25 November 2021

By Maynard Paton

Results summary for City of London Investment (CLIG):

- The Karpus merger ensured a record financial performance and a 10% dividend lift, although funds under management (FuM) during H2 (+4%) did not enjoy the buoyant market gains experienced during H1 (+31%).

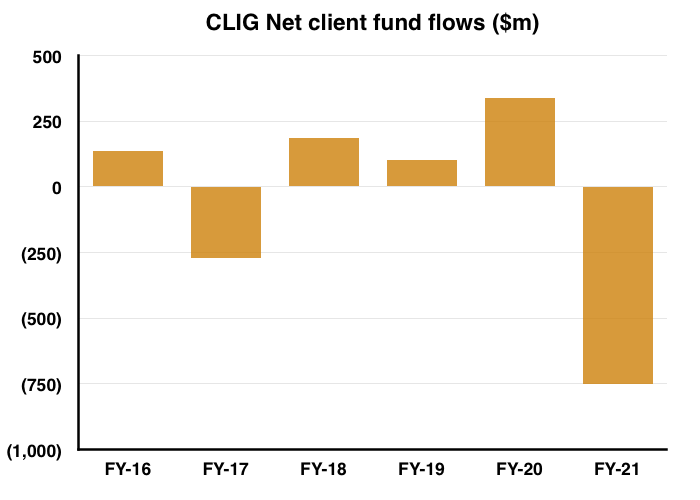

- Further client ‘rebalancing’ led to FuM withdrawals of $752m — almost entirely negating the net client inflows of $758m received during the previous five years.

- The absence of fresh client money and investment gains lagging the MSCI World index — as well as staff using paper payslips and fax machines — could be evidence of a business rather stuck in its ways.

- A startling 49% operating margin, net cash at a hefty £26m plus small demands on cash flow confirm the accounts remain in good shape.

- Although the possible P/E is 10-11 and the yield tops 6%, the shares have been rated modestly for years as major new clients remain very elusive. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own CLIG

- Results summary

- Fee income, profit and dividend

- FuM and net client withdrawals

- Liontrust comparison and capacity constraints

- FuM investment performance

- FuM fee rates

- Management

- Profit share and FuM/exchange-rate table

- Financials

- Valuation

Event links, share data and disclosure

Events: Annual report and results presentation for the twelve months to 30 June 2021 published 13 September 2021 and Q1 2022 trading update published 14 October 2021

Price: 510p

Shares in issue: 50,679,095

Market capitalisation: £258m

Disclosure: Maynard owns shares in City of London Investment. This blog post contains SharePad affiliate links.

Why I own CLIG

- Fund manager that employs a lower-risk strategy of buying investment trusts at wide discounts through a “team approach to investing“.

- Accounts showcase startling 49% margins, hefty net cash and ability to distribute majority of earnings via dividends.

- P/E of 11 and yield of 6% offer meaningful re-rating potential should sizeable new mandates ever bolster funds under management.

Further reading: My CLIG Buy report | All my CLIG posts | CLIG website

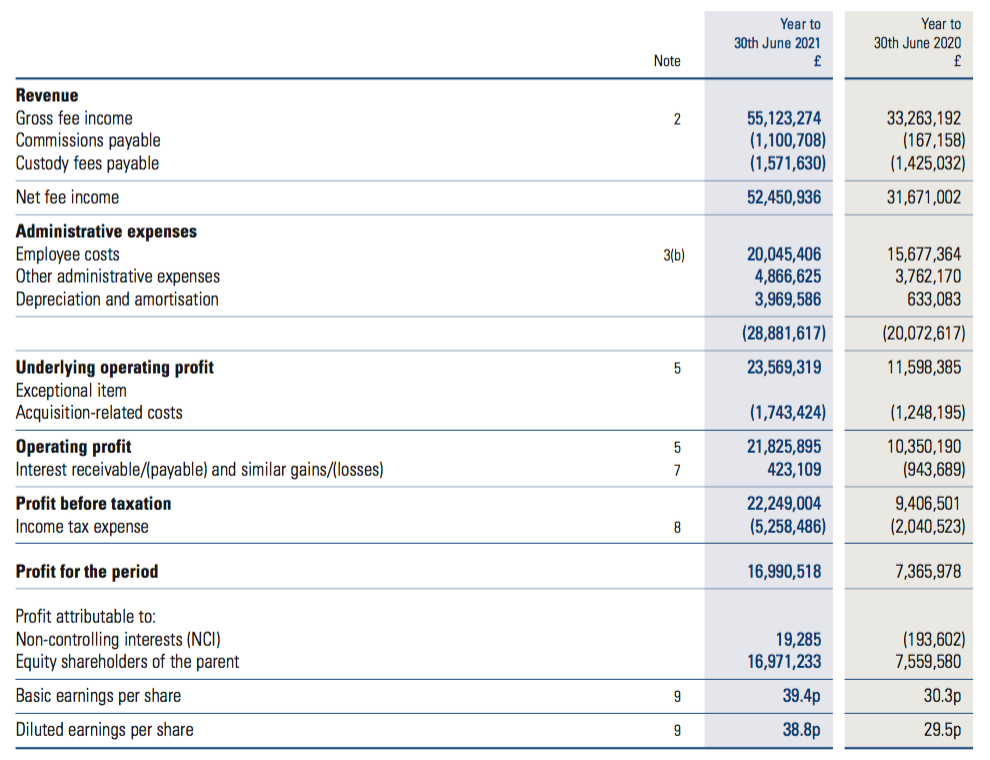

Results summary

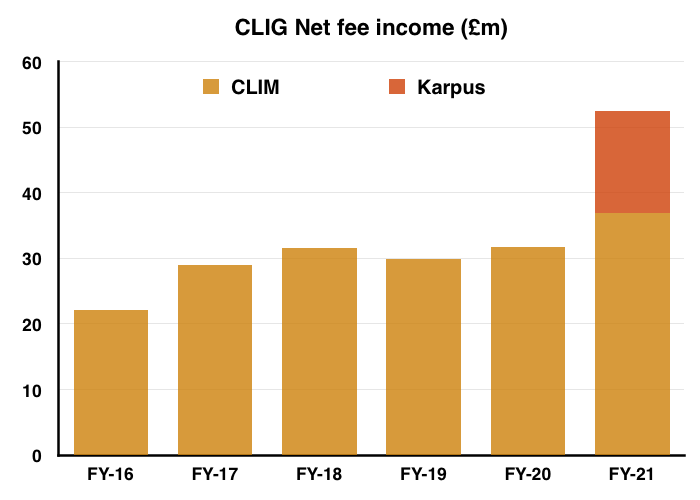

Fee income, profit and dividend

- The £102m merger with Karpus Management during H1 followed by slightly improved funds under management (FuM) for Q3 and Q4…

“At year end, both CLIG operating subsidiaries hit all-time FuM highs following the significant equity market gains of recent months and strong relative performance.”

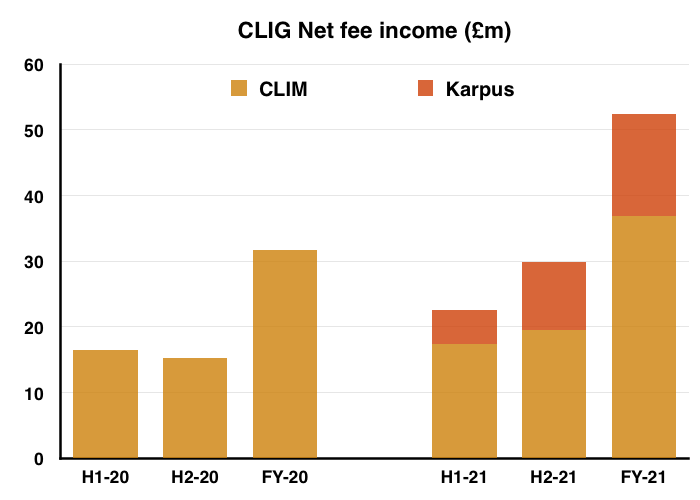

- …had already guaranteed these results would set new full-year records for net fee income and profit.

- Total net fee income increased 66% including Karpus, and 17% for the existing City of London Management (CLIM) division:

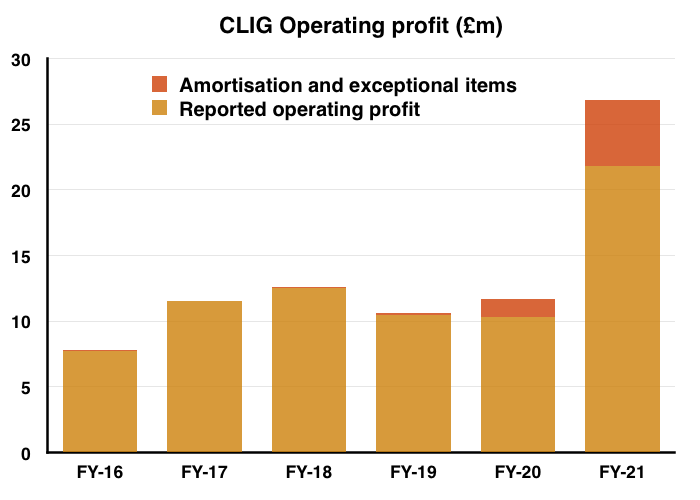

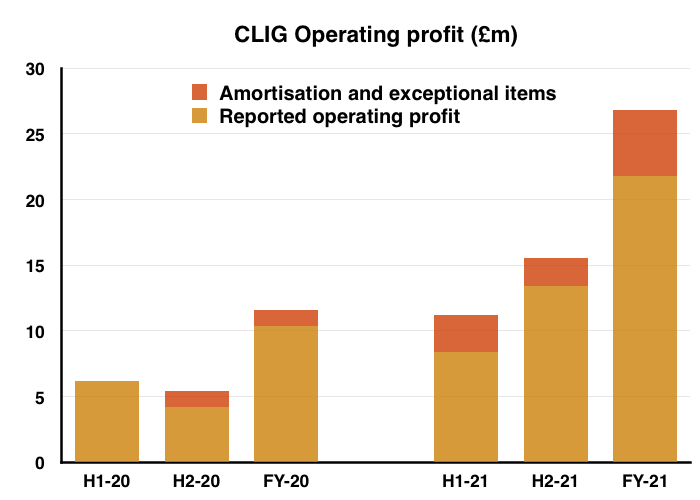

- Charges associated with the Karpus merger influenced reported profit, and consisted of:

- Exceptional merger expenses of £1.7m, all of which were incurred during H1, and;

- The amortisation of the acquired intangibles, which came to £3.3m, of which £2.2m occurred during H2.

- Excluding the Karpus exceptional items and amortisation charges, full-year operating profit surged 130% to £26.8m:

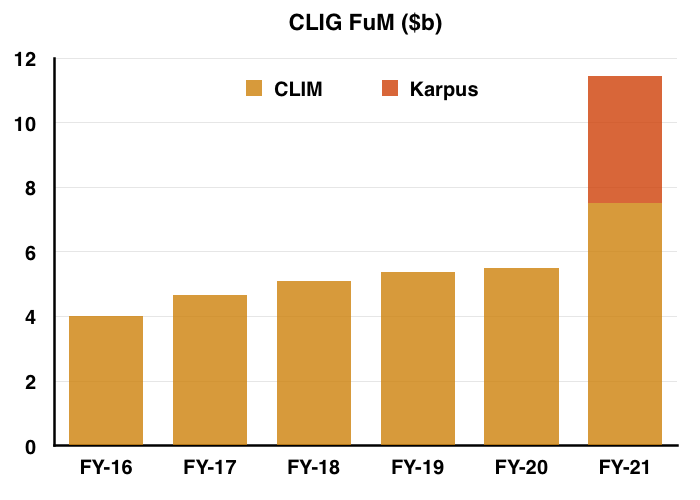

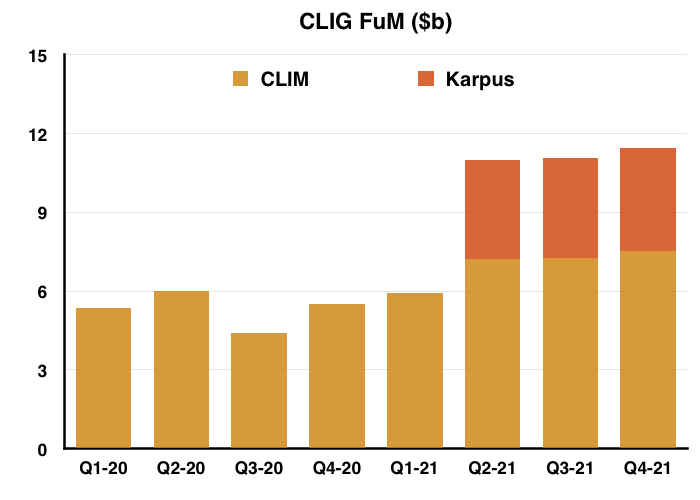

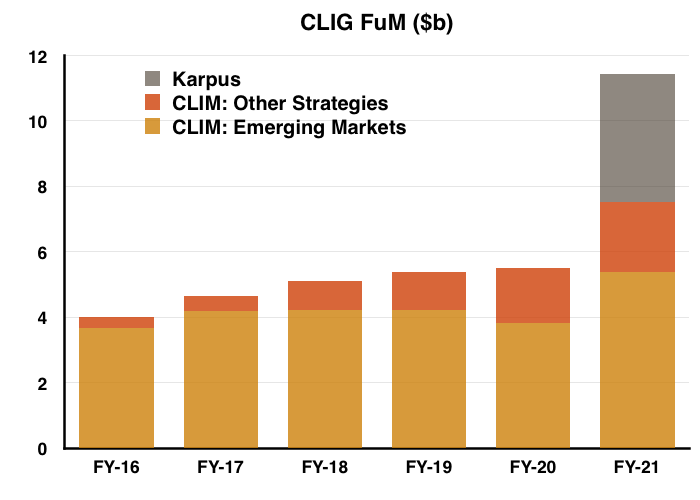

- Total FuM climbed 108% to $11.4b including Karpus, and 37% to $7.5b at the existing CLIM division:

- The FuM improvement at CLIM occurred largely during H1 (+31%), with modest gains for combined CLIM/Karpus FuM experienced during both Q3 (+1%) and Q4 (+4%):

- CLIM’s FuM has now advanced 71% since the pandemic low of Q3 2020.

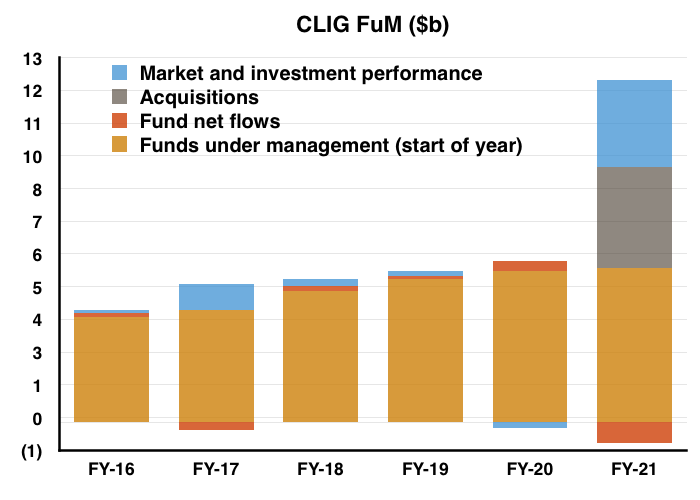

- The additional FuM enjoyed during FY 2021 was generated entirely by wider market movements and investment returns, which offset net fund outflows from clients (see FuM and net client withdrawals).

- A full six-month H2 contribution from Karpus alongside CLIM FuM holding steady during Q3 and Q4 ensured the full-year performance was weighted towards H2:

- CLIG claimed full-year fee growth (+66%) was less than average monthly FuM growth (+82%) because of a weaker USD compared to GBP (1.35 versus 1.26). More than 98% of group fee income is denominated in USD.

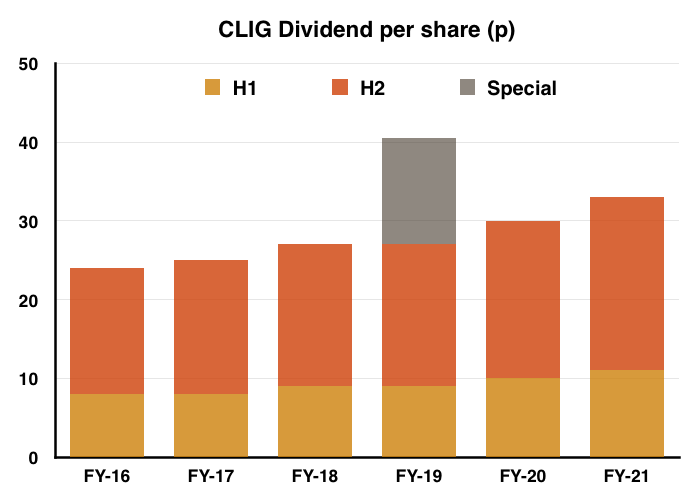

- The final dividend was raised 10% to match the lift applied to the interim payout and reflects a “period of strong appreciation of the underlying asset values managed by the team“:

Enjoy my blog posts through an occasional email newsletter. Click here for details.

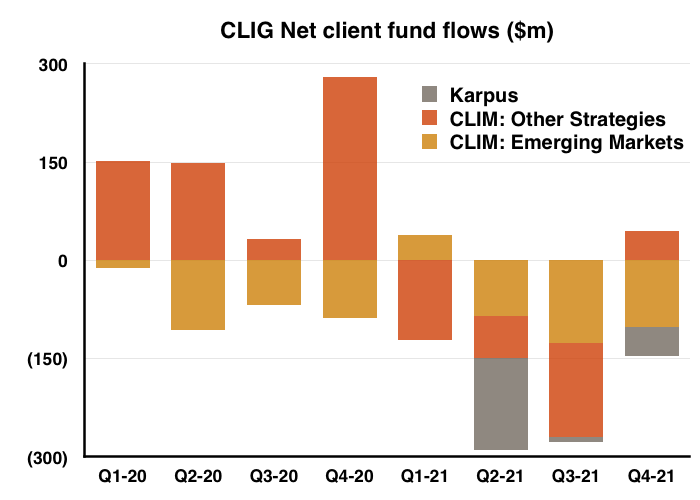

FuM and net client withdrawals

- CLIM’s FuM can be divided into two main categories:

- Emerging Markets (EM), and;

- Other Strategies, which cover developed markets, “opportunistic value“, frontier markets and REITs.

- Both categories apply CLIG’s long-standing ‘value’ approach of buying investment trusts at a discount.

- Karpus meanwhile manages a mix of US equities, including investment trusts, and fixed-income securities:

- Propelling overall FuM higher during FY 2021 were investment returns of $3.1b:

- However, FY 2021 witnessed client net withdrawals of $752m.

- The $752m outflow almost entirely offset the aggregate net client inflows of $758m enjoyed during the previous five years:

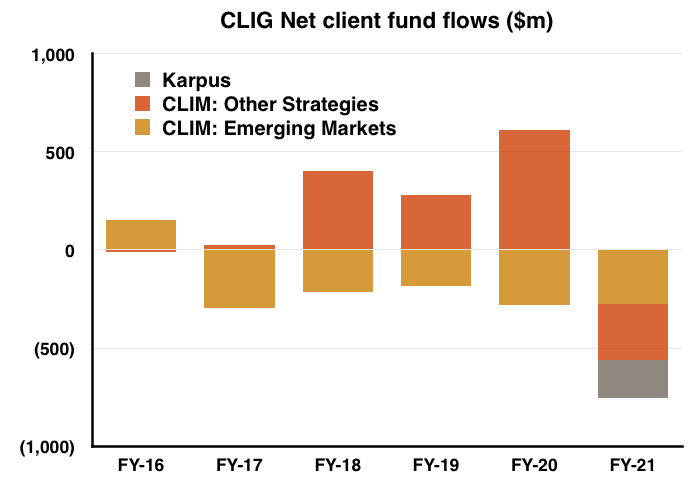

- CLIG gave three reasons for the net client withdrawals for FY 2021:

“(1) the International CEF strategy was closed to new investors for the year to December 2020 following a period of strong growth;

(2) the Opportunistic Value (OV) and Frontier CEF strategies lost two larger clients over the period; and

(3) we experienced disproportionate rebalancing from our institutional clients following a period of significant outperformance.“

- Closing strategies due to “strong growth” and experiencing client “rebalancing” after significant outperformance suggest attracting new client money when times are good may be limited.

- If attracting new client money when times are good is limited, the prospect of attracting new client money when times are bad could be very limited.

- CLIG also blamed restrictions due to Covid-19 for client money leaving:

“A number of factors, mixed with cancelled or postponed client investment committees and a lack of in-person marketing efforts due to the pandemic and resulting quarantine environment, contributed to net outflows. “

- Note that CLIM’s original EM division has now suffered net client outflows during each of the last five years…

- …as well as during seven of the eight quarters of FY 2020 and FY 2021:

- Client money has been leaving Karpus every quarter since the merger, too.

- CLIG claimed such departures at Karpus were due to client ‘rebalancing’ and the closure/distribution of several pension plans.

Liontrust comparison and capacity constraints

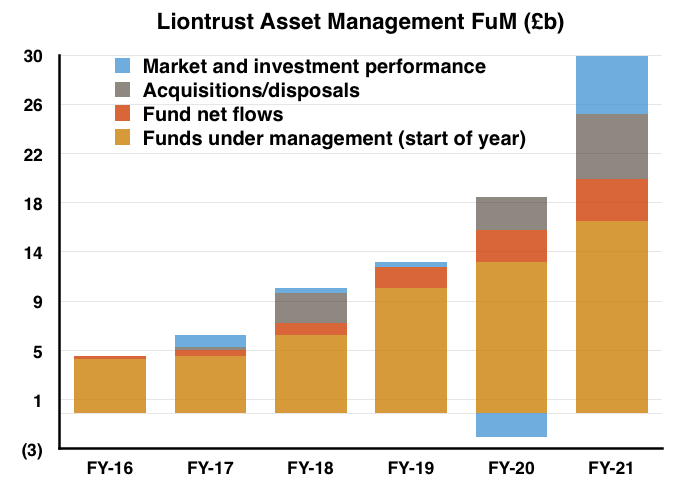

- The lack of net client money arriving at CLIG contrasts with the money pouring into other quoted fund managers.

- Liontrust Asset Management (LIO) is a prime example:

- LIO’s new client money has been consistently positive.

- Between FY 2017 and FY 2021, LIO received net new client money of £9.4b — almost double the £4.8b LIO managed at the start of that period.

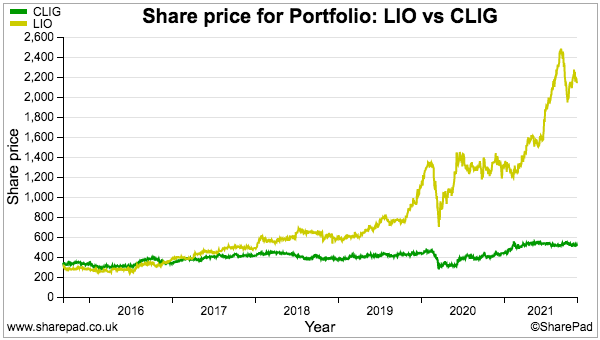

- No wonder LIO’s share price has trounced that of CLIG’s during the same time:

- A fundamental problem for CLIG trying to win new client mandates is a “capacity constraint” within the EM strategy.

- A “capacity constraint” occurs when a strategy finds itself unable to invest significant amounts — and then expect outperformance — because of the limited size of its target universe of stocks.

- CLIG said this time last year the EM strategy had a capacity of $4b, although management explained during the subsequent H1 webinar that the capacity level moves in tandem with the market and therefore presently exceeds $5b.

- Year-end EM FuM at $5.4b represented 47% of year-end group FuM. That 47% proportion is unlikely to attract notable new client money, which has implications for overall group FuM growth.

- CLIG acknowledged meaningful FuM expansion rested upon CLIM’s other strategies:

“International, OV [Opportunistic Value] and the REIT strategies remain a focus for growth in the medium term.“

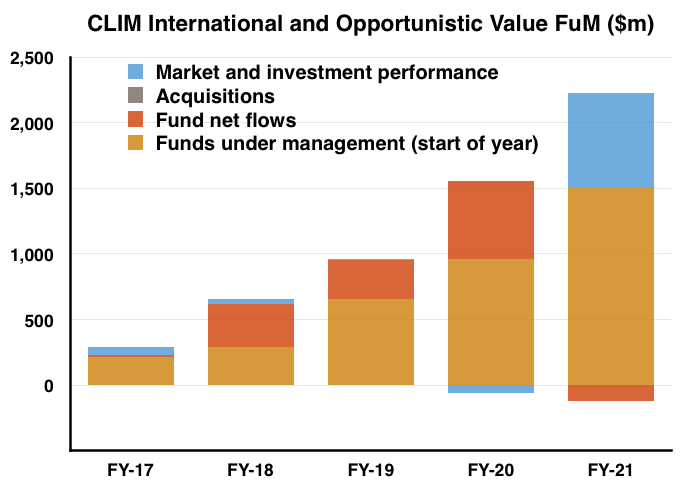

- International and OV enjoyed good FYs 2018, 2019 and 2020 for attracting new client money…

- …but suffered a large client departure during FY 2021:

“The OV strategy lost its largest client after the institution outsourced management. We are redoubling our efforts to replace these assets. Our International strategy is open again to new investors and CLIM’s REIT strategies will have the three-year track record necessary for institutional interest in January 2022.”

- At least the International fund has re-opened for new business.

- International and OV represented $2.1b or 18% of year-end group FuM.

- The REIT operation remains tiny with FuM at just $13m.

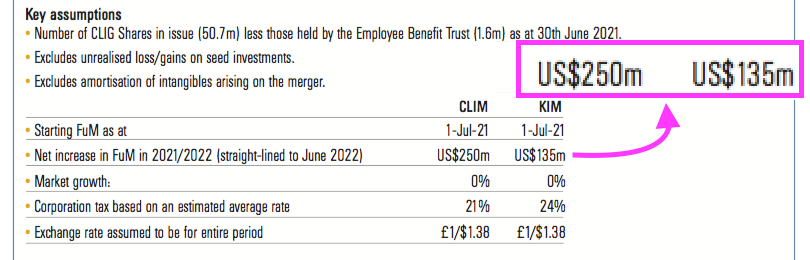

- CLIG still reckons new client money of $385m can be obtained by June 2022:

- An extra $385m is equivalent to only 3.4% of year-end FuM of $11.4b.

- If the extra net $250m expected for CLIM was invested entirely within International and OV, their year-end FuM of $2.1b would be improved by a welcome 12%.

- An extra net $250m for International and OV is not unprecedented.

- Although International and OV suffered net client withdrawals of $117m during FY 2021, the two strategies enjoyed combined net client deposits of $333m, $301m and $597m during FYs 2018, 2019 and 2020 respectively,

- The extra net new client money of $135m expected for Karpus does not cover the net $191m withdrawn from Karpus since the merger.

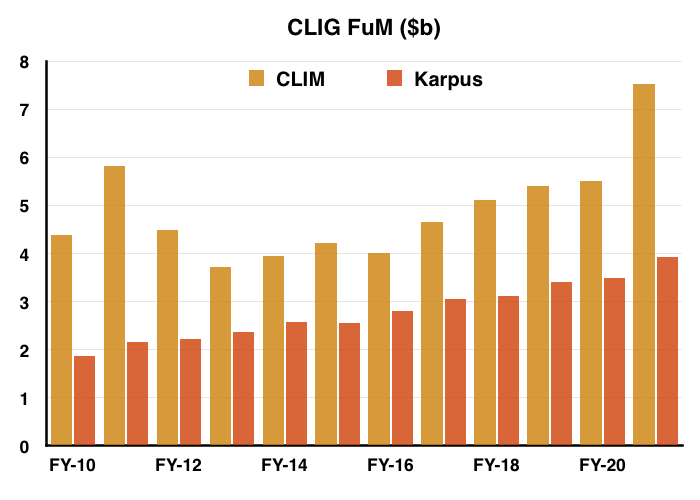

- For a longer-term perspective, total FuM at CLIM and Karpus has grown from $6.2b to $11.4b since 2010 — equivalent to an average annual growth rate of 5.7%:

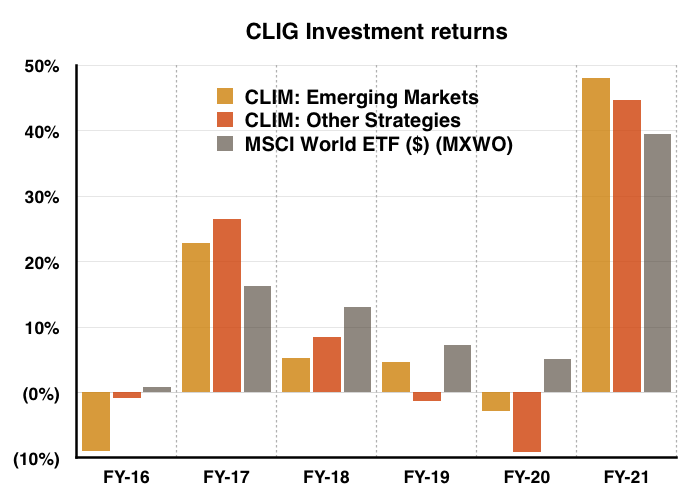

FuM investment performance

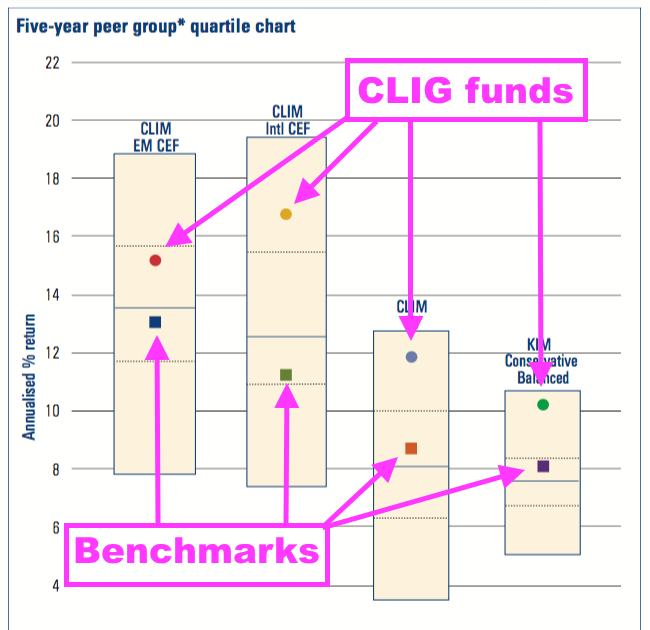

- The high levels of outgoing client money feel peculiar given CLIG’s claimed investment performance.

- The 2021 annual report includes charts such as these…

- …that display five-year outperformance against various benchmarks.

- CLIG claimed:

“Over 90% of the underlying strategies managed by CLIM and KIM are ahead of benchmark and peer group averages over five years.”

- The obvious question then: why aren’t more clients attracted to CLIG’s funds given the outperformance?

- True, the EM approach has capacity issues. True, some clients wish to ‘rebalance’ their portfolios. And true, some smaller CLIM strategies have failed and clients have left.

- But perhaps the over-riding problem is CLIM’s funds have under-performed the wider global market.

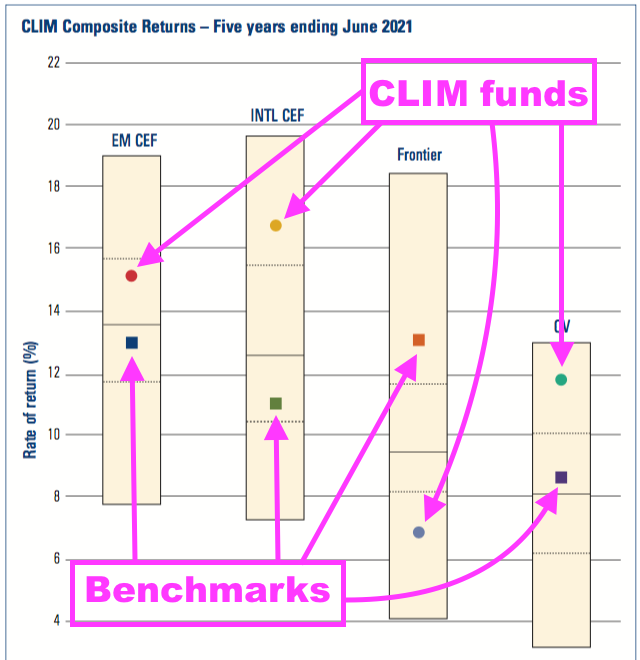

- CLIG said:

“Equities (MSCI World) delivered an annualised rate of return of 16% over the five years ending June 2021, almost double the average five-year return over the past 30 years.“

- Perhaps prospective clients have compared the performance of CLIM’s funds to the performance of the MSCI World rather than CLIM’s own benchmarks.

- The Invesco MSCI World ETF (MXWO) has gained 102% during the last five years (in USD), versus a 95% investment return for CLIM’s EM approach and 78% for CLIM’s other strategies:

- CLIG seems hopeful that its ‘value’ investing style may outperform the MSCI World during the next five years:

“With the trailing P/E of the global index approaching 25x, expectations for the next five-year period should be moderated.“

- With the MSCI World’s largest holdings including tech higher flyers Apple, Microsoft and Amazon, the global index has made many investors (including me!) look like fools during the last five years.

- Lower returns from the MSCI World do not of course mean CLIG’s investing returns will then outperform.

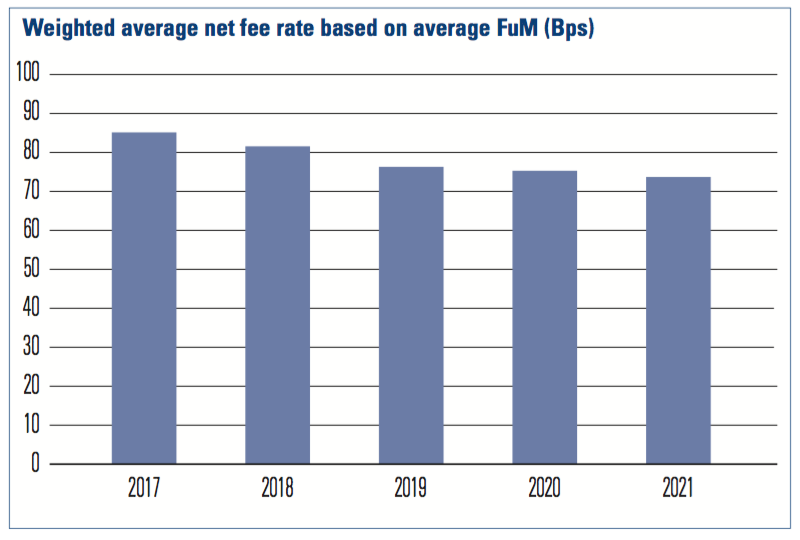

FuM fee rates

- The fee rate CLIM collects as a proportion of FuM continues to decline, this time by one basis point to 74 basis points:

- Note that the 74 basis points now includes Karpus, which enjoys higher fees than CLIM.

- The 74 basis points for the enlarged group implies CLIM’s fees have declined further from the 75 basis points reported for FY 2020.

- To recap:

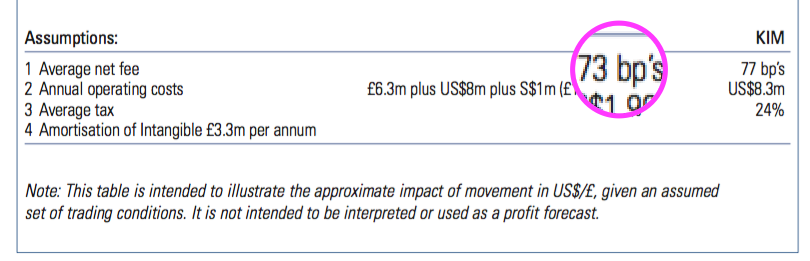

- The 2021 annual report included a revised FuM/exchange-rate table that indicated CLIM’s fee rate was now 73 basis points:

- CLIG claims the fee-rate decline since 2016 (then 86 basis points) has been due to the group’s greater proportion of Other Strategy funds, which levy lower charges.

- CLIG has never disclosed the exact fee rates charged on its EM and Other Strategy funds.

- My past algebra has indicated EM fees are applied at 90 basis points and Other Strategy fees are applied at 30 basis points to arrive somewhere close to the overall fee rates CLIG has declared:

- CLIG really ought to disclose the different fees charged by its strategies in order to remove any suspicion of clients chipping away at fees throughout all of its funds.

- The fee rate at Karpus has dropped, too.

- The merger document (point 5) claimed Karpus enjoyed a “fairly stable” rate of 80 basis points.

- The Q2 and Q3 statements said Karpus fees were 77 basis points, and following these results the Q1 2022 update admitted Karpus fees had been trimmed to 76 basis points (see Valuation).

- The declining fee trend is not encouraging and may well reflect existing clients mulling the 20 basis points charged for holding an MSCI World ETF.

Quality UK investment discussion at Quidisq. Visit forum.

Management

- This time last year I expressed a reluctance to buy more CLIG shares due to management changes:

“With the founders/ex-chief execs of both CLIG and Karpus no longer in charge, I have become reluctant to add to my CLIG holding. I simply prefer owner-orientated executives — rather than professional ‘salarymen’ — to lead my investments.”

- But I did add:

“Of course, the ‘salaryman’ now in charge of the combined business may well find new clients without adjusting the workplace culture or embarking on an acquisition spree.”

- I now wonder whether CLIG does in fact require fresh boardroom thinking.

- After all:

- Client fees seem on a downward trend;

- Attracting significant net new client money appears difficult, and;

- CLIM’s funds have struggled to match the MSCI World index.

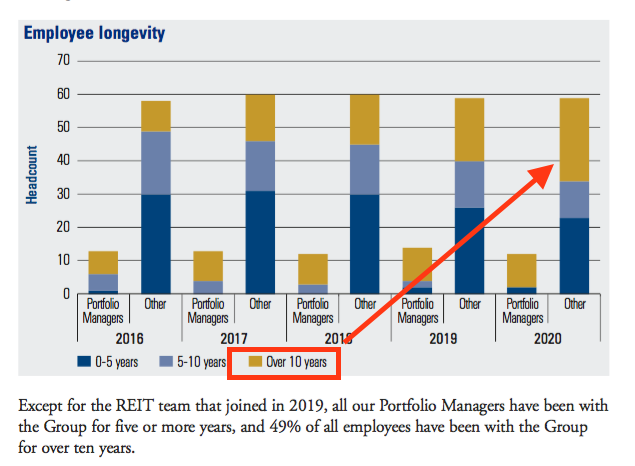

- I also wonder whether the workplace culture created by CLIG founder Barry Olliff has become a little too comfortable.

- Before the Karpus merger, 49% of all employees had served at CLIG for more than ten years…

- …and the 49% may quite like investing in the same old way for the same old customers.

- The 2021 annual report admitting the cessation of paper payslips and the ongoing use of fax machines…

- …feels like evidence of a business rather stuck in its ways.

- A boardroom of eleven directors, which CLIG says is “arguably… excessive“, does not seem ideal for decisive decision making and could explain why the business has been less dynamic than the likes of LIO.

- The founder of Karpus, George Karpus, retired to become a CLIG non-exec on the day of the merger but still retains a 36%/£95m CLIG shareholding.

- Mr Karpus may find selling down his shareholding more difficult than CLIG founder Barry Olliff, who (very commendably) first mentioned a desire to reduce his then £15m/20% stake in the 2008 annual report.

- The latest annual report showed Mr Olliff with a £6m/2% stake.

- In retrospect, perhaps Mr Olliff disposing of his shares during the ten years leading up to his 2019 retirement was a sign CLIG would not be going all out for growth.

- Whether Mr Karpus will be able to influence executive proceedings is hard to say.

- At least the Karpus chief investment officer is a CLIG executive, who may bring a different operational perspective to the three board executives from CLIM.

- I suspect any meaningful development of the CLIM business may well rest upon Mr Karpus and whether he wishes the value of his £95m shareholding to advance (or not).

- The annual report implies the Karpus merger tripled the number of group business development/marketing employees:

- Additional business development/marketing employees are a good first step to winning more client mandates.

- CLIG’s four-person business development/marketing team looked very inadequate before the Karpus merger.

- CLIG’s commentary on marketing was limited to the following and, save for the new Karpus sentence, was identical to last year:

“Marketing efforts will continue to be targeted at investment consultants, foundations, endowments and pension funds. An institutional marketing resource was hired to introduce [Karpus] investment strategies to US registered investment advisers. We will also continue to introduce our capabilities to family offices, outsourced CIO firms, and alternative consultants. “

- Before the merger, Karpus FuM per employee was 27% greater and Karpus revenue per employee was 31% greater than the respective levels at CLIM (point 9)

- Perhaps Mr Karpus can somehow encourage CLIM’s employees to be as productive as those working at Karpus.

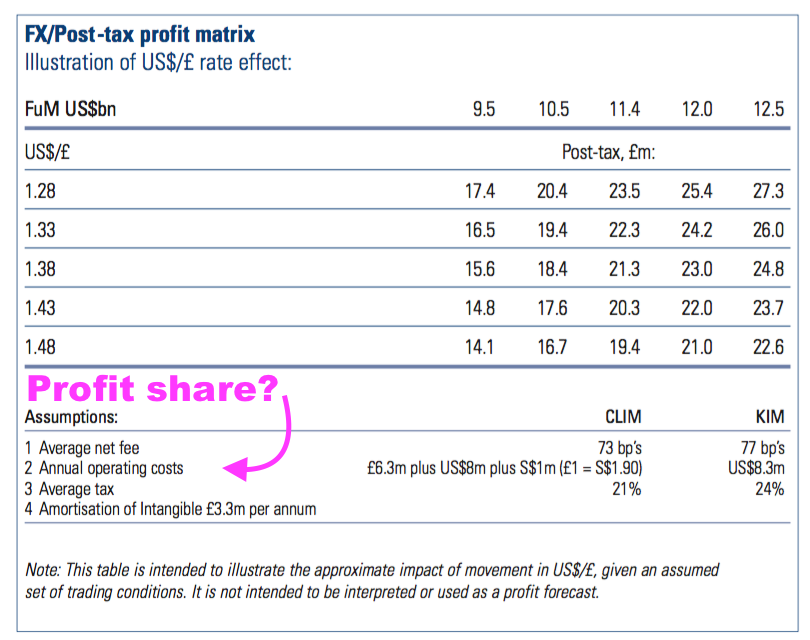

Profit share and FuM/exchange-rate table

- These FY 2021 figures appeared to clarify the profit-share arrangements with Karpus.

- CLIG staff have for years shared up to 30% of pre-profit-share profit as a bonus.

- But whether Karpus employees would participate in this 30% bonus pool was never made clear within the FY 2020 statement or the subsequent H1 results.

- The latest annual report showed profit share of £7.9m versus pre-profit-share profit of £35.6m…

- …which is equivalent to a 22% group profit share and compares to 33% for FY 2020 (I believe the 33% charge exceeds the 30% bonus-pool limit because of National Insurance payments).

- Profit share during H2 represented 21% of pre-profit-share profit.

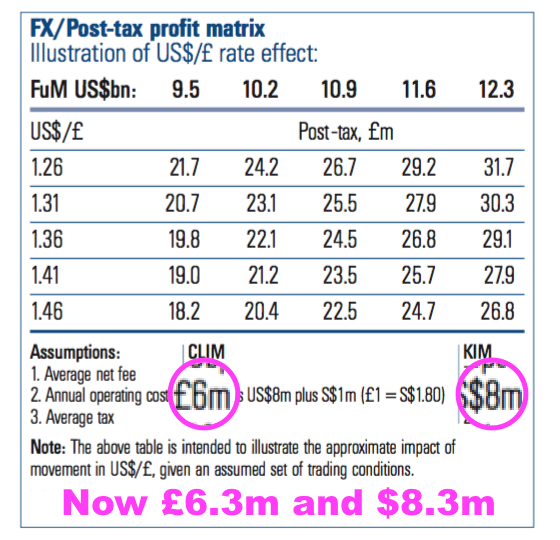

- Note the FuM/exchange-rate table within the 2020 annual report mentioned the 30% profit share:

- But theFuM/exchange-rate table within the 2021 annual report does not:

- Note, too, that CLIM operating costs have increased by £0.3m to £6.3m and Karpus operating costs have increased by $0.3m to $6.3m since the H1 presentation:

- Operating a percentage-based profit-share scheme might also explain why CLIG’s underlying FuM growth has been modest. Employees do not have to win new clients because they still collect a bonus even if earnings go nowhere.

- The Employee Incentive Plan (EIP) that was devised during FY 2016 incurred an additional £1m cost for this FY 2021.

- The EIP cost for FY 2022 ought to be covered by the profit-share scheme. Last year CLIG said:

“The EIP allows employees to forego a proportion of their cash bonuses to participate in share awards, with matching employer contributions, and this year will be the last in which these additional EIP charges will be incurred.”

- But this year CLIG mentioned only Karpus employees had joined the plan and nothing about whether the additional EIP charge had ceased:

“I am pleased to report that the Employee Incentive Plan (EIP) continues to attract wide support from employees across the Group, this being the first year in which KIM employees were invited to participate.“

- The next H1 results should reveal whether the EIP will in fact be covered by the 30% profit share.

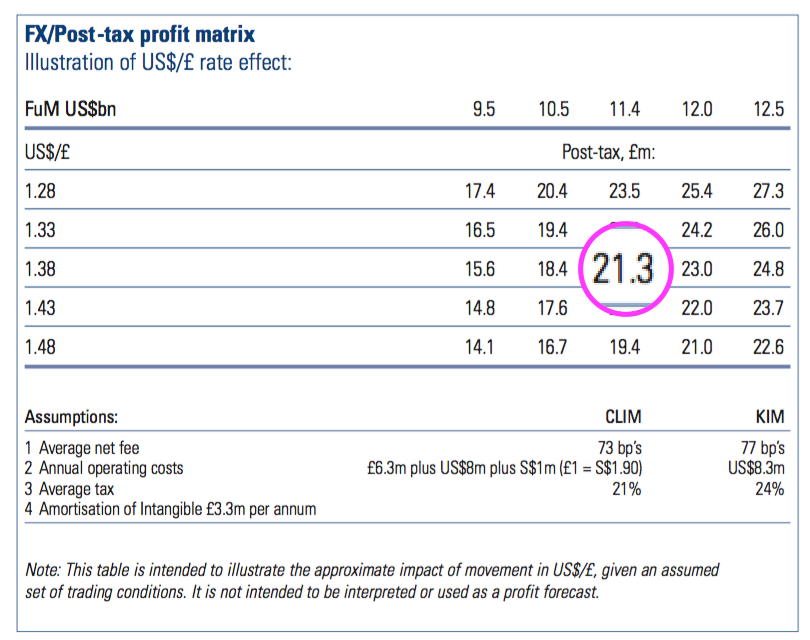

- The FuM/exchange-rate table within the 2021 annual report does not seem to add up.

- Assuming:

- A 30% bonus pool for CLIM;

- GBP:USD of 1.38, and;

- FuM of $11.4b split as per the year-end…

- …my sums indicate a post-tax profit of £27m.

- But the table gives a post-tax profit of £21m.

- CLIG has always said the table is “not intended to be interpreted or used as a profit forecast.“

- But I now believe the table applies assumptions no longer declared underneath and its usefulness to shareholders has therefore diminished.

Financials

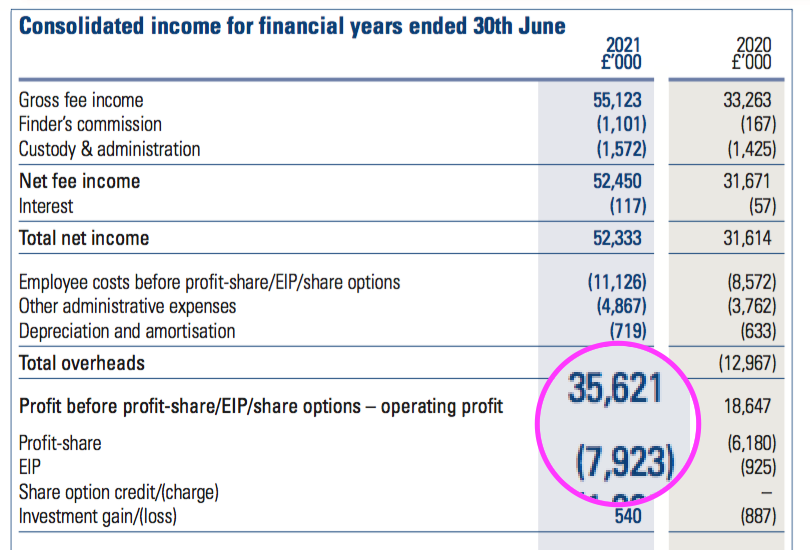

- By far the most impressive feature of these FY 2021 figures was the operating margin.

- Excluding the exceptional items and amortisation charges associated with the Karpus merger, CLIG converted gross fee income of £55.1m into operating profit of £26.8m — a startling 49% margin.

- The margin for H2 on the same basis was 50% (£15.6m/£31.4m).

| Year to 30 June | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating margin* (%) | 36.8 | 36.9 | 32.9 | 34.9 | 48.7 |

| Return on average equity (%) | 58.9 | 50.9 | 43.6 | 40.0 | 24.4 |

(*before exceptional items and amortisation of acquired intangibles)

- The startling margin is supported by Karpus. The accounting small-print said the division delivered post-merger earnings of £7.6m from net fee income of £15.5m — an after-tax margin of 49%.

- Post-merger Karpus earnings of £7.6m equate to £10.1m annualised, or 10% of the £102m value of the shares issued to fund the merger.

- The acquired goodwill and intangibles yielding a 10% return meant CLIG’s return on average equity reduced for the year to 24%.

- CLIG’s return on equity ratio is rather academic, as earnings growth is driven inherently by attracting greater FuM — which in turn is not directly correlated to reinvesting profit into tangible items such as computers and office furniture.

- The largest balance-sheet item after the Karpus intangibles is cash at a hefty £26m. The books remain free of conventional bank debt.

- Cash during the year improved by £11m. Operating cash flow of £29.0m funded tax of £6.4m, dividends of £9.7m and £2.5m spent on shares for the Employee Benefit Trust (EBT).

- The EBT expense was offset by raising £831k from selling shares to staff to satisfy their exercised options.

- Between FYs 2017 and 2021, the EBT spent £7.0m buying shares and received £3.5m from selling shares. During the same time the £3.5m difference has been almost entirely covered by the aggregate EIP charge of £2.9m.

- Working-capital movements and capital expenditure remain small versus operating profit:

| Year to 30 June | 2017 | 2018 | 2019 | 2020 | 2021 |

| Operating profit* (£k) | 11,509 | 12,528 | 10,504 | 11,598 | 26,820 |

| Depreciation and amortisation (£k) | 231 | 295 | 306 | 292 | 227 |

| Net capital expenditure (£k) | (485) | (137) | (421) | (79) | (93) |

| Working-capital movement (£k) | (533) | 1,423 | 894 | 69 | 2,361 |

| Net cash and investments (£k) | 15,022 | 19,937 | 18,232 | 18,419 | 29,699 |

(*before exceptional items and amortisation of acquired intangibles)

- CLIG’s accounts remain free of defined-benefit pension obligations.

Reader offer: Claim one month of free SharePad data. Learn more. #ad

Valuation

- The Q1 2022 update published last month was not spectacular:

- Clients withdrew a net $172m to mark the fifth consecutive quarter of net FuM outflows.

- FuM declining $531m including withdrawals of $172m implies a $359m negative investment movement.

- Down $359m on $11.4b is a 3.1% drop for the quarter. The MSCI World ETF by contrast gained 0.9%.

- FuM at $10.9b is now at its lowest level since the Karpus merger completed this time last year, when FuM was $9.5b.

- Assuming FuM can remain around the $11b level, doubling up the H2 performance should provide a reasonable profit guess for FY 2022.

- Underlying H2 earnings were £11.9m, which gives £23.8m or approximately 47p per share for twelve months.

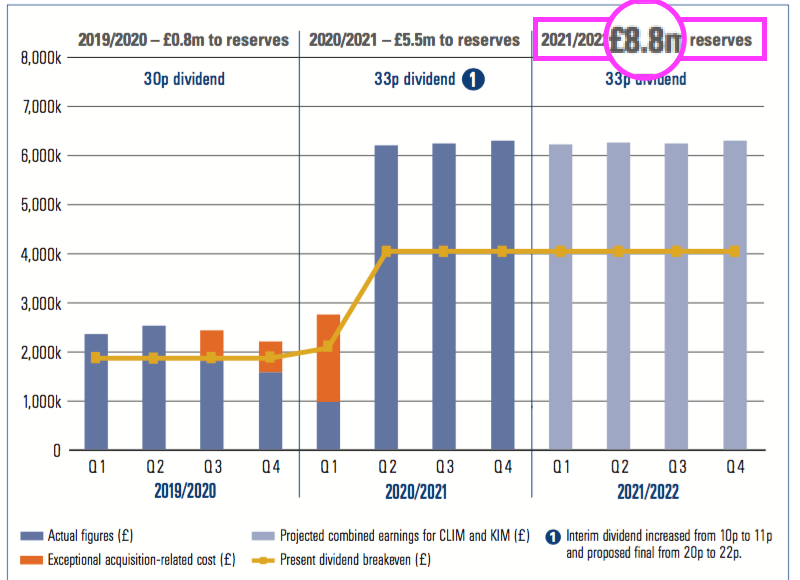

- CLIG’s dividend-cover chart continues to predict earnings of £8.8m will be retained for FY 2022…

- …as FuM increases by the aforementioned $385m:

- £8.8m is equivalent to 17p per share and, when added to the 33p per share dividend, implies earnings of 50p per share for FY 2022.

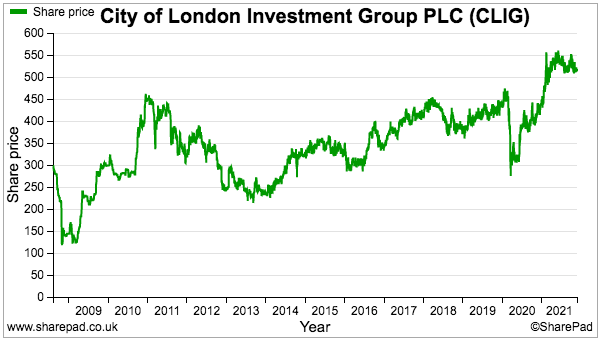

- The earnings guesswork could be fine-tuned further for the cash position, the Q1 2022 update and any further costs/benefits arising from the Karpus merger, but the 10-11x rating at 510p is already very ordinary.

- The 33p per share trailing dividend supports a 6.5% income.

- CLIG’s dividend-cover policy continues to be 1.2x over rolling five-year periods. But dividend cover based on underlying FY 2021 earnings was 1.45x (33p/48p) .

- CLIG noted dividend cover on reported earnings for the last five years was 1.29x, and “having regard to the buoyancy of markets over the last year” believed that a “modest degree of headroom above the target level [was] prudent.”

- Applying the five-year 1.29x dividend cover to projected earnings of 47p per share leads to a FY 2022 payout of 36p per share and a potential 7.1% income.

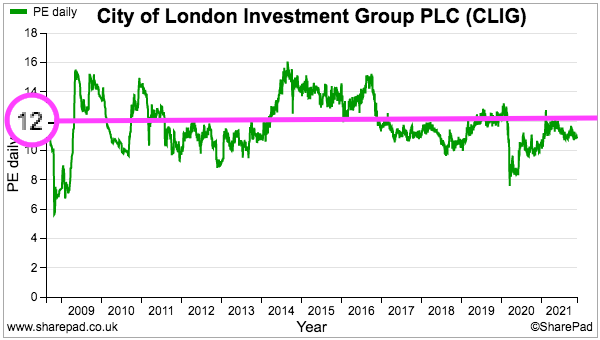

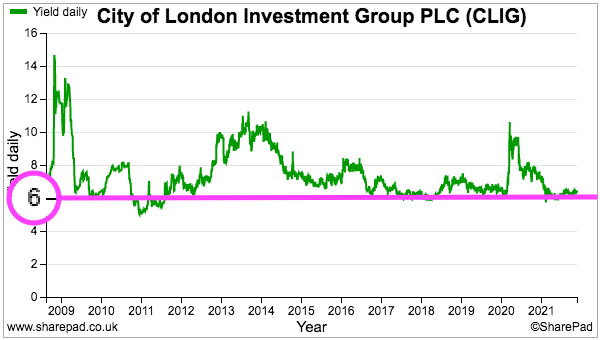

- CLIG’s rating does not look expensive, but the trailing P/E has frequently been less than 12 and trailing yield has almost always offered more than 6%:

- I remain convinced the shares will continue to trade on a modest rating until CLIG attracts a much greater rate of new client money.

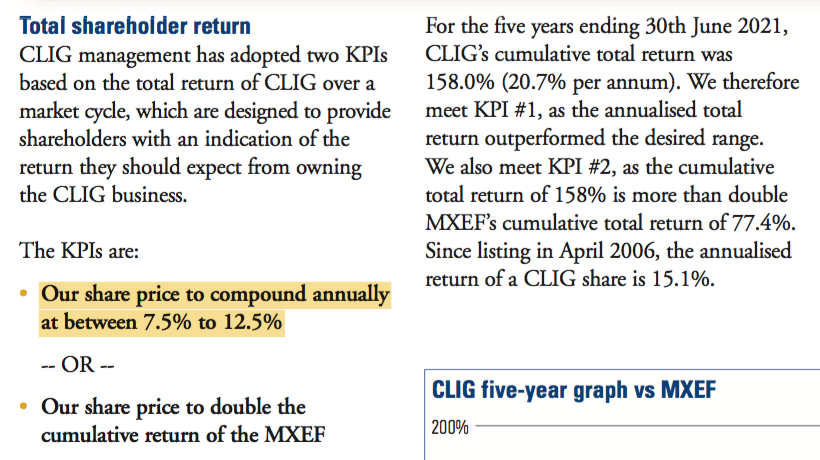

- Additional perspective on future returns is provided by a KPI.

- CLIG continues to be one of the very few quoted companies with a public share-price ambition:

- Over rolling five-year periods CLIG aims to deliver a total-return CAGR for shareholders of between 7.5% and 12.5%.

- A starting dividend yield of 6.5% means the share price may only have to grow at 1-2% a year to meet the KPI ambition.

- The share-price KPI ambition is very commendable but not a great endorsement of multi-bagger gains ahead.

- The share-price KPI was introduced within the results for FY 2019, the year-end share price for which was 406p.

- A five-year CAGR of the minimum 7.5% KPI requires a 177p per share return from that 406p by 30 June 2024.

- The share price has since improved 104p to 510p while dividends have come to 59p per share. Just another 14p is therefore required by 30 June 2024 to meet the 177p per share five-year KPI.

- The share-price KPI is now CLIG’s only KPI after these results confirmed a confusing goal relating to an emerging-market benchmark (point 8) had been scrapped.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Very good analysis. Thank you for sharing.

It’s worth reflecting that you can get similar-ish yields, and high single digit revenue growth, at similar price earnings from L and G – a far more resilient business. If life insurance is not your thing but you like lowish growth businesses with a generous payout (or an inability to reinvest profitably – depending on whether you are glass half full or half empty by inclination) then Direct Line.

Hi Ted

Thanks for the comment and alternative yield suggestions. I recognise LGEN and DL could be very useful members within a broad income portfolio. But insurance accounting is not straightforward and I prefer shares without such complexity. CLIG may not be resilient to the market’s ups and downs impacting its FuM, but the accounts are very simple!

Maynard

Interesting and thought provoking read. Many thanks.

Thanks Paul!

I have posted an answer to a question on a discussion board, which I will repeat here:

———–

Q: I’d be interested to know whether you anticipate George Karpus seeking to sell down his holding going forward – which I agree would not be so easy to do as was the case with Barry Olliff over a period of circa 12 years – or do you think that he may look to exit via some future M & A activity?

A: Not sure whether George Karpus (GK) will sell down or exit via M&A. At some stage he will want to exit I guess. For perspective GK has just turned 76 while Barry O turns 77 this December. GK was in attendance at the AGM, but a clash of results meant I could not attend and those that did (as reported on the ShareSoc members’ website) did not ask what his plans were. Argh! GK’s lock-up I think was 12 months, so he can start selling from now on.

———–

Also found this background on GK: https://karpusfamilyfoundation.org/#letter

I come from a rather humble background. My father was a sixth grade educated Pennsylvania coal miner who suffered a crushed pelvis in the mines and then worked in a sheltered work shop in Binghamton, NY later in life. My mother worked in a factory putting jackets on books. Together, they never made $20,000 in any year. My father taught me work ethic and to never quit. My mother taught me how to save and manage a budget.

Maynard

City of London Investment (CLIG)

Q2 FuM Update, Dividend & Special Dividend published 19 January 2022

A small inflow of net new client money plus a special dividend counterbalance lower company predictions of retained earnings.

Here is the full text interspersed with my comments:

——————————————————————————————————————

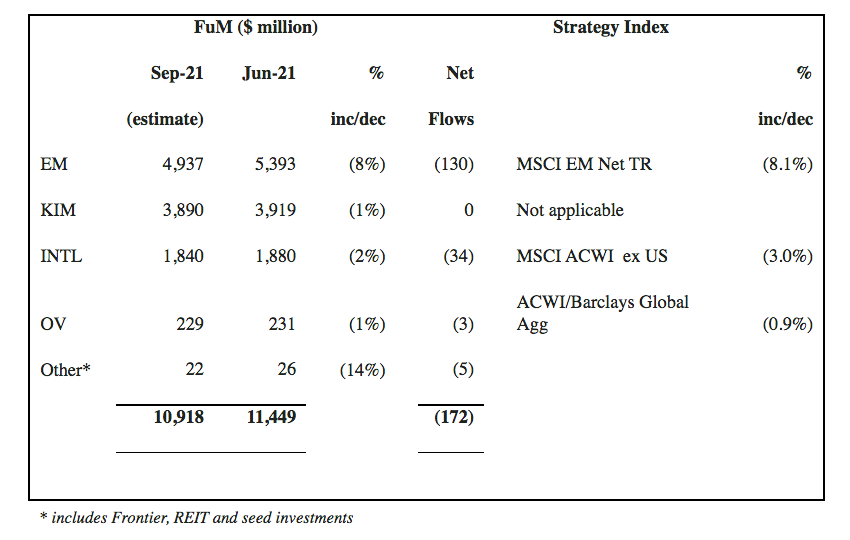

City of London (LSE: CLIG), a leading specialist asset management group offering a range of institutional and retail products investing primarily in closed-end funds, announces that on a consolidated basis, as at 31 December 2021, FuM were US$11.1 billion (£8.2 billion). This compares with US$11.4 billion (£8.3 billion) at the Group’s year end on 30 June 2021. A breakdown by strategy follows:

IM Performance

Solid relative performance across CLIG’s investment strategies resulted from good NAV performance at the underlying closed end funds and positive discount effects.

Over the period, there were net inflows of circa US$59 million across the Group’s strategies, due to asset raising for the International Equity strategy. Year-end rebalancing and tax planning led to outflows from the EM and KIM strategies.

Business development will focus on EM, International, and Opportunistic Value strategies, and KIM balanced mandates, where additional capacity is now available for prospects.

——————————————————————————————————————

At last, a quarter with a monthly inflow of new client money — albeit just $59m. CLIG’s previous five quarters had each experienced an outflow. But EM clients have now made net withdrawals during 14 of the last 16 quarters, and the EM FuM outflow during this H1 (at $279m) now tops that for FY 2021 ($275m) and FY 2020 (also $275m).

Still, the International approach attracted inflows of $265m and its FuM is now at its highest ever level at $2,147m. The International, OV and Other strategies combined currently represent 33% of group FuM — a new high for this trio.

The overall investment return for total FuM was 1.2% during Q2 and -1.6% for H1.

Interesting that “Business development will focus on EM” — I had thought EM had been sidelined for marketing purposes due to capacity constraints, but maybe no longer.

——————————————————————————————————————

Operations

The Group’s income currently accrues at a weighted average rate of approximately 72 basis points of CLIM’s FuM and at approximately 76 basis points of KIM’s FuM, net of third party commissions. “Fixed” costs are c. 1.6 million per month, and accordingly the current run-rate for operating profit, before profit-share is approximately 3.3 million per month based upon current FuM and a US$/£ exchange rate of US$1.3532 to 1 as at 31 December 2021.

The Group estimates the unaudited profit before amortisation and taxation for the six months ended 31 December 2021 to be approximately £15.5 million (2020: £9.9 million).

Inclusive of our regulatory and statutory capital requirements, cash in the bank stood at £24.5 million at the end of the calendar year (£25.5 million as at 30 June 2021), in addition to the seed investments of £6.1 million. Our cash reserves will allow us to continue managing the business conservatively through volatile markets while following our dividend policy for our shareholders.

The Company is currently in a close period which will end with the publication of results for the six months ended 31 December 2021 on 18 February 2022.

——————————————————————————————————————

CLIM FuM fees have been sliced lower, from 73 basis points at Q1 (see blog post above) to 72. No doubt this is due to a greater proportion of International FuM, which levies lower charges than the EM FuM. Karpus fees have held steady. Profit run-rate has not changed from Q1.

Pre-tax profit of £15.5m doubled and taxed at 22% (quick guess) gives annualised earnings of approximately £24m or 48p per share — in line with my calculations within the blog post above.

——————————————————————————————————————

Dividend

The Board declares an interim dividend of 11p per share, which will be paid on 25 March 2022 to shareholders registered at the close of business on 25 February 2022 (2021: 11 pence).

In addition, the Board announces a special dividend of 13.5p per share, which will also be paid on 25 March 2022 to shareholders registered at the close of business on 25 February 2022 (2021: Nil).

Shareholders may choose to reinvest their dividends using the company’s Dividend Reinvestment Plan, to do this please visit http://www.signalshares.com or if you hold your shares through a broker please contact them. The deadline to lodge your election is 4 March 2022.

Dividend cover template

Please see dividend cover template here: https://www.clig.com/dividend-cover.php

The dividend cover template shows the quarterly estimated cost of dividend against actual post-tax profits for last year, the current six months and the assumed post-tax profit for the remainder of the current year and the next financial year based upon specified assumptions.

——————————————————————————————————————

Happy with the special dividend. But the dividend template contains revisions from the template provided at the preceding full-year stage,

Retained earnings for 2021/22 are now projected to be £7.7m versus £8.8m before. The 13.5p per share special dividend will cost c£6.6m and appears not to be included in the £7.7m calculation. £7.7m is equivalent to c15p per share and when added to the ordinary 33p per share dividend gives the 48p per share earnings estimate I mentioned above.

The 2022/23 retained-earnings projection of £8.2m is new and is not affected by any special dividend. This £8.2m is lower than the £8.8m previously predicted for 2021/22. Retained earnings of £8.2m are equivalent to c16p per share, so with the 33p per share dividend implies earnings of 49p per share for FY 2023.

The template assumptions expect FuM to increase by $385m during FY 2023, as they still do for FY 2022. FuM so far for FY 2022 is down $299m.

Maynard

City of London Investment (CLIG)

Publication of 2021 annual report

Here are the points of interest:

1) RISK MANAGEMENT

No changes here. ‘Principal Risks’ remain:

* Key person risk

* Technology, IT/ cybersecurity and business continuity risks

* Material error/ mandate breach

* Regulatory and legal risk

* COVID-19

2) CORPORATE AND SOCIAL RESPONSIBILITY REPORT

Various bits of new text.

a) Workplace

New staff policies:

In December 2020, CLIG implemented the following two policies across the Group:

* Anti-Harassment policy and Compliant Procedure.

* Diversity, Equity and Inclusion policy.

Our goal was to provide greater clarity and guidance on the expectations of employees and their actions, as well as formalising the support of the Group, across these topics.”

b) Environment

Section revamped for 2021.

Virtual shareholder meetings sadly did not extend to the 2021 AGM:

“Continue to maximise use of video- conferencing facilities, which is available in each office and serves to limit inter-office air travel by employees. We anticipate that as we transition to a post-pandemic environment, many of CLIM and KIM clients will be much more receptive to video-conferencing which will translate to long-term improvements by a reduction in flights. In a similar vein, CLIG shareholder meetings have been held via video conference since March 2020, and will be offered in the future for shareholders that wish to meet virtually.”

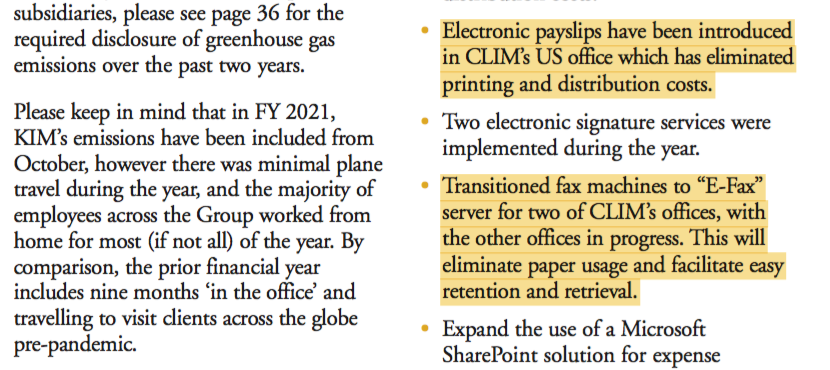

As per the blog post above, CLIG had recently used paper payslips and fax machines:

“Electronic payslips have been introduced in CLIM’s US office which has eliminated printing and distribution costs.

Transitioned fax machines to “E-Fax” server for two of CLIM’s offices, with the other offices in progress. This will eliminate paper usage and facilitate easy retention and retrieval.

Some of the climate change risks are very detailed:

“Our Singapore and Dubai offices are all subject to the projected rise in sea levels, which is a risk to our employees who live and work in those areas.”

“Additional issues relevant to our employees include the impact on infrastructure, agriculture, water supplies/scarcity, wildfires, and tree disease.”

c) Community

Suppliers now judged on “gender and ethnic characteristics“:

“During FY 2021, CLIG has partnered with at least three vendors that are female-led, which provide services across a variety of sectors including document production, website design and company secretarial services. We chose these companies because they offer best-in-class services and products. We are also aware of the benefit of diversity of thought and leadership provided by female-led companies, and will continue to include the gender and ethnic characteristics of the leadership teams in the consideration process for any vendors we look to partner with.”

3) BOARD OF DIRECTORS

a) Independent representation

The 11-person board had consisted of 5 independent non-execs, less than 50% of the directors, and so contravened the corporate governance code:

“we acknowledge that we have a way to go in order to reach compliance with provision 11 of the UK Corporate Governance Code, which stipulates that the Board should have majority independent representation.

But three execs have since stepped down from the board into a newly formed executive committee, which rebalances the board and meets the corporate governance code.

b) Diversity and inclusion

New stock-market rules could prompt a greater number of ethnic female directors within quoted companies:

“In addition to the level of independent representation on the Board, we are also cognisant of the requirements of the Hampton-Alexander Review and new consultation paper from the FCA on changes to the Listing Rules, both regarding the level of representation of those from diverse backgrounds on the Board and in senior management positions.

CLIG has made a start. The nomination committee text says:

“During the year, we recruited two new Independent Non-Executive Directors, Rian Dartnell and Tazim Essani. Tazim helps to bring us a step closer to the gender and diversity balance we hope to achieve as we continue to evaluate both the size and composition of the Board.”

c) No CFO

CLIG’s board lacks a chief financial officer, which is not ideal and may explain the FRC review and dividend infringement (see points 5b and 5c below)

4) BOARD ACTIVITIES

a) Board and committee meeting and attendance

The seventh consecutive year when the board held 3 audit meetings and 4 remuneration meetings. Boards talking more about their pay than their company financials are never ideal.

5) AUDIT & RISK COMMITTEE REPORT

a) Significant judgements, key assumptions and estimates

Useful new text for 2021 listing the accounting issues reviewed and monitored. Note the issues reviewed do not match the five key audit matters (see point 6a)

“* Share-based payments

* Acquisition-related costs

* Goodwill and intangibles

* Nature of interest in EM REIT fund”

b) FRC review of the CLIG’s Annual Report and Accounts for the year ended 30th June 2020

Oh dear, the FRC has been in touch about the FY 2020 accounts. Nothing too alarming, but not a great endorsement of the bookkeeping in what should be some very straightforward accounts:

“In March 2021, CLIG received a query from the FRC concerning the presentation of acquisition-related costs as investing activities in the Consolidated and Company cash flow statement, arising from the FRC’s review of the June 2020 Annual Report and Accounts.

The Committee reviewed all correspondence between CLIG and the FRC.

The FRC agreed with the Group’s undertaking to restate the comparative Consolidated and Company cash flow statement for the year ended 30th June 2021. The adjustments are explained in note 23 to the financial statements.

In their communication with the Group, the FRC also highlighted specific observations where the Group should consider improvements to its future reporting. The Committee reviewed and agreed with the proposed changes in respect of these observations.

The FRC’s enquiries regarding the above matters are now complete. It must be noted that the FRC’s review is limited to the published 2020 Annual Report and Accounts; it does not benefit from a detailed understanding of underlying transactions and provides no assurance that the Annual Report and Accounts are correct in all material respects.”

c) Distributions made other than in compliance with the Companies Act

Oh dear, another embarrassing bookkeeping oversight, this time a technical dividend infringement:

”Following the identification of the issue in respect of the payment of certain historic dividends, a thorough review of distributable reserves was performed by management which identified that certain distributions had been made otherwise than in accordance with the Act. This resulted in the circular to shareholders dated 2nd June 2021 and approval by the shareholders on 29th June 2021 of the resolutions to restore all parties to the position originally intended. Strict procedures have been put in place to ensure that this omission will not be repeated.”

The circular mentioned in the text above is available here, and reveals the infringements occurred every year between 2007 and 2017, and during 2019!

Points 5b and 5c do make you wonder about the lack of a CFO on the board (see point 3c)

6) BOARD ACTIVITIES

No major changes here.

a) 2022 remuneration policy review

A potential pay revamp for 2022.

“The Group’s remuneration policy was last reviewed in 2019 and is formally reviewed every three years. Our next review will therefore take place during the year and be addressed in next year’s Annual Report. As a committee, we will be allocating time throughout the period to ensure a comprehensive assessment as well as considering differences in compensation practices between CLIM and KIM.”

Will be interesting to see what emerges after “considering differences in compensation practices between CLIM and KIM.” The original CLIM business operates a 30% profit share, but whether the same scheme was widened to include Karpus staff was never made very clear. I trust the 2022 review will clarify the situation.

I get the impression from the numbers mentioned in the blog post above that Karpus employees are not part of the 30% profit share (yet!). Also, the profit-share small-print says “ Profit-share is currently paid annually in July to KIM employees“, while profit share for CLIM employees is paid quarterly.

a) CLIG’s KPI’s relationship to our remuneration policy

I do like the simplicity of the share-price total return KPI:

“We continue to believe that a key measure of the management team is the long-term total return of the shares of the company they manage. Our business model is very simple. We receive fees for managing client assets against a benchmark index.”

Also a re-iteration of the team process:

“We have developed and nurtured a team investment process which does not rely on “star” fund managers, rather upon experienced fund managers using a disciplined analytical process that can produce repeatable and sustainable first or second quartile performance versus our peers.

b) Single total figure of remuneration (audited)

No huge changes to pay levels from the prior year:

Chunky profit-share payments mean the board is not underpaid. The waived profit shares allow the directors (and other employees) to instead receive double the waived payment in shares through the Employee Incentive Plan (EIP).

But the directors did not take full advantage of the EIP:

“Due to high level of employee elections, participation had to be scaled back this year across the Group. In order to encourage maximum employee participation, and ownership of CLIG shares, the Directors elected to reduce their participation so that employees were not scaled down below 20%.”

The chief exec waived 5% of his salary to allow wider EIP participation, but the other two CLIM executives waived 15%.

Founder Barry Olliff continues to collect pension contributions even though he acts as a non-exec. Pension contribution for all executives were a useful 12.5% of salary. Mr Olliff retires from the board at the end of July 2022.

Taxable benefits for non-execs “relate to reimbursed accommodation expenses whilst attending UK Board and Committee meetings“.

The executives own 213k EIP awards and 188.5k options between them, and both schemes are available to all employees. The option count does not seem excessive and is less than the 874k ordinary shares (c£4m) owned by the execs.

Expected payouts for 2022 of between £700k and £900k for the three CLIM executive appear similar to those of 2021:

The Karpus CIO appears to be paid a lot less than the CLIM trio, which could have implications for the aforementioned pay review and “considering differences in compensation practices between CLIM and KIM“.

6) INDEPENDENT AUDITORS REPORT

Nothing untoward here.

a) Key audit matters

Two new key audit matters for 2021.

In addition to

“* Accuracy and completeness of management fees;

* Breach of investment mandates, and;

* Regulatory requirements“

are

“* Acquisition accounting, and;

* Impairment of goodwill and intangible assets“

Both were no doubt introduced following the Karpus merger.

b) Materiality and scope

Profit materiality is a standard 5% of pre-tax profit while 100% of revenue and pre-tax profit were subject to full-scope audits.

7) SEGMENTAL ANALYSIS

CLIG’s largest client generated 10% of gross fee income:

Fees from the largest client advanced 25%, which is below the 40% or so wider market movement experienced between the start and end of the year. Of course client income may not track year-start/year-end client FuM higher because FuM will fluctuate during the year.

CLIG started disclosing largest-client income in the 2020 report, and the proportion for 2020 and 2019 was 13%.

95% of gross fee income came from the States, and that proportion will increase for 2022 when Karpus contributes for a full year.

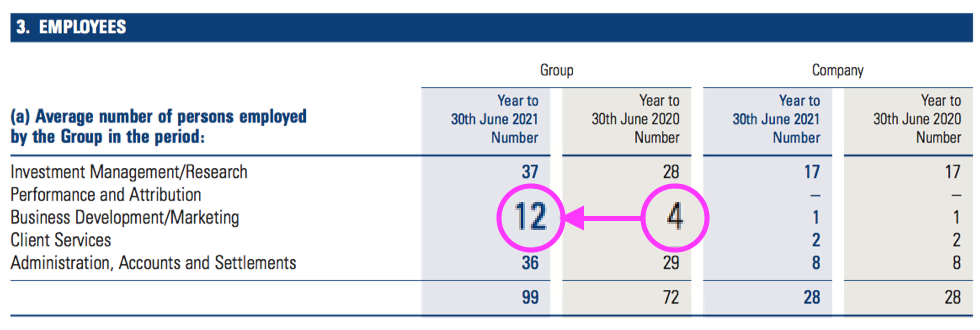

8) EMPLOYEES

Staff productivity ratios improved notably during 2021 following the Karpus merger:

99 employee averaged £557k gross fee income during 2021, setting a new high for CLIG (and beating 2011’s £537k). During the previous decade, gross fee income per employee ranged between £345k and £465k.

Total employee costs were 15.8% of gross fee income, the lowest since 2012 (15.5%). FuM per employee was $116m, the highest ever for CLIG and comparable to $60m-$80m during the previous decade.

All told these stats suggest Karpus operates with fewer but more productive employees than CLIM.

Note that profit-sharing payments of £7.43m and EIP charges of £0.95m in the accounting notes. These entries compare with £7.92m and £1.01m cited within the management narrative:

The difference I am sure is employee taxation. The total employee charge came to £20,045k in the accounting notes, and the total employee charge in the management narrative was also £20,045k (11,126k+7,923k+1,008k-12k).

9) BUSINESS COMBINATIONS and INTANGIBLES

a) Karpus contribution

Confirmation of the small print that divulged the fee income and profit from Karpus:

b) Intangible asset impairment testing

Karpus goodwill of £70m was tested using modest growth rates:

Karpus goodwill testing also involved FuM growing at 5% and an operating margin of 65%(!):

10) TRADE AND OTHER RECEIVABLES

The major entry remains accrued income, which represents revenue recognised but not yet invoiced to the customer.

I assume CLIG bills clients in arrears very early in the following month/quarter, and past cash flow statements suggest clients pay on time. Trade receivables — representing unpaid invoices — are very small at £110k.

Trade receivables and accrued income were an appealing 10.4% of gross fee income, the lowest level since 2013 (9.8%) and comparable to a more usual 12-18%.

11) TRADE AND OTHER PAYABLES

Outstanding client payments are more than counterbalanced by accrued expenses:

Pretty sure the expenses recognised in the P&L but not yet paid relate to staff bonuses.

13) OPTIONS

No option problems, with 406k options equivalent to less than 1% of the share count:

Note the £12k share-based payment credit. The wonders of IFRS2!

14) EIP

The EIP is now set to incur a total share-based payment charge of £3,686k following an extra £933k relating to the October 2021 awards:

Note the EIP totals of 2021 (£760k) and 2020 (£693k) do not equal the EIP amounts within the management narrative (£1,008k and £925k) and the accounting notes (£950k and £867k). I am not sure why that is.

14) FRC

Details of the minor FRC enquiry that is now complete (see point 5b):

Maynard