22 November 2022

By Maynard Paton

Results summary for Bioventix (BVXP):

- A somewhat better-than-expected FY performance, with record revenue and earnings supported by an exceptional H2 profit (+30%) that was bolstered by a post-pandemic recovery and stronger USD.

- Encouraging sales progress from best-seller vitamin D (+13%), future big-seller troponin (+81%) and sudden surprise-seller biotins (+67%) more than offset lost income from an expired product.

- Tweaks to management’s commentary plus a revised pipeline grid suggest the development work on dementia research now offers a greater chance of becoming a real money spinner.

- The accounts remain in great shape, with an astonishing 82% H2 margin, terrific employee productivity and robust cash conversion leading to the company’s seventh consecutive annual special dividend.

- Troponin’s finite income and a basic sum-of-the-parts valuation may explain why the £36 shares have not made headway during the last three years. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own BVXP

- Results summary

- Revenue, profit and dividend

- Vitamin D

- Troponin, biotin blockers and other antibodies

- Pipeline developments: Tau

- Pipeline developments: pyrene and industrial biomonitoring

- Pipeline developments: CardiNor and Pre-Diagnostics

- Financials

- Valuation

News links, share data and disclosure

News: Annual report and presentation for the twelve months to 30 June 2022 published 24 October 2022

Share price: £36

Share count: 5,209,333

Market capitalisation: £188m

Why I own BVXP

- Develops diagnostic blood-test antibodies, direct competition for which is limited due to the necessary scientific innovation, protracted regulatory testing, onerous switching procedures and ‘captive’ hospital end-customers.

- Boasts founder/entrepreneurial chief exec who has overseen an attractive growth record, retains an 8%/£15m shareholding and has declared seven special dividends.

- Employs ‘scalable’ royalty/licensing model that requires few employees and leads to terrific margins, generous cash flow and high returns on retained profits.

Further reading: My BVXP Buy report | All my BVXP posts | BVXP website

Disclosure: Maynard owns shares in Bioventix. This blog post contains SharePad affiliate links.

Results summary

Revenue, profit and dividend

- These FY 2022 results were somewhat better than I had expected following the unspectacular H1 performance.

- The preceding H1 had bemoaned pandemic disruption:

“The global pandemic has continued throughout the reporting period and has affected the activity within diagnostic pathways in hospitals and clinics around the world to which our business is intrinsically linked. The dynamics of the pandemic remain difficult to predict but when it eases, we believe our robust core business will respond accordingly.“

- But an update during September — BVXP’s first unscheduled RNS for five years! — revealed a much stronger H2:

“As announced in our interim results to 31 December 2021, we had a slow start to the financial year. However, in the second half, we have seen an improvement in performance and our trading result for FY2022 as a whole is likely to be significantly ahead of market expectations.“

- September’s update referred to a post-pandemic recovery and a stronger USD:

“This improvement reflects a degree of recovery from the pandemic effects experienced since early 2020, and we hope that this recovery will prove to be sustained and long-lasting…

In addition, our results are reported in UK Sterling and the recent fall in value of the UK Sterling against the US Dollar has had a positive effect.”

- Revenue in fact climbed 7% for the full year, which lifted reported operating profit by 15%. Both measures set new yearly records:

- H2 revenue advanced 21% while H2 operating profit surged 30%, or 26% adjusted for the effect of foreign-exchange gains (see Financials).

- BVXP said the stronger USD added £0.4m to H2 revenue.

- BVXP’s exceptional H2 witnessed a £5.7m operating profit, which equalled the level reported for the entire FY 2017.

- Total FY 2022 earnings of £7.7m exceeded the house broker’s earlier forecast by £1m:

- This FY performance was all the more impressive after BVXP suffered a £1.2m loss of revenue following a product licence expiry:

- BVXP appears to have outperformed Roche during the pandemic.

- Roche is the world’s largest in vitro diagnostic (IVD) company and is as good a benchmark as any to judge demand for the type of blood-test antibodies that BVXP develops.

- Between January-June 2019 and January-June 2022, BVXP’s revenue advanced by 42% (£4.9m to £7.0m) while Roche’s routine-diagnostic sales have at most expanded by approximately 30%:

- BVXP’s dividend payments were a lot higher than I had anticipated.

- The final payout was lifted a very useful 19%:

- My earlier H1 concerns about the size of any special dividend proved to be unfounded. BVXP declared a 26p per share extra payout, which takes the run of specials to seven years.

- The total ordinary/special payout for FY 2022 climbed 6% to 152p per share.

- Cash finished the year at £6.1m — a good £1m improvement from the preceding H1 — and exceeded BVXP’s liking for a minimum £5m cash balance:

“Our current view continues to be that maintaining a cash balance of approximately £5 million is sufficient to facilitate operational and strategic agility both with respect to possible corporate or technological opportunities that might arise in the foreseeable future. We have therefore decided to distribute surplus cash that is in excess of anticipated needs and we are pleased to announce a special dividend of 26 pence per share.”

- Cash topping that £5m ‘buffer’ could herald a special dividend for the eighth consecutive year.

- Note that the cash ‘buffer’ wording for this FY 2022 was encouragingly different to that of the comparable FY 2021 (below):

“Our current view continues to be that maintaining a cash balance of approximately £5 million is sufficient to facilitate operational and strategic agility both with respect to possible corporate or technological opportunities that might arise in the foreseeable future and to provide comfort against the ongoing impact of the pandemic and any economic uncertainty arising from it. We have therefore decided to distribute surplus cash that is in excess of anticipated needs and we are pleased to announce a special dividend of 38 pence per share.“

- No mention this time of providing “comfort” against the pandemic!

Vitamin D

- BVXP’s vitamin D antibody delivered welcome progress during H2.

- The preceding H1 had suggested vitamin D sales were stagnating or reversing:

“As reported previously, the growth rates for our vitamin D antibody sales were not expected to match those seen in recent financial years and a plateau in the downstream global vitamin D assay market had been anticipated. Sales associated with assay formats using larger quantities of antibody per test suffered more as price erosion in downstream markets puts pressure on costly “antibody-hungry” products“

- But this FY statement revealed vitamin D sales advancing a commendable 13%:

“Our most significant revenue stream continues to come from the vitamin D antibody called vitD3.5H10. This antibody is used by a number of small, medium and large diagnostic companies around the world for use in vitamin D deficiency testing. Sales of vitD3.5H10 increased by 13% to £5.4 million which we believe reflects an improved downstream market for vitamin D testing following a degree of recovery from coronavirus pandemic effects.“

- Vitamin D remains by far BVXP’s best seller at 46% of revenue:

- Vitamin D’s proportion of total revenue has been 38% or more since FY 2016.

- Perhaps vitamin D will continue to sell well after what seems to have been a pandemic-related blip.

- BVXP issued warnings about vitamin D income “plateauing” within its FY 2017, FY 2018 and FY 2019 results, when the antibody was delivering 20%-plus per annum revenue growth.

- Management has in the past claimed the ‘plateauing’ of vitamin D growth to mean the rate reducing to between 5% and 10% — to match the projected expansion of the wider antibody market.

- But FY 2022’s 13% advance suggests vitamin D may not have ‘plateaued’ just yet.

- Development on the vitamin D antibody started during 2008 and revenue was first earned during 2011.

- Going from zero revenue to £5.4m within eleven years gives some idea of the prospects for BVXP’s newish troponin antibody.

Troponin, biotin blockers and other antibodies

- This FY 2022 statement reminded shareholders that BVXP’s near-term progress remains dependent on its troponin antibody:

“Over the next few years, the continued commercial development of the new troponin assays and their roll out by our customers will have the most significant influence on Bioventix sales.“

- Development work on troponin — an element used to detect potential heart attacks — started during 2006 and the antibody first generated sales during FY 2019.

- Troponin income jumped a super 81% during this FY:

“Total troponin antibody sales from Siemens Healthineers and another separate technology sub-license almost doubled during the year to £1.23 million (2020/21: £0.68 million). This significant increase clearly demonstrates a gathering momentum of product roll-outs for the new high sensitivity troponin assays supported by SMAs and we believe that these revenues will continue to grow.“

- Troponin sales of £1.23m underpinned a management prediction from two years ago, which claimed troponin revenue advancing from £330k at the time to £1.2m by FY 2022 was “entirely plausible“.

- BVXP’s house broker continues to estimate troponin income could grow to between £3m and £3.5m by 2025.

- Among BVXP’s other antibodies, income from “biotins and biotin blockers” was divulged for the first time:

- T3 (tri-iodothyronine): £0.93 million (+25%);

- biotins and biotin blockers: £0.90 million (+67%)

- progesterone: £0.62 million (+14%);

- estradiol: £0.59 million (+34%);

- testosterone: £0.47 million (+7%);

- drug-testing antibodies: £0.38 million (-7%);

- Biotins and biotin blockers enjoyed 67% annual sales growth and now appear to be BVXP’s fourth best-selling product after vitamin D, troponin and tri-iodothyronine (T3).

- I don’t know why BVXP started to disclose income from biotins and biotin blockers this year rather than the prior year — when sales were £539k and already exceeded the revenue from many other disclosed products.

- Update 06 Jan 2023: My original interpretation of BVXP’s biotin blockers was wrong! Management clarified the situation at last month’s AGM.

Biotins and biotin blockers look to have been a relatively speedy success. BVXP’s first mention of biotin occurred within the FY 2018 results:

“Another project that is just starting at Bioventix features biotin. Biotin is a vitamin supplement that is widely available and has been associated by some people with claims relating to hair and skin health. Biotin is also part of a “chemical Velcro” that is used in assay formats by some of our customers. It has become clear that high dose consumption of these biotin supplements can result in aberrant results from some clinical assays and a solution to this problem could have value.”

Four years from drawing board to revenue of £900k is very impressive.

BVXP underplayed the progress of its biotin blockers by implying sales were “modest“:

“The biotin “blocker” antibodies and THC sandwich antibodies reviewed in our previous reports have now progressed at customers and modest sales are now being generated to add to our total revenues.”

In fact, BVXP implied within the prior-year statement that biotin blockers were not yet commercially feasible:

“As this project has evolved, it has become clear through FDA guidelines that much larger quantities of biotin blockers will be required in assay reagent packs. This imposes cost/price constraints in addition to manufacturing/capacity challenges. Over the next year, we will explore production systems (such as E.coli) in order to identify improved production techniques which could facilitate commercial feasibility.“

- As well as the biotin blockers becoming commercial, BVXP’s tetrahydrocannabinol (THC) test has also made it to market and presently earns “modest” sales.

- Yearly income from BVXP’s other five “core historic” antibodies — used for testing thyroid function, fertility and drug abuse — climbed 17% to support 26% of group revenue.

- Longer-term progress from the five antibodies has been mixed. Between FYs 2017 and 2022 for example, sales of T3 have rallied 88% while sales of testosterone have slid 19%:

- Within the prior-year statement BVXP described these five products as “lead” antibodies, and I am not sure whether the description change to “core historic” antibodies for FY 2022 signals the collection may have seen its best days.

Pipeline developments: Tau

- The removal of one sentence from these FY 2022 results could signal improved product-pipeline potential.

- BVXP said within the prior-year statement:

“There are currently no antibodies in the future pipeline that are comparable to our troponin products in potential value and the ability to influence revenues in the next few years.“

- But that sentence was omitted for FY 2022, which suggests the development pipeline may indeed be harbouring a product that now has troponin-type potential value.

- BVXP would not be drawn on any pipeline predictions:

“Whilst antibodies in the future pipeline are at stages of testing and development that do not allow us to make any prediction about their potential value and influence on future revenues there has still been encouraging progress.“

- I reckon the project concerning Tau proteins for dementia research offers the best chance of becoming a pipeline money spinner

- The Tau project had its probability of success improved during the year from Low to Medium:

- BVXP said efforts on the Tau project had been encouraging:

“Another biomarker that has shown potential in Alzheimer’s diagnostics is the Tau protein in the form of total Tau and phosphorylated Tau. During the year we created more anti-Tau antibodies and this work will continue into 2023. Our academic collaborators at the University of Gothenburg have used our antibodies to create prototype assays and have generated encouraging data from patient blood samples.“

- But work remains to be done to enhance the test:

“The levels of Tau detected using our antibodies are approximately 2 times higher in Alzheimer’s samples compared to controls, a ratio of 2 times being similar to other research groups. Our scientific target ratio is slightly higher at 4-5 times. We are encouraged by this progress and plan to create more antibodies to support further work with our collaborators in Gothenburg during 2023.”

- BVXP referred to Alzheimer’s developments elsewhere:

“The recent success of the Eisai/Biogen lecanemab clinical trial is likely to increase the need for early [Alzheimer’s] diagnostics and we are very fortunate to be working with one of the world’s leading labs focussed on Alzheimer’s biomarkers and tests.“

- Biogen describes lecanemab as an “investigational humanised monoclonal antibody for Alzheimer’s disease [AD]” that “selectively binds to neutralise and eliminate soluble, toxic amyloid-beta aggregates (protofibrils) that are thought to contribute to the neurodegenerative process in AD.”

“The study shows that removal of aggregated amyloid beta in the brain is associated with a slowing of disease in patients at the early stage of the disease”

- The phase 3 trial involved 1,795 volunteers with the early-stage Alzheimer’s being injected with lecanemab every two weeks for 18 months and undergoing regular memory tests. The pace of ‘cognitive decline’ was reduced by 27%.

- Regulatory approvals for lecanemab are the next step with submissions due by March 2023, although Biogen’s statement does suggest an FDA decision could be forthcoming by early January.

- Regulatory approvals for lecanemab could in turn spur demand for Alzheimer’s tests such as BVXP’s anti-Tau antibody, which hope to indicate the likelihood of developing the condition.

“Anti-tau antibody failures stack up

Lilly has discontinued development of zagotenemab, following the antibody’s failure in a phase II trial in Alzheimer disease. It is the fourth setback for the troubled anti-tau pipeline, following clinical trial misses for Roche and AC Immune’s semorinemab, AbbVie’s ABBV-8E12 and Biogen’s gosuranemab.“

Pipeline developments: pyrene and industrial biomonitoring

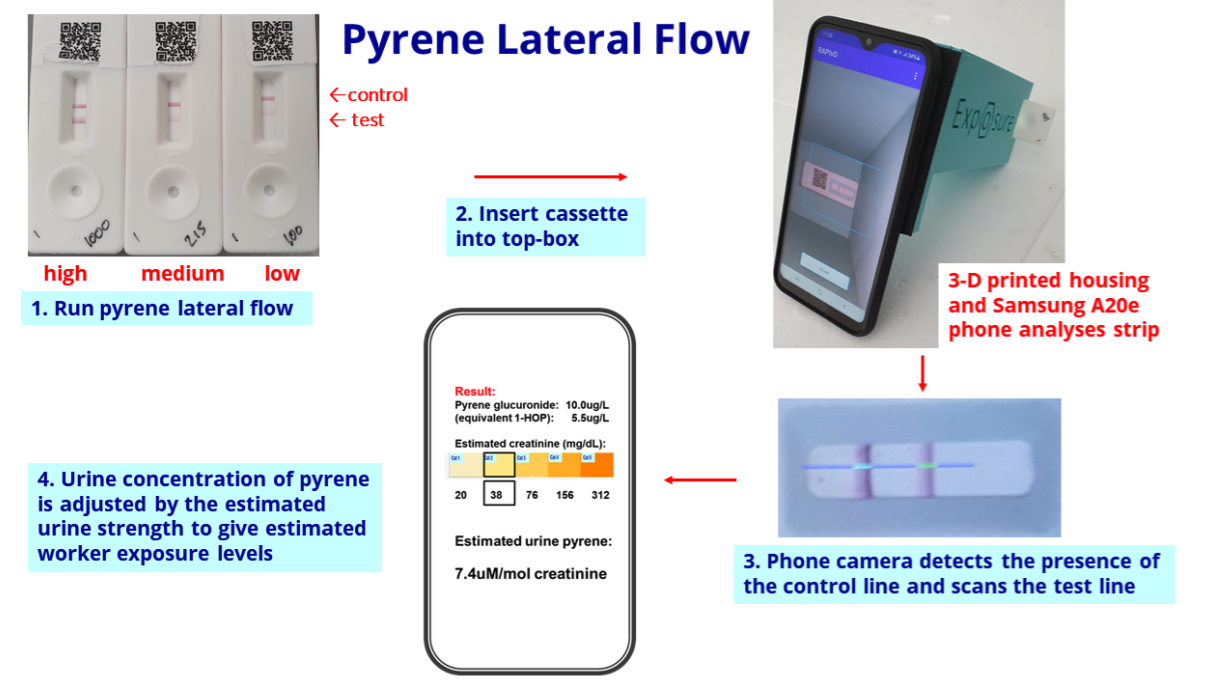

- BVXP’s pipeline grid sadly showed the group’s two biomonitoring projects downgraded from Medium to Low potential value:

- I had hoped BVXP showcasing pyrene biomonitoring its homepage was a sign the product had notable commercial value:

- The biomonitoring tests work by examining a urine sample through a mobile phone:

- BVXP confirmed development work on the biomonitoring projects would continue during next year:

“Our pyrene lateral flow system for industrial pollution biomonitoring completed a trial at a UK industrial site during quarter 4 of 2021. This went well and we plan to conduct additional site studies during 2023…

The progress of the pyrene project has encouraged us to consider additional assays for benzene and isocyanates, also in the field of industrial health and safety. Benzene exposure is of relevance to the petroleum industry and isocyanates are hazardous chemicals used in the manufacture of polyurethane paints and plastics. This work will continue into 2023 and 2024.”

- BVXP repeated the text below from FY 2021, which reiterated how the company is seemingly trying to create the market for these pollution tests by itself:

“We accept that the creation, manufacture and supply of final assay [biomonitoring] products is outside our normal focus of bulk antibody sales but we believe that through our own efforts we can substantiate the viability of such products and generate demand, thereby stimulating the interest of future commercial partners.”

- The present absence of clear commercial interest alongside the unknown economics of the test kits probably explain the aforementioned project downgrade to Low potential value.

- Manufacturing the pyrene kit is unlikely to enjoy the same wonderful economics as selling 15-20 grams of physical antibodies a year (point 1e).

Pipeline developments: CardiNor and Pre-Diagnostics

- The commercialisation of biotin blockers and THC leaves the collaborations with Norwegian research houses CardiNor and Pre-Diagnostics as BVXP’s third pipeline opportunity alongside Tau proteins and biomonitoring:

- BVXP has invested an aggregate £610k into CardiNor and Pre-Diagnostics since FY 2016.

- The Norwegian projects remain in deep development and show no signs of imminent revenue:

“Our partners at CardiNor (Oslo) have continued with their work to try and identify the possible utility of secretoneurin in heart failure patients and in particular those patients who might be candidates for implantable cardiac devices (ICDs). Data from recent patient sample studies does show a link with heart disease read-outs. The next step for CardiNor will be to define the potential utility of secretoneurin diagnostics in cardiac health.

Pre-Diagnostics (also in Oslo) and their clinical collaborators have two amyloid beta assays based on Bioventix antibodies available for research use. The goal of the project is to identify fragments of amyloid beta in patient samples that would be helpful in Alzheimer’s diagnostics. A new area of interest is the diagnosis of ARIA, a side-effect related to new anti-amyloid drugs.“

“Q: What further work has to happen now for secretoneurin to be developed into a commercial cardiovascular biomarker?

A: Much work on the assay development side has already been completed, and CardiNor has recently received CE-marking for its secretoneurin ELISA in Europe. Work has also been initiated for implementation of the assay on big laboratory platforms and preparations for submission to the FDA are being planned. The key for secretoneurin to be developed into a commercial cardiovascular biomarker is the results of ongoing and future clinical studies, validating the hypotheses of a secretoneurin being a strong biomarker of arrhythmia risk and of providing robust and complementary prognostic information to conventional risk markers, including cardiac troponins and BNP/NT-proBNP in patients with acute or chronic heart failure.“

- “…preparations for submission to the FDA” sounds promising. CardiNor’s secretoneurin biomarker tests for a particular type of heart failure and perhaps complements BVXP’s own troponin and (now terminated) NT-proBNP products that detect other heart complaints.

- Pre-Diagnostics is developing an Alzheimer’s test that would indicate early diagnosis of the disease, and appears similar to BVXP’s work with Tau proteins:

- News from Pre-Diagnostics talks of the “coming market phase“:

“After three years as a start-up in ShareLab’s shared facilities , we are moving to new offices at Parallell Oslo that include our own fully furnished lab. The move allows us to both concentrate on development work and prepare for the coming market phase. With this, we are one step closer to bringing our Alzheimer’s blood test to the market.“

- Note that BVXP now refers to “2026 to 2036” for the pipeline to create “shareholder value”:

“Excellent technical progress has been made with our research projects and we anticipate that our pipeline of opportunities will create additional shareholder value in the period 2026 to 2036.“

Financials

- The exceptional H2 witnessed an astonishing 82% operating margin — BVXP’s best ever conversion of revenue into profit for any six-month period:

- BVXP’s margin was enhanced by cost of sales decreasing by 13% despite revenue advancing by 7%:

- The lower cost of sales may be due to a greater proportion of royalty and licence fee income, which represented 69% of group revenue — the highest since FY 2017 (73%):

- The lower cost of sales may also be due to lower research and development expenditure:

- Lower R&D presumably reflects the recent commercialisation of biotin blockers and THC.

- Foreign-exchange gains/losses also interfered with reported operating profit:

- The foreign-exchange gains/losses arise when customers pay BVXP more/less than what was initially recognised as revenue because of subsequent exchange-rate movements.

- Such foreign-exchange gains/losses can be significant for BVXP because the bulk of group income is:

- Denominated in USD, EUR and various Asian currencies, and;

- Received every six months (which amplifies the accounting impact of currency movements).

- The gains/losses can affect BVXP’s short-term performance but have not been a significant long-term influence.

- Between FYs 2018 and 2022, aggregate foreign-exchange gains/losses came to a negative £169k versus aggregate revenue of £51m and aggregate reported operating profit of £39m.

- BVXP reiterated within these FY 2022 results that currency movements were not hedged.

- BVXP’s super margin reflects the company’s terrific employee productivity. The 2022 annual report revealed BVXP employed only 16 staff costing a total £1,261k…

- … which translates into a cost per employee of £79k, although revenue per employee is a superb £732k:

- Cash conversion during FY 2022 did not look problematic:

| Year to 30 June | 2018 | 2019 | 2020 | 2021 | 2022 |

| Operating profit* (£k) | 6,060 | 6,931 | 8,184 | 8,087 | 9,273 |

| Depreciation (£k) | 58 | 76 | 134 | 135 | 143 |

| Cash capital expenditure (£k) | (108) | (85) | (340) | (260) | (12) |

| Working-capital movement (£k) | (539) | (47) | 412 | (1,004) | (652) |

| Net cash (£k) | 6,987 | 6,537 | 8,076 | 6,495 | 6,127 |

(*before back-dated royalties)

- Working-capital absorbed an extra £652k to reflect the greater royalty and licence fees recognised as revenue during H2 that had still to be paid after the year-end.

- Within working capital, total debtors of £5.2m does appear alarming versus revenue of £11.7m:

- But the debtors mostly reflect the royalty and licensing income that is received after the year-end but before the final accounts are published, and as such the outstanding monies are (in theory!) always collected.

- The modest working-capital movement plus capex of just £12k allowed earnings of £7.7m to translate into free cash flow of £7.5m — up £1.4m on FY 2021.

- Total cash dividends of £7.9m then left the cash position £0.3m lighter at £6.1m over the FY.

- The balance sheet carries no bank debt and no pension complications.

- The £6.1m cash position exceeds the aforementioned £5m minimum by £1.1m.

- Were FY 2023 to repeat FY 2022 and produce free cash flow of £7.5m, an eighth consecutive special dividend would be very likely.

- The seventh consecutive year of declaring a special dividend re-emphasised how BVXP has expanded without significant retained profits.

- For example, since FY 2017 BVXP’s earnings have advanced £2.8m to £7.7m while shareholder equity (i.e. earnings less all dividends paid) has advanced £1.7m to £11.8m:

- Retaining £1.7m to earn an extra £2.8m since FY 2017 has been incredibly impressive.

- BVXP’s tax charge was assisted for the 15th consecutive year by tax credits:

- BVXP commendably disclosed the forthcoming increase to corporation tax would have lifted the tax charge from 17% to 23% (and would have reduced earnings by nearly 7%):

“Factors that may affect future tax charges

The rate of corporation tax in the UK is set to be increased from the current rate of 19% to 25% with effect from 1 April 2023. This change will increase the tax charge in future years such that, had the change been in place in the current year, it would have increased by £517,163 from £1,603,874 to £2,121,037.“

Valuation

- BVXP’s outlook contained a useful guide to potential future growth:

“We are pleased with our financial results for the year which we believe reflect both the growth in the use of our products and of course some relief from the global pandemic. In particular the continued roll-out of the high sensitivity troponin assays and the royalties associated with them have combined to help replace revenues from NT-proBNP which ceased from August 2021. After stripping out the impact of these 2 significant changes the growth in our underlying business over the year is in the range 8-10% which we believe is sustainable for the immediate future as our sales mix continues to change.“

- The FY presentation sadly did not include an updated broker forecast for FY 2023:

- BVXP had re-introduced the disclosure of broker forecasts within the preceding H1 presentation after dropping such estimates from the slides during the pandemic.

- Doubling up the stronger H2, ignoring foreign-exchange gains and applying that higher 23% tax rate leads to earnings of almost £8.7m or 166p per share.

- Earnings of 166p per share support a 22x multiple with the share price at £36.

- Earnings of 166p per share leave only 14p per share for higher FY 2023 dividends after a total 152p per share was declared through ordinary/special payouts for FY 2022.

- Bear in mind troponin revenue will cease during 2032 and the associated profit should not therefore be valued on a simple multiple.

- Assuming troponin revenue:

- Averages (a probably optimistic) £4m for the next 9.5 years before expiry;

- Has no associated cost, and;

- Is taxed at the upcoming 25% standard UK rate…

- …gives an after-tax value of £29m before any time-value discounting.

- The table below derives the possible earnings from BVXP’s vitamin D and other commercialised antibodies by:

- Estimating FY 2022 revenue without troponin and expired product revenue;

- Then subtracting all cost of sales and administration expenses;

- Then adding back all R&D costs, and;

- Ignoring foreign-exchange gains, share-based payments and R&D tax credits:

| Estimated FY 2022 for vitamin D and other antibodies | (£k) |

| Revenue | 11,719 |

| Less NT proBNP revenue | (80) |

| Less troponin revenue | (1,230) |

| Less cost of sales | (710) |

| Less admin expenses | (1,605) |

| Add back R&D expenses | 975 |

| Operating profit | 9,069 |

| Less tax at 25% | (2,267) |

| Earnings | 6,802 |

- Applying a 25x multiple to the derived £6.8m earnings values BVXP’s vitamin D and other commercialised antibodies at £170m.

- The present £188m market cap less the £29m troponin estimate less the £170m vitamin D/other estimate therefore leaves the pipeline valued at a negative £11m.

- Valuing the pipeline at a negative £11m does not feel optimistic given annual R&D costs are almost £1m and commercialisation is not expected until 2026 at the earliest.

- True, these valuation sums could be fine-tuned to:

- Calculate a more realistic net present value for troponin;

- Include R&D tax credits;

- Allocate cost of sales to the appropriate antibody, and;

- Apply different multiples to that £6.8m vitamin D/other estimate…

- …but right now signs of a compelling valuation are not truly obvious.

- The sums could explain why the shares have not made headway during the last three years:

- A premium rating is nonetheless understandable. Shareholder attractions remain:

- The predictable and ongoing income from antibody sales and royalties (pandemics aside);

- A competitive ‘moat’, helped in part by protracted development/regulatory timescales and ‘captive’ end-customers (e.g. hospitals) limited to particular blood-test machines (and therefore particular antibodies), and;

- The amazing margins and minimal reinvestment requirements, which underline the terrific economics of antibody commercialisation.

- The present market cap leaves longer-term upside rather dependent on the success of the pipeline, with the Alzheimer’s projects looking the favourite to become real money-spinners.

- In the meantime the dividend yield is a useful 4.2% if BVXP continues to distribute ordinary and special payouts that total 152p per share.

Maynard Paton

Bioventix (BVXP)

Publication of 2022 annual report

Here are the points of interest:

1) INTRODUCTION AND TECHNOLOGY

A number of minor text changes for 2022:

a) Downstream royalties were previously 60-70% of revenue but are now “approximately 70%“:

“In addition to revenues from physical antibody supplies, the sale by our customers of diagnostic products (based on our antibodies) to their downstream end-users attracts a modest percentage royalty payable to Bioventix. These downstream royalties currently account for approximately 70% of our annual revenue.”

b) This line about currencies is no longer included:

“Physical antibody sales and royalty revenues from our multinational customers are made in either US dollars or Euros.

c) Extra text concerning barriers to entry:

“However, because of the resource required to gain such approvals, after having achieved approval for an accurate diagnostic test using a Bioventix antibody, there is a natural incentive for continued antibody use. This results in a barrier to entry for potential replacement antibodies which would require at least partial repetition of the approval process arising on a change from one antibody to another. This barrier to antibody replacement arises from a combination of factors driven by the clinical criticality of the test and the potential consequences of making such a change which include the time and cost to register any changes required to validate the performance of the replacement antibody.”

d) As noted in the blog post above, the pipeline timeline has changed from 2025-2035 to 2026-2036:

“By the same dynamics, the current research work active at our laboratories now is more likely to influence sales in the period 2026 to 2036.”

e) Physical antibody volumes remain tiny:

“We currently sell a total of 15-20 grams of purified physical antibody per year, the vast majority of which is exported.”

2) TEAM AND FACILITY

a) Confirmation that the 16 employees listed in note 5 are actually 12 full-time equivalents, making underlying revenue per employee even better than what was stated in my blog post above:

“The composition of the Bioventix team of 12 full-time equivalents has remained stable over the year, facilitating excellent performance and know-how retention.”

b) Not as much text this year on supply chains, which seem to have been managed well despite problems:

“Supply chain issues relating to plastics and chemical reagents have persisted during the year but have been expertly managed by our procurement team.”

c) And new text about a diesel generator:

“Turmoil in the energy market has added another risk factor with some energy commentators predicting power outages during the winter of 2022/23. We plan to use our diesel generator and reserve fuel supplies to minimise any disruption caused to the lab by any such power outages.”

3) ENVIRONMENTAL, SOCIAL AND GOVERNANCE

An all-new section for 2022, which talks of improved productivity “yields” and possibly improved dementia testing “over the next few years“:

“Our production processes consume quantities of reagents and plastics. A key goal for the company is to use our various technologies to reduce the quantities of materials we consume. The use of bioreactor technology has resulted in a significant reduction in plastics consumption and we have converted one antibody to this production format during the year.

Genetic engineering techniques can also be used to enhance antibody productivity and we have successfully implemented techniques for one antibody during the year, resulting in a four-fold increase in yield.

The mass immunisation of sheep to make serum-based reagents for clinical assays has been commonplace since the 1970s. SMAs made in vitro can substitute for this large-scale use of animals and our T4 (thyroxine) antibody is reaching the market, thereby resulting in a reduction in animal usage.

Over the last 20 years, our SMAs have been used to improve the diagnostic processes at hospitals around the world. This has resulted in improved diagnostic tests for heart disease, thyroid function and fertility. Our goal over the next few years is to extend this success to dementia diagnostics.

Internally at Bioventix, we value our team and seek ways to help them as they develop their lives. We have supported new parents in their desire to return to work and we now have four employees who work part-time having returned to the laboratory after parental leave.

Regarding corporate governance, we continue to follow the guidelines of the Quoted Companies Alliance as described in our Governance Report on page 40. We are aware of the need to increase the diversity of our Board whilst maintaining skills and experience to underpin corporate culture and support business continuity which both bring benefits for all our stakeholders. In common with many businesses, we find that limited candidate availability has compromised our progress in this regard but our efforts will continue. ”

4) PRINCIPAL RISKS AND UNCERTAINITIES

No changes here from the previous year:

“* Dependence on key employees

* Technology (e.g. R&D failure, risk of disruption)

* Regulatory environment

* Distribution risk (e.g using sheep-derived antibodies)

* Market risk (e.g customers could merge, or no longer require BVXP antibodies)

* Competition“

The Competition section claims BVXP enjoys “unique” skills:

“Whilst the Company does not operate under granted patents, the directors believe that the Company has a significant set of know-how and skills that are unique”

5) DIRECTORS STATEMENT SECTION 172

a) This 2022 report did not repeat the following text from 2021:

“Culture, values and standards form the foundations for a company’s operating behaviours and processes by which it creates and sustains value. They also assist and guide decision-making and thereby help promote a company’s success. The Board will continue to build its model for engagement with key stakeholders and will, in future reports, provide more detail of our progress, including how we engage and the impact of such engagement on the Company’s strategy and principal decisions.

From what I can tell, this 2022 report did not include that much “more detail” on stakeholder engagement than last year.

b) The 2022 report now lists the 3%-or-more shareholders.

6) SUSTAINABILITY REPORT

Two revisions to this year’s text:

a) Further notification of the higher production “yields“:

“During the year we have converted one of our processes to use bioreactors, thereby reducing our use of plastic flasks. We also promote the effective and efficient use of equipment, facilities, services and supplies and have implemented genetic engineering techniques to deliver a four-fold increase in the yield in the production of one of our antibodies. In addition we are using SMAs made in vitro, to replace the mass immunisation of sheep, for our T4 (thyroxine) antibody which is now reaching the market, resulting in a reduction in animal usage. ”

b) BVXP is now helping new parents:

“Internally at Bioventix, we place great value on our team and wherever it is practicable we seek ways to help them as they develop their lives and their responsibilities increase. We are supportive of new parents in their desire to return to work and we now have four employees who work on a part-time basis having returned to Bioventix after parental leave.”

c) And the CEO commendably continues to brief staff about the results:

“Bioventix has a very at management structure. Interaction between the Executive Directors and staff is a daily event and very much part of the culture of the Company. In addition, to ensure that all staff are aware of the Company’s strategy and performance, all staff are notified when interim and full-year Annual Reports are published and the CEO conducts a briefing to which all staff are invited where full information is provided and discussed in an open and inclusive environment.”

7) THE BOARD OF DIRECTORS

No changes here, but worth reiterating the non-exec’s relevant sector experience:

a) Ian Nicholson

“Ian was appointed as Non-Executive Chairman of Bioventix in November 2004. Ian is also an Operating Partner at Advent Life Sciences LLP and a Trustee of LifeArc, a leading UK medical charity. From 2013 to 2021 Ian was Chief Executive Officer of F2G Ltd, an anti-fungal drug development company and from 2004 to 2012 Ian was Chief Executive of Chroma Therapeutics Limited, a drug discovery and development company. He previously held the position of Senior Vice President, Business Development at Celltech Group plc, then the UK’s largest biotechnology company. He has extensive experience in licensing, mergers and acquisitions, and market development in the UK, Europe and the US. ”

b) Nicholas McCooke

“Nick has worked in the biotech industry for over 30 years and is now an independent consultant providing operational, strategic and commercial advice and hands-on support to biotech companies. He has led several successful companies. He was the founding CEO of Solexa, the Cambridge University spin-out where he built the team that invented and developed Next Generation DNA sequencing. Subsequently he was CEO of Belgian company Pronota, which translated novel protein biomarkers into diagnostics, and where he gained much knowledge and expertise in the diagnostic development and market access process. Most recently he was CEO of DNA sequencing technology company Longas pty Ltd.”

The non-execs participate in the option scheme, which contravenes corporate-governance protocols, but BVXP’s progress over time does not suggest outside shareholders have been compromised:

“The Independent Non-Executive Directors, Ian Nicholson and Nick McCooke, are both considered as independent by the Board and are both participants in the Company’s Share Option Plan. The Board recognises that since independence can be easily compromised, Non-Executive Directors should not normally participate in performance-related remuneration schemes or have a significant interest in a company share option scheme. The QCA Code acknowledges that where performance-related remuneration is under consideration, it should be proportionate, shareholders must be consulted and their support must be obtained. Prior to the issue of share option awards, in 2017 and in 2020, the Board consulted with all material shareholders and there were no dissenting views. Furthermore, the Board believes that the participation, by the Non-Executive Directors, in the Company’s share option scheme has not and does not impair their ability to act as independent Non-Executive Directors.”

8) CORPORATE GOVERNANCE STATEMENT

No changes here from 2021. Point 10 reiterates PIs are welcome to attend the AGM (I plan to attend this year’s meeting):

“Smaller private investors are encouraged to attend the AGM, when permitted, at which the Company’s activities are considered and there is an opportunity for shareholders to meet, discuss the Company’s business and governance and for questions to be answered.”

9) AUDIT COMMITTEE

A change of auditor, which seems unprompted:

“During the year, the Committee met twice to consider standard business relating to the review of half-year and annual financial statements. The Committee also met on a further four occasions to consider the appointment of new external auditors and related auditor tender process, following the resignation of James Cowper Kreston as the Company’s external auditor; they have confirmed that there are no circumstances connected with their resignation that they consider should be brought to the attention of members or creditors of the Company.”

Not sure if the AIM rules mandate announcing the change of auditor through an RNS (this change was not announced at the time). Despite the similar names, former auditor James Cowper Kreston and the new auditor Kreston Reeves appear to be separate operations judging by their websites.

Text includes useful insight as to how auditors are selected:

“* Audit firms within the top 25 firms in the UK that are active and experienced in the market for auditing stock exchange listed companies that, because of the value of their market capitalisation, are defined as Other Public Interest Entities (OPIE);

* Experience of working with smaller growing businesses working in the Life Sciences and Biotech sector;

* A fit with Bioventix, its culture, ethos and aims;

* An audit approach bringing efficiencies or adding value; and

* Fee estimate.”

10) REMUNERATION COMMITTEE

a) A reminder that all options have no performance conditions:

“Under the terms of the Company’s 2013 EMI Share Option Scheme, the Approved Scheme, directors and employees are eligible for awards. Performance conditions do not apply to the awards and upon any change of control, all options vest in full. All options lapse upon the tenth anniversary of grant.“

Director options total 23,326 or 0.4% of the share count.

b) A reminder that the chief exec’s bonus seems linked to the share price:

“The Chief Executive’s bonus above is determined by the Remuneration Committee according to performance criteria designed to be consistent with companies of a similar profile and relating to EPS and share price parameters, together with a smaller R&D element.”

c) Director pay remained unchanged for 2022:

“In light of the ongoing COVID-19 pandemic and the ensuing uncertainty, remuneration remained unchanged for 2021/22. The Remuneration Committee plans to conduct a comprehensive review of remuneration in November 2022.”

BVXP’s board has always seemed good value for money, so let’s hope the “comprehensive review of remuneration” does not lead to some extravagances!

Last year the chief exec’s basic pay was lifted £5k, bonus reduced by £30k and pension contribution increased by £2k:

d) Extra text this year about director service contracts:

“The Executive Directors are subject to service contracts with a notice period of six and three months respectively for the Chief Executive Officer and Chief Financial Officer. Payments on termination for Executive Directors, other than on the grounds of incapacity or circumstances justifying summary termination, are restricted to the value of any unexpired notice period and the cost of providing other contractual benefits during the unexpired notice period.”

11) NOMINATIONS COMMITTEE

A reminder that new board appointments are more likely to be non-execs than execs:

“The Committee met twice during the year to consider the composition of the Board and, in particular, to review the requirement to appoint further Non- Executive Directors as the business grows. Future appointments will be made based on required expertise to match the needs of the business whilst bearing in mind the need to introduce diversity into the Board composition.”

12) AUDITOR’S REPORT

The change of auditor has led to numerous text alterations, but nothing obviously untoward has been removed or included.

a) Key audit matters

Remain ‘revenue recognition’, ‘valuation of investments’ and ‘management override’.

b) Materiality and scope

Materiality remains the standard 5% of pre-tax profit and scope remains 100% as the company has no subsidiaries.

c) Audit procedures

The new auditor includes a longer list of procedures than the previous auditor, which may be due simply to new audit-reporting requirements:

“* Detailed discussions were held with management to identify any known or suspected instances of non-compliance with laws and regulations; and

* Identifying and assessing the design effectiveness of controls that management has in place to prevent and detect fraud; and

* Challenging assumptions and judgements made by management in its significant accounting estimates; and

* Performing analytical procedures to identify any unusual or unexpected relationships, including related party transactions, that may indicate risks of material misstatement due to fraud; and

* Confirmation of related parties with management, and review of transactions throughout the period to identify any previously undisclosed transactions with related parties outside the normal course of business; and

* Performing analytical procedures with automated data analytics tools to identify any unusual or unexpected relationships, including related party transactions, that may indicate risks of material misstatement due to fraud; and

* Reading minutes of meetings of those charged with governance and reviewing correspondence with relevant tax and regulatory authorities; and

* Review of significant and unusual transactions and evaluation of the underlying financial rationale supporting the transactions; and

* Identifying and testing journal entries, in particular any manual entries made at the year end for financial statement preparation. ”

13) NOTES TO THE FINANCIAL STATEMENTS

BVXP’s accounts are presented in the ye old UK GAAP style because the AIM rules allow the accounts of the top parent entity to employ either the domestic accounting standards or IFRS, and BVXP having no subsidiaries means its financials are all in the top parent entity.

a) New for 2022 are finance costs

“Finance costs are charged to profit or loss over the term of the debt using the effective interest method so that the amount charged is at a constant rate on the carrying amount. Issue costs are initially recognised as a reduction in the proceeds of the associated capital instrument.”

Not sure what the £303 was spent on. Lease costs for the diesel generator?

Note how interest received has tumbled from £31k to £5k. I would like to think BVXP will soon benefit from higher rates on its cash savings.

b) Tangible fixed assets

Following the (relatively sizeable) lab fit-out costs of the prior year, capex for 2022 rescued to just £12k:

BVXP did not disclose the prior-year numbers for this note, which is poor form.

c) Stock

Average stock held during the year was £397k:

Versus cost of sales of £710k suggests stock stays in the lab freezer for 6-7 months before being sold. I suspect cost of sales includes other items beyond stock, so stock turn may be longer. For the past few years stock turn has been 3-4 months, so stock levels are relatively high. But I am sure BVXP’s stock of antibodies does not become obsolete overnight while the £462k year-end entry is only 4% of revenue.

d) Creditors

Nothing too amiss here:

Total creditors are equivalent to 11% of revenue, and the proportion has bobbed between 3% and 15% during the last decade. Creditors are mostly tax, accrued expenses or deferred income (advance customer payments), with trade creditors relatively small at £150-160k (although non-staff costs last year were not huge either at c£1m).

e) Options

Total options of 50,498 are equivalent to 1% of the share count:

Maybe further options will feature within the aforementioned “comprehensive review of remuneration!

Maynard

Biotins clarification (BVXP)

I attended BVXP’s AGM last month and obtained clarification on its biotins and biotin blockers.

My original interpretation of the sales progress of biotin blockers was completely wrong! Management confirmed sales of biotin blockers were indeed modest.

What has happened is the existing biotins product is driving sales. Developed in 1999, this biotins product is now used sometimes as a replacement for streptavidin. Some “good fortune” has apparently been involved here. BVXP has no insight into which product the streptavidin-lookalike is going into, with a confidentiality clause preventing any further disclosure.

More details from BVXP’s AGM within an upcoming podcast!

Maynard