26 June 2015

By Maynard Paton

Quick update on Mountview Estates (MTVW).

Event: Preliminary results published 25 June

Summary: MTVW’s best-ever results, albeit they included what looks to have been quite a weak finish to the year. Importantly, gross margins were high and management’s outlook continues to be positive. Furthermore, the dividend marched upwards once again. My sums point to a possible NAV of £180-plus per share based on the firm’s previous gains from its sold properties. I continue to hold.

Price: £120

Shares in issue: 3,899,014

Market capitalisation: £468m

Click here for my previous MTVW posts

Results:

My thoughts:

* Sparse management commentary and minimum accounting info

MTVW traditionally provides little detail within its RNS statements, which is not great. However, I can live with the sparse updates given the group’s illustrious long-term record — the dividend has grown at a 13.5% average during the last 25 years!

The forthcoming annual report will contain much more information, so until that’s published my current verdict involves a fair bit of guesswork. When the annual report is released, I’ll post a comment to this Blog post that evaluates the extra information.

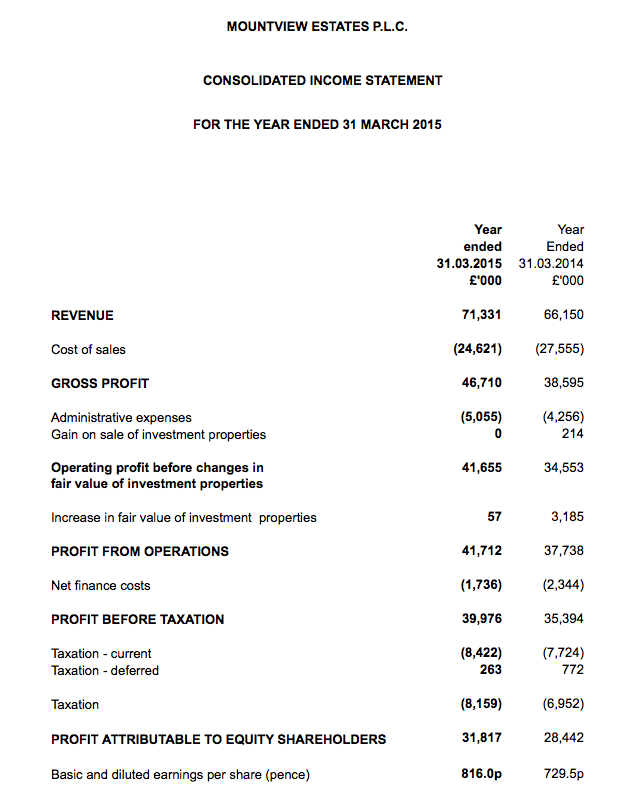

* These results were actually a record

You would not know it from the sparse management commentary, but these results were actually a record for the residential-property investing firm.

Revenue, gross profits and operating profit (before changes in the fair value of investment properties) were all ahead of the group’s previous peaks set during 2007.

Indeed, it is probably worth mentioning that since 2007 and the top of the property market, MTVW’s net asset value has still managed to advance 66% and the dividend has improved by 83%.

* H1 better than H2…but did the end of the year finish weak?

MTVW described the results as an “enhanced performance”, although progress was weighted towards the first half:

| H1 2014 | H2 2014 | FY 2014 | H1 2015 | H2 2015 | FY 2015 | ||

| Revenue (£k) | 28,825 | 37,325 | 66,150 | 36,900 | 34,431 | 71,331 | |

| Gross profit (£k) | 15,894 | 22,701 | 38,595 | 24,106 | 22,604 | 46,710 |

In fact, a statement in February said gross profits had improved by 41% during the first 10 months of the year, which compares to the 21% advance for the full year. The implication here is that gross profits for the final two months of the year were very weak.

I am not too concerned about a possible weak Q4. The nature of MTVW’s properties means they become available for sale at any time (usually when the sitting tenant leaves or dies) and revenue from month to month can therefore be unpredictable.

What’s more important to me is the gross margin — that is, the gain MTVW makes from selling its properties over their original cost. So I am pleased the overall gross margin throughout last year was 65% — the highest for seven years.

* Upbeat outlook

MTVW seemed positive on the future:

“Borrowings have been reduced and we are still able to make good purchases.”

At £60m, net debt is the lowest since 2007.

Lifting the annual dividend by 37.5% showed some confidence, too.

* No news of management succession

This time last year MTVW said:

“Duncan Sinclair has been with the Company for 43 years, during which he has occupied the positions of Company Secretary, Director, Executive Chairman and Chief Executive. The Company has grown and developed significantly since Duncan became Chief Executive in 1990. The search to find and establish Duncan’s successor is on-going and now intensifying. This is an important phase in the Company’s development.”

But there was no mention of succession planning this time. Mr Sinclair will turn 68 later this year and the word on the grapevine (at least from last year’s AGM) is that Mr Sinclair is in no hurry to relinquish his executive duties.

* No further revaluation developments

MTVW’s preceding interim figures revealed the group’s trading properties had a current market value of £666m versus a book value of £318m. As expected, there was no further update to the current market value other than to say the figure was “way beyond” the historical-cost number.

Valuation

These results showed trading investments of £323m which, if sold at the the average margin enjoyed during the last ten years, would yield about £840m.

Taxing the resultant gain at 20% and then adding on MTVW’s other investments of £29m and subtracting its debt of £61m, I arrive at a possible net asset value (NAV) of £705m or £180 a share.

(That compares to the £74 per share NAV reported by MTVW on a historical cost basis.)

Alternatively…

Using the £666m market-valuation figure presented within November’s interim results, and then assuming a 33% uplift for converting the properties from sitting tenancies to normal properties… I arrive at an £888m valuation.

Then taxing that gain at 20%, adding on the other investments of £29m and subtracting debt of £61m, I arrive at a potential NAV of £743m or £190 per share.

With the share price at £120, clearly there is still some upside potential in place here. But the big unknown is just how long it will take MTVW to sell its existing properties to realise my potential £180-plus per share NAV.

All told, it was far easier to judge MTVW back in 2011, when I bought at about £41 and when the NAV — based on historical cost! — was £55 per share.

Meanwhile, the lifted 275p per share dividend supports a 2.3% income.

* Next update — a Q1 update on 19 August.

Maynard Paton

Disclosure: Maynard owns shares in Mountview Estates.

Great post – I’ve submitted it to the UKFinanceOver30 sub-reddit.

https://www.reddit.com/r/UKFinanceOver30/

Mountview Estates has published its 2015 annual report:

http://www.mountviewplc.co.uk/AR2015.pdf

Here is what I found that was worth noting:

* Chief exec succession may be on hold

I mentioned in the initial Blog post above that chief exec Duncan Sinclair was in no hurry to relinquish his executive duties. The 2015 annual report provides further evidence of that being the case.

In the 2014 annual report, the chairman said:

But within the 2015 annual report, Mr Sinclair has written:

That reads to me as if Mr Sinclair is staying put as chief exec for some time.

The small print in the Directors’ Report suggests looking for a new chief exec was not a high priority for the Nomination Committee:

* Same old ‘still pleased with the results so far’ prospects for the group

MTVW repeated the same summary prospects used in the 2013 and 2014 annual reports for the 2015 annual report:

If the results for 2016 show the same sort of progress as the figures for 2014 and 2015 did, then I will be happy.

* 20% pay rise for the boss

I see chief exec Mr Sinclair enjoyed a £60k pay rise to £360k — plus a nice £300k bonus and hefty £99k pension contribution:

True, the 20% pay rise looks generous, but my records show Mr Sinclair’s salary has grown at an annual average of 7.6% during the last 5 years, while the dividend over the same time has been upped 10.8% a year on average.

The figures for the last 10 and 15 years are 4-6% compound annual growth for Mr Sinclair’s salary, versus 8-9% for the dividend. MTVW’s net asset value has also compounded at a rate greater than Mr Sinclair’s wage.

Overall, I don’t think shareholders can have too much to gripe about. I would be happy to see dividend and NAV growth outpace Mr Sinclair’s wages in the future.

* Profit on property sales at 186%

The initial Blog post above mentioned gross margins at 65% — their highest since 2008. I was pleased to see the accounting notes reveal properties sold during 2015 fetch 286% of their original cost value:

For perspective, the last 5, 10 and 15 years have on average seen properties sold at about 265% of their cost value — and my valuation sums in the above Blog post used 260%.

* Confirmation of the property revaluation

The property revaluation published at the preceding interim results was confirmed in the accounting notes:

The balance sheet continues to carry properties at the lower of cost or net realisable value.

The £666m revaluation figure is based on existing leases and tenancies — that is, before any uplift to the market value of the property as and when the regulated tenancy ends.

Maynard

HI Mayn,

I was just browsing through your two posts on MTVW and noticed that there was a very material uplift in your NAV guess from the first article (“Why I’m Up 70% in 3 Years”), where you guess a NAV of £103 per share, to this article, where you calculate £180 per share.

In the first article, you don’t give your exact working, but your method sounds similar to that which you use to calculate £180 per share in this article:

“My latest sums indicate the balance sheet could be worth £103 a share based on those interim accounts.

Again, I’m assuming the regulated properties in the books at £328m can be sold for 2.6 times their original cost. My calculations also assume the proceeds are subject to normal tax, all debts are paid off, and the group’s investment properties sustain their £26m value.”

Using the 2013 Interim figures, £328m trading properties x 2.6 times uplift = £853m, minus 20% tax on (£853m – £328m) = £105m, plus investment properties of £26m, minus debt of £99m gives a potential NAV of £675m, or £173 per share, using the first of the two methods in this post, the most recent article.

Obviously we have had the big independent valuation since your original post, however you don’t use this revaluation in your working. I was wondering if I was missing an assumption here in how you have come to your figures? If the original NAV guess should have closer to £173 per share in your original article it shows with hindsight what a steal they were at that point when they were £70 to buy!

Thanks,

GavSmith01

Hello GavSmith01

Super sleuthing!

I must admit I made a mistake in my initial spreadsheet that I discovered only in 2014 (and long after my first purchase)! I multiplied the trading-property stock by 1.6x rather than 2.6x.

(I realised here: http://uk.advfn.com/cmn/fbb/thread.php3?id=18565246&from=99)

If I had not made that mistake at the time of my original purchase at c£40, then I may have put a lot more into the shares. Oh well. At least even with the mistake I had a margin of safety. I always need an MOS just in case my sums are wrong!

Anyway, good spot. Well done.

Maynard