30 April 2023

By Maynard Paton

Results summary for Andrews Sykes (ASY):

- A satisfactory performance, with H1 revenue reaching a new £38m high, H1 profit gaining 8% and the welcome declaration of a £7m special dividend.

- Assisted by strong Italian progress, European revenue climbed 17% to represent 27% — a record proportion — of the total top line.

- A healthy 22% margin and favourable cash conversion lifting net cash to £34m left the accounts in good shape.

- A bombshell delisting on AIM brings greater attention to ASY’s 90% family ownership and the associated ‘relationship agreement’ small-print.

- The 10% free float may explain why the shares yield a useful 4.7% despite the robust financials, upbeat company-blog commentary and potential further European expansion. I continue to hold.

Contents

- News link, share data and disclosure

- Why I own ASY

- Results summary

- Revenue, profit and dividend

- UK

- Europe

- Middle East and Other operations

- Financials: margin and cash flow

- Financials: pension scheme

- Controlling shareholder and risk of delisting

- Valuation

News link, share data and disclosure

News: Interim results for the six months to 30 June 2022 published 28 September 2022.

Share price: 515p

Share count: 42,136,389

Market capitalisation: £217m

Disclosure: Maynard owns shares in Andrews Sykes. This blog post contains SharePad affiliate links.

Why I own ASY

- Supplies air conditioners, portable heaters and industrial pumps for hire, with success based on a prompt 24/7/365 service, high-quality rental fleet and commercial-only customer base.

- Straightforward accounts regularly showcase high margins, generous cash flow, net cash and satisfactory returns on equity.

- Chairman and family are 90%/£195m shareholders and their “presence and requirements… has resulted in a strategy with the key aim of creating long–term shareholder value” (point 2c).

Further reading: My ASY Buy report | All my ASY posts | ASY website

Results summary

Revenue, profit and dividend

- An encouraging FY 2021 performance followed by busy company-blog commentary…

- “Andrews warms guests in Six Nations corporate hospitality“;

- “Swift pump hire ensures sewage treatment maintenance project is completed months ahead of schedule“;

- “Divine intervention from Andrews Sykes keeps soul church warm“;

- “Manufacturing plant maintains output thanks to ventilation hire“, and;

- “Andrews delivers eye-catching performance at this year’s Glastonbury“.

- …had already suggested these H1 2022 results would reveal satisfactory progress.

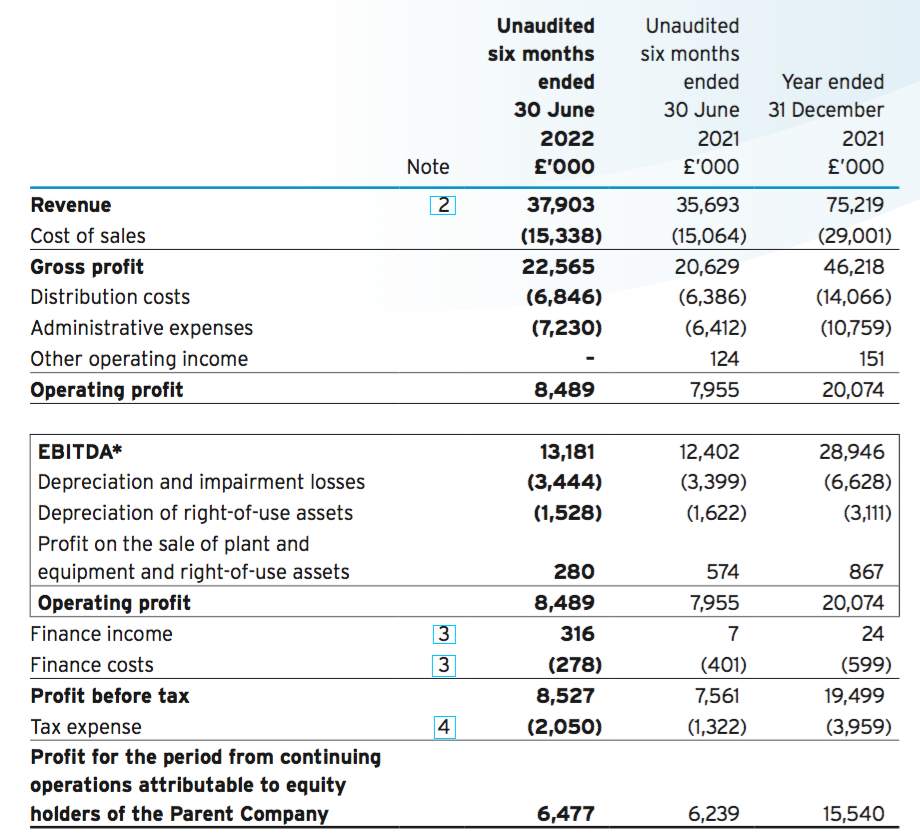

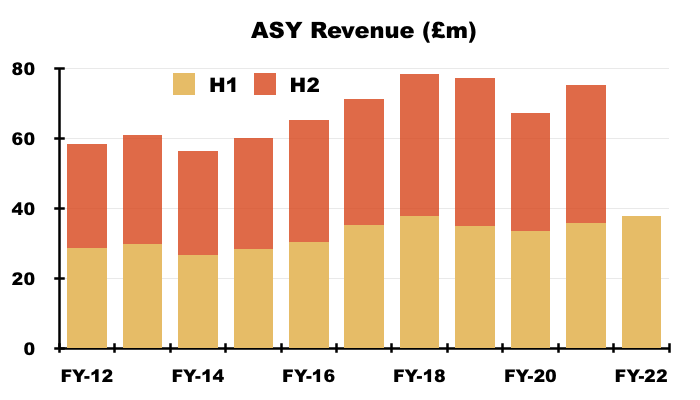

- H1 revenue gained 6% to £37.9m to set a new H1 record:

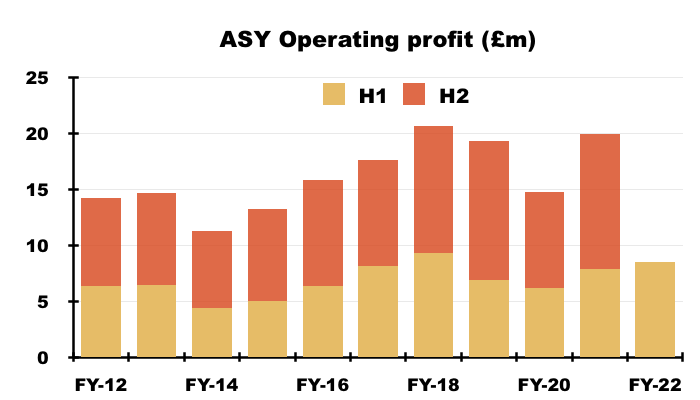

- H1 operating profit advanced 8% to £8.5m, which was ASY’s highest H1 profit bar H1 2008 (£8.8m) and H1 2018 (£9.3m).

- H1 operating profit would have been £9.0m but for restructuring costs in France of £0.5m. ASY commendably did not deem such costs to be ‘exceptional’ (see Europe).

- Reported profit also excluded additional pension contributions of £0.6m (see Financials: pension scheme).

- Extreme weather — particularly cold snaps, heatwaves and extensive rain — typically prompt sudden demand for the group’s hire equipment (primarily heaters, air conditioners and water pumps).

- Progress from year to year can therefore fluctuate due to different climatic conditions.

- Note the comparable H1 2021 performance had incurred some pandemic restrictions throughout the group’s UK, European and Middle Eastern operations:

“Andrews Sykes’ trading continues to be resilient as sectors in which we trade show ongoing demand, despite the unprecedented challenge in the form of the coronavirus pandemic.”

- ASY did not declare any pandemic interference for this H1 and for the first time since H2 2019, the group’s figures were not assisted by furlough income.

- ASY kept the operational commentary to its customary minimum:

“Revenue at Andrews Sykes Hire in the UK continues to grow and improved by 2.1% compared with the same period in 2021.“

“Our businesses in the rest of Europe experienced a very strong increase in revenue, improving 16.8% compared to the same period in 2021.”

“Khansaheb Sykes, our business based in the UAE, has continued to experience a difficult trading environment but pleasingly recorded revenue growth of 5.8% versus the first half of 2021″

- At least ASY’s super blog continues to showcase the group’s activities. H1 customers included:

- “Andrews takes centre stage at London’s Shaftesbury Avenue“;

- “Building dryer hire solves hospital’s water ingress quandary“;

- “Groundwater remedy keeps residential development on track“;

- “The show goes on for motorsport fans thanks to Andrews“;

- “Heater hire enables swift completion of Scottish bridge repairs“;

- “Server-room outage avoided thanks to out-of-hours air-conditioning rental“;

- “Air conditioners with HEPA filtration now the order-of-the-day for healthcare trusts“;

- “Andrews installs high-capacity air-conditioning solution inside multi-storey office building“;

- “Sykes Pumps provides over-pumping solution for local council“, and;

- “Andrews installs replacement cooling solution for major supermarket chain“.

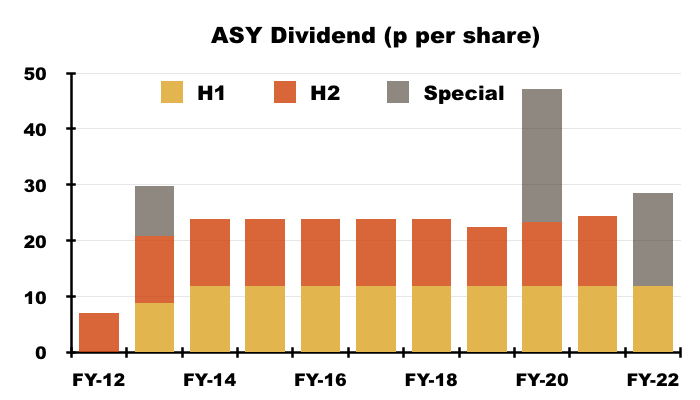

- The H1 dividend was set at 11.9p per share for the eighth consecutive H1:

- The highlight of these results was the declaration of a 16.6p per share special dividend.

- ASY said:

“In addition to the interim dividend, the board has assessed the company’s ongoing cash requirements and has concluded that, as a result of the company’s robust cash generation, a portion of the current cash reserves are surplus to the company’s requirements.

The board has therefore decided to return this surplus capital to Andrews Sykes shareholders by way of a special dividend of 16.60 pence per ordinary share which in total amounts to £7.0 million.”

“Wishful thinking perhaps, but net cash now at £29m could mean shareholders will not have to wait too long for another supplementary payment“.

- I bought my ASY shares 10 years ago at an average 233p and the latest dividends take my total ASY income to 270p per share.

UK

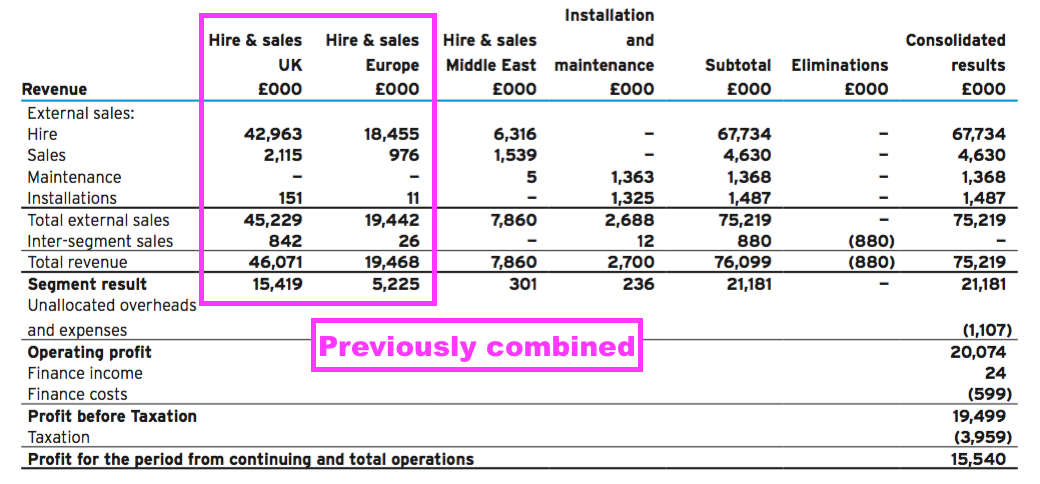

- The preceding FY 2021 results were the first to split both UK and European revenue and Hire and Sales revenue:

- ASY had previously lumped UK and European revenue together for Hire and Sales, and judging the progress of the group’s main division — UK Hire — had required subsidiary accounts from Companies House.

- The additional reporting disclosure for FY 2021 emphasised the significance of the UK operations to ASY. For FY 2021, UK Hire and Sales profit represented 73% of total profit while the division’s margin was a super 34% (£15.4m / £45.2m).

- ASY sadly did not include the additional reporting disclosure for this H1.

- Total H1 UK revenue gained 2% to £23.2m and the modest performance meant ASY’s domestic market represented 61% of group revenue:

- ASY’s UK operations include installing and maintaining fixed air-conditioning systems, revenue from which has bobbed around the £4m level for years and has rarely generated a significant profit.

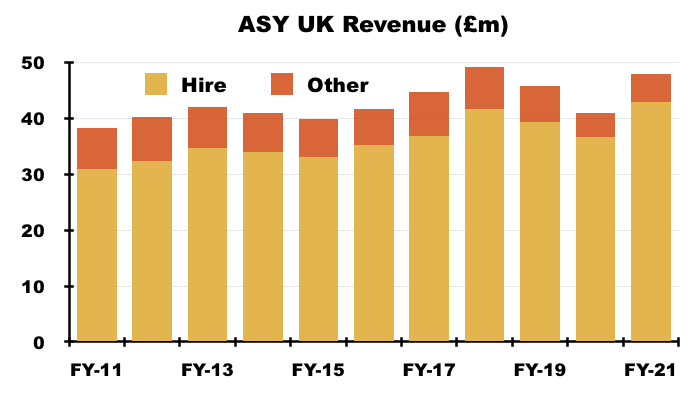

- ASY’s subsidiary accounts show UK Hire revenue advancing from £31m to £42m during the ten years to FY 2021 — equivalent to a 3% compound average:

- ASY’s UK Hire operations began during the 1960s and currently trade from 32 depots:

- The division’s longer history and larger size not surprisingly lead to greater levels of efficiency versus the group’s younger, smaller overseas operations.

- For example, revenue per UK depot during FY 2021 was an estimated £1.4m versus £1.1m in Europe.

- Furthermore, revenue per employee within the main UK subsidiary was £148k (£46m / 311 employees) during FY 2021, versus £133k for the entire group.

- And the 2021 annual report noted 7% of UK Hire and Sales revenue was spent on capex, versus 11% for ASY’s European subsidiaries (point 6a):

Europe

- I see Europe as ASY’s main opportunity for growth.

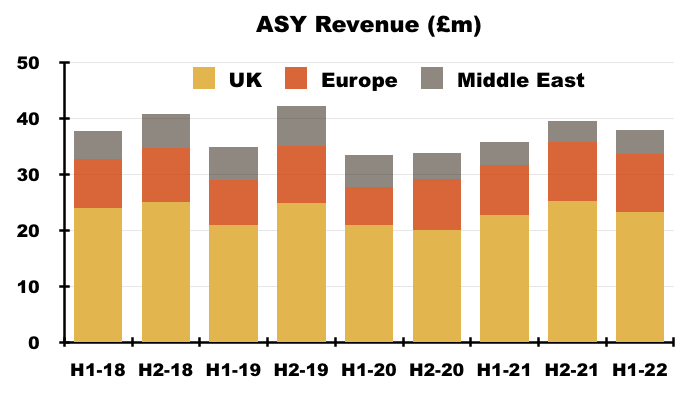

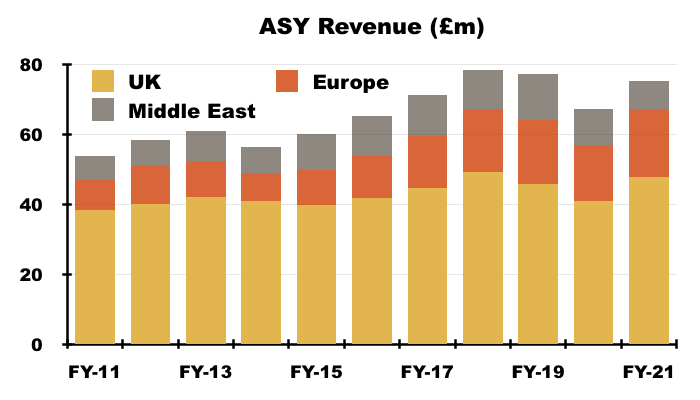

- Between FYs 2011 and 2021, European revenue expanded from £9m to £19m to represent 26% of total group sales:

- This H1 witnessed European revenue gain 17% to £10.4m and represent 27.3% — a record proportion — of the group’s top line:

- ASY’s European operations consist of:

- Netherlands:

- Opened FY 1971

- 4 depots (Amsterdam, Bleiswijk, Hoogeveen, Oirschot)

- Belgium:

- Opened FY 2007

- 3 depots (Antwerp, Brussels, Kortrijk)

- Italy:

- Opened FY 2011

- 3 depots (Bologna, Milan, Verona)

- France:

- Opened FY 2012

- 6 depots (Lille, Lyon, Marseille, Nantes, Paris, Toulouse)

- Switzerland:

- Opened FY 2013

- 2 depots (Geneva, Zurich)

- Luxembourg:

- Opened FY 2014

- 1 depot (Luxembourg)

- Netherlands:

- Since my FY 2021 write-up, ASY has added a third Belgian depot and I calculate 13 European depots have opened since FY 2011 to take the region’s total to 19.

- Opening 13 depots since FY 2011 could mean future European growth will be slow going.

- European progress during this H1 was mixed.

- Strong progress within Italy…

“This [European revenue] result was driven by an exceptional performance from our Italian subsidiary, Nolo Climat, with revenues 92.9% up on the same period in 2021 with the early and prolonged high summer temperatures seen in Italy increasing demand in our cooling products.“

- …was offset by difficulties within France:

“Climat Location in France has continued to struggle with revenues 12.0% lower than the same period in 2021. As a result, the decision has been made to restructure the business in France and restructuring costs, including depot closures and redundancy, of £0.5m have been incurred during the period. We are confident that once completed, the restructuring will right-size the French operation and lead to profitable future growth.“

Middle East and Other operations

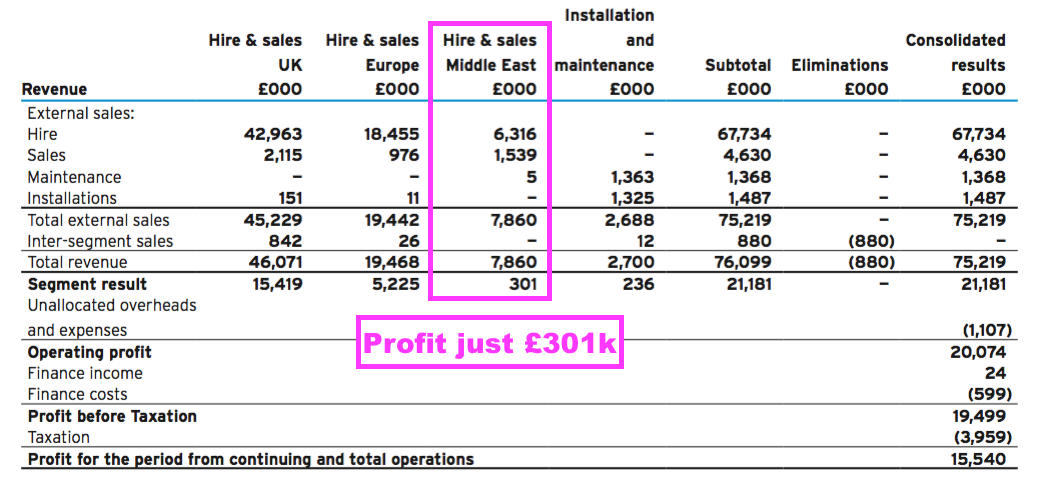

- The preceding FY 2021 had revealed Middle Eastern revenue diving 24% and divisional profit — which since FY 2015 had been running at between £2-£3m a year — collapsing to just £301k:

- The paltry FY 2021 Middle Eastern profit was due to the estimate of future unpaid debtors increasing by £1m.

- This H1 statement admitted some Middle Eastern invoices were continuing to go unpaid:

“Despite this [Middle Eastern] revenue increase and a favourable exchange rate between the Dirham and Sterling, operating profit is comparable to the first half of 2021 and continues to be depressed by increased historic bad debt charges.“

- The 2021 annual report (point 1e) cited seven-month waiting times for Middle Eastern bills to be paid:

“Total outstanding debtor days at the year-end increased from 74 days at the end of 2020 to 78 days at the end of the current year. Although still high in UK terms, the debtor day statistic in both years includes our subsidiary in the Middle East, whose debtor days were 220 days (2020: 225 days). The local economy remains badly affected by the coronavirus pandemic and slow-down in major construction projects.

Consequently, debtor days have increased dramatically in this region compared to historic levels as payment terms were extended. The group’s average debtor days for current unimpaired debts increased slightly to 42 days from last year’s level of 35 days.”

- The prospects for ASY’s ‘Other’ operations — which sell, install and maintain equipment — do not appear favourable:

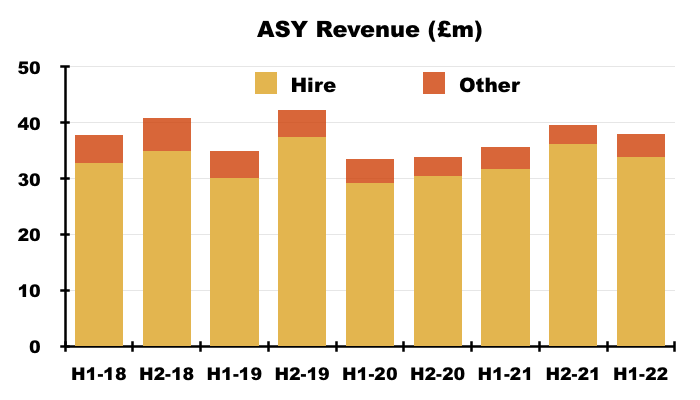

- Such revenue increased by 2% to £4.1m during this H1, but remains 17% down on that recorded during H1 2018.

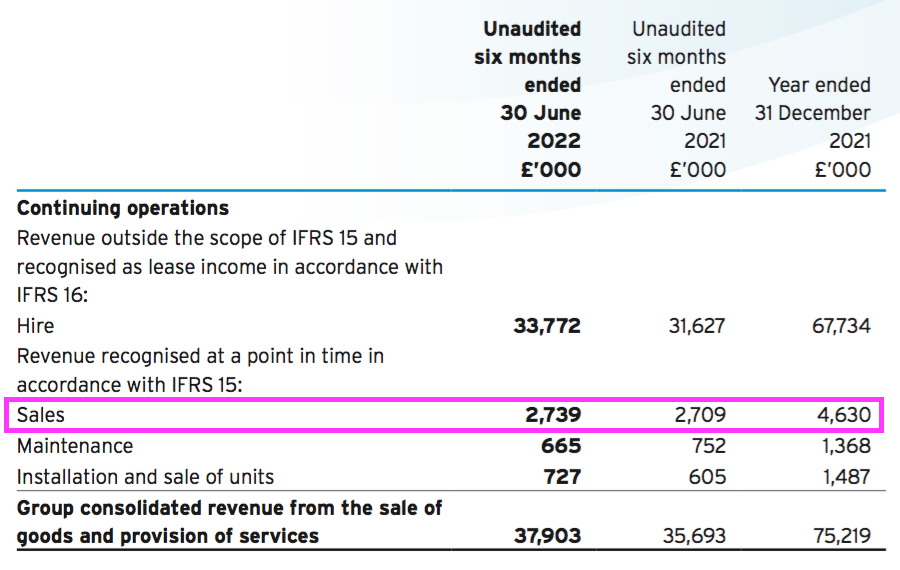

- Revenue earned from selling equipment came to £2.7m during this H1:

- I still have not worked out how FY 2021 revenue from selling equipment was £5m while the cost of stock sold was £10m:

Financials: margin and cash flow

- ASY’s accounts remain in good shape.

- Despite low-profit activities such as those in the Middle East and installing/maintaining fixed air-con systems, the H1 operating margin was a healthy 22.4% and was the highest for an H1 since H1 2018 (24.5%):

- ASY’s full-year operating margin has in fact topped 20% every year since 2002.

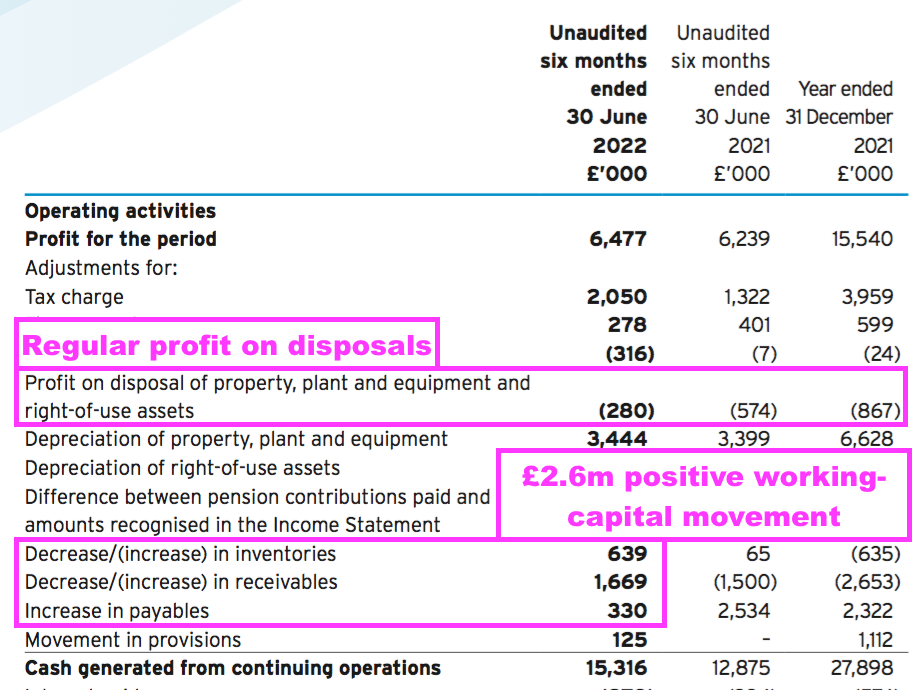

- Cash conversion was good. A positive working-capital movement of £2.6m supported free cash flow of £10.2m, which in turn funded a £3.0m debt repayment, the £5.3m FY 2021 final dividend and left £1.9m over to be added to the cash balance:

- Emphasising a conservative depreciation policy, ASY recorded a small profit over the book value of sold equipment during this H1 — and has done so every year since at least FY 2005.

- Net cash during the six months increased from £29.4m to £34.4m after the £3m debt repayment cleared the last of the group’s conventional bank borrowings.

- Net cash reaching £30m does now seem to be the level at which ASY declares a special dividend.

- Go back to July 2020, and ASY paid a £10m special dividend when net cash reached £30m:

“As at 22 July 2020, the Company had net cash reserves* of approximately £29.9 million. The Board has assessed the Company’s ongoing cash requirements under a range of forecast scenarios and has concluded that, as a result of the Company’s expected robust cash generation, a portion of these cash reserves is surplus to the Company’s requirements.“

- The 16.6p per share special dividend accompanying these H1 results is equivalent to £7m.

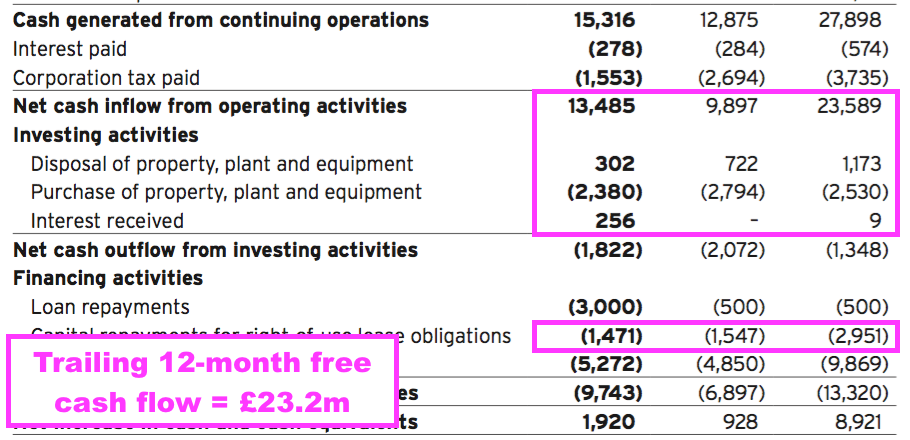

- Trailing twelve-month free cash flow is £23.2m…

- …which no longer has any debt to clear and amply covers the £10.3m (24.4p per share) trailing twelve-month ordinary dividend.

- Wishful thinking perhaps, but a repeat of the preceding H2 2021 and this H1 could witness ASY’s net cash approach £40m by H1 2023…

- …and therefore potentially fund yet another special payout.

- Emphasising ASY generating surplus cash, the group commenced purchasing its shares during H1 2023.

- The group’s 10% free float (see Controlling shareholder and risk of delisting) has limited the buyback to date to just £60k (at an average 517p per share).

- Prior to the recent purchases, ASY had only once bought back shares during the previous ten years: FY 2018, spending £438k at 494p.

Financials: pension scheme

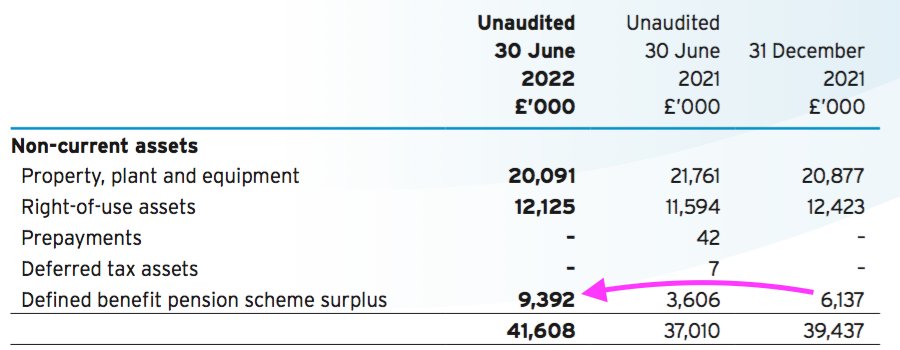

- ASY’s accounts continue to demonstrate how pension accounting does not always reflect the near-term cash reality of a defined-benefit pension scheme.

- Although ASY’s balance sheet shows the scheme surplus increasing by £3.3m during this H1 to £9.4m…

- …£1.3m was paid into the scheme during FY 2021, with a further £0.7m paid during this H1 and another £0.6m to be paid during H2 2022:

- You would imagine a pension scheme showing a £9m surplus would not require any further contributions.

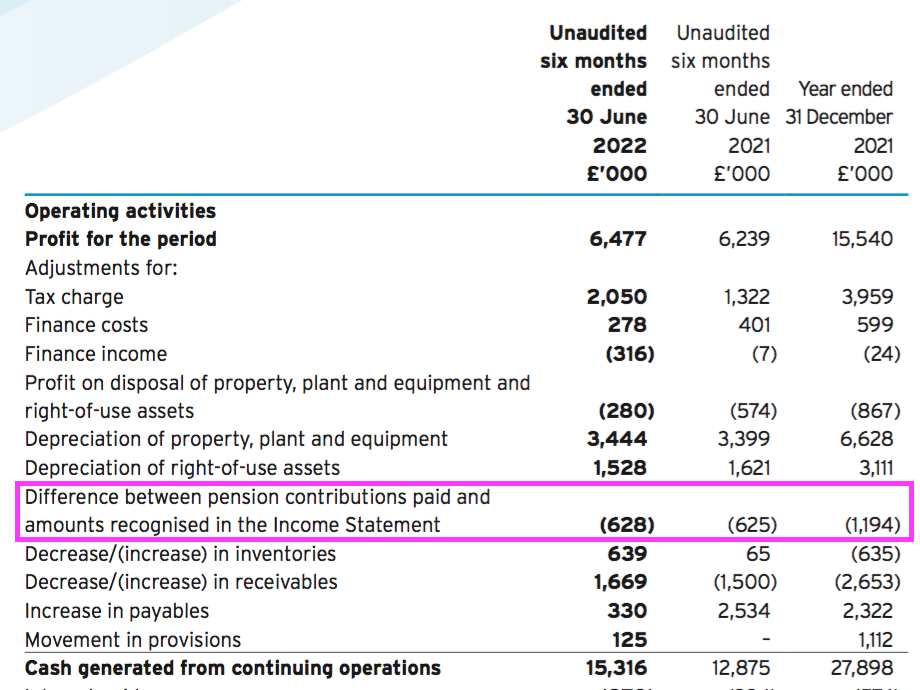

- Note that extra pension contributions bypass the income statement, with the cash flow statement highlighting the expense that is not charged to earnings.

- ASY reiterated scheme contributions will drop to £120k a year from FY 2023:

“Following the triennial recalculation of the funding deficit as at 31 December 2019, a revised schedule of contributions and recovery plan was agreed with the pension scheme trustees in March 2021 and was effective from 1 January 2021.

In accordance with this schedule of contributions and recovery plan, the Group will be making regular contributions of £110,000 per month for the period 1 January 2021 to 31 December 2022, and £10,000 per month for the period 1 January 2023 to 31 December 2025 or until a revised schedule of contributions is agreed, if earlier. Consequently, the Group expects to make total contributions to the defined benefit pension scheme of £1,320,000 during 2022.“

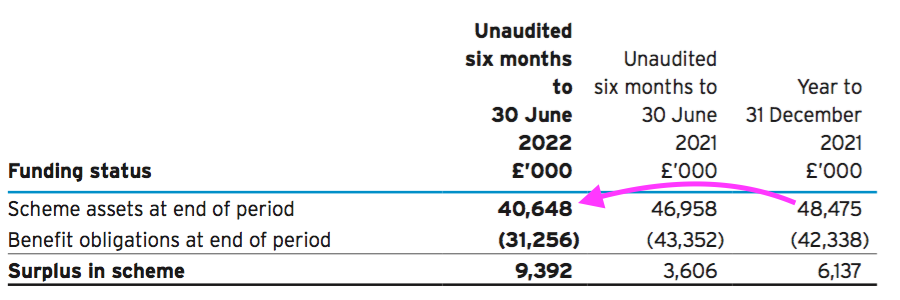

- Scheme assets dropped by £7.8m to £40.6m during this H1:

- Pensioner benefits from the scheme were £1.8m during FY 2021, and I am not convinced scheme assets of £40.6m are enough to sustain such benefits (as well as £100k-plus scheme admin charges) when annual contributions drop to £120k.

- Unless the pensioner benefits reduce significantly, I suspect the scheme’s triennial recalculation as at 31 December 2022 will conclude employer contributions must increase beyond £120k a year to limit the possibility of benefits becoming partly funded by selling scheme assets.

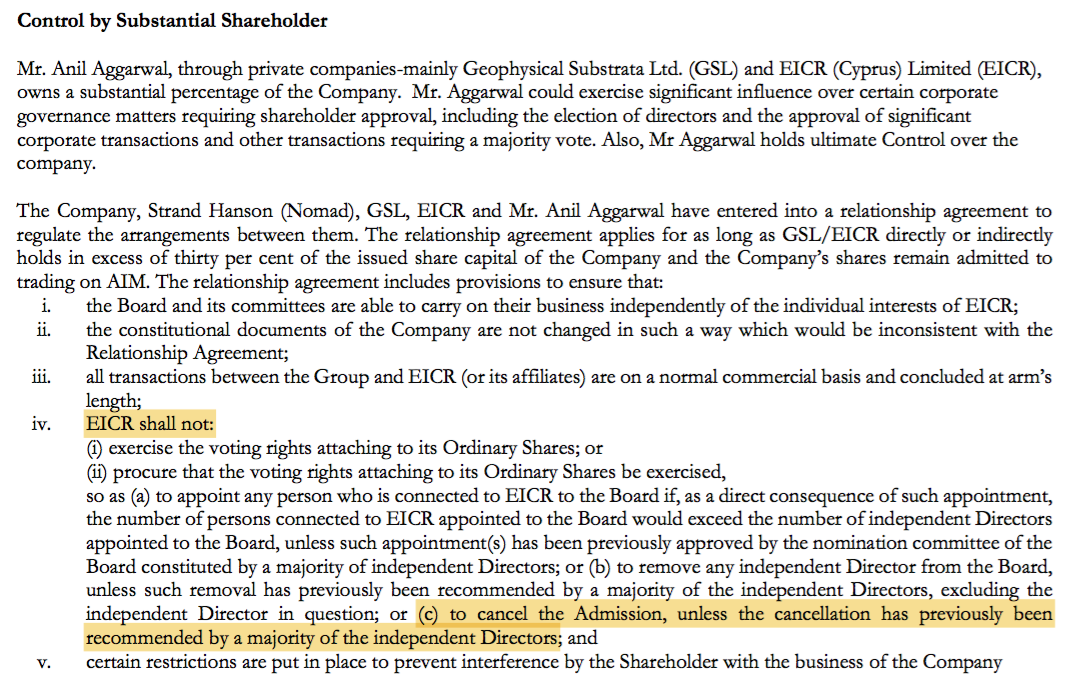

Controlling shareholder and risk of delisting

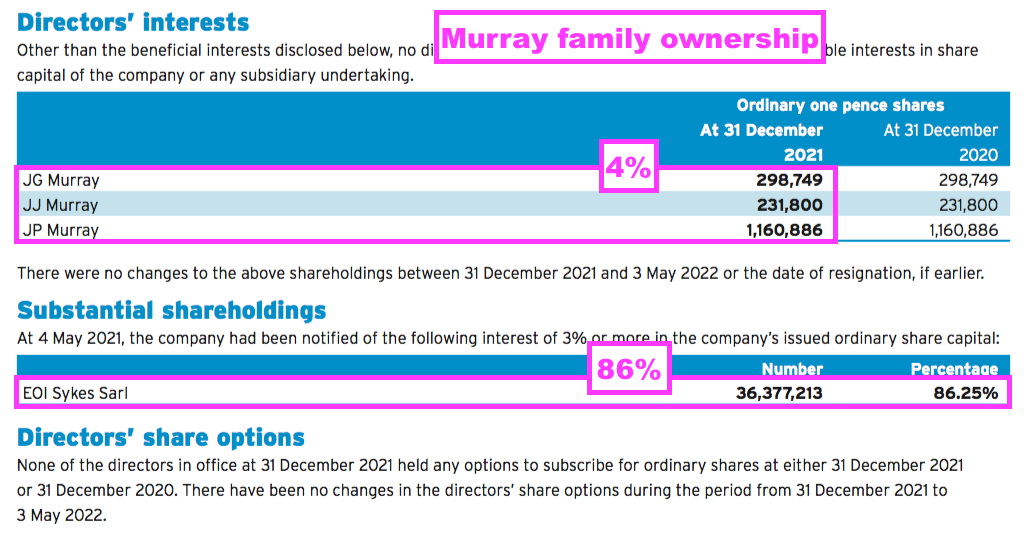

- The 2021 annual report confirmed 90% of ASY was owned by the Murray family (point 2a):

- Such controlling shareholdings always carry the risk of a sudden delisting, as majority owners can simply steamroller delistings through any shareholder vote.

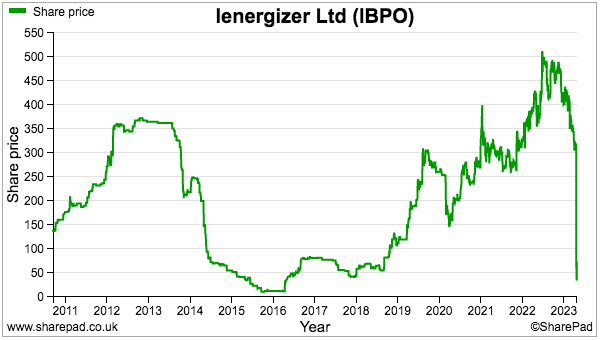

- Case in point: iEnergizer (IBPO) announced the other week it was delisting. IBPO stated:

“The Directors have conducted a review of the benefits and drawbacks to the Company and its shareholders in retaining its quotation on AIM, and believe that Cancellation is in the best interest of the Company and its Shareholders as a whole.“

- IBPO chief executive Anil Aggarwal owns 83% of the group — a stake worth £488m before the delisting announcement:

“EICR (Cyprus) Limited (“EICR”) holds 82.74 per cent. of the Company’s current issued share capital, resulting in a limited free float and liquidity of the Ordinary Shares with the consequence that the Directors believe that the quotation of the Ordinary Shares on AIM does not, in itself, offer investors the opportunity to trade in meaningful volumes or with frequency within an active market.“

- IBPO critically did not offer outside shareholders any consideration for their shares. The price dropped from 310p to 68p on the day of the announcement:

- Could an IBPO-type bombshell occur at ASY?

- I am hopeful it won’t, but cannot rule anything out.

- After all, both IBPO (at least for now) and ASY are quoted on AIM — the market rules for which seem to allow shady directors to behave as they wish without reprisal.

- Reassurance that ASY may not follow IBPO’s delisting could lay in their respective ‘Relationship Agreements’.

- These agreements ensure controlling shareholders (30%-plus) comply with the independence provisions set out in the listing rules (LR 6.1.4D).

- IBPO’s 2022 annual report carried the following text about the group’s relationship agreement:

- IBPO’s agreement included a proviso that a delisting could occur, albeit the delisting had to be recommended by the majority of the independent directors:

“EICR shall not… (c) to cancel the Admission, unless the cancellation has previously been recommended by a majority of the independent Directors…“

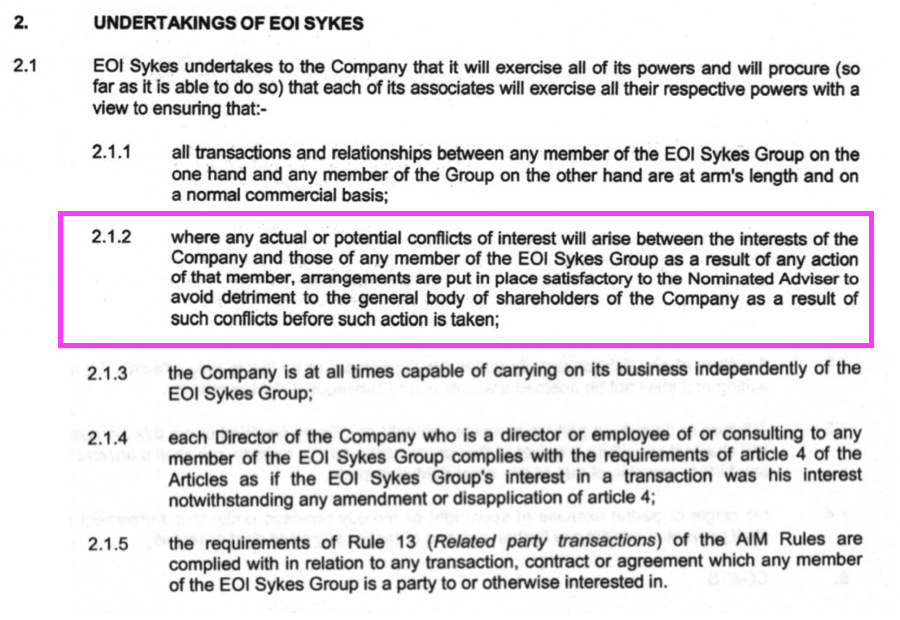

- In contrast, ASY’s relationship agreement does not include any delisting proviso:

- My reading of ASY’s relationship agreement suggests outside ASY investors are protected (in theory!) by the group’s Nomad becoming involved to “avoid detriment to the general body of shareholders” by the actions of the Murray family:

“…where any actual or potential conflicts of interest will arise between the interest of the Company and those of any member of the EOI Sykes Group as a result of any action of that member, arrangements are put in place satisfactory to the Nominated Adviser to avoid detriment to the general body of shareholders of the Company as a result of such conflicts before such action is taken“

- Companies House archives reveal the Murray family has enjoyed a majority interest in ASY since the mid-1990s, and therefore has resisted the temptation to delist for almost 30 years.

- At the 2016 AGM, ASY’s then executives told me the Murray family liked the “higher levels of management governance” a market listing offers:

“Listing — board owns 90% of the shares while the company has no option scheme nor has issued any shares to raise money (at least for a decade). So why have a quote? Governance — quoted firms are tightly regulated and controlling family, who are not involved in the operation of the business, like the higher levels of management governance a stock-market listing can provide. Question has been asked for at least the last ten years.“

- Note that omens of IBPO’s delisting were perhaps already emerging (at least with hindsight!).

- Two weeks before the delisting bombshell, IBPO announced two new non-execs had replaced two old non-execs:

“iEnergizer Limited (AIM:IBPO.L), an international and full service Business Process Outsourcing (BPO) business, is pleased to announce the appointment of Mr Nicholas (Nick) David Saul and Mrs Elizabeth (Liz) Anne Powell as Independent Non-Executive Directors of the Company, with immediate effect.“

“Christopher de Putron and Mark De La Rue, who have been on the Board as Non-Executive Directors since December 2011, are stepping down from their roles to pursue other business interests, with immediate effect.”

- I can only surmise the two old non-execs did not like the idea of IBPO delisting, and were replaced by two new non-execs that would provide the aforementioned non-exec delisting majority that was required by IBPO’s relationship agreement.

- Note also that IBPO undertook a three-month formal sales process during 2022, but did not attract a suitable bidder:

“On 13 June 2022, the Company announced a review of strategic options available to the Company and commenced a formal sale process under the Takeover Code.

The Company subsequently engaged with a limited number of parties but given stronger trading during the process… the Board felt that it was in the best interests of the Company to withdraw and terminate the Formal Sales Process at this time, and confirms that it is no longer in active discussions with any interested parties. “

- IBPO inviting takeover bids signalled a public quote was no longer appropriate for the group.

Valuation

- ASY gave a positive outlook for H2 following the 2022 summer heatwave:

“The second half of the year has started resiliently with record temperatures in the UK and Europe positively impacting demand for the Group’s air conditioning units and chillers. This increased summer demand leads management to be optimistic over the full year results.

In the longer term, management remains optimistic that the business will continue to improve but are mindful of the current economic climate and the impact that heightened energy prices, inflation and recession risk can pose to the business and customer demand.“

- Responding to the heatwave activity, ASY’s blog issued this “Unprecedented heat prompts us to pull out all the stops!” update:

“It’s fair to say that last week’s record-breaking temperatures put quite a strain on our resources. Staying on top of the online enquiries and inbound telephone calls was challenging enough, without the small matter of having to ensure each air conditioning hire was agreed, coordinated and delivered in as timely a fashion as possible… our teams around the country adopted a siege mentality in a bid to combat the seemingly never-ending flow of requests.“

- ASY’s blog suggests the group was still kept busy once the H2 2022 heatwave subsided:

- “30-unit boiler-hire package maintains district heating-system output“;

- “Sykes co-ordinates diesel extraction following super-yacht fire“;

- “Contractor firm seeks Andrews boilers for leisure-centre development“;

- “National food outlet seeks tailored heating replacement“;

- “Andrews lays on another assist for football-league club“;

- “Andrews’ engineers heralded following successful installation for major Belgian TV broadcaster“;

- “Offshore technology leaders turn to UK’s climate-control leaders“;

- “Last ditch air-conditioning hire keeps Luminarium exhibition open“;

- “Telecoms client comes back for more after positive first impression“, and;

- “Italy’s iconic Fashion Week: Four shows, various locations, dozens of units and one big triumph!“.

- ASY’s blog then revealed December had seen record UK revenue:

“[UK:] We knew last month had been a good one, but it has since come to light that it was our best December on record from a revenue perspective! Britain experienced snowfall, ice and bitter temperatures – and it’s fair to say our clients were cold.

Although we didn’t have a choice in the weather, our loyal customers chose us to provide temporary heating units. We’ve always made it our target to provide a high level of service and deliver during sleet, snow, or shine, and that’s exactly what we did!”

- The positive blog commentary suggests H2 2022 revenue may top the £40m witnessed during H2 2021 and may even top the record £42m registered during H2 2019.

- H2 2022 revenue of £42m would lead to FY 2022 revenue of £80m, which would surpass the record £79m set during FY 2018.

- The ‘going concern’ text within the FY 2021 results implied revenue that year was 12% below budget due to pandemic interference:

“Hire turnover and product sales [for FY 2022] reduced by 12% versus budget—a similar variance when comparing 2021 actual results to 2021 budgets;“

- Hire turnover and product sales being 12% below budget for FY 2021 implies actual hire and sales revenue of £72m could have been more like £82m in a pandemic-free year.

- Whether last summer’s “never-ending flow of requests” for air-con equipment and the “snowfall, ice and bitter temperatures” prompting record December UK turnover will both become normal for ASY remains to be seen.

- But extreme weather conditions do seem to be occurring with greater frequency, which ought to be favourable for ASY’s hire services.

- Trailing twelve-month operating profit excluding furlough payments but including IFRS 16 lease financing was £20.1m.

- Taxed at the new 25% UK standard rate gives earnings of £15.1m or 35.8p per share.

- That 25% tax rate may be a little light, given the tax rate during this H1 was 24% when UK standard tax was 19%:

“The total tax charge for the period increased by £0.7 million to £2.1 million (2021: £1.3 million), an effective tax rate of 24.0% (2021: 17.5%). The increase in the overall effective rate of tax is driven by a lower level of capital allowances claimed in the UK, coupled with higher profits generated in Italy which has a higher tax rate than in the UK.“

- Note my valuation sums do not include any leeway for the £0.5m restructuring costs in France, but do they not adjust for the pension situation either.

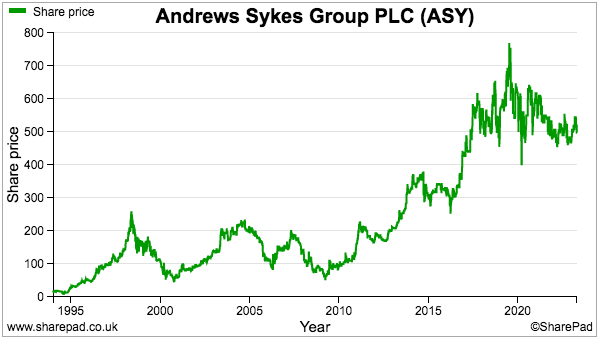

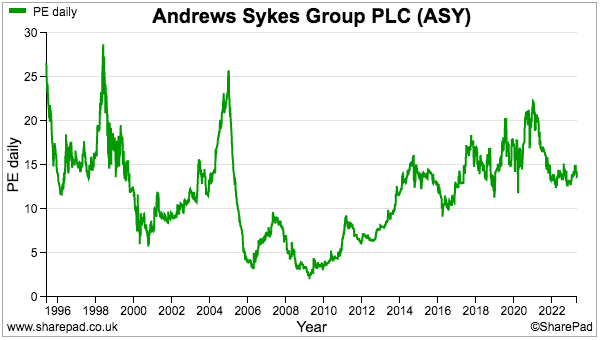

- The 515p shares are valued at 14-15x my 35.8p per share estimate.

- Bear in mind ASY has indirectly hinted any net cash beyond £30m may be returned to shareholders as a special dividend.

- As such, if my aforementioned wishful thinking proves accurate — and net cash does indeed approach £40m by H1 2023 — perhaps special dividends can become a regular fixture for shareholders (similar to Bioventix?).

- My estimated earnings of 35.8p per share paid out entirely as ordinary/special dividends would deliver a 6.9% income at 515p.

- Plus the 515p shares would be backed by £30m, or 71p per share, of cash with no bank debt.

- My sums suggest the 515p shares are not outrageously expensive for a high-margin and cash-rich business that:

- Proved reasonably resilient during the pandemic;

- May well have enjoyed an FY 2022 heatwave bonanza, and;

- Offers further expansion opportunities within Europe.

- Bear in mind ASY’s P/E has rarely climbed to a premium rating:

- Keeping a lid on the P/E may be:

- The very limited free float (see Controlling shareholder and risk of delisting);

- A lack of reinvestment opportunities for growth, underlined by the latest special dividend, and/or;

- The profit ups and downs due to the weather.

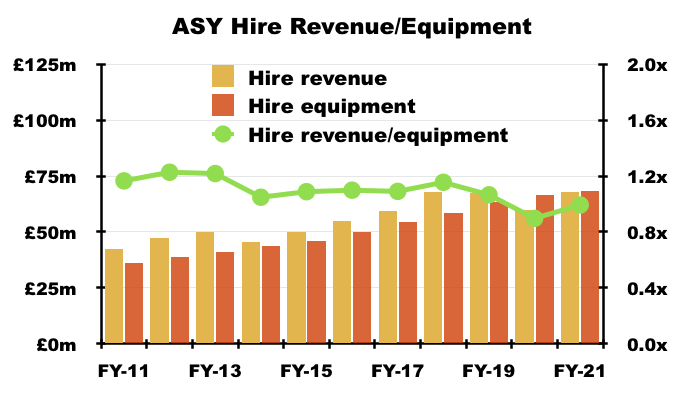

- Plus ASY’s economies of scale may not be fantastic. In particular, previous results have shown a consistent 1.2x limit between revenue generated from the group’s hire equipment and the original cost of that hire equipment:

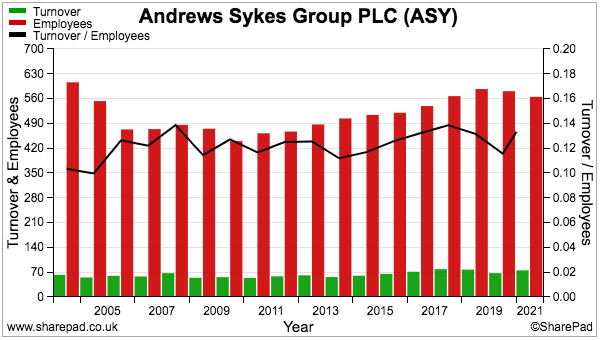

- Revenue per group employee bobbing within the £100k-£130k range could be further evidence of extra revenue requiring a commensurate level of extra (employee) expense:

- A sustained P/E re-rating may therefore require ASY to earn more revenue from its existing hire equipment and/or its workforce, rather than relying solely on opening more depots in Europe.

- For now the 24.4p per share trailing twelve-month dividend supplies a 4.7% income at 515p.

Maynard Paton

Hi Maynard,

Excellent stuff as always – I was interested by the pension information you’ve highlighted. Whilst you’ve mentioned the reduction in scheme assets I was more struck by the larger reduction (£11m) in benefit obligations primarily explained by the increase in bond yields.

On the surface the increased surplus and lower obligations suggest to me the scheme has been de-risked during the period.

Thanks Patrick.

Yes, total scheme obligations are lower but they are calculated using guesswork through NPVs. I take the view that assets and benefits payable are reported in today’s money, and assets have to generate the returns to fund the benefits — especially if ASY’s yearly contributions fall to £120k. Scheme needs a c4.4% return every year to cover the benefits, which compares to c2% return for typical FTSE 100 schemes. I believe contributions will have be raised from £120k, but hopefully I will be proved wrong. Thankfully the intricacies of the scheme’s funding required ought to be outweighed by proper business matters such as heatwaves :-)

Maynard