***ShareScope New Subscriber Special Offer***

Readers of my blog can enjoy a 20% first-year discount! Click here for details >>

12 October 2024

By Maynard Paton

Mark Leonard has been described as the “best capital allocator you have never heard of“.

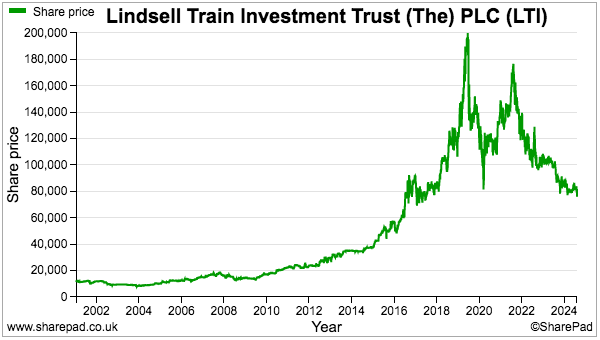

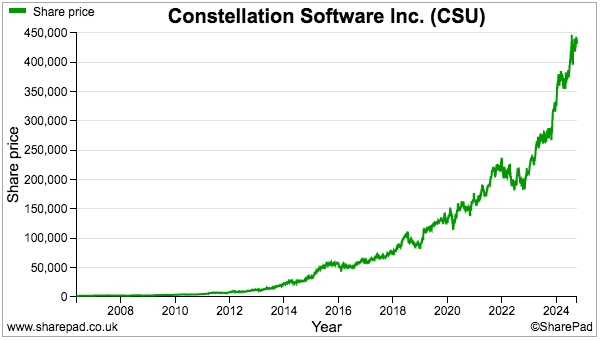

According to Forbes, Mr Leonard is now worth $5 billion after he established Constellation Software during 1995 and listed the group on the Toronto Stock Exchange during 2006. He then watched his shares soar more than 200-fold:

You may not have heard of Mr Leonard because he deliberately maintains an extremely low profile. He appears to have conducted only one public interview while pictures of him online are essentially variations of this particular image:

However, Constellation’s super stock price — currently supporting a £50 billion market cap — has gradually increased the number of investors who have heard of Mr Leonard…

…and the number of investors who have tried to replicate Constellation’s success. By 2018 Mr Leonard had seen enough copycats and decided to give up writing his annual Constellation letter. He lamented:

“For competitive reasons we are limiting the information that we disclose about our acquisition activity. We believe that sharing our tactics and best practices with a host of Constellation emulators is not in our best interest.”

Such has been the enthusiasm for how Mr Leonard created his immense wealth, a Constellation ’emulator’ has even emerged within the lower reaches of AIM.

Software Circle sports an £85 million market cap and is attempting its very own Constellation-like mega-bagger journey.

Let’s take a closer look.

Read my full SOFTWARE CIRCLE article for SharePad >>Maynard Paton