23 December 2024

By Maynard Paton

FY 2024 results summary for Tristel (TSTL):

- A record FY, showcasing revenue up 16%, profit up 32% and the dividend up 29%, with impressive 32% UK growth based upon 9% greater volumes and 23% higher pricing through a new NHS agreement.

- The retirement of the previous chief executive now makes sense after “purchasing bureaucracy” suddenly beset North American progress, which left TSTL alarmingly “a year behind” schedule after US partner Parker Laboratories proved ineffective with sales.

- The new chief executive has still to publish his financial targets, although the board has already re-committed to 5%-plus annual dividend growth while a new ‘boilerplate’ LTIP depressingly seeks only a 5.5% adjusted EPS CAGR to vest.

- The high-margin, cash-rich, low-tax accounts generally remain in good shape, but are let down by regular restatements alongside stagnant employee productivity that may be due to a 25% margin target limiting additional investment.

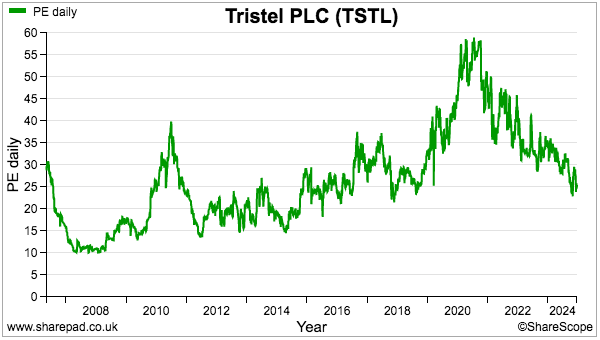

- The trailing 25x PE is the lowest since 2018 and could be justified by further meaningful growth within established markets, the prospect one day of lucrative US royalties, the ongoing ability to raise prices and the possibility of bumper surface-disinfection sales. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TSTL

- Results summary

- Revenue, profit and dividend

- Prior-year restatements

- Medical-device decontamination

- Surface disinfectants

- UK

- Overseas

- North America: royalties and bureaucracy

- North America: Parker Laboratories and potential opportunity

- Patents and competing technologies

- Share-based payments

- New LTIP

- Boardroom

- Financials: margin and employees

- Financials: balance sheet and cash flow

- New financial targets

- 2024 AGM statement

- Valuation

News links, share data and disclosure

- Annual results, presentation and webinar for the twelve months to 30 June 2024 published/hosted 21 October 2024;

- In-person investor meeting hosted 21 October 2024;

- Notice of AGM published 22 November 2024, and;

- AGM statement, result and voting published 16th December 2024.

- Share price: 380p

- Share count: 47,692,093

- Market capitalisation: £181m

- Disclosure: Maynard owns shares in Tristel. This blog post contains ShareScope affiliate links.

Why I own TSTL

- Develops the “simplest, quickest and most affordable high-performance disinfection” for medical devices, and faces limited direct competition due to proprietary chemistry, instrument-manufacturer approvals, scientific testimonies and regulatory hurdles.

- Enjoys a track record of superior growth founded upon a sizeable and resilient UK market position, alongside widening expansion opportunities abroad including — with the help of a new chief executive — the United States.

- Boasts financials that showcase superior gross margins, significant net cash, respectable cash conversion and relatively low operational capital, all of which underpin a bold commitment to lift the dividend at least 5% a year.

Further reading: My TSTL Buy report | All my TSTL posts | TSTL website

Results summary

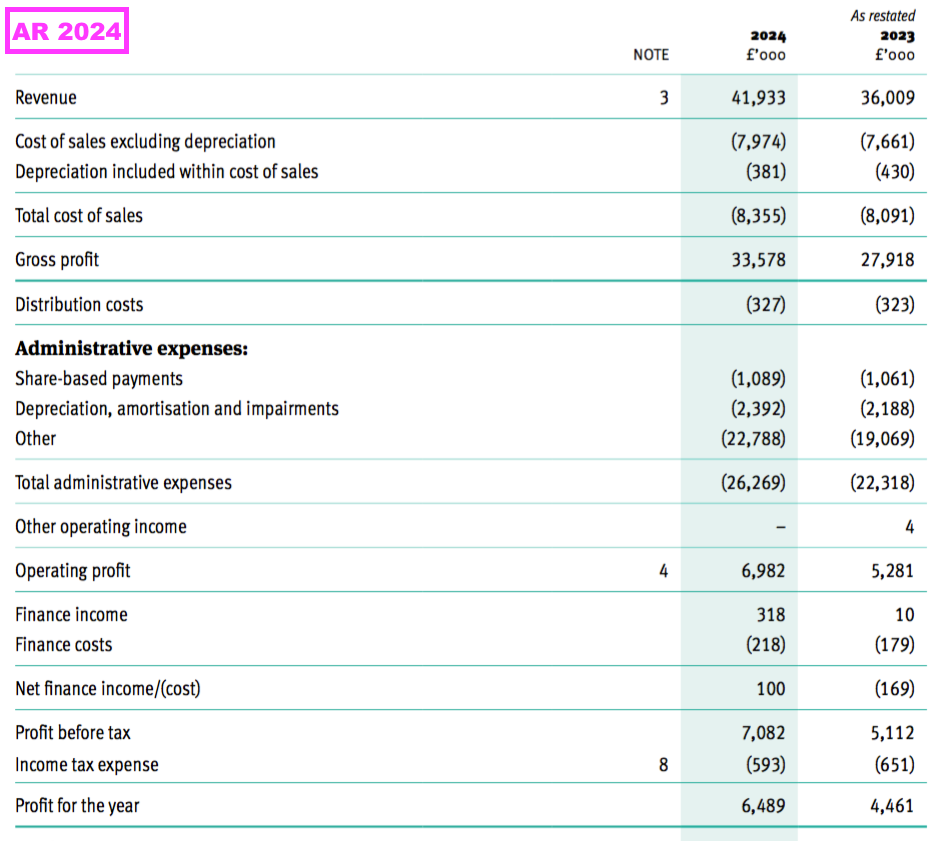

Revenue, profit and dividend

- An upbeat statement during July that summarised a “strong trading performance ahead of market expectations”…

[RNS July 2024]

“• Revenues for the year were up 16.4% to £41.9m (FY 2023: £36.0m), ahead of market expectations and above the Company’s performance target for revenue growth (an annual average of 10-15% over three years).

• Adjusted profit before tax* will be no less than £8.0m, ahead of market expectations and 29% ahead of last year (FY 2023: £6.2m).

• Tristel continues to be debt free and cash generative. Cash balances on 30 June 2024 were £11.6m (30 June 2023: £9.5m).”

- …had already ensured this FY would be very positive.

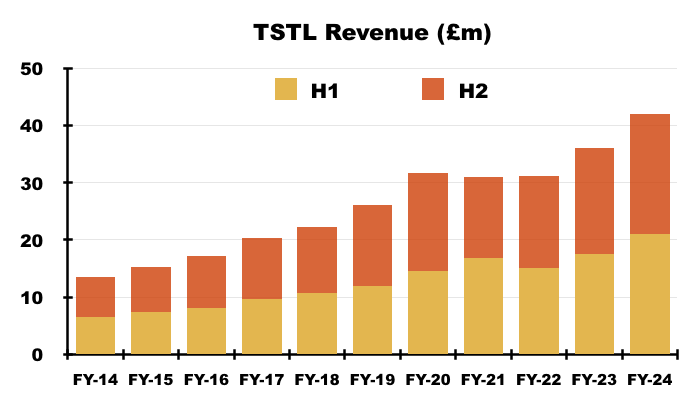

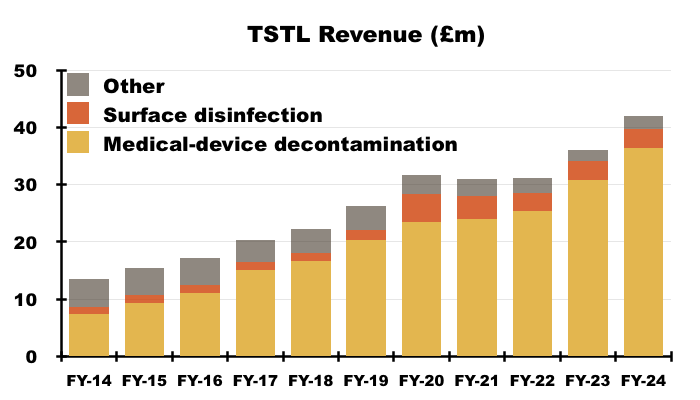

- FY revenue did indeed gain 16% to £41.9m to set a new FY record:

- FY adjusted profit before tax (i.e. profit before tax and share-based payments) was indeed “no less than £8.0m” at £8.2m, up 32%.

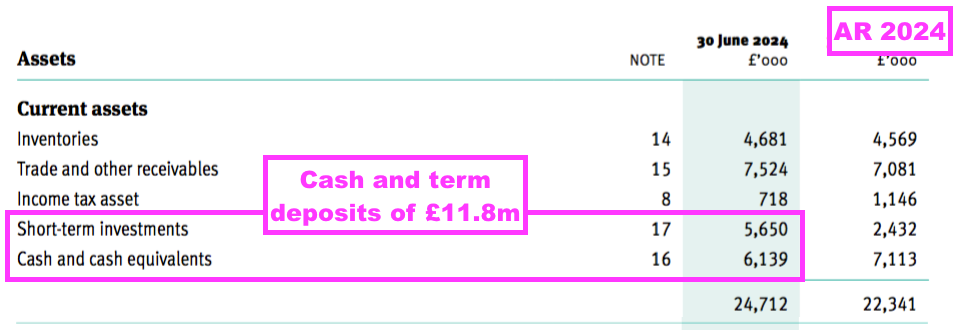

- And the FY cash balance was in fact £0.2m better than July’s prediction at £11.8m (see Financials: balance sheet and cash flow).

- This FY and the comparable FY were thankfully free of the revenue distortions — such as pandemic disruption, Brexit stock-piling and discontinued products — that had complicated TSTL’s progress between FYs 2020 and 2022.

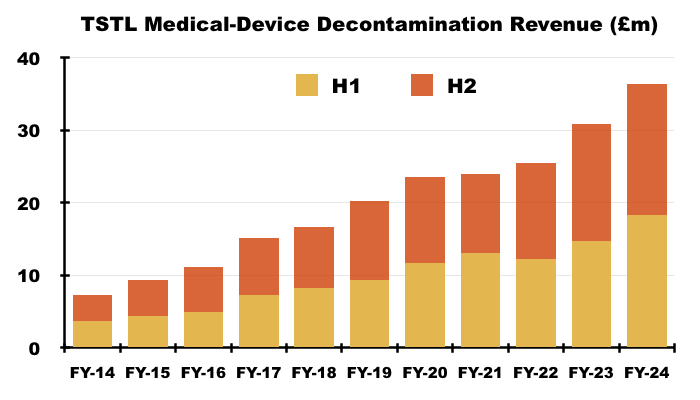

- After the preceding H1 reported H1 revenue up 20%, H2 revenue gained 13% to £21.0m — TSTL’s highest revenue for any six-month period.

- To underline how fast TSTL has grown during recent years, H2 revenue exceeded the £20.3m reported for FY 2017.

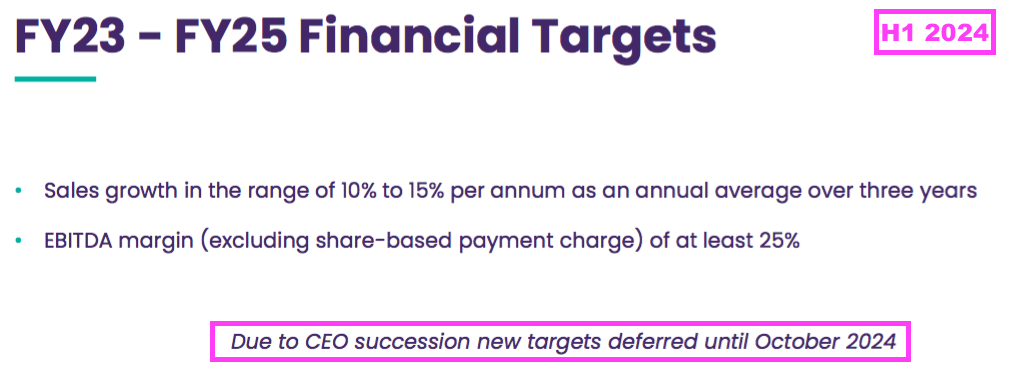

- This FY’s 16% revenue advance surpassed the group’s 10-15% revenue CAGR target:

“The Board and I remain committed to our financial plan for the three years to 30 June 2025, which was a continuation of the plan for the prior three-year period ending in June 2022. The three key financial targets of both the old and new plans are:

i. sales growth in the range of 10% to 15% per annum as an annual average over the three years

ii. the achievement in each year of an EBITDA margin (excluding share-based payment charge) of at least 25%, and

iii. to increase profit before tax (excluding share-based payments) year-on-year, independently of the other two targets.”

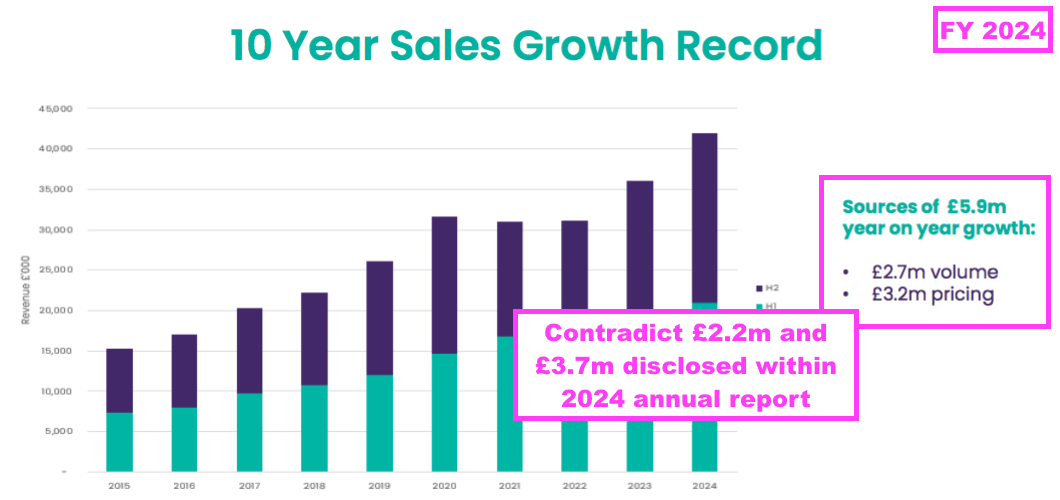

- TSTL commendably split this FY’s 16% revenue advance between volume (£2.2m) and pricing (£3.7m):

“Higher sales volume accounted for £2.2m of the £5.9m revenue growth and price increases accounted for the remaining £3.7m. This represents an average price increase of 11%, driven primarily by the UK where the increase has been higher because of supply agreements which require fixed pricing extending into future years.”

- The FY presentation contradicted the FY commentary by stating higher volumes accounted for £2.7m and higher prices accounted for £3.2m of the £5.9m total revenue advance:

- Assuming the FY commentary was correct and the average price increase was indeed 11%, then volumes must have improved by approximately 5% to reach the 16% total FY revenue advance.

- The reference to “supply agreements which require fixed pricing” in the UK relates to sales to the NHS supply chain, the pricing framework for which this FY confirmed would run for up to another six years (see UK).

- For further perspective on volumes and pricing, the preceding H1 had declared revenue up 20% split 12% through higher prices and 8% through higher volumes.

- If volumes increased by 8% during H1 and 5% during this FY, then volumes seemingly increased by approximately 3% during H2.

- Volume growth of 3% during H2 is not ideal given 8% was enjoyed during the preceding H1 and also the comparable FY.

- The FY webinar suggested seasonality may impact volume growth between H1 and H2:

“The northern hemisphere makes up 75% of our sales, where winter buying in preparation for high levels of infection gives a real boost to the October, November, December numbers, when as a consequence we see a strong half-one because of winter buying.”

- The FY webinar indicated near-term revenue growth would not be assisted greatly by further price increases:

“We think the most likely price increase that we will instigate is inflation and we’re settling down to 3-4% inflation and that will most likely be the increase that we implement from at different points in time in different countries. But in January, in March next year, we will be implementing that level of increase.“

- No doubt volume growth and price increases will be factors the new chief executive considers when he publishes TSTL’s new financial targets (see New financial targets):

- The preceding H1 had indicated this FY would unveil those new financial targets:

- But this FY delayed that unveiling:

“Having joined the business just a few weeks ago, I ask for a little time to work closely with stakeholders to review the company’s strategic direction. This process will ensure that we are well-positioned for the next phase of our growth journey. I look forward to updating investors on our financial targets beyond June 2025, as we define our goals to align with the growing opportunities in our core markets and new areas of expansion.”

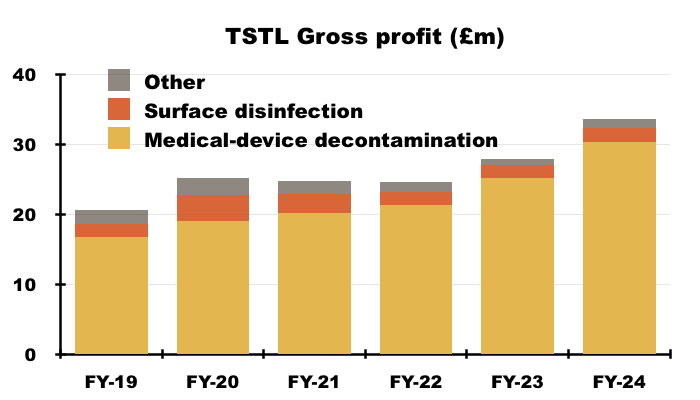

- This FY was the third consecutive FY complicated by a prior-year restatement. For the comparable FY, gross profit was restated from £29.2m to £27.9m and the gross margin was restated from 81% to 78% (see Prior-year restatements and Financials: margin and employees).

- As well as restatements, share-based payments remain a complicating factor when assessing TSTL’s profit (see Share-based payments).

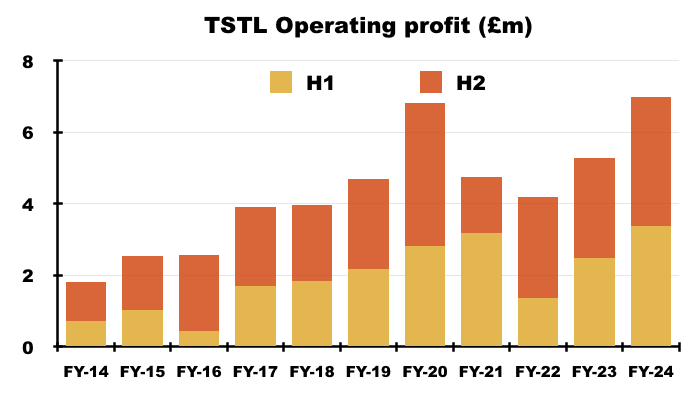

- Including share-based payments, this FY’s operating profit gained £1.7m, or 32%, to set a new FY record of £7.0m:

- Excluding share-based payments, this FY’s operating profit gained £1.7m, or 27%, to set a new FY record of £8.1m:

- Including share-based payments, H2 operating profit gained £0.8m, or 29%, to £3.6m.

- Excluding share-based payments, H2 operating profit gained £0.8m, or 26%, to £4.0m.

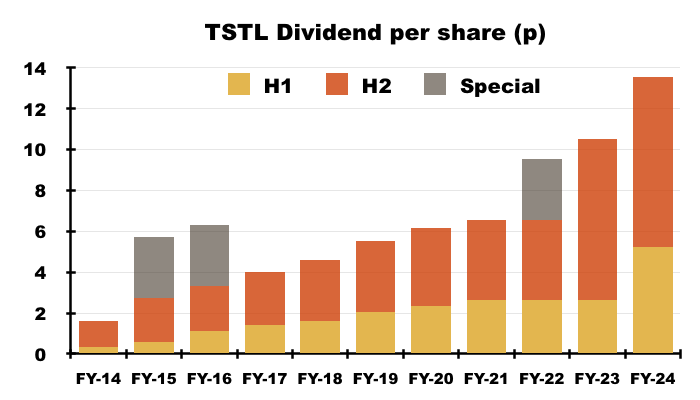

- The comparable FY revealed the ordinary dividend would advance by at least 5% a year — irrespective of whether earnings rise or fall.

- This FY repeated the 5% minimum dividend-growth rate:

“Going forward the Board’s intention is to increase the dividend annually, in line with the year’s increase in EPS, committing to minimum dividend growth of 5%.“

- Declaring a 5% minimum dividend-growth rate is a bold commitment, although whether the commitment ensures the new chief executive will unveil bold financial targets remains to be seen (see New financial targets).

- After the preceding H1 dividend was doubled to 5.24p per share, the final dividend was lifted 5% to 8.28p per share:

- The FY dividend was therefore 13.52p per share, up 29%, but covered only 1.13x by TSTL’s 15.34p per share adjusted earnings.

Prior-year restatements

- This FY was the third consecutive FY to reveal a prior-year restatement.

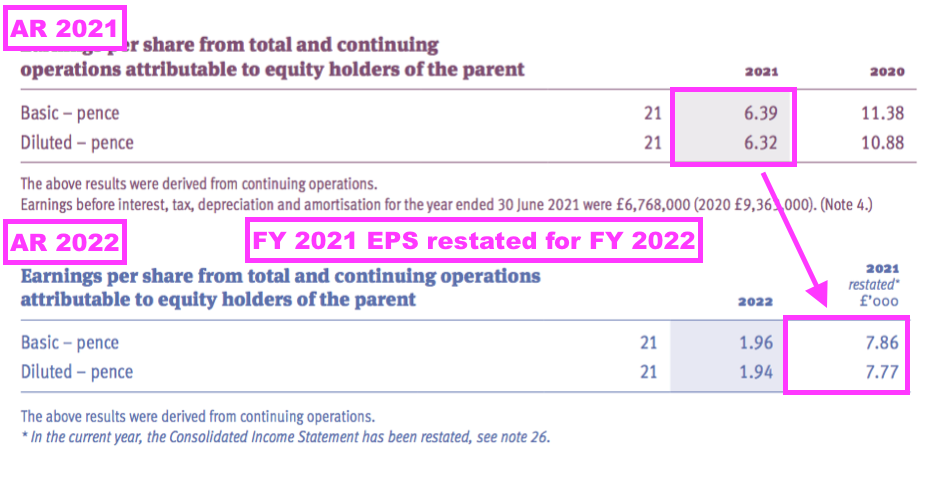

- To recap, FY 2022 revealed a prior-year restatement for FY 2021:

[FY 2022]

“During the current year, it was identified that deferred tax assets relating to unrecognised taxable losses of £3,600,000 in the UK had not been recognised in the prior year. Based on the circumstances in the prior year, these should have been recorded as a deferred tax asset at 19%, equating to £684,000. The prior year financial statements have been restated for this adjustment. In addition, in the prior year an income tax receivable for £170,000 was inappropriately classified as an income tax liability. The prior year comparatives have been restated to correctly reclassify the balance as an income tax receivable.”

- FY 2021 earnings that were originally declared as 6.39p per share were then revised 23% higher to 7.86p per share because of a much lower tax charge:

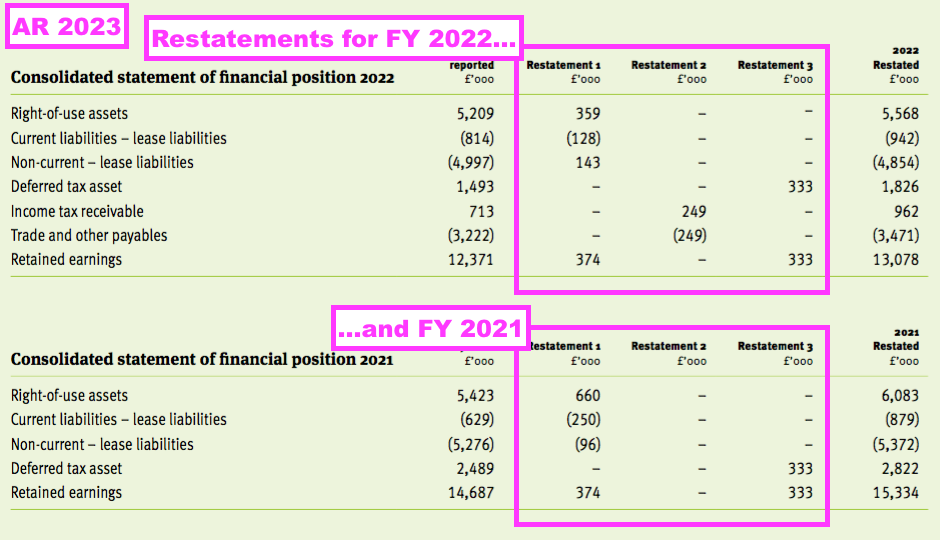

- Then the comparable FY disclosed a handful of minor prior-year restatements for FY 2022:

[FY 2023]

“Restatement 1

During the current financial year the Group adopted a suite of lease accounting software. The software has outlined the need for a restatement of the financial position of prior years which is detailed below. These differences emerged from varying discount rate applications and omitted leases, which in current year have been supplied by an independent third party due to the lack of borrowing within the Group and rectified respectively…

Restatement 2

During the current financial year it was identified that a corporate tax receivable balance had incorrectly been recorded as a sales tax payable in the prior year…

Restatement 3

During the current financial year it was identified that no adjustment had previously been made for the tax effect of unrealised intra-group profits…“

- This batch of restatements necessitated minor changes to FY 2021 as well as FY 2022…

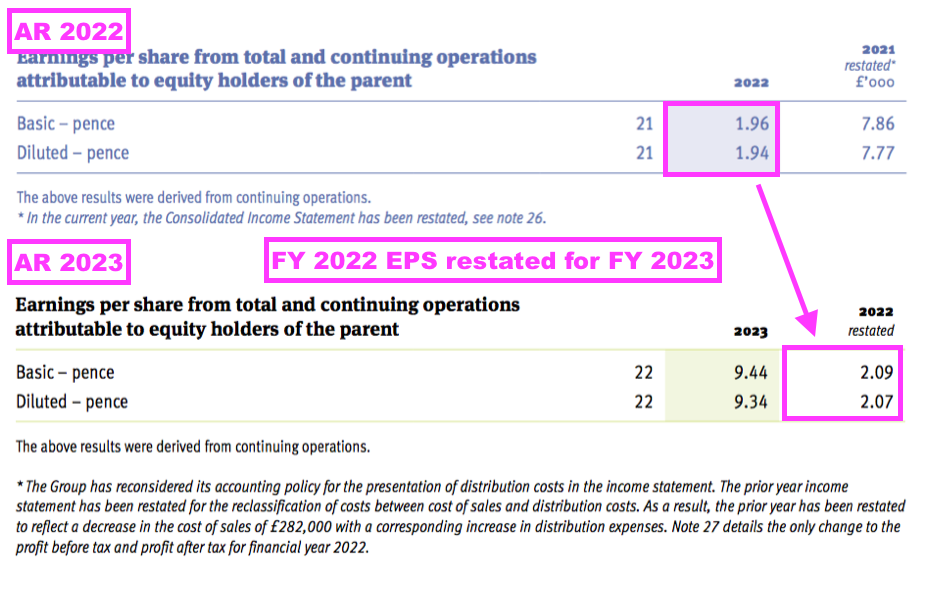

- …and meant FY 2022 earnings that were originally declared as 1.96p per share were revised 7% higher to 2.09p per share:

- These prior-year restatements announced for FY 2022 and FY 2023 meant net asset value for FY 2021 that was declared initially as £30,083k was restated to £30,767k for FY 2022 and then restated again to £31,414k for FY 2023.

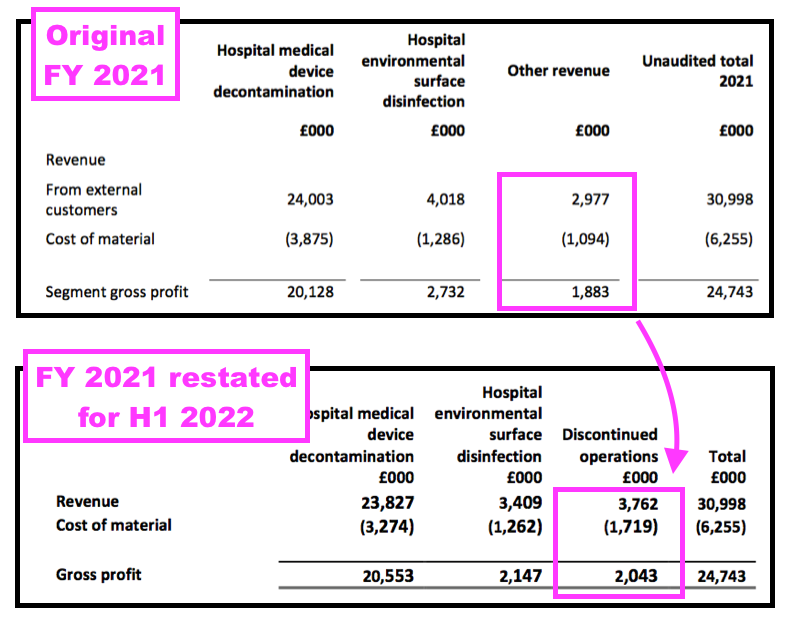

- These prior-year restatements coincided with TSTL deciding to distinguish between continuing operations and discontinued operations for H1 2022, which prompted the restatement of FY 2021’s divisional performances:

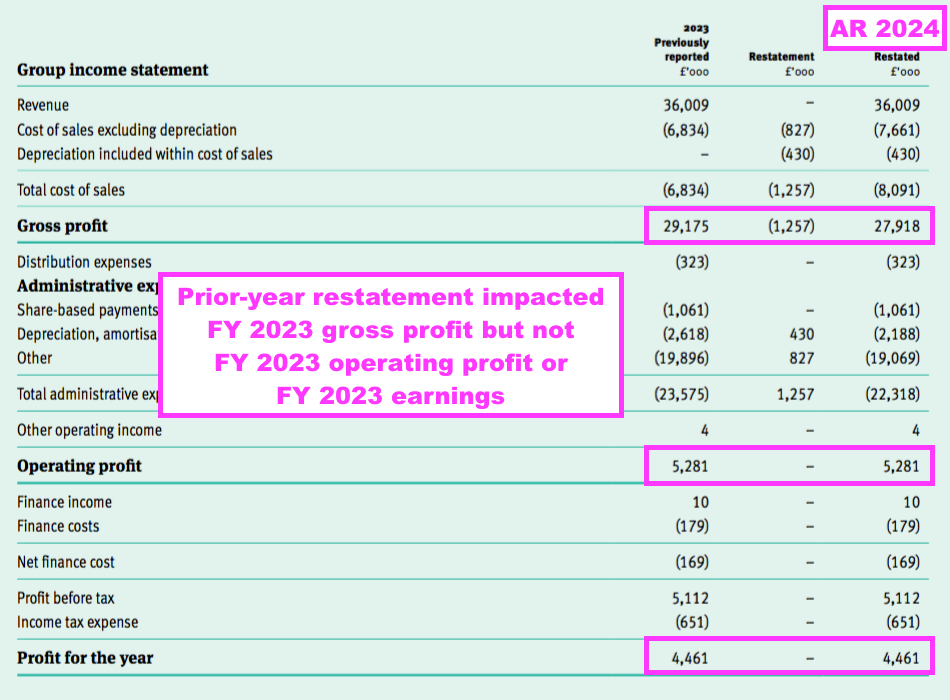

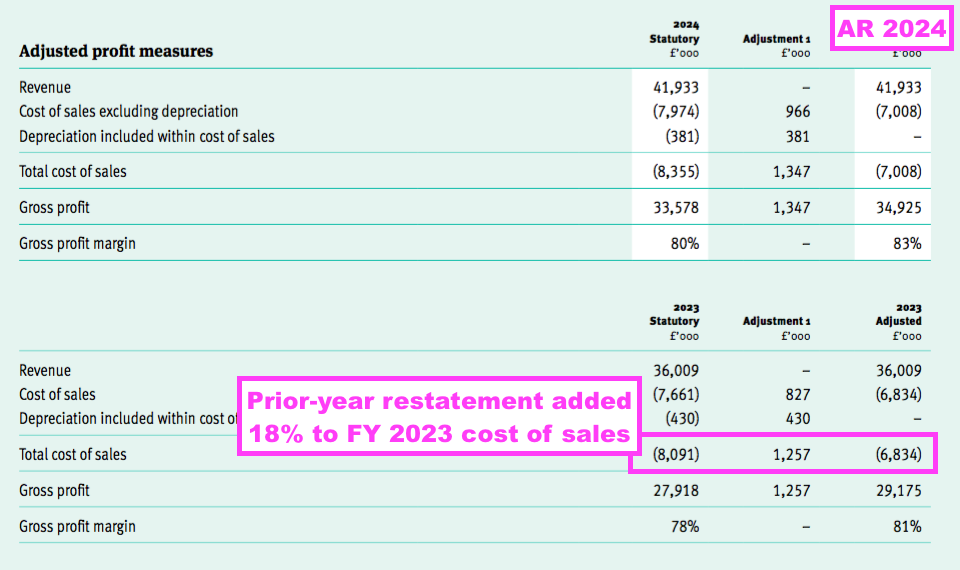

- This FY revealed a prior-year restatement for cost of sales, whereby £1.3m had been “erroneously” included within administrative expenses for the comparable FY:

“IAS 2: Cost of sales restatement

Within the prior-year income statement elements of the cost of production were erroneously included within administrative expenses, excluding share-based payments, depreciation, amortisation and impairment and depreciation, amortisation and impairments. £1,257,000 has been reclassified to cost of sales, £430,000 from depreciation, amortisation and impairments and £827,000 from administrative expenses, excluding share-based payments, depreciation, amortisation and impairment to align to the requirements of IAS 2. This has no overall effect on the total profit for the prior financial year. The adjustment does not impact the amounts previously presented on the balance sheet at 30 June 2022 and therefore a third balance sheet is not considered to provide a user of the financial statements with any additional information.”

- This FY’s prior-year restatement impacted gross profit and gross margin, but did not impact operating profit or earnings (see Financials: margin and employees):

- The FY webinar suggested TSTL’s latest prior-year restatement was due to certain costs becoming “material“:

“Looking at the gross margin as a whole… we have moved some of our overheads up to cost of goods this year. There are some production associated costs that now have become material so they tip the balance and move up into cost of sales.”

- But the misclassified expenses were already a sizeable £1.3m during the comparable FY, and the prior-year restatement added 18% to the comparable FY’s cost of sales:

- Management blamed the audit profession during the in-person FY meeting for this latest prior-year restatement:

- “There was a new partner at Grant Thornton who said ‘This is the way we want it to be calculated’“;

- “Our arguments [about the same audit firm approving the old calculation last year] fell on deaf ears. It’s like ‘Do you want your accounts signed off or not?’“;

- “We can’t tell you how horrified we are when there’s a restatement“, and;

- “There is no negative reflection on the Tristel team at all.”

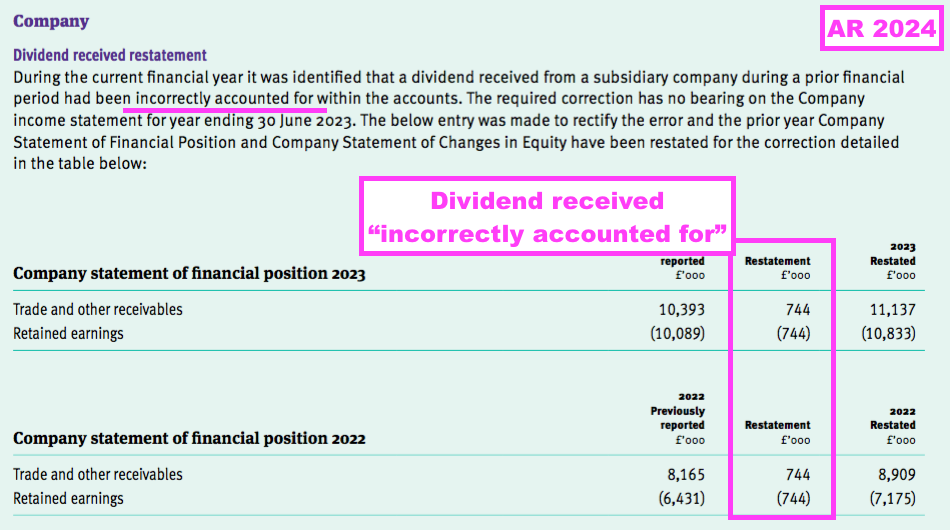

- This FY also revealed a prior-year restatement for an “incorrectly” recognised dividend within the parent-company accounts…

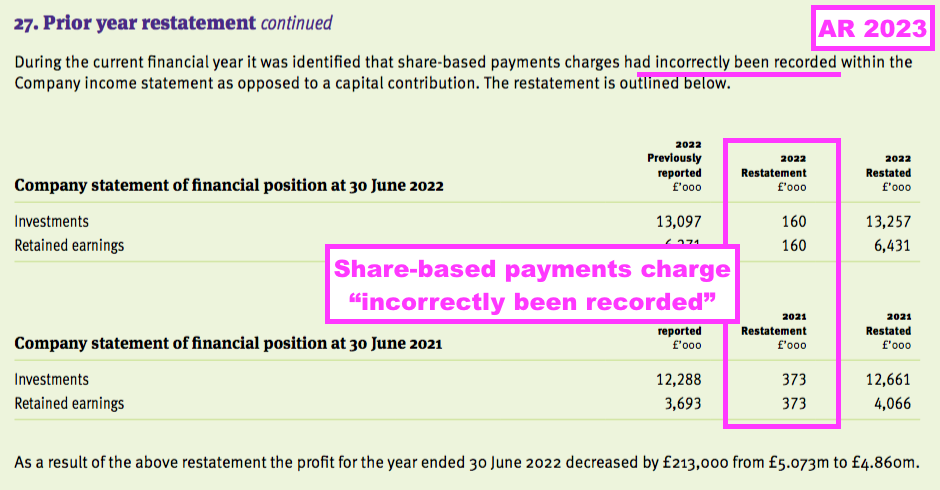

- …while the comparable FY revealed a prior-year restatement for “incorrectly” recorded share-based payments within the parent-company accounts:

- None of restatements during the last few years has been individually material to TSTL’s overall financial statements.

- But the revisions continue to rack up and shareholders are right to question whether:

- Any figures presented within this FY will be revised for FY 2025, and;

- TSTL’s accounting function requires some enhancement.

- Indeed, TSTL does appear highly unusual among established small-cap companies to have incurred regular prior-year restatements within its accounts….

- …especially when other small-caps must also experience a similar rotation of auditors and audit partners.

- This FY claimed TSTL’s audit committee considered the “value for money” provided by auditor Grant Thornton:

“During the 2023-24 year the Audit Committee met on two occasions to:

• Discuss findings and hear recommendations arising from the annual audit

• Discuss with the Company’s external auditors matters such as compliance with accounting standards

• Monitor the external auditor’s compliance with relevant ethical and professional guidance on the rotation of audit partners, the level of fees paid by the Company and other related requirements

• Consider the performance and value for money of the Company’s external auditors

• Approve the appointment of the Company’s external auditors, including their terms of engagement and fees.“

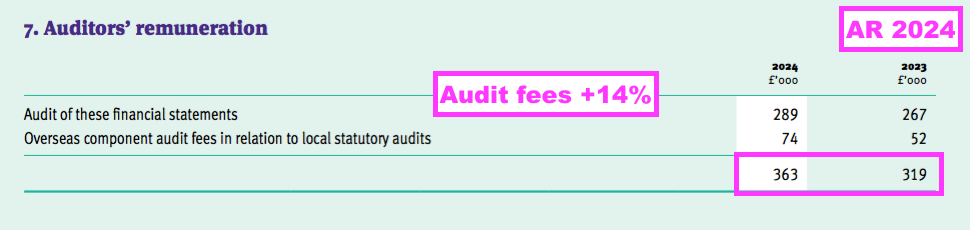

- FY audit fees increased 14% to £363k…

- …and absorbed 0.87% of FY revenue — the largest proportion within my portfolio:

| Company | Year to | Revenue (£k) | Auditor | Fees (£k) | Fees/ Revenue |

| ASY | 31-Dec-23 | 78,747 | Mazars | 309 | 0.39% |

| BVXP | 30-Jun-24 | 13,607 | Kreston Reeves | 33 | 0.24% |

| CLIG* | 30-Jun-24 | 69,453 | Grant Thornton | 283 | 0.41% |

| MCON** | 31-Dec-23 | 156,931 | Grant Thornton | 234 | 0.15% |

| MTVW | 31-Mar-24 | 79,472 | Moore KS | 105 | 0.13% |

| SUS | 31-Jan-24 | 115,437 | Mazars | 200 | 0.17% |

| SYS1 | 31-Mar-24 | 30,019 | Haysmacintyre | 110 | 0.37% |

| TFW | 30-Jun-24 | 175,798 | PwC | 538 | 0.31% |

| TSTL | 30-Jun-24 | 41,933 | Grant Thornton | 363 | 0.87% |

| WINK | 31-Dec-23 | 9,265 | Crowe | 69 | 0.74% |

(* figures in USD **figures in EUR)

- I am therefore not clear how TSTL’s audit committee decides how the auditor delivers “value for money“.

- Perhaps TSTL incurs relatively greater audit fees due to the regular corrections required to its accounts.

- The board has recently recruited a new chief executive while another executive has stepped down to focus on managing the group’s French subsidiary. I would not be averse to further director changes to help prevent further accounting restatements and inconsistencies within shareholder powerpoints (see Boardroom).

Medical-device decontamination

- TSTL’s wipes and foams that decontaminate medical devices remain by far the group’s most successful products:

- During this FY, 87% of revenue and 90% of gross profit were generated by the medical-device wipes and foams:

- H2 revenue from the medical-device wipes and foams improved 12% to £18.0m, which meant FY revenue from the wipes and foams finished 18% higher at £36.3m:

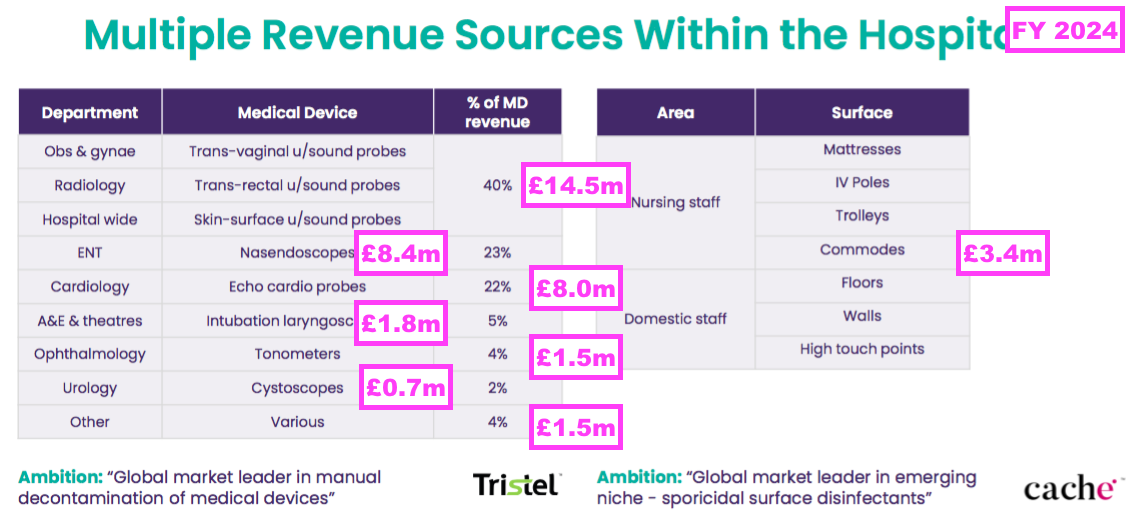

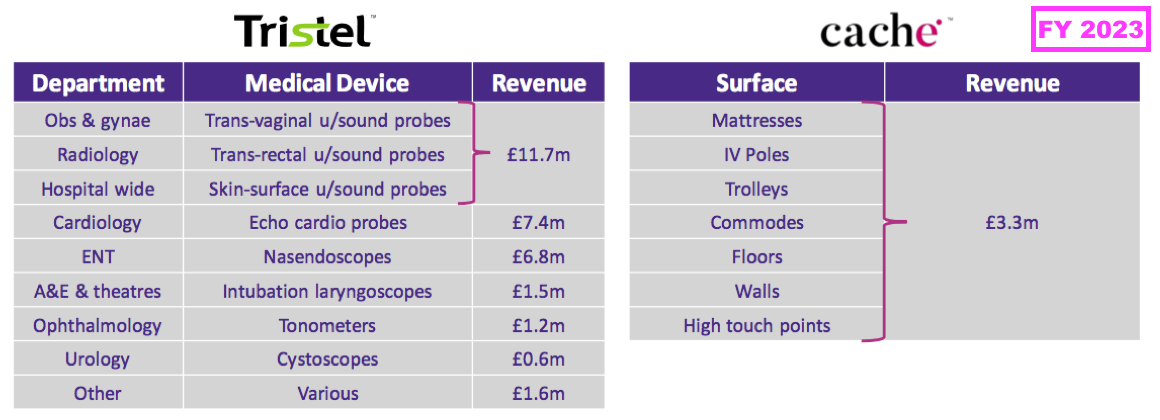

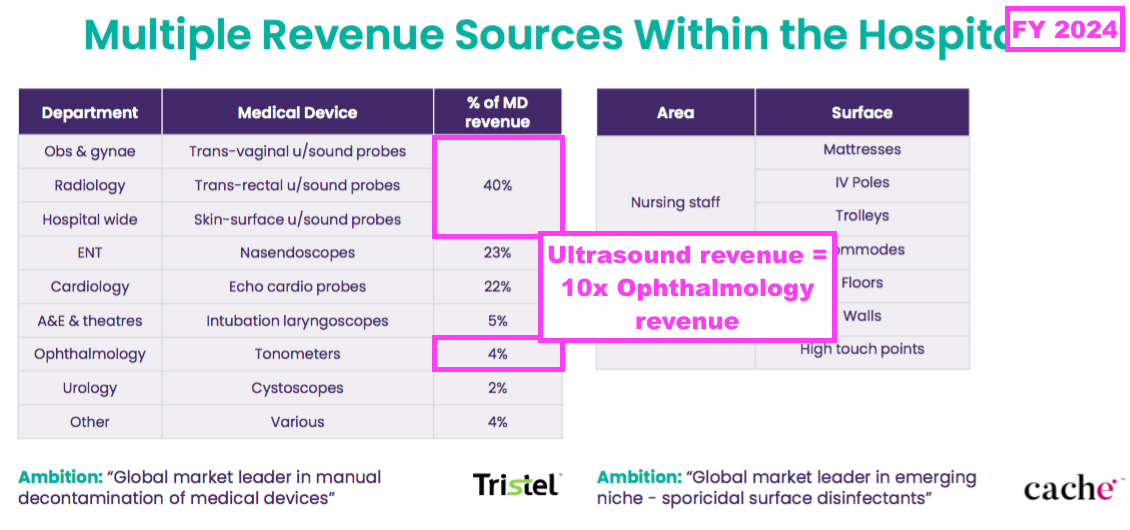

- This FY provided a useful breakdown of revenue generated by different hospital departments:

- Ultrasound probes remain the most popular medical device for the wipes and foams, representing 40% or £14.5m of FY medical-device revenue (and 35% of FY total revenue).

- The comparable FY conveyed the following breakdown:

- This FY therefore enjoyed medical-device revenue growth throughout all of TSTL’s main hospital departments:

- Ultrasound: +24%

- ENT: +23%

- Cardiology: +8%

- A&E and Theatre: +21%

- Ophthalmology: +21%

- Urology: +21%

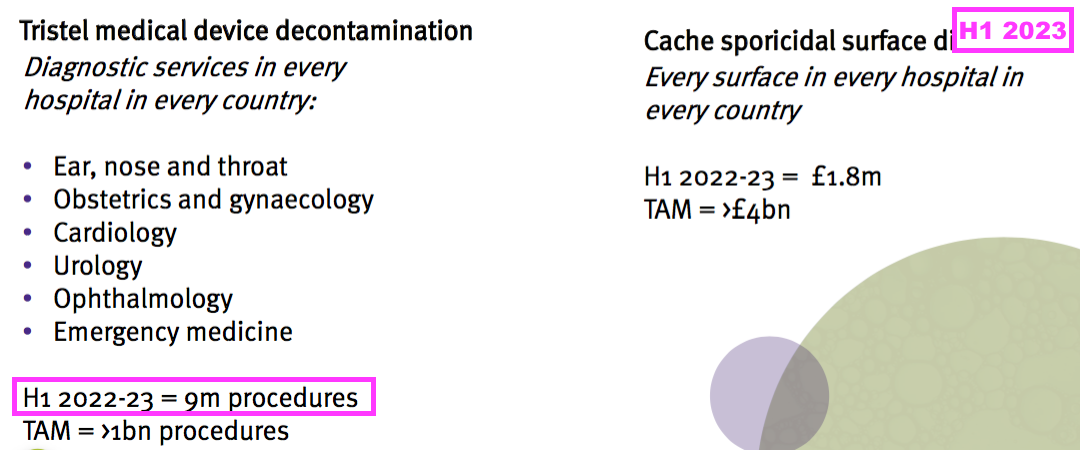

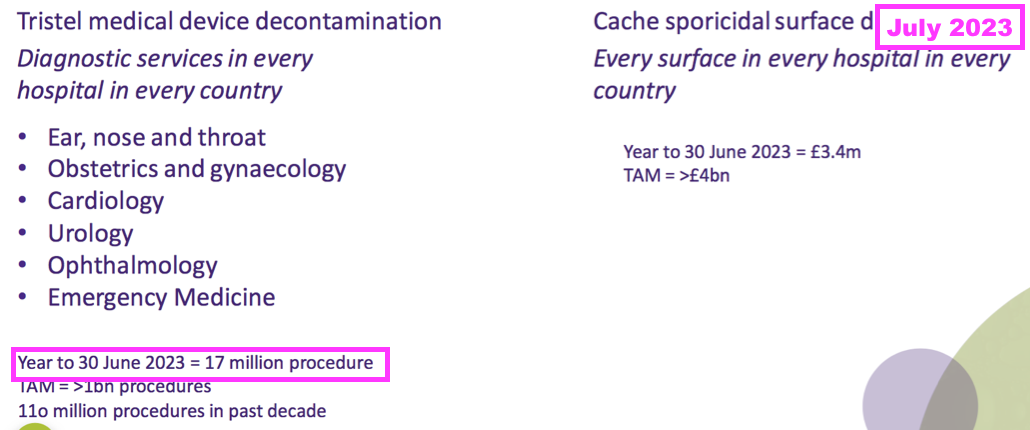

- The number of decontamination procedures undertaken using TSTL’s wipes and foams was published during the comparable FY…

- …but sadly went missing during this FY.

- Calculating a revenue per procedure (and in particular, per ultrasound procedure) can help shareholders gauge the market potential of the United States (see North America: Parker Laboratories and potential opportunity).

- My online searching shows TSTL’s Trio Wipes system available to buy for £377 + VAT and its Duo ULT foam available to buy for £264 + VAT. These online prices have increased for both products by £13 since my FY 2023 review.

- The Trio Wipes system contains enough wipes to conduct 50 disinfections and therefore costs the purchaser £7.54 per disinfection (£377/50). The Duo ULT foam gives 310 doses — equivalent to 155 disinfection procedures — and therefore costs the purchaser £1.70 per disinfection (£264/155).

- TSTL’s income will be less than £7.54 or £1.70 per disinfection because:

- A gross margin will be captured by the retailer selling the wipes and foams, and/or;

- Major buyers can buy in bulk direct through TSTL at reduced prices.

Surface disinfectants

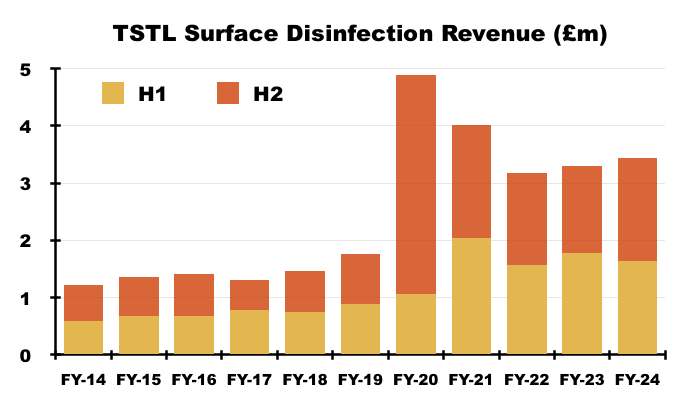

- FY revenue from TSTL’s hospital-surface disinfectants gained 4% to £3.4m:

- After H1 surface revenue declined 8%, H2 surface revenue advanced a welcome 18% to £1.8m — the highest six-month level for surface revenue since H2 2021 (£2.0m).

- The regulatory approval of TSTL’s new TANK system during February possibly assisted the division’s H2 performance:

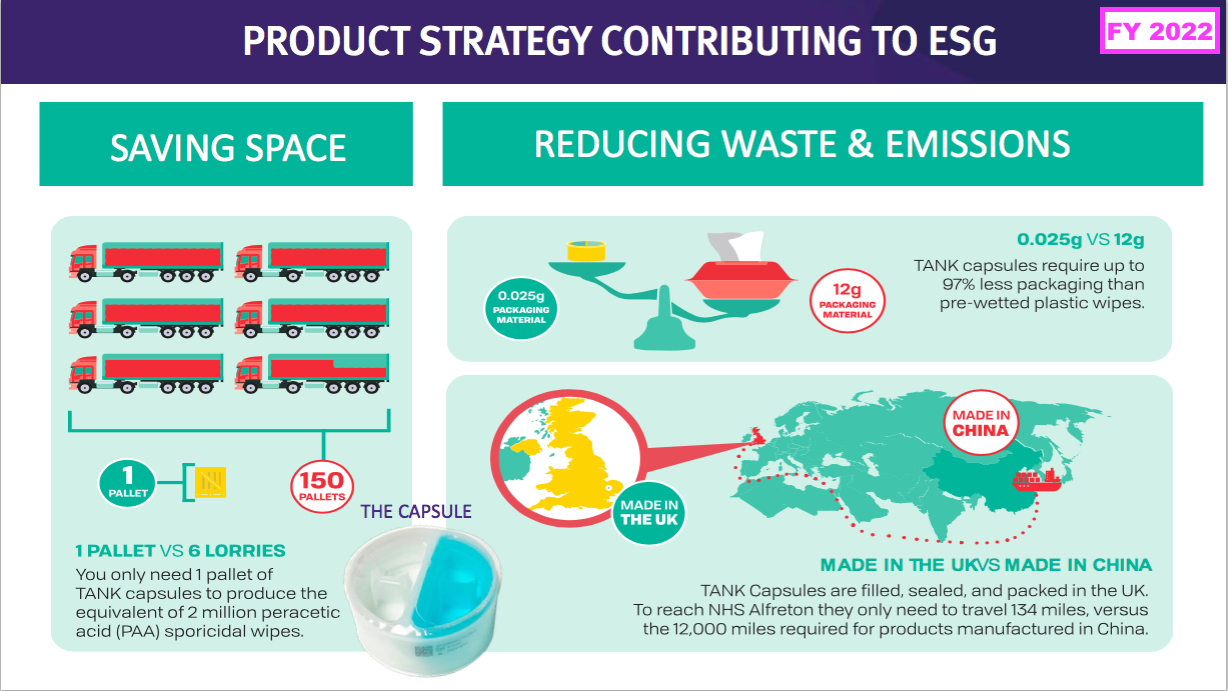

“Our second product range, Cache, made slower progress during the year. Revenue was £3.4m compared to £3.3m in the previous year. As announced in February, the Company gained Medical Devices Regulation 2002 (UK MDR) and the European Union Medical Device Regulation 2017/745 (EU MDR) approval of its TANK ClO2 Sporicidal Disinfectant system. These newest additions to the Cache range, which provides sporicidal surface disinfection in a format which is a sustainable alternative to commonly used pre-wetted plastic wipes, and our continued success in gaining regulatory approvals in key markets, give us confidence that the Cache range will deliver significant sales growth going forward.”

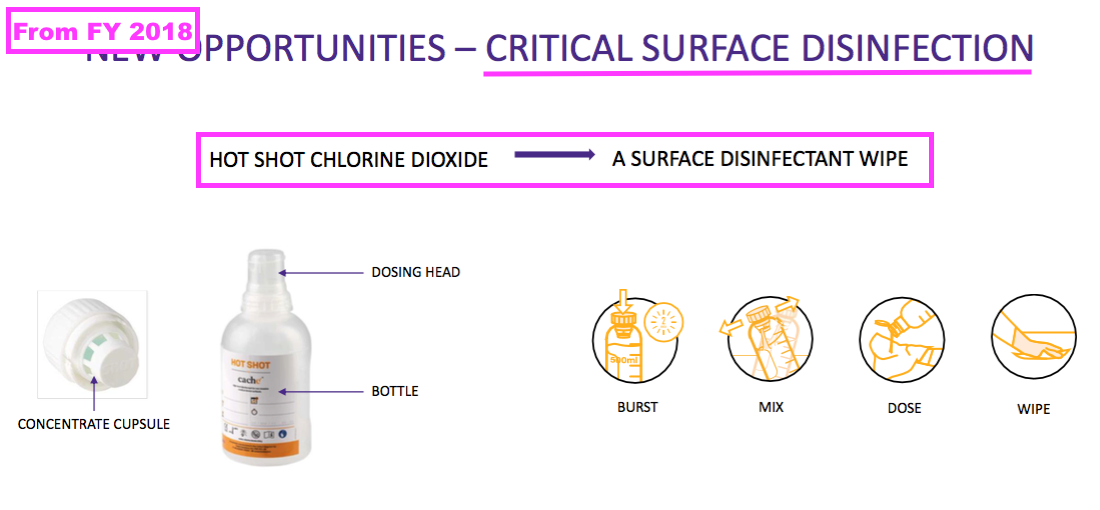

- Development of new surface products has been slow going, with prototypes showcased as far back as FY 2018:

- Save for the pandemic panic-buying of FYs 2020 and 2021, demand for TSTL’s surface disinfectants has struggled to take off due to higher pricing versus less effective alternatives.

- But the preceding H1 webinar reiterated the new TANK system would offer pricing comparable to the low-cost alternatives:

[H1 2024]

“Certainly the surface disinfection market is not willing to pay the premium that that the device disinfection market is willing to pay.

So we’ve designed our [TANK] product for two purposes: one, to address bleach, which is used to mop floors and clean large surface areas within the hospital, and; two, to be used for damp-dusting around the patient, so mattresses, UV poles, trolleys, bedside tables, all of those areas where patients are placed and they are high touch surfaces so in that instance a sporicidal disinfectant is really, really important.

Not every hospital can afford to use a sporicide around the patient, so we are bringing our product to market at the lowest possible price to combat the products that are incumbent within floor cleaning, which is bleach, and near patient areas, which tend to be plastic wipes pulled out of a flow wrap for continual use. We can we can rival both of those products and price [TANK] at the lower of the two prices.”

- This FY’s webinar explained why NHS England would consider switching from using 600 million plastic wipes to TSTL’s surface products:

“NHS England is looking to not only address cost savings… but has some significant goals with regards to sustainability. Today they are using 30 million chlorine tablets. Chlorine is damaging to the clinical infrastructure, it is not meeting the efficacy demands of the hospitals and they need to find an alternative to that. In the same way, NHS England is using 600 million pre-wetted plastic disinfection wipes annually and those wipes are not fitting into their sustainability goals either.”

“So why would the customer want to swap to our [Cache surface] products? It’s very simple. We are giving them a product that is convenient, simple to use but also one that is meeting their demands. It meets all their efficacy needs, it meets their environmental-sustainability needs and is allowing them to adopt a technology that is going to be transformational to what they’re trying to achieve. So now it’s about executing on our Cache portfolio.”

- The FY webinar helpfully disclosed NHS England spent £20m a year on alternative disinfection wipes:

“Currently NHS England spends £20m a year on pre-wetted wipes and our TANK system is going head to head with those exact pre-wetted plastic wipes, so that gives you an idea of the target for us”

- Spending £20m a year on 600 million low-grade surface wipes therefore costs NHS England 3.3p a wipe.

- The FY webinar was bullish on the prospects for the new TANK surface product:

“What we would just say is that we have high expectations for Cache. We feel very confident now we’ve got this more complete range with the MDR approvals in Europe. We also recognise that it’s going to be a growth driver for the business, so we’re investing significantly to get that success.”

- Management made the following surface-cleaning points during the in-person FY meeting:

- Surface products will not enjoy the “high” gross margin of the medical-device wipes and foams, but will instead be “slightly lower” (see Financials: margin and employees);

- The new TANK system is an “elegant solution“, unlike an earlier surface-cleaning product, and;

- Work is required to “focus” the sales team on generating surface revenue.

- The preceding H1 webinar claimed the new surface products could one day generate sales equal to those of the medical-device wipes and foams:

[H1 2024]

“How far do we think we can go with our Cache product range? I’m not going to say when, but in time we expect it to rival the size of our medical-device sales. It is a huge market. It’s a niche for us because we provide a very high level disinfecting performance level and we can do that at the price of a low- or intermediate-level competitive product. So there is a huge opportunity for us to be transformational in the surface-disinfection Market. Although it sounds like a big ask to grow our Cache market to the size of our Tristel market there is the potential for it.“

- TSTL will need to capture a significant market share of the hospital surface-cleaning market for the new TANK product to generate sales anywhere close to the amount earned by the medical-device wipes and foams.

- Indeed, during this FY, medical-device revenue of £36m was 10-11x the size of surface-disinfection revenue of £3.4m.

- To put the £20m spent by NHS England on surface-disinfection wipes into context, TSTL’s medical-device revenue in the UK during this FY was £13m (see UK).

- My online searching found 200 basic wipes for £7.55 + VAT, or 3.8p + VAT a pop.

- For perspective, assuming TSTL price-matches the 3.3p NHS England seemingly spends on each surface wipe, the TANK product would need to sell the equivalent of more than a billion surface wipes to equal this FY’s £36m revenue earned from the medical-device wipes and foams.

- This TSTL website showcases the new surface disinfectants and their environmental credentials versus pre-wetted plastic wipes:

- In theory at least, a much more effective surface cleaner that price-matches low-grade plastic wipes — as well as being much more environmentally friendly — ought to have a big future…

- …or leave TSTL with very awkward questions to answer should surface-disinfection sales never take off.

- Another awkward question might concern the Trio Wipes system using plastic wipes when TSTL is promoting the environmental benefits of TANK against similar wipes:

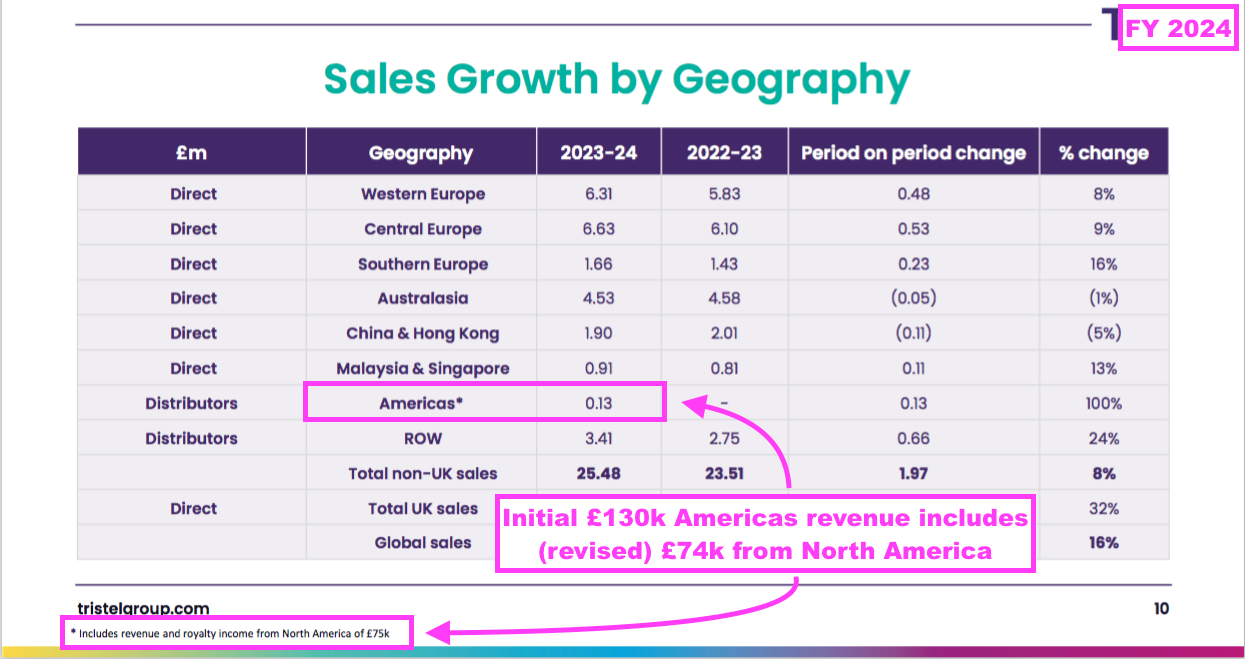

UK

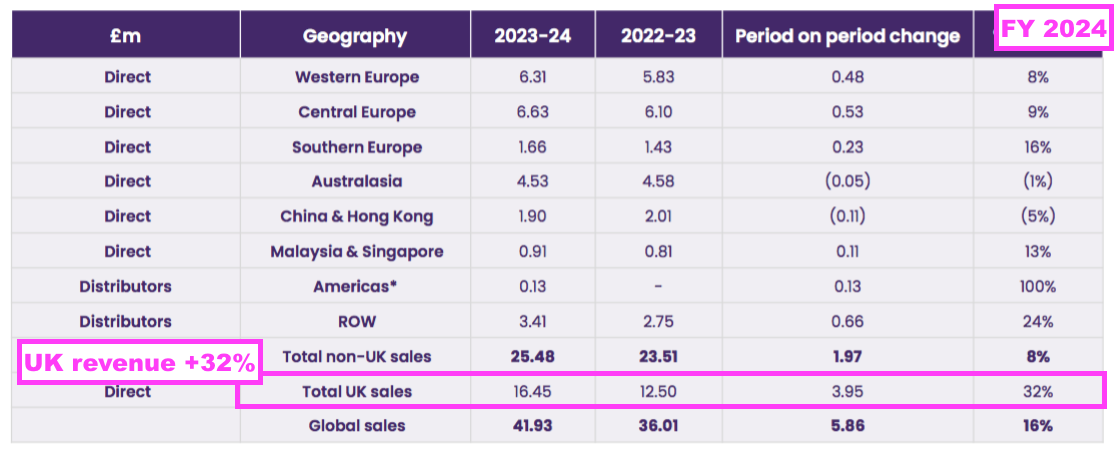

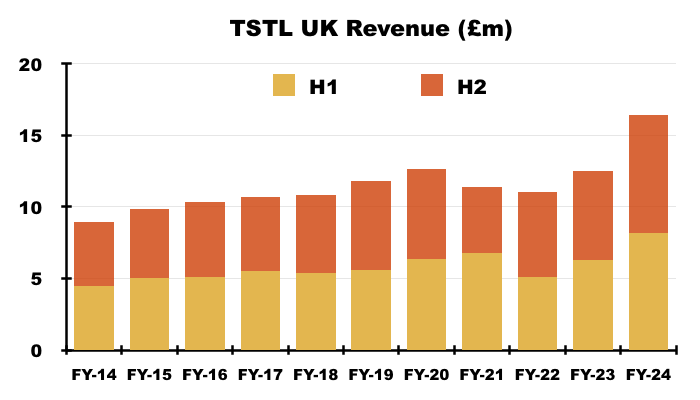

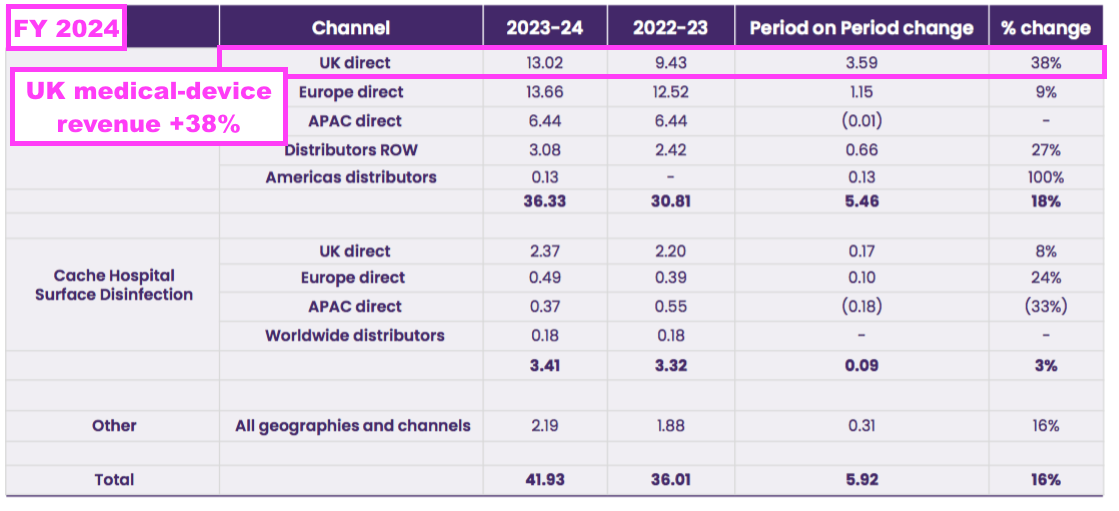

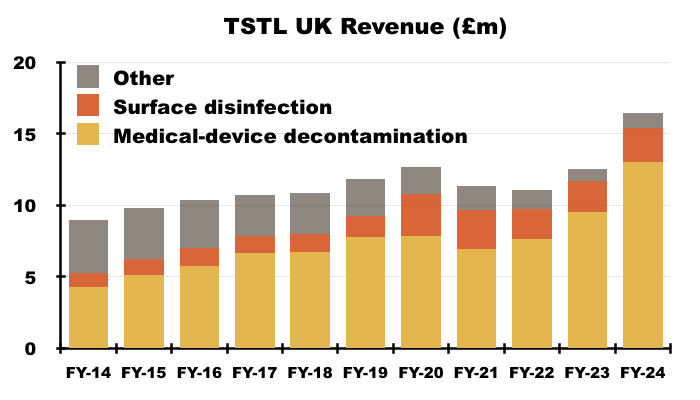

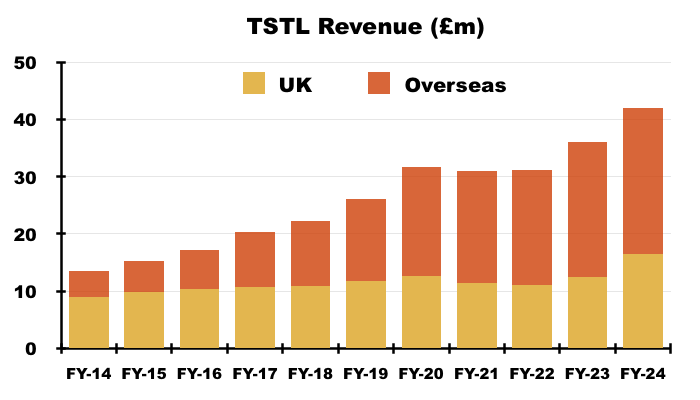

- The UK remains TSTL’s largest individual market after FY UK revenue gained a startling 32% to set a new FY UK record of £16.5m:

- The aforementioned “supply agreements which require fixed pricing” for the NHS undoubtedly underpinned the 32% improvement.

- The FY webinar commendably revealed how UK revenue growth was split between volume and pricing:

“The UK has shown the highest growth year-on-year with an increase of £3.95m, which is 32%. £1.1m of that £3.95m comes from volume, and £2.8m from pricing.”

- The £1.1m/£2.8m split suggests extra UK revenue gained 9% from additional volume and 23% from higher pricing.

- Volumes growing 9% within TSTL’s “most mature market” is very welcome, and the FY webinar suggested new medical devices and a greater frequency of usage had supported UK progress:

“Seeing at least £1m of volume growth from a market that we’ve been selling into for 20-plus years with this product set does demonstrate that we have not reached saturation point in our most mature market.

New devices are constantly being found within hospitals that are relevant for decontamination by our products, and the use of diagnostic devices within hospitals is constantly increasing with population growth and more advanced healthcare.“

- Volumes growing 9% within the UK is all the more impressive given the preceding H1 webinar reiterated the high levels of Tristel usage within the NHS:

[H1 2024]

“We measure [NHS penetration] by different areas of the hospital. As an example, we estimate… within the NHS around 60-70% of ultrasound procedures… use a Tristel product. The ENT market is about the same level of penetration for Tristel products used to decontaminate nasendoscopes. Within Cardiology for T probes, we have a very high level of penetration, in the region of 85-90%… We do certainly sell into every hospital within the UK. In some hospitals we are widely used and in others less so.“

- I trust this FY’s impressive 9% UK volume growth was not due to hospitals stock-piling product ahead of a significant price rise…

- The FY webinar confirmed a new multi-year agreement with the NHS had underpinned the 23% extra UK revenue from higher pricing:

“The [UK] pricing has come from a contract that we’ve entered into with the NHS. It’s a three-year contract that we have, and we expect it to be extended by the NHS for another three years. We took advantage of the long contract to put in a relevant inflationary increase based upon that six-year period.”

- Bear in mind UK prices for medical-device wipes and foams may have increased by much more than 23%, given such revenue during this FY gained a staggering 38% to £13.0m:

- Medical-device UK revenue supported 79% of total UK revenue during this FY, the highest FY proportion ever:

- TSTL’s income from the NHS supply chain can be deduced from the revenue disclosure of its largest customer:

“Hospital medical device decontamination revenues were derived from a large number of customers but include £9.0m from a single customer in the UK which makes up 25% of this product division’s revenue (2023: £6.1m, being 20%). Hospital environmental surface disinfection revenues were derived from a number of customers but include £2.0m from a single customer in the UK which makes up 57% of this product division’s revenue (2023: £1.8m, being 55%). Other revenues also were derived from a number of customers, with the largest customer in the UK accountable for £0.3m, which represents 14% of revenue for that product division (2023: £0.2m, 9% from a single customer). During the year 27% of the Group’s total revenues were earned from a single customer (2023: 22%).“

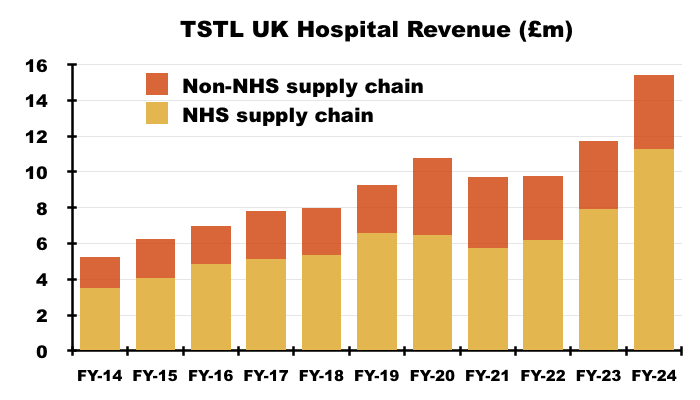

- The NHS supply chain generated FY revenue of £11.3m, which represented 73% of total UK revenue — the highest proportion since at least FY 2013:

- The NHS price increase helped total UK revenue to represent 39% of total FY revenue — the highest FY UK proportion since FY 2020 (40%):

- Longer term though, UK revenue has progressively become a smaller part of TSTL as the group expanded overseas through deft purchases of international distributors (see Overseas).

- Still, the UK may continue to expand at a respectable rate; the comparable FY (point 19e) had employed a 9% revenue growth rate to test the value of TSTL’s UK goodwill:

[AR 2023]

“Tristel UK For Tristel UK, the key assumptions used to determine the recoverable value of goodwill are those regarding discount rates and growth rates… Based on a revenue growth rate of 9%, the net present value of future cash flows exceeds the carrying value of £8.602m by £64.390m, as such no impairment has been recorded.”

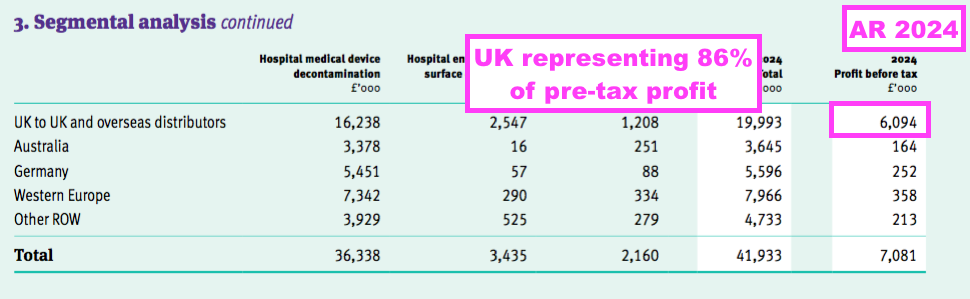

- This FY revealed segmental profit for the UK and other sales regions:

- A UK pre-tax profit of £6.1m represented 86% of group pre-tax profit, despite UK sales representing 39% of total revenue.

- The comparable FY’s webinar explained the UK profit bias, citing the group’s “transfer pricing policy” and wishing to “achieve the best tax profile“.

- Almost all of TSTL’s manufacturing occurs in the UK, and the products are sold to the group’s overseas divisions on an ‘arm’s length’ basis for resale within their respective markets.

- TSTL therefore registers its ‘manufacturing profit’ within the UK.

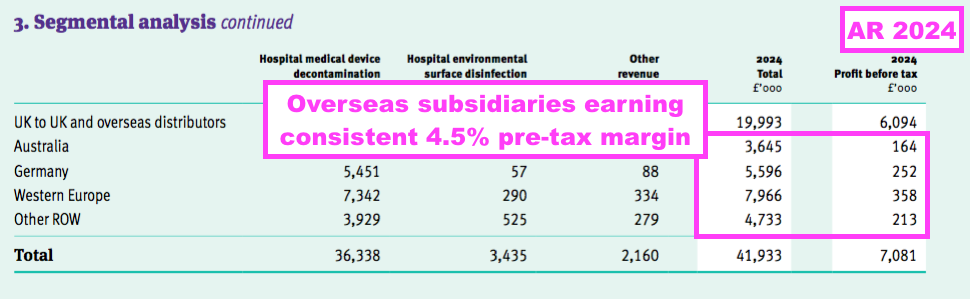

- The comparable FY’s webinar noted all the overseas sales regions have their profit margin set at 4.5%.

- A 4.5% margin was once again declared for all of the overseas regions for this FY:

- FY UK revenue of £16.5m remains the benchmark for the sales potential of other countries.

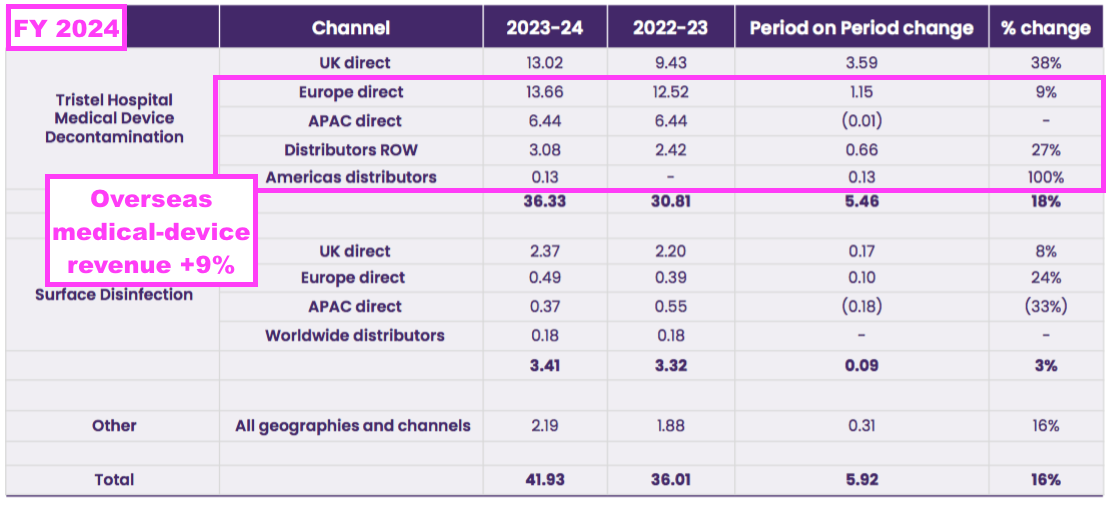

Overseas

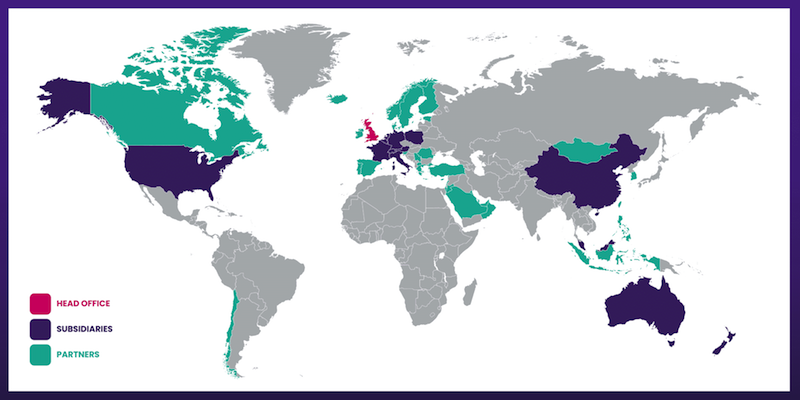

- Overseas revenue is derived from a mix of direct operations and independent distributors that combine to sell TSTL’s products within what this FY claimed were 61 countries:

- 61 countries is 21 more than the 40 cited by the comparable FY, and TSTL appears not yet to have updated the map above to properly identify the new sales territories.

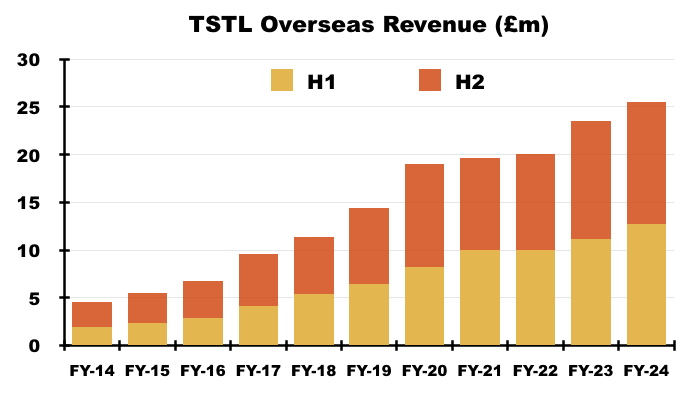

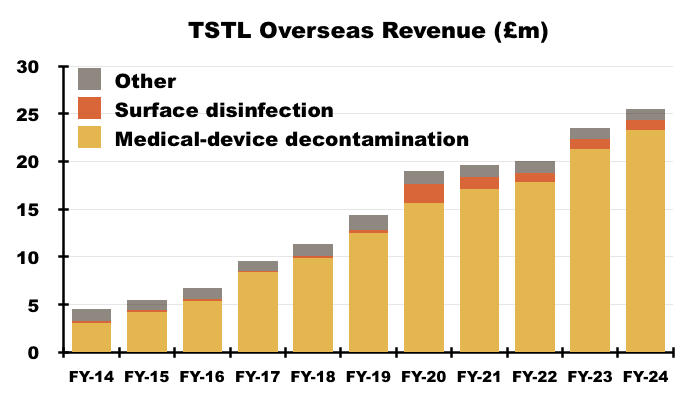

- FY Overseas revenue climbed 8% to £25.5m to set a new FY Overseas record:

- After H1 Overseas revenue advanced by 13%, H2 Overseas revenue gained only 4% to £12.8m.

- FY Overseas sales of the ‘core’ medical-device foams and wipes climbed 9% to £23.3m:

- After H1 Overseas medical-device revenue advanced by 16%, H2 Overseas medical-device revenue gained only 4% to £11.6m.

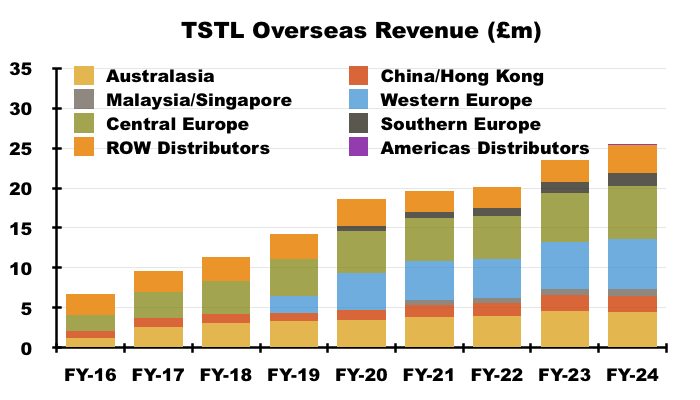

- TSTL’s Overseas subsidiaries registered differing FY revenue progress:

- Australia, New Zealand, China and Hong Kong combined to report lower FY revenue.

- The FY webinar cited staff departures for the lower Australasian performance:

“Unfortunately APAC was a little bit disappointing this year, hampered by sales team losses. We lost a few members of our Australian sales team, but we are now back to a full capacity out in Australasia, and so those issues have been fully resolved and we now expect to see growth return within Australasia.”

- The in-person FY meeting noted China and Hong Kong are:

- “Cost sensitive” markets;

- Liable to often revert to “local, lower-performing” alternatives;

- Biased towards surface products, and;

- Expected to recover when the new TANK system becomes available.

- The FY webinar claimed the group’s “global footprint” would counterbalance those parts of the business that were not growing:

“There will always be certain parts of the business which are down but the beauty of Tristel is that we have such strong foundations and with such a global footprint that we can compensate for those areas should they have any weakness from a year-to-year perspective.”

- The in-person FY meeting claimed there was “much more to come” from Europe, especially after the Ministry of Health in Germany recently confirmed the manual disinfection of medical devices was a “validatable technology” (see 2024 AGM statement).

- TSTL’s third-party distributors suffered a very mixed FY, with H1 revenue up a bumper 43% followed by H2 revenue up only 4%. The preceding H1 cited Spain and Ireland as particularly successful distributors.

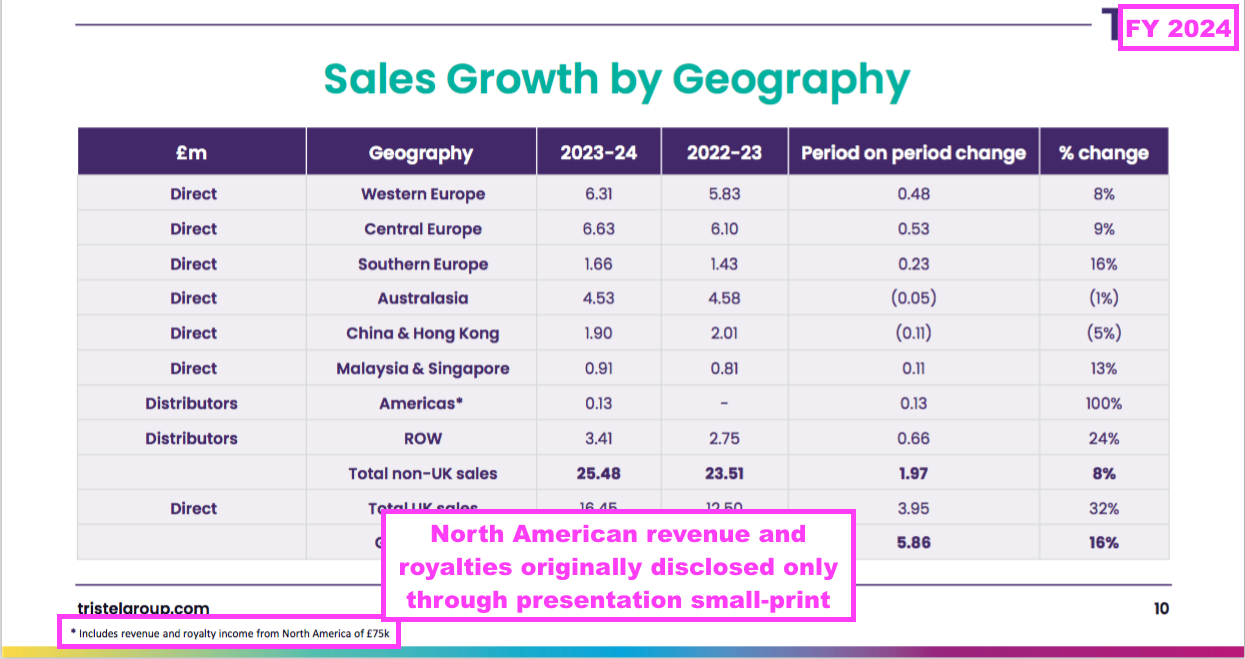

- This FY disclosed the very first distributor revenue from ‘Americas’ (£130k).

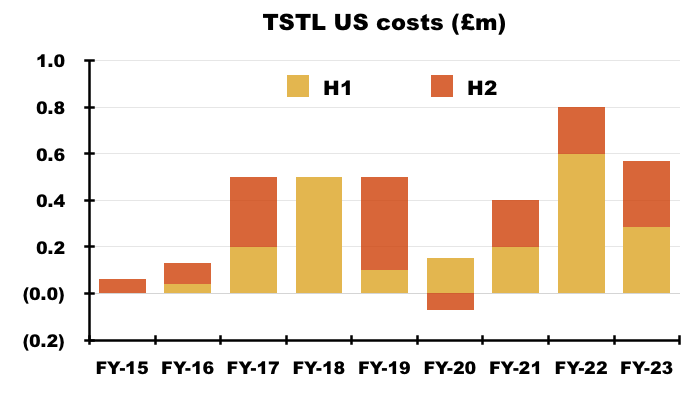

- FY Americas revenue included income of £74k from the United States and Canada (see North America: royalties and bureaucracy):

- Judging by the earlier map, TSTL’s Chile distributor looks to have earned the remaining £56k Americas revenue.

- This FY claimed last year’s US regulatory approval of TSTL’s ultrasound foam could prompt greater sales within Central and South America:

“We expect to see further growth across all of our markets in FY 25, and we are particularly focussed on making the most of the significant opportunity that last year’s FDA approval for Tristel ULT offers us: access to the largest healthcare market in the world. This also gives us the opportunity to leverage the significance of an FDA approval in countries that look to the US regulator for their own practice, such as countries across Central and South America.”

- Third-party distributors that perform well can become acquisition targets for TSTL.

- TSTL acquired:

- Its Australian distributor for £1.1m during FY 2017;

- Its Belgian/Dutch/French distributors for £6.4m during FY 2018, and;

- The remaining 80% of its Italian distributor for £0.6m during FY 2020.

- I calculate:

- Annual Australasian sales (i.e. Australia and New Zealand) have since climbed 124% from approximately AU$3.9m to approximately AU$8.7m (8-year CAGR: 11%);

- Annual Western Europe sales (i.e. Belgium, Netherlands and France) have since climbed approximately 148% from €3.1m to approximately €7.6m (6-year CAGR: 16%), and;

- Annual Southern Europe sales (i.e. Italy) have since climbed 146% from €700k to approximately €2.0m (5-year CAGR: 24%):

- In addition, TSTL established a Malaysian subsidiary at the start of FY 2021 after recruiting the team that had worked previously as the country’s distributor. Annual Malaysian revenue currently runs at £0.9m.

- And TSTL paid £339k during the comparable FY for a distributor selling to the Middle East and North Africa. TSTL has yet to disclose any revenue from this operation.

- However, the country that offers by far the greatest third-party distributor potential is the United States.

North America: royalties and bureaucracy

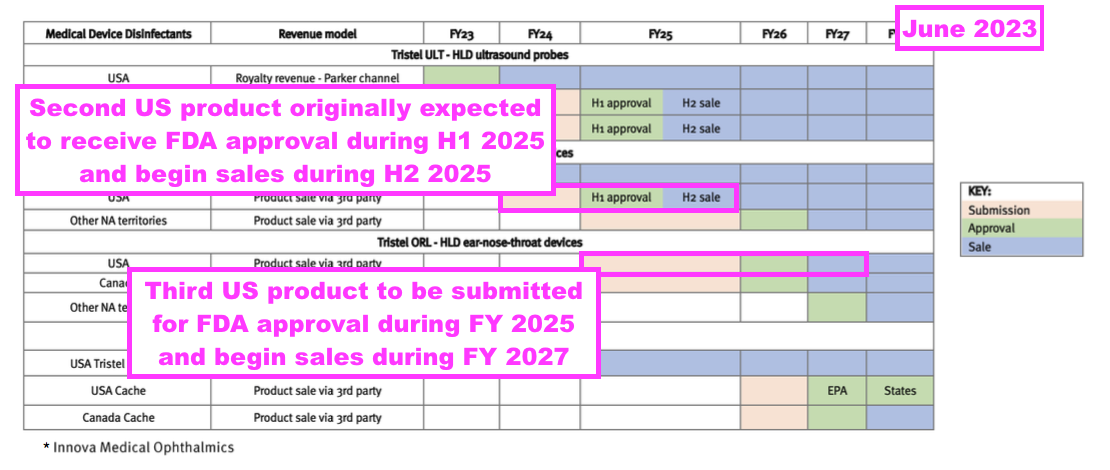

- TSTL received regulatory approval for selling an ultrasound-probe disinfectant within the United States during June 2023, and the comparable FY confirmed the first US orders had been “shipped and invoiced“:

[FY 2023]

Sales and marketing:

First orders shipped & invoiced

• Parker distributors include: Medline Industries / Henry Schein / Owens & Minor / McKesson Corp

• Listing in hospital and distributor procurement systems underway

• FY24 Parker exhibiting at 7 major USA conferences and Innova at 2 major Canadian conferences, supported by Tristel team

- The preceding H1 then revealed the initial US orders had received “very positive feedback“ from US hospitals undertaking “beta testing“:

[H1 2024]

“Parker’s manufacturing processes have been validated by our quality team and production is now underway. The product has been through beta testing at a number of healthcare institutions in the United States,with very positive feedback. Parker Laboratories plans an extensive marketing and trade show programme throughout 2024 and is in the process of expanding its salesforce in order to capitalise on the potential that Tristel ULT represents.”

- The preceding H1 also revealed North American royalties of £46k during the first “ten weeks of activity”:

[H1 2024]

“During the first ten weeks of activity our revenue and royalty income from North America totalled £46k. We are very encouraged by this positive start.”

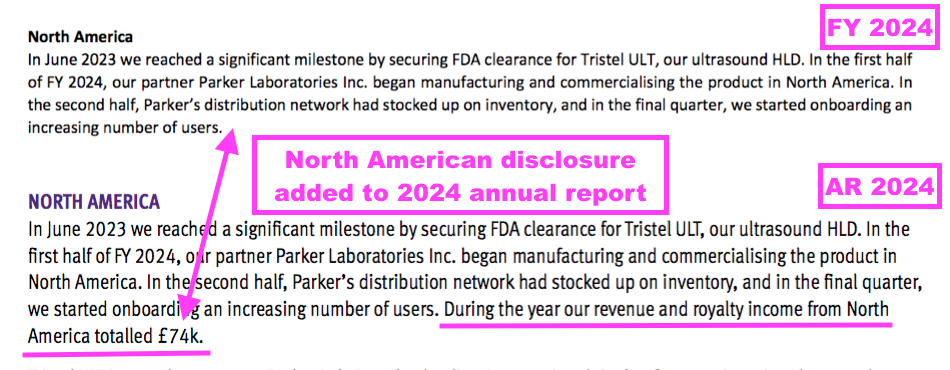

- However, this FY then admitted US sales activity had suffered from “stringent post-COVID purchasing bureaucracy”:

“In the US, our partner Parker Laboratories began manufacturing and commercialising Tristel ULT during the year, gaining significant traction with several hospitals onboarded in the final quarter. They have built a strong pipeline of opportunities but acknowledge that the more stringent post-COVID purchasing bureaucracy is making the sales process longer than initially anticipated.”

- Clearly the “very positive feedback” reported during the preceding H1 could not overcome the sudden emergence of “purchasing bureaucracy“.

- This FY originally disclosed North American revenue and royalties of £74k (originally stated as £75k) only through the presentation small-print:

- After the preceding H1 reported North American royalties of £46k over ten weeks, FY North American revenue and royalties of £74k means H2 collected North American income of £28k over 26 weeks.

- In other words, North American income was a weekly £4.6k during H1, but was a weekly £1.1k during H2.

- Weekly North American revenue and royalties had clearly collapsed during H2, which is presumably why the £74k was relegated to the presentation small-print.

- During the in-person FY meeting, I asked management why the preceding H1 had disclosed North American royalties of £46k within the RNS results commentary, but this FY had disclosed the FY North American revenue and royalties of £74k only within the presentation small-print.

- Management said the £74k disclosure was an “oversight” and my point would be “taken on board“.

- Another private investor attending the in-person FY meeting told me during the post-presentation canapés that the directors “knew damn well what they were doing” by relegating the £74k to the presentation small-print.

- I do wish more investors would speak out at company presentations when they feel directors are not being entirely frank with shareholders.

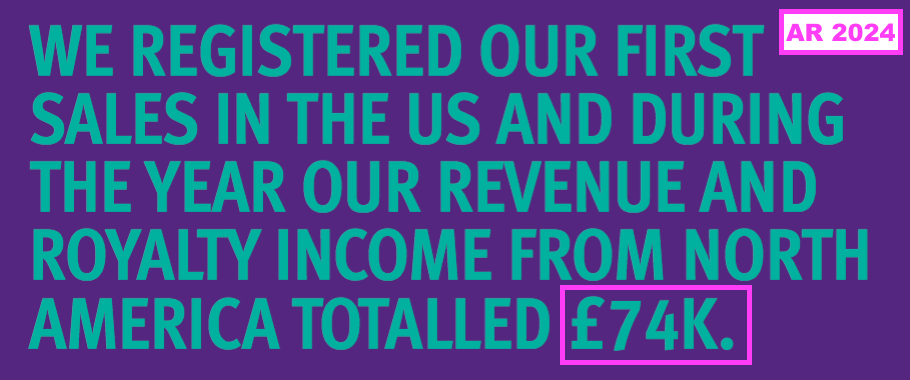

- Management has commendably taken my point “on board“, and the full 2024 annual report refers to the £74k revenue and royalties within the introductory highlights…

- …and the (amended) results commentary:

- The FY webinar explained the £46k earned during H1 related to the “initial stocking of the distribution chain“, which shareholders now realise was used to fulfil “beta testing” orders during H1 and H2.

- The FY webinar provided details of the “purchasing bureaucracy”:

“US hospitals really have cracked down on new products coming into their facilities. The days have gone in the US where a clinician would phone up the purchasing department and they would order it straight away.

Now they put in a variety of different processes. As a completely new product we are not on a hospital’s system at all. There are the steps you have to go through in order to get into a hospital’s system.

At the same time each of the departments are being pressurised on cost. They have their own different committees to review clinical applications for an adoption of new technology. We have to go through all these different steps, and they are not uniform. Every hospital, every health system will have slightly different nuances about the way they approach [new products].“

- The FY webinar admitted the “purchasing bureaucracy” — and a sales cycle of up to 18 months — were “nothing unique“:

“This sales cycle that we’re experiencing and the hurdles we have to overcome to get the customer to actually purchase our product is nothing unique to Tristel. Up to 18 months is the reality. That’s the way of doing business.“

- Mind you, if a US sales cycle of up to 18 months is “nothing unique“… why then did this FY also say the sales process had become “longer than initially anticipated“?

“They have built a strong pipeline of opportunities but acknowledge that the more stringent post-COVID purchasing bureaucracy is making the sales process longer than initially anticipated.”

- TSTL shareholders were certainly not told about US sales cycles lasting up to 18 months before this FY.

- For example, during July 2022, TSTL claimed the US could become a “significant” profit contributor “within the next five years“:

[RNS July 2022] “Within the next five years we have high hopes that America will be a significant revenue and profit contributor to the Group”.

- Two years later, and North American revenue and royalties of £74k will have to increase substantially during the next three years for the US to become a “significant” profit contributor.

- Furthermore, my conversations with senior management during TSTL’s 2022 open day yielded very confident talk of early US success:

- Already educated the US market about high-level disinfection;

- “Receiving questions from US hospitals on a daily/weekly basis”;

- “Strong expressions of interest”;

- “Expect first year to be significant” — no real lag;

- “Long list of American customers”, and;

- Receive maybe five enquiries a week [from the US], from Google search on ultrasound disinfection.

- Perhaps the most alarming US comment from this FY’s webinar was:

“We’re a year behind where we wanted to be.“

- US FDA approval for the ultrasound foam was granted on 02 June 2023, while the FY webinar was hosted on 21 October 2024….

- …which means less than 18 months after FDA approval, TSTL is already a year behind schedule in the US!

- Following the lacklustre US progress, I now understand why:

- TSTL’s former chief executive announced his retirement just six months after the FDA approval, and;

- TSTL appointed a new chief executive who ticked a lot of boxes for marketing healthcare products in the US (see Boardroom).

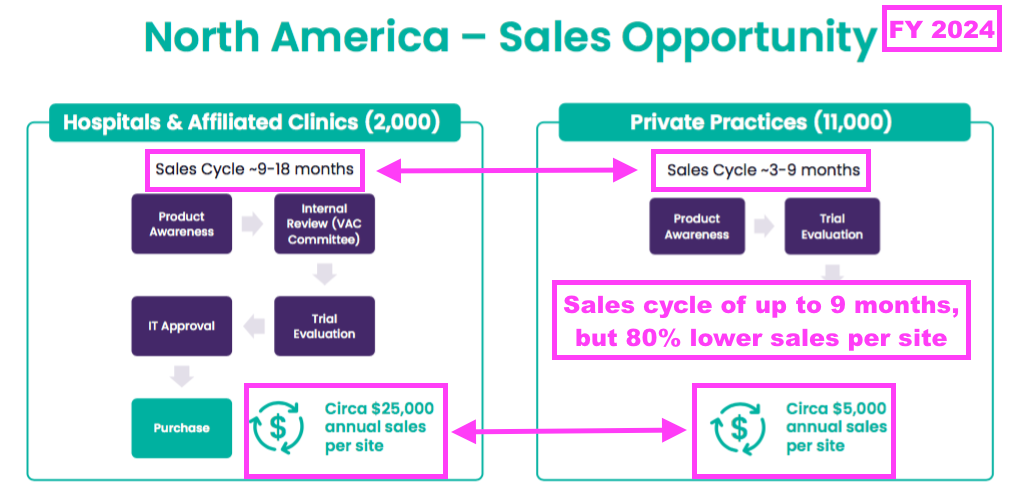

- This FY indicated US private practices could adopt TSTL’s foam within nine months versus large US hospitals adopting within 18 months. But the volumes purchased by US private practices would be much smaller:

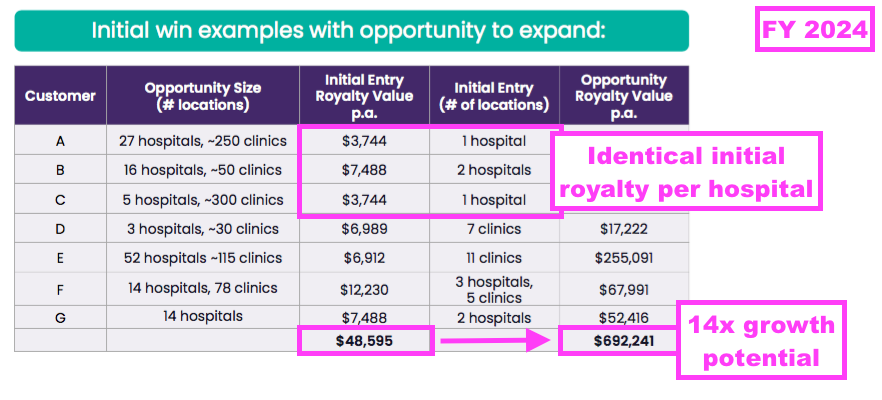

- This FY also suggested that early US customers could increase their TSTL purchases 14-fold once TSTL’s ultrasound foam is established throughout all of their facilities:

- Note that the slide above shows each US hospital trialling TSTL’s foam delivering an identical initial royalty of $3,744.

- The FY webinar admitted TSTL had “extrapolated some of the initial purchases” and “the information we put on slide 16 was more to be indicative rather than something that should be analysed in depth.”

North America: Parker Laboratories and potential opportunity

- This FY revealed a startling fact about Parker Laboratories, TSTL’s US manufacturing and distribution partner:

“Tristel ULT is complementary to Parker Labs’ market-leading Aquasonic gel, in that for every invasive ultrasound procedure the gel must be used and an HLD must be used. Parker is a well-qualified manufacturing partner for Tristel ULT, providing the highest quality standards in its FDA-approved New Jersey facility, and also selling our product through its existing nationwide distribution channels. To support our partnership, Parker has expanded its own direct sales team from 2 people to 10.”

- I did not know Parker had operated with only two direct sales people for its entire product range, a fact confirmed during the in-person FY meeting.

- At the time of the FDA approval, TSTL said Parker earned annual revenue of $60m through its “leading global brand” of ultrasound gel:

- $60m is a lot of revenue for a two-person sales team to handle.

- The in-person FY meeting confirmed Parker also sold its flagship ultrasound gel through third-party distributors.

- I get the distinct impression the US “purchasing bureaucracy” that has now emerged is due to Parker’s direct and indirect sales forces enjoying a very comfortable position when selling a “leading global brand” of ultrasound gel into US hospitals…

- …but being very ineffective when having to sell a brand-new product.

- The FY webinar implied TSTL’s new chief executive had been instructing Parker’s sales reps on the basics of selling:

“I have met with the Parker team twice already and been laying out my experience and some best practices.

Let’s say you’re on the agenda for [a US hospital’s] quarterly meeting. That’s your opportunity. If you do not answer all the questions, if you are not successful there or there’s a reason for delay, you can lose three months by being pushed back

So what I’ve been working with Parker is to say, okay, what have we experienced so far? What are the things that are coming up? And how are we ensuring that we have the full packet of information supplied to [US hospital] committees to ensure we’re not having any delays and we’re going through the process as smoothly as possible?”

- Management made the following points about Parker during the in-person FY meeting:

- Having increased the salesforce from two to ten and incurred extra staffing costs, Parker has now become “more receptive” to TSTL’s advice;

- Parker’s salesforce has to be “really focused on the details“;

- Parker “sees the opportunity we have“, and;

- If greater sales come through, Parker is prepared to go from ten to “20 or 30” sales reps.

- The post-FY AGM statement confirmed my impression that Parker’s sales team was not properly prepared to sell TSTL’s foam (see 2024 AGM statement).

- At least the FY webinar made clear the US opportunity had not diminished:

“Although we are stating within this set of results that the contribution from the US is slightly behind the position that we hoped we would be in, we see that as a slight deferral of revenue, but certainly not a reduction in the opportunity that we have laid out and described to our shareholders.”

- The comparable FY’s webinar said US hospitals were expected to pay between $3 and $3.50 per disinfection procedure for TSTL’s foam, which would be split three ways:

- Parker’s indirect sales distributors capturing between $1 and $1.50;

- Parker collecting $2 for the manufacturing, and;

- TSTL earning a 24% royalty from Parker’s $2.

- TSTL’s 24% royalty therefore equates to 24% of $2 = $0.48 = 38p per US disinfection with GBP:USD at 1.26.

- Between $3 to $3.50 is equivalent to between £2.38 to £2.78, and is 40%-plus greater than the aforementioned £1.70 per disinfection when buying the equivalent foam within the UK.

- Parker increasing its direct sales force from two to ten implies Parker could eventually capture more of the distributor’s $1 to $1.50 per disinfection for itself, which in turn would give a greater value to TSTL’s 24% royalty.

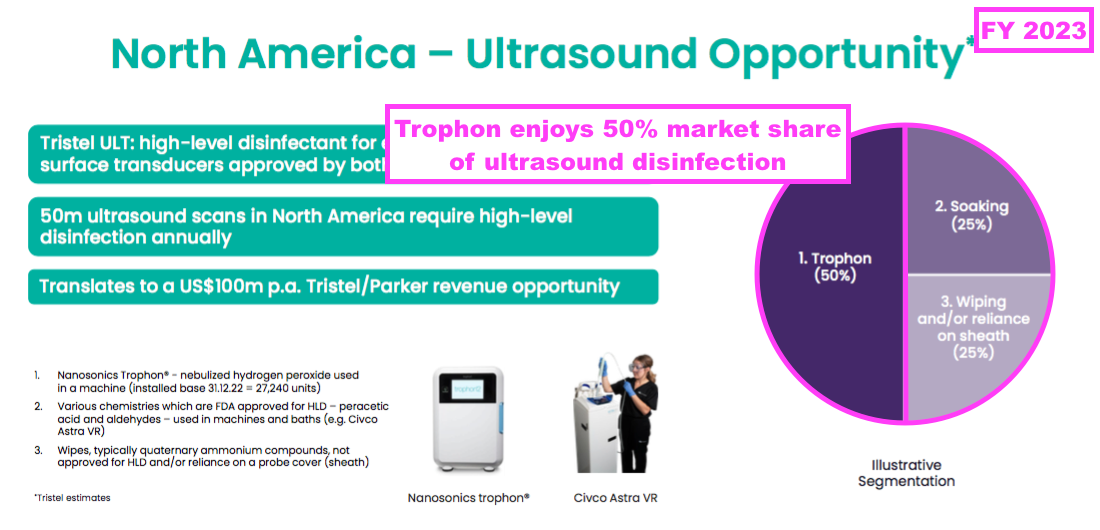

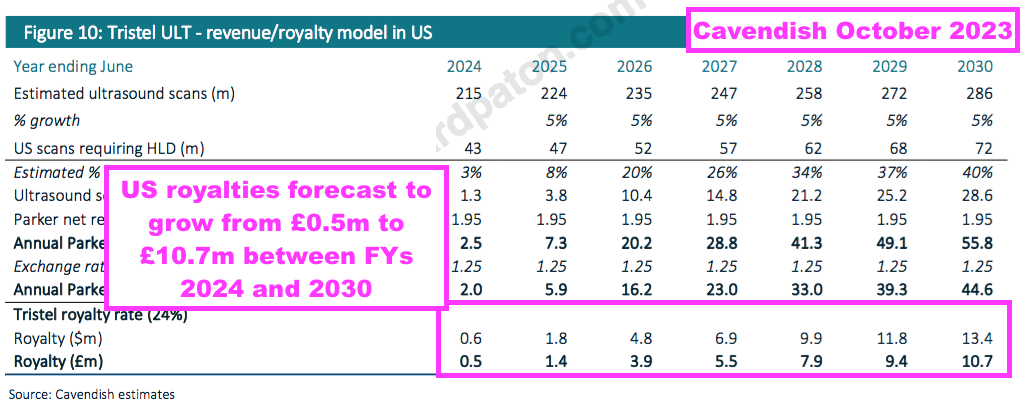

- But for now, this FY repeated how North American hospitals require 50 million ‘high-level’ ultrasound disinfection procedures annually…

- …which still translate into a “$100m per annum opportunity” for TSTL and Parker (i.e. 50 million procedures at the aforementioned $2 per procedure for Parker).

- A “$100m opportunity” leads to a potential $24m ultrasound-royalty opportunity for TSTL, and — using the aforementioned $3 to $3.50 per procedure — implies a possible maximum expenditure by North American hospitals of $175m on TSTL’s ultrasound foam.

- The FY webinar underpinned TSTL’s confidence about the US by referring to the convenience of the group’s foam versus a Trophon machine:

“When we have been talking to the customers in the US, we can see they are using Trophon. They have those machines, but the machine is down the corridor, or maybe it is even a floor away. They are having to disconnect these expensive [ultrasound] probes, walk them all the way [to the Trophon room] and put them into the Trophon machine. You go into the Trophon room and you see… a machine and these numerous probes hanging up on the wall. As you can imagine, this [Trophon decontamination process] is extremely expensive and time-consuming for the customers.“

“What Tristel offers is… disinfection at the point of care, and disinfection in a speedy fashion that makes clinical workflows more and more efficient. That is why we are getting this strong pull from the market, because there is this unmet need that we are able to address for those users.“

- The FY webinar also mentioned a US hospital manager who appeared to regret her Trophon purchase:

“I was at a US hospital last week, a very renowned hospital, and [a US hospital manager] turned around to me and said: ‘Where were you two years ago?’ She had bought 10 Trophon machines to… expand her high-level disinfection and she said: ‘Look, we needed you two years ago, but we are so pleased you are on market now.’ I am very pleased to tell our shareholders that she is using Tristel now, and she is expanding it through the hospital.”

- Comments at the in-person FY meeting suggested this US hospital manager was previously a “talker” for Trophon, but has now “agreed to talk” for TSTL.

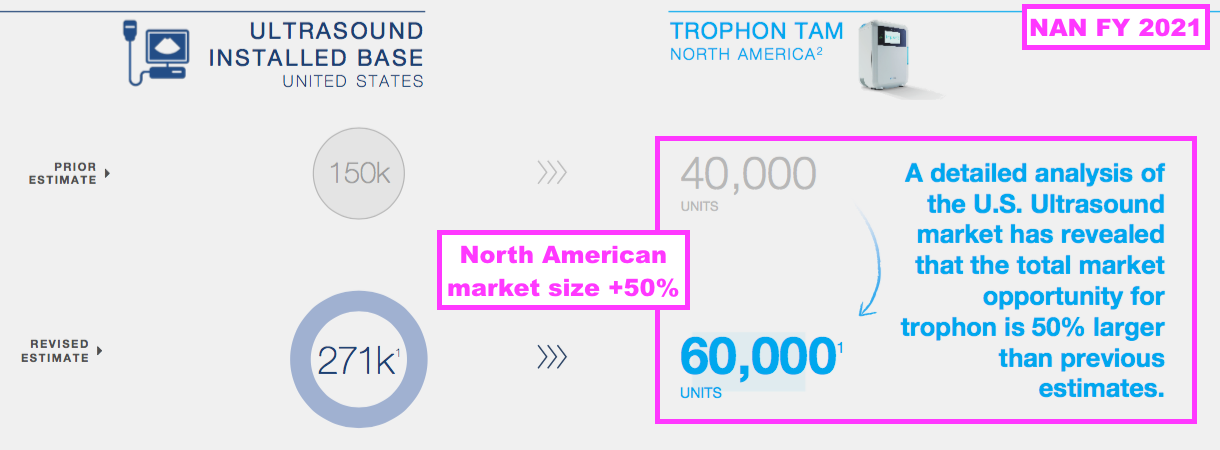

- Trophon machines are manufactured by Nanosonics (NAN), the quoted Australian group that sets the US benchmark for ultrasound-probe decontamination. Trophon machines are limited to cleaning ultrasound probes only:

- This FY reiterated how 50% of ultrasound-probe disinfection procedures within the US are performed by Trophon machines:

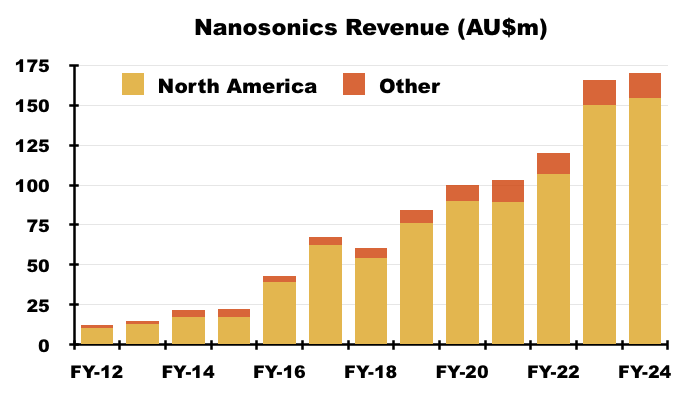

- NAN’s FY 2024 results disclosed revenue of AU$170m, of which AU$154m was earned within North America:

- AU$154m perhaps coincidentally translates to approximately $99m, which matches the aforementioned “$100m opportunity” for TSTL and Parker.

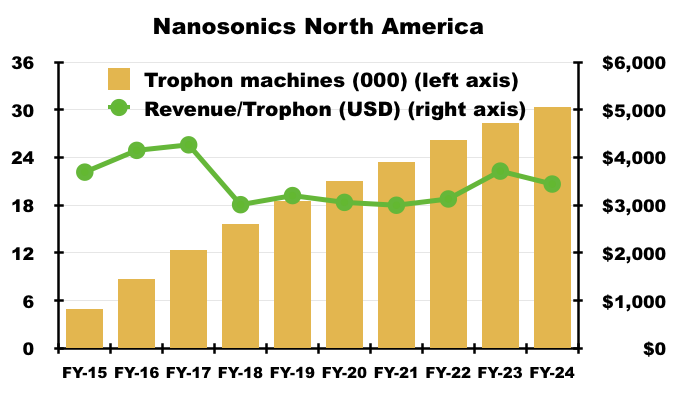

- NAN’s FY 2024 results also confirmed 30,390 Trophons currently operate within North America, which equates to revenue per Trophon machine of approximately $3,440:

- NAN increased the potential of its North American market from 40,000 to 60,000 Trophons during FY 2021:

- NAN’s theoretical market size for North American high-level ultrasound disinfection is therefore 60,000*$3.44k = $206m.

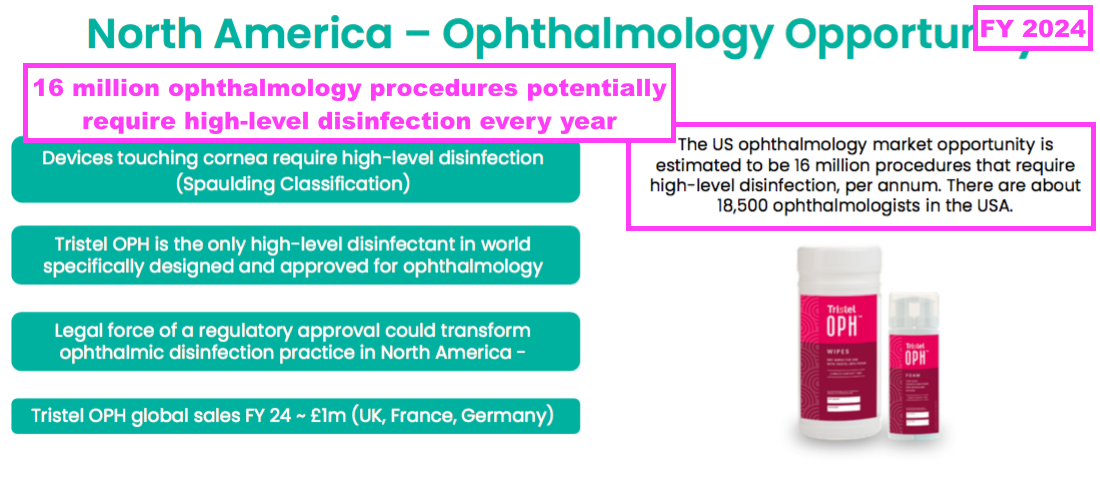

- This FY repeated the North American potential for a second FDA-approved foam for ophthalmology devices, with 16 million ophthalmology procedures requiring high-level disinfection a year:

- This FY claimed an FDA verdict for the US ophthalmology foam would be received before the end of December:

“We also expect to see future growth from the successful execution of our North American strategy for Tristel OPH, with sales already building up in Canada, and FDA 510(k) clearance targeted for the end of this calendar year.”

- But the post-FY AGM statement admitted approval for the US ophthalmology foam had been delayed due to the FDA requiring additional information (see 2024 AGM statement).

- To date, TSTL’s ophthalmology foam has generated only a fraction of the revenue of ultrasound disinfectants within TSTL’s established markets:

- An FDA-approved ophthalmology foam may therefore enjoy only a fraction of the sales of the FDA-approved ultrasound foam in the US.

- Last year TSTL suggested its third FDA regulatory submission would occur during FY 2026 and involve the foam that disinfects nasendoscopes:

- This FY did not refer to US operating costs, but did say TSTL had “established a Boston office with four full-time equivalents supporting our North American expansion.”

- I calculate TSTL’s aggregate US regulatory expenditure during the nine-year application process for the ultrasound foam to have been £3.5m:

- Only time will tell how large the 24% royalties will become and whether that £3.5m — plus the costs subsequently incurred — have been spent wisely.

Patents and competing technologies

- This FY once again cited patents as part of the group’s competitive advantage:

“INTELLECTUAL PROPERTY PROTECTION

On 30 June 2024, we held 149 patents granted in 32 countries providing legal protection for our products. In its broadest sense, our intellectual property relates to:

1. Patents, trademarks and registered designs

2. The scientific validation of our chemistry and our products that have entered the public domain, via a number of peer-reviewed and published papers

3. The certification by medical device manufacturers that our chemistry is compatible with their products. We enjoy official compatibility with the instrumentation of 56 medical device manufacturers, with respect to 1,449 of their individual models.”

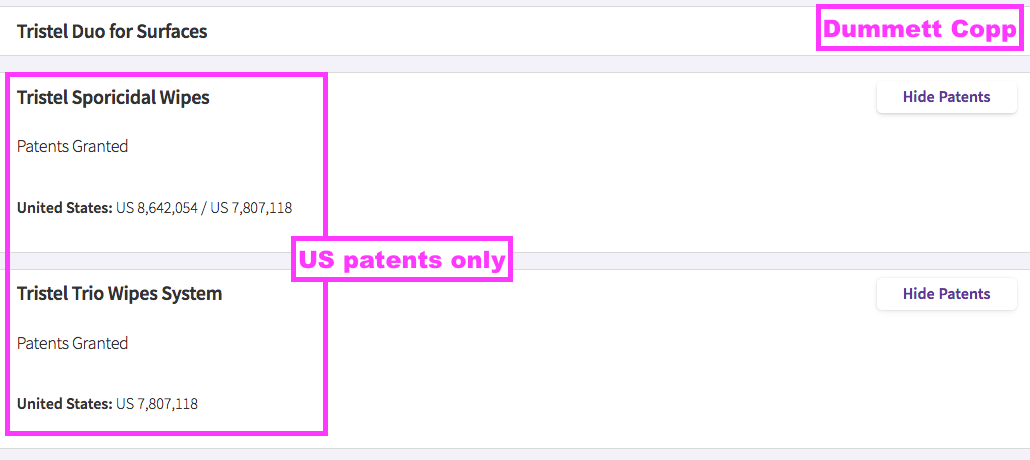

- TSTL’s UK and EU patents protecting the group’s Trio Wipes system expired during and after this FY.

- Google Patents shows the expiry dates were:

- UK: 07 May 2024 (GB 241 3765), and;

- EU: 26 July 2024 (EP 174 2672).

- TSTL’s patent attorney now shows only the US wipe patent in force…

- … which Google Patents says will expire on 11 January 2026.

- Google Patents shows the anticipated expiry dates of TSTL’s foam patents to be:

- UK: 27 January 2026 (GB 242 2545);

- EU: 27 January 2026 (EP 184 3795), and;

- US: 11 September 2030 (US 884 0847).

- The FY webinar suggested secret formulae, industry guidelines and manufacturer compatibility would minimise any patent-expiry disruption:

“When the [2026] patents expire, we do not expect it to have very much impact upon the business. We view the IP that protects our technology as being multi-layered and the patent is only one element of that. The patent itself does not contain the formulation and the formulation is the most important thing when it comes to the manufacturing with the chlorine dioxide. Our proprietary chlorine dioxide formulation is under lock and key. There are less than five people who have access to it.

The broader and more significant protections that we have come in the form of guidelines. For example, the Ultrasound Society within the UK, their guidelines state that chlorine dioxide in the form of a wipe or a foam is an appropriate technology to be used to decontaminate the devices that that Society is interested in. We have worked hard to find ourselves written into such guidelines, which creates a protection. They keep us in and they keep others out.

In addition we have over 2,000 material compatibility statements which have been put together by the device manufacturers. They have tested our decontamination products upon their devices to ensure that no damage is done to them… because those devices are so expensive.

Hospitals require those compatibility statements to be in place before that device can be used. Because we have been doing this for 30 years, it would take an incredibly long time and an awful lot of cost for a newcomer to take their own decontamination process and replicate that level of protection that we have achieved”

- My 2022 discussion with Bruce Green, the chemist who devised TSTL’s disinfectant chemistry, confirmed competitors were kept at bay through secret chemical ingredients and secret manufacturing processes.

- US manufacturing partner Parker seemingly operates with very few patents, suggesting other competitive factors may be more important when supplying products to the US ultrasound market.

- Any impact from the aforementioned Trio Wipes patent expiries will be felt during FY 2025 and beyond.

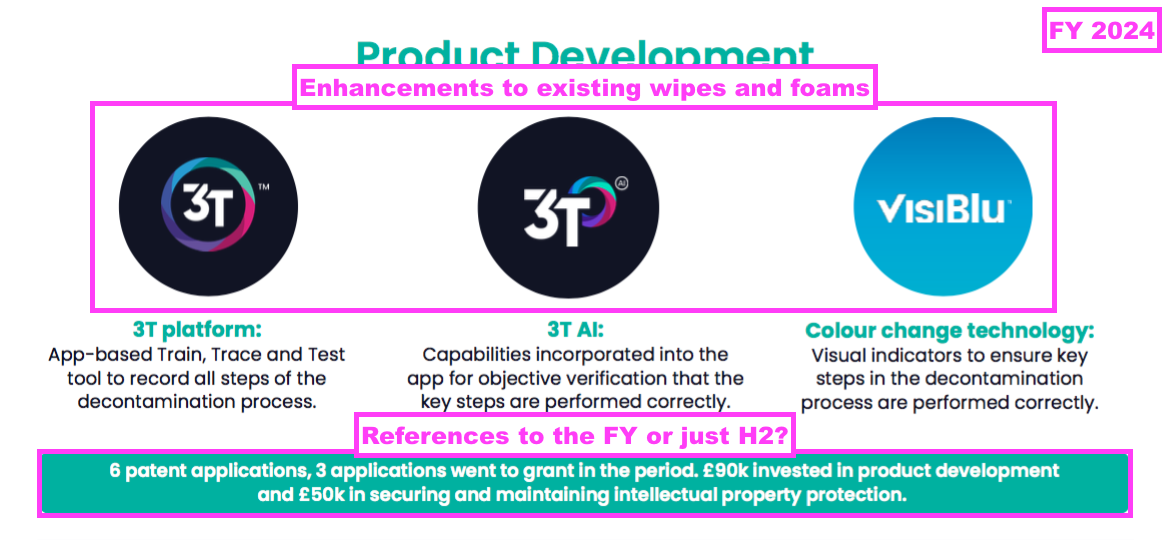

- I am not quite sure what is happening to TSTL’s product development.

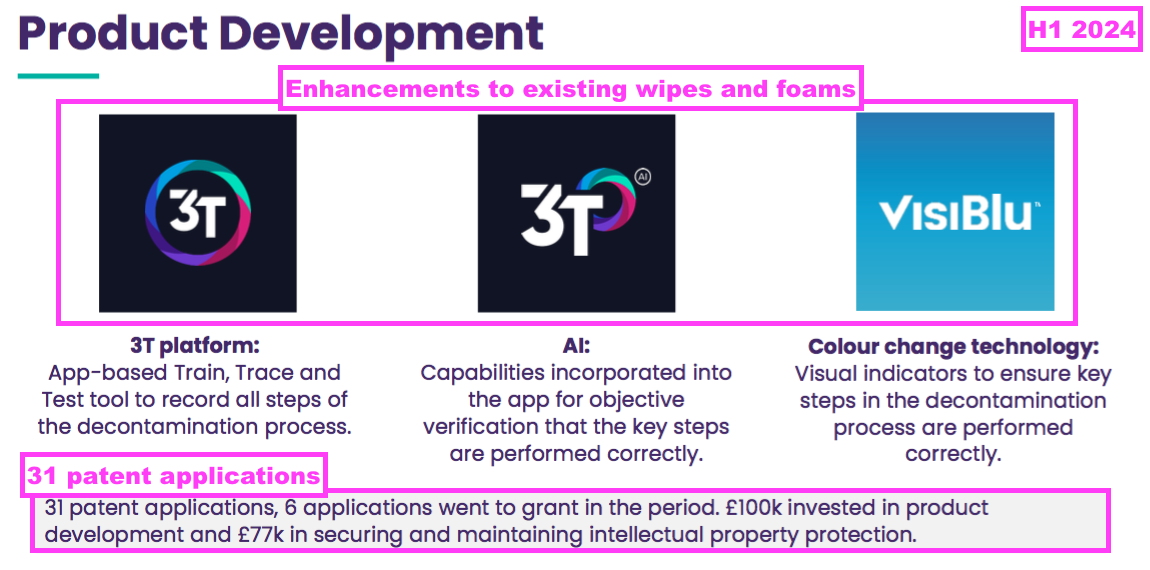

- The preceding H1 recapped three product enhancements and claimed 31 patent applications with £100k invested in product development and £77k spent “securing and maintaining intellectual property protection”:

- But this FY referred to only 6 patent application, only £90k spent on product development and only £50k spent on “securing and maintaining intellectual property protection”:

- The FY commentary then contradicted the presentation and referred to £900k (not £90k) spent on product development and £500k (not £50k) spent on “securing and maintaining intellectual property protection”:

“We made six patent applications during the year and three applications went to grant. During the year we invested £0.9m in product development and £0.5m in securing and maintaining intellectual property protection.”

- This FY reiterated copycat disinfectants were not the most significant risk to TSTL. Instead the main three dangers continue to be:

- “Competing technologies“;

- “Divergence by regulators away from chemical disinfectant products“, and;

- “A shift in market acceptance of manual decontamination systems“.

- TSTL may not face equivalent competition from other wipes and foams, but “competing technologies“ include:

- The preceding H1 webinar appeared unconvinced about the decontamination qualities of UV light:

[H1 2024]

“Light is a new technology, and the market needs to catch up and the regulators need to catch up and put in place a form of assessing its effectiveness. Certainly Chronos is a competitor. Is it an equivalent? We have to wait until there’s proper data to demonstrate that its performance really is equivalent to chemical decontamination“

- Germitec’s Chronos machine was approved for use by the FDA during September, and TSTL will therefore compete with Trophon and Chronos in the States:

- Perhaps the development of new UV-light decontamination devices will amplify those other TSTL risks:

- “Divergence by regulators away from chemical disinfectant products“, and;

- “A shift in market acceptance of manual decontamination systems“.

- The FY webinar claimed Germitec’s Chronos machine would be more of an issue for NAN’s Trophon machine than TSTL’s foams:

“Why are US customers turning to Tristel now? They have this room for the Trophon, they are having to disconnect the probes, they are having to invest in more probes than they need — and these probes cost tens of thousands of dollars at a time — and the probes are being tied up and they are tying up healthcare practitioners [during] decontamination. That is no different whether it is a UV machine or a Trophon machine. We do not see any increased threat from Germitec with regards to our North American ambitions.

What we do see is Nanosonics having increased competition. Those customers looking to replace their Trophon machines now have an alternative. We think for us we see little risk and for Nanosonics we see increased competition.“

Boardroom

Share-based payments

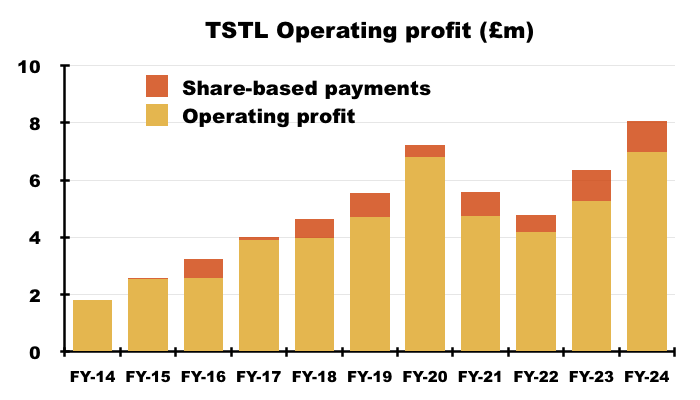

- Significant share-based payments have featured regularly within TSTL’s accounts.

- Between FYs 2016 and 2024, share-based payments reduced aggregate operating profit by £6.3m, or 13%:

- This FY witnessed share-based payments reduce operating profit by £1.1m, or 13%.

- TSTL presents an adjusted profit excluding share-based payments:

“Charges associated with share-based payments have been included as adjusting items. Although share-based compensation is an important aspect of the compensation of our employees and executives, management believes it is useful to exclude share-based compensation expenses from adjusted profit measures to better understand the long-term performance of the underlying business.”

- One reason for adjusting for share-based payments is such charges can occur despite the options eventually becoming worthless.

- This FY revealed an executive LTIP incurred a £0.3m cost:

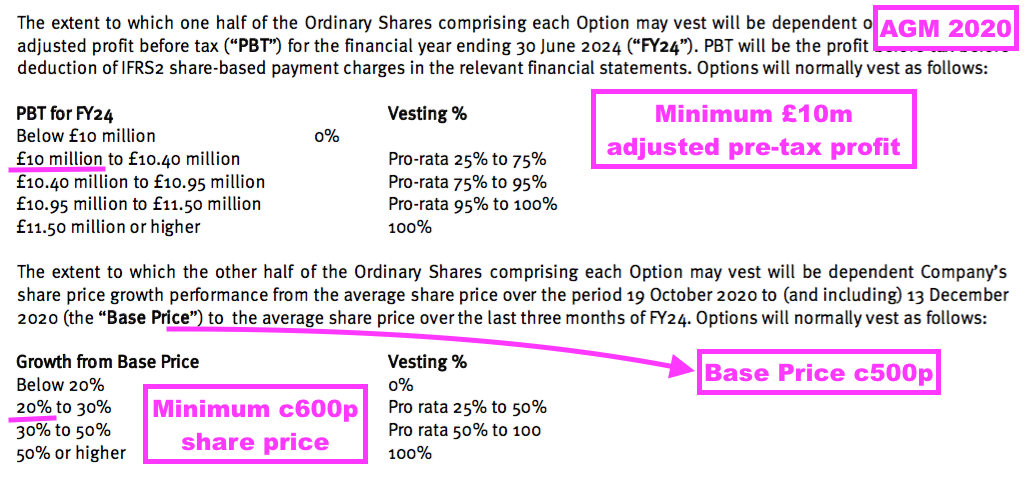

“The non-cash IFRS2 charge (share-based payment charge) for the year was £1.1m (2023: £1.1m). £0.3m (2023: £0.3m) of the charge relates to the Executive Management LTIP scheme approved at the Company’s 2020 AGM, the remaining £0.8m (2023: £0.7m) relates to the Companyʼs All Staff share option scheme.“

- The LTIP in question relates to 800k options that vested if profit (before share-based payments!) reached £10m during this FY or the share price traded at a c600p average during April/May/June 2024:

- The 800k options all expired worthless, as:

- Profit for this FY did not reach £10m, and;

- The share price did not trade anywhere near 600p during April/May/June 2024.

- The true long-term cost of options to ordinary shareholders is through permanent dilution and not accounting charges.

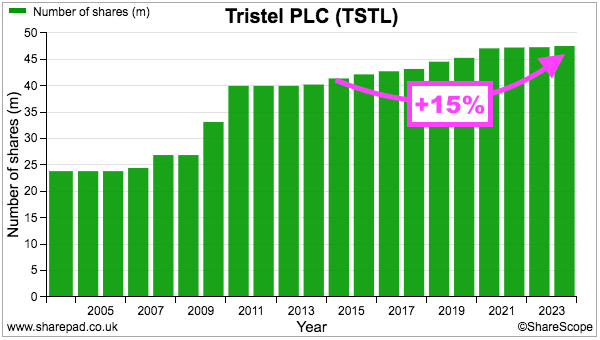

- TSTL’s share count has advanced 15% between the start of FY 2016 and the end of this FY, with 13% due to options and 2% due to the purchase of third-party distributors:

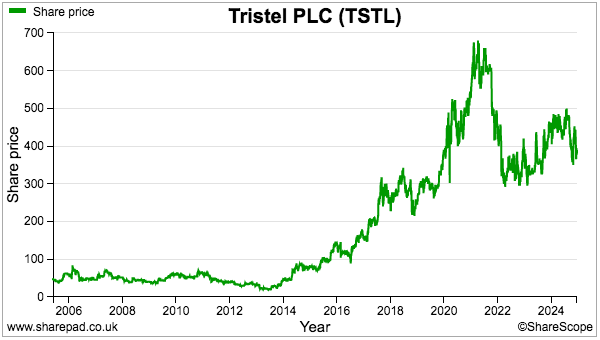

- During the same period, the share price increased from 101p to 458p while the dividend increased from 2.72p to 13.52p per share. Outside shareholders were therefore still rewarded despite the dilution.

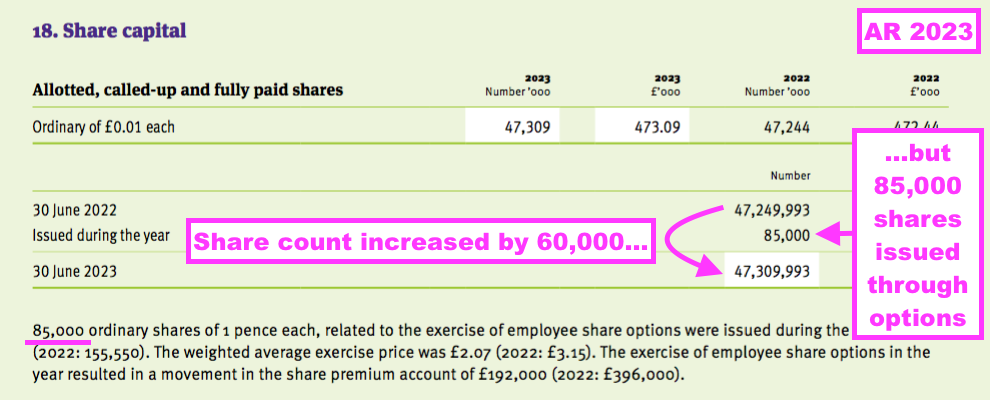

- Note that TSTL’s option reporting has not always been 100% accurate, with FYs 2019, 2020, 2021, 2022 and 2023 each showing a minor mismatch between the number of options exercised and the increase to the share count.

- For example, the comparable FY reported the exercise of 85,000 options…

- …while the share count increased by 60,000:

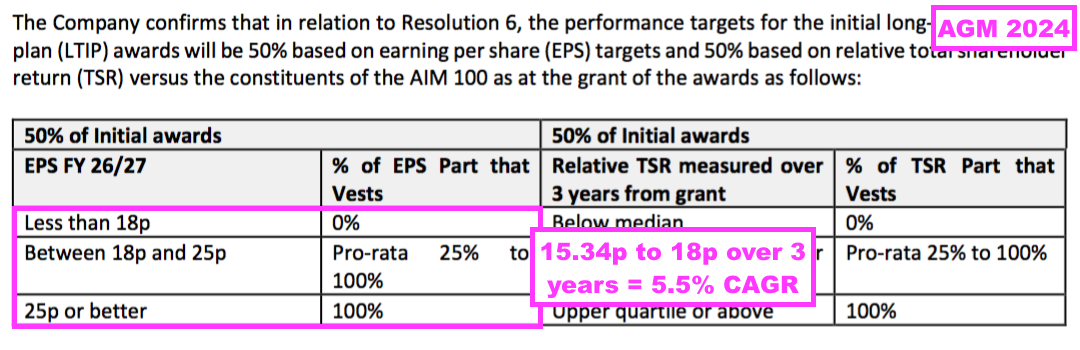

New LTIP

- Following this FY, TSTL’s AGM notice published during November revealed a proposed replacement LTIP for shareholders to approve at December’s AGM:

[AGM Notice November 2024]

“ORDINARY RESOLUTION

14. THAT, the rules of the Tristel plc Long Term Incentive Plan (the LTIP), the principal terms of which are summarised in the Appendix to this notice, and a copy of which are produced in draft to this meeting and initialled by the Chair of the meeting for the purpose of identification, be and are hereby approved and the Directors be authorised to:

14.1. make such modifications to the LTIP as they may consider appropriate to take account of the requirements of best practice and for the implementation of the LTIP and to adopt the LTIP as so modified and to do all such other acts and things as they may consider appropriate to implement the LTIP; and

14.2. establish further plans based on the LTIP but modified to take account of local tax, exchange control or securities laws in overseas territories, provided that any shares made available under such further plans are treated as counting against the limits on individual or overall participation in the LTIP.”

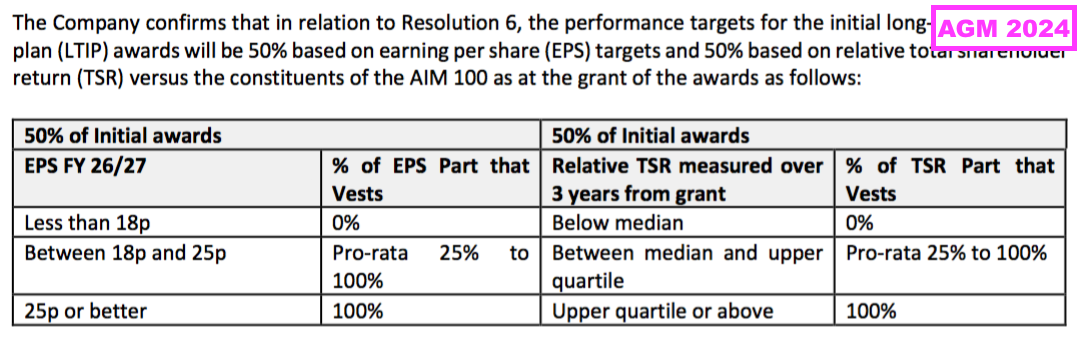

- Shareholders were asked to approve the LTIP despite the AGM notice not defining the LTIP’s actual performance measures:

[AGM Notice November 2024]

“The first awards under the LTIP are planned for grant to the Company’s executive directors within six weeks of shareholder approval of the LTIP. Such first awards will be granted at reference grant levels of 100% of annual base salary and will have an associated normal vesting date of the third anniversary of grant. Such first awards will be subject to performance conditions relating to measures of relative total shareholder return performance and earnings per share performance over three year periods.“

- Ahead of the AGM, I sent the following LTIP questions to TSTL’s remuneration chair Isabel Napper:

[Maynard Paton December 2024]

“a) Can you explain why specific LTIP targets are not being disclosed at this AGM? In contrast, at the 2020 AGM, shareholders were presented with detailed LTIP performance targets for approval.

b) How can shareholders be sure suitably stretching LTIP targets will now be set? As it stands, the LTIP authority leaves the door open for low-ball targets that bypass shareholder approval.

c) The new LTIP grants will occur within six weeks after the upcoming AGM. Why not formulate the LTIP targets properly and then host the AGM six weeks later (or even host a standalone General Meeting) for formal approval? That way shareholders would not be left in the dark about the targets before giving their approval.”

- Mrs Napper replied with the following answers:

[Isabel Napper December 2024]

“(a) We didn’t set out the performance targets in the Notice of AGM for the new LTIP because at the point of going to print, our major shareholders were still being consulted on the earnings per share (EPS) and total shareholder return (TSR) target ranges.

Following the completion of the consultation exercise, I am pleased to confirm that none of our major shareholders raised any concerns in respect of the targets. As such, and subject to the LTIP gaining shareholder approval, I confirm that the performance targets for the initial awards will be 50% based on EPS targets and 50% based on relative TSR versus the constituents of the AIM100 as at the grant of the awards as follows:

The above targets will be set out in the RNS issued immediately following the grant of the awards and the Directors’ Remuneration Report for 2024/25.

(b) As I mention above, we consulted with our major shareholders (over 50% of the Company’s investor base) and received no concerns regarding the targets.

(c) As above.“

- I would make the following points:

- The unfinished consultation is a poor excuse for asking a significant minority of shareholders to approve unspecified LTIP targets: A much better example of corporate governance was undertaken by fellow portfolio member FW Thorpe, which held a general meeting earlier this year just to approve its new share schemes.

- The board has prioritised management’s LTIP over the financial targets to be published to shareholders: Surely the new chief executive ought first to publish his new financial targets, after which the board can then devise an LTIP that aligns management to those targets (see New financial targets).

- The new LTIP targets are indeed low-ball: For the new LTIP to vest, adjusted EPS has to compound at only 5.5% per annum over three years — despite TSTL’s current financial targets including revenue compounding at 10-15% per annum:

- TSTL’s major shareholders no longer seem bothered about enforcing appropriate LTIP targets: You may recall TSTL’s 2021 LTIP was commendably altered ahead of the 2020 AGM to include “more onerous” targets:

[RNS December 2020]

“Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, announces that the terms of the options to be granted under the rules of the Tristel plc Executive Performance Share Plan 2021 (the “Plan”) to be put to shareholders for approval at the Annual General Meeting of the Company to be held on 10.00 a.m. on 15 December 2020 (the “AGM”) will be amended to include more onerous performance targets for the vesting of the options.”

- All told, this entire LTIP episode does seem indicative of the dismal box-ticking corporate governance that pervades today’s stock market…

- …whereby boilerplate non-execs engage boilerplate consultants to design boilerplate LTIPs to satisfy boilerplate institutions.

- Perhaps if all parties spent a bit more time and effort considering an LTIP specifically for TSTL and its particular growth prospects, all shareholders could genuinely prosper from a suitably incentivised management team.

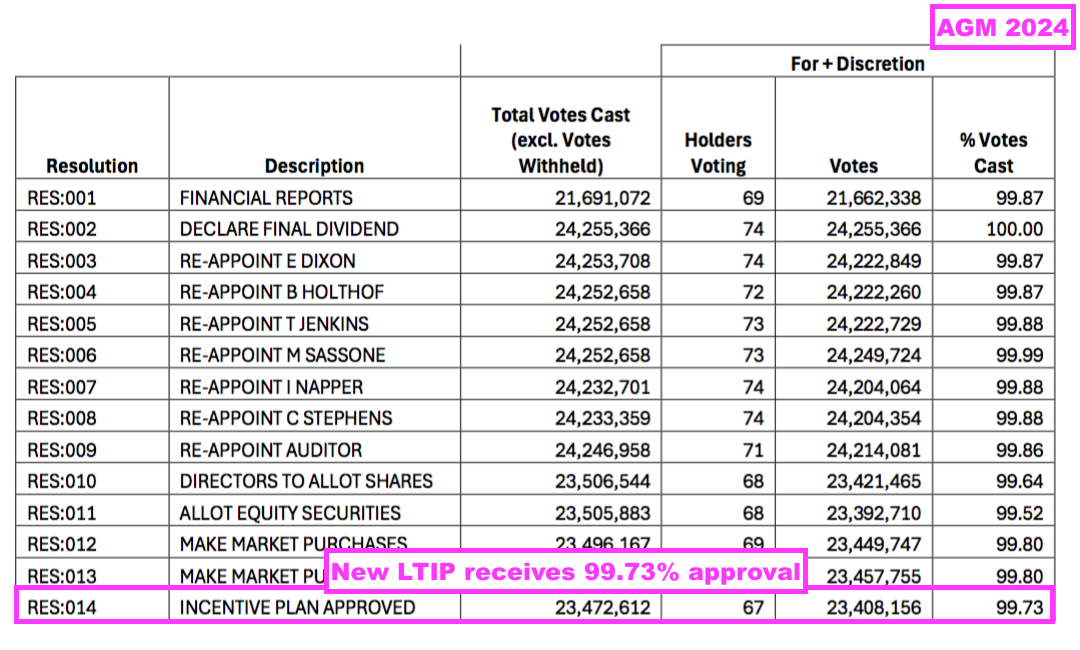

- The LTIP was depressingly voted through with 99.73% support:

- Unlike TSTL’s previous schemes, at least this new LTIP will adhere to the best practice of limiting option grants to 10% of the share count over ten years:

[AGM Notice November 2024]

“Overall dilution limit

…

In any ten calendar year period, the Company may not issue (or grant rights to issue) more than 10% of the issued ordinary share capital of the Company under the LTIP and any other (executive or otherwise) share incentive plan adopted by the Company.”

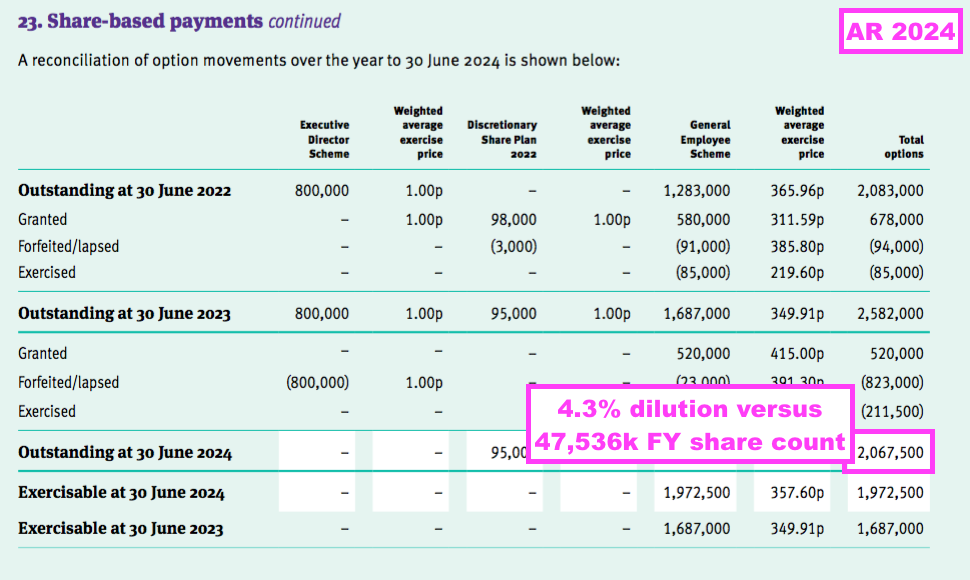

- For perspective, TSTL granted 7.1 million options during the ten years to this FY…

- …which is equivalent to 18% of the share count at the start of that ten-year period (40.2 million).

- This FY reported 2,068k options outstanding, which equate to potential further dilution of 4.3% before the new LTIP:

Financials: margin and employees

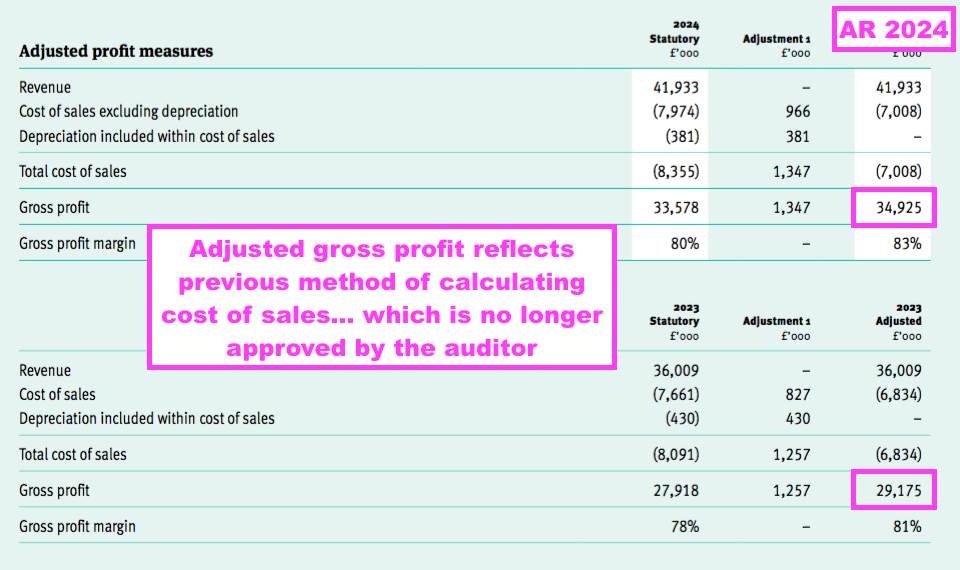

- The aforementioned prior-year restatement of gross profit led to TSTL remarkably reporting an adjusted gross profit for this FY:

- The adjusted gross profit reflects TSTL’s old method of deriving cost of sales, which as mentioned earlier excluded “elements of the cost of production [that] were erroneously included within administrative expenses” (see Prior-year restatements).

- I cannot recall ever studying another company that declared adjusted gross profit…

- …especially when the adjusted version was effectively deemed by the auditor to have been “erroneously” calculated.

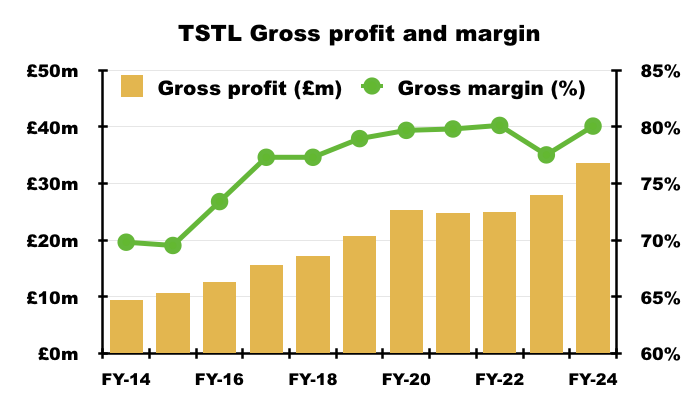

- My chart below shows gross profit and gross margin for this FY and the comparable FY calculated using the new way of deriving cost of sales…

- …with gross profit and gross margin for prior years calculated using the old way of deriving cost of sales.

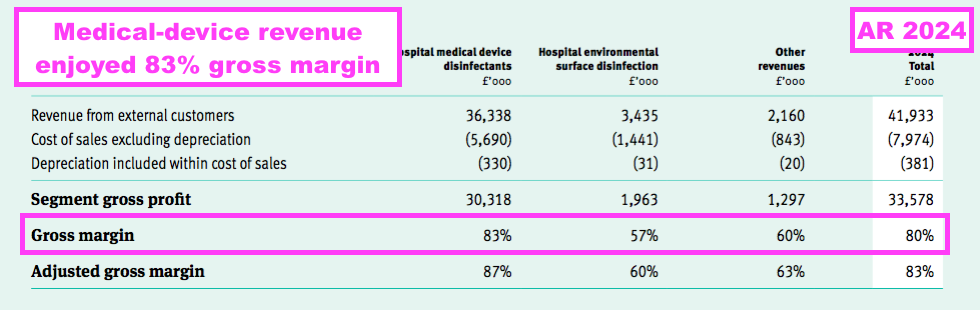

- Despite the gross-margin re-jig, what remains clear is the medical-device wipes and foams are by far TSTL’s most profitable products — boasting an 83% gross margin during this FY:

- An 83% gross margin is equivalent of buying stock for £17 and selling it for £100, and underlines how TSTL’s customers value the effectiveness of the group’s best-selling products.

- TSTL has in the past talked of its foams achieving a terrific 95% gross margin:

[H1 2023]

“Discussions culminated in a fresh renegotiation and recasting the royalty rate that we will earn from the ultrasound activity in the US, in conjunction with Parker. Previously we had from the FDA-approved product a 17.5% royalty of revenue, and it is now 30% of gross profit. But the gross margin will be about 95%. And with the EPA-approved product, rather than the 14.5% royalty on revenue, it goes up to 20%.”

- The 57% gross margin earned from the surface disinfectants was unimpressive (and less than the 60% achieved for TSTL’s ‘Other’ products!), and suggests the new TANK system is really needed to shore up that division’s profitability.

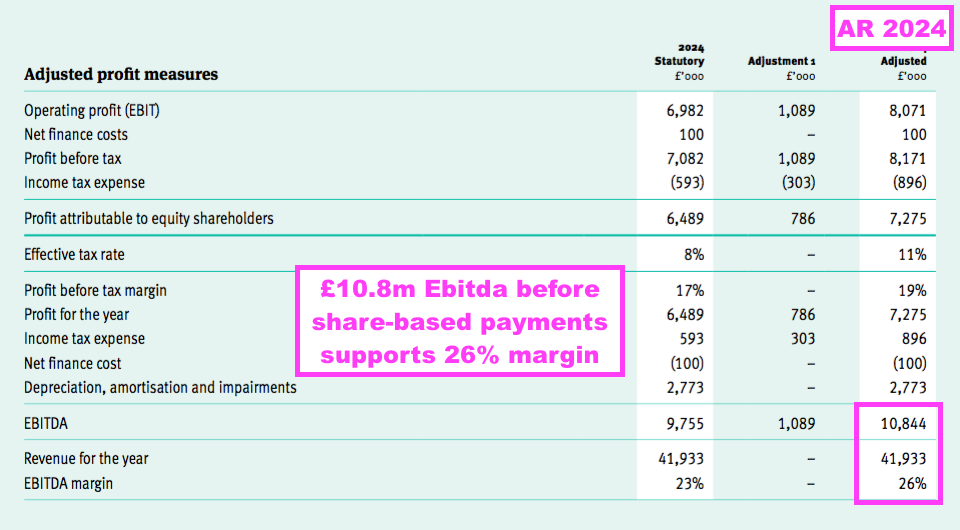

- The FY 80% group gross margin helped TSTL surpass its Ebitda target, which this FY reiterated to be at least 25%:

“i. sales growth in the range of 10% to 15% per annum as an annual average over the three years

ii. the achievement in each year of an EBITDA margin (excluding share-based payment charge) of at least 25%, and

iii. to increase profit before tax (excluding share-based payments) year-on-year, independently of the other two targets.”

- This FY’s Ebitda (before share-based payments) was £10.8m to give an Ebitda margin of 26%:

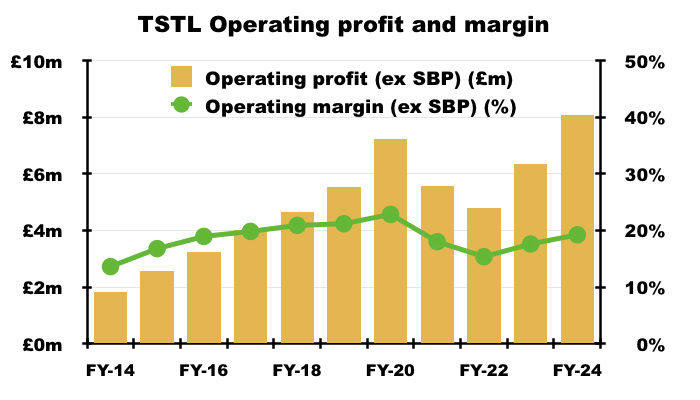

- The FY operating margin (before share-based payments) was a useful 19% versus 18% during the comparable FY and 15% during FY 2022:

- Note that FYs 2018, 2019 and 2020 did witness a 20%-plus operating margin (before share-based payments).

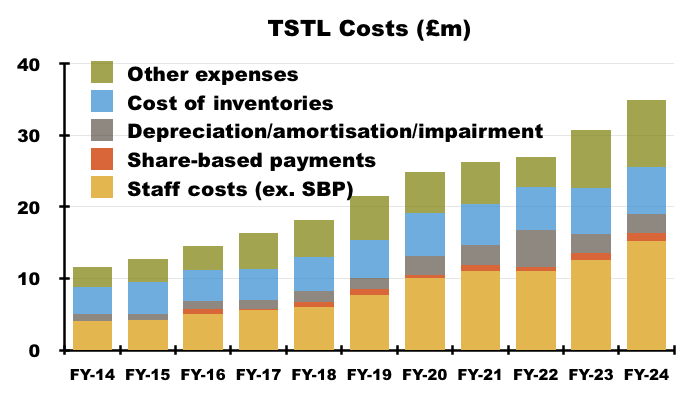

- This FY’s 80% gross margin ensured this FY’s operating profit (before share-based payments) could improve by 27% despite ‘overheads’ advancing by 19%:

“Total revenues increased 16% to £41.9m for the year (2023: £36.0m). Our gross profit margin increased by 2%. Overheads (excluding share-based payments, depreciation, amortisation and impairment) rose by 19%, principally due to the increase in average headcount to 238 (2023 212). Increases in wages and salaries for the Group were £2.7m.“

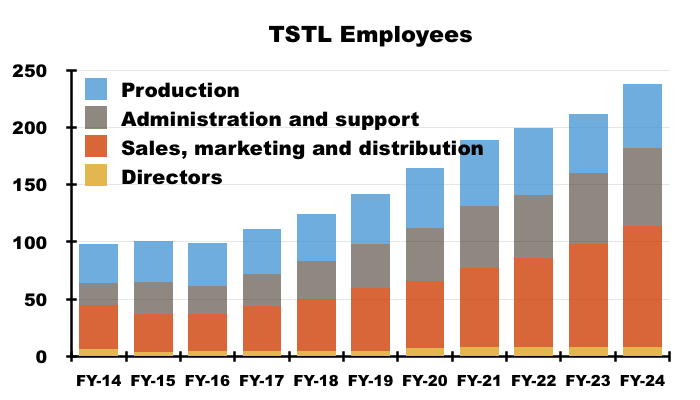

- Of the 26-person increase to the average headcount, 16 were recruited within sales, marketing and distribution:

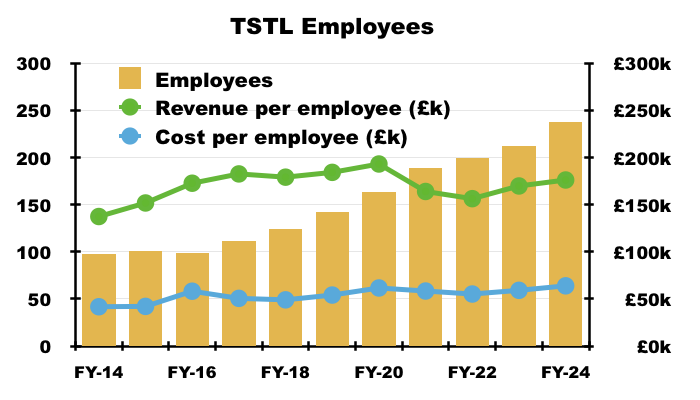

- TSTL’s workforce productivity has disappointingly stagnated during recent years. Revenue per employee for this FY was £176k and only £3k greater than that of FY 2016:

- Revenue per employee not advancing is especially frustrating given staff employed within sales, marketing and distribution represented 45% of the headcount during this FY versus 32% during FY 2016.

- Flat-lining revenue per employee is not ideal given staff costs absorbed 35% of revenue during this FY versus less than 30% during FYs 2017, 2018 and 2019:

- Reasons why revenue per employee has not advanced may include recruiting employees to:

- Operate within overseas markets where price points are lower than within the UK;

- Handle the US regulatory submission;

- Administer tasks involving compliance and ESG, and;

- Undertake R&D for products yet to become commercial.

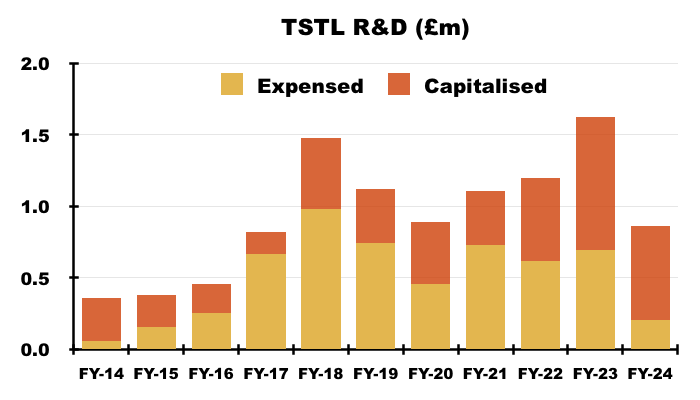

- Expensed R&D was only £205k during this FY — the lowest since FY 2015 (£159k) — with a a further £656k capitalised on to the balance sheet (see Financials: balance sheet and cash flow):

- TSTL had never made clear whether its R&D has ever led to significant extra revenue and/or significant new products. The surface-disinfection R&D for example seems unlikely to have earned a great return to date.

- I just wonder whether the effectiveness of TSTL’s R&D — and employee productivity in general — has been restricted by the group’s margin target (see New financial targets).

Financials: balance sheet and cash flow

- The aforementioned £11.8m cash position included £5.7m cash deemed as “short-term investments” held within term-deposit accounts:

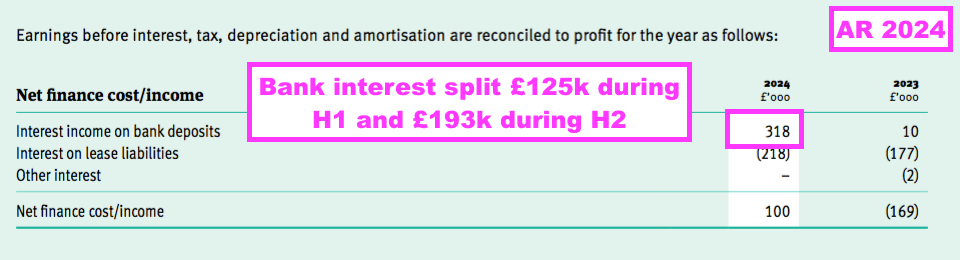

- Interest earned on the average £10.7m held throughout this FY was £318k, which suggests a 3.0% annual interest rate:

- The £193k interest earned during H2 implied a useful 3.4% interest rate.

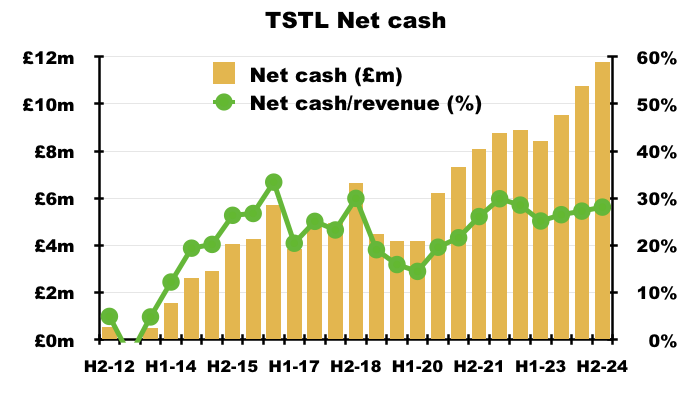

- TSTL’s accounts remain free of debt and FY cash of £11.8m is equivalent to a sizeable 28% of FY revenue of £41.9m:

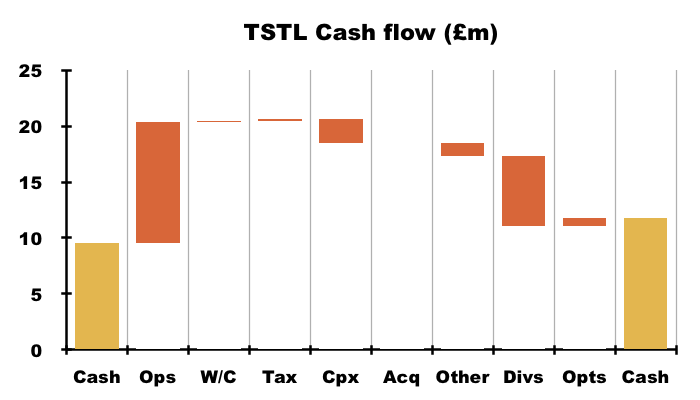

- Cash flow was very respectable during this FY, with adjusted earnings of £7.3m translating favourably into free cash of £8.0m.

- Very welcome cash movements during this FY included:

- A working-capital inflow of £115k, and;

- A net £153k tax refund:

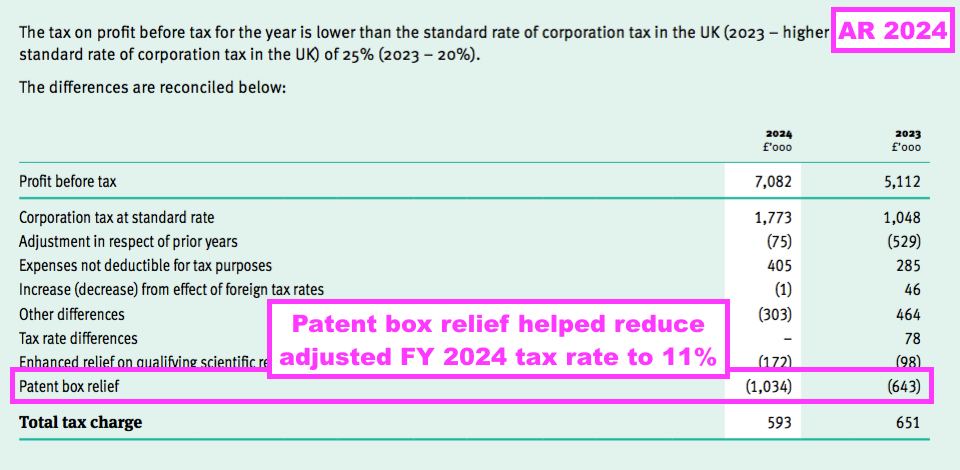

- TSTL’s tax profile for this FY and the comparable FY was assisted by notable patent box relief:

- The patent box relief helped ensure an adjusted tax rate of 11% for this FY versus 18% for the comparable FY and the standard 25% UK rate.

- I am not clear how likely an 11% adjusted tax rate will persist.

- This FY’s cash position was helped also by exercised options raising £676k.

- All told, the respectable cash flow plus significant cash position underpins this FY’s 29% dividend lift, the 1.13x dividend cover and confirmation the payout will still advance by at least 5% a year.

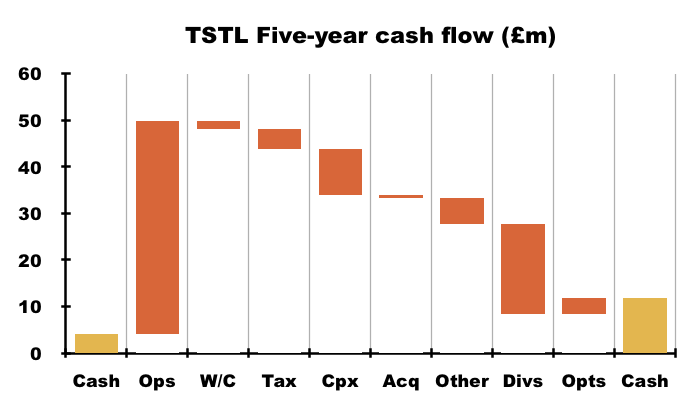

- TSTL’s cash flow is very respectable on a five-year view:

- Between FY 2020 and this FY, cash flow from operations totalled £45.7m and funded extra working-capital of only £1.7m, supported capex of £10.0m and incurred tax of £4.2m… which allowed a welcome £19m to be paid as dividends.

- TSTL’s five-year £10.0m capex was almost covered by the five-year £8.7m depreciation and amortisation expensed against five-year earnings.

- TSTL’s capex includes capitalised R&D, of which £2.0m was carried on this FY’s balance sheet and therefore has yet to be expensed against earnings. Amortisation of such development expenditure runs between seven and (an extremely lengthy) 25 years(!).

- TSTL’s ‘other’ cash movements are predominantly lease payments for properties that currently run at approximately £1m a year.

- Proceeds from option exercises have raised a useful £3.5m since FY 2020.

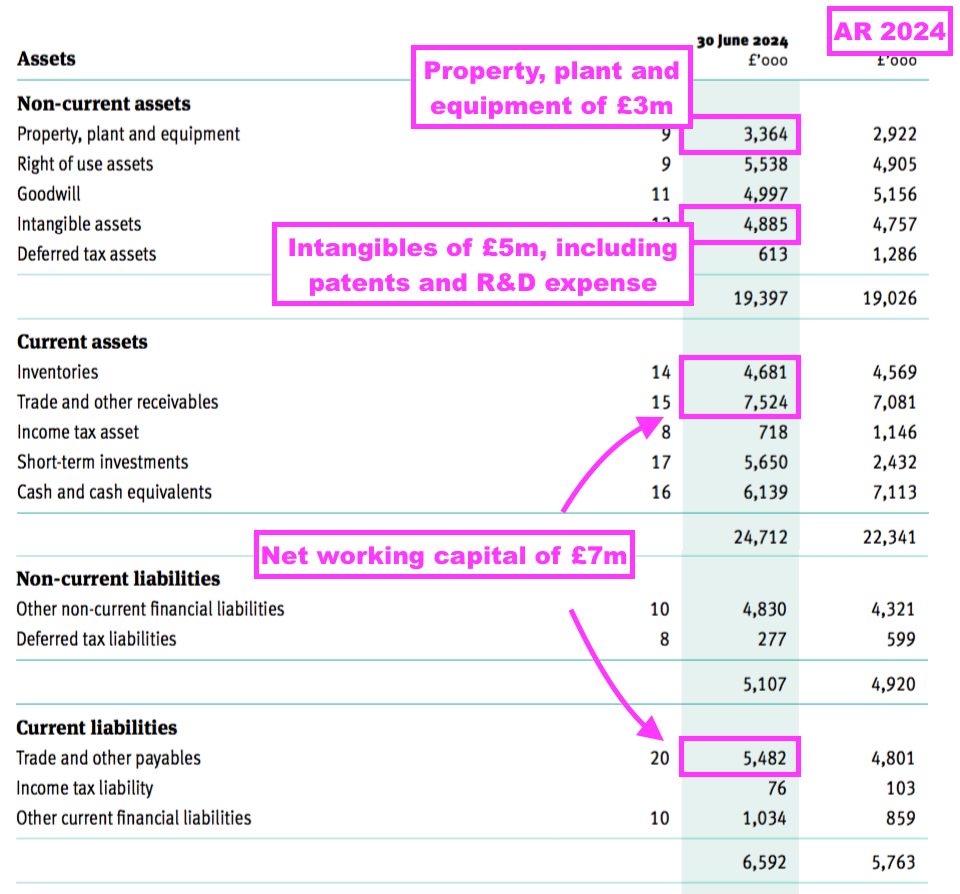

- TSTL’s balance sheet still implies the business remains an inherently capital-light operation.

- Net assets of £32m less goodwill (£5m) and cash (£12m) leaves £15m, represented mostly by working capital (£7m), various intangibles (£5m) and conventional property, plant and equipment (£3m):

- That £15m compares to this FY’s adjusted earnings of £7.1m and — alongside this FY’s lowly 1.13x dividend cover — supports the notion TSTL does not need to retain significant amounts within the business to advance profit further.

- TSTL carries no final-salary pension obligations.

New financial targets

- As mentioned earlier, this FY said TSTL’s new chief executive would publish his financial targets in due course: