***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

17 October 2025

By Maynard Paton

I can’t be the only investor who likes to collect a reliable dividend.

Hence this revisit to an old screen that pinpoints companies boasting a long-running payout, a meaningful yield and respectable prospects.

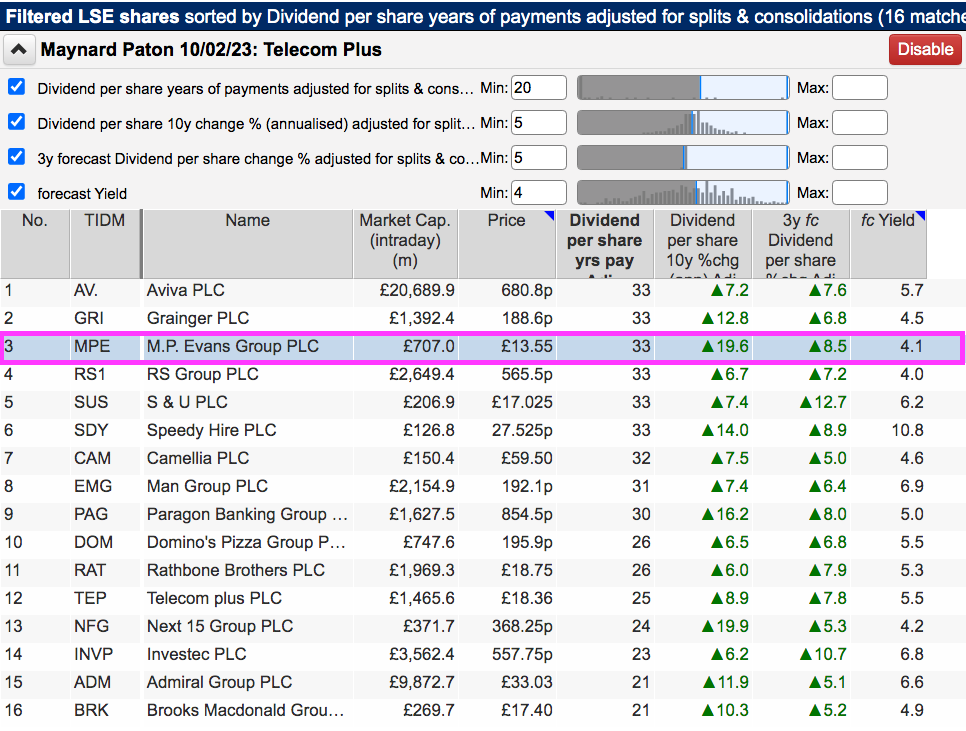

The exact criteria I redeployed for this search were:

- A history of dividend payments spanning at least 20 years;

- A 10-year dividend growth record of 5% or more;

- A minimum forecast three-year dividend growth rate of 5%, and;

- A forecast dividend yield of at least 4%.

I applied the screen the other day and ShareScope returned 16 matches:

I selected MP Evans primarily because the company has never cut its dividend during the last 33 years:

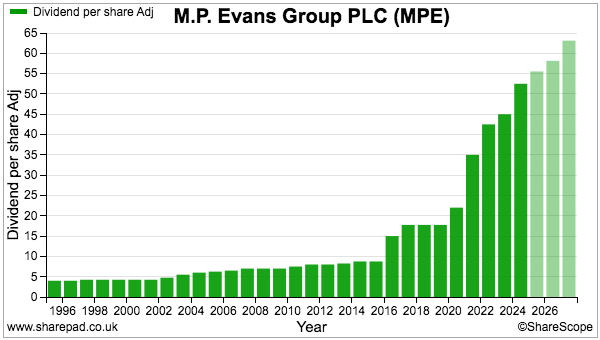

The payout has in fact advanced by a near-20% CAGR during the last decade, while future income growth also appeared very reasonable.

Let’s take a closer look.

Read my full MP EVANS article for ShareScope >>Maynard Paton