09 April 2021

By Maynard Paton

Results summary for Bioventix (BVXP):

- Acceptable interim figures that showed revenue up 1% and profit down an underlying 2% after the pandemic reduced demand for routine blood tests.

- The performance appeared to have outpaced the wider in vitro diagnostics (IVD) market, with a 20% dividend lift underpinning management’s confidence.

- Progress from the important vitamin D and troponin antibodies was positive, while R&D efforts seem now to focus on just three projects.

- The accounts remain healthy with a super 76% margin, light demands on cash flow, a £5m-plus cash buffer and a potentially understated investment.

- Predictable income and a competitive ‘moat’ presently offset the effective dependence on just two products to keep the P/E at an elevated 32x. I continue to hold.

Contents

- Event links, share data and disclosure

- Why I own BVXP

- Results summary

- Revenue, profit and dividend

- Wider IVD market

- Vitamin D

- Troponin

- Other antibodies and pipeline developments

- Financials

- Valuation

Event links, share data and disclosure

Event: Interim results and presentation for the six months to 31 December 2020 published 29 March 2021

Price: £41

Shares in issue: 5,209,333

Market capitalisation: £214m

Disclosure: Maynard owns shares in Bioventix. This blog post contains SharePad affiliate links.

Why I own BVXP

- Develops diagnostic blood-test antibodies, direct competition for which is limited due to the necessary scientific innovation, protracted regulatory testing, onerous switching procedures and ‘captive’ hospital end-customers.

- Boasts founder/entrepreneurial chief exec who has overseen an attractive growth record, retains an 8%/£17m shareholding and has declared five special dividends.

- Employs ‘scalable’ royalty/licensing model that requires few employees and leads to terrific margins, decent cash flow, high returns on equity and no debt.

Further reading: My BVXP Buy report | All my BVXP posts | BVXP website

Results summary

Revenue, profit and dividend

- The preceding FY 2020 results had already hinted the pandemic would influence this H1 performance.

- BVXP said in October:

“The Covid-19 pandemic impacted sales during Q2 2020 as routine blood-testing at hospitals continued but at a lower volume. The timing of a return to normality remains uncertain.”

- At the time BVXP implied routine blood-test volumes had dropped by 15-20% during the initial lockdown:

“There have been reports in the market that the routine global IVD market suffered a 15-20% reduction in activity during the period April to June 2020 (eg Siemens Healthineers Q2.2020 revenues as reported on 2 August). The six-monthly nature of our customer royalty reporting limits our visibility but we can see clear evidence from our physical product sales during this Q2.2020 period that corroborate such a pandemic effect.”

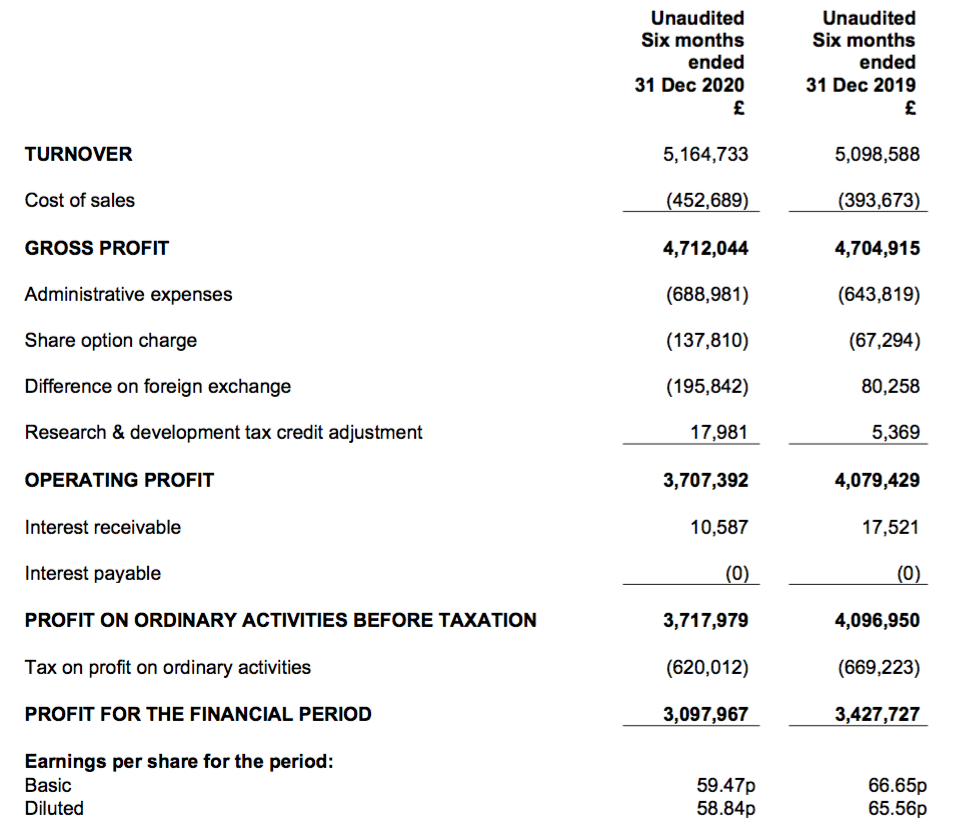

- The lower level of blood testing was reflected by revenue growth of 17% for H1 2020 reducing to only 6% for H2.

- Revenue growth reduced to just 1% for this H1.

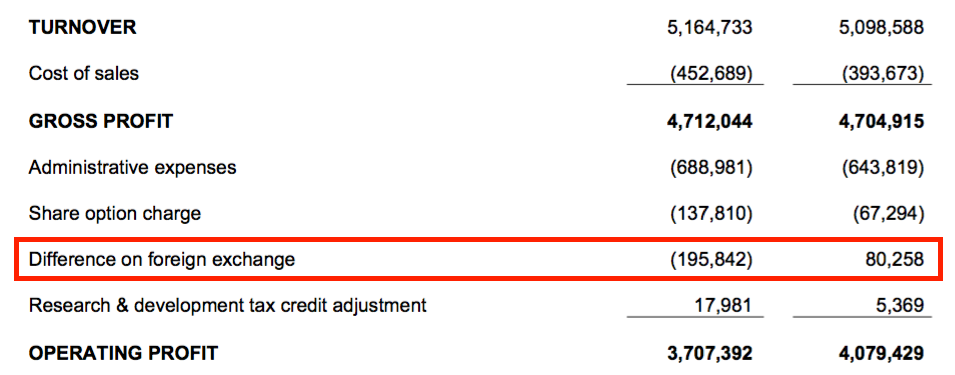

- H1 profit progress was meanwhile distorted by foreign-exchange gains/losses:

- The FY 2020 results explained how foreign-exchange gains/losses occur within the income statement:

“Any difference in exchange rate between the date of invoice and the date of receipt is reported in the form of an exchange rate adjustment and is recorded in the period as a loss or gain when it is crystallised.”

- Invoices denominated in USD and EUR typically represent more than 90% of total revenue.

- BVXP does not undertake any currency hedging.

- Reported operating profit fell 9%, but fell 2% before the foreign-exchange gains/losses.

| H1 2019 | H2 2019 | H1 2020 | H2 2020 | H1 2021 |

|||

| Revenue (£k) | 4,365 | 4,925 | 5,099 | 5,215 | 5,164 | ||

| Operating profit before FX (£k) | 3,212 | 3,819 | 3,999 | 3,982 | 3,903 | ||

| Difference on FX (£k) | 25 | (124) | 80 | 122 | (196) | ||

| Operating profit (£k) | 3,236 | 3,695 | 4,079 | 4,105 | 3,707 |

- The interim dividend was the only measure that moved significantly higher, up 20%.

- If the second-half payout is also lifted 20%, the annual dividend will have been raised 20% or more for nine consecutive years.

Wider IVD market

- BVXP claimed some patients remain reluctant to visit hospitals and undergo blood tests:

“The continuing global pandemic has, without doubt, affected the activity within diagnostic pathways in hospitals and clinics around the world to which our business is intrinsically linked. Not only have medical care resources been diverted to cope with COVID-19 patients but, even where capacity remains, there is ongoing evidence that patients are choosing not to present to healthcare professionals or not to enter diagnostic pathways“.

- The manufacturers of the blood-testing systems to which BVXP supplies antibodies disclosed similar experiences within their 2020 annual reports:

Abbot: “[Diagnostics] sales growth in 2020 was driven by demand for Abbott’s portfolio of COVID‐19 diagnostics tests across its rapid and lab‐based platforms, partially offset by lower volumes of routine laboratory testing due to the pandemic.”

Roche: “In the Diagnostics Division, sales of COVID-19-related tests totalled CHF 2.6 billion and drove the 14% increase in divisional sales, which more than offset a decline in routine testing across the portfolio.“

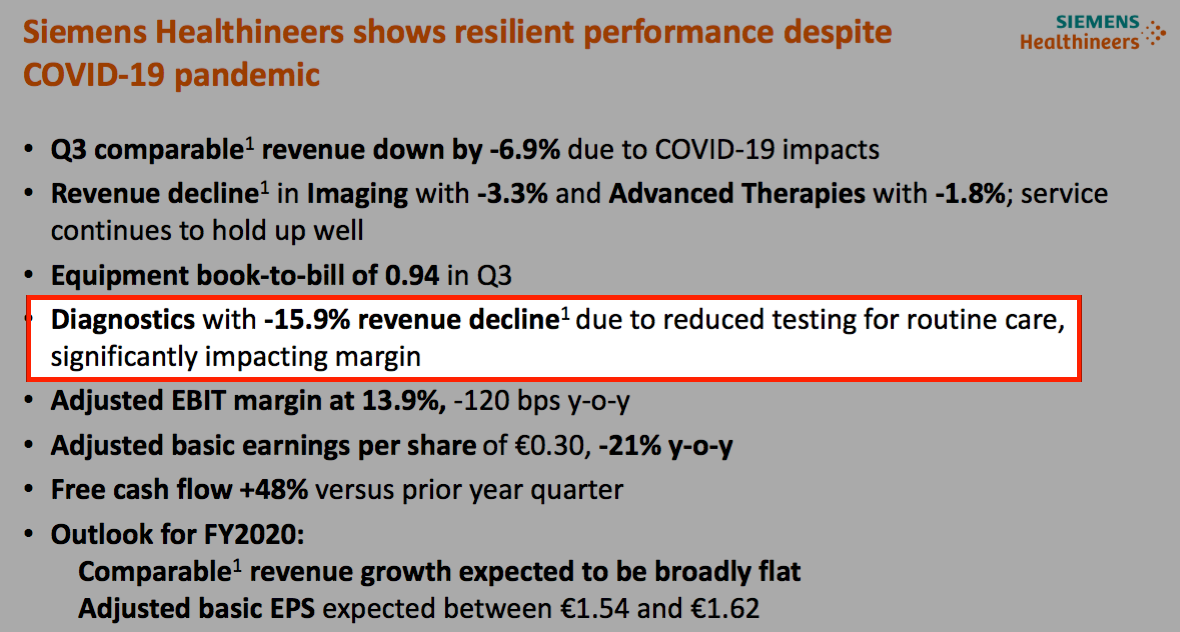

Siemens Healthineers: “Although diagnostic tests were widely applied to identify SARS-CoV-2 including large scale testing of whole populations of certain regions, this additional demand could not counterbalance the downturn for routine care resulting in a significant market decrease of the overall Diagnostics market.”

- Siemens Healthineers for example witnessed its Diagnostics revenue slide 16% during April, May and June 2020:

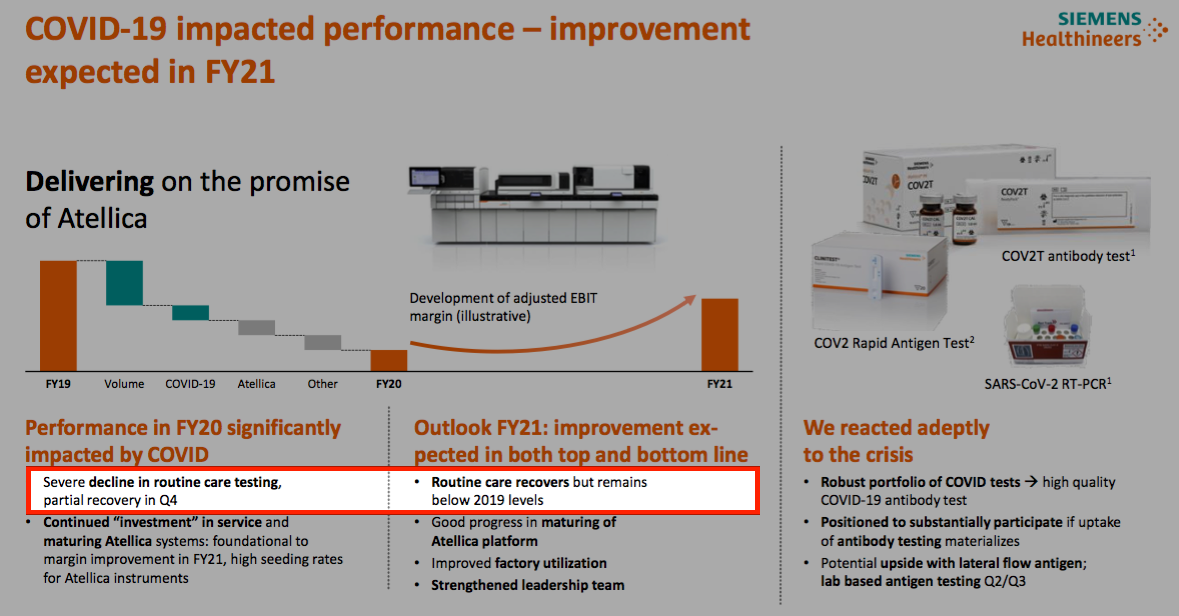

- Siemens Healthineers also claims routine blood-tests have recovered but are forecast to remain “below 2019 levels” for 2021:

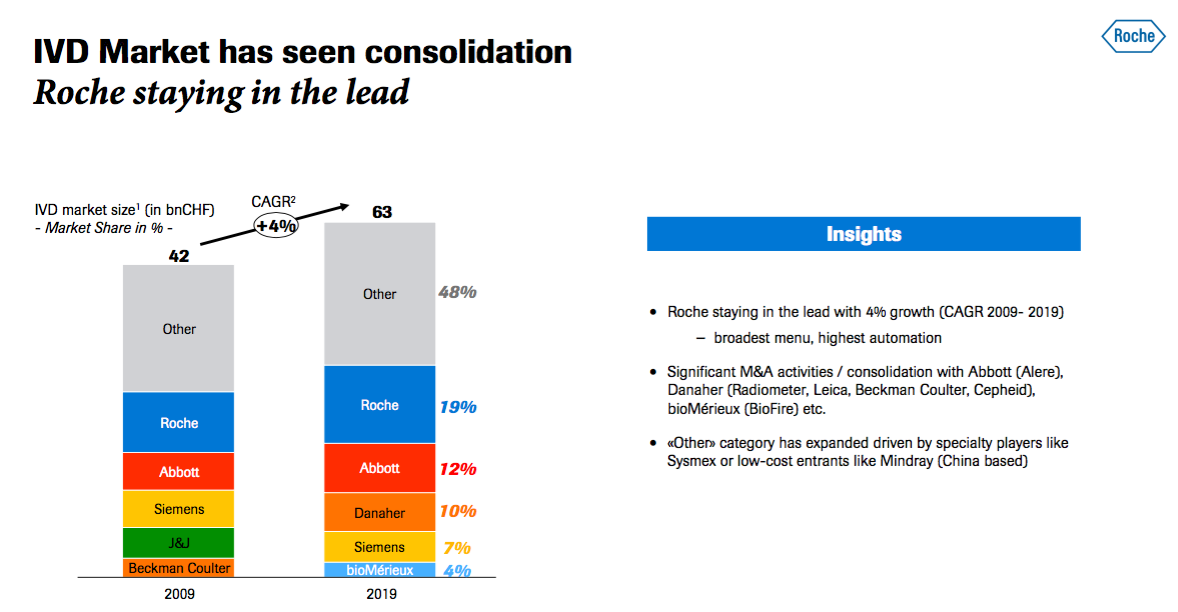

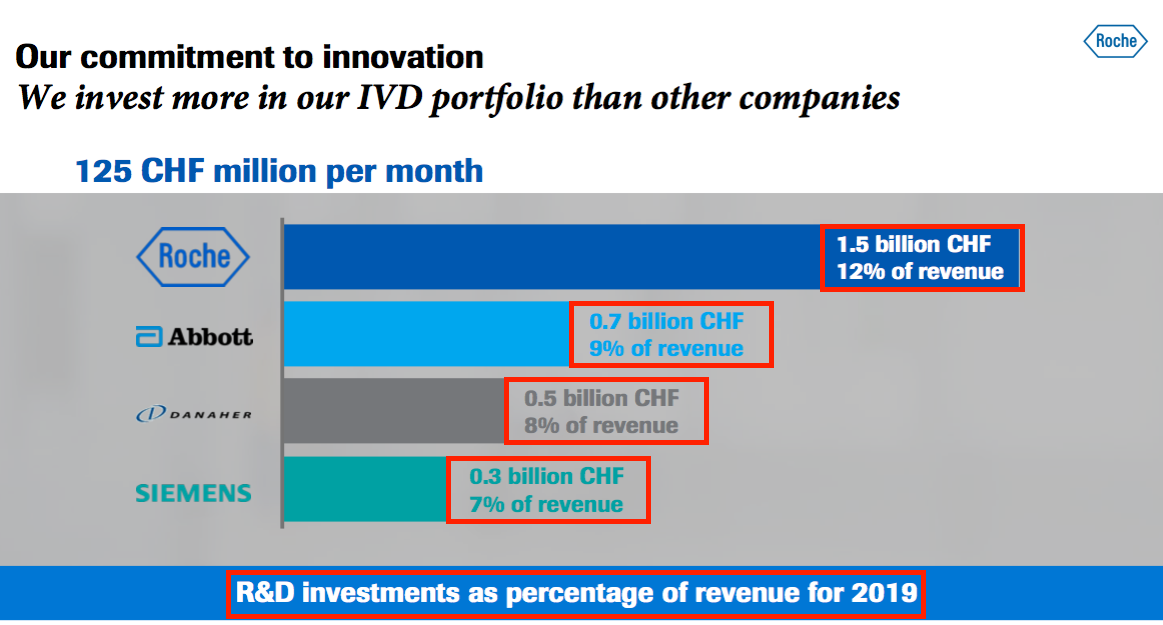

- A slide from a Roche presentation last month outlined the composition of the in vitro diagnostics (IVD) market into which BVXP supplies its antibodies:

- BVXP appears to have outperformed the IVD market during calendar 2020.

- The table below compares revenue at BVXP to that generated by the relevant divisions within Roche, Abbot and Siemens Healthineers:

| Year to 31 December | 2019 | 2020 | Change |

| Bioventix | |||

| Total revenue (£k) | 10,024 | 10,380 | 4% |

| Roche | |||

| Centralised/Point of Care Solutions revenue (CHF m) | 7,819 | 7,273 | (7%) |

| Abbot | |||

| Core Laboratory revenue (USD m) | 4,656 | 4,475 | (4%) |

| Siemens Healthineers | |||

| Diagnostics revenue (EUR m) | 4,182 | 4,094 | (2%) |

- The table data is not perfect as the divisional revenue may include income from products and services well beyond the scope of BVXP’s business.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

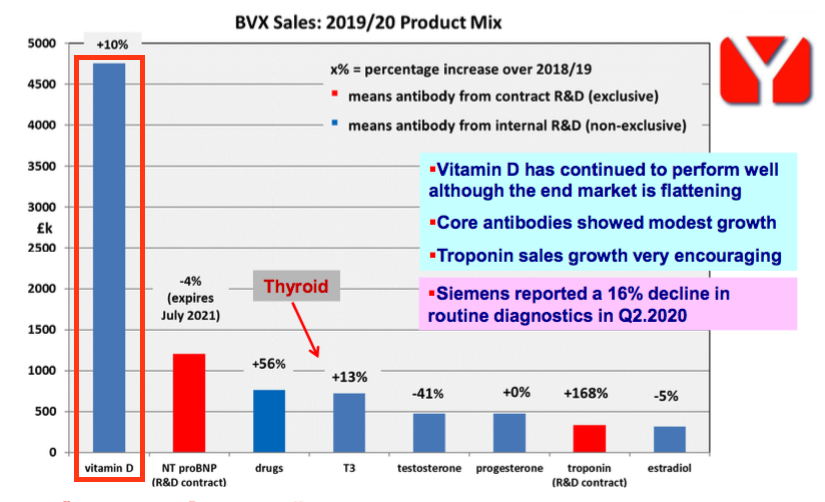

Vitamin D

- Representing 47% of revenue during FY 2020, BVXP’s vitamin D antibody is by some distance the group’s best-seller:

- BVXP seemed pleased vitamin D income had experienced “very modest growth“:

“As reported previously, vitamin D antibody sales were not expected to match the growth rates seen in recent financial years and a plateau in the downstream global vitamin D assay market had been anticipated. The very modest growth seen was perhaps better than could have been anticipated.”

- Vitamin D revenue had advanced 10% during FY 2020 and 20%-plus per annum before that.

- Warnings of the vitamin D market “plateauing” were issued within the results for FY 2017, FY 2018 and FY 2019.

- Management has in the past described the plateauing of vitamin D as growth reducing from 20%-plus to between 5% and 10% — to match the annual expansion of the general antibody market.

- I interpret this H1’s”very modest growth” for vitamin D to be less than 5%.

Troponin

- The preceding FY 2020 statement had reiterated medium-term growth was dependent mostly on sales of the troponin antibody used to diagnose heart attacks:

“Over the next few years, the commercial development of the new troponin assays will have the most significant influence on Bioventix sales. There are no antibodies in the future pipeline that are comparable to our troponin product in clear potential value and that have the ability to influence revenues in the next few years.”

- This H1 update revealed nothing to contradict that dependence.

- Troponin sales appeared promising. BVXP said:

“Sales relating to troponin antibodies grew significantly once again during the period. The continued roll-out of high sensitivity troponin tests provides further encouragement for our future sales in this area.“

- Troponin income gained 175% to £0.33m during FY 2020. I therefore interpret “grew significantly once again” as troponin sales doubling during this H1.

- Troponin revenue represented 3% of total revenue during FY 2020 and my interpretation sees that proportion move to 6%.

- Management has remarked previously that:

- Troponin revenue reaching £1.2m during FY 2022 — or 12% of current revenue — is “entirely plausible”.

- House broker Finncap “predicts revenues that are around £3m for troponin going into the future.”

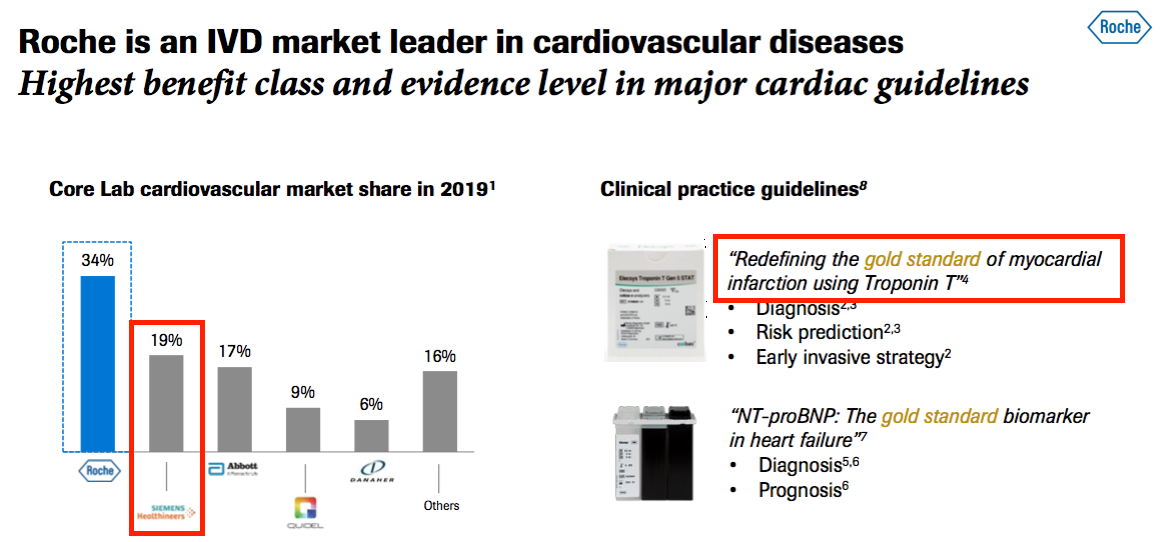

- The aforementioned Roche presentation from last month contained some informative slides.

- This first slide revealed:

- Roche has its own troponin test, and;

- Siemens Healthineers, to whom BVXP is supplying its troponin antibody, has a 19% share of the wider cardiology diagnostic market:

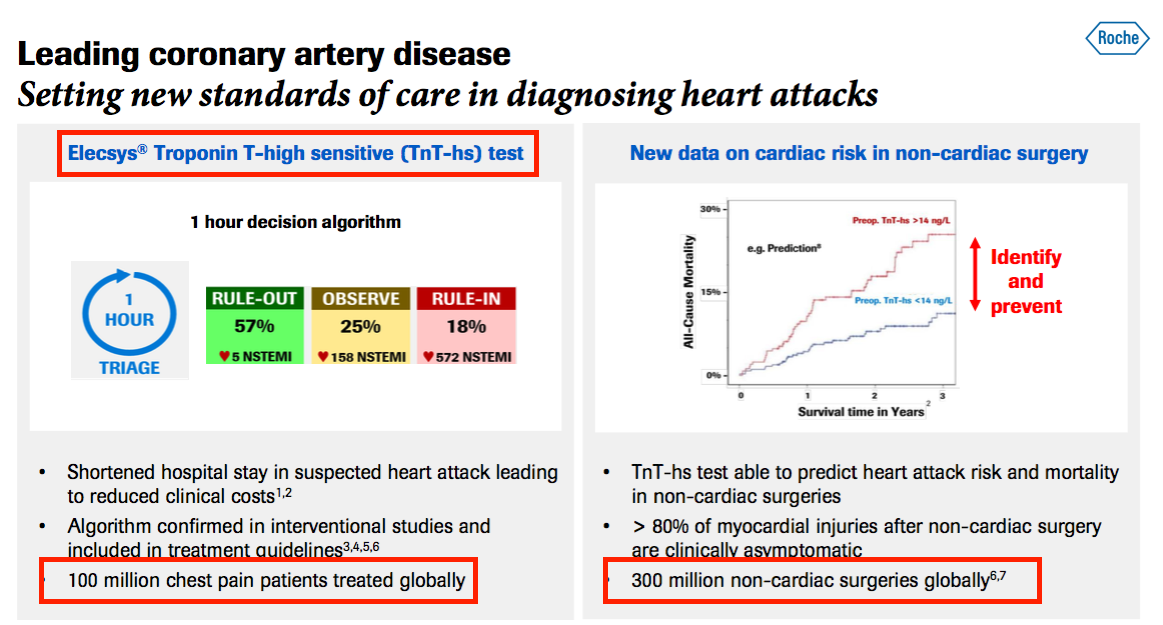

- This second slide claimed:

- 100 million patients are treated every year for chest pains, and;

- Troponin could be used to help diagnose 300 million “non-cardiac surgeries” a year:

- Siemens Healthineers’ 19% share of the cardiology diagnosis market could imply a possible 19 million potential BVXP troponin tests annually.

- Reaching the house broker’s £3m troponin sales guess therefore requires a 16p income from each of the 19 million troponin tests.

- Include the extra 300 million tests then implies a 4p income per test.

- I am not sure whether these assumptions are credible. I had always understood BVXP’s income per blood test was much less than 16p and also less than 4p.

- Perhaps troponin will earn extra income beyond that from Siemens Healthineers.

- My contact form is here should you wish to help me out with my troponin guesswork.

Quality UK investment discussion at Quidisq. Visit forum.

Other antibodies and pipeline developments

- BVXP said fewer blood tests were performed using its other antibodies:

“Our antibodies for thyroid disease diagnostics (T3) and others for fertility diagnostics (estradiol, progesterone and testosterone) form part of routine diagnostics for chronic conditions which are often not life-threatening. We believe that such diagnostic tests have experienced lower volumes in pandemic affected areas and this has had a small impact on our own revenues.”

- Assuming vitamin D sales advanced by an estimated 5% and troponin sales advanced by an estimated 100%, income from these other antibodies would have dropped 4% during this H1.

- Nothing was said about NT proBNP, the income from which will cease during July 2021 and represented 12% of FY 2020 revenue.

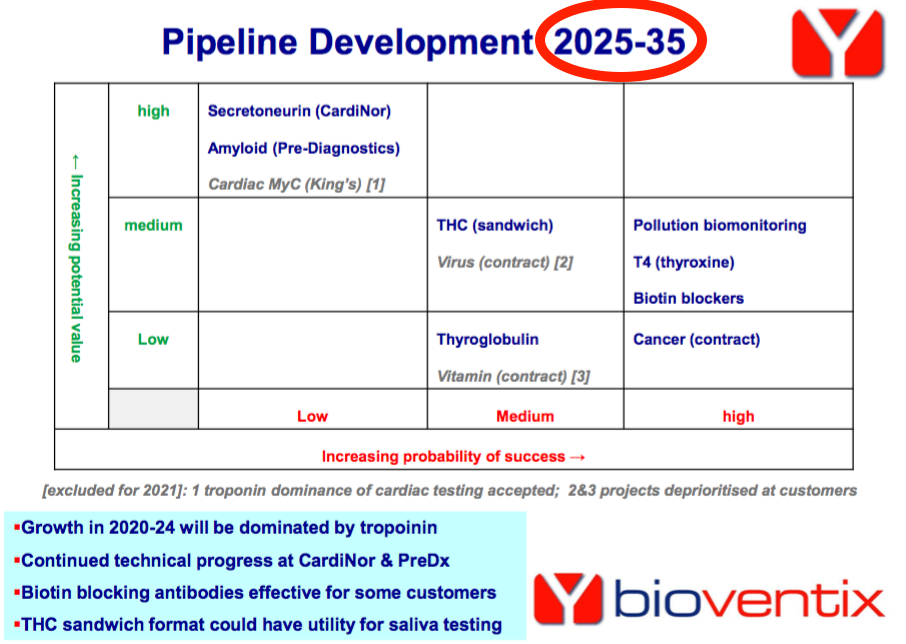

- The pipeline grid that showcases the possible value and probability of success for each development project…

- …was this time replaced by “research news“:

- I presume the three projects highlighted have become the main potential money-spinners.

- I note the 2025-2035 cited on the pipeline grid above was not included within this H1 presentation.

- Perhaps BVXP is no longer as confident about its pipeline timescale as it once was.

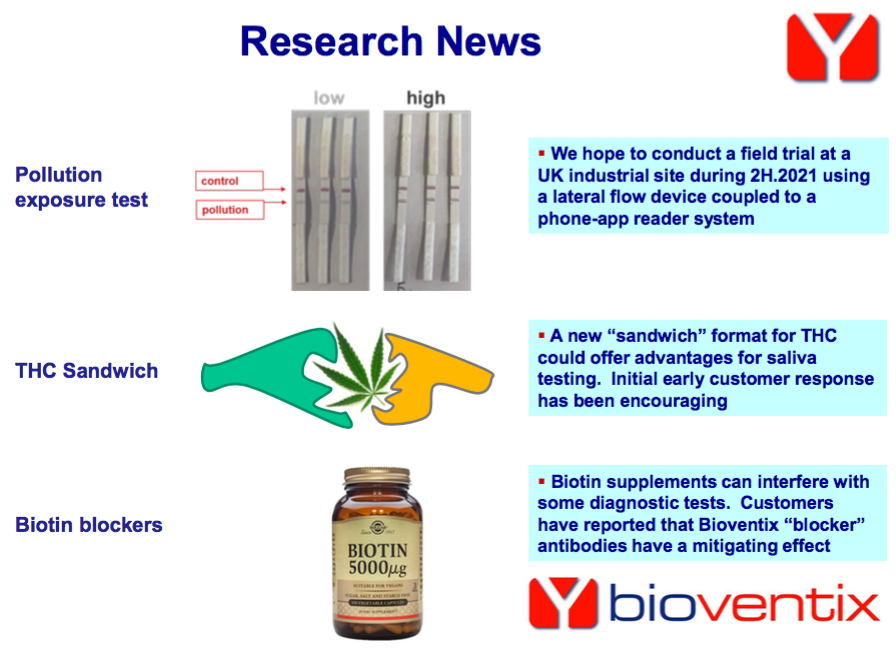

- The leading hope appears to be a pollution exposure project. BVXP said:

“We are particularly pleased with the development of our pollution exposure assay. We hope to have a prototype urine lateral flow test featuring in a field trial at a UK industrial site later in 2021.“

- No mention was made of the pollution project’s lab-based ELISA (enzyme-linked immunosorbent assay) kit that was highlighted this time last year.

- The commentary on biotin ‘blockers’ — antibodies intended to mitigate interference from biotin supplements during certain blood tests — appears to have improved.

- The preceding FY 2020 statement had admitted:

“Early evaluation samples have had mixed results at different customers.“

- But this H1 update claimed:

“We have received early positive feedback on the performance of these blockers from some customers. During 2021, we will continue to receive feedback and consider further the possible commercial development of these blockers where bulk manufacture at low cost will be important.“

- The relatively new Tetrahydrocannabinol (THC) project seems to be going well:

“In December 2020, we sent samples of THC (the active ingredient in cannabis or marijuana) antibodies to a few selected customers who are interested in improving their THC lateral flow assays for saliva. The early feedback from these customers has been encouraging and we expect to gather more feedback during the year.”

- Exactly which products (if any) from the pipeline eventually make it to market remains anyone’s guess. For perspective, the troponin antibody took more than ten years in development before its commercial launch.

Financials

- BVXP’s accounts remain in good shape.

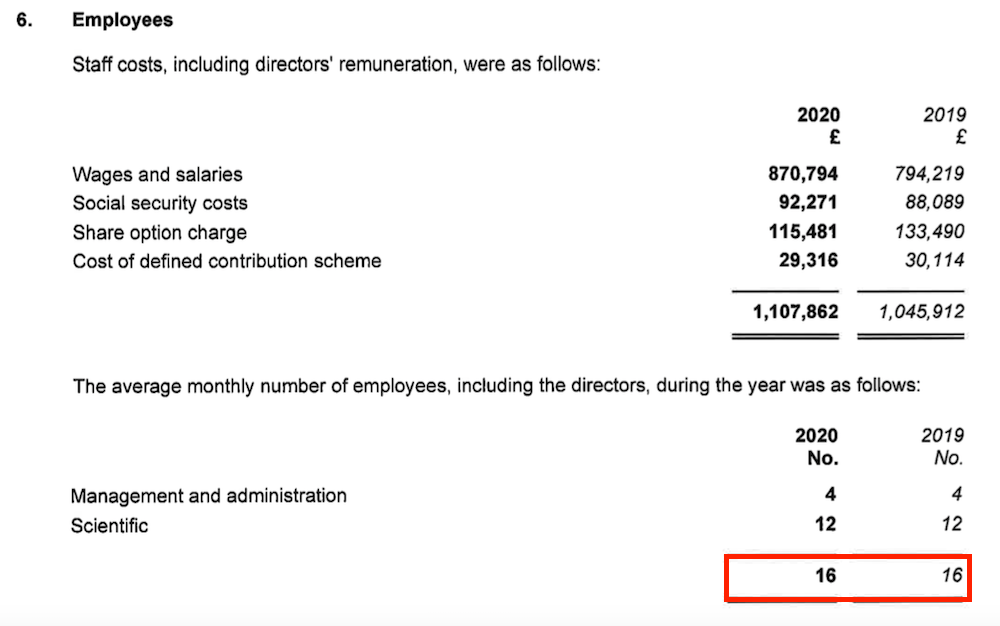

- The operating margin (before foreign-exchange gains/losses) continues to be superb at 76%, and underlines the wonderful economics of earning license fees and royalties from successful antibodies.

- The superb margin is a result of extra fees and royalties attracting little (or no) incremental cost, with expenses being kept under control by employing only 16 people (point 9):

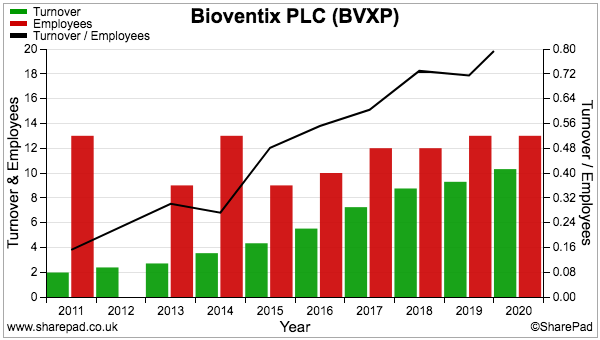

- The ‘scalable’ nature of BVXP’s business is emphasised by revenue per employee more than quadrupling during the last decade (black line, right axis):

- Demands on cash flow continue to be modest, with reported H1 earnings of £3.1m converting into free cash flow of £3.2m following £0.2m diverted into working capital, £0.1m spent on capex and £0.4m not yet paid as tax.

- The cash position reduced by £2.2m to £5.8m after paying £5.5m to cover last year’s second-half/special dividends.

- The £5.8m cash position exceeds the £5m that BVXP has previously declared as:

“…sufficient to facilitate operational and strategic agility both with respect to possible corporate or technological opportunities that might arise in the foreseeable future and to provide comfort against the ongoing impact of the pandemic and any economic uncertainty arising from it.”

- A repeat of the cash generation witnessed during this H1 for the current H2 2021 could/should justify another special dividend. BVXP has declared a special payout during each of the last five years.

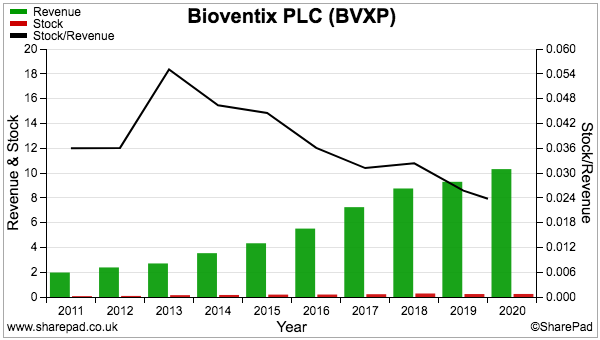

- Stock at £225k represents a tiny 2% of revenue…

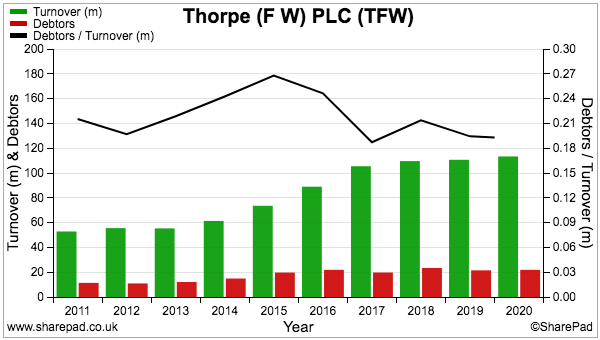

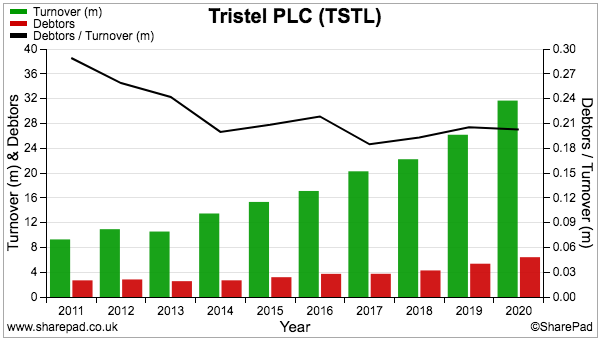

- …and compares very well to fellow portfolio holdings Mincon at 41%, FW Thorpe at 22% and Tristel at 15%.

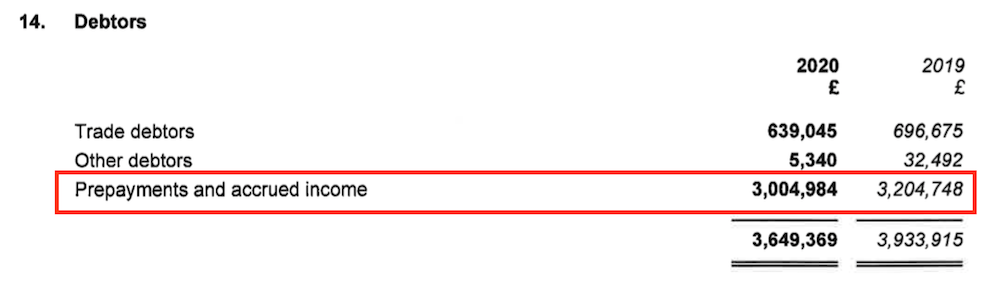

- After the cash position, the largest balance-sheet entry is debtors.

- Debtors are dominated by accrued income (point 14), which represents revenue earned but has yet to be invoiced at the balance-sheet date:

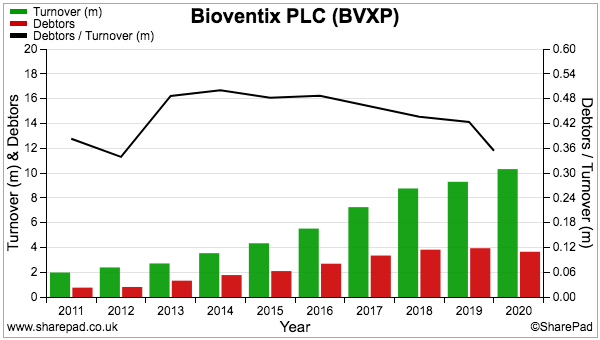

- BVXP has a relatively high level of debtors.

- Debtors have often represented more than 40% of revenue and represented 35% of revenue at the FY 2020 year end:

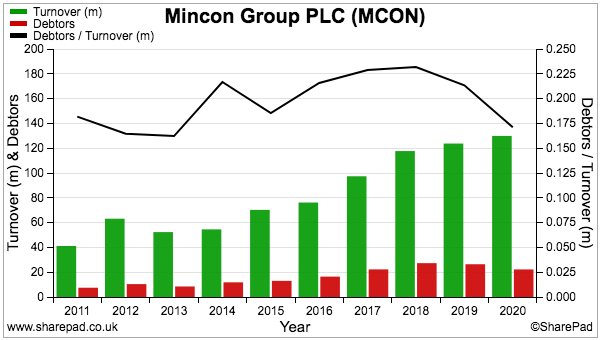

- In comparison, debtors represent approximately 20% of revenue at Mincon, FW Thorpe and Tristel:

- High debtor levels can sometimes mean customers are tardy payers and/or revenue has been recognised aggressively.

- However, BVXP’s high debtors are simply a function of its royalty business.

- IVD companies such as Siemens Healthineers pay their royalties to BVXP only twice a year. Fewer payments from customers therefore lead to greater levels of unpaid/unraised invoices at the balance-sheet date.

- In contrast, customers at Mincon, FW Thorpe and Tristel settle their invoices throughout the year, thereby leading to lower levels of outstanding invoices at the balance-sheet date.

- BVXP’s long record of 20%-or-more annual dividend increases suggests converting debtors into cash has not been difficult.

- The balance sheet carries no bank debt and no pension complications.

- A hat-tip to valuestar1 on the ADVFN bulletin boards for highlighting Intuitive Investments (IIG) paying £125k last month for 1.8% of Cardinor.

- BVXP acquired 10% of Cardinor during 2016 for what the 2016 annual report implied was £43k.

- BVXP’s 10% investment may therefore have increased from £43k to £0.7m.

- The book value of BVXP’s investments in Cardinor and Pre-Diagnostics is £610k.

Which is best for stock-screening: Stockopedia or SharePad? See my verdict.

Valuation

- BVXP’s immediate outlook did not seem too concerning:

“[W]e are encouraged by the performance of Bioventix for the current half-year and pleased with the continued success of our vitamin D antibody and core antibody business. We remain optimistic about our troponin revenues and the success of these high sensitivity troponin products around the world and we look forward to reporting further progress in the second half of the year.”

- The text was almost identical to the outlook given this time last year…:

“[W]e are encouraged by the performance for the six months ended December 2019 and pleased with the continued success of our vitamin D antibody and core antibody business. We remain optimistic about our troponin revenues and the success of these high sensitivity troponin products around the world. Whilst we are mindful as to the potential impact of COVID-19, we currently expect further progress in the second half of the year. “

- …and the year before that…:

“We are delighted to be able to report such positive news for the current half-year. We are pleased with the continued success of our vitamin D antibody and the remainder of the core antibody business. We remain optimistic about our troponin revenues and the success of these high sensitivity troponin products around the world and we look forward to further progress in the second half of the year.“

“We are delighted to be able to report such positive news for the current half-year. We are pleased with the continued success of our vitamin D antibody and the remainder of the core antibody business. We remain optimistic about our troponin project and the success of Siemens as their product launches around the world and we look forward to further progress in the second half of the year.”

- Each time BVXP then proceeded to report respectable H2 progress, so the omens for this H2 2021 seem positive.

- The aforementioned 20% dividend lift does not imply trouble either.

- BVXP’s past presentations included house-broker forecasts for the upcoming year:

- The inclusion of these forecasts was very commendable — companies typically don’t endorse broker projections in case the projections are not met.

- But this H1 presentation and the preceding FY 2020 presentation did not include a house-broker forecast for the upcoming year.

- I trust BVXP has not become nervous about its future performance. I suspect the house broker has asked BVXP not to make its forecasts available to the wider public.

- BVXP’s valuation can of course be judged without the house broker.

- Excluding foreign-exchange movements, BVXP’s trailing operating profit is £7.9m.

- Taxed at the 16% applied during this H1 gives earnings of £6.6m or 127p per share.

- BVXP’s £5.8m cash position equates to 112p per share and does not make a great difference to valuation when the share price is £41.

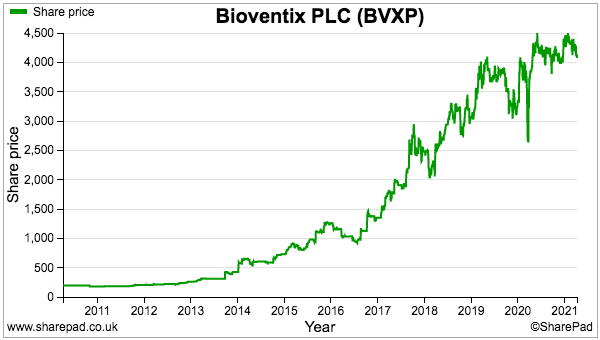

- Dividing the £41 share price by my 127p per share earnings estimate gives a trailing P/E of 32.

- The rating remains understandably lofty. Justifications for the elevated multiple may include:

- The predictable and seemingly pandemic-resilient income from antibody sales and royalties;

- A competitive ‘moat’, helped in part by replacement antibodies needing to be much more effective to justify the protracted development/regulatory undertaking;

- The notable growth opportunity through troponin alongside various speculative pipeline efforts, and;

- The amazing 76% margin that underlines the very attractive economics of antibody commercialisation.

- BVXP does have downsides. Reasons to be wary may include:

- A material dependence on vitamin D, sales growth from which is slowing;

- Profit advances for the next few years resting almost entirely on the popularity of troponin, the income from which will expire during 2032;

- The lead pipeline project (pollution monitoring) appearing to deviate from BVXP’s blood-testing heritage;

- Other pipeline antibodies seeming to be un-troponin-like in terms of medical importance and sales potential, and;

- Inherently limited R&D opportunities owing to huge competing budgets at IVD giants such as Roche, Abbot, etc.

- The twelve-month 95p per share ordinary dividend supports a 2.3% yield.

- Given BVXP has distributed all of its earnings as ordinary and special dividends between FY 2016 and FY 2020, then perhaps the 3.1% yield based on my 127p per share earning guess is a more appropriate income measure.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

I just wonder if antibodies for vitamin D tests will be as weak as described. A number of commentators, including John Campbell and my wife, believe low levels of vitamin D MAY be a factor in weakening resistance to viral inections including covid. May this not give a fillip to the utility of such testing?

Hi Stephen

Many thanks for the comment and highlighting John Campbell.

BVXP’s management has briefly mentioned vitamin D testing and coronavirus:

“I think there’s been a degree of interest in vitamin D and its association with coronavirus patients and how they perform in hospitals, so there might be some extra testing taking place through medical curiosity and the gathering of research.”

Management has generally tended to downplay/under-promise BVXP’s prospects, so there might be something more to this, but I did not read anything definitive into the comments made.

Some links to John Campbell on Youtube:

https://www.youtube.com/channel/UCF9IOB2TExg3QIBupFtBDxg

https://www.youtube.com/watch?v=au6FKi8aAsA

His comments during the vitamin D video seem encouraging. So yes, perhaps such testing may not be as weak as management describes. Would be positive for BVXP if vitamin D deficiency is indeed linked to greater chance of viral infection.

Maynard

Thanks for your analysis Maynard. I have been pleasantly surprised by the resiliance of BVXP’s Vit D sales (in the light of my comment at the full year stage). Clearly, the demand for Vit D testing has not waned as much as that for other hospital tests/procedures. Such waning evidenced by these recent examples:

1) Tristel’s results, your Quote: UK hospital-related revenue fell 4% to £5.0m — with UK medical-device revenue dropping 20% to £3.5m.

2) Clinigen: “The negative impact of Covid-19 is primarily due to the global reduction in hospital-based oncology treatments and delays to clinical trials. In particular, demand for Proleukin within its current approved indications was significantly weaker than expected in recent months,”

John Campbell has indeed become an internet star, particularly in the US, and this, and the whole Vit D story, may have ‘pulled’ some patients into the Doctor’s office to request Vit D tests, helping to maintain Vit D testing at last years’ levels.

The voting is out on whether Vit D helps alleviate symptoms of Covid. John Campbell takes part in a Vitamin D debate with Professor Tim Spector here (https://www.youtube.com/watch?v=aCAvvZXUW08). This is an excellent overview of the debate from both sides of the argument. Clearly, what’s needed is a large scale trial, (maybe replicating the Spanish trial that Campbell references, where patients entering hospial with Covid were dosed with Vit D).

Personally, I’ve bought the story, as the only supplement I take is Vit D and then only in the winter. I do this eventhough:

1) I’ve never had my Vit D levels measured (nor likely to, this is the UK after all!)

2) Its based on correlation rather than causation

Hi Roger,

Thanks for the comment and I hope all is well. Yes, vitamin D keeps on delivering for BVXP and Peter H seemed optimistic when asked about the subject last year. I confess I have not kept up with the scientific debate but I take some comfort that you and lots of Youtube commenters take interest in their vitamin D levels!

Maynard

Dear Maynard:

Thank you very much for your thorough analysis of BVXP. Just a follow-up question to your statement “Profit advances for the next few years resting almost entirely on the popularity of troponin, the income from which will expire during 2032;”

What is your understanding of what can/will happen to troponin after 2032? Is it certain that BVXP’s revenue stream will be zero, or is it e.g. that a new agreement will have to be reached? Or perhaps continue at a lower price point? (Presumably physical product will still be needed in the market, and the product produced somewhere?)

Hello Martin,

My understanding is the troponin revenue stream will terminate during summer 2032 and will be zero thereafter. At least that was the message given by the chief exec during this ShareSoc webinar (available to ShareSoc members only; question asked at c50mins). The chief exec said the troponin expiry “does underline the need for us to develop new things that have value in 2025-2035.”

Maynard