16 May 2023

By Maynard Paton

Results summary for Mountview Estates (MTVW):

- A positive H1 2023 performance, with revenue up 21% and profit up 17% due to property selling prices gaining 19% and a greater number of properties sold.

- A significant £26m spent on new properties implies buying opportunities are emerging as “difficult times” and “economic storms” are forecast.

- A 54% sales premium was realised against the 2014 Allsop valuation, and the remaining Allsop-valued properties now represent less than half of the property estate.

- Net debt remains very modest at just 6% of the property estate and allowed the welcome declaration of a 250p per share/£10m special dividend.

- The £115 shares trade at a lowly 13% premium to net asset value, which inched higher to a fresh £102 per share high, although the balance sheet could one day still be worth £200 per share. I continue to hold.

Contents

- News link, share data and disclosure

- Why I own MTVW

- Results summary

- Revenue, profit, dividend and net asset value

- Trading properties: gross margin and rental income

- Allsop valuation

- Financials

- Concert party, protest votes and shareholder engagement

- Valuation

News link, share data and disclosure

News: Interim results for the six months to 30 September 2022 published 24 November 2022

Share price: £115

Share count: 3,899,014

Market capitalisation: £448m

Disclosure: Maynard owns shares in Mountview Estates. This blog post contains SharePad affiliate links.

Why I own MTVW

- Buys, holds and sells regulated-tenancy (and similar) properties and boasts an illustrious, 40-year-plus history of net asset value and dividend advances.

- Board led by veteran family management that continues to boast an aggregate 50%/£226m shareholding.

- Properties are carried at cost, and when eventually sold at their ‘reversionary’ values may generate total proceeds significantly in excess of the recent market cap.

Further reading: My MTVW Buy report | All my MTVW posts | MTVW website

Results summary

Revenue, profit, dividend and net asset value

- The preceding FY 2022 results expressing caution about “difficult economic circumstances“…

“As we now enter a period of what are expected to be difficult economic circumstances…”

- …and restraint towards property buying opportunities…

“We believe that our decision… to stick to our principles of risk management and not chase purchases at any price is proving a sound one that will protect shareholder value going forward.”

- …had already set the tone for an unspectacular H1 2023 statement.

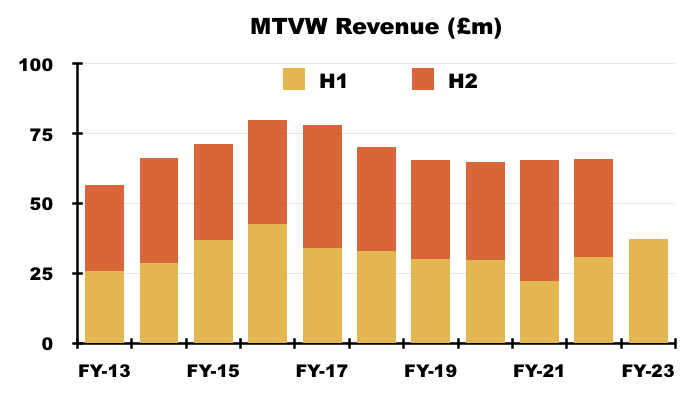

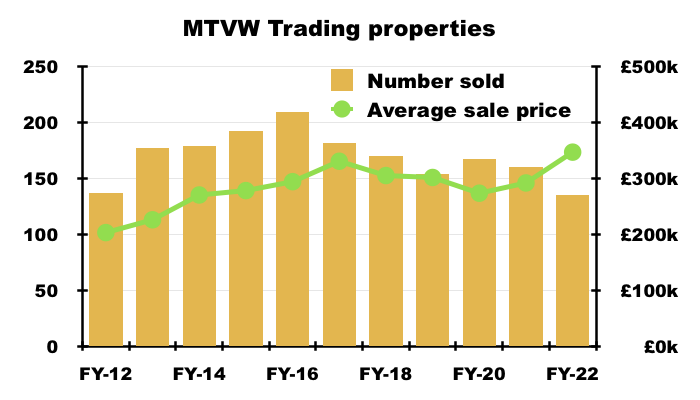

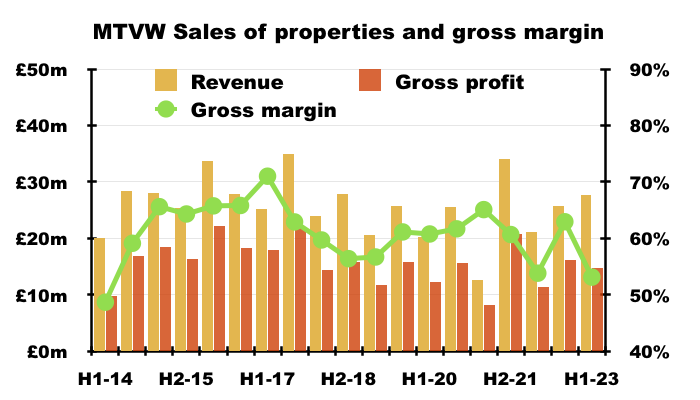

- But these six-month figures in fact showed revenue up 21% to beyond £37m, the highest H1 level since H1 2016 (£42m):

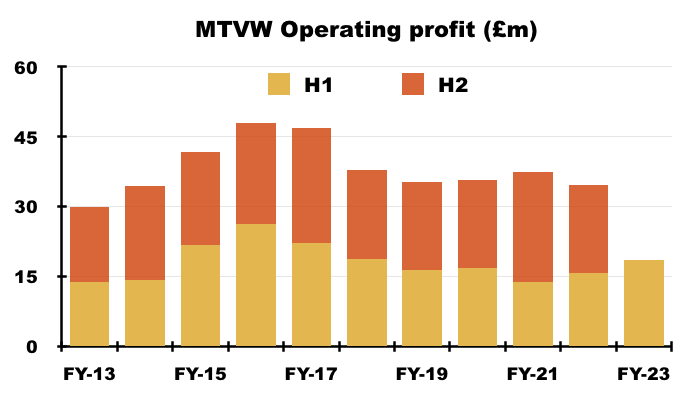

- Operating profit climbed 17% to £18.5m, the highest H1 level since H1 2018 (£18.6m):

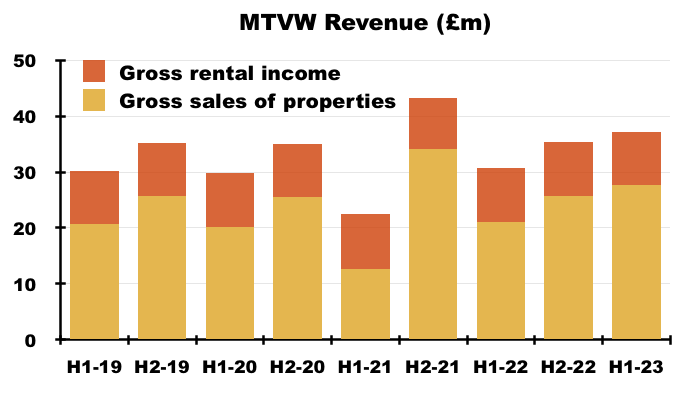

- Revenue was split 74%/26% between property sales and rental income, which matched MTVW’s preceding ten-year average (73%/27%):

- Note that MTVW sells its regulated-tenancy properties only when the tenancy ends — which typically occurs when the tenant dies (point 5a).

- The mix of properties becoming available for sale — and the total proceeds MTVW earns — can therefore vary significantly from one set of results to the next.

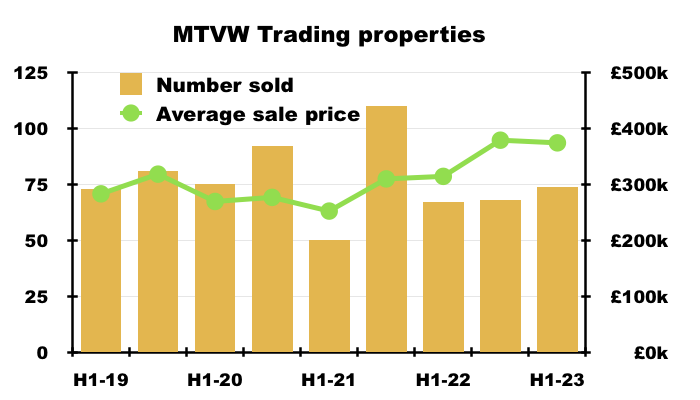

- The 74 properties sold during H1 2023 compared to 67 during the comparable H1 2022 and 68 during the preceding H2 2022:

- The 143 run-rate of properties sold remains historically low versus the five years to FY 2018:

- The silver lining to MTVW preferring to “not chase purchases at any price” is favourable sale prices. The average price achieved from the properties sold during this H1 remained elevated at £374k — up 19% versus the £314k achieved during the comparable H1 2022.

- The £374k average price perhaps reflects the “different type of purchaser” MTVW said had been attending auctions during FY 2022:

“On the purchase side, the tail end of Covid-19, and in particular the stamp duty holiday, attracted a different type of purchaser into the auction rooms who was willing to buy regulated tenancies at smaller discounts than we believed was reasonable.“

- Still, suitable buying opportunities appear to have re-emerged. This H1 said:

“Our purchasing activity has been strong during these six months and our long standing financial prudence keeps us in position to take advantage of further good purchasing opportunities.”

- MTVW in fact managed to spend £26m on new properties during this H1 (see Financials).

- MTVW continued to express caution about the wider economy:

“We are all aware that difficult times lie ahead but the financial strength of this Company should enable us to weather the economic storms that lie ahead better than most.”

“We all know that times are going to be tough, but I believe that this Company is better placed than most to survive the difficulties and indeed prosper. “

- Most of MTVW’s properties are located within London and south-east England, and are of relatively low value.

- Of the 74 properties sold during this H1, 54 achieved less than £500k and just one raised more than £1m:

- A good chunk of this H1’s terse 511-word statement was devoted to denouncing government policy:

“Boris Johnson “got Brexit done” nearly three years ago. We have learnt to live with Covid although it will never have just gone away. Last Thursday (17 November 2022) we were told how the Government plan to recover the vast sums of money that bureaucratic profligacy spent in trying to help the country through the various economic travails.

This Company did not furlough any staff, did not reduce staff numbers in any other way and did not take any government assistance. However as a successful company we are obliged to help repay the government’s debt.”

- I speculated within my FY 2022 write-up about another special dividend:

“With MTVW presently struggling to find suitable purchasing opportunities, perhaps excess cash flow can instead deliver further special dividends and temporarily enhance that 3.6% yield.”

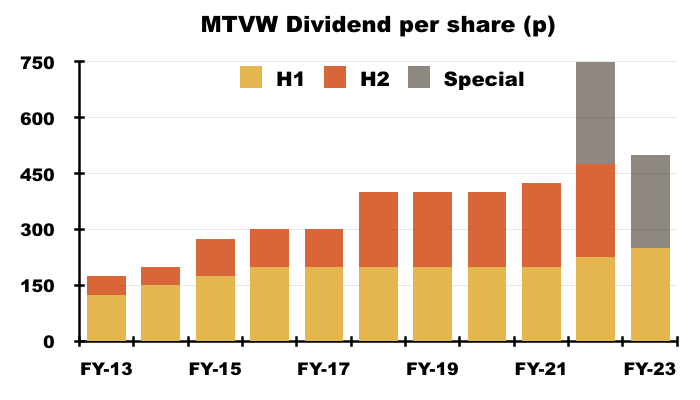

- Sure enough, the highlight of this H1 was a 250p per share special dividend that followed the 275p per share extra payout declared during the comparable H1 2022:

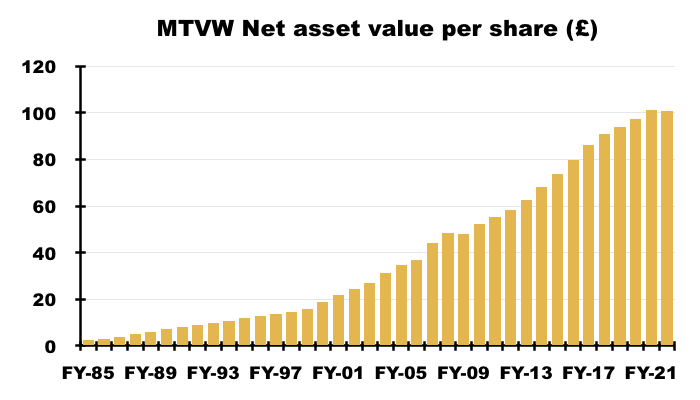

- Net asset value (NAV) ended the half at £398m, or £102 per share, which struck a new NAV record and compared to £393m six months earlier:

- The ordinary H1 dividend advanced 11% to 250p per share, which was 11% better than MTVW had anticipated during the comparable H1 2022. Back then MTVW suggested the H1 payout would be maintained at 225p per share:

“It is not anticipated that this interim dividend will limit the final dividend payable in August 2022 in any way, but it would be prudent to presume that the interim dividend payable in March 2023 will be maintained at the new increased level of 225p per share.“

- This H1 gave a similar standstill expectation towards the H1 2024 dividend:

“The Board is confident that the Company remains in a strong position to make further purchases and to meet all its regular outgoings including the final dividend payable in August 2023. However it would be prudent to only anticipate an interim dividend payable in March 2024 at the increased basic rate of 250p per share.”

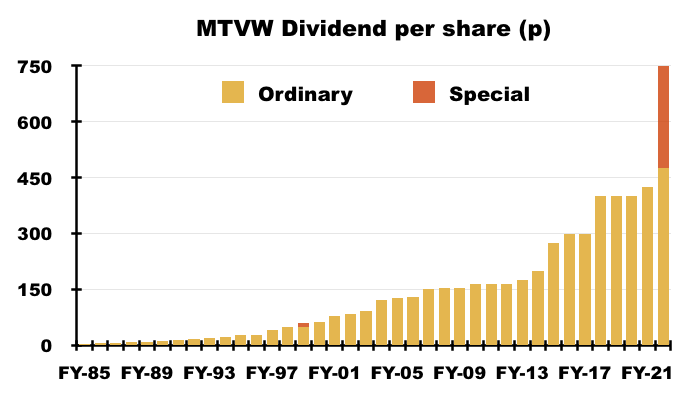

- Companies House shows the dividend has never been cut since at least 1979 — after which the payout has risen 317-fold:

Trading properties: gross margin and rental income

- Similar to revenue, MTVW’s margin and profit can also fluctuate due to the unpredictable mix of properties becoming available for sale during any particular period.

- The percentage gain on each property sold — reflected by MTVW’s gross margin — is typically correlated to the duration of MTVW’s ownership, which can range from a few years to a few decades.

- A 53% gross margin was achieved through property sales during this H1:

- The 53% property-sales gross margin was the lowest since H1 2014 (49%).

- A property-sales gross margin of 53% is equivalent to buying a property for £100k and selling it for £213k.

- For perspective, during the previous 20 years MTVW has only twice recorded annual property-sales gross margins below 55%:

- FY 2014 (54.8%), and;

- FY 2009 (43.2%).

- A 53% property-sales gross margin is therefore very unusual, especially as average selling prices remain at an elevated £374k.

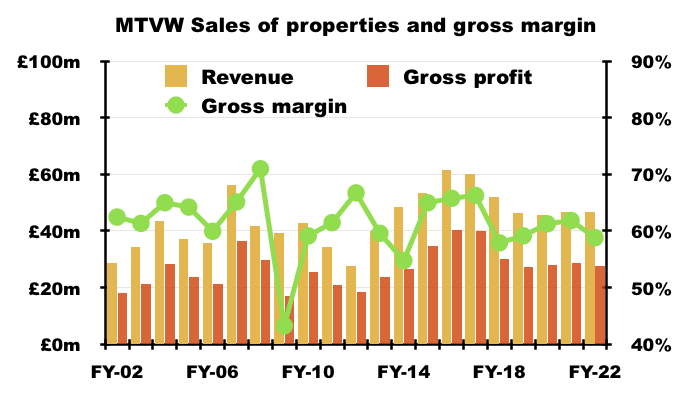

- But the mix of properties sold tends to even out over time. MTVW’s average property-sales gross margin over five-year periods has been remarkably consistent:

- FYs 2018 to 2022: 60%

- FYs 2013 to 2017: 62%

- FYs 2008 to 2012: 60%

- FYs 2003 to 2007: 63%

- A more typical gross margin of 60% is equivalent to buying a property for £100k and selling it for £250k.

- Emphasising the gross-margin fluctuations due to the unpredictable mix of properties becoming available for sale, the aforementioned 49% property-sales gross margin for H1 2014 was followed by a super 66% property-sales gross margin for H1 2015.

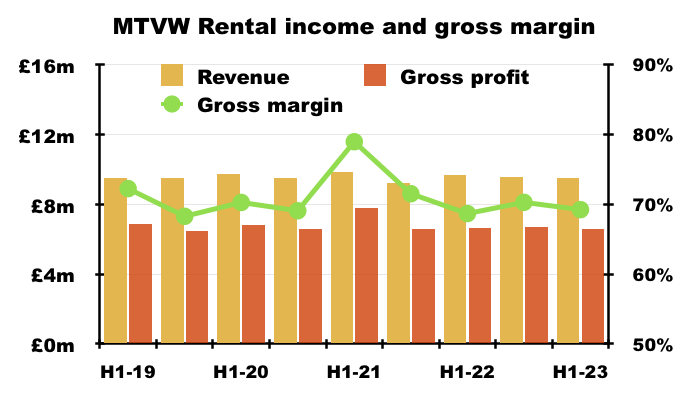

- MTVW’s rental-income gross margin remained at a normal 69% after certain maintenance work was deferred during the pandemic:

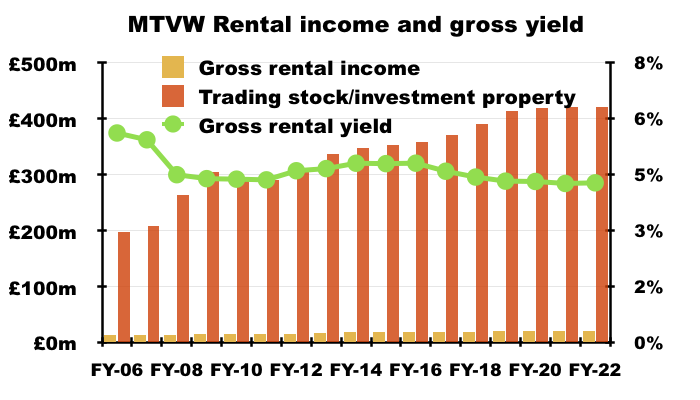

- Trailing twelve-month rental income was £19m and gave a 4.5% rental yield from the carrying value of all properties:

- That 4.5% rental yield is the lowest since at least FY 1998 and supports MTVW’s decision to “not chase purchases at any price”.

Allsop valuation

- A disappointing development during this H1 concerned the proceeds from sold properties compared to a past valuation.

- To recap, MTVW commissioned property agent Allsop during September 2014 to assess the group’s estate.

- Allsop returned a £666m valuation — some 2.1x the £318m book value of the properties owned at the time.

- The Allsop assessment was based on MTVW’s properties remaining in their regulated-tenancy state and therefore excluded any ‘reversionary’ gain (i.e. the value uplift that occurs when a regulated tenancy finishes, the rent reverts to a proper market level and the property can then be sold at a fair market value).

- The Allsop assessment was not applied to the audited accounts. MTVW’s properties instead remain on the balance sheet at their cost price.

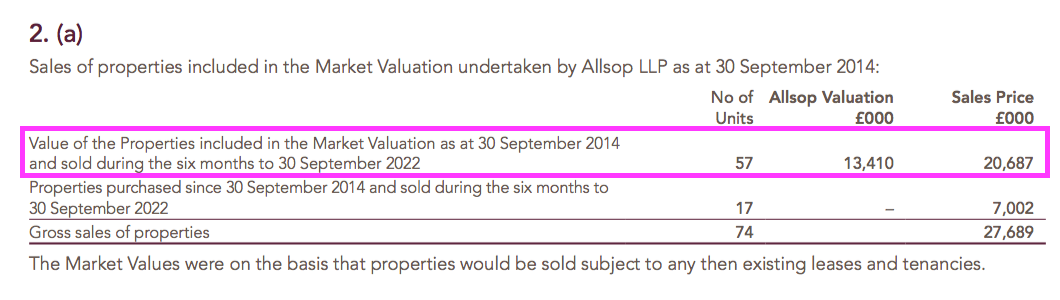

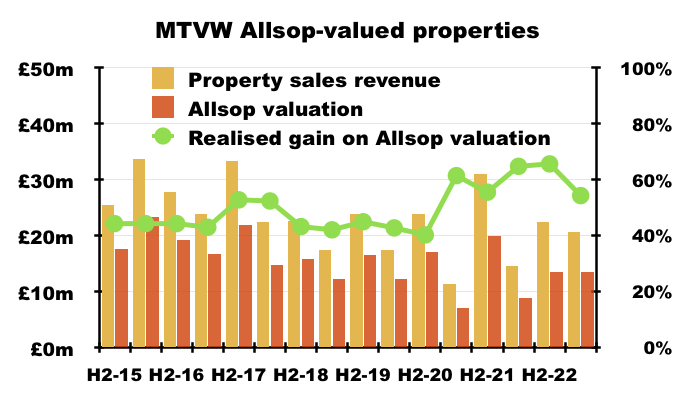

- Following the Allsop assessment, MTVW reveals the proceeds from sold properties versus their Allsop valuation:

- This H1 witnessed MTVW sell properties with a combined £13.4m Allsop valuation for £20.6m.

- Prior to the pandemic, premiums of between 43% and 53% on the Allsop valuation were realised on sales proceeds:

- But the preceding FY 2022 statement showed realised gains on the Allsop valuation at a terrific 65%.

- This H1 showed the premium falling back to 54%.

- MTVW’s results commentary has never referred to the Allsop valuation since the assessment was undertaken.

- As such, shareholders are left to guess whether the premium reverting to 54% was due simply to FY 2022’s terrific 65% level being supported by an unusually favourable mix of sold properties…

- …or something more untoward.

- The lower realised gain versus the Allsop valuation has implications for estimating MTVW’s potential share price (see Valuation).

- During the eight years following the Allsop assessment, MTVW has raised £372m from selling properties that the agent had valued at £250m.

- Selling properties that Allsop had valued at £250m implies the book value (i.e. the original cost) of the properties sold was £119m (£250m divided by that aforementioned 2.1x multiple).

- Selling Allsop-valued properties with a £119m book value indicates Allsop-valued properties with a £198m book value remain within MTVW’s ownership today (i.e. the £318m book value at the September 2014 assessment less the £119m since sold).

- MTVW during this H1 and the preceding H2 sold Allsop-valued properties with an estimated book value of approximately £13m, which indicates the remaining Allsop-valued properties of £198m could take a further 15 years to sell.

- This H1 showed total trading properties with a £407m book value, implying properties purchased after the Allsop review have a £208m book value (i.e. £407m less the remaining Allsop-valued properties of £198m).

- For the first time, the book value of Allsop-valued properties represents less than half of MTVW’s property-trading estate (£198m/£407m = 49%).

- Bear in mind the figures above are guesstimates (and include rounding ‘errors’) and could be rather inaccurate.

- As more Allsop-valued properties are sold and other properties are purchased, the less relevant the 2014 Allsop valuation becomes to the share price.

- MTVW refuses to undertake another Allsop-type valuation.

- The 2022 annual report reiterated the following text from previous years (point 5c):

“The [Allsop] valuation is not a useful tool for running the business because we are always going to await vacant possession, and no perceived uplift in value can justify selling a tenanted property. The nature of our business and the rules and conventions under which we operate place no obligation upon us to value our trading stock at any given time and therefore the valuation has not been updated since.”

- During the 2021 AGM, the board:

- Repeated it was “reluctant to inflict shareholders the cost” of another assessment;

- Disclosed Allsop was paid £600k for the 2014 assessment, and;

- Described the expense as a “substantial amount for something of very little use”.

- I maintain MTVW ought to implement regular valuations to provide greater clarity as to the inherent value of the group’s property estate.

- Further valuations would help shareholders judge the astuteness of MTVW’s more recent purchases and perhaps the appropriateness of the board’s pay (point 4f).

- Mind you, the Sinclair family’s 50.4% concert party leads MTVW (point 3d), and the long-term dividend and NAV records do not suggest the other 49.6% of shareholders have been hard done by through a lack of formal valuations (see Concert party, protest votes and shareholder engagement).

- September 2024 will mark ten years since the Allsop valuation was undertaken.

Financials

- MTVW’s accounts remain very straightforward.

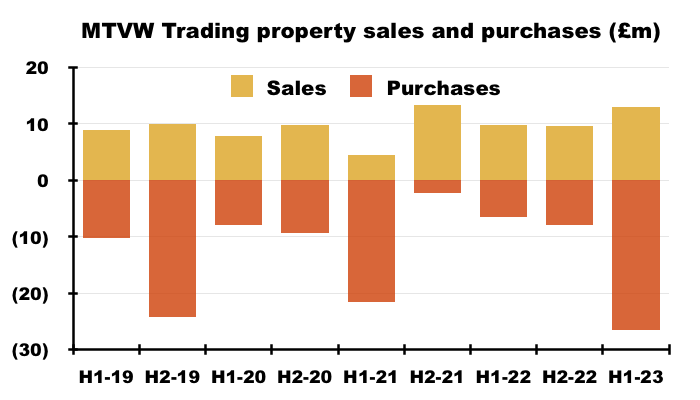

- Some £26m (after acquisition expenses) was used to acquire new properties during this H1:

- The £26m was the highest amount spent during a six-month period since H2 2018 (£43m), and exceeded the twelve-month expenditure for FYs 2020 (£17m), 2021 (£24m) and 2022 (£14m):

- The £26m expense signals MTVW finding notable buying opportunities despite average sales prices remaining at the aforementioned elevated £374k.

- MTVW does not disclose the number of properties acquired within its H1 statements, but will do so for the full year within the 2023 annual report.

- The expenditure on new properties left free cash flow for his H1 at just £1m.

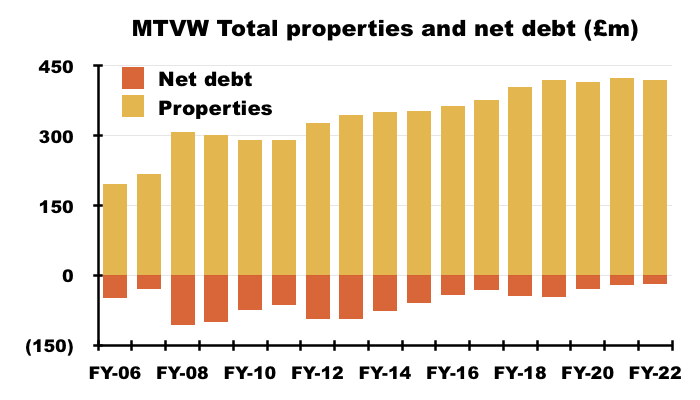

- Then paying the £10m FY 2022 final dividend during this H1 caused net debt to increase by £9m to £27m.

- Net debt of £27m is equivalent to 6% of the group’s £432m total property estate — historically very low versus the 25%-plus levels witnessed during FYs 2008, 2009, 2010, 2012 and 2013:

- Finance costs of £336k for this H1 exceeded the ultra-low £298k for FY 2022, and implied a manageable 2.8% annualised interest rate on the six month’s £24m average debt.

- The annual-report small-print disclosed banking facilities of up to £90m (point 5e).

- The modest gearing plus ample debt headroom suggest MTVW would have no problem acquiring property bargains should any “difficult times” and “economic storms” emerge.

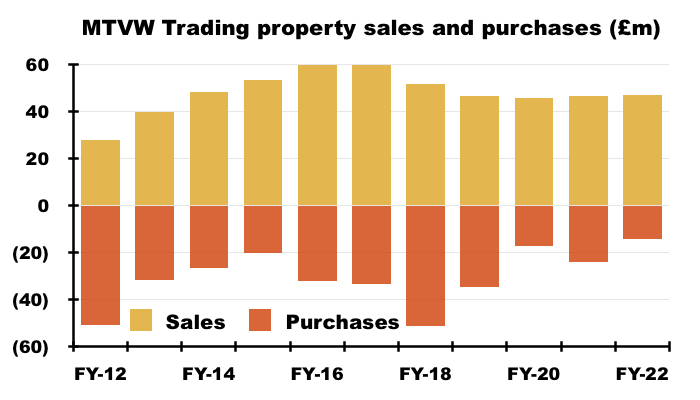

- The £26m spent on new purchases puts FY 2023 on track to be the first year since FY 2012 when MTVW buys more properties than it sells.

- But the market for MTVW’s regulated tenancies is always shrinking, and MTVW will at some point go into ‘run off’ and consistently sell more properties than it buys.

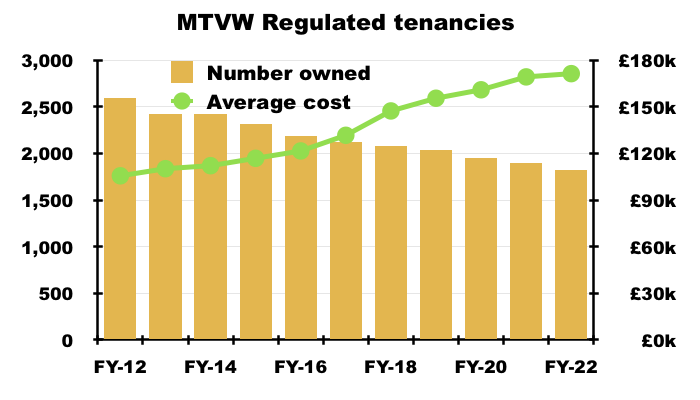

- Regulated tenancies have (with limited exceptions) not been created since 1989 and Allsop estimates fewer than 75,000 now exist.

- The number of regulated tenancies owned by MTVW topped 3,000 20 years ago, topped 2,500 ten years ago but at the end of FY 2022 was approximately 1,800:

- MTVW’s conventional investment properties remain in the books at £25m or £6.53 a share.

- MTVW’s accounts remain free of defined-benefit pension obligations.

Concert party, protest votes and shareholder engagement

- MTVW’s shareholders fall into three camps:

- The Sinclair family concert party, which is led by chief executive Duncan Sinclair and controls 50.4% of the share count;

- The Murphy family and connected parties, who claim to own 24% of the share count and whose leading shareholder is the chief executive’s sister, and;

- Everybody else, who own approximately 25% of the share count.

- The 50.4% holding makes the Sinclair concert party MTVW’s controlling shareholder, which under stock-market rules has to enter a ‘relationship agreement’ with MTVW to comply with certain ‘independence provisions‘.

- The bombshell iEnergizer (IBPO) delisting has brought controlling shareholders into greater focus, although I doubt the Sinclair concert party will take MTVW down the same private-company route.

- Reasons to be optimistic about an ongoing market quote for MTVW include (point 3d):

- The Sinclair concert party has only a very slim majority of shares (50.4%);

- The concert party is represented by numerous family members, not all of whom will want to be ‘trapped’ in an unlisted business;

- The ‘minority’ 49.6% already consists of unhappy shareholders prepared to vote regularly against the board, and;

- MTVW trades on the main market while most delisting shenanigans occur on AIM.

- A statement during November 2022 carried this interesting snippet:

“The members of the Concert Party have re-affirmed to the Company that the Concert Party remains in place though they have decided that a formal agreement is no longer needed.“

- This particular agreement relates to the “code of conduct” between concert-party members, and scrapping the formal version could allow the membership to become a little more fractured…

- …which may have implications as to how votes are cast at shareholder meetings.

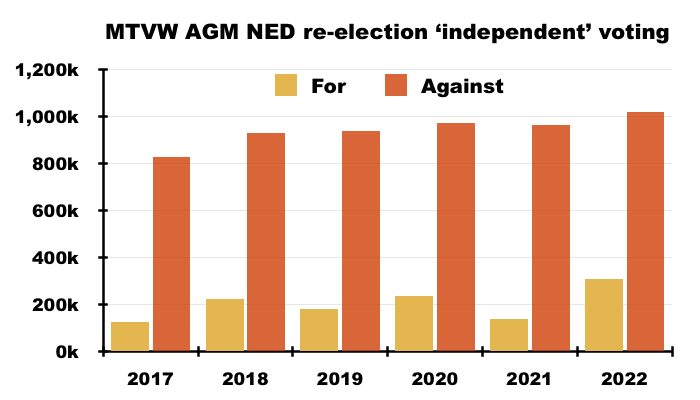

- MTVW’s last six AGMs have witnessed c30% protest votes against:

- Re-electing independent non-execs;

- Approving the board’s pay, and;

- Re-appointing the auditors.

- The protest votes come from the Murphy family and connected parties.

- From what I can tell, the Murphy family is broadly satisfied with how MTVW’s day-to-day operations are run, but:

- Is aggrieved about the board’s pay;

- Has lost the trust of the non-execs to act on the views of all shareholders, and;

- Is frustrated about a general lack of influence at board level.

- The Murphy family stated during the 2021 AGM that it was no longer in direct communication with the company and would engage with the directors only through a “public forum“.

- The Murphy family and other unhappy shareholders have prevented the re-election of certain non-execs at the last six AGMs:

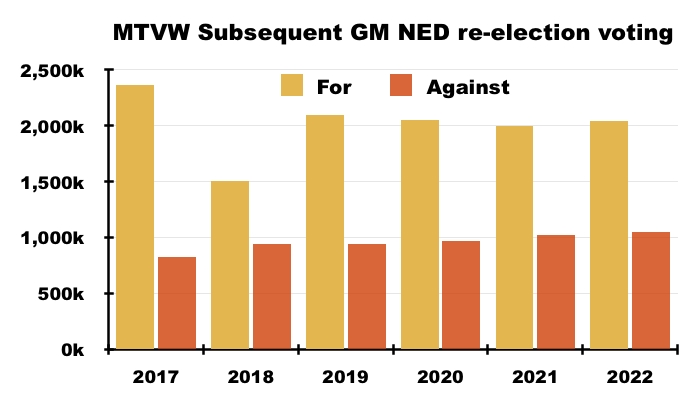

- Following each AGM, MTVW is entitled to convene a general meeting and hold a further vote to re-elect the ousted non-execs.

- The ousted non-execs have (to date) all been re-appointed at the subsequent general meetings because the Sinclair concert party can then vote on the non-exec re-elections (unlike at the AGMs, where the concert party is prohibited from voting on particular ‘independent’ resolutions):

- The voting charts above show the average votes for and against the re-election of the contentious non-execs. The average protest votes against are slowly increasing, rising from 826k to 1,050k since 2017.

- Stock-market rules dictate any company incurring a 20%-plus AGM or EGM protest vote has to contact the unhappy investors and publish an update to shareholders within six months.

- Six months after the 2022 AGM, during February 2023, MTVW stated:

“Following the 2022 AGM, and as it has done previously, the Company identified as far as possible those shareholders who did not support the various resolutions and attempted to engage with them to seek their views. Those shareholders did not wish to engage. The Company remains committed to shareholder engagement and we will continue to offer to have discussions with shareholders and will take into account their concerns and considerations in the future.”

- Whether any dissident shareholders are engaging privately with MTVW is hard to say.

- But twelve AGM/EGM protest votes since 2017 suggest any engagement that has occurred has fallen on deaf ears.

Valuation

- MTVW’s shares could be worth £200, assuming all of the group’s regulated tenancies end immediately and the properties then fetch a fair market value.

- The following table outlines the sums:

| Property stock Sept 2014 (£k) | 317,651 |

| Less sold Allsop-assessed stock (£k) | (119,189) |

| 198,462 | |

| Allsop-premium-to-book | 2.10x |

| Sold-premium-to-Allsop | 1.54x |

| 640,672 | |

| Stock purchased since Sept 2014 | 208,350 |

| Sold-premium-to-Allsop | 1.33x |

| 277,105 | |

| Possible property stock value (£k) | 917,777 |

- I have taken the original September 2014 estate value of £318m and subtracted the (estimated) £119m book value of Allsop-assessed properties sold since that date.

- I then multiplied the £198m remainder by the 2.1x ‘Allsop-premium-to-book’ multiple and then added a 54% ‘sold-premium-to-Allsop’ gain that was enjoyed during this H1.

- I arrived at a £641m estimate for all of MTVW’s properties that were owned at September 2014 but have yet to be sold.

- Since September 2014, MTVW has acquired additional properties with a £208m book value.

- I have assumed these additional properties can be sold for a total £277m based on management comments of wishing to buy properties at 75% of their fair market value (i.e. the ‘reversionary’ gain will be 33%).

- Adding the £641m and the £277m together gives £918m.

- This next table adjusts that £918m for 25% taxation, the £25m conventional property portfolio, net debt as well as other liabilities to give a possible book value of £782m or £200 per share:

| Possible property stock value (£k) | 917,777 |

| Less tax at 25% (£k) | (127,741) |

| Plus other investments (£k) | 25,451 |

| Less net debt (£k) | (27,072) |

| Less other liabilities (£k) | (6,697) |

| Possible NAV (£k) | 781,718 |

| Possible NAV per share (£) | 200.49 |

- Bear in mind my estimated value of MTVW’s property estate has not really improved during recent years. Previous estimates were:

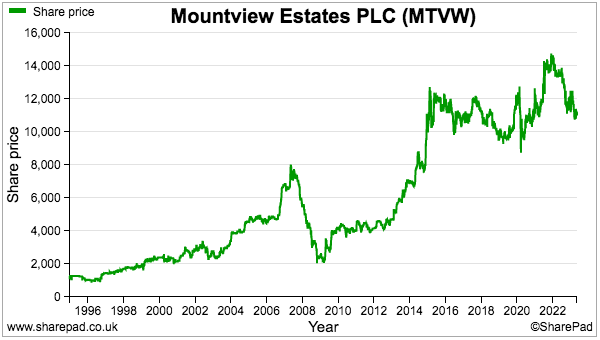

- The £200-£214 range-bound estimates may explain why the share price has made little headway during the same time:

- The range-bound estimates might also suggest MTVW exhibits:

- ‘Value trap’ characteristics, whereby all the property trading is not really creating much additional benefit for shareholders, and/or;

- ‘Safe haven’ characteristics, whereby the property estate is likely to retain a steady value irrespective of future “difficult economic circumstances“.

- The range-bound estimates might also suggest there is something inherently wrong with my calculations. MTVW’s NAV has after all increased from £80 to £102 per share since FY 2016.

- My estimated NAV sums are clearly not perfect, and the following questions remain unanswered:

- How long will MTVW take to sell all of its properties?

- Will future house-price advances compensate for being unable to sell all the properties immediately?

- How reliable is the 2014 Allsop valuation today?

- What impact could annual admin costs of £7m have on the calculations? (I have ignored such costs)

- My H1 2022 write-up attempted to address some of these issues through a discounted cash flow (DCF), whereby MTVW continues to sell its properties as normal but no longer buys any replacements…

- …but I now believe the additional complexity of forecasting sale prices, rental income and admin costs did not provide that much extra insight.

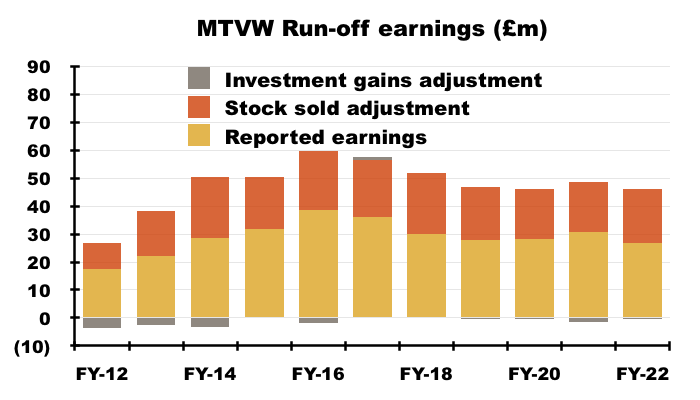

- A watered-down DCF alternative is based on a similar ‘run-off’ scenario, whereby ‘run-off earnings’ are calculated by adding back sold stock to reported earnings but no adjustments are made to reflect future sale prices, rental income and admin costs.

- Run-off earnings have bobbed around the £46m mark during the last four years, but came to £52m during this H1 and the preceding H2:

- Those run-off earnings of £52m were generated by selling properties with a £23m book value.

- With the half-year-end estate carrying a £407m valuation and, assuming stock of £23m is sold every twelve months, MTVW would take another 18 years to dispose of all of its trading properties.

- 18 years of run-off earnings of £52m give an aggregate £943m or £242 per share valuation.

- Discount all 18 payments of £52m at 9% per annum, and their total net present value would equal the recent £448m market cap.

- In theory at least, the calculations imply shareholders might enjoy 9% annual returns should MTVW never buy another property.

- These run-off sums are not perfect, as they do not account for:

- Fluctuating sale prices;

- Lower rental income and admin costs as the property estate shrinks, and;

- The new 25% tax rate.

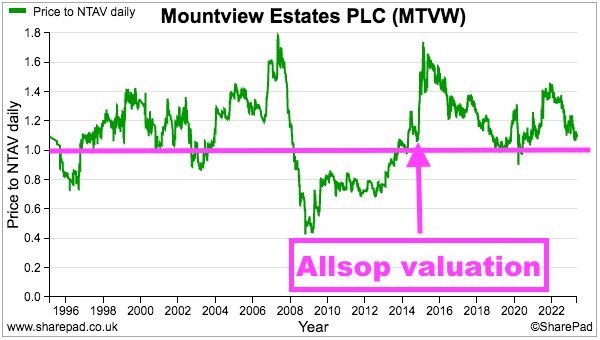

- Turning to more traditional valuation measures, MTVW’s shares have generally traded ahead of NAV following the Allsop valuation:

- The premium to NAV with a £115 share price is 13%, which is not the largest surplus the shares have ever traded post-Allsop.

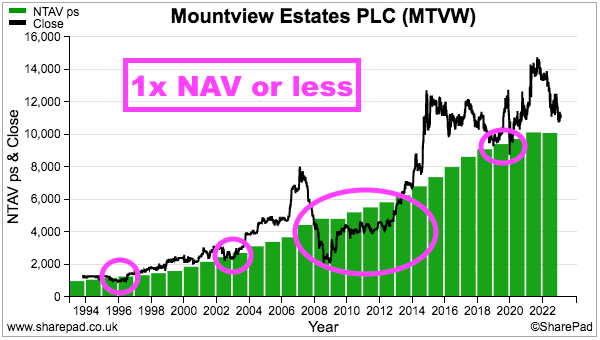

- The very best time to buy appears to be when the market cap slides to (or below) NAV, at which point no future gains from the original property purchases are priced into the valuation:

- My original MTVW purchase occurred during 2011 when the £41 shares traded at 0.75x the then £55 per share NAV.

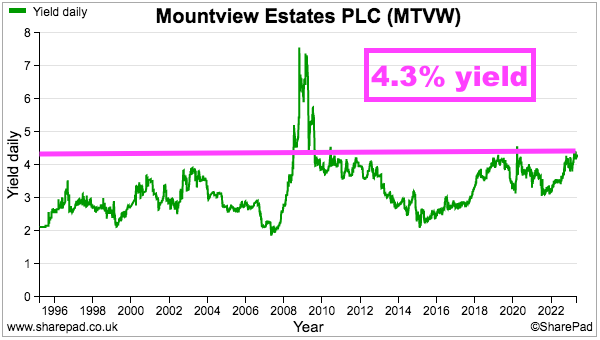

- The 500p per share trailing twelve-month ordinary dividend meanwhile supplies a 4.3% income.

- Only during the banking crash of 2008/09 has the 4.3% income been surpassed by a significant margin:

- Aside from the banking crash and pandemic crash of 2020, the price-to-NAV and yield charts above suggest the £115 shares trade at one of their least demanding levels of the last 20 years.

Maynard Paton

I have held MTVW in several portfolios for some years now, what I call a steady Eddy, pays out reasonable divs, some small capital gain. As a landlord of three small ptoperties, I am now in the process of selling them as the new legislation coming through makes them a risky project, particularly the requirement in the future of lifting the EPCs for the type of property I have. The costs of improvement could be considerable and whether you would get a sufficient uplift in rent to pay for it seems a bit hairy. It would be interesting to find out how MTVW intends dealing with this.

Hi Bertie

MTVW’s EPC commentary is limited to the annual report — point 2i here:

“As noted in our work programme we are monitoring the development of the EPC regulations though the operational and financial impact will only be properly quantifiable once the final regulations, requirements, improvement options and exemptions have been published. No scenario has indicated the need to revisit our strategy and business model.”

Plus various EPC reader comments from last year here.

Maynard

Mountview Estates (MTVW)

Update on General Meeting Voting Outcome published 23 May 2023

Listing rules require companies that suffer a 20%-plus protest vote at a shareholder meeting to consult with the unhappy investors and report back to the market within six months.

This is MTVW’s eighth such statement since the start of 2020. Here is the full text:

——————————————————————————————————————

“In accordance with provision 4 of the UK Corporate Governance Code, the Company is providing the following update to the General Meeting voting results announced on 21 November 2022 regarding the significant vote against both resolutions which were put to shareholders at the General Meeting, namely:

Resolution 1: to re-elect Mr. A. W. Powell as a director of the Company; and

Resolution 2: to re-elect Ms. M.L. Archibald as a director of the Company.

At the General Meeting, both Mr. A.W. Powell and Ms. M.L. Archibald were re-elected as directors of the Company.

Following the meeting, the Company identified, as far as possible, those shareholders who did not support the resolutions and attempted to engage with them to seek their views. Some shareholders did not wish to engage, other shareholders raised matters which are under consideration by the Board. The Board is grateful to those shareholders who took part in the engagement process and value the feedback provided. The Company re-affirms its commitment to ongoing shareholder engagement and will continue to offer to have discussions with shareholders and will take into account their concerns and considerations in the future.”

——————————————————————————————————————

The interesting line here is “other shareholders raised matters which are under consideration by the Board“.

That text has not been included before within MTVW’s previous meeting-update statements, which implies some dissatisfied shareholders are now communicating with the board. But which shareholders were involved, what matters were raised and whether the board will take any action remain a mystery.

The only major shareholder beyond members of the founding Sinclair family is the Talisman Dynamic Master Fund, which owns a 5.7% stake and is controlled by the William Pears group. Would be encouraging if Talisman is talking to the board, as the fund can be seen as ‘neutral’ versus the majority of unhappy shareholders who form one branch of the Sinclair family.

Maynard