19 June 2018

By Maynard Paton

Update on Mountview Estates (MTVW).

Event: Preliminary results for the twelve months to 31 March 2018 published 14 June 2018

Summary: This RNS was more interesting for the management comments — all 626 words — than the actual 2018 financials. Indeed, MTVW’s chief exec is probably the first-ever boss to tell shareholders their business has a “finite life” and had essentially operated in an ex-growth market for 30 years. Hardly inspirational stuff… until you realise the dividend was lifted 33% and has now grown 47-fold during the last three decades. Mind you, this property-trading specialist will at some point have to call it a day — and dissolve an estate that could be worth almost double the current share price. I continue to hold.

Price: £110

Shares in issue: 3,899,014

Market capitalisation: £429m

Click here to read all my MTVW posts

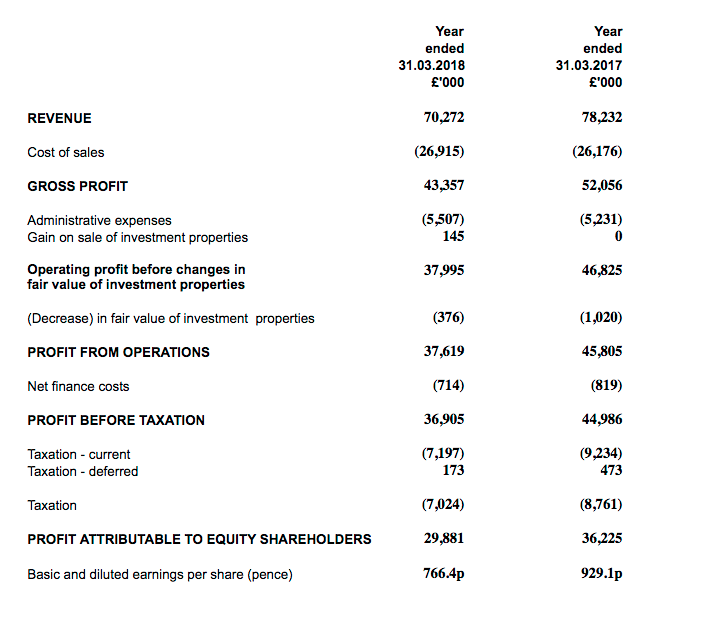

Results:

My thoughts:

* Longer completion times hit gross margins and stifle earnings

November’s interim results — the weakest for four years — had already ensured these preliminary figures would not be spectacular.

In the event, full-year revenue slid 10% while operating profit dived 19%. MTVW blamed a lower rate of property sales — due in part, apparently, to Brexit — for the shortfall:

“In uncertain times transactions usually take longer to complete and so it is that during the year ended 31 March 2018 we completed significantly less sales than in the previous financial year…

When Brexit negotiations and other economic uncertainties are resolved the purchases we are presently able to make will realise good profits and we can look forward to future increased earnings.”

The 2018 performance was below the achievements recorded during 2015, 2016 and 2017:

| Year to 31 March | 2014 | 2015 | 2016 | 2017 | 2018 |

| Net asset value (£k) | 265,591 | 287,661 | 311,752 | 336,279 | 354,462 |

| Net asset value per share (p) | 6,812 | 7,378 | 7,996 | 8,625 | 9,091 |

| Revenue (£k) | 66,150 | 71,331 | 79,765 | 78,232 | 70,272 |

| Gross profit (£k) | 38,595 | 46,710 | 53,014 | 52,056 | 43,357 |

| Operating profit (£k) | 34,553 | 41,655 | 47,866 | 46,825 | 37,850 |

| Net valuation gain (£k) | 3,185 | 57 | 1,504 | (1,020) | (376) |

| Finance income (£k) | (2,344) | (1,736) | (1,179) | (819) | (714) |

| Other items (£k) | - | - | 197 | - | 145 |

| Pre-tax profit (£k) | 35,394 | 39,976 | 48,388 | 44,986 | 36,905 |

| Earnings per share (p) | 730 | 816 | 993 | 929 | 766 |

| Dividend per share (p) | 200 | 275 | 300 | 300 | 400 |

MTVW said:

“This fall in the number of sales has caused the fall in profits to a far greater degree than any perceived fall in prices”

However, it is worth noting that gross margins declined significantly during the year:

| Year to 31 March | 2014 | 2015 | 2016 | 2017 | 2018 |

| Group gross margin (%) | 58.3 | 65.5 | 66.5 | 66.5 | 61.7 |

| Property sales gross margin (%) | 54.8 | 65.0 | 65.8 | 66.3 | 58.1 |

And the first-half/second-half split showed a lower gross margin during H2 than H1:

| H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | ||

| Revenue (£k) | 34,047 | 44,185 | 78,232 | 33,027 | 37,245 | 70,272 | |

| Gross profit (£k) | 24,139 | 27,917 | 52,056 | 20,770 | 22,587 | 43,357 | |

| Property sales revenue (£k) | 25,133 | 35,021 | 60,154 | 23,953 | 27,887 | 51,840 | |

| Property sales gross profit (£k) | 17,843 | 22,024 | 39,867 | 14,297 | 15,721 | 30,018 | |

| Property sales gross margin (%) | 71.0 | 62.9 | 66.3 | 59.7 | 56.4 | 57.9 |

Clearly MTVW is no longer making as much profit from its property sales as it once was.

For some perspective, a 58% gross margin is equivalent to MTVW selling a property for a 138% gain. The group enjoyed a 197% gain on properties sold during 2017, and has earned an average 156% gain on sold properties during the last ten years.

Certainly falling house prices can effect the gross margins MTVW enjoys — although the firm is not too exposed to elevated property valuations. The average proceeds from homes sold during 2017 was £330k.

However, MTVW’s general style of property trading can also lead to haphazard earnings.

As a reminder, MTVW’s portfolio is dominated by 2,000 or so regulated-tenancy (or similar) properties, and the number of the group’s properties becoming available for sale — and the proceeds they generate — can be unpredictable.

You see, MTVW sells its properties only when the regulated tenancy ends — which most often occurs when the tenant dies.

Furthermore, the gain on each property sold — typically correlated to how long the property has been owned by MTVW — can vary somewhat.

As such, if the properties sold during 2018 were bought relatively recently, then the resultant gross margin would indeed be much lower than if the properties had been owned for decades.

* NAV inches to new £91 per share high

Although MTVW’s full-year profit was not the highest the firm has ever recorded, it did add £18m to the balance sheet to help take net asset value (NAV) to a fresh £354m/£91 per share peak. The 5% increase was the lowest percentage gain since NAV dipped slightly during 2009.

MTVW’s November interims indicated the group had spent significant sums on acquiring properties during H2. In fact, stock levels increased by £29m during the second half and net debt ended the year £14m higher at £45m.

Net debt now represents (a relatively lowly) 12% of the group’s £377m property stock:

| Year to 31 March | 2014 | 2015 | 2016 | 2017 | 2018 |

| Trading properties (£k) | 321,323 | 323,020 | 334,108 | 347,380 | 376,879 |

| Net debt (£k) | (76,751) | (59,538) | (41,619) | (31,217) | (44,995) |

In the past, this ratio has topped 30% and suggests MTVW could have the capacity to borrow another £70m.

* The chief exec admits the business has a “finite life”

The management narrative accompanying these results was quite unusual.

First off, the 626-word statement was double the length of last year’s effort and quadruple the length of the 2016 RNS. So the chief exec certainly had something to say…

…which turned out to be about the company’s “finite life”.

The chief exec stated:

“It is now nearly 30 years since regulated tenancies were last created but this asset class continues to exist in sufficient quantities to be the mainstay of our business.

We have made modest diversification into life tenancies and as leases become shorter where we are the ground landlord there is money to be made in granting lease extensions. Nevertheless these are only supplementary to our main business of buying residential properties that are subject to regulated tenancies and awaiting vacant possession.

Whilst regulated tenancies continue to exist for longer than may have been anticipated when the 1988 Rent Act became effective, a business as narrowly focused as our does have a finite life.

The business will continue to prosper but it will become increasingly difficult to replace stock as it is sold.

Some shareholders may wish to pursue their own avenues of diversification without selling Mountview shares and so the final dividend payable on 13 August 2018 will be increased to 200 pence per share. This will make a total of 400 pence per share in respect of the Company’s year ended 31 March 2018.”

The remarks were the first I can recall in an MTVW RNS that acknowledged the ever-diminishing number of properties available to purchase.

Reading between the lines, I do wonder if the dissident shareholders that caused the ructions with the AGM voting have engaged further with the board… and have been placated by a greater payout.

It is certainly worth noting MTVW’s majestic progress since the implementation of the 1988 Rent Act. The past 30 years have seen the dividend balloon 47-fold and NAV surge 23-fold — equivalent respectively to 14% and 11% compound annual growth rates. And yet during the same time, the number of regulated-tenancy properties available has consistently decreased.

One minor point from these results concerned the group’s standard investment properties — a group of homes located in Belsize Park, London.

These properties lost £376k of their collective fair value during the year — after losing £1m during 2017. The properties were acquired during 1999 and, until now, had never suffered a devaluation for two consecutive years.

This investment portfolio is now in the books at £28m.

Valuation

This RNS revealed trading properties with a £337m book value, which could be worth £965m if they were all sold at the average margin enjoyed during the last ten years.

Taxing the resultant gain at 19%, adding on the £28m Belsize Park portfolio and then subtracting net debt of £45m and other liabilities of £5m, the possible NAV comes to £831m or £213 a share.

That £213 compares to the £91 per share NAV reported by MTVW using its conventional historical-cost basis.

With the share price at £110, clearly there remains some upside potential here.

But as always, the big question is how long it will take MTVW to sell all of its properties to realise that potential £213 per share NAV guess.

For a more immediate valuation, there is the £666m figure assigned to MTVW’s trading stock by an independent assessment as at September 2014.

This £666m valuation is becoming rather stale now, but for what it is worth, adjusting the valuation for tax, those investment properties and the debt gives an NAV of £148 a share.

I should add that this £148 estimate is based on MTVW’s properties being in their current ‘regulated tenancy’ state — so does not include any upside potential for when the property is vacated and can be sold at market value.

Furthermore, this £148 estimate does not include any house-price gains experienced since the September 2014 assessment, and nor does it adjust for properties bought or sold thereafter.

Meanwhile, the lifted 400p per share dividend provides a useful 3.6% yield at £110.

Maynard Paton

PS: You can now receive my Blog posts through an occasional e-mail newsletter. Click here for details.

Disclosure: Maynard owns shares in Mountview Estates.

A slowing of the sales due to market conditions implies that the number of properties available for sale has increased. This will cause the rate of repayment of debt to reduce, but that will reverse when market conditions normalise and sales gather speed again. Additionally, if the rate of property purchases remains constant then debt will increase, and so it has. Maintaining property purchases in a buyers market makes perfect sense.

I do not think that the availability of properties will decline for quite some time, but the chairman makes a good point. The end game will be some form of self-liquidation, but I will be in the ground before then. I continue to hold and will look to increase should the sp take a drop in sympathy with the overall stock market.

Mountview Estates (MTVW)

Publication of 2018 annual report

A few interesting snippets here.

1) Gross margins

The original results RNS did not contain the full property sales and property income gross margins. My Blog post above had estimated the gross margins, but the annual report confirms the actual figures:

Property sales during the full year and H2 actually produced gross margins of 57.9% and 56.4% respectively — well below the comparable figures for 2015, 2016 and 2017.

I have now amended the Blog post above to reflect the actual gross-margin figures.

2) Allsop valuation

The note below is probably the most informative part of the report:

Properties that had been valued by Allsop at £30,954k during September 2014 were sold during the year for £45,156k — i.e. 1.48x.

However, the second half saw properties valued by Allsop at £15,827k during September 2014 sold for £22,660k — i.e. 1.43x (H1 was 1.52x)

So, the H2 ‘Allsop multiple’ was notably weaker during H2 — as per the gross margin.

Remember that the Allsop valuations of 2014 were 2.1x greater than the then book value of the properties. Based on the small sample of properties sold during H2 2018, it appears today’s market values are 2.1 x 1.43 = 3.0x the value stated in the books.

My very rough sums suggest MTVW’s book value could be £205 per share based on this 3.0x multiplier (the sums are complicated and adjust for properties sold and bought since September 2014, the group’s investment properties, debt and tax).

3) Property buys and sells

This is what MTVW purchased during the year:

Average price per unit was £396k, the highest ever, and which compares to £253k, £315k, £226k and £133k for 2017, 2016, 2015 and 2014 respectively.

Average price per regulated property was £490k, the highest ever, and which compares to £325k, £293k, £417k and £151k for 2017, 2016, 2015 and 2014 respectively.

Clearly regulated tenancies and similar are no longer as inexpensive as they were.

Here is what MTVW sold during 2018:

Last year saw the average sale price decline by £25k to £305k — the first reduction since MTVW first disclosed the information in 2009 (when the average sale price was £161k).

The lower average sale price is not great when the average purchase price has reached a fresh peak.

4) Additional management narrative

The original results RNS did not contain these snippets from the non-exec chairman:

Not too much of consequence, but I thought the remark about smaller investors was interesting — perhaps only the larger players are now able to make property investment work given the extra sector costs (higher stamp duty etc).

5) Risks

MTVW presented a more comprehensive Risk section this year. Nothing too revelatory was revealed:

6) Breaches

Company secretary (and finance director) Maria Bray probably has to own up to these oversights:

7) New accounting rules

This time last year a property-valuation rule-change was possibly on the cards:

It now appears the rule change won’t affect MTVW:

8) Expected stock disposals for 2019

MTVW’s annual report gives this snippet:

I am not sure how useful the snippet is though. True, the prediction was £20.0m within the 2017 annual report and in the event stock of £21.8m was sold. But profitability was somewhat lower.

9) Director pay

The execs continue to be very well paid:

The reasons behind the chunky bonuses were not explained well:

Not everyone is happy at the new pay policy, introduced during 2017:

10) Concert party

The Sinclair family concert party now stands at 52% ownership:

11) Employees

Some unusual figure here:

Just 28 people are employed at MTVW.

Average pay per employee (including directors) dropped by £5k, but remains lofty at £134k. Revenue per average employee is an amazing £2.5m — and has generally bounced around between £2m to £3m during the last 10 years.

12) Trading properties

This footnote might be interesting.

This time last year MTVW’s small-print said:

“Any valuation within less than five years would serve little purpose, and would be a disproportionate expense”

This time around that line has been removed:

The valuation exercise was performed as at September 2014, so I wonder if another Allsop valuation is due within the next year or two.

13) Trade receivables

I always like this accounting note at MTVW:

Revenue of £70m… yet trade receivables are just £427k.

14) Loan rates

The cost of MTVW’s (larger) debt has risen, but not by much:

Maynard

Mountview Estates (MTVW)

Result of Annual General Meeting

Another year, another AGM with dissident voting. My sources report the meeting was once again used by the Murphy family (which owns 18%-plus) to question the board at length. Shareholder Mrs MA Murphy (15% holder) is the sister of MTVW’s chief exec.

Last year’s voting saw 1,700k votes for and 828k votes against some of the normal resolutions. This year the voting was c2,170k for and 927k against — so the Sinclair concert party (led by the chief exec) rallied an extra c470k of votes versus the dissidents’ extra 101k.

The RNS said:

“The Company is disappointed to note that Resolutions 8 and 9, to re-elect Tony Solway and to elect Tony Powell as Directors of the Company, were not approved by a majority of the Company’s independent shareholders. The Company is entitled, in accordance with the UKLA Listing Rules, to convene a general meeting (to be held within 90 and 120 days of today’s date) at which resolutions may be put to the meeting to re-appoint Tony Solway and appoint Tony Powell as Directors of the Company. A further announcement will be made in due course.”

Resolutions 8 and 9 were ‘independent’ resolutions, whereby the aforementioned Sinclair concert party did not vote. The 927k votes from the dissidents outweighed the 226k votes from non-concert party members.

A similar defeat occurred at last year’s meeting. A special general meeting was then later convened, with the unsuccessful resolution put to shareholders — but this time including the Sinclair concert party. The resolution was passed. The same procedure is set to happen, with a special general meeting planned with the voting again including the concert party. No doubt the unsuccessful resolutions will be passed this time, too.

As far as I can tell, the only notifiable (3%-plus) shareholder that could be a dissident is Talisman Dynamic Master Fund, with 4.14%. Talisman is an investment vehicle ultimately owned by the Pears family. The Murphys and Talisman represent c875k shares or 22.55%. Other voting dissidents have c50k shares, or c1.3%.

Similar to last year, I am not sure what to make of all of this voting. The resolutions will eventually go through and the non-execs will be appointed. But I guess it shows a sizeable minority of shareholders want change and would (probably) like the business to be sold.

Maynard