07 March 2022

By Maynard Paton

Results summary for Andrews Sykes (ASY):

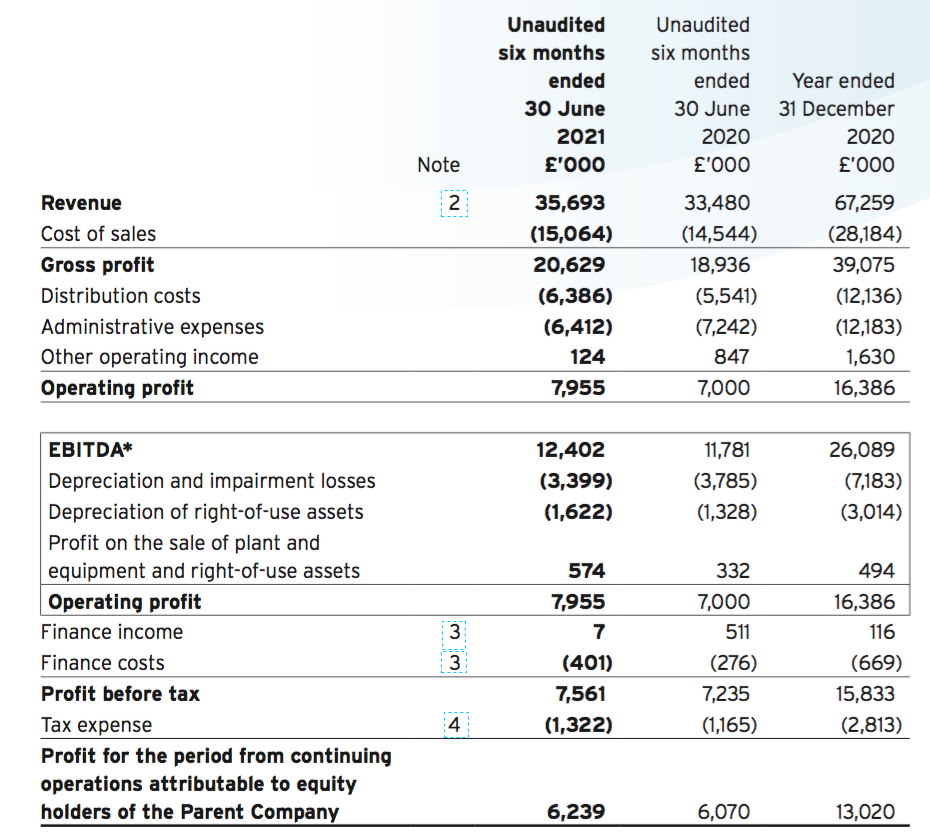

- Following the disappointing finish to FY 2020, a better-than-expected H1 performance with revenue and profit up 7% and 14% respectively.

- Progress was buoyed by ASY’s European operations, which witnessed sales rebound 29% to set a new divisional H1 record.

- A restatement revealed previously undisclosed furlough income had represented 12% of H1 2020 profit.

- The books remain in good shape, with a robust 22% margin and net funds at a sizeable £22m, although extra pension contributions are still required.

- A possible P/E of 13.5 and yield of 5% hardly seem expensive for the appealing financials and potential of further European expansion. I continue to hold.

Contents

- News link, share data and disclosure

- Why I own ASY

- Results summary

- Revenue, profit and dividend

- Furloughed employees

- Overseas and Other operations

- Financials: Margin and cash flow

- Financials: Pension scheme

- Valuation

News link, share data and disclosure

News: Interim results for the six months to 30 June 2021 published 28 September 2021.

Price: 470p

Shares in issue: 42,174,359

Market capitalisation: £198m

Disclosure: Maynard owns shares in Andrews Sykes. This blog post contains SharePad affiliate links.

Why I own ASY

- Supplies air conditioners, portable heaters and industrial pumps for hire, with success based on a prompt 24/7 service, high-quality rental fleet and commercial-only customer base.

- Accounts regularly showcase high margins, generous cash flow, net cash and attractive returns on equity.

- Chairman and family are 90%/£178m shareholders and ensure management focuses on “long-term shareholder value creation” (point 10).

Further reading: My ASY Buy report | All my ASY posts | ASY website

Results summary

Revenue, profit and dividend

- A “particularly challenging” finish to FY 2020…

“The fourth quarter of 2020 was particularly challenging due to the combination of severe Covid-19 restrictions being imposed by the governments in the UK and Europe and a relatively mild winter in the UK.“

- …alongside ‘going concern’ text that suggested FY 2021 may experience similar pandemic interference…

“It has been assumed that the impact of the coronavirus pandemic continues to affect trading for the remainder of 2021 but with trade returning to a more normal level in the latter part of the year.“

- …had already suggested these H1 2021 results would not be spectacular.

- But the H1 performance appeared better than expected.

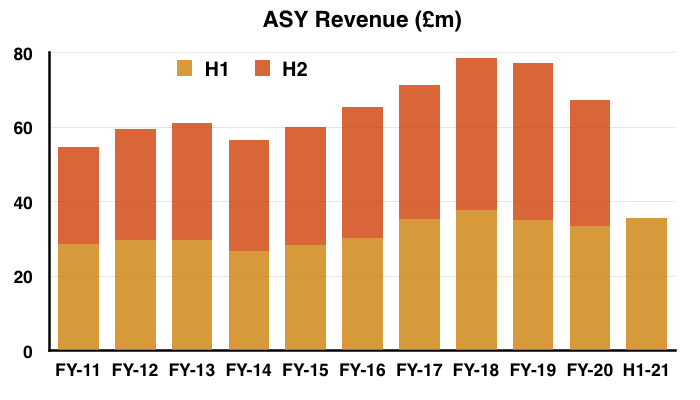

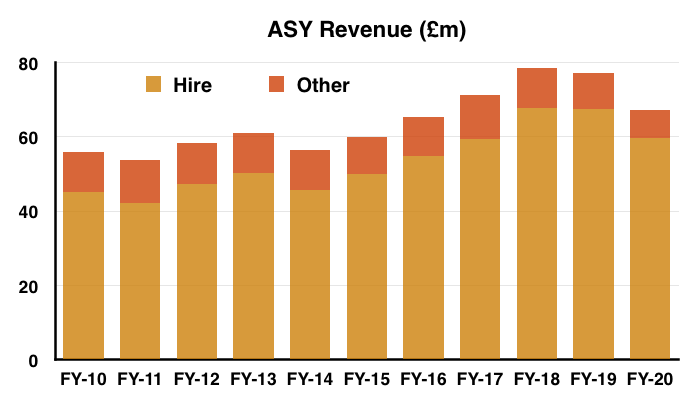

- Revenue in fact gained 7% on H1 2020 to set ASY’s second-best H1 performance after H1 2018. Revenue was up 2% versus the pre-pandemic H1 2019.

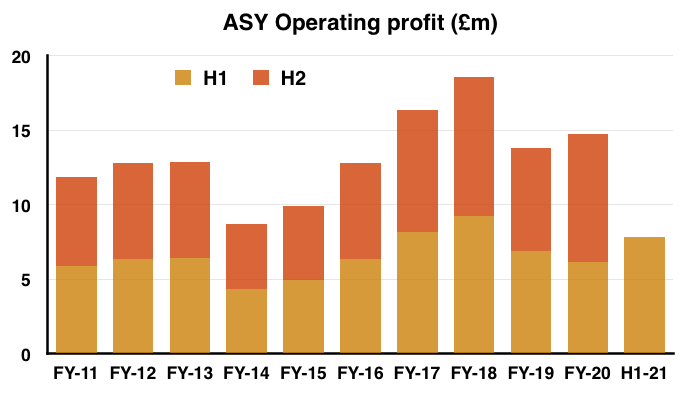

- Reported operating profit meanwhile advanced 14% on H1 2020 (and +14% on the pre-pandemic H1 2019) to reach a level beaten only by H1 2017 and H1 2018 during the last decade:

- Extreme weather — notably cold snaps, heat waves and extensive rain — typically prompt sudden demand for the group’s equipment (primarily heaters, air conditioners and water pumps).

- Progress from one year to the next can therefore fluctuate due to different climatic conditions.

- ASY described this H1 performance as “resilient” and kept operational commentary to a minimum:

“[T]he pumps business in the UK continues to perform… above pre-pandemic levels.”

“Our businesses in the rest of Europe experienced a significant rebound in revenue… on the back of reduced covid restrictions and increased business activities.”

“Our business based in the UAE… continued to experience a difficult trading environment during the period due to the coronavirus pandemic and reduced demand during Ramadan.“

- But ASY’s blog thankfully continues to showcase the company’s activities. H1 customers included:

- “Replacement heating system bails out major British retailer“

- “Global healthcare company seeks heater hire for warehouse staff”

- “Andrews installs high capacity air conditioning solution inside multi-storey office building”

- “Pump hire tackles crippling floods to preserve busy train timetable”

- “Andrews provides climate control for eagerly anticipated US-Russia summit”

- “Dehumidification hire enables building refurb at nuclear power station”

- “Data centre cooling package preserves network infrastructure at Mont Blanc tunnel”

- “Digester boiler hire helps preserve energy output at sewage treatment plant”

- “Multi-solution climate control arrangement keeps major vaccination hub active“

- “Latest depot opening highlights ongoing success in Italy”

- ASY’s reported profit was bolstered by government furlough grants of £124k (see Furloughed employees) and did not include an increased pension contribution of £625k (see Financials: Pension scheme).

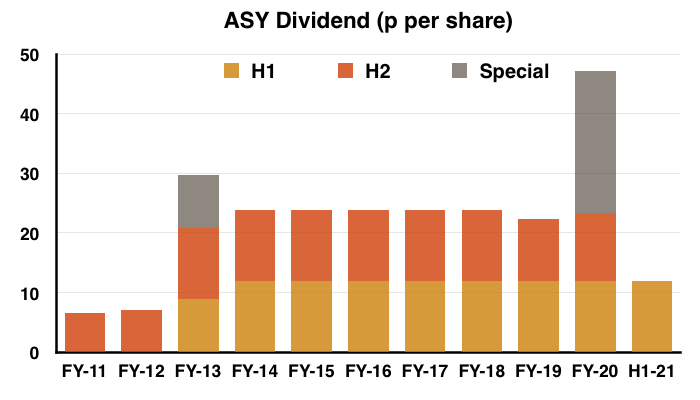

- For the eighth successive year, the H1 dividend was set at 11.9p per share.

- I am hopeful the forthcoming final dividend for FY 2021 will return to 11.9p per share after being cut slightly for FYs 2019 and 2020 following the pandemic.

- A final 11.9p per share dividend would mean a full-year 23.8p per share payout, and would match the annual dividends declared for FYs 2014, 2015, 2016, 2017 and 2018.

Furloughed employees

- These H1 results shed some light on ASY’s mysterious furlough income.

- To recap, the FY 2019 annual report (point 2) claimed 50% of UK employees were furloughed at the time of the report’s publication (May 2020)…

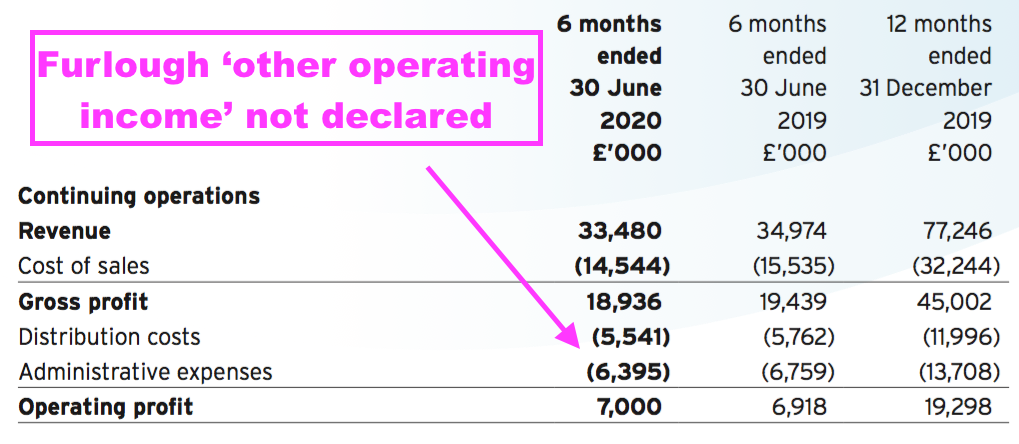

- ..and yet the H1 2020 results did not declare any furlough benefits:

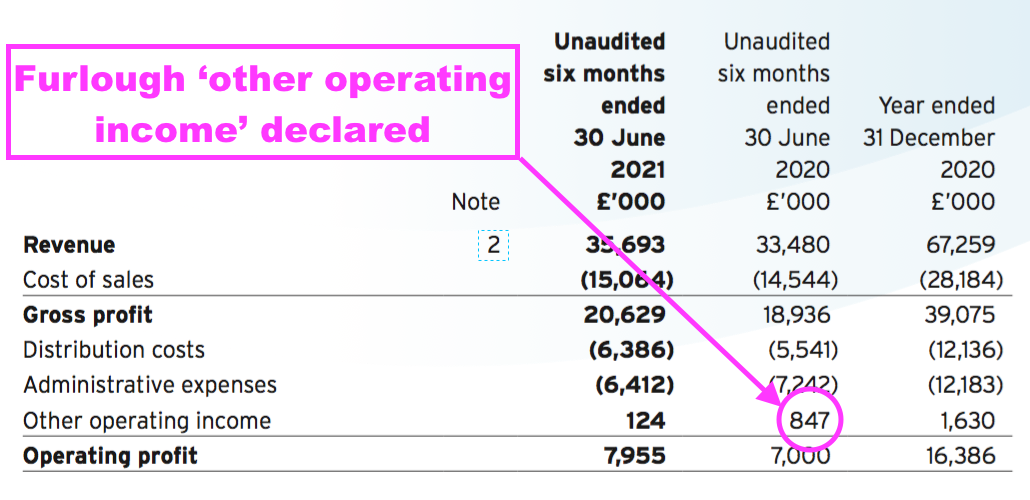

- This H1 statement restated the comparable H1 2020 figures and revealed ASY did in fact receive furlough income at that time:

- For H1 2020, furlough income of £847k represented a notable 12% of the declared £7.0m operating profit.

- Not disclosing furlough benefits as ‘other operating income’ — but instead amalgamating the payment into ‘administrative expenses’ — was very bad form from ASY.

- Mind you, ASY’s finance director resigned during January 2020 and a replacement was not appointed until December 2020…

- …and perhaps Covid accounting disclosures were not among the most pressing matters for the “other members of the senior management team” who took on the FD responsibilities during the first pandemic lockdown.

- One furlough mystery that may never be solved is the H1 2020 UK performance. My emailed question for ASY’s behind-closed-doors 2021 AGM did not receive a reply:

“Q) The 2019 annual report stated “In the UK, approximately 50% of our employees are furloughed”.

The half-year results to June 2020 then showed UK revenue unchanged at £20.9m.

Could the board explain how UK revenue was maintained during those six months when, at some point, 50% of UK employees were seemingly not at work due to Covid? The performance implies the business could actually operate with fewer employees, with some benefit perhaps to profit.”

- ASY received furlough payments of £1.6m during FY 2020, which represented approximately 9% of the year’s total wage bill.

- I can only assume the 50% of UK employees furloughed during H1 2020 were furloughed for a very short time.

- ASY collected furlough grants of only £124k during this H1, and I trust the subsequent relaxation of pandemic restrictions will mean results from H2 2021 onwards will not be distorted by further furlough payments.

Overseas and Other operations

- Europe remains ASY’s main opportunity for growth.

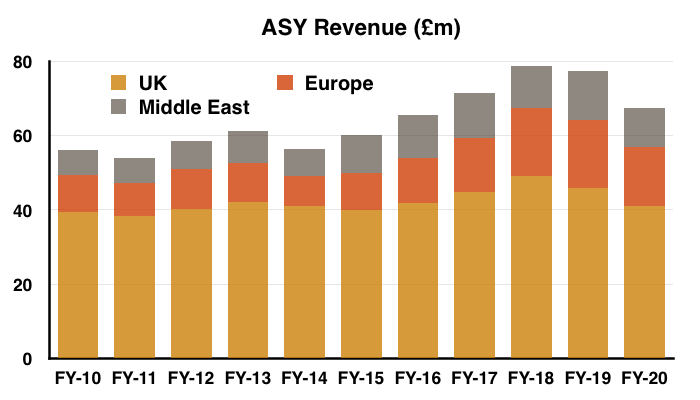

- Between FYs 2010 and 2019, European revenue expanded from £10m to £18m to represent 24% of total group sales:

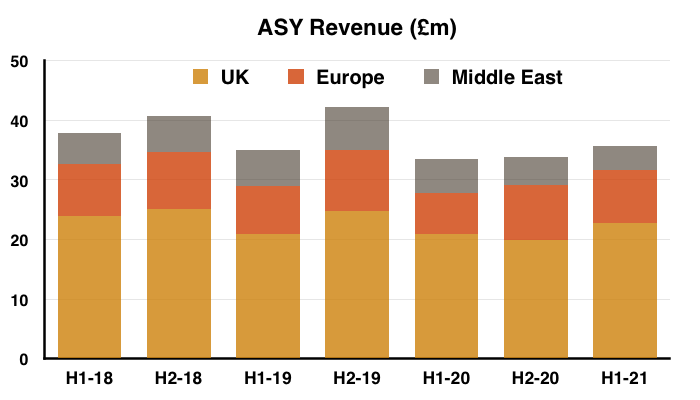

- European revenue dropped to £16m during FY 2020 because of the pandemic, but advanced 29% for this H1 to £8.9m — a record European H1 performance:

- ASY’s European operations consist of:

- Netherlands:

- Opened FY 1971

- 4 depots (Amsterdam, Bleiswijk, Hoogeveen, Oirschot)

- Belgium:

- Opened FY 2007

- 2 depots (Anvers, Brussels)

- Italy:

- Opened FY 2011

- 3 depots (Bologna, Milan, Verona)

- France:

- Opened FY 2012

- 6 depots (Lille, Lyon, Marseille, Nantes, Paris, Toulouse)

- Switzerland:

- Opened FY 2013

- 2 depots (Geneva, Zurich)

- Luxembourg:

- Opened FY 2014

- 1 depot (Luxembourg)

- Netherlands:

- At least twelve European depots have opened since FY 2011 to take the region’s total to 18.

- Revenue per European depot during FYs 2019 and 2020 was approximately £1m.

- ASY presently operates 32 depots within the UK. Revenue per UK depot during FYs 2019 and 2020 was approximately £1.3m.

- Wishful thinking perhaps, but maybe the European operations could in time:

- Open another 14 depots to match the number within the UK, and;

- Advance revenue per depot towards the £1.3m enjoyed within the UK.

- European expansion has been relatively slow. Another 14 depots could take a decade at the pace witnessed since FY 2011.

- ASY’s Middle Eastern operations may offer potential, too.

- Revenue from the Middle East had improved from £10m to £13m between FYs 2015 to 2019, but fell back to £10m during the pandemic and has yet to rebound.

- Profit of between £2m and £3m from the Middle East has been helpful, but the division’s margins are lower than those achieved within the UK and Europe, while payment terms for Middle Eastern customers are very generous (point 4).

- The prospects for ASY’s ‘Other’ operations — involving selling, installing and maintaining equipment — do not appear favourable.

- ‘Other’ revenue had been running at a regular £11m until FY 2016, since when revenue has dropped to £7m. Profitability at this division has never appeared significant.

Financials: Margin and cash flow

- ASY’s accounts remain in relatively good shape.

- A 22% operating margin (excluding furlough benefits) was ASY’s highest for an H1 since H1 2018 and underlines the notion of ASY operating very efficiently.

- ASY’s full-year operating margin has in fact topped 20% every year since 2002.

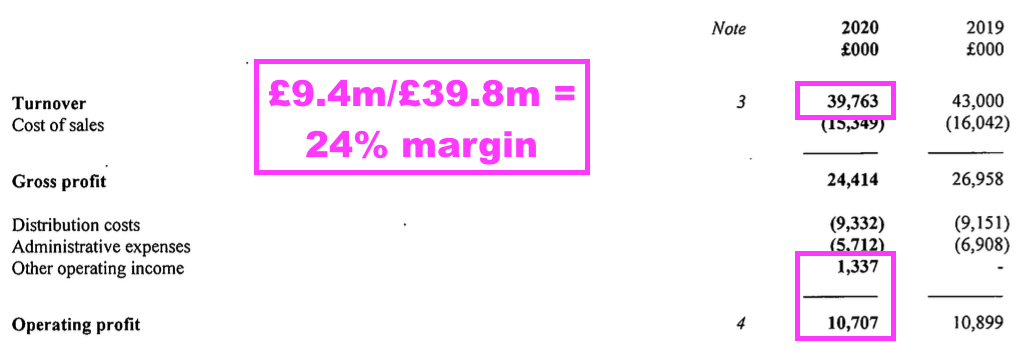

- Companies House now reveals ASY’s main UK hire division, Andrews Sykes Hire limited, enjoyed an appealing 24% margin (excluding furlough benefits) during the pandemic-disrupted FY 2020:

- Cash flow looked good. Free cash flow of £6.3m matched reported earnings and funded a £0.5m loan repayment and a £4.9m dividend payment.

- The H1 cash position was enhanced by £0.9m to £24.7m. Bank debt was £3.0m and therefore left net cash at £21.7m or 51p per share.

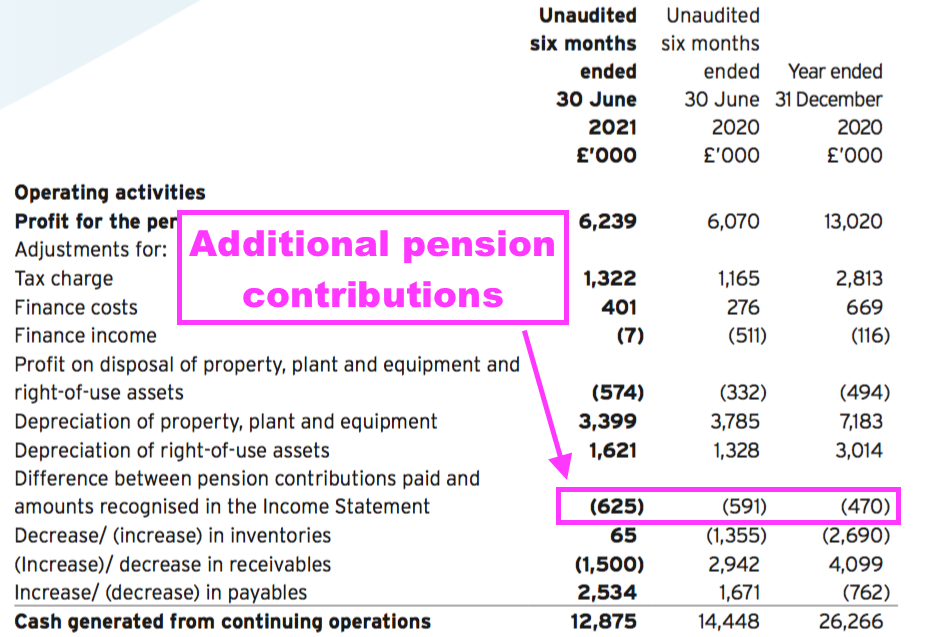

- ASY’s cash flow showed a notable payment to the pension scheme that bypassed the income statement (see Financials: Pension scheme):

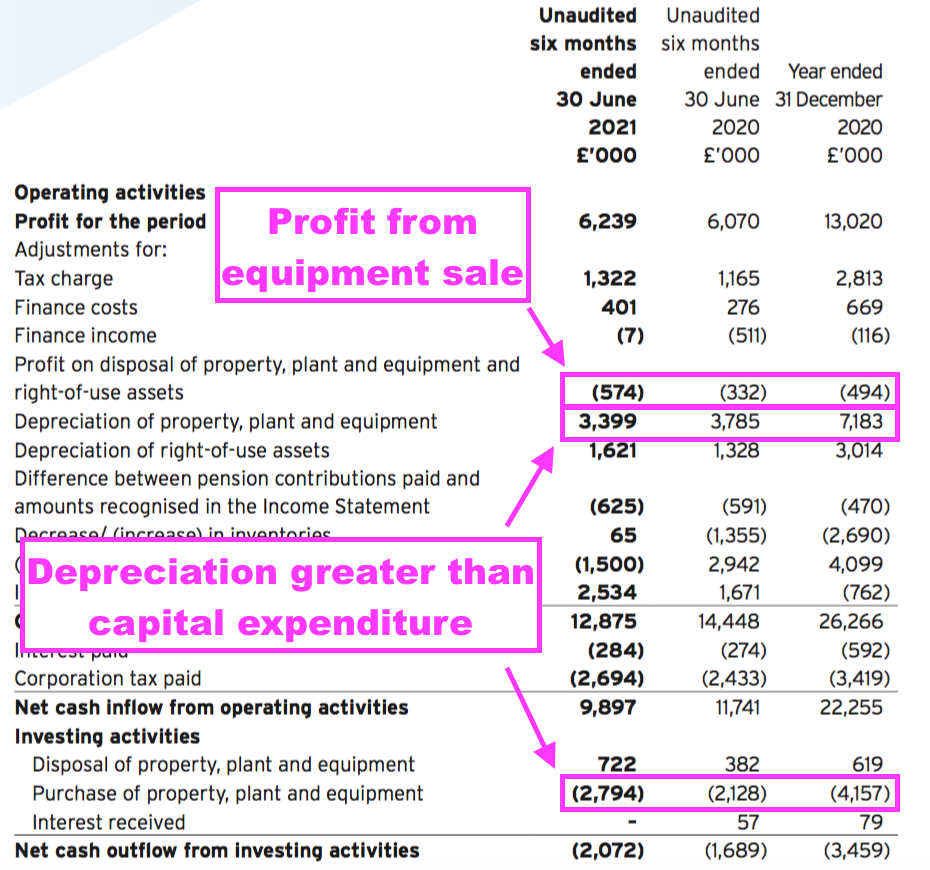

- Depreciation commendably continues to more than cover cash capital expenditure. Emphasising the conservative accounting, ASY recorded a H1 £0.6m profit over the book value of sold equipment:

- Working-capital cash movements appeared under control, registering an aggregate H1 £1.1m inflow.

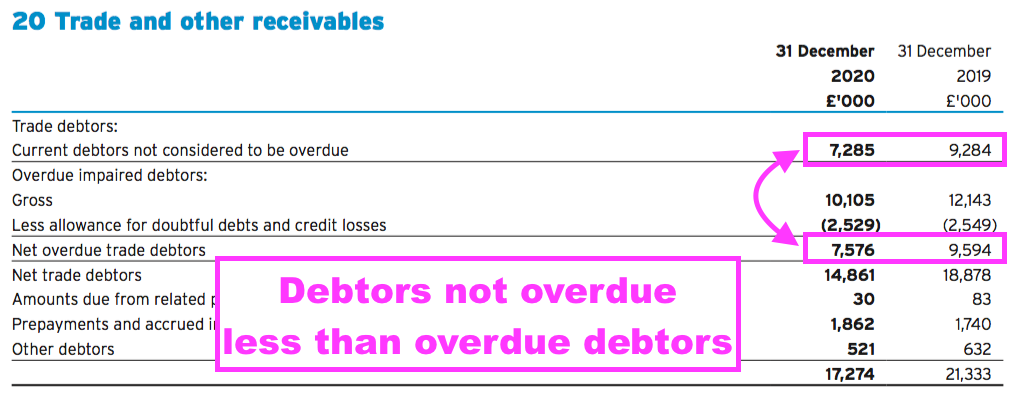

- ASY’s receivables in particular require monitoring, as overdue customer payments typically represent a hefty 50% of all outstanding payments:

Financials: Pension scheme

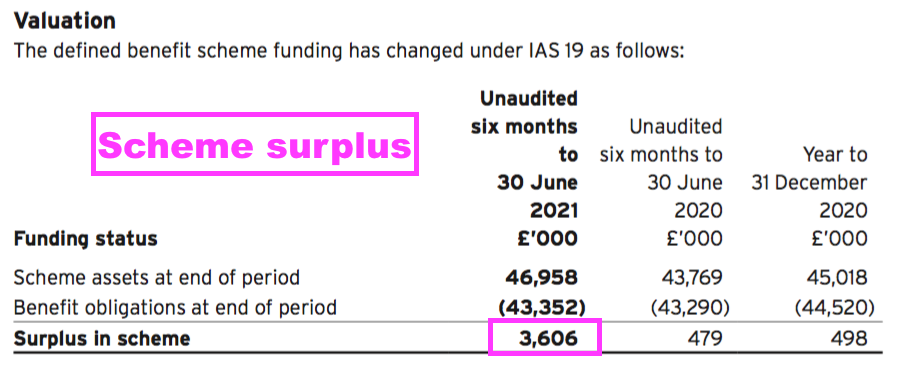

- ASY’s defined-benefit pension fund demonstrates how long-term pension accounting does not always reflect the near-term cash reality of a pension scheme.

- Although ASY’s balance sheet continues to show a scheme surplus…

- …the company’s pension fund requires higher contributions.

“A formal funding valuation as of 31 December 2019, together with a revised schedule of contributions and recovery plan, was agreed by the Board with the pension scheme trustees in March 2021. In accordance with this agreement, the group will be paying £1.3 million per annum into the pension scheme in both 2021 and 2022.“

- This H1 statement reiterated the £1.3m per annum payments for FYs 2021 and 2022, with a reduction back to £120k for FYs 2023, 2024 and 2025:

“In accordance with this schedule of contributions and recovery plan, the Group will be making regular contributions of £110,000 per month for the period 1 January 2021 to 31 December 2022, and £10,000 per month for the period 1 January 2023 to 31 December 2025 or until a revised schedule of contributions is agreed, if earlier.”

- Scheme assets during this H1 advanced by £2m to £47m, which should be enough to sustain recent annual benefits of £2m assuming contributions stay above £1m.

Valuation

- ASY’s outlook statement did not seem too awful:

“Whilst certain of the Group’s business operations continue to be affected by the coronavirus pandemic, for example the performance of Khansaheb remains depressed compared to historical levels, demand in Europe has increased and the pumps business in the UK continues to perform in line with last year’s levels and above pre pandemic levels.

Management remains optimistic that the business will continue to improve as the economy recovers fully but are mindful that we live in uncertain times and circumstances can change very quickly.”

- Current geopolitical events sadly confirm “we live in uncertain times and circumstances can change very quickly“.

- ASY and its blog has nevertheless kept busy:

- “Andrews heat for hire keeps shoppers warm at new retail store“

- “Heater hire warms visitors at iconic Batman franchise filming location“

- “Groundwater removal paves the way for luxury spa“

- “High capacity heating arrangement aids hotel building fit out“

- “Sykes Pumps provides emergency pumping solution for housebuilding contractor“

- Trailing twelve-month operating profit excluding furlough payments but including IFRS 16 lease financing is £15.8m. Taxed at the standard UK 19% gives earnings of 30.4p per share.

- For perspective, the comparable profit for pre-pandemic FY 2019 was £18.7m. Taxed at the standard UK 19% gives earnings of 35.9p per share.

- Subtract the £22m net cash position from the £198m market cap and the underlying business could be valued at approximately £176m or 418p per share.

- Whether the entire net cash position is truly ‘surplus to requirements’ is debatable, given ASY has operated with net funds of at least £15m since 2012.

- Depending on your view of earnings (returning soon to pre-pandemic levels or not) and the cash position (truly surplus or not), ASY’s P/E could be 11.7x, 13.1x, 13.8x or 15.5x. The average of 13.5x feels about right.

- The valuation sums could be fine-tuned further to reflect ASY’s pension situation…

- … but a possible 13.5x multiple hardly seems expensive for a high-margin and cash-rich business that proved reasonably resilient during the pandemic and may have further expansion opportunities within Europe.

- Assuming the full-year dividend does return to 23.8p per share, the 470p shares would supply a 5.0% income.

Maynard Paton

Great up-date, thanks.

European potential appears central to the growth case. As a I recall, sales per base in Europe were c. £1.4m in 2018 with 13 sites. Since then, four new sites were openned at Marseille, Tolouse, Nantes and Verona. I suspect there is a maturity profile, while the site builds staff, kit and customers, of c. 3 years – Covid probably elongated this. Even with no new sites, European sales should therefore increase. Like you, I would like to see a more aggressive European openning programme. Is the business mix the same in Europe? I believe it is.

I also suspect the UK could be consoldidated into a more efficient network with fewer larger sites. New openings/up-grades suggest this approach.

It seems a solid business at a fair price.

Hi MTIOC

Thanks for the comment. Yes, I should have looked at sales per depot for previous years to gain a greater perspective! I agree there is a maturity profile for any new depot, and perhaps for the wider ASY brand in new overseas markets. European sales should inherently outpace UK sales with greater scope for new depots, although let’s see. I got the impression from an AGM I attended years ago the business mix is quite similar; management said any equipment from Europe could be re-used in the UK. I don’t know whether fewer UK sites would make the business more efficient for the customer, with equipment perhaps taking longer to collect/deliver?

Maynard