mostly because I have genuine faith in the group’s veteran executives. They steward a 50%-plus family shareholding and have overseen NAV advancing 39x and the dividend expanding 40x since 1987.

My SUS buy report | All my SUS posts

2) System1 (SYS1)

- Bid-price: 220p

- Market cap: £29m

- Portfolio weighting: 16.9%

What a mess SYS1 has become.

A bombshell warning during September prompted me to tell the board — face-to-face at the AGM the next day! — how the executives had completely lost touch with the business. I am not sure present management can remain credible after revising full-year revenue guidance from 15% growth down to 0% growth within less than three months.

I am now convinced the only way SYS1 can truly maximise the value of its “world class platform and product suite” is through selling itself to a larger competitor led by competent directors.

Last year had actually started very promisingly for the ad-testing specialist.

Shareholders had just been presented with an upgraded “illustrative growth scenario” that claimed an extra £2m investment could help deliver a tantalising 20-30% platform-revenue CAGR that implied a “longer term” £36m Ebitda.

January’s Q3 statement then brushed off economic concerns by suggesting H2 revenue could be better than expected. The statement also lifted profit guidance for the full year.

April’s Q4 update in contrast contained some ominous developments, not least referring to “downside risks” to client budgets and much slower growth within the group’s important US market.

July’s in-line FY 2025 results were accompanied by a Q1 update that showed revenue down 7% alongside that aforementioned — and what we know now to be irresponsible — 15% revenue-growth projection for FY 2026.

I bought SYS1 at 325p (2016), 238p (2018), 183p (2020) and 242p (2021), and much to my regret have never sold a single share. With hindsight I should have followed the unhappy German shareholders and exited entirely at 430p during 2023.

Instead I imagined SYS1’s promising transition from bespoke consultancy towards automated ‘platform’ services — plus refreshing talk of establishing a “performance culture” — could deliver multi-bagger returns. I started 2025 with SYS1 supporting 38% of my portfolio after lamenting how I sold other multi-baggers far too early.

I note AI featured very prominently during October’s Capital Markets Day, and I have a strong suspicion clients diverting to AI may have caused the September warning. For what it may be worth, December’s H1 2026 results talked about a “stronger start” to H2. You may wish to read my forthright results feedback to SYS1’s broker Canaccord.

A priority task for me during 2026 is deciding how and when I can exit this somewhat illiquid share with the 220p bid-price back at levels first witnessed during 2011.

My SYS1 buy report | All my SYS1 posts

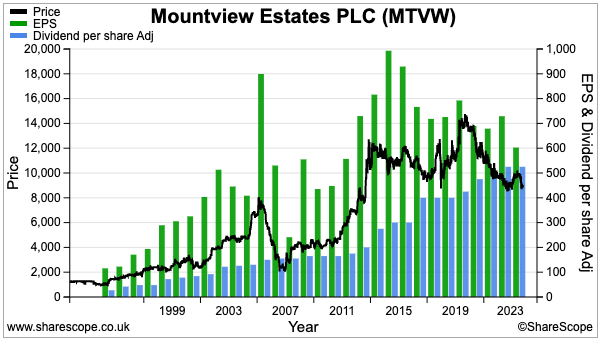

3) Mountview Estates (MTVW)

- Bid-price: £89.00

- Market cap: £347m

- Portfolio weighting: 14.6%

Wishful thinking probably, but could MTVW be about to go into ‘run off’?

November’s H1 2026 results were notable for disclosing a complete absence of property purchases. The regulated-tenancy landlord has purchased properties during every H1 and H2 since at least H1 2007, signifying the decision not to buy is at the very least extremely unusual.

Mix in the fact MTVW deployed a considerable £40m, £45m and £53m on additional properties during the preceding three years, and the sudden spending cessation becomes all the more intriguing.

Maybe the board has (finally) realised regulated tenancies no longer generate the long-term returns they once did.

In particular, during the 2010s and before, property-sales gross margins typically averaged approximately 60%. But June’s FY 2025 figures revealed a sub-60% gross margin for the fourth consecutive year. November’s H1 meanwhile showed a 46% gross margin — the lowest since H1 2009 when property prices were reeling from the banking crash.

Doubts about future returns probably explain why the £89 bid-price is at a level first achieved during 2014 and 14% below the £103 per share net asset value.

Unfavourable EPC legislation alongside a consistent “economic difficulties” narrative are other explanations why the stock market remains wary.

I first bought during 2011 at £42, bought more at £98 (2018 and 2019), bought more at £96 (2024) and have never sold — primarily because the business is simple, the assets seem safe and the valuation has always looked cheap.

MTVW’s trading properties are carried at cost and I estimate NAV — up 42x since 1985 — could eventually realise approximately £170 per share. The dividend — up 117x since 1985 — meanwhile supports a near-6% income.

Note that MTVW’s ownership structure draws a very fine line between ‘value bargain’ and ‘value trap’. The chief executive’s 50% family concert party dictates proceedings and overlooks ongoing AGM protest votes from his sister (15% ownership and speaks for 24%) and property tycoon David Pears (7% ownership).

I had hoped MTVW’s new non-executive might have found favour with dissenting shareholders last year. But her replies during a lively 2025 AGM — not least wondering why attendees were “fixated” by (the lack of) independent valuations — suggest she supports the intransigent board.

Still, there’s always the chance MTVW will indeed go into ‘run off’ and distribute of all its profits through dividends. After all, the entrenched chief exec is 78, has no obvious successor… and must at some point decide how MTVW will operate without him.

My MTVW buy report | All my MTVW posts

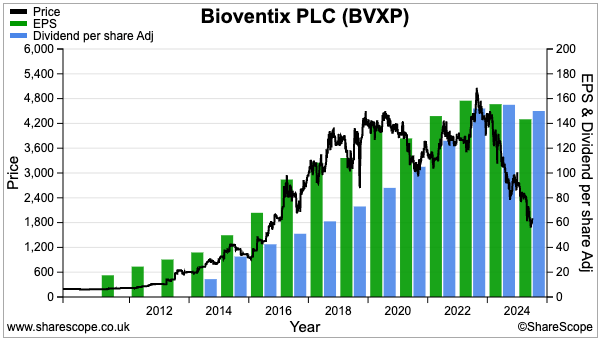

4) Bioventix (BVXP)

- Bid-price: £18.20

- Market cap: £95m

- Portfolio weighting: 13.0%

BVXP was my largest top-up idea of 2025: I increased my holding by approximately 145% (Q1, Q2) at a £29 average. My previous purchase was undertaken at £11 (2016) and I have never sold.

This year’s top-up was unfortunately very misjudged. I can now see I was too enthusiastic about the prospects for the company’s Alzheimer’s R&D and not careful enough about the threat of lower-priced Chinese competition.

The board of the diagnostic-antibody developer was also caught out by China. Attendees at the 2024 AGM were reassured Chinese rivals were more focused on developing new antibodies and how switching from BVXP products remained “non-trivial” for Chinese customers.

Fast forward to October’s FY 2025 results, and BVXP admitted revenue had declined 4% because its Chinese sales had plunged 27%. Some 18% of revenue remains derived from China and presumably is now at risk of further disruption.

Attendees at the 2025 AGM were actually told BVXP would “still have a Chinese business in 2030“, but the accompanying explanation was very vague. I am not entirely convinced the board has suddenly become more enlightened about Chinese progress between the two AGMs. No wonder the shares dived 41% last year.

I am far more convinced about BVXP’s Alzheimer’s R&D.

October’s results confirmed six prototype antibodies for detecting the very early signs of Alzheimer’s had moved into full-scale production and were being testing by at least five commercial partners. BVXP said the testing volumes were “much higher than… previously expected“.

Remarks during the 2025 AGM included talk of an Alzheimer’s antibody perhaps becoming commercial during 2027. Comments also included using the company’s £5m cash position to help fund R&D and support the dividend (to “show confidence” about the “exciting future“).

The dividend remains the principal source of return as the shares languish at levels first achieved during 2017. The payout was trimmed by 5p to 150p per share last year and, if maintained for 2026, would yield close to an astonishing 8%.

Despite the Chinese disruption, BVXP’s wonderful royalty model continues to enjoy superb economics. A stratospheric 76% of revenue was converted into profit last year, partly because BVXP’s physical antibodies sell for up to £208k a gram and only 16 people are employed in the company’s small lab.

The chief executive founded BVXP, still owns 6% and seems very positive about the Alzheimer’s R&D. I trust I do not misinterpret his AGM remarks again during 2026.

My BVXP buy report | All my BVXP posts

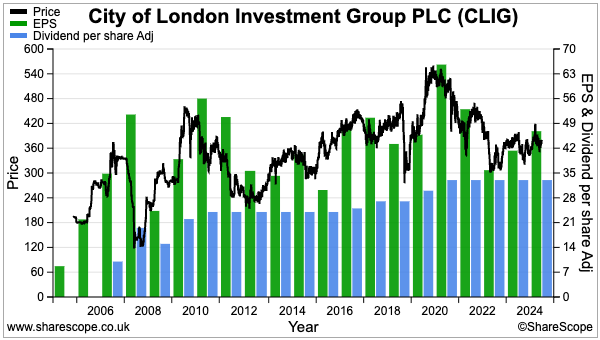

5) City of London Investment (CLIG)

- Bid-price: 365p

- Market cap: £185m

- Portfolio weighting: 11.6%

My portfolio’s most welcome RNS of 2025 was this fund manager announcing the departure of its chief executive.

The outgoing boss had taken charge during 2019, oversaw the merger with Karpus Investment Management during 2020… and then watched clients withdraw a net $2.2b.

Some $1b was withdrawn during FY 2025 alone — rather alarming when total client money is approximately $11b — and action had to be taken to stop the exodus.

The replacement chief exec has yet to be recruited, and the chairman reckons the ideal candidate will possess “the drive and commercial acumen to propel our firm to the next level.”

Remarks during the 2025 AGM summarised the task ahead for the new leader: “Find us new places to get money. The shareholders want capital inflows. That’s the priority.”

But that task could be difficult when global trackers boast three-year 20% CAGRs and have trounced CLIG’s ‘ye olde value’ approach of buying investment trusts at wide discounts.

Searching for the new chief exec commenced during June and I had expected an appointment by now. I am hopeful details will emerge during early 2026 — otherwise shareholders will start to worry nobody suitable is willing to take on the role.

The search for fresh leadership means a lot of pressing issues will now sit on the back burner. In particular, fees continue to be squeezed by those clients remaining loyal to the original City of London division (I estimate from 82 to 67 basis points since FY 2019).

Employee pay is another topic the new boss must consider. The average salary has advanced 29% since FY 2022 while the dividend has remained unchanged at 33p per share. The profit-share pool, the share incentive scheme and the lack of individual KPIs are other matters for reassessment.

The standstill dividend supports an astronomic 9% yield but was covered only 1.1x during FY 2025. Further client-money withdrawals, fee-rate cuts and/or employee-pay rises could compress medium-term earnings and hurt the payout. But last year’s 41% margin plus $35m net cash should support my income for 2026.

The saving grace here remains George Karpus, who heads a 38% concert party and during the 2023 AGM demanded the board “be replaced with a seasoned group of directors”. I trust he will berate the board once again if the new chief exec disappoints.

I invested initially at a 281p average (2011-2013), but sold 42% of those shares at 335p (2015). I then bought more at 350p (2022), 320p (2023) and 332p (2024).

My CLIG buy report | All my CLIG posts

6) M Winkworth (WINK)

- Bid-price: 182p

- Market cap: £23m

- Portfolio weighting: 9.4%

This time last year I asked if WINK had put itself up for sale.

The appointment during 2024 of two non-executives with extensive corporate-finance backgrounds certainly suggested the estate-agency franchisor was at least contemplating some M&A activity.

But after attending WINK’s 2025 AGM, I must confess to be in two minds about a possible buyout.

A bid could of course deliver a useful short-term capital gain. However, shareholders would then have to reinvest in a business that is also:

- Run by owners (WINK’s family management holds 47%);

- Focused on dividends (the payout has doubled in 10 years), and;

- Valued with a decent yield (c7%) to sustain a similar quality and level of income.

And I do like WINK’s quarterly payouts, which may well be unique on AIM.

Board remarks at the 2025 AGM unsurprisingly did not hint at any M&A action. Attendees were instead told the appointment of the new non-execs was a move to “rejuvenate the board” (their predecessors were in their 80s).

The AGM was in fact a very refreshing affair because attendees did not have to concern themselves with any bombshell profit warning, ongoing protest votes, heightened Chinese competition or a sudden leadership change.

The convivial meeting reflected a positive FY 2024, results for which were published during April and showed franchisees lifting their income by 12% that raised WINK’s own revenue by 17% and underlying profit by 24%. Buoyed by group net cash that remains at £4m, this year’s Q1, Q2 and Q3 payouts were all lifted a very welcome 10%.

WINK’s headline progress is somewhat distorted by its three (stop press: now two) company-owned offices, which at the last count ran close to breakeven as the up-and-coming (employed) agents in charge aim one day to become (self-employed) branch franchisees.

WINK’s real value is within the the franchising division, which collects an 8% slice (plus other fees) from all commissions generated by the 100-branch franchisee estate. This division delivered a remarkable 29% pre-tax margin during 2024.

Swapping lacklustre franchisees with “best-in-class” replacements should help WINK prosper even if housing transactions remain subdued within its core London market. The board has also expressed caution about the consequences of new rental legislation, and future earnings may become more volatile if branches increase their dependence on sales transactions.

My initial WINK buy occurred at 90p during 2011 and I sold 70% at 173p (2013 and 2014). I then topped up at 116p (2016 and 2017) and 178p (2021).

My WINK buy report | All my WINK posts

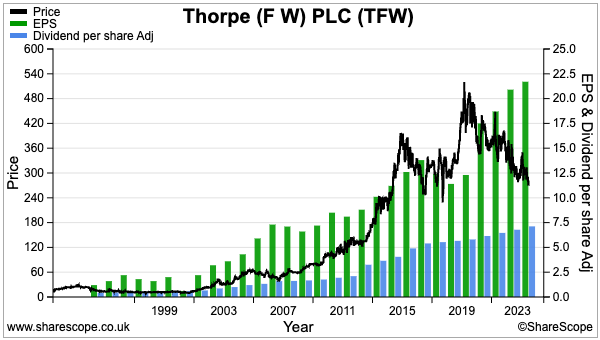

7) FW Thorpe (TFW)

- Bid-price: 274p

- Market cap: £326m

- Portfolio weighting: 5.6%

I am pleased TFW combining the roles of chief executive and finance director during 2024 did not create any obvious adverse developments during 2025.

Mind you, October’s FY 2025 results did show revenue flat at £176m and operating profit flat at £33m… and I still can’t recall another quoted business the size of this industrial lighting specialist entertaining such a powerful executive position.

At least TFW’s board remains reassuringly staffed by two Thorpe-family non-executives, who:

- Spent their careers overseeing the group;

- Have (presumably) accrued plenty of knowledge about leadership appointments, and;

- Risk an aggregate 43% shareholding if the management composition has been misjudged.

The stagnant FY 2025 performance belied disparate subsidiary performances. The group’s main division, Thorlux, reported profit up 7% while Spanish unit Zemper lifted profit by a super 27%. Counterbalancing such positive progress was divisional Dutch profit plunging 28%.

The annual dividend meanwhile advanced a helpful 5% to extend TFW’s run of consecutive payout increases to a terrific 23 years. Margins remain healthy, with 19% of annual revenue converting into profit, and net cash now tops a mighty £60m.

I speculate a large portion of that £60m will eventually be spent on European acquisitions. The last decade has witnessed TFW spend c£80m — with another c£10m earmarked for final earn-outs — on businesses within the Netherlands, Spain and Germany.

The FY 2025 statement said “various acquisition opportunities were investigated” although none were “deemed suitable”.

Even after their recent profit dive, the Dutch businesses have proven to be very smart purchases. Zemper meanwhile is finally starting to show real promise following four years of TFW ownership. But German firm SchahLED is sadly struggling with a domestic recession.

TFW’s immediate outlook is not incredible after November’s AGM indicated “results to date are in line with last year”. But long-term demand for the group’s energy-efficient lighting — this recent case study boasts an annual energy saving of 84%! — ought not to diminish.

Indeed, lighting R&D continues apace, including “dynamic” exit signs deployed at Brussels airport within an “adaptive evacuation system designed to revolutionise how buildings respond to emergencies“. Thorlux’s SmartScan wireless lighting system meanwhile remains “among the most widely adopted in the industry”.

Although the shares are back to levels first reached nine years ago, the 12-13x P/E is also the lowest for ten years. I first bought TFW during 2010 at 69p, added more at 80p (2011) and 89p (2012), and sold 25% at 234p (2016).

My TFW buy report | All my TFW posts

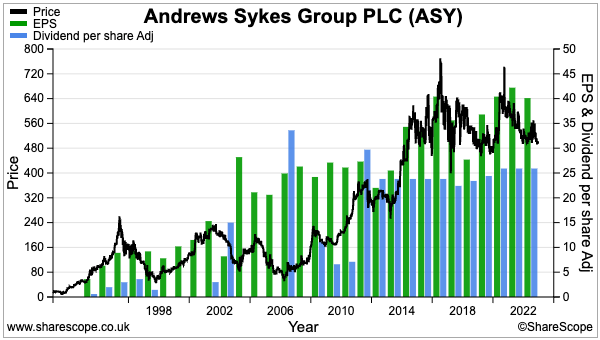

8) Andrews Sykes (ASY)

- Bid-price: 480p

- Market cap: £201m

- Portfolio weighting: 2.8%

I am convinced ASY has transformed its working practices.

May’s FY 2024 results showed a remarkable headcount of 446 — the lowest since at least FY 2004. Revenue per employee since FY 2019 has in fact surged 31% to £170k as the equipment-hire outfit pruned 25% of its workforce.

Maybe the Covid lockdowns inspired new ways of working. Or maybe the fresh leadership appointed during 2021 has had an impact. Or maybe the hire-equipment ASY suppplies no longer needs as much manual intervention.

Either way, a tip-top workforce underpins ASY’s “premium level of service 24 hours per day, 365 days per year” that in turn allows the group to become “the preferred supplier to many major businesses and operations spanning a huge range of industries and geographic locations“.

The equipment supplied is predominantly water pumps, air conditioners and heaters — demand for which is prompted by heavy rain, heatwaves and cold snaps respectively. But the weather during the last few years has not been too kind to ASY.

The UK did not experience another 2022 40-degree summer during 2023, 2024 or 2025, while September’s H1 statement admitted “one of the driest springs on record” had (again) left both revenue and profit unchanged. Revenue for FY 2025 looks set to be less than reported for FY 2018.

At least ASY’s accounts remain pristine. Highlights include net cash last seen at £23m and the greater employee efficiency pushing the annual margin to a super 31%. However, hire-equipment productivity remains flat. For some years now, £1 invested in new kit continues to earn £1 of annual revenue.

Growth is most likely to be driven by extra European depots, revenue from which has more than tripled since FY 2009 to support almost a third of the top line. But overseas progress has not always been straightforward; the recent closure of the six-depot French subsidiary was particularly disappointing.

The shares trade at levels first achieved eight years ago and do not seem extravagantly valued at 12-13x earnings and yielding c5%. I purchased at 233p during 2013 and have never top-sliced.

I hope to attend the 2026 AGM and discover what has supported the greater employee productivity. I also want to understand the potential for the group’s fledging water-treatment service.

And I trust I can speak to the Murray family — who own 91% of ASY — to judge the ‘delisting risk’ and likelihood of earnings continuing to be mostly distributed through ordinary/special dividends.

My ASY buy report | All my ASY posts

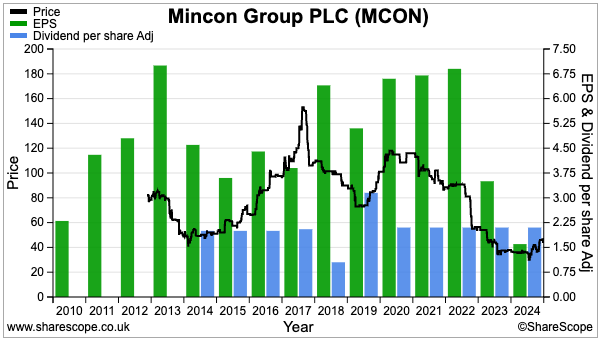

9) Mincon (MCON)

- Bid-price: 43p

- Market cap: £91m

- Portfolio weighting: 1.6%

This time last year I confessed ‘life events‘ had prevented me from spending time evaluating MCON during 2024. I then spent very little time monitoring the Irish drill manufacturer during 2025 and really have no idea what has been happening.

So imagine my relief when two renowned UK small-cap investors — Richard Penny of Oberon Investments and Laurence Hulse of Onward Opportunities — recently disclosed owning MCON during separate Vox Markets podcasts.

Rather than revisit two years of overlooked results, I will instead rely on these two experts for this year’s MCON text :-)

Both men were excited about MCON’s new-but-still-being-tested Greenhammer drill. Mr Penny reckoned the drill could be “totally transformational“:

[Richard Penny December 2025]

“Where it gets really interesting is a product called Greenhammer, which is a hydraulic rather than a pneumatic product, and gives you more energy at the point of interface with the rock. Basically it’s 55% to 60% more productive.

It’s now with Atlas Copco in a copper mine in Arizona. The addressable market here is c1,000 rigs in North America with the addressable size of the market some 15 times MCON’s existing revenue.

But the share price is a third of what it was when people were excited about this. It seems to be happening. Seems to be robust. It seems to work. Greenhammer is not going to be an overnight success. But potentially it’s totally transformational.”

Mr Hulse was meanwhile projecting profits to triple:

[Laurence Hulse December 2025]

“Our simplistic thesis is margins recover from 6% back to kind of 13%. And with some higher turnover from new products, especially Greenhammer, in simplistic maths we see profits trebling…If the 12-13x rating stays flat, the shares should treble to boot.

We like this one. If there wasn’t the large family stake and it wasn’t exposed to capital projects, this would have all the makings of a core holding for us. But a 3x-er from some kind of fairly formulaic catalysts is super attractive. It’s got a brand. It’s got a balance sheet trading at a discount to NAV. Profits can grow and customer markets are improving. There’s a lot to like here”.

MCON first mentioned Greenhammer to shareholders during early 2017 and I believe development work started five years before that.

Messrs Penny and Hulse have not held MCON shares for long, so they have not yet had the, er, ‘full experience’ of Greenhammer delays. But their stock-picking records are far better than mine and I am willing to trust their judgement.

I paid 45p for MCON during 2015 and have never sold. Until I listened to those podcasts, I had assumed I was the only UK investor who had ever heard of — let alone owned shares in and (once) blogged about — this Irish business.

My MCON buy report | All my MCON posts

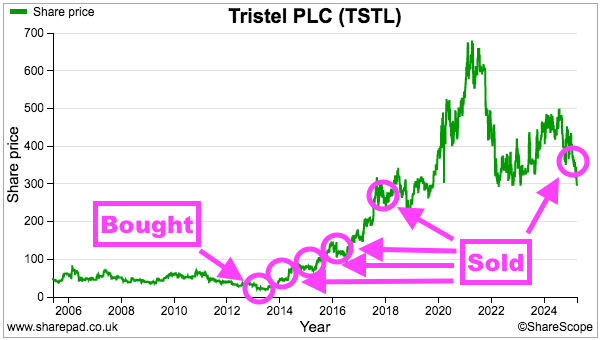

SOLD) Tristel (TSTL)

I exited TSTL at 352p including all costs at the start of 2025 (Q1).

The disposal marked the end of an eleven-year investment that at one point rallied 14x following my 46p purchase during 2013 and 2014. Although I sold well below the very top, I did manage a respectable 408% total return of which dividends represented almost 60 percentage points.

Before last year, I had sold at 79p during 2014, 100p during 2015, 123p during 2016 and 289p during 2017p:

When I sold my shares, I wrote:

“TSTL’s executives never truly convinced me and over time the board has evolved into a depressingly standard set-up that seemingly prioritises management over shareholders.

…

I was particularly irritated by the board devising an LTIP while the new chief executive had yet to announce the group’s financial targets (and still hasn’t).How can shareholders be sure the new LTIP correlates with those targets?

…

Paying the former chief exec a year’s salary as a “retirement package” also seemed extremely generous given his long-time ‘over-promising and under-delivery’ of TSTL’s US expansion.“

Seems like TSTL shareholders have now woken up to the board’s remuneration behaviour. A 41% protest vote was lodged at the recent AGM:

[TSTL RNS December 2025]

“Resolution 1, which sought to receive and adopt the Company’s annual accounts for the financial year ended 30 June 2025, together with the Directors’ report, the Directors’ remuneration report and the auditor’s report on those accounts, passed with 59% of votes cast.

With respect to this resolution the Company received notice from one of the proxy voting advisers that they were recommending investors to vote against it, due to lack of a separate vote for remuneration policy and the level of loss of office payment to a former Director accompanied by limited disclosure.

Resolution 1 has been discussed with several of the institutional shareholders and within the Board. The Board undertakes that it will ensure any necessary future disclosure complies with best practice, along with committing to put the remuneration policy to a separate vote at future AGMs, in line with QCA guidance.

The Company would like to reiterate that it takes its shareholder responsibilities seriously and has a clear focus on striving for governance best practice, sharpening capital allocation and driving sustainable growth.“

The 2025 accounts showed the former chief executive receiving a £365k payment in lieu of notice and a further £375k “retirement package“.

The former chief exec was married to TSTL’s (now former) finance director, which I speculate allowed the couple to hold sway over the board… until reality dawned about the former chief exec’s persistent ‘over-promising’ of the US potential.

Then last year the (now former) finance director suddenly resigned. I had regularly highlighted TSTL’s prior-year restatements and therefore always had some suspicion about the accuracy of the group’s financial reporting.

Blog reader Roger kindly alerted me to a former TSTL employee stealing £84k from the group under the watch of the (now former) finance director. I speculate news of this deception becoming public last year and the sudden search for a new finance director were not a coincidence.

The 2025 accounts show the (now former) finance director collecting a £260k payment in lieu of notice.

The pay-offs to the former executives total a nice round £1m, which seems a lot of compensation for effectively being fired after their leadership shortcomings were finally exposed.

System1 (SYS1)

H1 2026 group investor presentation hosted 05 December 2025

I attended SYS1’s H1 2026 results presentation that was conducted online to selected investors (mostly from small fund managers). House broker Canaccord always requests feedback, and I am always happy to oblige. Thought I would publish this feedback to a wider audience:

—————————

Hi Canaccord,

Thanks once again for the call invite and I did attend. Always happy to supply feedback.

Lots of forthright points below. I am happy for you to attribute all the comments to me.

Regards,

Maynard

—————————

* Lack of management credibility: Following September’s update and as I stated at the AGM: i) management has completely lost touch with the industry/business and should now be replaced, and; ii) SYS1 should be sold to a larger operator that can maximise the IP and extract full value for shareholders. That view has not changed.

* Format: Call was much more useful this time as management skipped the basics, went straight into the details and opened up to Q&A early on.

* Q&A: I did not ask questions as the investment case with SYS1 really depends on the board’s (or John Kearon’s) desire to create shareholder value and not the nitty-gritty H1 details. Call lasted only 40 minutes with some awkward silences when waiting for questions, which might suggest other investors are not 100% sure about management’s credibility either.

* KPIs: Slide deck did not show NRR nor reiterate the past ‘illustrative growth scenario’ that touted future 30% Ebitda margins. But at least the call did disclose 84% NRR and SYS1 not going back on the 30% Ebitda-margin target.

* NRR: Call claimed 84% NRR was not shown on slides due to potential confusion, yet no such confusion arose in the past when the figure surpassed 100%. Would not have been hard to construct a trailing 12-month NRR figure as per FY 25’s 106% for this H1. Lack of public NRR disclosure implies management somewhat embarrassed about the 84% and about to quietly drop the measure.

* 30% Ebitda margin: Management with real conviction about the 30% Ebitda-margin target — and associated ‘illustrative growth scenario’ — really ought to keep such details in the slides for all to see. Margin-target absence from latest slides suggest management is withdrawing the past optimism that justified extra £2m expenditure. Withdrawal of the ‘illustrative growth scenario’ reminds me of that £1billion market-cap ambition from a few years ago — a very punchy public goal that was also withdrawn from the slides and clearly nonsensical now.

* Public webinars: Management has seemingly given up on hosting public post-results webinars on InvestorMeetCompany. Not sure why. Gives the impression of not wanting to answer awkward results questions on the record. Not the behaviour I would expect from a corp-gov award-winning board.

* Lower-than-expected H1 revenue: Explained on the call as clients i) creating less content for testing; ii) creating same content level but testing less, and/or iii) going elsewhere for testing.

Call claimed iii) was least likely as clients normally have only one ad-test supplier and clients were still spending at SYS1. But go back to July’s FY 25 group call, and management claimed SYS1 could ‘double in size’ were the business to have ‘full share of wallet’ with its top 10 UK/US clients,.

Not having ‘full share of wallet’ in July suggested clients then had multiple ad-test suppliers. So this call provided contradictory comments about how many testing suppliers clients employ, which does imply management is not on top of the business — and which creates greater credibility doubts.

Plus…management on the call made an alarming off-the-cuff remark about not counting every single ad test that clients had performed in this H1 versus the comparable H1. Management said this exercise ‘might be quite helpful’ to do (!!!). Last time I looked, SYS1 was a data business… and information about client testing volumes really should be at management’s fingertips. Underlines the impression the executives are just not on top of the business.

Indeed, SYS1 tests every new UK/US advert, so management should know the volume of new adverts from clients and the industry generally. Correlate the volume of new adverts to the volume of testing from clients, and management should be able to reasonably judge how much of September’s warning was due to i) or ii) or even iii).

* Trading narrative: General management commentary on the call was one of SYS1 being impacted by macro events. In contrast, the upbeat performances of the prior two years was previously described as being due to SYS1’s super platform and taking market share from incumbents with a better/faster/cheaper service. If SYS1’s progress really was tied to macro events, then it would not have enjoyed those two years of major industry outperformance. Management had regularly said SYS1’s market share is tiny compared to the huge TAM, and a genuinely disruptive better/faster/cheaper service with minimal market share should still have a 100%-plus NRR despite macro events. In short: out-of-touch management is blaming macro events when in reality SYS1 now faces being disrupted itself…

* AI: I have a strong suspicion AI is disrupting SYS1’s business and led to the September warning. October’s CMD was dominated by AI and this call had lots of unprompted AI talk as well. Prior to October, SYS1 barely mentioned AI in its decks. The CMD was postponed from May to October, and I suspect the first rumblings of AI disruption prompted the postponement and a re-jig of what was to be presented. Coke is once again using AI to create its Xmas ads — presumably to save money. Coke may well be the thin end of the AI wedge that will force ad-testing rates to reduce commensurately.

* Revenue guidance: Management comments on the call referred to ‘the madness kicked off in January’ and ‘strange stuff’ happening when the £2m extra investment was announced this time last year. Seems as if management now admits trading was somewhat peculiar in December/January, which does again beg the question why management then issued the bullish (15% FY growth) guidance in July.

* New business: Call said new business might be £9m for FY 26 versus £8m for FY 25. Seems encouraging that clients such as Dr Pepper and Disney+ have signed up, but are we to really believe such multinationals use only one ad-testing service? Also, if new business increases by £1m for FY 26 but overall FY 26 revenue is flat, then this implies the new clients of FY 25 will spend less during FY 26 than they did during FY 25… which does not sound promising. Seems like the new clients of FY 25 — having ‘traded down’ to SYS1 — are now ‘trading down’ to AI or in-house testing.

* Incumbents: Call said Kantar, Ipsos and Nielsen ‘probably have done relatively well’ versus smaller outfits such as SYS1 of late, perhaps due to offering a wide range of services. Validates the argument for SYS1 to become part of a larger group, whereby proper management and a proper global sales force can finally maximise the commercial value of SYS1’s IP.

* USA: Where’s Mike Perlman? Has been part of SYS1 for almost two years as chief commercial officer and responsible for USA revenue in particular (one of SYS1’s three strategic goals). CMD really could have done with Mike P explaining the USA opportunity and what exactly the SYS1 sales team does to ‘land and expand’ clients beyond podcasts and LinkedIn. Call talked about ‘small’ USA clients spending £1m, so huge USA potential that has (mysteriously) never been properly showcased to ordinary shareholders.

* Ad-testing database: Described on the call as the ‘crown jewel’ but admitted ‘not articulated well enough’ to clients, as every client should be subscribed. Database has been available since 2018/19, so really has become a failure of the leadership team to exploit it.

* Long-term shareholder failure: Shares at c200p are now back to a level first achieved in 2007 and witnessed on numerous occasions in the last 18 years. Common denominator of the long-term failure to build sustainable shareholder value is John Kearon, whose 20%-plus shareholding has always dictated SYS1’s board composition and working culture.

I can only conclude John K is not concerned about creating sustainable shareholder value, but rather enjoying a ‘lifestyle’ business with an emphasis on keeping him and his team popular within industry circles. I find it telling senior employees have failed to perform satisfactorily enough to collect any LTIP shares since 2017 and currently look on course to extend that failure to 2029.

The EGM in 2023 attempted to instigate board changes to maximise the IP value, and for the following two years the board suddenly became energised to accelerate the platform strategy to keep dissident shareholders happy.

But the unhappy German shareholders were (with hindsight) clearly alarmed at something, selling out completely last year at a steep discount to the then prevailing share price. The German exit has left the board free from another major protest vote, and so John K’s haphazard working culture of the past has quickly re-emerged and here we are (yet again) with the shares at 200p.

Management has been oblivious to industry events and now seems to be playing catch-up with clients shifting to AI. September’s warning clearly exposed management’s shortcomings and who now can trust executives that can so badly over-promise and under-deliver in the space of three months?

The fact the chairman (and presumably the other non-execs) is very supportive of the executives is truly shocking. The non-execs really should have read the Riot Act to the executives on behalf of outside shareholders in September — but instead they remain comfortable taking their fees, ticking a few boxes and not causing a fuss… their cosy roles protected of course by John K’s major shareholding.

John K really needs to wake up, realise the value of his life’s work is on the line, clear out the current board and install a batch of competent new execs/non-execs to restore SYS1’s fortunes and then sell the business to a larger operator to maximise the IP value. If the board’s status quo is maintained, shareholders at best face many years of value stagnation and at worst SYS1 risks complete AI disruption.

Thank you so much for all your hard work over the last decade. I have been a regular and avid reader. You have taught me a great deal, and I will continue to learn from you, even though you will no longer be publishing your blog. I wish you all the very best for the future, and know mine will be better for having read your fine work. Thank you again.

Thanks for this instructive summary of your portfolio developments, and all the best!