***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

15 July 2023

By Maynard Paton

I love ‘owner managers’ — company bosses with significant shareholdings who live and breathe their business and want to build wealth for the long haul.

Typically entrepreneurs, the owner-managers who lead quoted companies do seem to think and act differently to standard chief executives.

A hefty investment complemented perhaps by substantial dividends should certainly focus the mind on fundamental business matters…

…versus more common executive considerations such as bonuses, LTIPs, adjusted earnings and career progression.

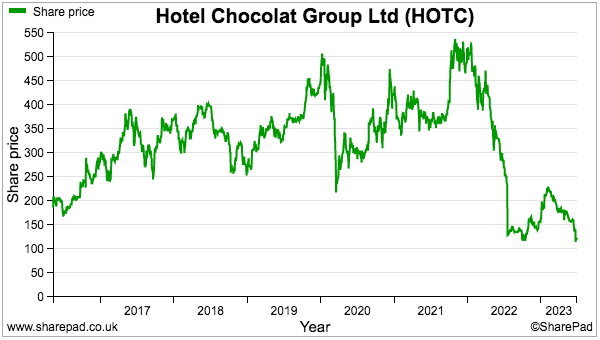

But seeking owner-managers is not a foolproof way to identify your next great multi-bagger. Hotel Chocolat provides a useful example of what can go wrong even with devoted founders in charge.

The upmarket chocolate retailer floated at 148p during 2016 and its shares reached 530p the other year…

…but a series of mishaps has since dragged the price down to 120p and raised questions about the board’s decisions and composition.

Let’s take a closer look.

Read my full HOTEL CHOCOLAT article for SharePad >>Maynard Paton