26 August 2022

By Maynard Paton

Results summary for Bioventix (BVXP):

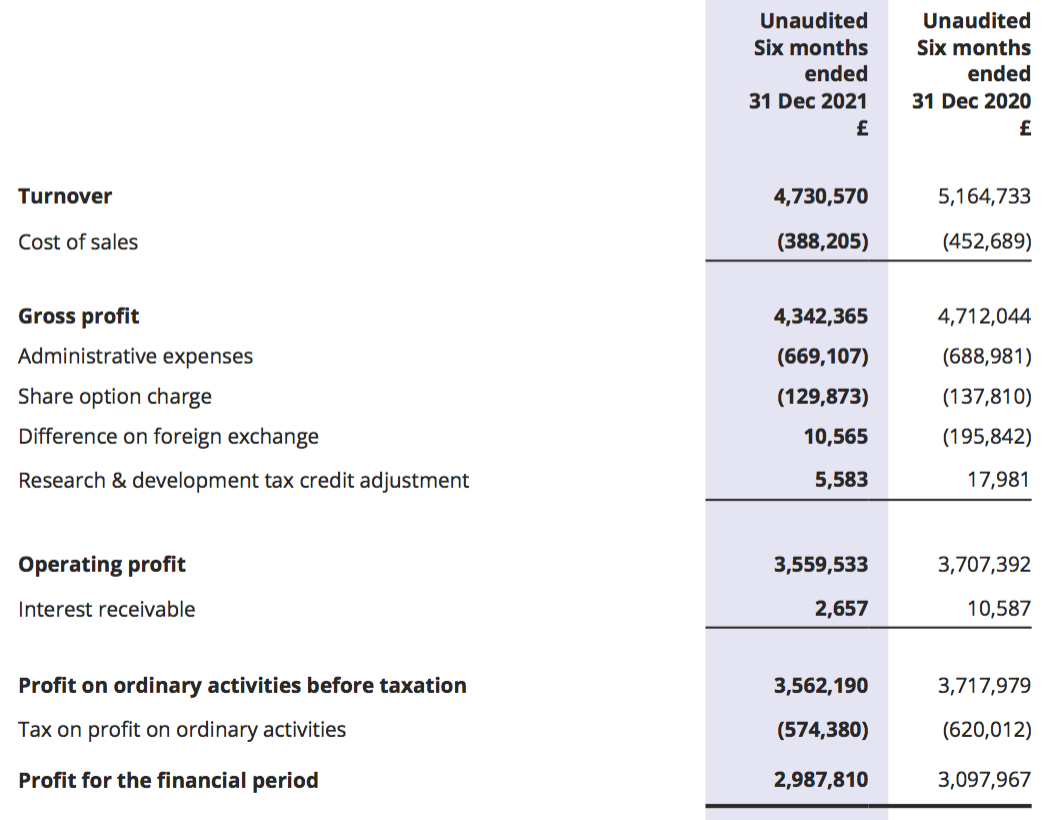

- An unspectacular H1 performance, albeit accompanied by a 21% dividend lift, after further pandemic disruption left revenue down 8% and adjusted profit down 9%.

- Muted progress from vitamin D and other established antibodies continues to leave near-term growth dependent on the fast-selling troponin product.

- The “exciting” potential of a Tau biomarker alongside the BVXP website selling pyrene test kits suggest positive developments within the research pipeline.

- Net cash at £5m is the lowest for six years, and combined with standstill earnings seems likely to reduce the size of any FY 2022 special payout.

- Troponin’s finite income and a resultant sum-of-the-parts valuation do not indicate an obviously compelling £33 share price. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own BVXP

- Results summary

- Revenue, profit and dividend

- Vitamin D

- Troponin and other antibodies

- Pipeline developments

- Financials

- Valuation

News links, share data and disclosure

News: Interim results and presentation for the six months to 31 December 2021 published 28 March 2022

Share price: £33

Share count: 5,209,333

Market capitalisation: £172m

Why I own BVXP

- Develops diagnostic blood-test antibodies, direct competition for which is limited due to the necessary scientific innovation, protracted regulatory testing, onerous switching procedures and ‘captive’ hospital end-customers.

- Boasts founder/entrepreneurial chief exec who has overseen an attractive growth record, retains an 8%/£14m shareholding and has declared six special dividends.

- Employs ‘scalable’ royalty/licensing model that requires few employees and leads to terrific margins, generous cash flow and high returns on retained profits.

Further reading: My BVXP Buy report | All my BVXP posts | BVXP website

Disclosure: Maynard owns shares in Bioventix. This blog post contains SharePad affiliate links.

Results summary

Revenue, profit and dividend

- These H1 2022 results were never going to be amazing after the preceding FY 2021 statement carried a somewhat muted outlook:

“We are pleased with our financial results for the year considering the continued negative impact of the global pandemic. The core business is linked to routine testing at hospitals around the world and this has undoubtedly been affected by the COVID-19 pandemic. The timing of a return to normality is uncertain but when it does, we expect our business will revert to an established trajectory, albeit without the income from NT-proBNP which ceased from July 2021“

- Ongoing pandemic disruption — evidenced by fewer hospital patients undertaking routine blood tests — alongside the cessation of certain product income did indeed hamper the performance.

- Revenue fell 8% while reported operating profit fell 4%, or 9% adjusted for the effect of foreign-exchange movements (see Financials).

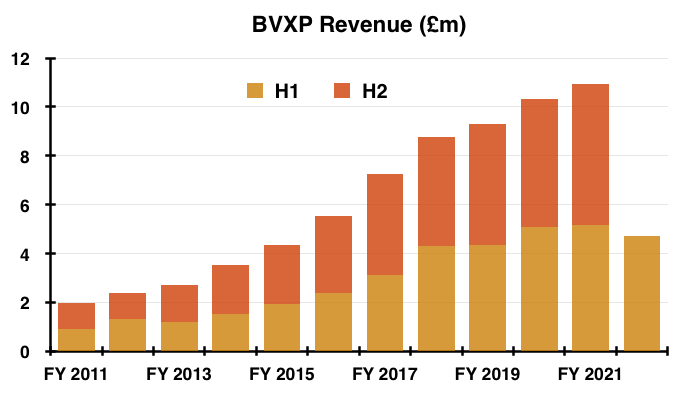

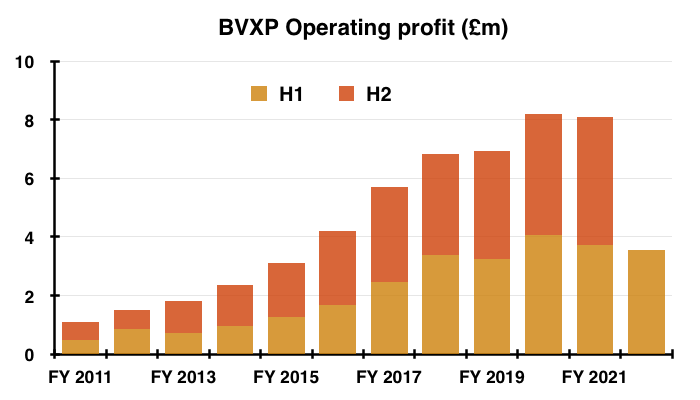

- This H1 performance was the first since 2013 during which both profit and revenue declined versus the prior H1:

- The H1 progress contrasted to the preceding H2, which witnessed BVXP’s best-ever six-month performance for both revenue and profit.

- BVXP claimed the loss of product income amounted to £600k:

“As we have previously reported, the contractual payment period relating to our NT-proBNP sales terminated in July 2021. This resulted in a reduction of our revenue of approximately £600k for the period which masked a steady performance for the remainder of the business.“

- H1 revenue would have climbed 3% had BVXP collected extra revenue of £600k.

- BVXP said the pandemic disruption had continued during this H1:

“The global pandemic has continued throughout the reporting period and has affected the activity within diagnostic pathways in hospitals and clinics around the world to which our business is intrinsically linked. The dynamics of the pandemic remain difficult to predict but when it eases, we believe our robust core business will respond accordingly.“

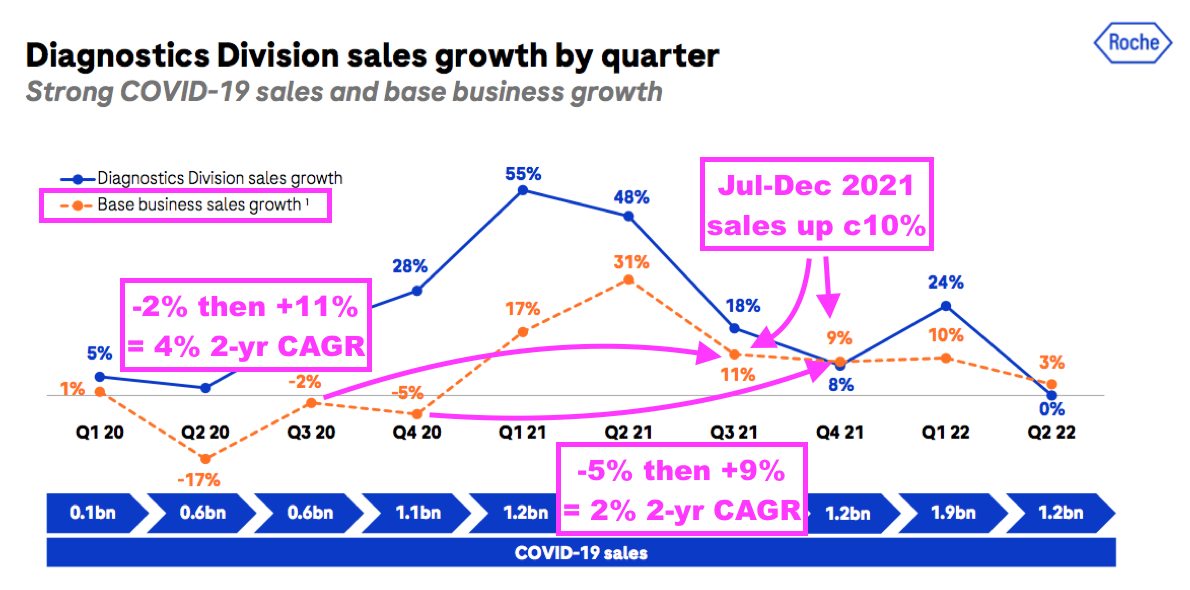

- Mind you, a Q2 2022 update from Roche showed its base diagnostic sales (i.e. excluding income from Covid-19 tests) recovering by approximately 10% during the same six months:

- Roche is the world’s largest in vitro diagnostic (IVD) company and is as good a benchmark as any to judge demand for the type of blood-test antibodies that BVXP develops.

- Roche’s 10% sales growth looks better than BVXP’s 3% improvement (adjusted for lost product income of £600k).

- But for the previous year, BVXP’s H1 revenue gained 1% when Roche’s base diagnostic sales declined by approximately 3%.

- Progress at Roche and BVXP seems to even out over the two years since the pandemic emerged.

- Between June-December 2019 and June-December 2021, Roche’s routine-diagnostic sales have compounded by an approximate 3% average while BVXP’s revenue (adjusted for lost product income of £600k) has compounded by an approximate 2% average.

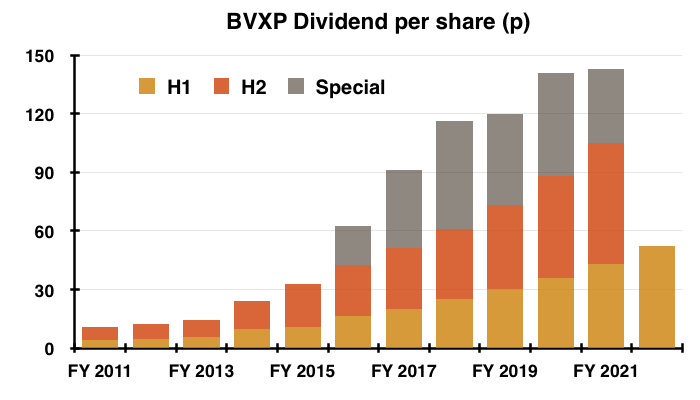

- The only H1 headline number moving in the right direction and required no adjustments was the dividend, which was lifted a very welcome 21%:

- The payout improvement bodes well for the H2 dividend, but the size of any further special dividend may not be as large as those enjoyed during previous years (see Financials).

- Cash finished the half at £5.1m — the lowest level for six years — and did not leave much surplus money beyond BVXP’s £5m “comfort” balance:

(FY 2021): “Our current view continues to be that maintaining a cash balance of approximately £5 million is sufficient to facilitate operational and strategic agility both with respect to possible corporate or technological opportunities that might arise in the foreseeable future and to provide comfort against the ongoing impact of the pandemic and any economic uncertainty arising from it.“

Vitamin D

- BVXP frustratingly discloses individual product revenue only within its FY statements and not within its H1 statements.

- But research notes published by BVXP’s house broker do include estimated figures for H1 product revenue, which presumably have been endorsed by BVXP and therefore give some indication of particular antibody progress.

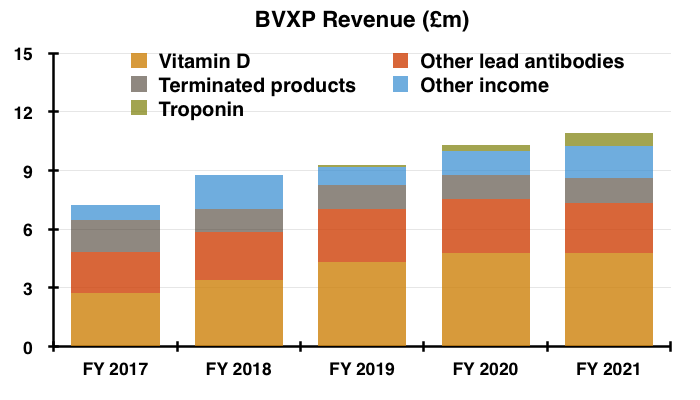

- The preceding FY 2021 results showed BVXP’s vitamin D antibody remaining by some distance the group’s best-seller at 44% of revenue:

- That 44% proportion would have been 50% had the product revenue lost during this H1 had also been lost during FY 2021.

- BVXP hinted vitamin D sales had stagnated or reversed during this H1:

“As reported previously, the growth rates for our vitamin D antibody sales were not expected to match those seen in recent financial years and a plateau in the downstream global vitamin D assay market had been anticipated. Sales associated with assay formats using larger quantities of antibody per test suffered more as price erosion in downstream markets puts pressure on costly “antibody-hungry” products“

- BVXP’s broker reckoned H1 troponin sales were flat at c£2.6m and represented 55% of total revenue.

- BVXP issued warnings of vitamin D income “plateauing” within its FY 2017, FY 2018 and FY 2019 results, when the antibody was delivering 20%-plus per annum revenue growth.

- Management has in the past claimed the ‘plateauing’ of vitamin D growth to mean the rate reducing to between 5% and 10% — to match the projected expansion of the wider antibody market.

- But vitamin D sales staying flat for FY 2021 and suffering some “price erosion” during this H1 suggest 5-10% annual future growth is somewhat optimistic (at least for now).

- BVXP’s archives reveal development on the vitamin D antibody started during 2008 and revenue was first earned during 2011:

“One of the most exciting developments for the company has been the vitamin D project which has been the subject of intensive internal R&D since the summer of 2008.

A leading antibody called vitD3.5H10 has moved into large scale manufacturing at the company in order to supply increased quantities of antibody required for our customers’ own R&D use. Revenue from the supply of this product has been generated for the first time during the period.“

- Going from revenue of zero to £4.8m within ten years gives some idea of the prospects for BVXP’s newish troponin antibody.

Troponin and other antibodies

- The preceding FY 2021 statement reminded shareholders that BVXP’s near-term progress remained dependent on its troponin antibody:

“Over the next few years, the commercial development of the new troponin assays will have the most significant influence on Bioventix sales. There are currently no antibodies in the future pipeline that are comparable to our troponin products in potential value and the ability to influence revenues in the next few years.”

- Development work on troponin — an element used to detect potential heart attacks — started during 2006 and the antibody first generated sales during FY 2019.

- BVXP said troponin income during this H1 “grew significantly once again“:

“Sales relating to troponin antibodies grew significantly once again during the period. The continued roll-out of high sensitivity troponin tests provides further encouragement for our future sales in this area.“

- Troponin sales doubled during FY 2021, and maybe they doubled once again during this H1.

- BVXP’s broker reckons H1 troponin revenue advanced 79% to £500k and now accounts for 11% of total revenue.

- Troponin revenue came to £680k during FY 2021, and coincidentally requires the 79% advance estimated by the house broker to reach the “entirely plausible” £1.2m for FY 2022.

- BVXP’s broker reckons troponin income could grow to between £3m and £3.5m by 2025.

- BVXP sadly did not refer to its five other antibodies within this H1 statement.

- Income from these five products — used for testing thyroid function, fertility and drug abuse — represented 23% of revenue during FY 2021.

- Revenue from the five antibodies declined by 6% between FY 2019 and FY 2021 as the pandemic disrupted their usage.

- BVXP’s broker claims the five antibodies improved their collective sales by 2% during this H1 to surpass £1.5m.

Pipeline developments

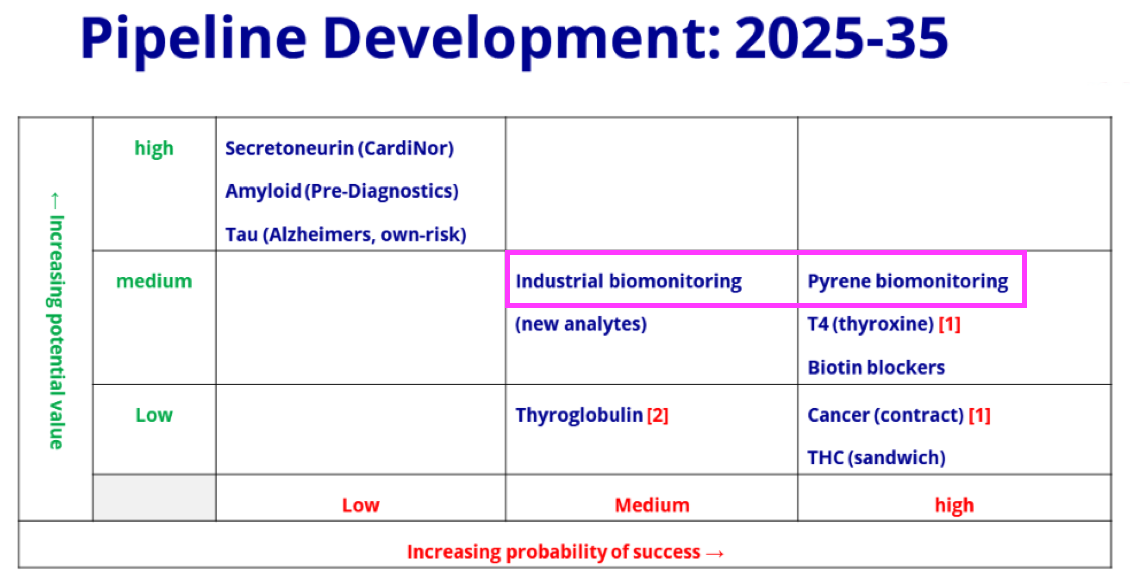

- Modest growth from BVXP’s established antibodies alongside a finite income from troponin places significant importance on the company’s research activities.

- The pipeline front-runners appear to be projects concerning Alzheimer’s disease and exposure to industrial pollution.

- BVXP referred to the “exciting potential” of its work on Tau proteins for dementia research:

“Since the summer of 2020, a considerable amount of our laboratory resources has been focused on the Tau biomarker which shows exciting potential in neuropathological diseases including Alzheimer’s.

Some new antibodies were made during 2021 and we have more antibodies in the development pipeline for 2022. The antibodies have been and will continue to be subjected to assay development and validation using clinical samples at the world-renowned laboratory of Kaj Blennow and Henrik Zetterberg at the University of Gothenburg.

We are delighted with the continuing development of this collaboration and look forward to the generation of new data with our partners during 2022.”

- BVXP does not use the word “exciting” that often. The previous appearance occurred within the H1 2018 statement and concerned troponin:

“In October 2017, we conveyed our expectation that the commercial development of this exciting new product would not gear up until calendar year 2018 and this expectation has been manifest in the reporting period.“

- Another previous appearance occurred within the FY 2011 results about vitamin D:

“One of the most exciting developments for the company has been the vitamin D project which has been the subject of intensive internal R&D since the summer of 2008.”

- The implication perhaps is BVXP’s infrequent use of “exciting” signals the Tau work having genuine commercial possibilities.

- Mind you, BVXP’s FY 2017 statement described the work with Norwegian collaborators CardiNor and Pre-Diagnostics as “exciting“:

“On a longer term perspective, we continue to work with our partners in Norway on the secretoneurin (CardiNor & heart diagnostics) and amyloid projects (Pre-Diagnostics & dementia). We have made exciting antibodies to contribute towards the scientific development of these projects and we look forward to developing the science of these long term projects over the coming years.”

- Five years on and both Norwegian projects remain in development as BVXP currently awaits further “news and critical data”.

- “Exciting” projects may therefore take some time to become viable products (if they ever do).

- Working with the “world-renowned laboratory of Kaj Blennow and Henrik Zetterberg at the University of Gothenburg” sounds promising.

- Professors Blennow and Zetterberg appear to be leading authorities on Alzheimer’s research (here, here, here and here), and I would like to think their laboratory would only get involved with BVXP’s antibodies if the antibodies showed genuine promise:

- BVXP continues with its pollution monitoring tests:

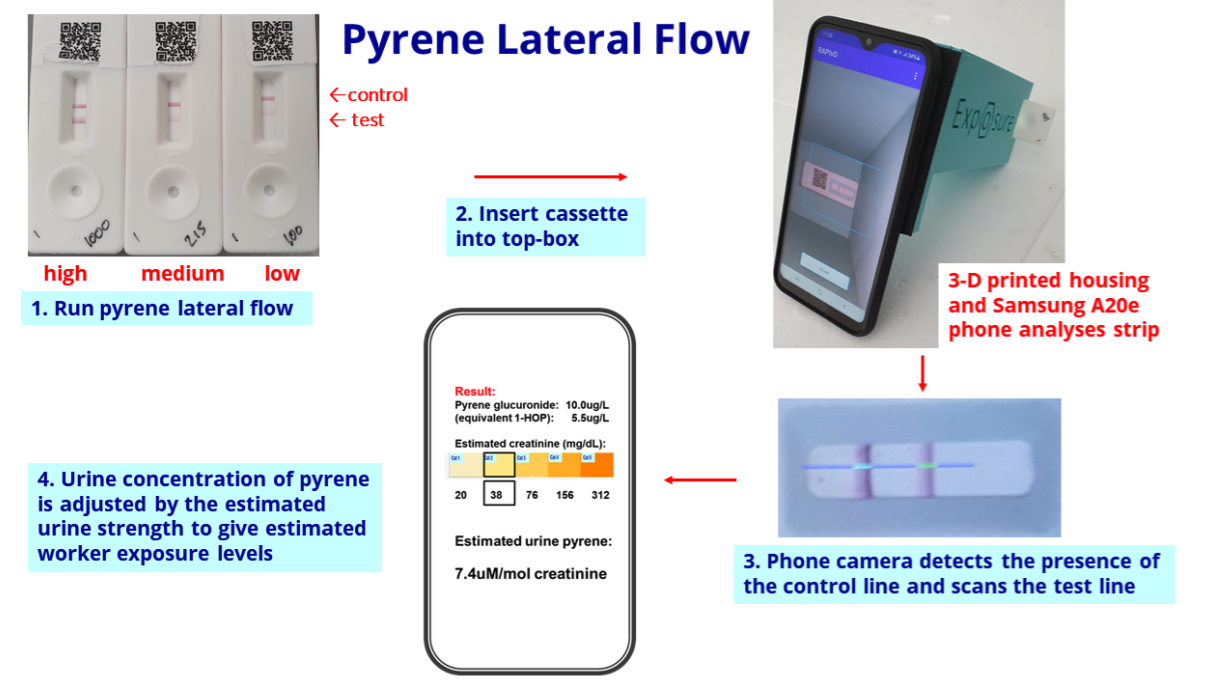

“We are pleased with the continued development of our industrial pollution exposure assay. Our prototype lateral flow test for pyrene in industrial worker’s urine featured in a field trial at a UK industrial site during Q4.2021. The results from the device and phone-app correlated relatively well with results from parallel samples analysed by a central health and safety laboratory. Important feedback from the trial was gained and has prompted a minor modification of the phone-app camera reader system and we plan further trials in 2022.“

- BVXP referred to both “industrial pollution” and “pyrene” within this H1 statement, which is a little confusing as industrial biomonitoring and pyrene biomonitoring were separate projects on the FY 2021 pipeline grid:

- The pipeline grid was not included within the H1 presentation, and presumably the grid layout has not changed during the intervening six months.

- But BVXP’s website has changed. The home page now showcases the pyrene test kits:

- Trials of the pyrene tests have presumably shown good results and the kits appear available to buy for research purposes:

- The pyrene test works by examining a urine sample through a mobile phone:

- Manufacturing the pyrene kit is unlikely to enjoy the same wonderful economics as selling 15-20 grams of antibodies a year (point 1) (see Financials).

- Among BVXP’s other pipeline products, the tetrahydrocannabinol (THC) test currently seems the most likely to show some monetary promise:

“Our new THC/cannabis antibody “sandwich” format which has been in development for approximately two years is now successfully working in a number of customer products and is moving into commercial development thereby adding to overall revenues in the future.“

- Exactly which of the pipeline products (if any) eventually make it to market remains anyone’s guess. Development of the troponin antibody took more than ten years before its commercial launch.

- BVXP has said since FY 2019 that its pipeline products could influence revenue beyond 2025 — which is now less than three years away.

Financials

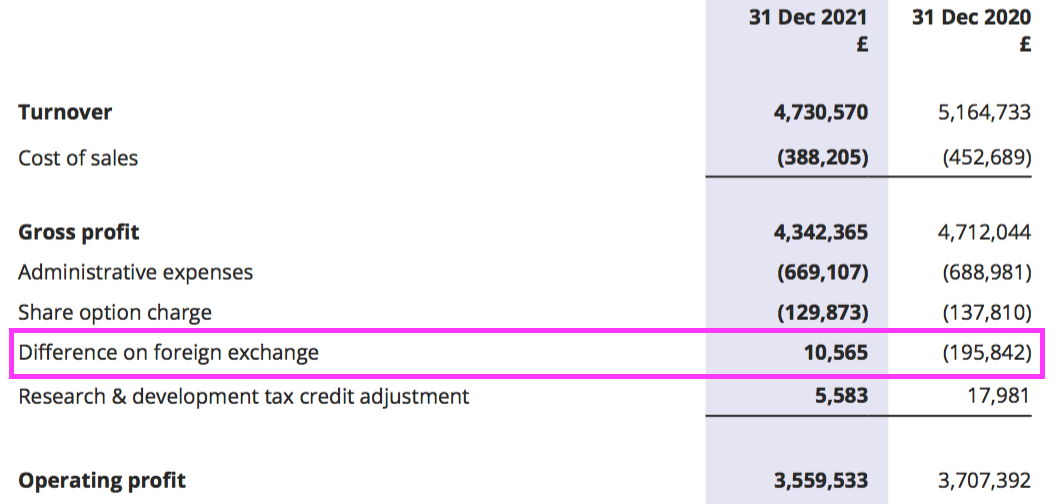

- Foreign-exchange gains/losses once again interfered with reported operating profit:

- The foreign-exchange gains/losses arise when customers pay BVXP more/less than what was initially recognised as revenue because of subsequent exchange-rate movements.

- Such foreign-exchange gains/losses can be significant for BVXP because the bulk of group income is:

- Denominated in USD or EUR, and;

- Received every six months (which amplifies the accounting impact of currency movements).

- The gains/losses can affect BVXP’s short-term performance but have not been a significant long-term influence.

- Between FYs 2017 and 2021, aggregate foreign-exchange gains/losses came to a negative £262k versus aggregate revenue of £47m and aggregate reported operating profit of £36m.

- The foreign-exchange gains/losses have made little difference to interpreting BVXP’s operating margin.

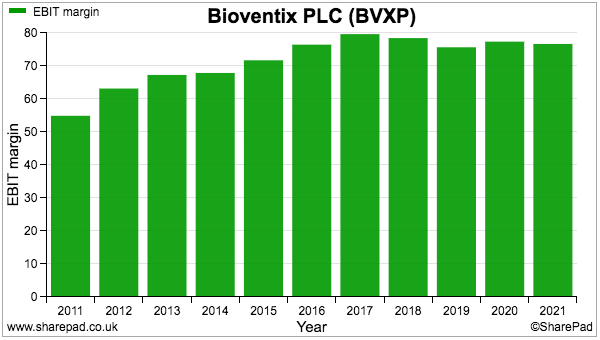

- BVXP typically converts 70% or more of revenue into profit, which underlines the wonderful economics of collecting royalties and license fees from successful antibodies:

- Some 75% of revenue was converted into profit for this H1.

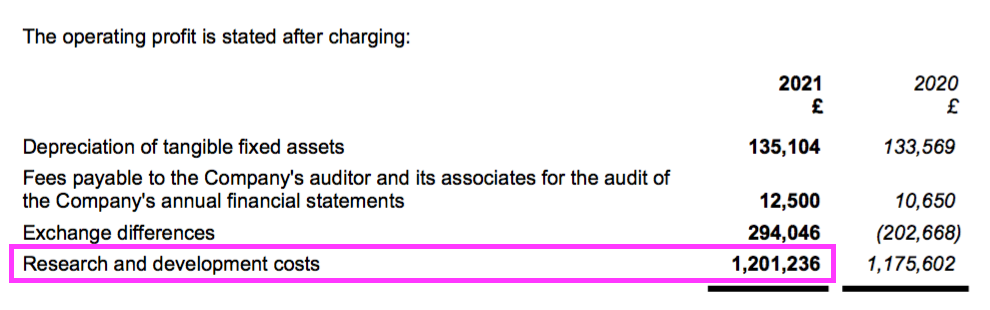

- Bear in mind BVXP’s reported margin is lowered by R&D work that is all expensed as incurred and at present generates no associated revenue.

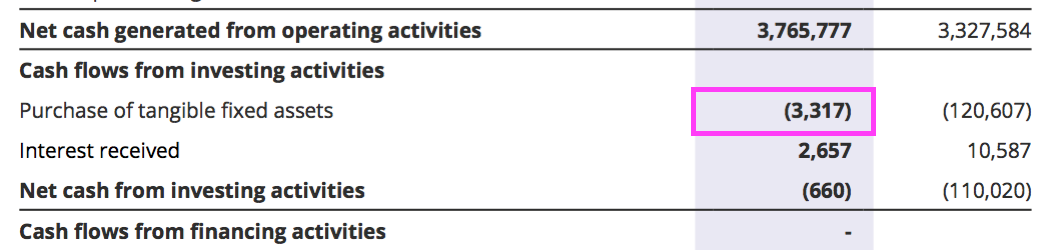

- The super margin reflects BVXP’s low cost base. The 2021 annual report (point 12) disclosed employing only 17 staff and this H1 statement revealed capex amounting to just £3k:

- The tiny capex allowed earnings of £3.0m to translate into free cash of £3.8m, which in turn helped fund the preceding year’s H2/special dividends of £5.2m.

- BVXP’s cash position therefore finished the six months £1.4m lighter at £5.1m, which is the company’s lowest bank balance since H1 2016 (£4.6m).

- The balance sheet carries no bank debt and no pension complications.

- BVXP has declared special dividends during each of the last six years, but the prospects for a seventh special do not appear as great as they once were.

- This H1’s 52p per share dividend will cost £2.7m, which will reduce the net cash position to £2.4m. A repeat of this H1 performance during H2 would then increase that £2.4m cash position by £3.8m to £6.2m.

- The £6.2m cash position exceeds the aforementioned £5m “comfort” buffer by £1.2m.

- The £1.2m difference between my £6.2m cash guess and the £5m buffer equates to 23p per share — and compares to the 20p, 40p, 55p, 47p, 53p and 38p per share special dividends declared since FY 2016.

- Unless BVXP enjoys a bumper H2, any seventh special dividend could be among BVXP’s lowest.

- Indeed, a 21% lift to the H2 dividend to match this H1’s 21% advance would supply a total 127p per share ordinary payout that would cost £6.6m.

- Doubling up this H1’s free cash flow gives £7.5m — leaving £0.9m spare if BVXP were indeed to pay total FY 2022 ordinary dividends of £6.6m.

- £0.9m equates to just 18p per share, and is further evidence perhaps of little leeway to fund a major special dividend for FY 2022.

- BVXP has a commendable history of returning the vast majority of earnings to shareholders. Between FYs 2016 and 2021, BVXP has declared aggregate earnings of £34m while paying cash dividends of £31m.

- The £610k book value of BVXP’s investments in pipeline-development partners Cardinor and Pre-Diagnostics still looks understated.

- Intuitive Investments (IIG) paid £125k for 1.8% of Cardinor during March 2021, which implies Cardinor was then worth almost £7m. IIG continues to hold its Cardinor stake at cost.

- This 2018 document from the Cardinor website indicates BVXP was then a 21.5% Cardinor shareholder, and suggests BVXP’s investment could be worth up to £1.5m based on IIG’s purchase.

- This 2020 document from the Pre-Diagnostics website indicates BVXP is a 7.5% Pre-Diagnostics shareholder, the investment cost of which I think is approximately £0.4m.

Valuation

- BVXP’s outlook did not appear too awful:

“In conclusion, there have been challenges over the last two years but we continue to have confidence in the strength of our core business and the outlook for the full year. We remain optimistic about our troponin revenues and the success of these high sensitivity troponin products around the world and we look forward to reporting further progress in the second half of the year.“

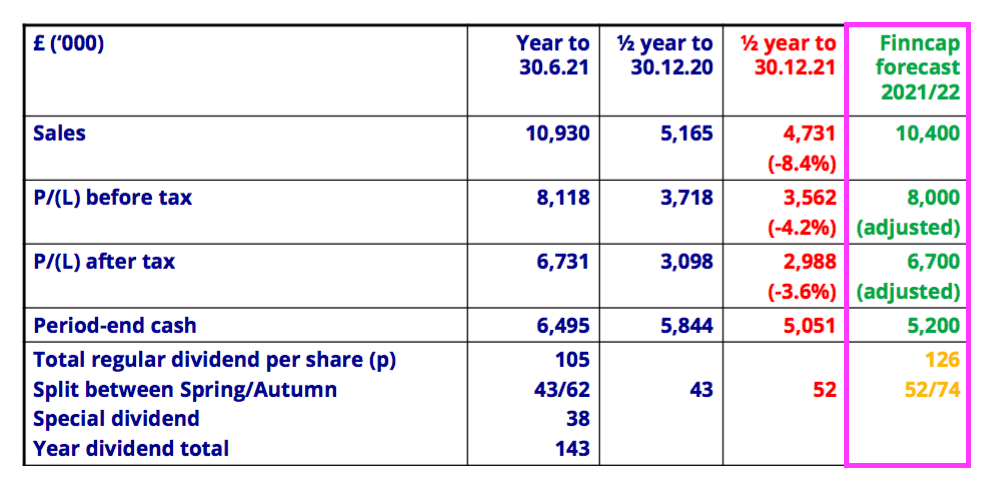

- The H1 presentation re-introduced the disclosure of broker forecasts:

- BVXP had commendably included broker forecasts within its presentations until FY 2020, at which point the pandemic presumably persuaded management to drop the estimates just in case they proved too optimistic.

- The broker’s projections for FY 2022 imply earnings will remain unchanged versus FY 2021, with H2 revenue of £5.7m (down 2%) and H2 profit before tax of £4.4m (up 1%).

- Projected FY 2022 year-end cash of £5.2m suggests H2 free cash flow will be £2.8m after accounting for the 52p per share/£2.7m dividend declared within this H1.

- Projected year-end cash of £5.2m looks light to me given my aforementioned sums pointing towards £6.2m.

- Trailing operating profit before foreign-exchange gains/losses runs at £8.0m, which after applying the upcoming 25% UK tax rate gives earnings of £6.0m or 116p per share.

- The 2021 annual report (point 15) reveals the tax charge would have been 22% for FY 2021 had the 25% tax rate been applied for that year.

- The lower 22% rate benefited from R&D tax credits, which BVXP has enjoyed since FY 2008. Applying a 22% rate to the £8.0m trailing operating profit gives earnings of 120p per share.

- Earnings of 116p (or 120p) per share support a 28x multiple with the share price at £33.

- Earnings of 116p (or 120p) per share do not leave much room for special dividends if the H1 payout is now 52p per share and the forthcoming H2 payout stays at 62p per share (i.e. totalling 114p per share).

- Bear in mind troponin revenue will cease during 2032 and the associated profit should not therefore be valued on a simple multiple.

- Assuming troponin revenue:

- Averages (a probably optimistic) £4m for the next 10 years before expiry;

- Has no associated cost, and;

- Is taxed at the upcoming 25% standard UK rate…

- …gives an after-tax value of £30m before any time-value discounting.

- The table below derives the possible earnings from BVXP’s vitamin D and other commercialised antibodies by:

- Estimating FY 2021 revenue without troponin and lost product revenue;

- Then subtracting all cost of sales and administration expenses;

- Then adding back all R&D costs, and;

- Ignoring foreign-exchange gains, share-based payments and R&D tax credits:

| Estimated FY 2021 for vitamin D and other antibodies | (£k) |

| Revenue | 10,931 |

| Less troponin revenue | (680) |

| Less lost product revenue | (1,280) |

| Less cost of sales | (817) |

| Less admin expenses | (1,507) |

| Add back R&D expenses | 1,201 |

| Operating profit | 7,848 |

| Less tax at 25% | (1,962) |

| Earnings | 5,886 |

- Applying a 25x multiple to the derived £5.9m earnings values BVXP’s vitamin D and other commercialised antibodies at £147m.

- The present £172m market cap less the £30m troponin estimate less the £147m vitamin D/other estimate therefore leaves the pipeline valued at a negative £5m.

- Valuing the pipeline at a negative £5m feels about right if annual R&D costs are £1.2m and commercialisation is not expected until 2025 at the earliest:

- True, these valuation sums could be fine-tuned to:

- Calculate a more realistic net present value for troponin;

- Include R&D tax credits;

- Allocate cost of sales to the appropriate antibody, and;

- Apply different multiples to that £5.9m vitamin D/other estimate…

- …but right now signs of a compelling valuation are not truly obvious.

- The sums could explain why the shares have not made headway during the last three years:

- A premium rating is nonetheless understandable. Shareholder attractions include:

- The predictable and ongoing income from antibody sales and royalties (pandemics aside);

- A competitive ‘moat’, helped in part by protracted development/regulatory timescales and ‘captive’ end-customers (e.g. hospitals) limited to particular blood-test machines (and therefore particular antibodies), and;

- The amazing margins and minimal reinvestment requirements, which underline the terrific economics of antibody commercialisation.

- If vitamin D and the other established antibodies are now set to experience modest growth, the present market cap leaves longer-term upside very dependent on the success of the pipeline.

- October’s FY 2022 results will reveal the scale of BVXP’s seventh special dividend (assuming any such payment is declared).

- The trailing 114p per share ordinary dividend meanwhile supports a 3.5% yield.

Maynard Paton

Bioventix (BVXP)

Trading Update published 14 September 2022

A collector’s item this — an unscheduled trading update from BVXP. The previous such update occurred five years ago! The statement was thankfully positive. Here is the full text:

——————————————————————————————————————

Bioventix plc (BVXP), a UK company specialising in the development and commercial supply of high-affinity monoclonal antibodies for applications in clinical diagnostics, is pleased to announce a trading update for the year ended 30 June 2022 (“FY2022”).

As announced in our interim results to 31 December 2021, we had a slow start to the financial year. However, in the second half, we have seen an improvement in performance and our trading result for FY2022 as a whole is likely to be significantly ahead of market expectations.

This improvement reflects a degree of recovery from the pandemic effects experienced since early 2020, and we hope that this recovery will prove to be sustained and long-lasting. We are pleased that the roll-out of high sensitivity troponin products, that are supported by our technology, has also matched our expectations.

In addition, our results are reported in UK Sterling and the recent fall in value of the UK Sterling against the US Dollar has had a positive effect. Approximately 50% of our revenues are linked to US Dollars and royalties received recently from customers in respect of our H2 sales have been converted at more favourable exchange rates.

——————————————————————————————————————

Perhaps we now know why BVXP re-instated broker forecasts within its results presentations!

Those broker forecasts had indicated profit after tax of £6.7m, and translating this update’s “significantly ahead of market expectations” to mean at least 10%, profit after tax could now be £7.4m or 141p per share.

Useful to know revenue is c50% denominated in USD; BVXP lumps USA income within its Rest of the World segment. The £10.4m broker estimate for FY 2022 revenue therefore implies annual US revenue of c£5.2m

GBP:USD averaged 1.32 during March when BVXP published its H1 presentation (complete with broker forecast), and during August the rate had decreased to an average 1.20.

USD revenue is therefore now translating into 10% more GBP, and an extra £5.2m*10% = £520k of annual revenue due to FX movements, most of which may convert into operating profit given the group’s royalty/licensing model.

The wording “This improvement reflects a degree of recovery” gives the impression the post-pandemic recovery is ongoing and could extend throughout FY 2023.

Maynard