29 March 2018

By Maynard Paton

Update on M Winkworth (WINK).

Event: Final results for the twelve months to 31 December 2017 published 28 March 2018

Summary: The London estate-agency group was never going to issue stunning figures. Nonetheless, a credible performance was reported and I am impressed the business continues to fare well against sector rival Foxtons. Note, too, that WINK’s average percentage commissions actually increased — so perhaps online competition is not that big a threat after all. Meanwhile, the books remain cash rich, the outlook does not seem too bad while the 10x multiple and 6% yield appear modest. I continue to hold.

Price: 120p

Shares in issue: 12,733,238

Market capitalisation: £15.3m

Click here to read all my WINK posts.

Results:

My thoughts:

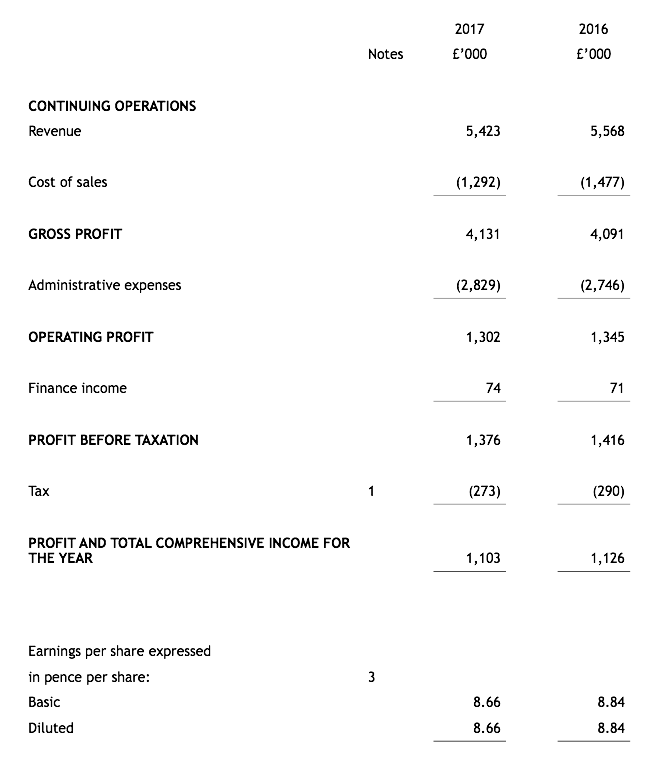

* Revenue and profit broadly flat, but sale prices held up and commission rates actually increased

January’s trading update had already ensured these 2017 results would hold no surprises.

As WINK had forecast, revenue was indeed “less than 5% lower than 2016” — the top line dipped 3% — while profit before tax came in at £1,376k versus a projected “£1.3m”.

The firm’s subdued first half was never going to make 2017 a vintage year, and this annual statement reiterated the “political developments” and stamp-duty changes behind the “testing” London housing market — from which WINK derives 80% of its business.

The end result was the lowest level of revenue since 2013 and the lowest operating profit since 2011:

| Year to 31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Gross Franchise Sales & Lettings (£k) | 46,100 | 50,100 | 49,010 | 46,120 | 46,200 |

| Revenue (£k) | 4,945 | 5,495 | 5,865 | 5,566 | 5,423 |

| Operating profit (£k) | 1,659 | 1,840 | 1,817 | 1,346 | 1,302 |

| Finance income (£k) | 33 | 86 | 90 | 71 | 74 |

| Other items (£k) | - | - | - | - | - |

| Pre-tax profit (£k) | 1,692 | 1,926 | 1,907 | 1,417 | 1,376 |

| Earnings per share (p) | 10.05 | 11.83 | 11.95 | 8.84 | 8.66 |

| Dividend per share (p) | 5.40 | 6.20 | 6.50 | 7.20 | 7.25 |

| Special dividend per share (p) | - | - | 1.80 | - | - |

At least the dividend inched higher to reach a new peak.

Chief executive Dominic Agace provided a couple of encouraging remarks:

“We are also particularly pleased to note that the average price of a property sold by Winkworth’s London offices rose from £692,000 to £718,000, an increase of 4% despite property prices declining across the city over the course of the year.”

“In addition, we recorded a rise in average percentage commissions, reflecting the value that customers put on trusted advisers in an uncertain market. We see this as endorsement of the strengthening Winkworth proposition.”

So sale prices held up, even as transaction volumes declined.

What’s more, the average commission rate actually increased.

I had always assumed a standstill London property market — and the (apparent) growing popularity of cheap online agents such as Purplebricks (PURP) — would harm commission rates. It would seem not — or at least not yet.

* WINK outperformed Foxtons yet again

I always like to compare WINK’s achievements to those of rival London agent Foxtons (FOXT).

I am pleased to say my favoured agent is performing much better than the owners of those green minis. Here are some statistics:

| Year to 31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Winkworth | |||||

| Gross Franchise Sales Revenue (£m) | 30.0 | 32.6 | 30.1 | 26.0 | 24.8 |

| Gross Franchise Lettings Revenue (£m) | 16.1 | 17.5 | 18.8 | 20.1 | 21.3 |

| Total Gross Franchise Revenue (£m) | 46.1 | 50.1 | 49.0 | 46.1 | 46.2 |

| Foxtons | |||||

| Sales Revenue (£m) | 67.4 | 69.8 | 72.5 | 55.5 | 42.6 |

| Lettings Revenue (£m) | 66.4 | 67.4 | 69.0 | 68.3 | 66.3 |

| Total Revenue (£m) | 133.8 | 137.2 | 141.5 | 123.8 | 108.9 |

| Winkworth / Foxtons | |||||

| Sales Revenue (%) | 44.5 | 46.7 | 41.5 | 46.8 | 58.2 |

| Lettings Revenue (%) | 24.2 | 26.0 | 27.2 | 29.4 | 32.1 |

| Total Revenue (%) | 34.5 | 36.5 | 34.6 | 37.3 | 42.3 |

Back in 2013, WINK’s franchisees earned 34% of FOXT’s annual sales and lettings revenue. Last year they earned 42%, and even reached 45% during the second half.

(While this comparison may not be strictly like-for-like — WINK generates 80% of its revenue from its London-based franchisees, while FOXT’s income is almost entirely derived within the capital — I think the overall trend is quite telling.)

WINK claimed its franchise structure was more effective than a conventional agency chain during tougher markets:

“The strength of the Winkworth franchise model, however, has demonstrated the benefit of having individually owned businesses, which are more resilient to market change.”

I note FOXT’s sales income dived 15% during H2 2017 — WINK’s gained 12%.

* Stable lettings income now represents 47% of total franchisee revenue

WINK’s first-half/second-half split showed H2 profit advancing 21% — although the £795k achieved was lower than that recorded between 2012 and 2015:

| H1 2016 | H2 2016 | FY 2016 | H1 2017 | H2 2017 | FY 2017 | ||

| Revenue (£k) | 2,747 | 2,819 | 5,566 | 2,544 | 2,879 | 5,423 | |

| Operating profit (£k) | 688 | 658 | 1,346 | 507 | 795 | 1,302 |

I should add that WINK’s H1 2016 was inflated by a buy-to-let “mini boom” ahead of greater stamp duty on second properties.

The H1:H2 split also revealed the total revenue earned by WINK’s franchisees shifting further from property sales to lettings:

| Gross Franchise Revenue | H1 2016 | H2 2016 | FY 2016 | H1 2017 | H2 2017 | FY 2017 | |

| Sales (£m) | 14.3 | 11.7 | 26.0 | 11.7 | 13.1 | 24.8 | |

| Lettings (£m) | 9.3 | 10.8 | 20.1 | 9.7 | 11.6 | 21.3 | |

| Total (£m) | 23.6 | 22.5 | 46.1 | 21.4 | 24.7 | 46.2 |

WINK has a long-stated target of earning 50% of its income from lettings, which ought to be a more stable source of revenue over time than collecting commissions from property transactions.

The 50-50 split is inching nearer, with 47% of total franchisee income coming from rents during H2 2017. Back in 2013 the ratio was 35%.

* WINK continues to enjoy a 12% cut of franchisee revenue

WINK confirmed its estate-agency franchisees generated gross revenue of £46.2m during 2017 — broadly equal to that witnessed during 2016.

WINK’s own revenue of £5.4m represented close to 12% of that £46m — just about sustaining the proportion of the last two years:

| Year to 31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Gross Franchise Sales & Lettings (£k) | 46,100 | 50,100 | 49,010 | 46,120 | 46,200 |

| Revenue (£k) | 4,945 | 5,496 | 5,865 | 5,566 | 5,423 |

| Revenue/Gross Franchise Sales & Lettings (%) | 10.7 | 11.0 | 12.0 | 12.1 | 11.7 |

The near-12% cut is represented by an 8% slice of franchisee sales and lettings income, with the balance consisting of revenue from various franchisee support services alongside franchise establishment/re-selling fees.

* Useful cash flow and collection of franchisee loans bolsters cash position

I am quite happy with WINK’s cash flow:

| Year to 31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating profit (£k) | 1,659 | 1,840 | 1,817 | 1,346 | 1,302 |

| Depreciation and amortisation (£k) | 210 | 244 | 275 | 368 | 246 |

| Net capital expenditure (£k) | (159) | (237) | (108) | (250) | (247) |

| Working-capital movement (£k) | 274 | (878) | (195) | (145) | 567 |

| Net cash and investments (£k) | 2,656 | 2,513 | 3,175 | 2,979 | 3,586 |

Certainly the group’s capital expenditure continues to be adequately reflected within the earnings calculation by the combined depreciation and amortisation charge.

Meanwhile, there was a useful cash inflow from working capital.

WINK’s working-capital movements include sums lent to franchisees to help fund their businesses. In the past, these movements have generally shown WINK advancing — rather than collecting — the money.

However, this time some loans seem to have been repaid — entries on the balance sheet suggest £400k was collected. The forthcoming 2017 annual report should reveal the actual amount, and how much the franchisees still owe. For now I estimate outstanding loans to be approximately £800k, equivalent to 6p per share.

The franchisee repayments helped free cash reach a very useful £1.5m, of which £917k was paid as dividends and £608k was added to the cash pile. The bank balance finished the year at £3,579k, equivalent to 28p per share. The books remain free of debts and pension obligations.

I should add that, despite WINK’s revenue and profit remaining stuck at 2016 levels, the franchising structure continues to earn a very acceptable margin and return on equity:

| Year to 31 December | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating margin (%) | 33.5 | 33.5 | 31.0 | 24.2 | 24.0 |

| Return on average equity (%)* | 86.2 | 87.0 | 71.2 | 49.5 | 48.5 |

(*adjusted for net cash and investments)

* I remain unconvinced by online agents and Purplebricks in particular

WINK seemed happy with its new website:

“We are pleased that our updated website, launched in March 2017, has delivered more leads to our franchisees despite a weak second half of the year in terms of overall applicants.

It has provided a robust platform for our digital evolution, enabling the launch of our vendor portal in November to which 40 offices have already signed up. We are pleased that it was recognised as website of the year at the Negotiator awards in November 2017…

We are currently two months into our digital campaign and this is on track to deliver an additional 200,000 visits per month to our website and, in turn, to our franchisees.”

However, there is no plan to become an online-only service.

Mr Agace told me at an AGM that the firm would remain a full-service agency, and his narrative accompanying these results underlined that commitment.

As before, my best guess of the future is that traditional agents may see their fees squeezed a little by online alternatives, but won’t endure complete destruction.

I still maintain the overriding challenge for online agents is being able to grow their businesses without needing as many staff as traditional agents.

You see, an estate-agent employee can manage only so many property transactions to completion, and the lower fees charged by an online agency could mean its staff handling many more customers to earn a decent wage.

And handling more customers may then lead to a poor service and chains falling through…

Ultimately a house seller wants his/her home sold and to get the money in the bank — simply paying upfront for a Rightmove listing may not always get that same result.

Well, at least that’s my view.

Anyway, I see PURP’s latest trading statement has owned up to a UK sales wobble. I would have thought any pioneering online ‘disruptor’ could easily navigate “underlying macro issues”, “poor weather” and a so-called “training initiative”.

Valuation

Mr Agace’s outlook did not read too badly. Here are a few snippets:

“The underlying fundamentals of the market remain positive.

Sellers [in London] are accepting these reductions and this, in turn, is in some areas leading to improved levels of transactions despite applicant numbers remaining at low levels.

“On the lettings side of the business, our applicants are tracking at some 12% ahead of the same period of last year, which should support further growth in 2018.

New franchising applicant numbers are more than 25% above this point in 2017, and with two offices already opened in Banstead and Poringland we look forward to maintaining the momentum gained in 2017 by targeting to open eight new offices in 2018 in areas affiliated to our extensive London network…

We believe that a broadly flat market will continue to suit our franchise model.

We remain debt free, with a strong cash position and an increasing number of opportunities to grow in 2018.”

Taking WINK’s 2017 operating profit of £1.3m and applying 19% standard UK tax gives earnings of close to £1.1m or 8.3p per share.

Adjusting the £15.3m (at 120p) market cap for my £4.4m guess of cash and franchisee loans, I arrive at an enterprise value of £10.9m or 86p per share.

Then dividing that 86p by my 8.3p per share earnings guess gives a P/E of 10.

That rating does appear good value to me. Mind you, this share has traded on that multiple for some years now… and not even the 7.25p per share dividend and current 6% income have tempted extra buyers.

I guess gains from this shareholding may only materialise once the London property market perks up and earnings start to climb towards their previous peak.

Maynard Paton

PS: You can now receive my Blog posts through an occasional e-mail newsletter. Click here for details.

Disclosure: Maynard owns shares in M Winkworth.

M Winkworth (WINK)

Publication of 2017 annual report

A few points of interest:

1) Review of business

An interesting snippet:

It seems revenue declined a fraction due to lower marketing spend, which does not sound too bad in light of the standstill London property market that WINK serves.

2) Risks

WINK’s risk section referred to the same dangers as last year:

3) New accounting standards

New rules for accounting for financial instruments (IFRS9), revenue recognition (IFRS15) and leases (IFRS 16) should not really trouble WINK:

IFRS 9:

IFRS 15:

IFRS 16:

4) Restated accounting

The 2016 annual report (point 6) showed WINK lumping a £106k intangible write-off together with the normal amortisation charge, which I thought underplayed the group’s profitability somewhat.

Last year the 2016 income statement showed a £321k amortisation charge:

This year the 2016 income statement has been restated to show a £215k amortisation charge:

The restated £118k ‘loss on disposal of fixed assets’ represents the aforementioned £106k and an extra £12k of similarly restated depreciation. It is now clear the 2016 profit figure included a £100k-plus write-off.

5) Employees

WINK’s staff enjoyed pay rises and took home almost 30% of revenue during 2017 — by far the highest proportion since at least 2006:

Each WINK employee costs on average £48.5k (vs £46.6k last year) and earns average revenue of £164k (vs £174k last year). Employee costs at 30% of revenue compares to c26% for 2016 and 2015, and sub-24% for prior years. I trust WINK can now keep a lid on that 30% proportion, and that the extra pay will translate into extra revenue in due course.

6) Director pay

The chief exec enjoyed a useful 20% pay/bonus increase:

I hope the 20% pay/bonus increase followed a market review of board wages, as I would be disappointed to see a 20% hike awarded following a flat year for profit and revenue. Perhaps the appointment of a new, and full-time, finance director, prompted a pay review.

I should add that Mr Agace’s pay/bonus has climbed 34% during the last five years, versus 48% for the ordinary dividend. So at least shareholders have seen their income expand at a greater rate.

7) Trade receivables

Some good news with trade receivables and collecting money from franchisees:

Trade receivables of £491k represent 9.1% of revenue — the lowest percentage since 2011.

Also, the £308k of trade receivables deemed to be ‘not due’ equate to 63% of all trade receivables — the highest percentage since these particular stats were first disclosed during 2012:

These figures follow on from the improved collection times implied by the 2016 annual report. Perhaps the new finance director is getting a better grip on cash management.

8) Loans to franchisees

The receivables note also confirmed the reduction to the amount loaned to franchisees:

Total loans to franchisees fell by £226k to £981k, which, as I noted in the Blog post above, helped support the group’s wider cash generation. Loans of £981k equate to 8p per share.

Maynard

M Winkworth

Dividend Declaration

The first-quarter payout has been raised from 1.8p to 1.85p per share, and should mean the full-year payout comes to 7.4p per share (versus 7.25p for 2017). Here is the full text:

—————————————————————————————————————-

The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 1.85p per ordinary share for the first quarter of 2018 to shareholders. The timetable is as follows:

Ex-Dividend Date * 26/04/18

Record Date ** 27/04/18

Expected Payment Date 24/05/18

* Shares bought on or after the ex-dividend date will not qualify for the dividend

** Shareholders must be on the Winkworth share register on this date to receive this dividend.

—————————————————————————————————————-

Maynard

Hi Maynard,

Bought WINK as a result of your blog a while back. Liked your analysis. Think I like about WINK is its resilience – their market might be in a major lull but they seem to have a very robust business model. Siting on a tidy profit and I’m getting a large special dividend ! Keep up the good work!

Thanks BerksBee. I am hoping the staff at WINK keep up the good work, too.

Maynard

M Winkworth (WINK)

Proposed return of capital

A 9p per share cash handout is on its way.

———————————————————————————————————————————

M Winkworth plc (“Winkworth” or the “Company”), the leading franchisor of real estate agencies, is proposing to return approximately £1.146 million of surplus funds to its shareholders by way of a capital payment (the “Return of Capital”), subject to finalisation of the process and shareholder approval. The effect of the proposed Return of Capital will be that for every fully paid ordinary share of 0.5 pence in the Company held at the Record Date, a shareholder will receive 9 pence in cash.

The proposed cancellation of the Company’s share premium account of approximately £1.793 million will enable the Company to make the Return of Capital to shareholders of approximately £1.146 million in aggregate. The balance of approximately £0.647 million, less the costs of the Return of Capital, would then be transferred to the Company’s profit and loss account thereby creating additional distributable reserves, which may be utilised by the Company for facilitating future returns of cash to Shareholders.

A circular, containing further details of the Return of Capital, will be posted today to the Company’s shareholders (the “Circular”) along with a Form of Proxy to vote at a General Meeting to be held at the offices of Norton Rose Fulbright LLP at 3 More London Riverside, London SE1 2AQ at 10.30am on 9 July 2018.

Dominic Agace, CEO of the Company, commented: “Winkworth’s franchising model is not capital intensive and, since its admission to AIM in 2009, the Company has created regular free cash flow. We believe that it is currently in shareholders’ best interest for excess capital to be returned. We remain alert to acquisition opportunities and, should the need arise, we will approach shareholders to help fund any sizeable acquisitions. In the meantime, we continue to successfully grow our franchise network organically, with a further eight offices scheduled to be added in 2018.”

———————————————————————————————————————————

Year-end cash was £3,579k, so this capital return will leave £2,433k. Add on the £981k franchisee loans and cash/franchisee investments come to £3,414k or 27p per share. Using my 8.3p earnings per share guess as per the Blog post above, my EV/EPS sum is (130p share price less 27p)/8.3p = 12.5. So not an extended rating, but this share has traded on a single-digit multiple in the past.

I am not sure what to make of the chief exec saying he remains “alert to acquisition opportunities“. I had the impression the management was not interested in buying other firms. The idea of handing money back to shareholders only then to ask for it back to support an acquisition is not great.

In contrast, I would like to think WINK would be an acquisition target for another agent. Quoted agents Belvoir and Property Franchise have made substantial acquisitions during recent years, and Belvior even proposed a merger with Property Franchise not so long ago. I would be very surprised if Belvoir or Property Franchise had not considered WINK as a target.

Maynard

Apologies for the tardy comment – but I bought in at just over a £1 a while back based on your analysis. Now with divs I am at 95p. There’s a lot to like about WINK. Thanks for sharing your thoughts.

Thanks BerksBee.

Maynard

Really useful – missed this news as I was away. I take it as a sign of confidence – even if the message was a bit confusing.

M Winkworth (WINK)

Dividend Declaration

The Q1 dividend of 1.85p per share will be repeated for Q2 and ex-div date coincides with the ex-entitlement date for the 9p per share return of capital.

—————————————————————————————————————

The Directors of M Winkworth Plc (“Winkworth” or the “Company”) are pleased to announce that the Company will pay a dividend of 1.85p per ordinary share for the second quarter of 2018 to shareholders. The timetable is as follows:

Ex-Dividend Date 26/07/18

Record Date 27/07/18

Expected Payment Date 23/08/18

—————————————————————————————————————

WINK’s annual dividend look set to be 7.4p per share. The 9p return of capital ought to be paid around 8 August, with the Q2 div paid two weeks later.

Maynard