02 April 2025

By Maynard Paton

Happy Wednesday! I trust your shares have performed better than mine since the start of the year.

A summary of my portfolio’s first quarter:

- Q1 return: -6.5%*

- Q1 trades: 1 Top-up (Bioventix at £30) and 1 Sell (Tristel at 352p).

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees, paid dividends and cash interest)

I will do well to catch up with the FTSE 100 during 2025. The blue-chip index has powered 6% higher during this Q1, outperforming every one of my holdings. Indeed, seven of my shares declined despite the rising market.

Newsflow from my holdings has been mostly unremarkable, as demonstrated by the modest dividend improvements or unchanged payouts at Bioventix, City of London Investment, Mincon, FW Thorpe and M Winkworth. S & U has meanwhile continued to trim its dividend following adverse regulatory matters.

The subdued progress has left most of my holdings trading at prices first seen during 2017 or before, with their ratings the lowest for years. I am not short of top-up ideas.

Picking winners has certainly become harder. A quick check on ShareScope reveals only 191 of the 552 FTSE All-Share constituents — 35% — delivered share-price gains during this Q1. Over the last three years, the proportion is a woeful 33%.

You may not be surprised to learn that picking AIM winners has been even harder. During the last three years, just 20% of AIM-traded shares have moved higher.

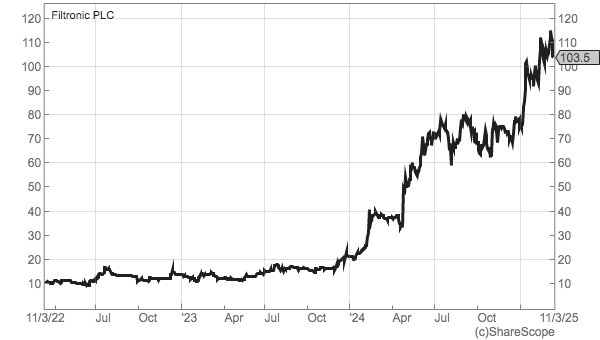

Nonetheless, buyers remain out there for the right opportunities. I wrote about Filtronic recently, mostly to remind myself that multi-baggers do still exist!