26 October 2018

By Maynard Paton

Update on Tristel (TSTL).

Event: Final results for the twelve months to 30 June 2018 published 17 October 2018 and shareholder presentation hosted 18 October 2018.

Summary: I was broadly satisfied with these full-year figures, which set new records for revenue, profit and the dividend. However, the statement and City presentation provided numerous little niggles — not least a bizarre management decision that has delayed product approval within the United States for a further six months. Still, TSTL’s collection of medical disinfectants continue to produce attractive accounts and perhaps their biocidal qualities have been underlined by recent deals with the NHS and Parker Laboratories. I continue to hold.

Price: 220p

Shares in issue: 43,700,048

Market capitalisation: £96m

Click here to read all my TSTL posts.

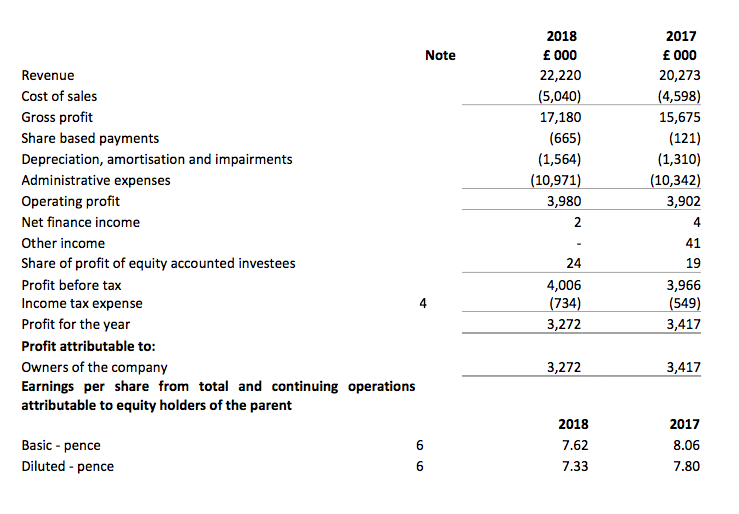

Results:

Picture:

My thoughts:

* Record results highlight questionable slides from July’s open day

TSTL’s open-day trading statement from July had already heralded these results:

“Tristel will report record turnover of £22.2m (2017: £20.3m) and pre-tax profit (before share-based payments) of at least £4.4m (2017: £4.1m). Revenue from overseas markets contributed 51.3% of the Group total – a record level (2017: 47%).”

Revenue was indeed a record at £22.2m (up 10%), while pre-tax profit (before some hefty share-based payments) was actually better-than-projected at £4.7m (up 14%). Revenue from overseas markets contributed 51.2% of the group’s top line.

The performance showed revenue, pre-tax profit and the dividend all setting new peaks for the fourth consecutive year:

| Year to 30 June | 2014 | 2015 | 2016 | 2017 | 2018 |

| Revenue (£k) | 13,470 | 15,334 | 17,104 | 20,273 | 22,220 |

| Operating profit (£k) | 1,819 | 2,541 | 2,568 | 3,902 | 3,980 |

| Associates (£k) | 8 | 8 | 13 | 19 | 24 |

| Finance income (£k) | (4) | 3 | 12 | 4 | 2 |

| Other items (£k) | - | - | - | 41 | - |

| Pre-tax profit (£k) | 1,823 | 2,552 | 2,593 | 3,966 | 4,006 |

| Earnings per share (p) | 3.25 | 5.44 | 5.01 | 8.06 | 7.62 |

| Dividend per share (p) | 1.62 | 2.72 | 3.33 | 4.03 | 4.58 |

| Special dividend per share (p) | - | 3.00 | 3.00 | - | - |

Indeed, turnover of £22.2m was just shy of the £22.8m minimum TSTL had projected for 2019 back in October 2016. Meanwhile, pre-tax profit after share-based payments inched only 1% higher. More on share-based payments later.

I should add that these results highlighted a couple of questionable slides from July’s presentation.

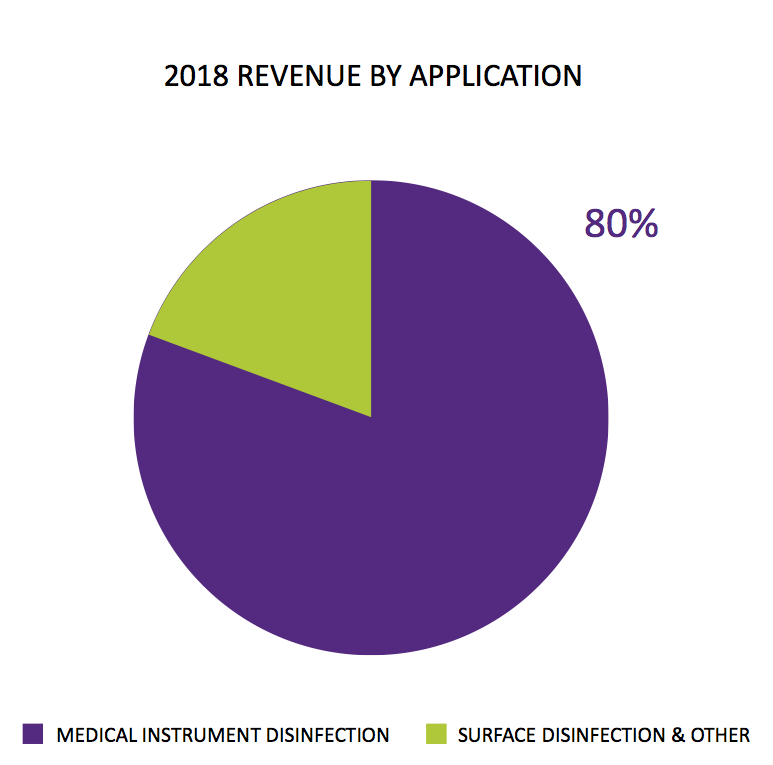

In particular, TSTL had said in July that 80% of 2018 revenue “by application” related to products that disinfected medical instruments:

I could not reconcile that 80%. The presentation accompanying these results indicated 75% of all revenue — and 83% of all human healthcare revenue — came from the ‘core’ patent-protected foams, wipes and solutions that disinfect medical devices:

I had assumed the 80% referred to all revenue, which led me to believe in July that sales of the group’s ‘core’ disinfectants had gained a very impressive 19% during the second half.

In actual fact, ‘core’ second-half sales gained only 4%:

| Revenue | H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | |

| Medical device disinfection (£k) | 7,279 | 7,822 | 15,101 | 8,180 | 8,410 | 16,590 | |

| Other (£k) | 2,469 | 2,703 | 5,172 | 2,547 | 3,083 | 5,630 | |

| Total (£k) | 9,748 | 10,525 | 20,273 | 10,727 | 11,493 | 22,220 |

Suffice to say, I will now treat TSTL’s open-day charts with a little more caution.

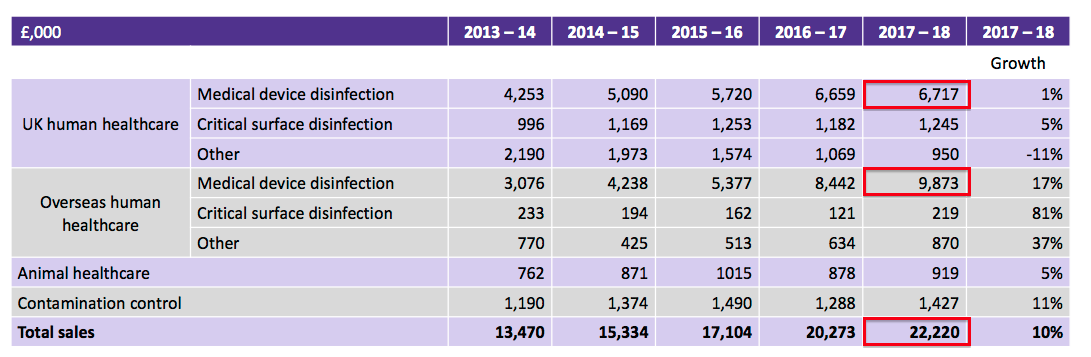

* Impressive new agreement with NHS sees prices rise by at least 10%

My sums from July suggested UK revenue had grown 6% during the second half. As such, I formed the impression that domestic sales of the ‘core’ medical-instrument disinfectants may have performed particularly well.

Alas, I was a little optimistic. UK progress during the second half was dictated mostly by extra sales of surface disinfectants (for cleaning hospital floors) and a variety of legacy products:

| UK revenue | H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | |

| Medical device disinfection (£k) | 3,478 | 3,181 | 6,659 | 3,604 | 3,113 | 6,717 | |

| Critical surface (£k) | 683 | 499 | 1,182 | 601 | 644 | 1,245 | |

| Other (£k) | 1,394 | 1,440 | 2,834 | 1,149 | 1,724 | 2,873 | |

| Total (£k) | 5,555 | 5,120 | 10,675 | 5,354 | 5,481 | 10,835 |

UK sales of the ‘core’ medical-instrument disinfectants fell 2% during the second half. I must confess, that progress does not look great.

At least management provided some background to the UK performance during the City presentation.

First, NHS ordering patterns are somewhat unpredictable.

Apparently, a month with, say, four Thursdays could see lower sales than a month with five Thursdays. Such order timings could then create a sales swing of a few £000k — and the difference between a positive and negative revenue change.

Of more significance was management owning up to “competitive churn” within NHS ultrasound departments. The trophon machines produced by Nanasonics (ASX: NAN) (see below) appear to have persuaded some hospitals to use fewer TSTL wipes.

I was told Nanosonics supplies the machines to UK hospitals for free, and that the firm charges only for the disinfectants. This Nanasonics presentation says:

“A broadening number of selling models each with different revenue profiles, including Managed Equipment Service (MES) in the UK, where a growing number of trophon units were placed with no upfront capital revenue.”

So the hospitals have entered into some sort of service/leasing agreement, which appears to be proving increasingly popular. The same Nanasonics presentation also says:

“MES program in the UK to continue gaining momentum — expect FY19 new unit growth of 75% to 100% over FY18, of which 90% will be under MES”.

Mind you, Nanosonics’s entire revenue from Europe, the Middle East and Africa was AUD$3m, or £1.6m, last year. So right now at least, TSTL’s lost sales could be relatively small.

Furthermore, TSTL’s management told me the trophon machines do break down… and that hospitals have to ensure TSTL’s wipes are stocked ready for such occasions.

In addition, the trophon machine disinfects only ultrasound probes.

As far as I know, there is no trophon-equivalent for instruments used within cardiology and ear/nose/throat departments. Some 70%-plus of such departments within UK hospitals currently use TSTL’s wipes and foams.

Probably the most encouraging UK snippet from the City presentation was news that the NHS supply chain had agreed to pay higher prices for TSTL’s products. Amazingly enough, TSTL has pushed through a one-off increase of between 10% and 15% for a new multi-year agreement.

When the price hike was mooted at July’s open day, I doubted whether TSTL could extract such higher payments from the NHS.

So perhaps this new agreement underlines the biocidal attractions of the group’s disinfectants to the health service. I understand the products covered by the price rise earned sales of £6m from the NHS last year.

* International distributors continue to blow hot and cold

Back in July I calculated second-half overseas revenue had grown by 11%, which I thought was “a little weak” given the 28% overseas advance witnessed during H1.

These results confirmed the 11% H2 increase:

| Overseas revenue | H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | |

| Medical device disinfection (£k) | 3,801 | 4,641 | 8,442 | 4,867 | 5,006 | 9,873 | |

| Other (£k) | 392 | 764 | 1,156 | 506 | 1,006 | 1,512 | |

| Total (£k) | 5,555 | 5,120 | 10,675 | 5,373 | 6,012 | 11,385 |

International sales of the ‘core’ medical-instrument disinfectants did not seem impressive during the second half — my sums indicate an 8% H2 advance.

Questions during the City presentation about the second-half overseas performance did not elicit a clear-cut management explanation. However, my calculations point to sluggish sales from TSTL’s third-party overseas distributors:

| Overseas revenue | H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | |

| Australasia (£k) | 1,075 | 1,520 | 2,595 | 1,529 | 1,537 | 3,066 | |

| China & Hong Kong (£k) | 649 | 463 | 1,112 | 519 | 552 | 1,071 | |

| Germany/Europe (£k) | 1,526 | 1,795 | 3,321 | 1,953 | 2,233 | 4,186 | |

| Total in-house (£k) | 3,250 | 3,717 | 6,967 | 4,001 | 4,322 | 8,323 | |

| Distributors (£k) | 943 | 1,627 | 2,570 | 1,372 | 1,689 | 3,061 | |

| Total (£k) | 4,193 | 5,405 | 9,598 | 5,373 | 6,011 | 11,384 |

I reckon TSTL’s German subsidiary — which also supplies other central and eastern European countries — lifted sales by 28% during H1 and 24% during H2.

Revenue from Australia and New Zealand (now reported as a single operation) gained 42% during H1, but only 1% during H2.

The first-half Australasian surge was due to the acquisition of the Australian distributor during the previous year. I would like to think this particular division continues to enjoy greater selling opportunities.

Anyway, total in-house international sales gained 14% during H2, compared with 4% for third-party distributor sales.

Management has previously mentioned its distributors blow hot and cold with their sales of TSTL products — often these third parties can be distracted by selling products for other companies.

For example, during 2017, overseas distributor sales dropped 16% during H1 and gained 5% during H2.

The City presentation also revealed a useful snippet on China.

Management said the Chinese operation is to refocus on selling TSTL’s flagship wipes and foams, and will lose other product sales of some £400k during the current year.

(Apparently the lady managing the Hong Kong subsidiary — which was taken in-house by TSTL during the year and is now “performing well” — has started to oversee China, too.)

* Expected Brexit “turbulence” is not management code for a future profit warning

TSTL’s results RNS declared:

“Brexit looms. Our response to the uncertainty surrounding this event is to build inventory of all component parts and finished products. We have advised our continental customers to increase their stockholdings over the coming months in preparation for possible disruption to the supply chain.

Based upon available advice, we believe that we will be able to CE mark our disinfectants and sell them within Europe irrespective of the outcome of the Brexit negotiation.

The only certainty is that we will experience turbulence this year and our normally predictable pattern of trade will be disrupted to some extent. Notwithstanding this near-term uncertainty, the outlook for the Company remains very positive.”

Certainly the phrase “we will experience turbulence this year” read to me as if the company was preparing the ground for a future profit warning. Management told me at the City presentation that my interpretation was definitely not the case.

Instead, management claimed it would be remiss not to mention the likelihood of Brexit causing some disruption — although the scale of any disruption is unknown at present.

Management reckoned the advice for continental customers to “increase their stockholdings” would not bolster the group’s forthcoming interim results through one-off ‘forward orders’.

Attendees at the City presentation were told that new revenue-recognition rules (IFRS 15) would “smooth out” any distortion. For example, if a customer buys some wipes during the first half for use during the second half, revenue and profit would be recognised during the second.

I can only presume TSTL will be told by the customer about such ‘forward orders’. IFRS 15 will not re-jig cash movements, and any pre-Brexit bulk purchases will naturally bolster TSTL’s bank balance.

For what it is worth, the CE mark mentioned within the results RNS should be obtained through a straightforward “paper exercise”.

* Choosing the FDA’s predicate option seems completely bizarre to me

The following text was the most disappointing part of the results RNS (my bold):

“We are preparing a submission to the FDA for Duo as a high-level disinfectant. The intended use patterns will be for intra-cavity ultrasound probes, nasendoscopes, and lastly certain ophthalmic devices. If successful, this will position us in three of the clinical areas in which we are most successful in other geographical markets. We expect to submit the application for 510(K) approval during the financial year ending 30 June 2019.”

Oh dear. Back in July, the directors had reiterated an FDA submission would be made by the end of December 2018.

A delay of six months may not seem long, but TSTL’s North American project has now become very protracted. My notes from 2015 recall management initially hoping FDA approval would be received by June 2017!

Anyway, the results RNS said:

“Our submission to the Food and Drug Administration for Duo is progressing well and we recently received very constructive feedback from the agency which will help guide us to its completion.”

Management admitted at the City presentation that the “constructive feedback” concerned the approval procedure TSTL had taken. Essentially TSTL had chosen the wrong option.

You see, the FDA has two application processes:

i) predicate, for products that possess a “substantial equivalence” to a product that is already approved by the FDA, and;

ii) de novo, for products that are essentially new to the FDA.

TSTL and its consultants had believed a (quicker and easier) predicate application was going to be sufficient. However, the FDA’s “constructive feedback” suggested a de novo application would be more suitable.

I have to say, the decision to even consider a predicate application seems completely bizarre to me.

That’s because past TSTL presentations have witnessed management bemoan how the FDA has never:

i) approved a chlorine dioxide disinfectant before (TSTL’s disinfectants are based on chlorine dioxide), and;

ii) approved a disinfectant foam before (TSTL’s initial products for approval are foams).

Even to me — a layman shareholder with no FDA knowledge whatsoever — attempting the “substantial equivalence” route was always going to be rather optimistic.

This predicate/de novo bungling underlines the seemingly botched leadership of this entire FDA application process.

A striking example of why the FDA project has taken so long lays within my notes from a February 2017 presentation.

I wrote then:

“I thought it a tad ominous that management used the adjective “tortuous” to describe the FDA’s demands for ensuring the disinfectants continued to work properly right until the end of their shelf lives.”

Well, 18 months later, and the 12-month shelf-life tests for the FDA will only finish in November! I am not sure why the shelf-life tests were so late in starting.

Anyway, the time between now and June 2019 will be spent converting the predicate application to a de novo application, and collecting yet more data.

Extra details required include an “ergonomic study”, which will prove how hospital staff can apply TSTL’s disinfectants correctly on medical instruments.

* Parker Laboratories and a mooted 17.5% royalty

An encouraging snippet from the City presentation was the revelation that TSTL would earn at least a 17.5% royalty from its US sales.

Parker Laboratories — TSTL’s sales, manufacturing and marketing partner in the States — is set to earn the same profit following a “balanced negotiation”.

TSTL’s directors reckoned a 17.5% royalty was the minimum level acceptable — as the rate reflected the margin enjoyed within the rest of the group.

I must confess, a 17.5% royalty agreement does seem very generous. Bioventix (BVXP) for example earns a 2% royalty from its antibodies. Let’s hope Parker has calculated its projections properly.

I should add that TSTL’s tie-up with Parker is perhaps the saving grace of this protracted US project.

To recap, Parker is the world’s leading supplier of ultrasound gel and offers TSTL a ready-made nationwide salesforce alongside FDA-approved manufacturing facilities. Parker also boasts a 60-year history of private, family ownership — suggesting the business takes a cautious, long-term outlook.

In fact, I would like to think the likes of Parker would only become involved with a small UK firm such as TSTL because the disinfectants concerned are actually quite good and are likely to sell quite well.

The following picture shows some early exhibition co-operation:

At least Parker appears confident TSTL’s disinfectant foams will eventually receive FDA approval.

TSTL’s executives told the presentation that the relationship with Parker was “very, very productive and harmonious”, and that Parker has even asked TSTL to manufacture some of its own low-level disinfectants.

I should add that TSTL’s executives continue to avoid giving any projections concerning the potential of the US market. Instead, management pointed investors to Nanosonics and its trophon machine to judge the Stateside sales potential.

Last year, Nanosonics earned revenue of AUD$54m — approximately £30m — from disinfecting ultrasound probes within North America:

For what it is worth, back in 2016, TSTL’s management said the US market could be worth £18m annually based on just the two disinfectants being submitted for FDA approval.

These days, not even the February 2018 guidance of commencing US sales during the year to June 2019 is mentioned.

* The ‘one-off’ write-off could have been deemed ‘exceptional’ — but wasn’t

These results contradicted another slide from July’s open-day presentation.

Attendees sitting in the summer marquee were shown this chart:

The US regulatory project apparently represented 3% of revenue — or £660k. However, these results said the cost was £500k — and management said all the costs were expensed during the first half (although the work was undertaken during both halves). This time last year, management was predicting US project costs of £800k for 2018.

I am not sure what to make of all of this — although I think the lower-than-expected US costs are due to conservative accounting rather than management massaging the books.

Whatever, operating profit before share-based payments and US regulatory costs were flat during the second half:

| H1 2017 | H2 2017 | FY 2017 | H1 2018 | H2 2018 | FY 2018 | ||

| Operating profit before SBP and US costs (£k) | 1,898 | 2,625 | 4,523 | 2,504 | 2,641 | 5,145 | |

| Share-based payments (£k) | (5) | (116) | (121) | (164) | (501) | (665) | |

| US costs (£k) | (200) | (300) | (500) | (500) | - | (500) | |

| Operating profit (£k) | 1,693 | 2,209 | 3,902 | 1,840 | 2,140 | 3,980 |

In my view, the notion of TSTL’s conservative bookkeeping is underlined by the accounting treatment of the firm’s Hong Kong purchase. A footnote in the annual report reveals:

TSTL did not deem such a ‘one-off’ write-off to be exceptional — although it easily could have been declared as such. Second-half operating profit gained 8% adjusted for this write-off, share-based payments and US costs.

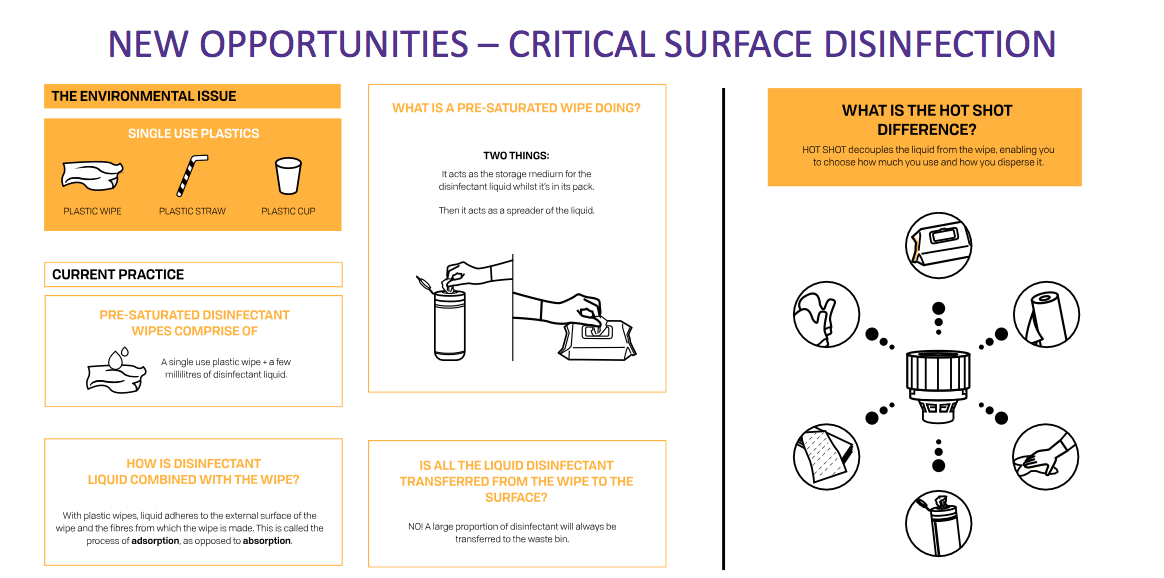

* Attempting to disrupt the 2p-per-wipe hospital-cleaning market

Management spent a lot of time extolling Hot Shot during the City presentation. Hot Shot is a new product for cleaning mattresses, bedside tables and other items that hospital patients come into contact with.

The presentation slideshow showcased the product’s environment-friendly credentials.

The aim is to “disrupt” the suppliers of ordinary cleaning wipes. “Good data” from the NHS supply chain apparently indicates 17 wipes are used per patient per day by the health service.

TSTL’s management claimed the cleaning wipes are only as effective as Flash or Dettol domestic cleaners and are sold to the NHS for as little as 2p each.

In contrast, Hot Shot would be much more effective as a hospital disinfectant — but would be sold to the NHS at 5p per dosage.

TSTL’s executives argued a premium product should be priced accordingly. The execs added that Hot Shot’s greater cost would be counterbalanced by the savings following fewer hospital infections — although the details of such savings were not revealed.

I can’t say I was convinced. In fact, TSTL’s management admitted a pilot project within four Sheffield hospitals had required an “immense” effort to change the working habits of staff from using the 2p wipes to TSTL’s Hot Shot.

Management did say at the presentation that if Hot Shot was priced at between 2.5p and 3p per dosage, a good margin would still be generated.

The executives also mentioned the group’s product for cleaning hospital floors earned revenue of £1.25m last year from 80 (20%) UK hospitals. The market size for disinfecting UK hospital floors is £20m.

* Substantial share-based payments may only be relevant if the share price reaches 350p

The headline figures within these results were blighted by a significant £665k share-based payment charge.

TSTL has some form with share options. I will not recount the whole sorry saga (you can read full details here) but during 2016, the executives and senior managers collected a £1m options windfall following — in my view — the dubious disclosure of trading information and of the option plan itself.

I must add that the directors have since told me they “strongly rebut” the allegations of a lack of disclosure and of them “dipping their fingers into the till”.

Anyway, the directors decided to award themselves more options during 2017.

This time the terms of the award were announced very clearly and the new scheme was actually put to a vote at last year’s AGM.

This latest option batch will come good only if:

i) the share price trades at 350p or more for at least three months before 30 June 2021, or;

ii) the company is acquired (which is standard for option schemes).

I like option plans that are based on share prices. You see, everyone knows exactly when the options have vested and shareholders can always take advantage of the higher price and sell.

True, a share price may not reflect the long-term value of a business. But then again, alternative measures such as earnings per share, return on equity, and so on, can all be fudged to trigger option payouts — and subside thereafter, too.

The drawback to TSTL’s new options is the 1p exercise price. So if the company is taken over for peanuts, the options will vest and management will receive some extra money — yet shareholders will be mugged.

TSTL’s management told me at the City presentation that the £665k option cost was represented by a £200k charge for general staff options and £465k for the new management scheme.

Note that accounting rules require a share-based payment charge to be applied even if these management (and any other) options turn out to be worthless (i.e. the share price never trades at 350p or more for at least three months before 30 June 2021).

As such, I would argue that considering only the cost of the general staff options might be more practical — at least until the share price approaches 350p and the management options stand any chance of vesting.

* Cash flow, net cash, operating margin and return on equity

Despite the questionable open-day charts, hefty share-based payments and inconsistent reporting of US costs, TSTL’s financials generally look in good shape.

Cash generation appears fine:

| Year to 30 June | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating profit (£k) | 1,819 | 2,541 | 2,568 | 3,902 | 3,980 |

| Depreciation and amortisation (£k) | 885 | 844 | 966 | 1,243 | 1,498 |

| Net capital expenditure (£k) | (1,084) | (1,045) | (889) | (959) | (1,450) |

| Working-capital movement (£k) | 524 | (606) | 467 | (530) | (520) |

| Net cash (£k) | 2,614 | 4,045 | 5,715 | 5,088 | 6,661 |

During the last five years, total expenditure on tangible and intangible assets has been matched by the combined depreciation and amortisation charged against earnings.

Meanwhile, the aggregate working-capital movement shows a £665k outflow of cash — which looks modest to me given operating profit has more than doubled to £4m-plus since 2014.

Following £1.8m spent on dividends, the year-end cash position improved by £1.6m to £6.7m. At the City presentation, management revealed the latest cash position to be £7.3m (equivalent to 16.7p per share). The balance sheet continues to carry no debt and no pension obligations.

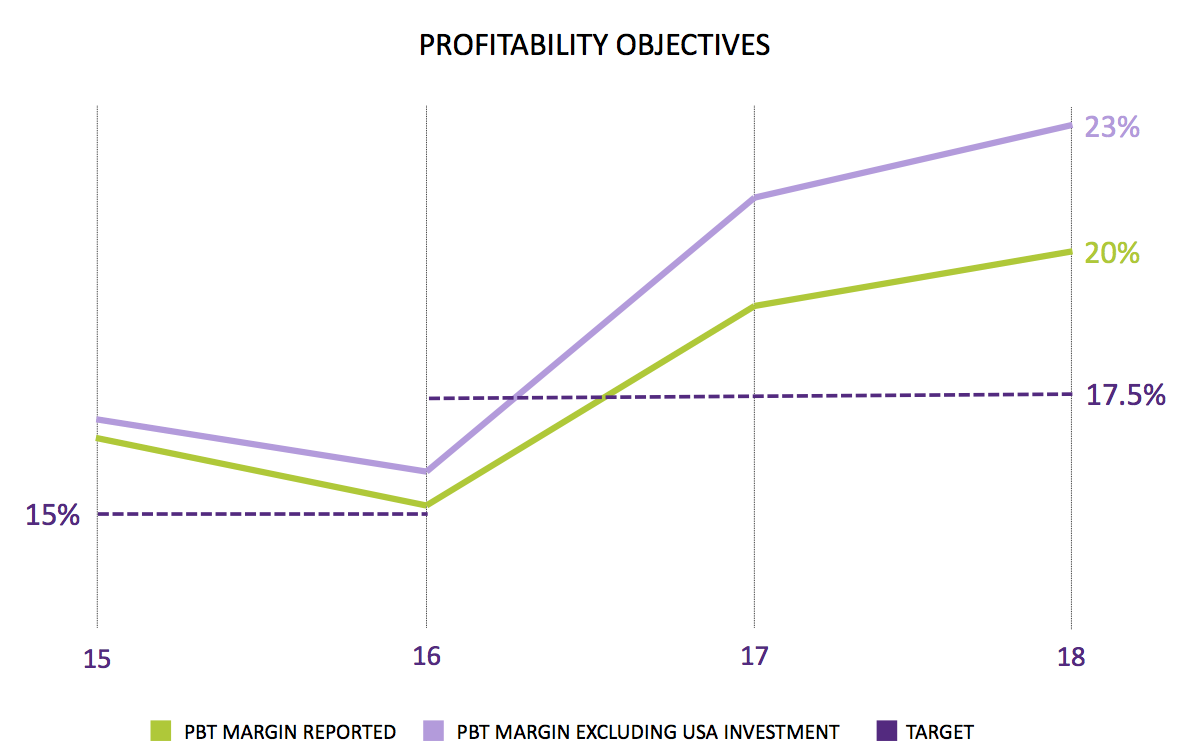

Elsewhere, TSTL’s operating margin remains at a level that underlines the competitive strength of the group’s patents, secret ingredients, proprietary know-how and independent scientific testimonies:

| Year to 30 June | 2014 | 2015 | 2016 | 2017 | 2018 |

| Operating margin* (%) | 13.5 | 17.0 | 15.8 | 21.7 | 20.2 |

| Return on average equity** (%) | 13.1 | 22.6 | 21.7 | 33.8 | 28.8 |

(*before US regulatory costs **adjusted for net cash)

Returns on equity remain at very acceptable levels, too.

Valuation

My previous TSTL write-ups have often mentioned the share price expecting great things from North America.

But with the share price now down to 220p, perhaps investors have cooled on the FDA application and subsequent US progress. I can’t blame them — I mean, the FDA application process has dragged on for three years now, while early US sales are still a few years away, too.

Anyway, taking TSTL’s 2018 pre-tax profit before share-based payments of £4,645k and:

* Adding £500k to adjust for US regulatory costs;

* Adding £196k to adjust for the early termination charge paid to the Hong Kong distributor, and;

* Subtracting £300k as a guess for share-based payments relating only to the general staff scheme (which is £100k more than management’s estimate to give some room for error)

…I arrive at an ‘underlying’ pre-tax profit of £5.0m. Applying the standard 19% UK tax rate gives earnings of £4.1m or 9.3p per share.

After subtracting the year-end 15p per share cash position from the 220p share price, my underlying P/E comes to 205p/9.3p = 22.

In the past I have ‘fairly valued’ TSTL excluding the US at 20 times earnings, which seems about right given the business enjoys a decent competitive position, repeat revenue, satisfactory financials and respectable growth opportunities elsewhere in the world.

On that 20x multiple, TSTL excluding the US could be worth 187p per share, or £82m. As such, the US project could be valued currently at 33p per share, or £15m.

Look forward long term, and that £15m might one day seem quite cheap.

As I mentioned earlier, Nanosonics generates revenue of £30m a year within North America for disinfecting ultrasound probes. FDA approval for Nanosonics’s trophon machine was granted during 2011.

Could TSTL’s disinfectants also generate North American sales of £30m seven years after FDA approval? To be honest, I do not know.

But I am sure my £15m North American valuation would become a lot larger if such sales were actually achieved.

In the meantime, the 4.58p per share dividend provides patient shareholders with a 2.1% income.

Maynard Paton

PS: You can now receive my Blog posts through an occasional e-mail newsletter. Click here for details.

Disclosure: Maynard owns shares in Bioventix and Tristel.

Dear Maynard

Having recently retired, with the idea of researching small companies in depth to make better investments, I found your note on Tristel very impressive. I thought I went into sufficient detail with my research, but you have inspired me to go far deeper.

I also attended the recent afternoon city presentation in Birchin Lane. I did have some considerations not mentioned in your note.

I found the arrangements concerning Mr Soler’s retirement, with an NED standing in for 1 year as Chairman, as being somewhat unusual. Surely a permanent Chairman could be recruited in the 6 months following the July announcement? Given that, as well as the fact that Mr Soler is a substantial shareholder, could it be Mr Soler is working behind the scenes to negotiate the sale of the company? Parker Laboratories would be have been an ideal candidate as a buyer, but they are not listed, and may not have the resources to hand.

I was shocked to hear that often a colposcope is used in the third world without adequate sterilisation between each patient. Effectively, the examination was potentially spreading the HPV virus, resulting in the very cervical cancer that the examination was intended to detect. It was therefore good news to hear that TSTL has invented a new type of colposcope that would work with a mobile phone, as well as being made safe with a Tristel sterilising wipe between each use. One can imagine in the future AI being used to cheaply interpret transmitted results.

Bioquell, a similar company that specialises in hydrogen peroxide cleaning systems, has a PE of 42. In that respect, TSTL doesn’t seem overvalued.

Although irritated that the director’s share option scheme charge effectively absorbed all the growth in EPS from normal shareholders, like you I will continue to hold TSTL, hoping that the US certification finally comes through, or even better, that an offer is received.

Hello Gerard,

Thanks for the comment. I am glad to be an inspiration :-)

(I should add that, to all the new visitors to my site, not all my posts are as in-depth as the one above!)

I spoke to Mr Soler at July’s open day. He said his retirement and recent share sale was due to a health issue last year. I have not really considered the arrangements for Mr Soler’s replacement, as to be frank, the qualities of the products are what stand out about the company (rather than the board). If you look at Mr Soler’s bio in the annual report, he has sold various ventures and I think TSTL will ultimately be sold as well. I certainly got the impression from Mr Soler that he would accept a premium bid today than wait for an even higher share price years down the road following good sales in the States.

I could not find any financial details on Parker, but I have the impressions it is a reasonably sizeable company. Bigger than TSTL at any rate. Yes, I would agree that Parker would be an ideal buyer. All speculation of course. Note that TSTL’s executives have been awarded options that vest only on a takeover, which is an unusual award and must tell us something about Mr Soler’s intentions (past or future).

TSTL’s wipes can clean the mobile colposcope, but the manufacturer of the device is in fact MobileODT, a private Israeli business in which TSTL owns a small stake and has board representation. Mr Soler and his chairman successor also own MobileODT shares. I think the opportunity here could be not insignificant. There is some social good, too.

Maynard

Many thanks for your very rapid reply!

I note from your blog that you are using MS Money to record all your transactions. I am a user of ShareScope, the sister system of SharePad, which along with SharePad, I am very happy with. ShareScope has an import facility for transactions; I’m sure your colleagues at Ionic could help you transfer your complete data set.

Hello Gerard,

I am catching up with some ‘work’ on a rainy Sunday afternoon after some half-term duties! Yes, I must admit I have not yet used the SharePad portfolio system. On my to-do list. Possibly an Xmas break task.

Maynard

Tristel (TSTL)

Publication of 2018 annual report

Full marks for TSTL for publishing its 2018 annual report on the day of the results RNS. Here are the points of interest:

1) Brexit and IFRS 15

The ‘principal risks and uncertainties’ section included a new part on Brexit:

It is useful to know that “sales expectations are expected to be achieved“.

The report refers to the new IFRS 15 revenue recognition rule that came into force this year:

My notes in the Blog post above refer to management believing that IFRS 15 will “smooth out” any Brexit ordering disruption due to this new revenue recognition.

However, the IFRS 15 note above says the new rule will not have a significant effect on the group’s revenue recognition. As such, I am not sure whether management’s comments about customers stock-building will cause any Brexit revenue distortion or not.

2) Corporate governance review

The annual report carried a long new section about corporate governance. Here is just the introduction:

There were two interesting snippets among what was pretty standard text.

The firms looks at “popular online blogs“:

I wonder if this Blog counts as popular.

There was also talk of a “protective moat“.

The last company in my portfolio to mention a “moat” was System1, which has since seen its “moat” breached. I hope the “moat” term has not become a ‘kiss of death’.

3) Director biographies

Adapting the new corporate-governance reporting regime prompted some awkward additions to the directors’ biographies:

4) Director pay

Details of the board’s pay are shown below:

Chief exec Paul Swinney saw his basic pay rise 24% while finance director Elizabeth Dixon saw her basic pay rise 20%. Both executives have seen their pay double during the last five years, although their current levels of pay do not appear excessive given the present size of the business and the group’s run of record results during the last few years.

I am not sure whether evaluating the board should include achieving a broker’s profit forecast:

Quite often such forecasts are effectively guided by the executives themselves.

I see the annual bonus award was not huge:

Executive wages will be held for the current year:

Options have been added to the list of remuneration policies:

I dare say that means options will become a regular feature of the board’s pay.

5) Gross margin

A little snippet on gross margins:

These rising costs are something to keep an eye on.

6) Cash management

A few years ago when announcing a couple of 3p per share special dividends, the board said it wanted at least £3m to be kept in the bank.

That £3m minimum remains the case:

However, cash at the 2018 year-end was approaching £7m.

There has been no management talk of special dividends of late, so I get the impression the cash hoarding may be to do with funding the US project.

7) Stock levels

TSTL’s stock control remains impressive:

Revenue gained 10% during the year, while year-end stock remained unchanged. Indeed, year-end inventory as a proportion of revenue has dropped from 18.1% to 10.3% between 2012 and 2018.

8) Trade receivables

There are no problems with late payers, which is pleasing given the NHS is the group’s largest customer (see below):

Trade and other receivables of £3,745k represent 17% of revenue, which compares well to the 16% to 24% seen since 2010.

Receivables that are ‘past due’ at 24% of the £3,745k are the lowest percentage since 2014 (17%) and 2012 (13%). The ‘past due’ percentage has in the past often topped 30%.

9) Largest customer

TSTL’s largest customer, the NHS supply chain, increased its purchases by an acceptable 4% during the year:

I mentioned in the Blog post above about a new NHS purchasing agreement. I therefore hope the 2019 annual report shows sales to the largest customer having advanced notably.

10) Employees

Here are the employee details:

Revenue per employee came to £179k, just shy of £183k for 2017 but well ahead of the sub-£150k figures TSTL used to produce. Total employee costs are influenced by management’s new option scheme, but total employee costs as a proportion of revenue, at 30%, remains in the 28% to 34% range seen since 2011.

The 11 extra additions to the marketing and admin teams are notable, as is the extra two people recruited for production. I am hopeful the extra sales people will drive sales further, and I like how extra sales do not require that many new production staff.

The following extract reads as if the £0.3m “exceptional performance-related bonus” is a one-off:

However, the staff collected a similar £0.4m payment during 2017 and a similar £0.55m payment during 2016.

I like the following extract:

Even better, long-time staff now enjoy 40,000 options rather than the 30,000 cited in last year’s report.

Maynard

Hi Maynard, Congratulations on the detailed update on two of your holdings. I find your posts more influential than any posts. It is an education to have the regular reviews.

I assume that you were able to buy at prices before they were inflated.

The more analysis you do on these two companies the more I question whether you would buy them now to the same proportion of your portfolio or whether you are tempted to do now what John Lee has done to some of his favourites.

Looking at your dividend leader direction and away from small value companies leaves me still pondering how we should judge which value companies have the continuing power to grow profit margins.

Colin

Hello Colin

Thanks for the comment. I hope you don’t find my posts too influential, given my portfolio’s rather modest progress during the last few years. My purchase prices are all listed on my portfolio page.

I doubt I would buy TSTL now to the same proportion of my portfolio. That proportion has grown over time with the share price. I can’t recall what proportion TSTL was at the time of my original purchases. I have not bought any TSTL for four years now. With SYS1, I have bought more shares earlier this year after buying originally in 2016. SYS1 is my smallest holding and I may increase my holding further once I have a better grasp of how potential clients view its services.

I am not sure what John Lee has done, but I assume he has top-sliced. Every time I have top-sliced my better performers, they have gone on to do better things and the share price has risen. That said, I should have sold SYS1 at £8-plus (did not sell any) and sold more TAST at 150p-plus (sold some).

My SharePad articles referred to dividend leaders, but right now I remain in my small caps and I dare say my shares will remain predominantly the same for the time being. I think judging companies and their margin power remains the same, too — you have to take a view on their own individual business qualities. That said, companies that have consistently enjoyed higher margins may be a good place to start — at least you should be able to discover what has sustained the margins in the past. And that may help you judge whether those same margins can be sustained in the future.

Maynard

Tristel (TSTL)

Acquisition & Board Appointment

I am catching up with this statement that was issued on 19 November.

I have mixed feelings. On the plus side, the deal seems logical. TSTL bought its Australian distributor during 2016 and that purchase appears to have worked out well. So this latest deal to purchase the TSTL distributor for Benelux and France could be another success. The downside appears to be price. The valuation does not appear to be a bargain.

Here is the full announcement:

——————————————————————————————————————

Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, announces the acquisition of Ecomed Services N.V. (Belgium), Ecomed Nederland B.V. (Netherlands) and Ecomed France SARL (France), together the “Ecomed Group”, and the appointment of the Ecomed’s CEO, Bart Leemans, to the Tristel Board as an Executive Director.

Ecomed Group

The Ecomed Group is Tristel’s exclusive distributor in Belgium, the Netherlands, Luxembourg (“Benelux”) and France. The Ecomed Group has achieved strong growth in recent years and is both cash generative and profitable. Its sole office and warehousing facility is in Antwerp, Belgium. The beneficial owners of the Ecomed Group companies are Bart and Jan Leemans (“the Vendors”).

The Ecomed Group’s sales during the twelve-month period ending 30 June 2018 were €3.07m of which €2.54m were of Tristel products. In the six months ended 30 June 2018 the Ecomed Group achieved EBITDA of €0.57m (unaudited) on revenues of €1.66m. At 30 June 2018, the Ecomed Group had net assets of €1.3m.

Highlights:

· The Company expects the acquired business to contribute incremental earnings in its current financial year of at least £250,000 after transaction and integration costs, and in subsequent years to be materially earnings enhancing;

· The Ecomed Group’s highly experienced management and sales team led by Bart and his brother Jan Leemans are to remain with Tristel. Bart Leemans joins the Tristel plc Board as an Executive Director;

· Bart and Jan Leemans are restricted from disposing of the Consideration Shares for a period of twelve months;

· The acquisition expands Tristel’s footprint of wholly-owned operations across continental Europe. Tristel now operates from subsidiaries in Belgium, Netherlands, France, Germany, Poland and Switzerland and has a 20% stake in Tristel Italia Srl. The Company’s salesforce increases to 18 across continental Europe and eight within the United Kingdom;

· Ecomed Belgium occupies a 14,000 sq ft office, warehousing and logistics hub in Antwerp which will be very beneficial to Tristel’s European operations post Brexit;

· The Consideration Shares are expected to be admitted to trading on the AIM Market of the London Stock Exchange on 22 November 2018.

Terms of the Acquisition

The consideration of €5.0m is to be paid upon completion, of which €3.4m is payable in cash and €1.6m from the issue of 573,860 ordinary shares (the “Consideration Shares”). The Consideration Shares will be issued at 242.7 pence per share, the average price during the thirty-day period to 15 November 2018.

Additional deferred consideration of up to €1.8m may be paid before July 2019 based upon final audited EBITDA for the calendar year 2018 exceeding €0.84m, and sales growth of at least 15% for the year ending 30 June 2019 being achieved. The deferred consideration will be paid in a combination of cash and ordinary shares with the allocation between cash and ordinary shares to be decided by the Vendors. If ordinary shares are issued to satisfy all or part of the deferred consideration they will be issued at 242.7 pence per share.

Board appointment

Bart Leemans founded the Ecomed Group in 2005 and has been CEO since that date. The Ecomed Group became Tristel’s distributor in Belgium in 2005; Ecomed Netherlands was incorporated in 2013 and Ecomed France in 2016. Before establishing the Ecomed Group, Bart Leemans had founded various e-commerce business, including Eccent NV which he successfully exited via a trade sale. He commenced his career with IBM Global Services.

Bart Leemans is the beneficial owner of 280,000 ordinary shares in Tristel plc.

Commenting on the acquisition and appointment, Paul Swinney, CEO Tristel, said: “We are very pleased to announce the purchase from Bart and Jan Leemans of their businesses in Benelux and France, and to welcome them and their highly experienced team into the Tristel group. This is an important strategic advance for our Company. France, in particular, is a very undeveloped market for Tristel. Sales of our products in the country are only a fraction of those that we achieve in Germany, a market of comparable size. With a direct presence and an expanded sales team we are targeting rapid growth in France and will continue to increase our market share in Belgium and the Netherlands.”

——————————————————————————————————————

For some context, TSTL acquired its Australian distributor during 2016 for AUD1.35m in exchange for sales of AUD3.0m during 2016. The sales were “almost entirely” related to TSTL products.

Now we have TSTL paying EUR5.0m for Benelux/France sales of EUR3.07m, of which EUR2.54m are TSTL products. So the multiple paid to TSTL sales has shifted from below 1 for Australia to 2 for Benelux/France.

Note that my sums do not include the possible additional deferred consideration of EUR1.8m:

“Additional deferred consideration of up to €1.8m may be paid before July 2019 based upon final audited EBITDA for the calendar year 2018 exceeding €0.84m, and sales growth of at least 15% for the year ending 30 June 2019 being achieved.”

The EBITDA hurdle for calendar 2018 looks straightforward, as EBITDA of EUR0.57m was scored during the first six months of the year. I get the impression the deferred consideration will be split into two parts — as I am not sure how a payment can be made “before July 2019” when the payment is dependent on sales for the year ending 30 June 2019.

So this Benelux/France deal looks expensive, at least compared to Australia.

Positives from the deal:

* a new executive director, who I hope can inject additional entrepreneurial drive into the business;

* ready-made and sizeable EU infrastructure post-Brexit;

* direct control of a significant distributor, which apparently could enjoy sizeable sales potential in France

Total TSTL sales to distributors during 2018 were £3.06m. Benelux/France sold EUR2.54m, which might equate to actual revenue to TSTL of £1.1m. So I think Benelux/France represented about a third of TSTL’s distributor income.

In the Blog post above, I noted distributors can blow hot and cold with sales, as sometimes they become distracted with non-TSTL products. This deal should lessen such fluctuations and ought to make TSTL’s overseas sales performance a little easier to interpret over time.

I calculate sales in Australia/New Zealand have climbed from £2.2m to £3.07m following the Australian purchase of 2016. Let’s hope Benelux/France can enjoy such a sales improvement under TSTL’s ownership to justify the price paid.

Maynard

Tristel (TSTL)

AGM statement

Here is the full text:

————————————————————————————————————–

Tristel plc (AIM: TSTL), the manufacturer of infection prevention, contamination control and hygiene products, will hold its Annual General Meeting today at 10am at Lynx Business Park, Fordham Road, Snailwell, Newmarket, Cambridgeshire CB8 7NY.

At the meeting Paul Swinney, Chief Executive Officer, will provide shareholders with the following update:

“We expect unaudited pre-tax profit (before share-based payments) for the first half to be no less than £2.2 million, compared to £2 million for the same period last year. The expected pre-tax profit figure takes account of the transaction costs arising from the acquisition of the Ecomed companies (‘Ecomed Group’) which we concluded last month; but it will include only one full month’s revenue and profit contribution from them. Our integration of these new French and Benelux businesses is progressing well.

“The Company is performing in line with management’s expectations and our United States regulatory approvals project is progressing as planned.”

Paul Barnes, Interim Chairman, will add:

“On behalf of my Board colleagues I would like to thank Francisco Soler, who steps down today after 25 years, for his many years of service to the Company, and to honour him with the title of Lifetime President. Francisco co-founded the business with Paul Swinney in 1993.

“I step into the role of Non-Executive Chairman for one year to oversee the Board’s transition at this exciting time in the Company’s development and will pass the reins over to a new Chair at next year’s AGM. We are making good progress in our search for new additions to our Board of Directors.”

The Company’s unaudited interim results will be announced on Monday 25 February 2019.

————————————————————————————————————–

TSTL’s AGM statements have usually underplayed the actual H1 result, so I suspect £2.2m might turn out to be £2.3m. Bear in mind, too, that these figures include regulatory costs associated with the US project. £500k was expensed during H1 last year, and I have no idea what will be spent during the current H1. No sales figure was given, too, which now appears to be the norm with these AGM statements after the options fiasco from a few years back.

Maynard

Tristel (TSTL)

Director appointment

Just catching up with this statement issued on 5 February. Here is the full text:

——————————————————————————————————————–

Tristel plc (AIM: TSTL), the manufacturer of infection prevention and contamination control products utilising proprietary chlorine dioxide chemistry, announces the appointment of Dr. Bruno Holthof to its Board as a non-executive director.

Dr. Bruno Holthof is the Chief Executive Officer of Oxford University Hospitals (“OUH”). Before OUH, he was CEO of the Antwerp Hospital Network from January 2004 until September 2015. Bruno Holthof is also Chair of the Board of Armonea, a European private care home provider.

Before becoming a CEO, he was a partner at McKinsey & Company. During this period, he served a wide range of healthcare clients in Europe and the United States and gained significant expertise in the areas of strategy, organisation and operations. He holds an MBA from the Harvard Business School and an MD/PhD from the University of Leuven.

Commenting on the appointment, Paul Swinney, CEO of Tristel, said: “We are delighted to welcome Bruno to our Board. Bruno has more than 10 years of board level experience on publicly listed companies. He also brings to the Board an in-depth knowledge and operational experience of healthcare systems in different markets. We very much look forward to working together.”

——————————————————————————————————————–

As non-exec appointments go, this one appears encouraging (i.e. not an accountant or ex-City adviser). An NHS Trust chief exec ought to be able to assist TSTL selling its disinfectants into UK hospitals.

The non-exec is in charge of four Oxfordshire hospitals (https://www.ouh.nhs.uk/about/trust-board/directors.aspx) and knows something about profitability (“During this period, he transformed ZNA into the most profitable hospital group in Belgium.“).

Hello Maynard,

Thanks for your interesting report on Tristel, a company which was in my portfolio from December 2016 until recently. I decided to sell as I am concerned that healthcare organisations are increasingly using disposable medical devices such as disposable endoscopes and that this will create a long term headwind for the company as these obviate the need for disinfection. As a private investor I do not have access to analyst reports on Tristel but I note from the internet that the market for disposable endoscopes is expected to grow at a CAGR of around 25% through to 2025 by which time it will become a multibillion dollar market led by the Danish company Ambu A/S. This must surely create a headwind for Tristel as I believe most of this growth will come from companies changing from re-usable to disposable devices. The US is leading the way in this change but other markets are following and I wonder if the company’s management would agree with my concerns over this trend.

Best regards,

John

Hello John

Thanks for the comment and apologies for the tardy reply.

I must admit I had never heard of disposable endoscopes until I read your post.

https://www.ambu.com/

https://www.ambu.com/about/corporate-info/investors/reports/reports-in-english

I see Ambu is a substantial quoted company that is very profitable. I am unclear as to what proportion of revenue is derived from single-use instruments, but the stats show the number sold has been growing strongly. So this is not a blue-sky business (and it also has FDA approvals (unlike TSTL!))

I guess the main issue for hospitals is the cost benefit.

I have found this https://onlinelibrary.wiley.com/doi/full/10.1111/anae.13011 which compares re-useable and single-use fibrescopes. The report says: “It appears cheaper to use single‐use fibrescopes at up to 200 fibreoptic intubations per year (a range commensurate with normal practice) even when the repair rate for re‐usable fibrescopes is low.”

So there is some evidence of this being a threat to TSTL. That said, the method of disinfection was not stated in that report.

Something I can’t quite fathom is how a single-use device can be sold cheaper than a re-usable device. What technically is different between the two? I suspect if the manufacturers of re-usable devices lose market share, they could always lower their prices to make the switch to single-use less cost-effective.

TSTL management has never mentioned single-use devices, so I will have to ask at the next presentation.

Maynard