01 October 2024

By Maynard Paton

H1 2024 results summary for Tristel (TSTL):

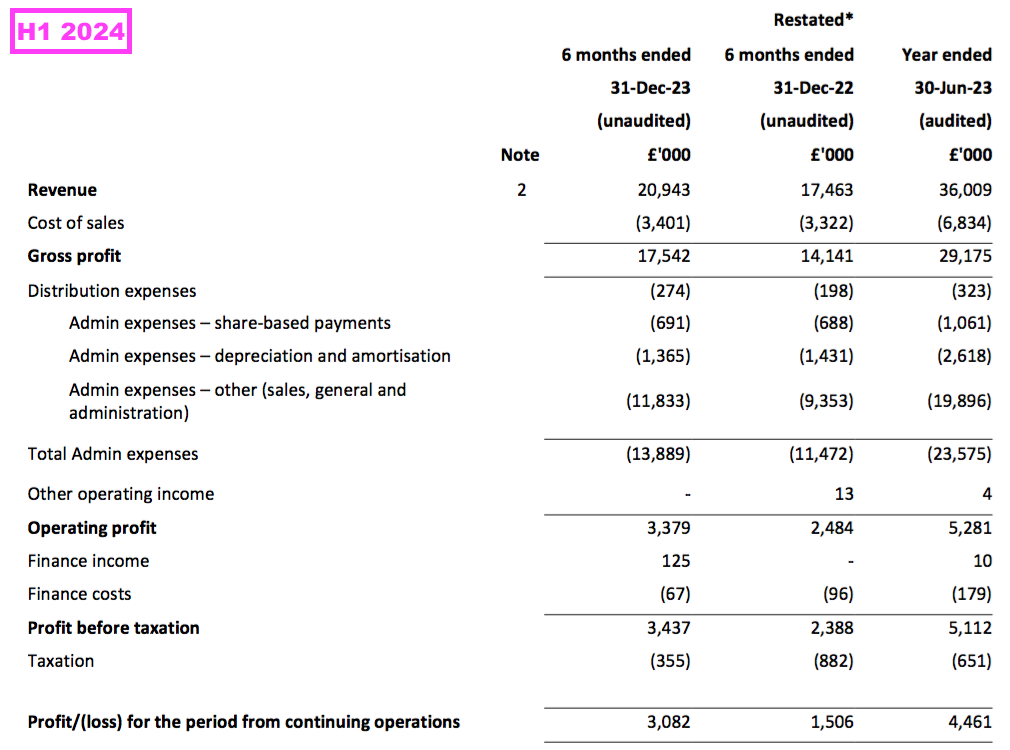

- A record H1, displaying revenue up 20%, profit up 28% and the dividend up 100% underpinned by remarkable 30% UK growth and notable price increases accepted by the NHS.

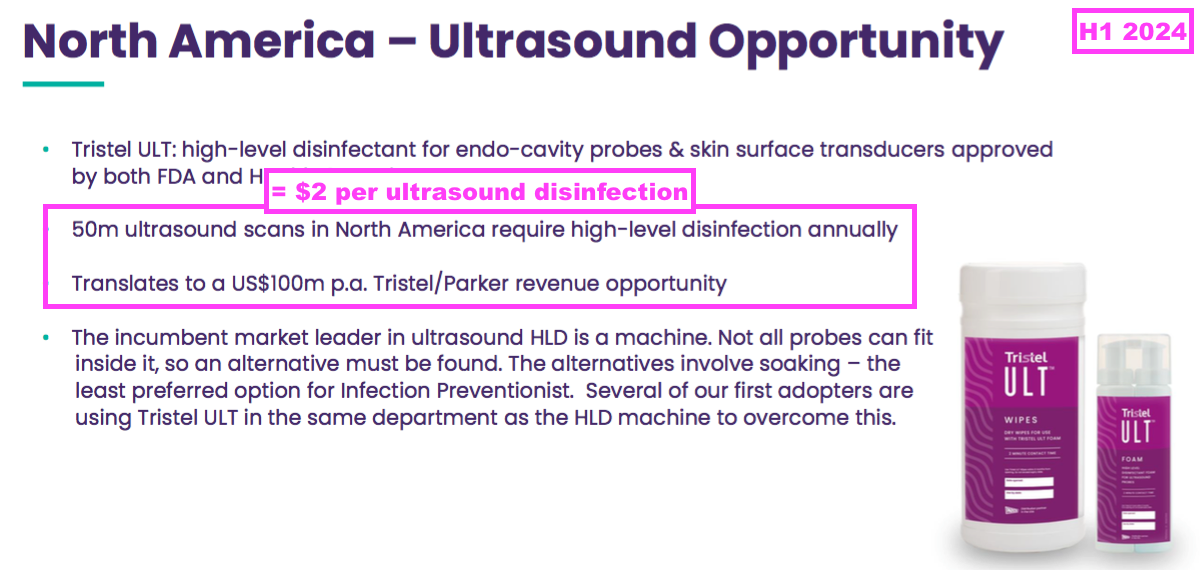

- North America is now deemed a “$100m per annum opportunity” for TSTL’s initial FDA-approved foam, although competition now involves an FDA-approved UV-light machine that may strengthen the wider argument for automated disinfections.

- The new chief exec ticks a lot of boxes for marketing healthcare products in the US, but his stint at LiDCO was unspectacular and shareholders keenly await his strategic ambitions, financial targets and details of his LTIP package.

- Although employee productivity has flat-lined, the financials remain in good shape with a bumper 84% gross margin and net cash approaching £12m that could lead to another special dividend.

- A near-term 32x P/E is not an obvious bargain, but a premium rating could be justified by further meaningful growth within established markets, the prospect of lucrative US royalties, the ongoing ability to raise prices and the possibility of successful R&D. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own TSTL

- Results summary

- Revenue, profit and dividend

- Medical-device decontamination

- Surface disinfection

- UK

- Overseas

- North America

- Patents and competing technologies

- Boardroom

- Share options

- Financials: margin and employees

- Financials: balance sheet and cash flow

- Valuation

News links, share data and disclosure

- Interim results, presentation and webinar published/hosted 26 February 2024;

- UK and EU regulatory approval update published 26 February 2024;

- Appointment of CEO published 10 June 2024;

- Trading update published 22 July 2024;

- Confirmation of CEO transition and Directorate Change published 02 September 2024, and;

- FDA 510(k) submission for Tristel OPH published 12 September 2024.

- Share price: 400p

- Share count: 47,650,093

- Market capitalisation: £191m

- Disclosure: Maynard owns shares in Tristel. This blog post contains SharePad affiliate links.

Why I own TSTL

- Develops the “simplest, quickest and most affordable high-performance disinfection” for medical devices, and faces limited direct competition due to proprietary chemistry, instrument-manufacturer approvals, scientific testimonies and regulatory hurdles.

- Enjoys a track record of superior growth founded upon a sizeable and resilient UK market position, alongside widening expansion opportunities abroad including the United States.

- Boasts financials that showcase super gross margins, significant net cash, respectable cash conversion and relatively low operational capital.

Further reading: My TSTL Buy report | All my TSTL posts | TSTL website

Results summary

Revenue, profit and dividend

- An upbeat outlook from the preceding FY…

[FY 2023] “We now have the opportunity to establish a global footprint for our products and technology. The outlook for the Company is the strongest it has been in its 30 year history.”

- …followed by positive progress reported at December’s AGM…

[RNS December 2023] “I am pleased to report that the Company has had a record first half with revenue for the six months ending 31 December 2023 expected to be £20.7m, an increase of 18% compared to £17.5m in the first half of last year. Revenue growth has been delivered across all our geographical markets. Gross margin remains above 80% in line with our expectations.

…

The business is performing strongly on all fronts and the confidence that we expressed in October in our medium-term outlook remains unchanged. With the growth possibilities for our business stronger than ever, and as a business with no debt and forecast cash balances of approximately £10.4m after payment of this year’s final dividend on 22 December, we are in a strong position to capitalise upon our global leadership position in the medical device decontamination market.”

- …had already signalled an encouraging H1 2024.

- This H1 boasted a slightly better performance versus the figures predicted at the AGM.

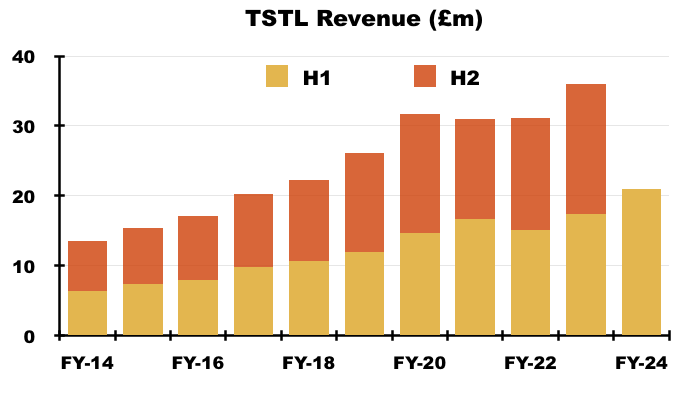

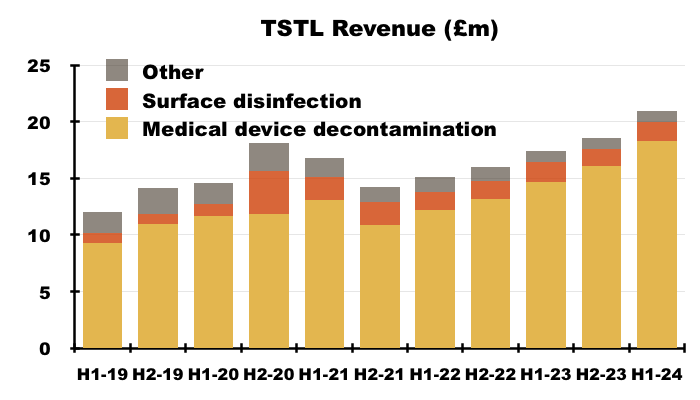

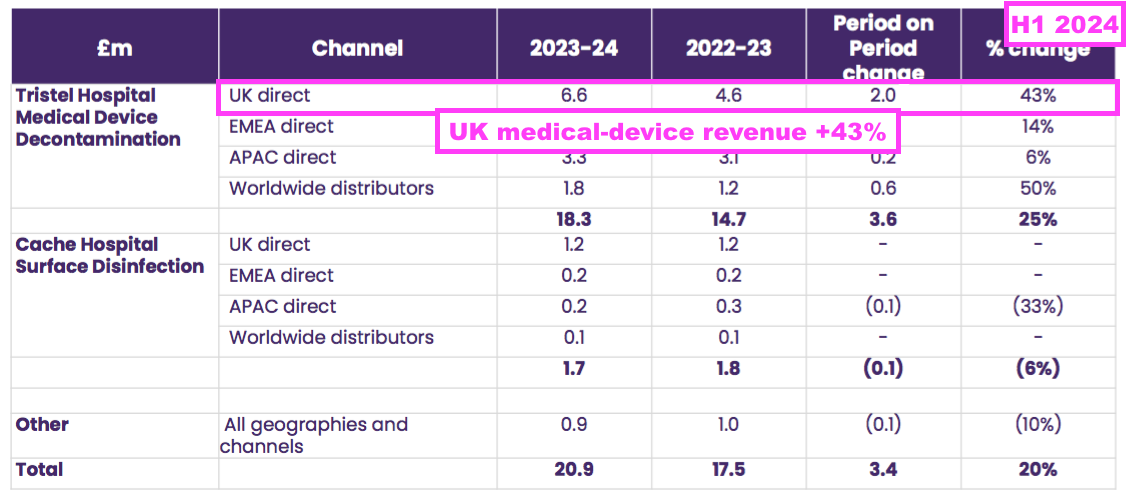

- H1 revenue in fact gained 20% to £20.9m to set a new H1 record:

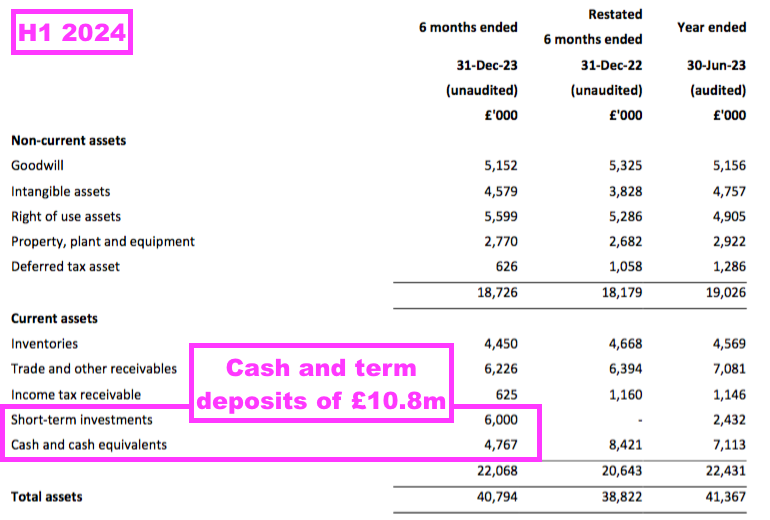

- Furthermore, the H1 cash balance was in fact £0.4m better than predicted at £10.8m (see Financials: balance sheet and cash flow).

- To underline how fast TSTL has grown during recent years, this H1’s revenue exceeded the £20.2m reported for FY 2017.

- This H1 was thankfully free of the revenue distortions — such as pandemic disruption, Brexit stock-piling and discontinued products — that have complicated TSTL’s progress since FY 2021.

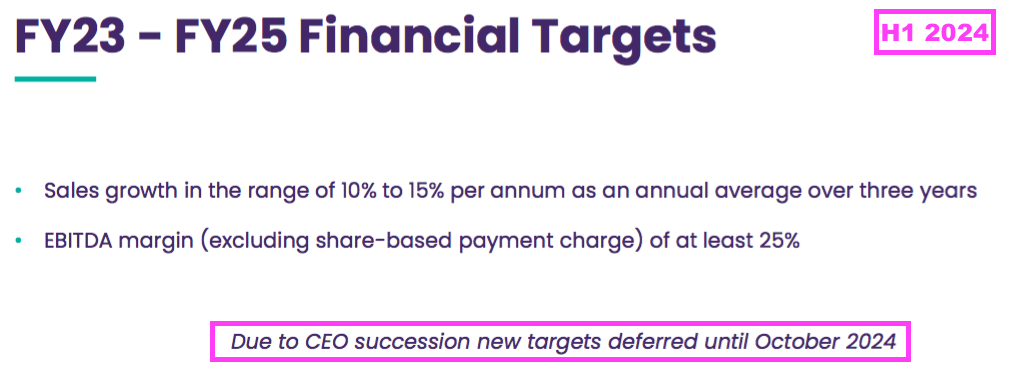

- This H1’s 20% revenue advance exceeded the 15% target reiterated during the preceding FY:

[FY 2023]

“In October 2022 we established our financial plan for the three years to 30 June 2025, which was a continuation of the plan for the prior three-year period ending in June 2022. The three key financial targets of both the old and new plans are:

1. Sales growth in the range of 10% to 15% per annum as an annual average over the three years

2. The achievement in each year of an EBITDA margin (excluding share-based payment charge) of at least 25%, and

3. To increase profit before tax (excluding share-based payments) year-on-year, independently of the other two targets”

- TSTL commendably split the 20% revenue advance between volume and pricing:

“Higher sales volume accounted for £1.5m of the £3.4m revenue growth and price increases accounted for the remaining £1.9m. This represents an average price increase of 12%, reflecting the global inflationary environment. In the UK the increase has been higher because of supply agreements which require fixed pricing extending into the future.“

- If the average price increase was 12%, then volumes must have improved by approximately 8% to reach the 20% total revenue advance.

- The reference to “supply agreements which require fixed pricing” in the UK presumably relates to sales to the NHS supply chain, the pricing frameworks for which TSTL has in past disclosed run for four years (see UK).

- For perspective, the comparable H1 witnessed an average 4% price rise that implied volumes advanced by approximately 12%:

[H1 2023] “Of the increase in revenue of £2.4m, £1.8m relates to additional volume and £0.6m to pricing, which reflects a 4% global price rise.“

- Volume growth reducing from 12% during the comparable H1 to 8% during this H1 is not ideal.

- Given this H1’s average 12% price rise, management’s H1 webinar unsurprisingly stressed future revenue would be driven by greater volumes rather than further inflationary increases:

“We have our financial targets of sales growth in the range of 10 to 15% but I think it is safe to say those growth rates will be absolutely very much volume-led. We do have a price increase annually but we generally pitch that at inflation.“

- Assuming UK and EU inflation both run at their targeted 2%, volumes need to advance by a minimum 8% annually to meet the group’s 10-15% average revenue growth target.

- No doubt volume growth and price increases will be factors the new chief executive considers when (or if) he publishes TSTL’s new financial targets (see Boardroom):

- This H1 was thankfully not blighted by further restatements beyond those already recorded for FYs 2022 and 2023.

- Without Brexit stock-piling, discontinued products and US regulatory costs, TSTL’s profit progress has become easier to analyse. Only share-based payments remain a complicating factor (see Share options).

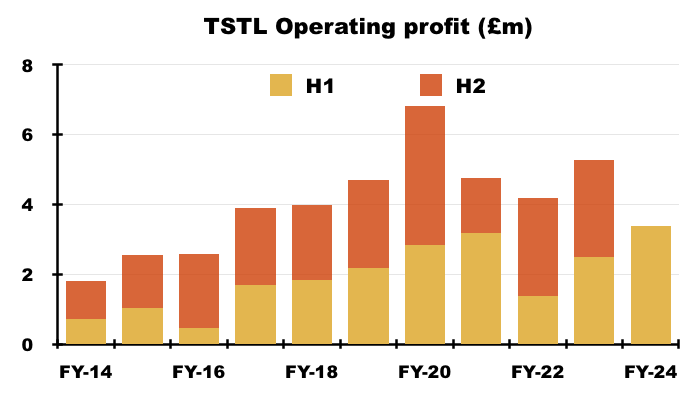

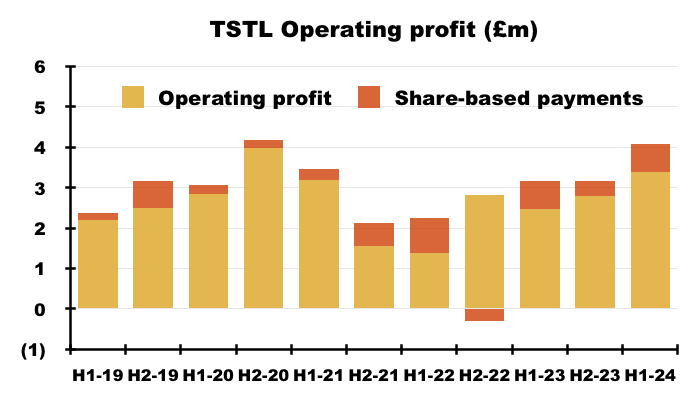

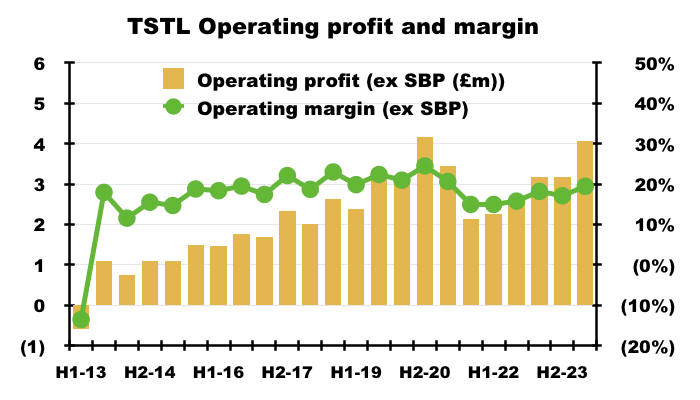

- Including share-based payments, this H1’s operating profit gained £0.9m, or 36%, to set a new H1 record of £3.4m:

- Excluding share-based payments, this H1’s operating profit gained £0.9m, or 28%, to set a new H1 record of £4.1m:

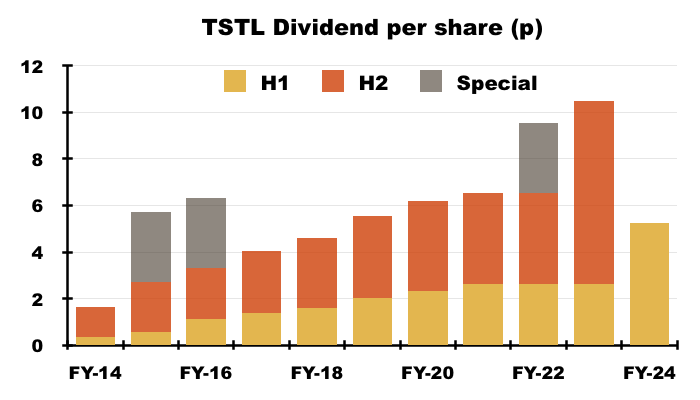

- The preceding FY revealed the ordinary dividend will now advance by at least 5% a year — irrespective of whether earnings rise or fall:

[FY 2023] “Going forward the Board’s intention is to increase the dividend annually in line with the year’s increase in EPS, committing to minimum dividend growth of 5%.”

- Whether the new chief executive will maintain this bold payout commitment remains to be seen (see Boardroom).

- The H1 dividend was lifted a very welcome 100% to 5.24p per share and matched the doubling of the preceding FY’s final payout:

- The doubled H1 dividend was still covered 1.65x by TSTL’s 8.68p per share adjusted earnings.

- Management’s H1 webinar referred to a 40/60% split between interim and final dividends…

“It’s not a straightforward doubling of the interim and a doubling of the final. The new dividend policy is that for the full year, the dividend will follow the same percentage increase as EPS achieved for the full year and with a floor of 5%, so we will always increase our dividend by 5%. But if EPS is increased by more, we will increase the dividend by more. We have a 40/60% split of interim to final and the maths worked out that there’s a doubling of the interim. It’s just a simple calculation.”

- …which, if implemented for FY 2024, implies the upcoming H2 2024 final payout will be unchanged at 7.88p per share.

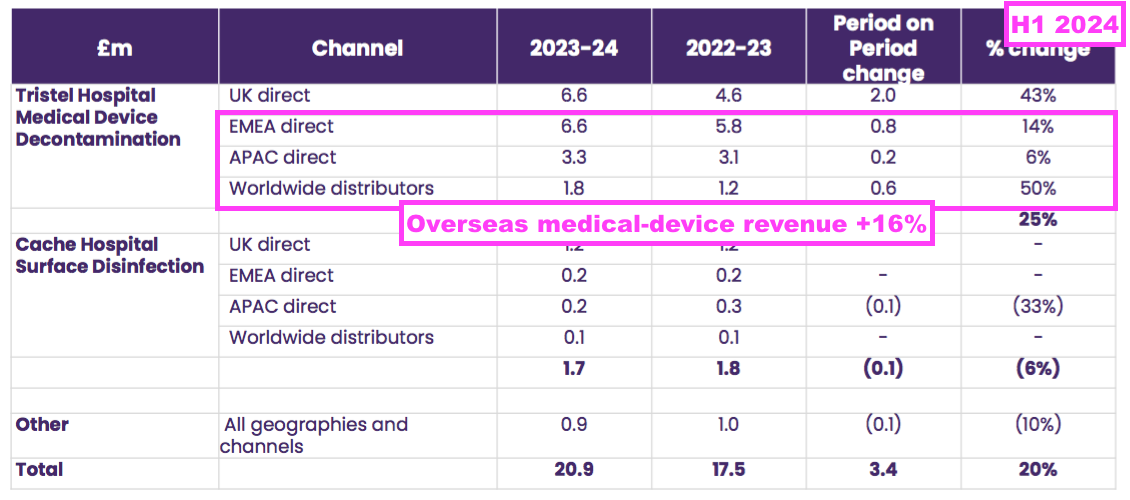

Medical-device decontamination

- TSTL’s wipes and foams that decontaminate medical devices remain by far the group’s most successful products:

- During this H1, 87% of revenue and 91% of gross profit were generated from the wipes and foams:

- H1 revenue from the medical-device wipes and foams improved a super 25% to £18.3m.

- TSTL implied the 25% advance had led to market-share gains:

“Tristel medical device sales grew by 25%, reaching £18.3m. In all countries in which we sell we continue to build our market leadership position. We are also benefiting from an increase in diagnostic procedure numbers as hospitals worldwide continue to tackle backlogs caused by the pandemic.“

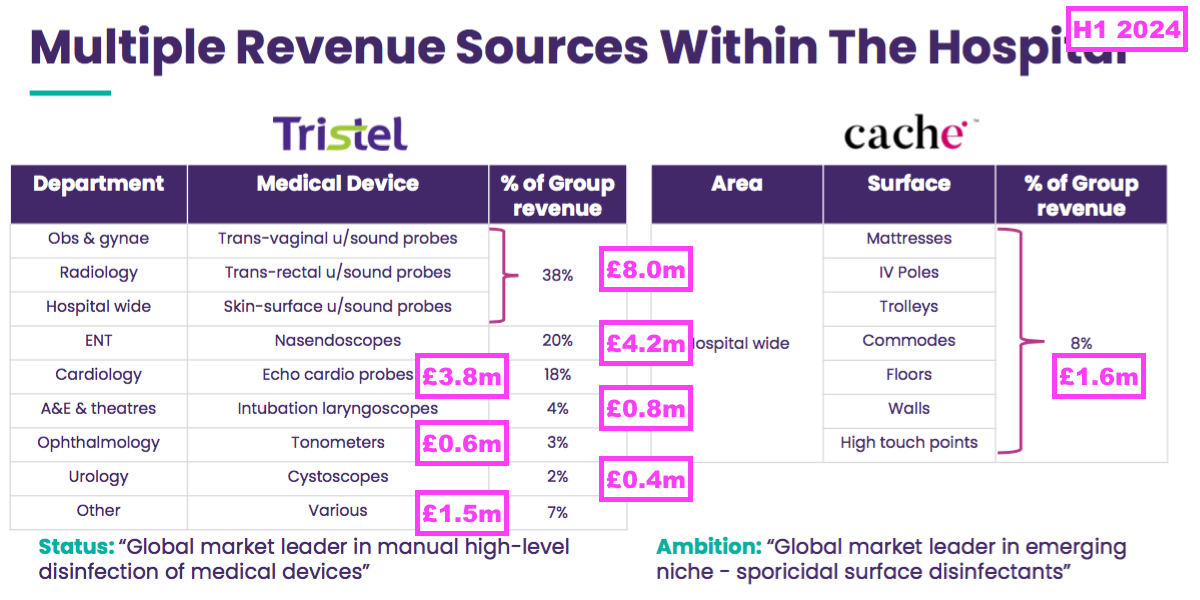

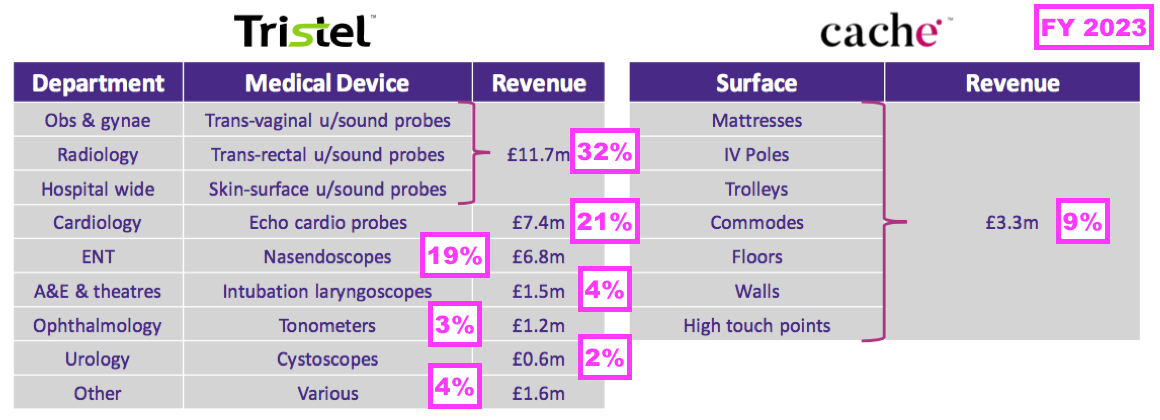

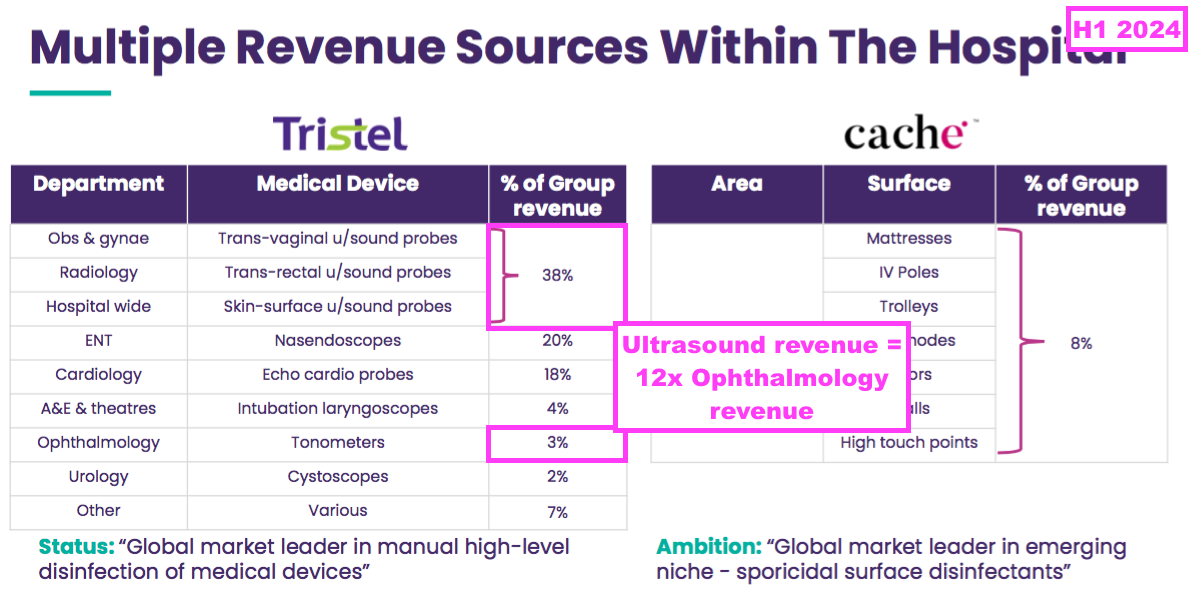

- This H1 provided a breakdown of revenue generated by different kinds of medical device:

- Decontaminating ultrasound probes represented 38% or £8.0m of total H1 revenue (and 43% of H1 medical-device revenue).

- However, last year’s FDA-approval RNS suggested the figure was closer to 50%:

[RNS June 2023] “Approximately half of Tristel’s global revenue is generated from the ultrasound market.“

- Decontaminating ultrasound probes appears to have become more significant to TSTL during this H1 versus the preceding FY:

- Revenue of £11.7m earned from decontaminating ultrasound probes during the preceding FY supported 32% of the preceding FY’s revenue, versus 38% for this H1.

- Other hospital departments changing their revenue proportion between the preceding FY to this H1 were:

- Cardiology, from 21% to 18%;

- ENT, from 19% to 20%, and;

- ‘Other’, from 4% to 7%.

- Management’s H1 webinar reiterated the high levels of Tristel usage within the NHS:

“We measure [NHS penetration] by different areas of the hospital. As an example, we estimate… within the NHS around 60-70% of ultrasound procedures… use a Tristel product. The ENT market is about the same level of penetration for Tristel products used to decontaminate Nasendoscopes. Within Cardiology for T probes, we have a very high level of penetration, in the region of 85-90%… We do certainly sell into every hospital within the UK. In some hospitals we are widely used and in others less so.“

- Although TSTL helpfully disclosed the number of procedures during the comparable H1…

- …and the July 2023 open day…

- … no mention of procedure numbers was made during this H1.

- Revenue per procedure (and in particular, per ultrasound procedure) can help shareholders gauge the market potential of the United States (see North America).

- My online searching shows TSTL’s Trio Wipes system available to buy for £377 + VAT and its Duo ULT foam available to buy for £264 + VAT.

- For what it is worth, both products have seen their prices increase by £13 since my FY 2023 write-up.

- The Trio Wipes system contains enough wipes to conduct 50 disinfections and therefore costs the purchaser £7.54 per disinfection (£377/50). The Duo ULT foam gives 310 doses — equivalent to 155 disinfection procedures — and therefore costs the purchaser £1.70 per disinfection (£264/155).

- TSTL’s income will be less than £7.54 or £1.70 per disinfection because:

- A gross margin will be captured by the retailer selling the wipes and foams, and/or;

- Major buyers can buy in bulk direct through TSTL at reduced prices.

Surface disinfection

- FY revenue from TSTL’s hospital-surface disinfectants fell 8% to £1.6m:

- The preceding FY had blamed regulatory backlogs for delays to launching new surface products:

[FY 2023] “Our second product range, Cache, made much slower progress during the year. Revenue was £3.3m compared to £3.2m in the previous year. Part of the new Cache range is still in the product design and testing stage, and the part of the range which is ready to be actively marketed is waiting for regulatory approvals in key markets.

In Europe, CE marking is required for medical device disinfectants, and while the Cache product range is intended for environmental surfaces, many of the surfaces around the patient are considered medical devices requiring CE marking as well as approval under the European Biocidal Products Regulation. Post Brexit, the UK introduced UKCA Marking Certification for medical devices, and we are waiting to receive UKCA approval for the new Cache products.”

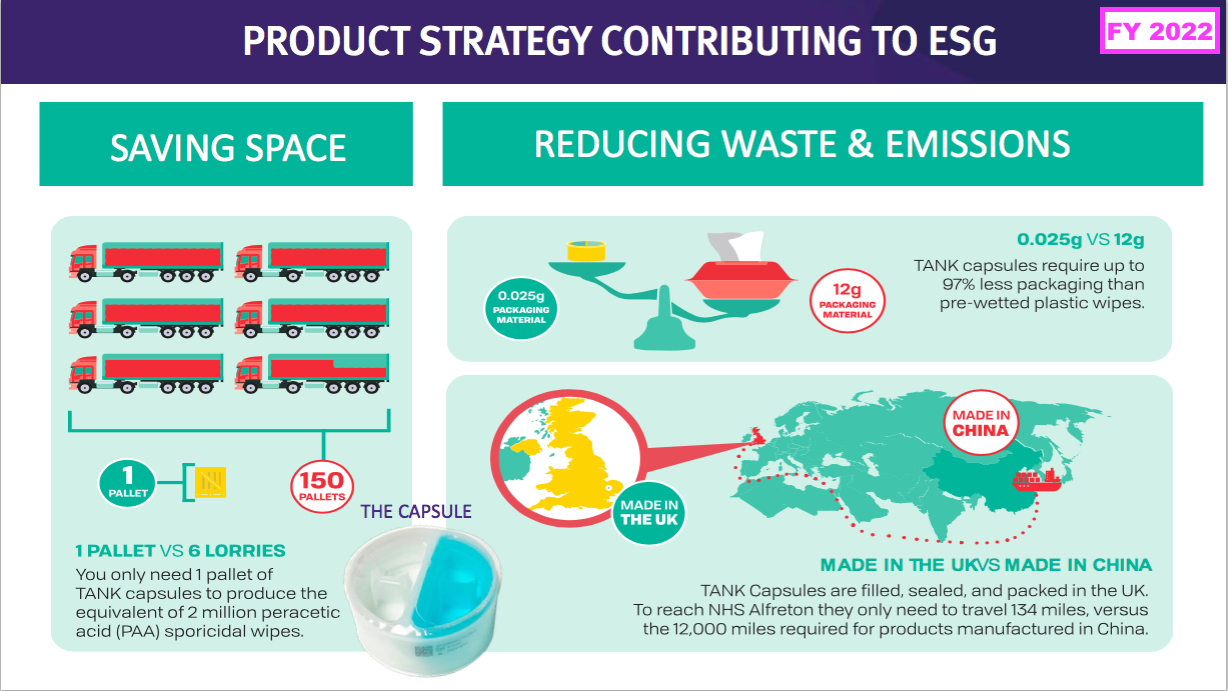

- An announcement accompanying this H1 confirmed the regulatory backlogs had been cleared and regulatory approvals had been granted for TSTL’s TANK system:

[RNS February 2024] “Tristel plc (AIM: TSTL), the manufacturer of infection prevention products utilising proprietary chlorine dioxide technology, announces that all reviews under the Medical Devices Regulation 2002 (“UK MDR”) and the European Union Medical Device Regulation 2017/745 (“EU MDR”) for approval of the Company’s TANK ClO₂ Sporicidal Disinfectant system have been successfully concluded and a positive recommendation for UKCA and MDR certification has been made.

The TANK system and accompanying capsules are the newest additions to the Cache range, which provides sporicidal surface disinfection in a format which is a sustainable alternative to commonly used pre-wetted plastic wipes.”

- The accompanying RNS claimed the approval provided the opportunity for “significant growth is sales” in a “largely untapped” surface-disinfection market:

[RNS February 2024] “Following MDR approvals Tristel will be able to accelerate sales activity for this product throughout Europe and across geographies that recognise the high standard of safety and quality demonstrated by products conforming to the new EU MDR. The Directors believe that approval, will give Tristel the opportunity to deliver significant growth in sales of the Cache product range going forward, targeting a largely untapped sporicidal surface disinfection market. The Company expects to officially launch these latest products in Europe before the current financial year end on 30 June 2024.

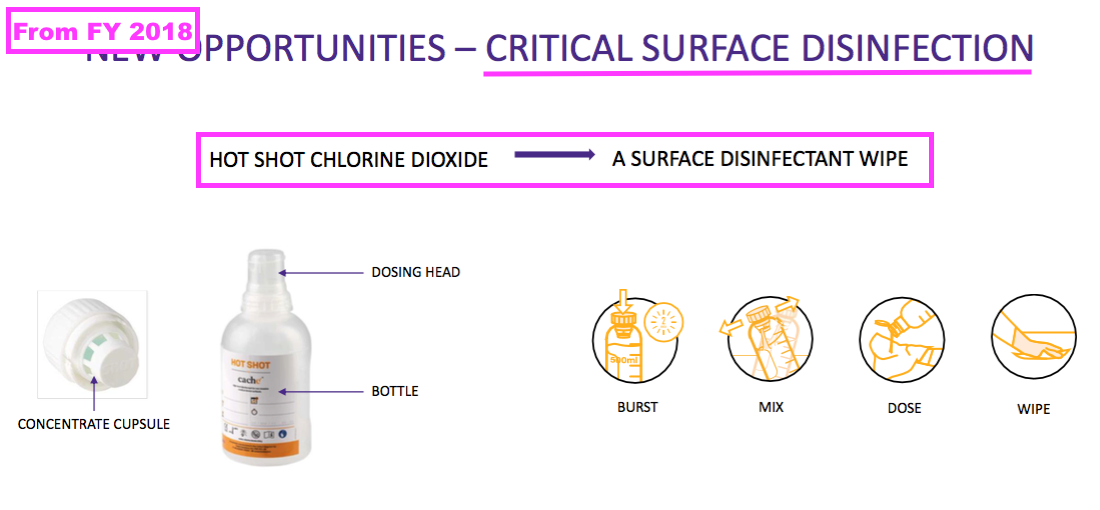

- Development of the new surface disinfectants has been slow going, with prototypes showcased as far back as FY 2018:

- TSTL’s surface disinfectants have struggled to take off due to their higher pricing versus less effective alternatives.

- But management’s H1 webinar reiterated the new TANK product would offer pricing comparable to the low-cost alternatives:

“Certainly the surface disinfection market is not willing to pay the premium that that the device disinfection market is willing to pay.

So we’ve designed our [TANK] product for two purposes: one, to address bleach, which is used to mop floors and clean large surface areas within the hospital, and; two, to be used for damp-dusting around the patient, so mattresses, UV poles, trolleys, bedside tables, all of those areas where patients are placed and they are high touch surfaces so in that instance a sporicidal disinfectant is really, really important.

Not every hospital can afford to use a sporicide around the patient, so we are bringing our product to market at the lowest possible price to combat the products that are incumbent within floor cleaning, which is bleach, and near patient areas, which tend to be plastic wipes pulled out of a flow wrap for continual use. We can we can rival both of those products and price [TANK] at the lower of the two prices.”

- Management’s H1 webinar repeated claims the new surface products could one day generate sales equal to those of the medical-device disinfectants:

“We have valued the surface-disinfection market at £4 billion globally. How far do we think we can go with our Cache product range? I’m not going to say when, but in time we expect it to rival the size of our medical-device sales. It is a huge market. It’s a niche for us because we provide a very high disinfecting performance level and we can do that at the price of a low- or intermediate-level competitive product. So there is a huge opportunity for us to be transformational in the surface-disinfection market. Although it sounds like a big ask to grow our Cache market to the size of our Tristel market, there is the potential for it.“

- Medical-device revenue of £18m was 11x surface-disinfection revenue during this H1.

- The drawback to surface disinfectants for shareholders may be their significantly lower price point compared to the medical-device wipes and foams.

- Enormous volumes will be needed for surface disinfectants to represent a notable proportion of TSTL’s business.

- For example, management’s FY 2018 presentation suggested the NHS was purchasing low-grade surface wipes at 2p a pop.

- My online searching found 200 basic wipes for £7.55 + VAT, or 3.8p + VAT a pop.

- For perspective, assuming TSTL price-matches the 2p, selling the TANK equivalent of 900 million surface wipes — i.e. 450,000 TANK capsules — would equal the £18m revenue from medical devices during this H1.

- This TSTL website showcases the new surface disinfectants and their environmental credentials versus pre-wetted plastic wipes:

- In theory at least, a much more effective surface cleaner that is priced identically to bleach and low-grade plastic wipes — as well as being much more environmentally friendly — ought to have a big future…

- … or leave TSTL with very awkward questions to answer should surface-disinfection sales continue to stagnate.

- Another awkward question might concern the Trio Wipes system using plastic wipes when TSTL is promoting the environmental benefits of TANK against similar wipes:

UK

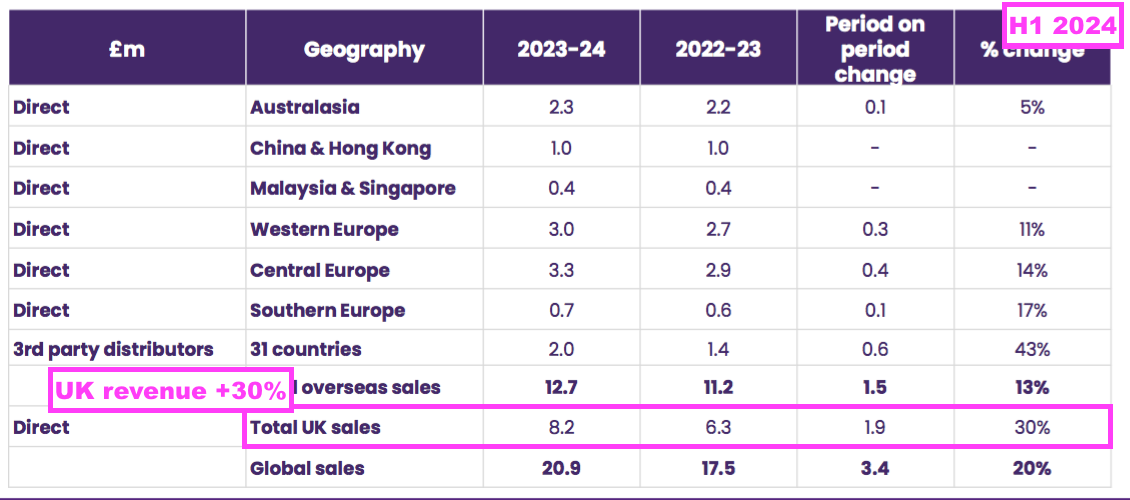

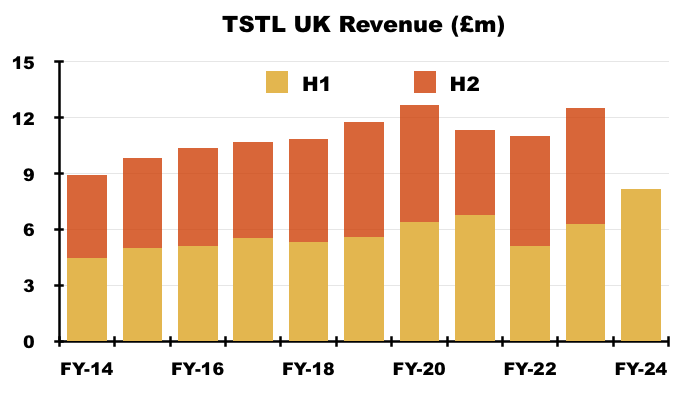

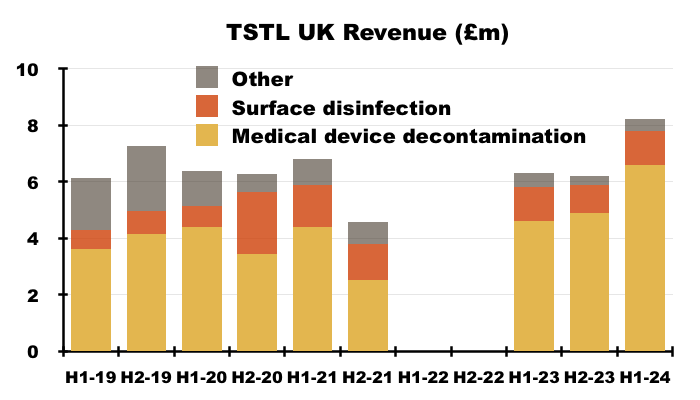

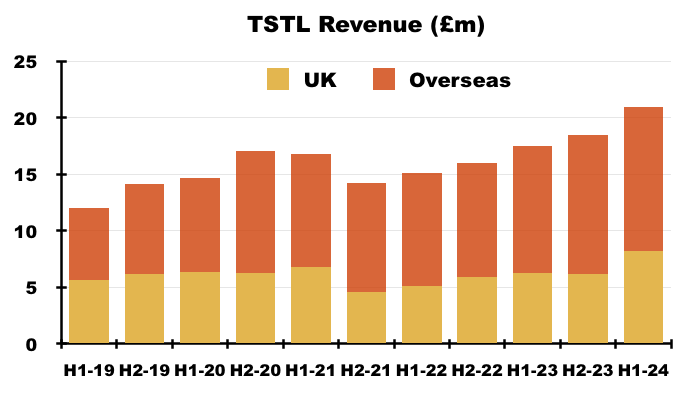

- The UK remains TSTL’s largest individual market after H1 revenue gained a startling 30% to to set a new six-month UK record of £8.2m:

- The aforementioned “supply agreements which require fixed pricing” for the NHS undoubtedly underpinned the 30% improvement.

- If UK volumes matched group volumes and increased by approximately 8% during this H1, then NHS price increases may therefore have been approximately 20% — albeit with NHS prices fixed thereafter for the next few years.

- UK progress has in the past been influenced by Brexit stock-piling and sales of legacy/discontinued ‘Other’ products.

- But a clearer picture is now emerging about TSTL’s UK efforts — and a 30% sales increase that was mentioned only briefly during management’s H1 webinar…

“Within the UK, we’re reporting 30% growth. So again, very encouraging for us with new and an increasing number of customers. Our procedure numbers are up and our market penetration continues to increase.”

- …might suggest a very favourable pricing agreement with the NHS that TSTL does not want to publicise.

- Indeed, UK price increases for medical-device wipes and foams may have increased by much more than 20%, given such revenue during this H1 advanced by a staggering 43% to £6.6m:

- Medical-device UK revenue supported 80% of total UK revenue during this H1, the highest proportion ever:

- The NHS price increase helped total UK revenue to represent 39% of total H1 revenue — the highest six-monthly UK proportion since H1 2021:

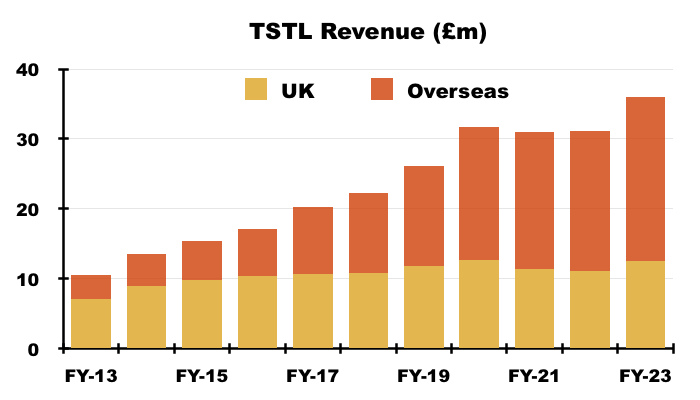

- Longer term though, UK revenue has progressively become a smaller part of TSTL as the group expanded overseas through deft purchases of international distributors (see Overseas):

- Still, the UK may continue to expand at a respectable rate; the 2023 annual report (point 19e) disclosed a 9% revenue growth rate was employed to test the value of TSTL’s UK goodwill:

[AR 2023] “For Tristel UK, the key assumptions used to determine the recoverable value of goodwill are those regarding discount rates and growth rates… Based on a revenue growth rate of 9%, the net present value of future cash flows exceeds the carrying value of £8.602m by £64.390m, as such no impairment has been recorded.”

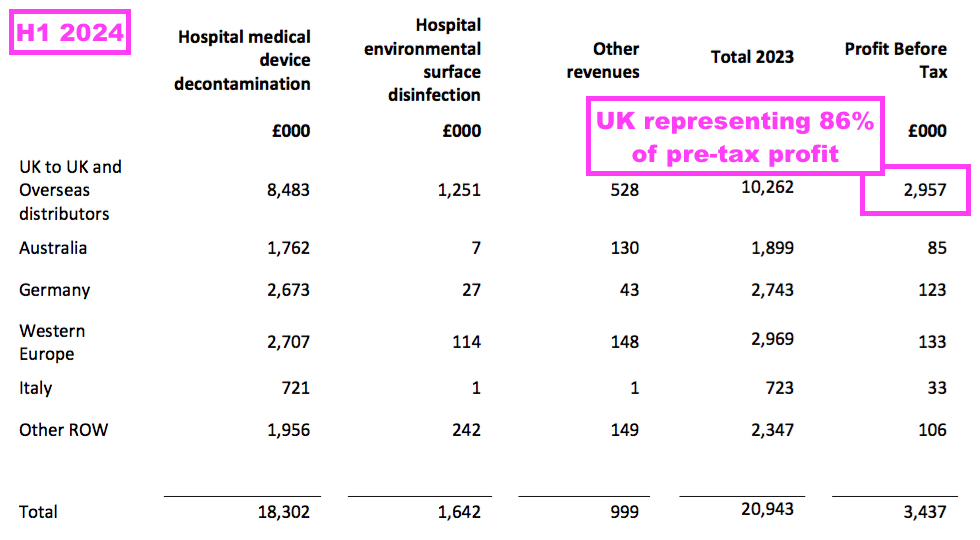

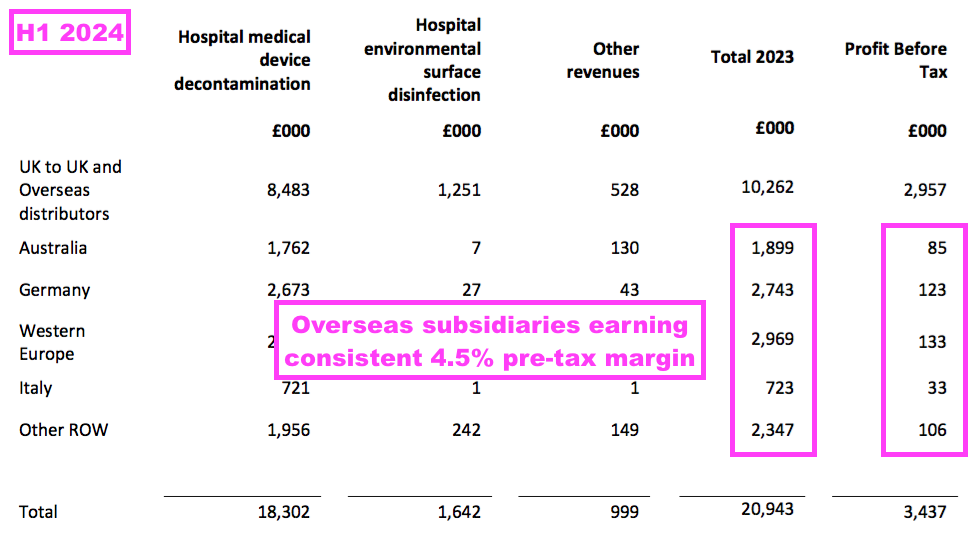

- This H1 revealed segmental profit for the UK and other sales regions:

- A UK pre-tax profit of £3.0m represented 86% of group pre-tax profit, despite UK sales representing 39% of total revenue.

- Management’s preceding FY webinar explained the UK profit bias, citing the group’s “transfer pricing policy” and wishing to “achieve the best tax profile“.

- All TSTL’s manufacturing occurs in the UK, and the products are sold to the group’s overseas divisions on an ‘arm’s length’ basis for resale within their respective markets.

- TSTL therefore registers all of its ‘manufacturing profit’ within the UK.

- Management’s preceding FY webinar noted all the overseas sales regions have their profit margin set at 4.5%.

- A 4.5% margin was once again declared for all of the overseas regions for this H1:

- Trailing twelve-month UK revenue of £13.7m still provides a good benchmark for the sales potential of other countries.

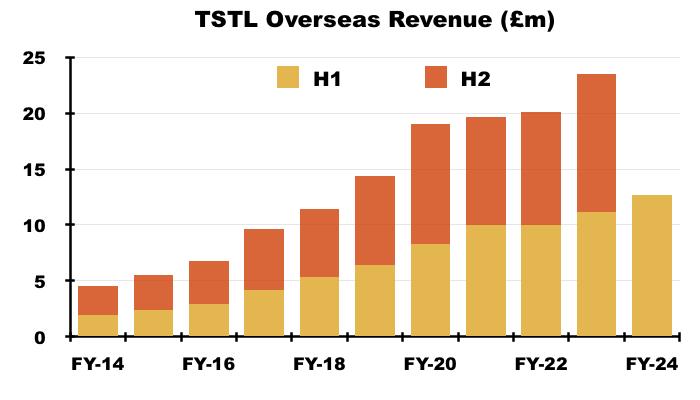

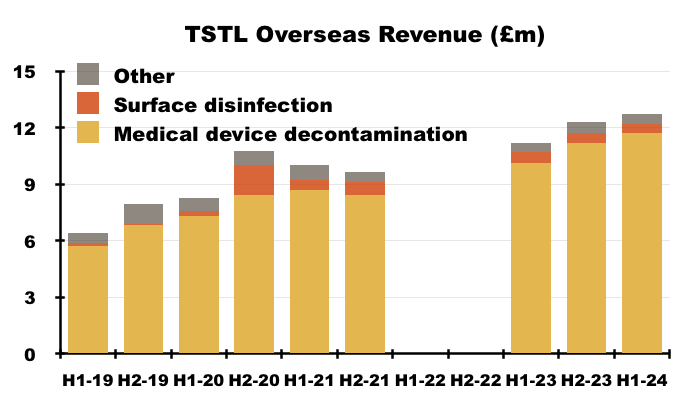

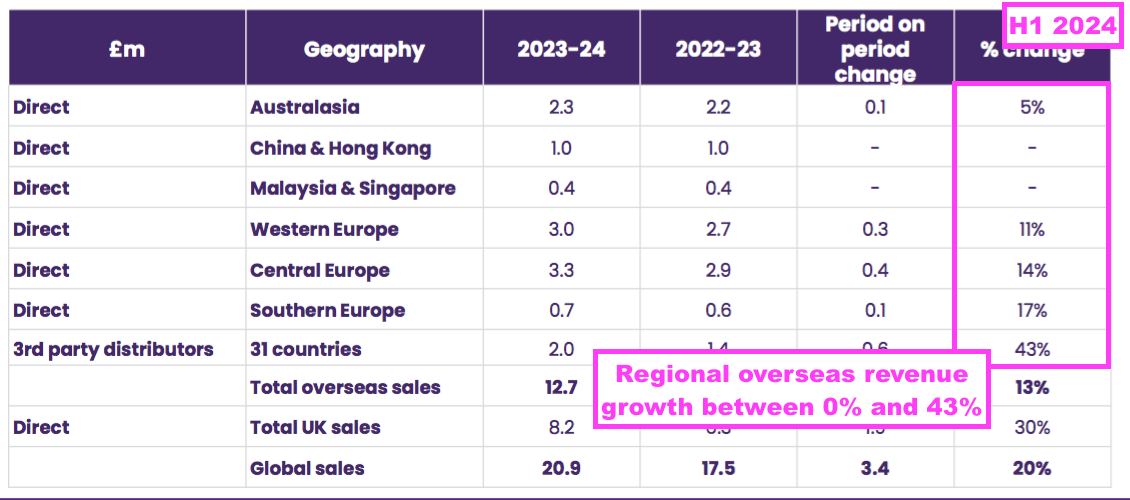

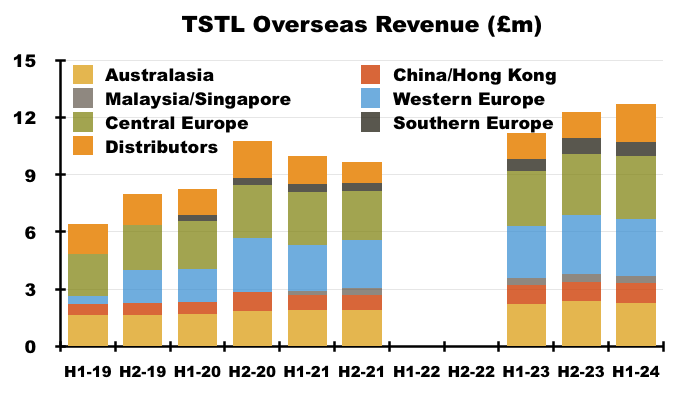

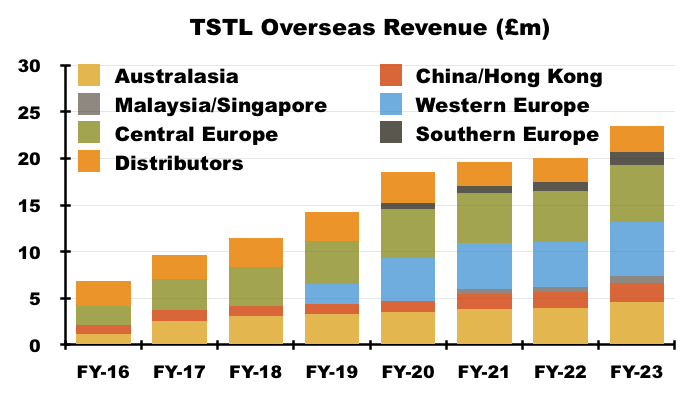

Overseas

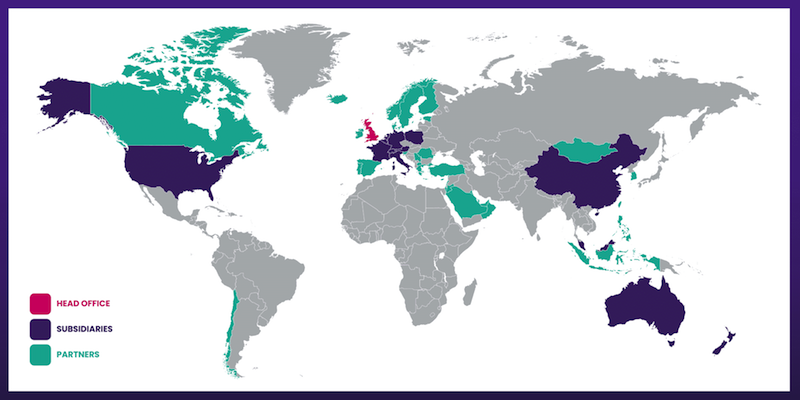

- Overseas revenue is derived from a mix of direct operations and independent distributors that combine to sell within more than 30 countries:

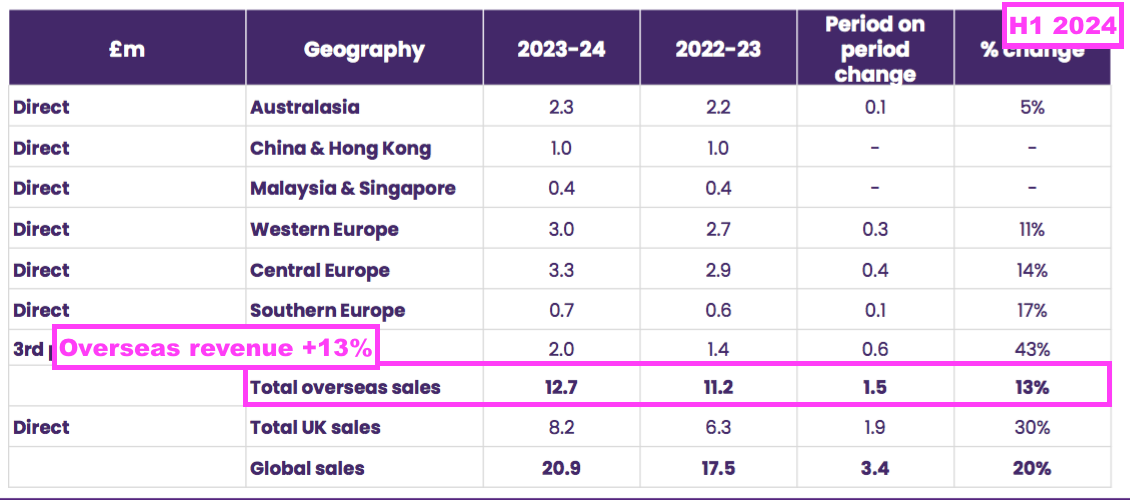

- Overseas revenue climbed 13% to £12.7m during this H1 to set a new six-month Overseas record:

- Overseas sales of the ‘core’ medical-device disinfection products gained 16% to £11.7m:

- TSTL’s Overseas subsidiaries registered differing H1 revenue progress:

- Management’s H1 webinar claimed the static progress within the Asian operations was due to lower demand for hospital-surface disinfectants:

“Asia has been a bit of a conundrum for us. China, Hong Kong, Malaysia and Singapore have been flat during the six months. The underlying mechanics of that are that our medical-device business grew but our Cache surface product sales declined very slightly, the reason for which we think is down to pricing. But with the recent approval of TANK, we believe we can go back into those hospitals in Asia and demonstrate the product and offer it at a lower price, which will enable us to get back onto a growth trajectory within Asia.“

- That earlier slide did show APAC surface-disinfection sales down 33%.

- Management’s H1 webinar noted the impressive achievements of the third-party distributors:

“Our international third-party distributors achieved the highest level of growth within the entire business of 43% which is really encouraging… because it demonstrates that in these in these younger markets the same thing is happening as has happened in the early stages of our direct-sales teams.

We are achieving high growth rates in particular, we’ve noticed the Middle East is a very encouraging area for us. Saudi sales grew by£230,000 of that £600,000 growth. Spain increased by over a £100,000 and Ireland and the UAE were all really strong contributors to our distributor growth number.”

- Third-party distributors that perform well can become acquisition targets for TSTL.

- TSTL acquired:

- Its Australian distributor for £1.1m during FY 2017;

- Its Belgian/Dutch/French distributors for £6.4m during FY 2018, and;

- The remaining 80% of its Italian distributor for £0.6m during FY 2020.

- I calculate:

- Annual Australasian sales (i.e. Australia and New Zealand) have since climbed 126% from approximately AU$3.9m to approximately AU$8.8m (7.5-year CAGR: 11%);

- Annual Western Europe sales (i.e. Belgium, Netherlands and France) have since climbed approximately 128% from €3.1m to approximately €7.0m (5.5-year CAGR: 16%), and;

- Annual Southern Europe sales (i.e. Italy) have since climbed 146% from €700k to approximately €1.7m (4.5-year CAGR: 22%):

- In addition, TSTL established a Malaysian subsidiary at the start of FY 2021 after recruiting the team that had worked previously as the country’s distributor. Annual Malaysian revenue currently runs at £0.8m.

- And TSTL paid £339k during the preceding FY for a distributor selling to the Middle East and North Africa. TSTL has yet to disclose the revenue from this operation.

- Management’s H1 webinar claimed there was “still a lot to go for here within Europe”.

- Mind you, not every foreign market has been performing strongly. The 2023 annual report (point 19c) disclosed revenue within Belgium and the Netherlands declined during the preceding FY:

[AR 2023] “Management has considered the sales decline shown in Belgium and Netherlands in the current year and sensitised the recoverable value calculation to show 2-7% sales growth over the five-year period and an increasing cost base of between 4% and 7%, assuming all other assumptions remain unchanged.“

- France may therefore have performed very well given total Western Europe sales gained 11% during this H1.

- And TSTL has barely mentioned its progress within India after first gaining regulatory approval from the country during 2019.

- The aforementioned positive H1 webinar references to Spain and Ireland…

“Spain increased by over a £100,000 and Ireland and the UAE were all really strong contributors to our distributor growth number.”

- …coupled with dormant subsidiaries in both countries…

[FY 2023] “We have subsidiaries in the United States, Japan, India, Spain and Ireland which are not yet active in terms of selling.”

- …suggests the two nations may become TSTL’s next in-house operations.

- One subsidiary that has recently moved from dormant to active is the United States.

North America

- TSTL received regulatory approval for selling an ultrasound-probe disinfectant in the United States during June 2023, and the preceding FY confirmed the first US orders had been “shipped and invoiced“:

[FY 2023]

Sales and marketing:

First orders shipped & invoiced

• Parker distributors include: Medline Industries / Henry Schein / Owens & Minor / McKesson Corp

• Listing in hospital and distributor procurement systems underway

• FY24 Parker exhibiting at 7 major USA conferences and Innova at 2 major Canadian conferences, supported by Tristel team

- This H1 revealed the initial US orders were “shipped and invoiced“ for “beta testing“:

“Parker’s manufacturing processes have been validated by our quality team and production is now underway. The product has been through beta testing at a number of healthcare institutions in the United States, with very positive feedback. Parker Laboratories plans an extensive marketing and trade show programme throughout 2024 and is in the process of expanding its salesforce in order to capitalise on the potential that Tristel ULT represents.”

- “Beta testing” suggests US hospitals conduct a trial period before committing to proper orders.

- This H1 revealed North American income of £46k during the first “ten weeks of activity“:

“During the first ten weeks of activity our revenue and royalty income from North America totalled £46k. We are very encouraged by this positive start.”

- Management’s H1 webinar reiterated TSTL collects a 24% royalty on US product sales, which implies US manufacturing partner Parker Laboratories generated US revenue via TSTL of up to £192k.

- The preceding FY’s webinar said US hospitals were expected to pay between $3 and $3.50 per disinfection procedure for TSTL’s foam, with Parker collecting $2 and its appointed sales distributors capturing between $1 and $1.50.

- TSTL’s 24% royalty therefore equates to 24% of $2 = $0.48 = 36p per US disinfection with GBP:USD at 1.33.

- Between $3 to $3.50 is equivalent to between £2.26 to £2.63, and is 33%-plus greater than the aforementioned £1.70 per disinfection when buying the equivalent foam within the UK.

- Management’s H1 webinar disclosed Parker was “doubling” its national salesforce, which may imply Parker could capture more of the $3 to $3.50 per disinfection for itself, which in turn would give a greater value to TSTL’s 24% royalty.

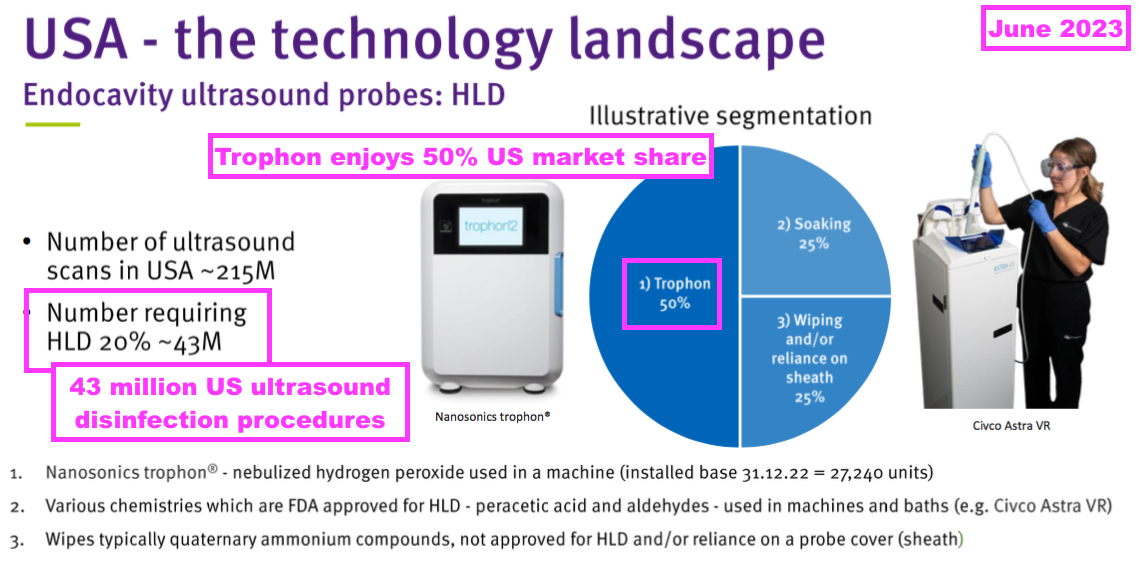

- TSTL previously indicated US hospitals should undertake 43 million ‘high level’ ultrasound-disinfection procedures a year:

- This H1’s webinar reckoned North American hospitals require 50 million ‘high-level’ ultrasound disinfection procedures annually…

- …which translate into a “$100m per annum opportunity” for TSTL and Parker Labs.

- 50 million procedures at the aforementioned $2 per procedure for Parker gives that $100m.

- A “$100m opportunity” leads to a potential $24m ultrasound-royalty maximum for TSTL, and — using the aforementioned $3 to $3.50 per procedure — implies a possible maximum expenditure by North American hospitals of $175m on TSTL’s ultrasound foam.

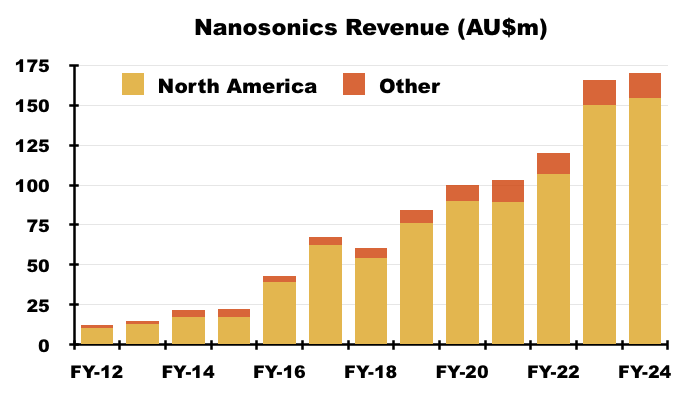

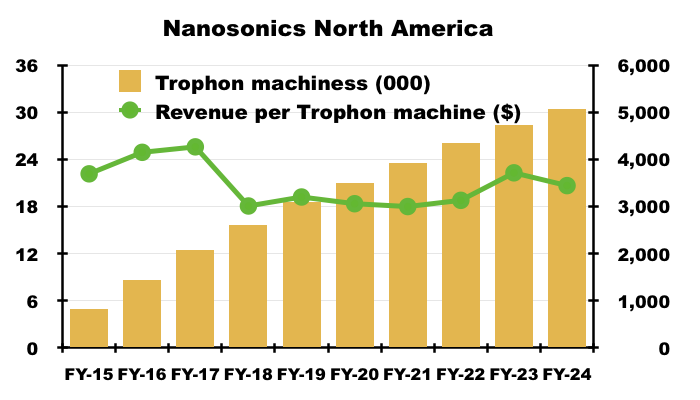

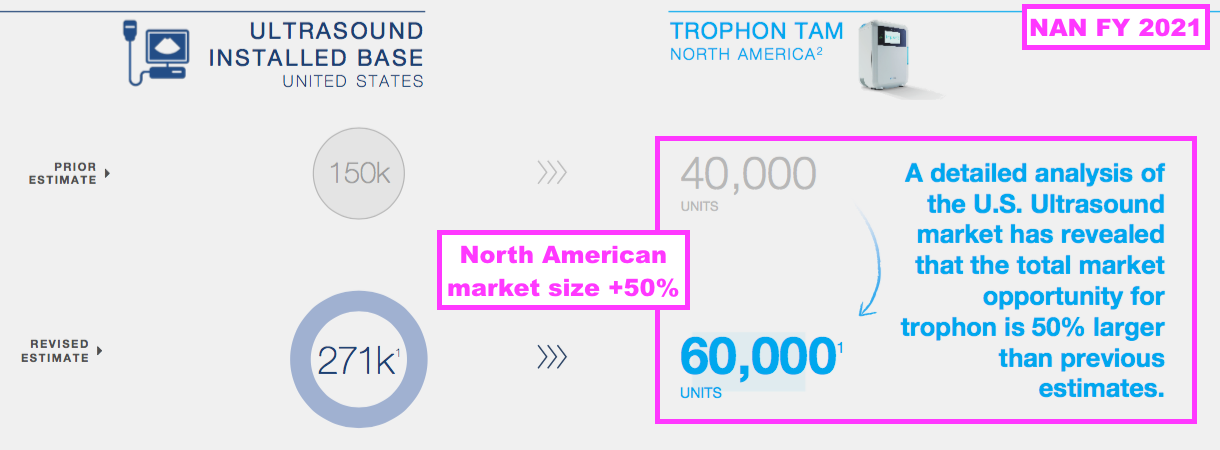

- The US benchmark for ultrasound-probe decontamination is set by Nanasonics (NAN), the quoted Australian group that manufactures the Trophon machine. Trophon machines are limited to cleaning ultrasound probes only:

- That TSTL slide above indicates 50% of ultrasound-probe disinfection procedures within the US are performed by a Trophon machine.

- NAN’s FY 2024 results disclosed revenue of AU$170m, of which AU$154m was earned within North America:

- AU$154m perhaps coincidentally translates to approximately $101m, which matches the aforementioned “$100m opportunity” for TSTL and Parker Labs.

- NAN’s FY 2024 results also confirmed 30,390 Trophons now operating in North America, which equates to revenue per Trophon machine of approximately $3,440:

- NAN increased the potential of its North American market from 40,000 to 60,000 Trophons during FY 2021:

- NAN’s theoretical market size for North American high-level ultrasound disinfection is therefore 60,000*$3.44k = $206m.

- This testimonial from an American urologist suggests TSTL’s early US customers may be using old-style cleaning techniques:

[Parker Labs website] “Our clinics switched from manual aldehydes to using Tristel ULT for [high-level disinfection] of our ultrasound probes.“

- The same testimonial noted the cost per disinfection using TSTL’s foam was “approximately $3“.

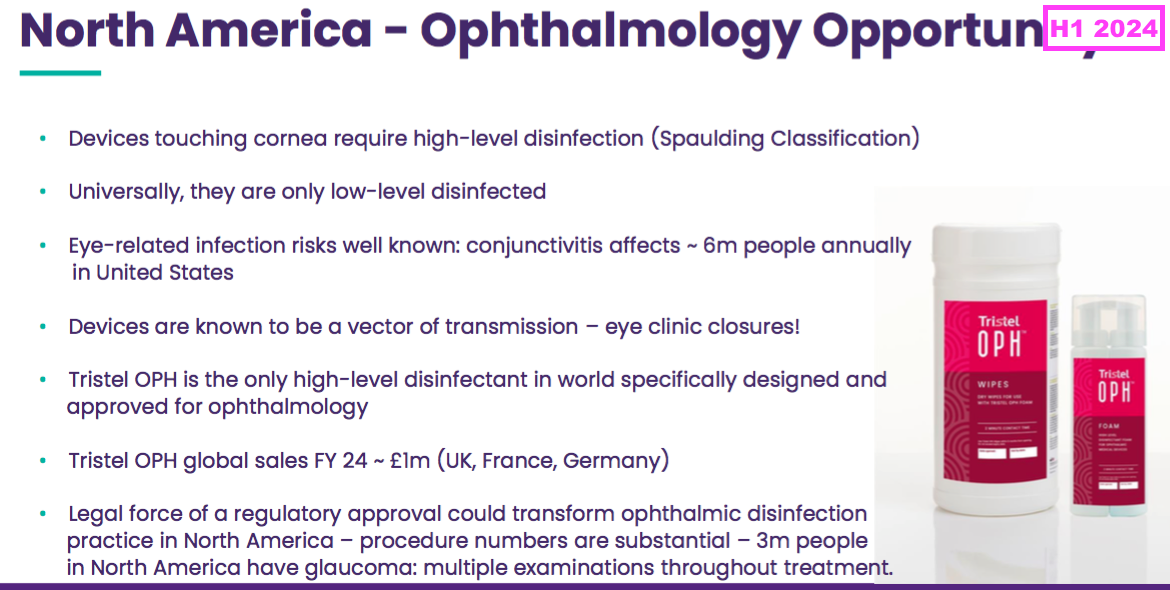

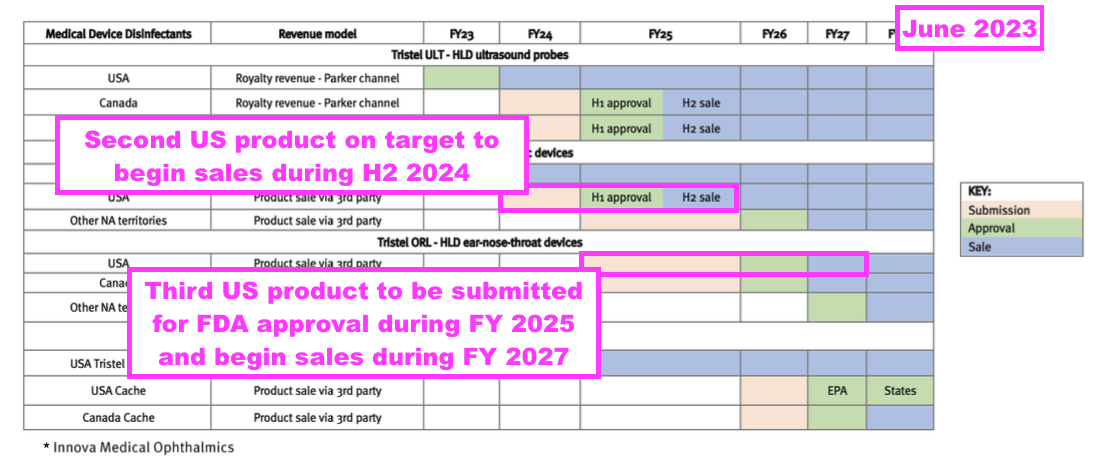

- This H1 outlined the North American potential for a second FDA-approved foam for ophthalmology devices:

- An RNS the other week confirmed TSTL had submitted the FDA application for the ophthalmology foam and an FDA verdict should be forthcoming before the end of December.

- The same RNS talked of the ophthalmology foam’s “potential to transform” a North American market with up to 16 million procedures requiring a high-level disinfection:

[RNS September 2024] “The Board believes that FDA clearance has the potential to transform ophthalmic disinfection practice in North America. According to the Spaulding classification, semi-critical devices require reprocessing with a HLD because they touch mucous membranes or non-intact skin, which is the case for nearly all ophthalmic devices. Very few semi-critical ophthalmic devices are subjected to an effective HLD in the US. Low-level disinfectant options such as alcohol wipes are used as an alternative, or devices may be soaked in sodium hypochlorite (bleach) or hydrogen peroxide in open trays with long contacts times.

Tristel OPH is the only HLD in the world designed specifically for ophthalmic devices and if 510(k) filing is successful it would become the only FDA cleared HLD, effective with short contact times and no requirement to soak devices in chemicals in an open tray, available for use in the c. 16m ophthalmic procedures that require HLD annually in the US, such as glaucoma diagnosis and cataract surgeries.”

- To date, TSTL’s ophthalmology foams have generated only a fraction of the revenue of ultrasound disinfectants within TSTL’s established markets:

- An FDA-approved ophthalmology foam may therefore enjoy only a fraction of the sales of the FDA-approved ultrasound foam in the US.

- Last year TSTL suggested its third FDA regulatory submission would occur during FY 2026 and involve the foam that disinfects devices examining ears, noses and throats:

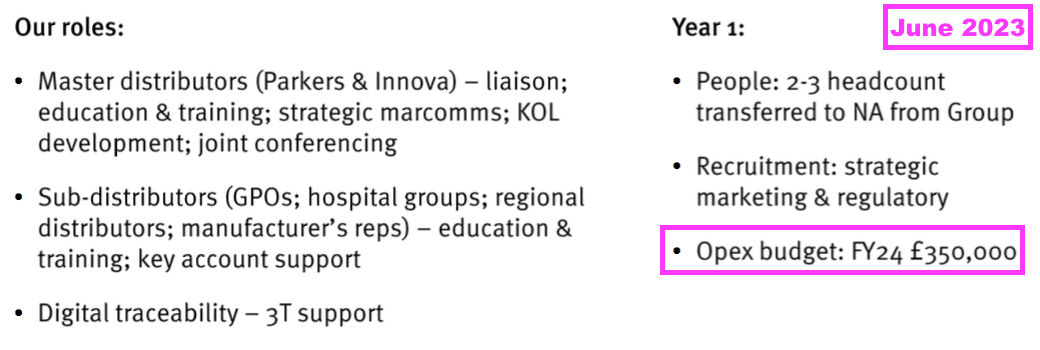

- TSTL did not refer to US operating costs within this H1, but did say the group was “establishing a Boston office and transferring two of its senior business developers to North America”.

- The comparable H1 had predicted North American operating costs of £350k for FY 2024:

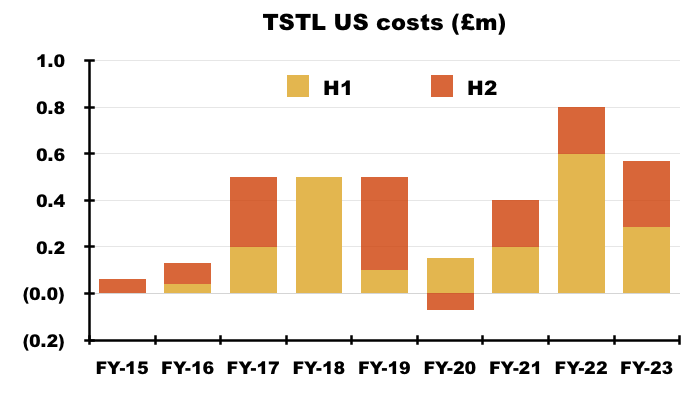

- I calculate TSTL’s aggregate US regulatory expenditure during the nine-year application process for the ultrasound foam to have been £3.5m:

- Only time will tell how large the 24% royalties will be and whether that £3.5m has been spent wisely.

- £3.5m is equivalent to only 1.5% of the aggregate £231m revenue reported during the nine-year FDA application process, and will become a worthwhile investment should US sales really take off.

Patents and competing technologies

- TSTL has regularly cited patents as part of the group’s competitive advantage:

[AR 2023]

“INTELLECTUAL PROPERTY PROTECTION

On 30 June 2023, we held 142 patents granted in 32 countries providing legal protection for our products.

In its broadest sense, our intellectual property relates to:

1. Patents, trademarks and registered designs

2. The scientific validation of our chemistry and our products that have entered the public domain, via a number of peer-reviewed and published papers

3. The certification by medical device manufacturers that our chemistry is compatible with their products. We enjoy official compatibility with the instrumentation of 56 medical device manufacturer, with respect to 1,449 of their individual models

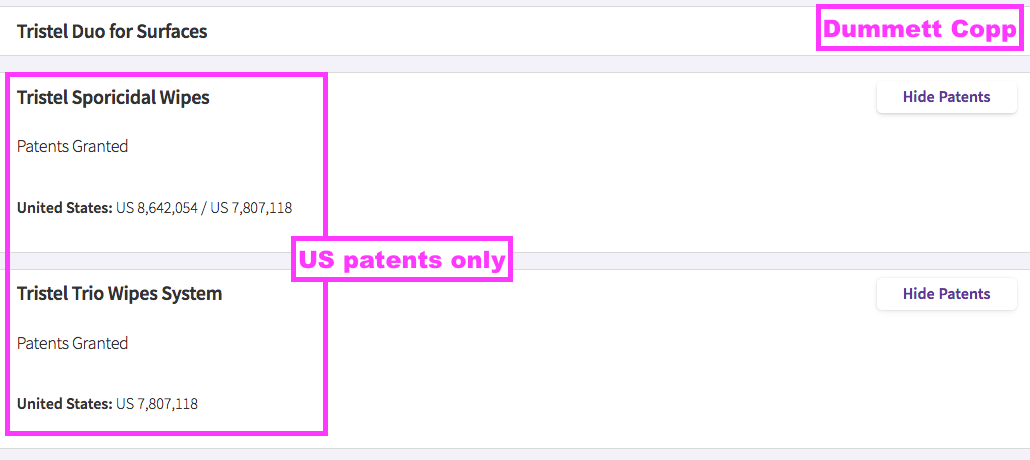

- TSTL’s UK and EU patents protecting the group’s Trio Wipes system expired after this H1.

- Google Patents shows the expiry dates were:

- UK: 07 May 2024 (GB 241 3765), and;

- EU: 26 July 2024 (EP 174 2672).

- TSTL’s patent attorney now shows only the US wipe patent in force…

- … which Google Patents says will expire on 11 January 2026.

- Google Patents shows the anticipated expiry dates of TSTL’s foam patents to be:

- UK: 27 January 2026 (GB 242 2545);

- EU: 27 January 2026 (EP 184 3795), and;

- US: 11 September 2030 (US 884 0847).

- The Q&A during the 2023 open day prompted extensive management remarks about patents and general intellectual-property protection, which concluded:

[Open day 2023] “Patents are quite important, but not at the top of the list of the protections we enjoy that help us with our competitive position.”

- Management’s preceding FY webinar repeated the same message, and confirmed the chemistry includes a “trade secret“:

[FY 2023] “Patenting is not the only IP protection that we have. The chemistry itself is protected by a trade secret within the formulation, something that only a handful of people have access to, and something that has never been reversed engineered.“

- My discussion with Bruce Green, the chemist who devised TSTL’s disinfectant chemistry, at the 2022 open day confirmed competitors were kept at bay through secret chemical ingredients and secret manufacturing processes.

- I note US manufacturing partner Parker Labs seemingly operates with very few patents, suggesting other competitive factors may be more important when supplying products to the US ultrasound market.

- Any impact from the aforementioned Trio Wipes patent expiries will be felt during FY 2025 and beyond.

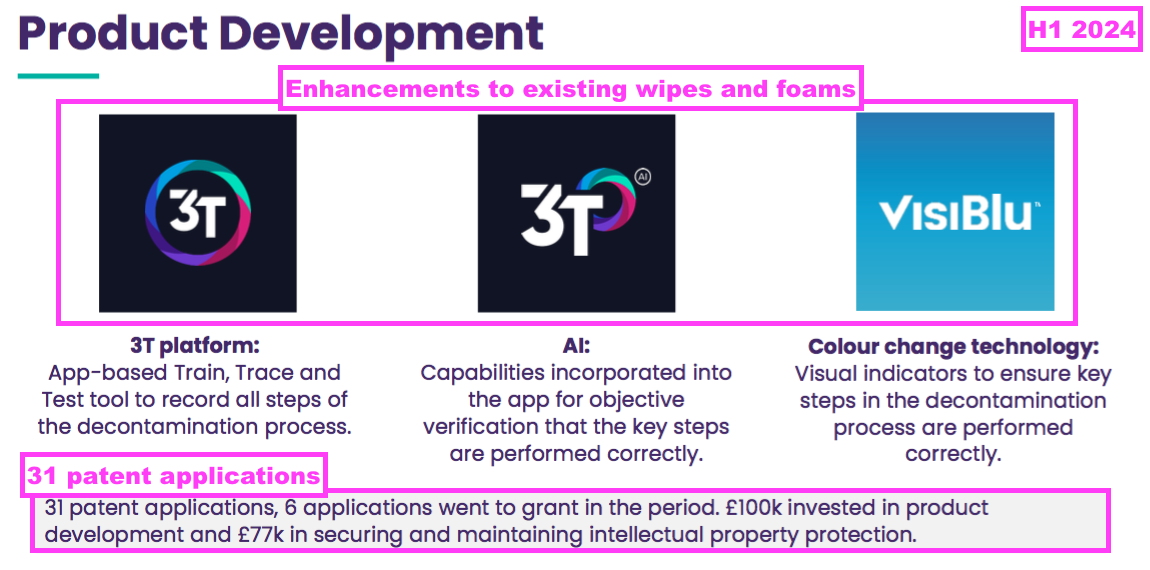

- This H1 recapped three product enhancements and claimed a further 31 patent applications:

- New text within the 2023 annual report (point 12c) did not suggest copycat disinfectants were a significant risk to TSTL. Instead the main three dangers were listed as:

[AR 2023]

“• Competing technologies

• Divergence by regulators away from chemical disinfectant products

• A shift in market acceptance of manual decontamination systems“

- TSTL may not face equivalent competition from other wipes and foams, but “competing technologies” include:

- Management’s H1 webinar appeared unconvinced about the decontamination qualities of UV light:

“[Chronos] is a UV-light box into which an ultrasound probe is placed. It’s available in some of the markets in which we operate and it is a competitor. Is it an equivalent disinfection process? That’s difficult to determine because there currently is not in place a standard evaluation methodology that’s designed specifically for UV light.

As a consequence, Germitec, which produces the Chronos machine, has adapted a chemical-decontamination standard and modified it to carry out the testing on its Chronos machine. There’s a big difference between using a chemical to decontaminate a device and using lights to decontaminate a device, and questions are being raised over whether the adaption Germitec has made to the standard is appropriate and whether customers can actually rely upon the data that has been created as a consequence.

Light is a new technology, and the market needs to catch up and the regulators need to catch up and put in place a form of assessing its effectiveness. Certainly Chronos is a competitor. Is it an equivalent? We have to wait until there’s proper data to demonstrate that its performance really is equivalent to chemical decontamination“

- The regulators — at least in the US — do not share TSTL’s scepticism of UV light…

- …because last month Germitec’s Chronos machine was approved for use by the FDA:

- TSTL will therefore compete with Trophon and Chronos in the US.

- Perhaps the development of new UV-light decontamination devices will amplify those other new TSTL risks:

[AR 2023]

“• Divergence by regulators away from chemical disinfectant products

• A shift in market acceptance of manual decontamination systems“

- NAN for instance has discredited manual disinfection to help promote its latest CORIS machine:

- Germitec has also denounced manual disinfection.

- The aforementioned testimonial from the US urologist now using TSTL’s foam contained a very limited argument for manual cleaning over automated cleaning:

[Parker Labs website]

“A CHOICE OF MANUAL VS. AUTOMATED HIGH-LEVEL DISINFECTION

When choosing between manual and automated HLD options, there is often concern manual disinfection is less effective, highly variable, and inherently more prone to human error. However, no studies have demonstrated manual application of Tristel ULT is less effective than automated systems. FDA clearance indicates the Tristel ULT is considered safe and effective for achieving HLD of ultrasound probes, eliminating this concern.”

Boardroom

- December’s AGM announced the retirement of TSTL’s chief executive:

[RNS December 2023]

“Paul Swinney, co-founder of the business in 1993 and Group CEO for the past thirty years, has informed the Board of his intention to retire within the next twelve months. Paul will continue in his post until a successor is appointed and has committed to remain available thereafter to support and advise the business in executing a successful transition in the leadership of the Group. The Board has, therefore, initiated a formal succession process, supported by the global organisational consulting firm The Coulter Partnership, that will consider both external and internal candidates.

The Group’s new CEO will join a strong executive leadership team with significant functional and market experience, gained from within and outside the business.”

- This H1 supplied a short update on the matter:

“CEO succession

At the time of our AGM in December, Paul Swinney, the Company’s founder and CEO of 30 years, announced his plans to retire in 2024 following a successful transition of leadership. A competitive selection programme is currently underway.“

- During management’s H1 webinar, TSTL’s PR handler frustratingly refused to raise shareholders’ questions about the chief executive’s retirement (“I shouldn’t be putting Paul on the spot to give reasons“).

- TSTL did not hold its usual open day during July, which also prevented shareholders asking questions about the chief executive’s retirement.

- Why the chief executive retired just as TSTL stands on the cusp of great progress in the States therefore remains a mystery.

- Credible bulletin-board talk by James188 on ADVFN suggested 30 years in charge had taken its toll:

[ADVFN July 2024]

“I was at the Tristel AGM last December and spoke to both Paul Swinney and Liz Dixon about Paul’s retirement decision, plus various other things. There was not the slightest hint that it was illness related and he looked in pretty good nick.

I think that the demands and stresses placed on a CEO at a fast growing company are sometimes underestimated. Those demands are certain to grow now that the US/Canadian business is taking off and the company is expanding in other parts of the world. I can understand why Paul is happy to go out on a high.“

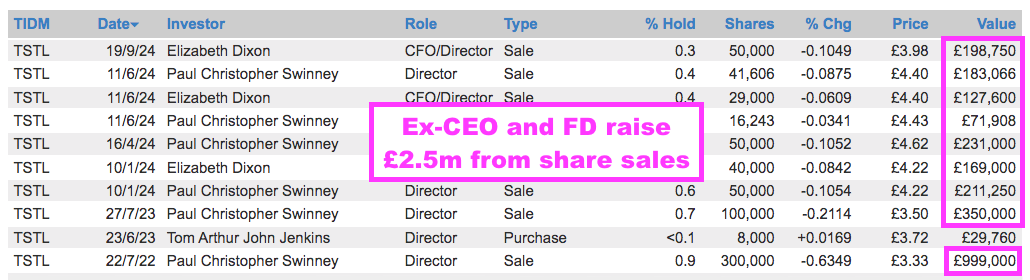

- TSTL’s former chief executive and current finance director are married (point 12f), have been selling shares (point 10e) and are probably both now thinking of life beyond TSTL:

- Matthew Sassone started as TSTL chief executive last month:

[RNS June 2024] “Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, announces the appointment of Matthew (“Matt”) Sassone as Chief Executive Officer (“CEO”) and to the Tristel Board, with effect from 2 September 2024.”

- On paper at least, Mr Sassone ticks a lot of boxes for marketing healthcare products in the US:

“Matt joins Tristel from Masimo Corporation (NASDAQ: MASI), a global medical technology company, where he is Senior Vice-President Marketing. During his tenure at Masimo, Matt lived and worked in the USA, gaining invaluable experience in the American healthcare market. He has over 27 years’ experience in the medical industry in various sales, marketing, business development and senior management roles. He joined the Board of AIM-listed cardiovascular monitoring company, LiDCO Group Plc (“LiDCO”), in June 2015, becoming CEO in August 2015. LiDCO was bought for £31m by Masimo in February 2021.

Matt started his career in sales for Quintiles in 1996. He spent 12 years at Smiths Medical in various sales, marketing and business development roles achieving the role of Managing Director, Northern and Eastern Europe and Russia in 2010 where he had full P&L responsibility for 300 employees and £150m of revenue. In 2012 he moved to ArjoHuntleigh, a division of the Getinge Group, as Senior Vice President Global Marketing and was Chief Marketing Officer of Maquet (turnover £1.1 billion in intensive care, surgery and anaesthesia systems), also a division of Getinge. Matt has a degree in biochemistry with microbiology, a diploma in management studies and a CIM diploma.”

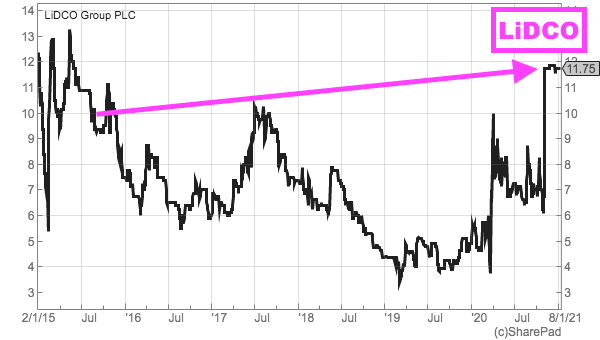

- Mr Sassone’s stint at AIM-quoted LiDCO — a manufacturer of blood-flow monitors for operating theatres and intensive care units — was not sparkling for shareholders.

- Between Mr Sassone’s appointment as LiDCO chief executive during August 2015 and the announcement of the recommended offer for LiDCO during November 2020:

- Annual revenue bobbed between £7m and £8m;

- Adjusted losses were recorded during FYs 2016, 2018, 2019 and 2020;

- An adjusted £60k profit was recorded for FY 2017, and;

- The shares started at 10p, fell to less than 4p, recovered to 6p before being acquired at 12p:

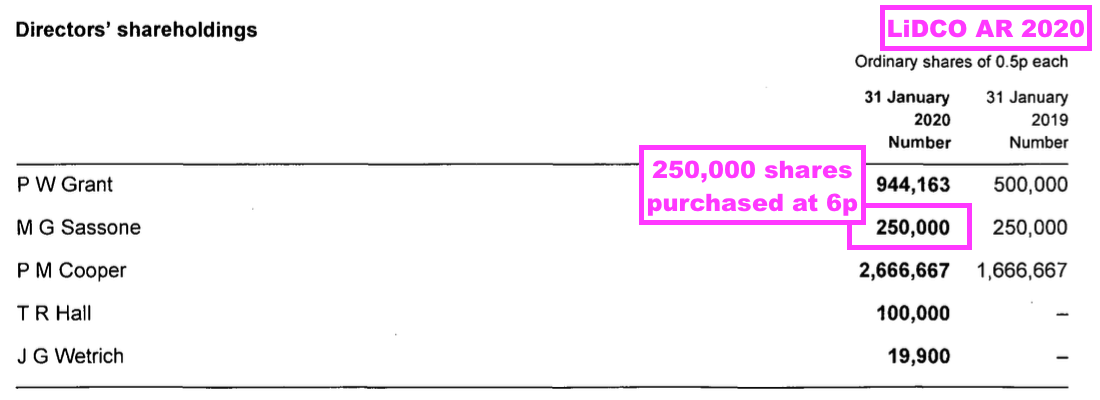

- During his LiDCO leadership, Mr Sassone spent only £15k to buy 250,000 LiDCO shares at 6p during an FY 2016 placing:

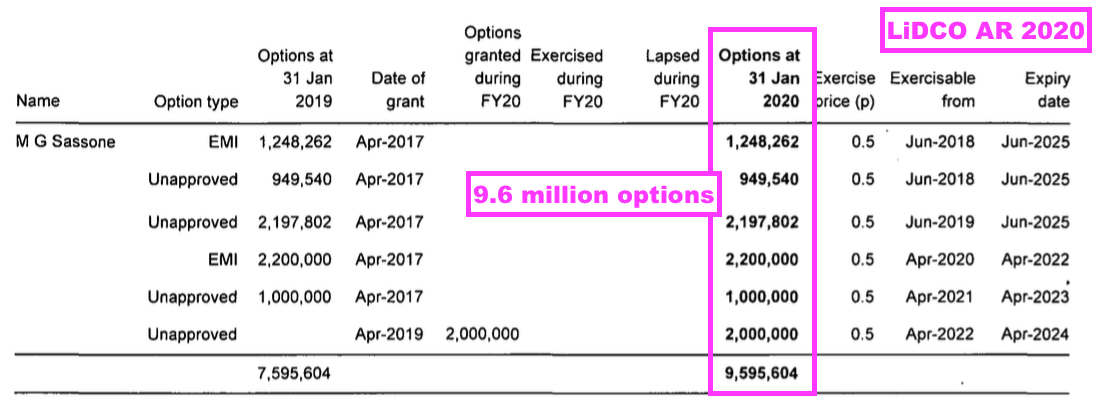

- But by FY 2020 Mr Sassone had also amassed 9.6 million LiDCO options:

- I must confess Mr Sassone’s talent for creating long-term shareholder value is not clear from LiDCO or the rest of his CV — although his willingness to sell LiDCO to a large US business is encouraging for TSTL investors.

- I would like to think TSTL’s established competitive position — underlined by the aforementioned significant presence of TSTL products within UK hospitals — means Mr Sassone does not have to work miracles for TSTL to prosper.

- Mr Sassone’s first encounter with TSTL shareholders will occur after publication of the FY 2024 results on 21 October.

- I trust Mr Sassone will then:

- Outline his strategic ambitions for the group;

- Reveal new three-year revenue growth and Ebitda-margin targets, and;

- Reiterate the policy to lift the annual dividend by a minimum 5% every year.

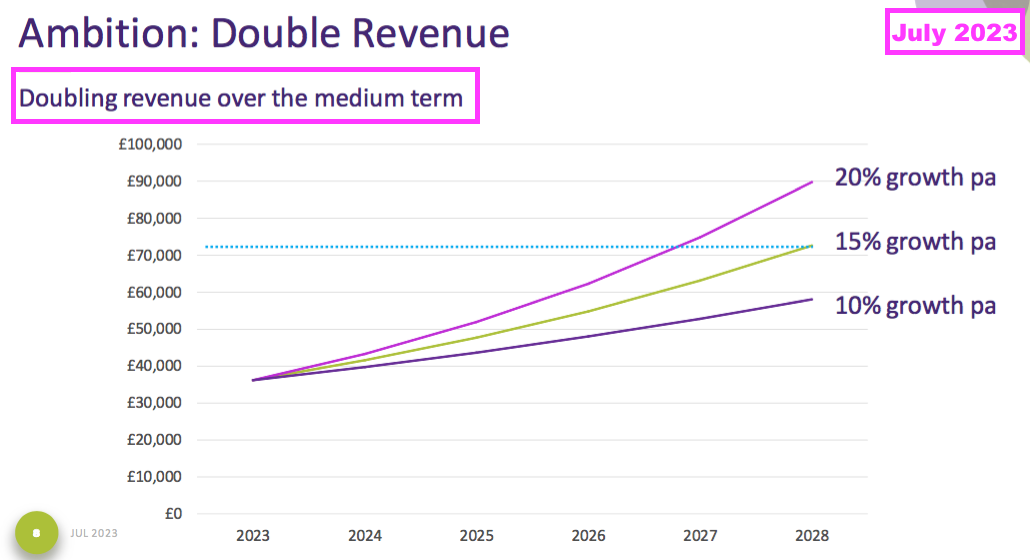

- TSTL’s previous chief executive set expectations high during the 2023 open day after presenting an ambition of “doubling revenue over the medium term“:

- Coinciding with the appointment of Mr Sassone, Bart Leemans — the former owner of the Belgian, Dutch and French distributors — has stepped down from the board but remains employed as MD of TSTL’s impressive French subsidiary.

- Mr Leemans sold his distributorships to TSTL during FY 2019 and took c950k TSTL shares (2%) as part payment — and has commendably never sold a share since (point 10e).

- As far as I am aware, during his time as a board executive, Mr Leemans has appeared at only one of TSTL’s six HQ open days and has never attended a private-investor presentation. I get the (welcome) impression Mr Leemans prioritises talking to customers over talking to shareholders.

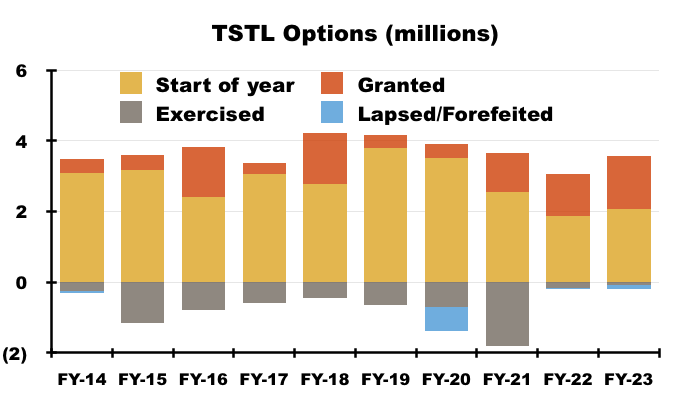

Share options

- Significant share-based payments have featured regularly within TSTL’s accounts.

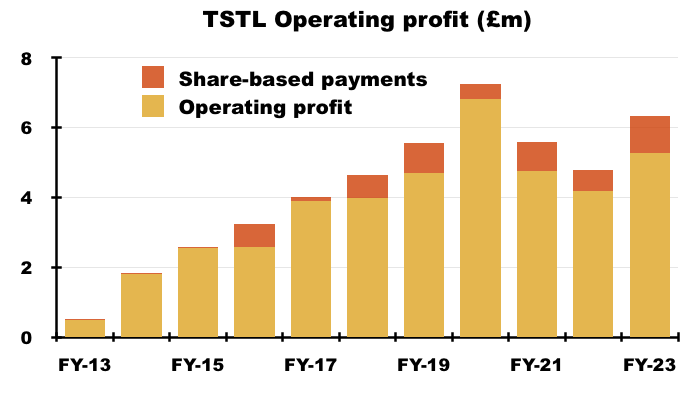

- Between FYs 2016 and 2023, share-based payments reduced the aggregate pre-exceptional operating profit by £5.2m, or 13%:

- This H1 witnessed share-based payments reduce operating profit by £691k, or 17%:

- TSTL presents an adjusted profit excluding share-based payments:

“The Board believes that these share schemes help to retain staff and link their interests to shareholders. The value of share-based payments is significantly influenced by the volatility of the Company’s share price, a factor that is out of the Board’s control. As consequence, profit and earnings are reported on both an adjusted basis, adding back share-based payments, alongside unadjusted, so that the underlying profitability of the Company can be understood.”

- One reason for adjusting for share-based payments is such charges can occur despite the options eventually becoming worthless.

- This H1 revealed an executive LTIP incurred a £0.2m cost:

“The share-based payment charge of £0.7m is derived from the Group’s All-Staff share option scheme which is based upon periodic share option grants to staff members (£0.5m), and the Executive Management LTIP scheme (£0.2m).”

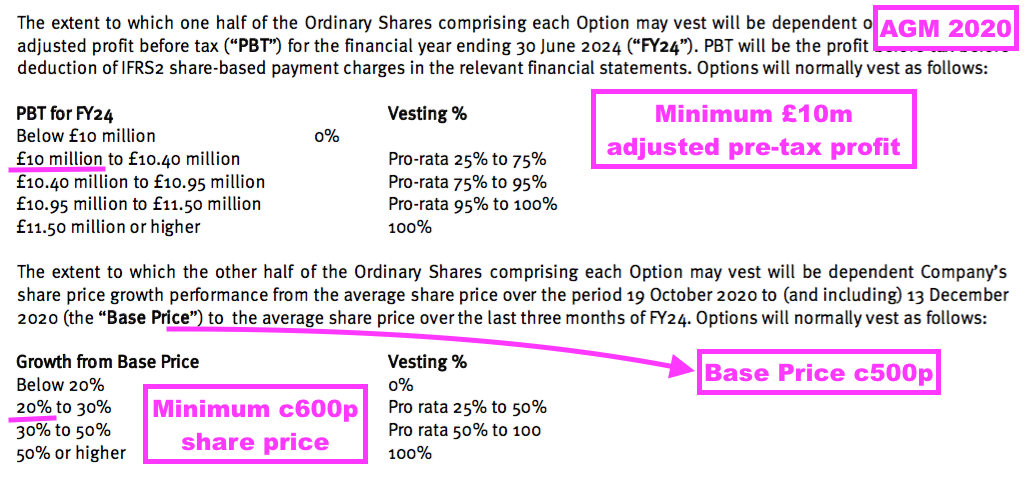

- The LTIP in question relates to 800k options that pay out if profit (before share-based payments!) reached £10m during FY 2024 or the share price traded at a c600p average during April/May/June 2024:

- The 800k options have now expired worthless, as:

- A post-H1 update (see Valuation) confirmed FY 2024 profit did not reach £10m, and;

- The share price did not trade anywhere near 600p during April/May/June 2024.

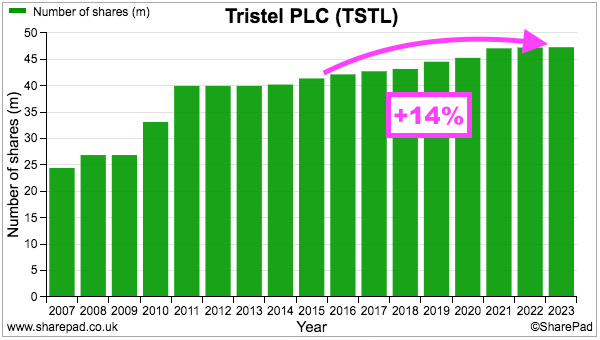

- The true long-term cost of options to ordinary shareholders is through permanent dilution and not accounting charges.

- TSTL’s share count has advanced 14% between the start of FY 2016 and the end of the preceding FY, with 12% due to options and 2% due to the purchase of the Belgian/Dutch/French distributor (see Boardroom):

- During the same period, the share price increased from 101p to 425p while the dividend increased from 2.72p to 10.5p per share. Outside shareholders were therefore still rewarded despite the dilution.

- I presume TSTL’s board is currently devising a new scheme to replace the now worthless LTIP.

- LTIP features for the remuneration committee to consider are:

- The demands of the new chief executive, who may require more than the 500,000 options the previous chief executive received;

- The LTIP’s financial targets (previously profit and share price), and whether they match the financial targets announced to shareholders (currently revenue growth and Ebitda margin), and;

- Whether the new LTIP will contravene the best practice of limiting option grants to 10% of the share count over ten years.

- On that final point, TSTL granted 6.9 million options during the ten years to the preceding FY…

- …which is equivalent to 17% of the share count at the start of that ten-year period (40 million).

- Following the 800k-option LTIP becoming worthless, I calculate TSTL now has 1,442k options outstanding equating to potential further dilution of 3.0%.

Financials: margin and employees

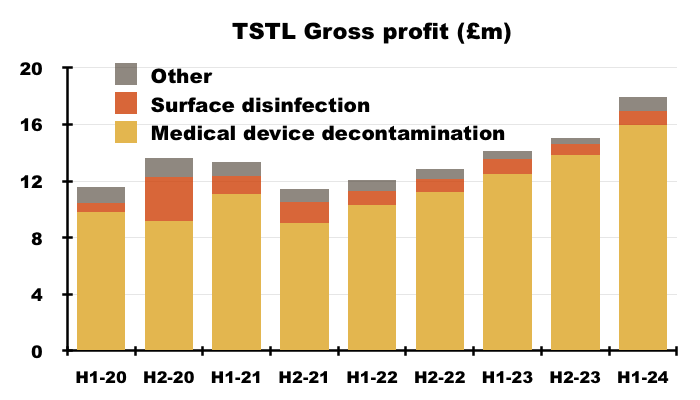

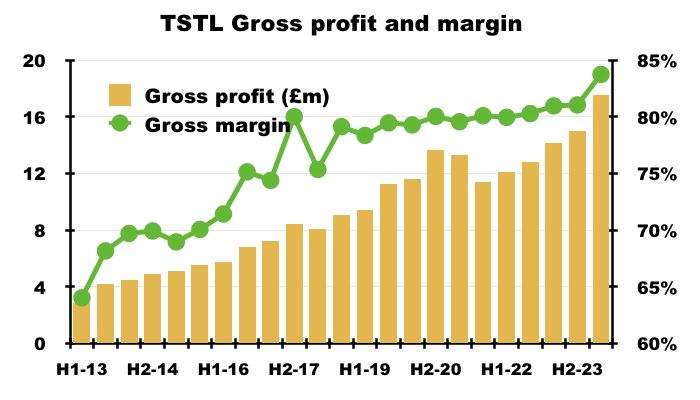

- A financial highlight from this H1 was the gross margin reaching a record 84%:

- An 84% gross margin is equivalent to buying stock for £16 and selling it for £100, and underlines how TSTL’s customers value the effectiveness of the group’s disinfection chemistry.

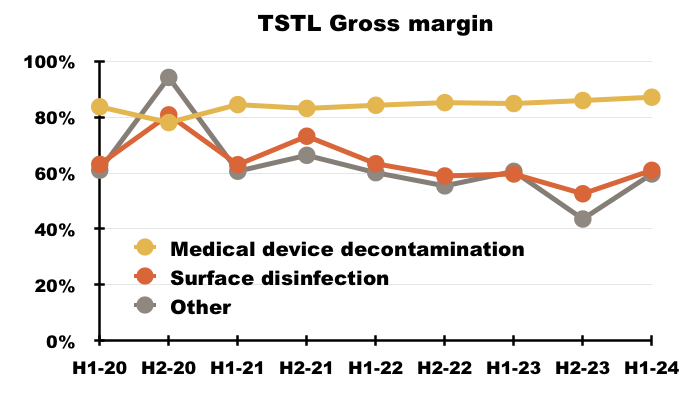

- The medical-device wipes and foams boasted an 87% gross margin during this H1:

- The 61% gross margin earned from the hospital-surface disinfectants remains relatively unimpressive, and suggests the new TANK product is needed to shore up that division’s profitability.

- Management’s H1 webinar revealed the higher gross margin was due to price increases:

“Within the six months there were price increases, which benefited revenue and benefited gross margins equally. We keep ahead of inflationary cost increases and non-inflationary cost increases.“

- Management’s H1 webinar also claimed gross margin reaching 90% was not within the group’s forecast.

- The 84% gross margin helped TSTL surpass its Ebitda target, which the preceding FY reiterated was at least 25%:

[AR 2023]

“1. Sales growth in the range of 10% to 15% per annum as an annual average over the three years

2. The achievement in each year of an EBITDA margin (excluding share-based payment charge) of at least 25%, and

3. To increase profit before tax (excluding share-based payments) year-on-year, independently of the other two targets”

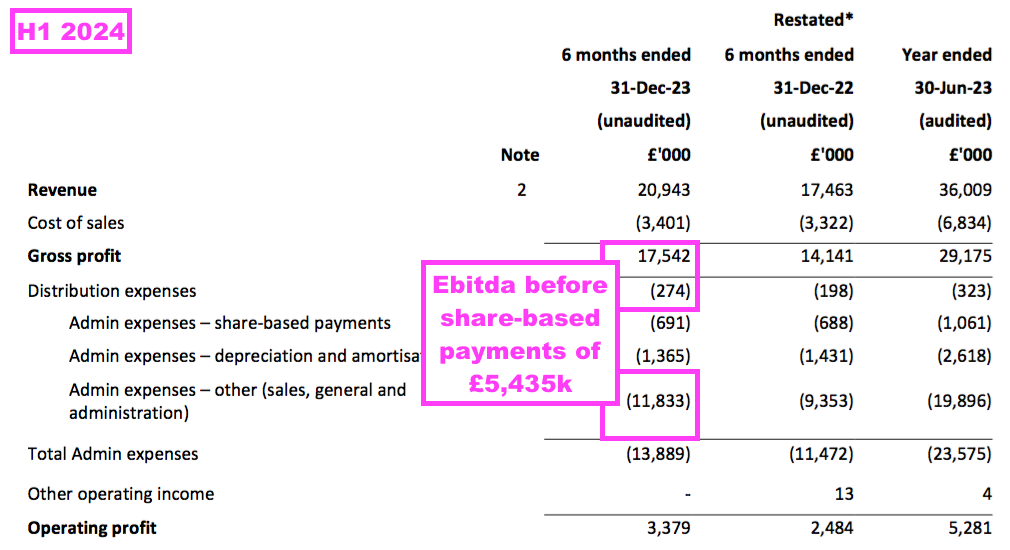

- This H1’s Ebitda (before share-based payments) was £5.4m to give an Ebitda margin of 26.0%:

- The H1 operating margin excluding share-based payments was a useful 19% versus 18% during the comparable H1:

- The record 84% gross margin ensured this H1’s operating margin excluding share-based payments could improve to 19% despite expenses increasing by 27%:

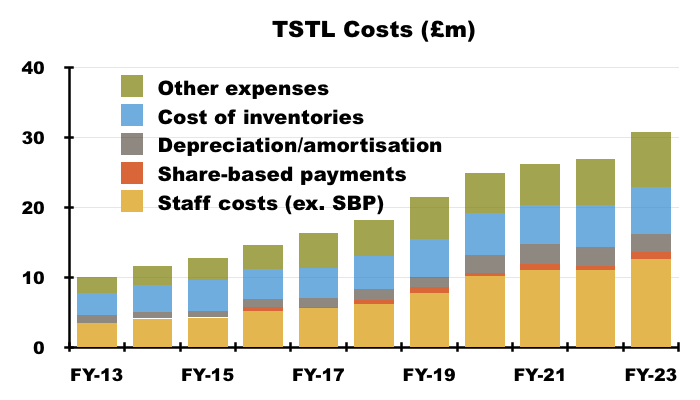

“Sales, general and administrative expenses were £11.9m (2022: £9.5m), a 27% increase. This cost growth is due to a combination of inflationary increases and the recruitment of an additional 27 staff into our sales, marketing and distribution areas. We implemented pay increases during 2023 to ensure our pay rates remain competitive and to secure staff retention. “

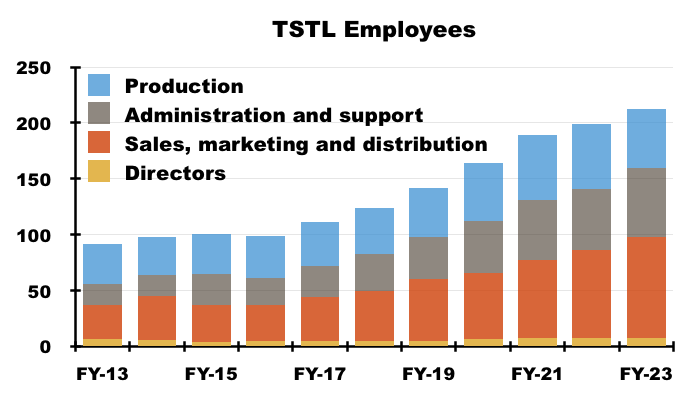

- The recruitment of 27 staff within sales, marketing and distribution is very notable given those departments employed an average of 90 people during the preceding FY:

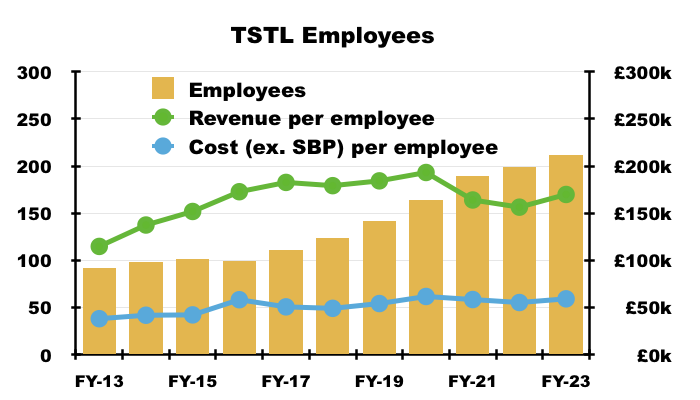

- Recent years have witnessed TSTL’s workforce productivity stagnate; for example, revenue per employee for the preceding FY matched that of FY 2016:

- Revenue per employee not advancing is disappointing, especially as the proportion of the workforce employed within sales, marketing and distribution represented 42% of the headcount during the preceding FY versus 33% during FY 2016.

- But management’s H1 webinar did offer the prospect of workforce productivity improving… assuming the sales team could sell surface disinfectants in much greater volume:

“The economy of scale that is available to us is that we aren’t creating a second salesforce to represent the Cache products within the hospital marketplace. They sell to the infection-prevention community worldwide and represent the Tristel product range to that community and now they can talk to the infection preventionists about surface disinfection as well with the same chemistry… So, double sales on the same cost base as is represented by that salesforce and that’s one very significant economy of scale”

- Flat-lining revenue per employee is not ideal when staff costs are increasing.

- Staff costs are TSTL’s largest expense, representing 35% of revenue during the preceding FY versus 30% or less between FYs 2014 and 2019:

- I am not convinced a higher gross margin will always be able to offset higher employee expenses if revenue per head does not improve.

Financials: balance sheet and cash flow

- The aforementioned £10.8m cash position included £6.0m cash deemed as “short-term investments” held within term-deposit accounts:

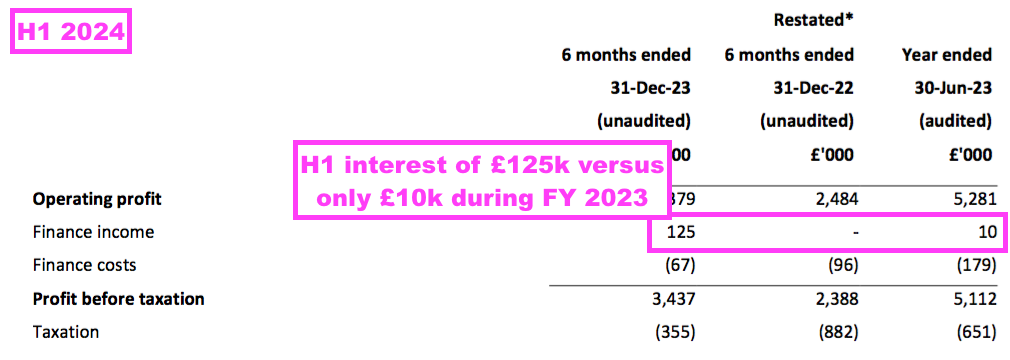

- Interest earned on the £10m or so held throughout this H1 was £125k, which suggests a c2.5% annual interest rate:

- £125k earned on the £6m held within term-deposit accounts suggests a useful 4% rate assuming the £4m balance collected no interest.

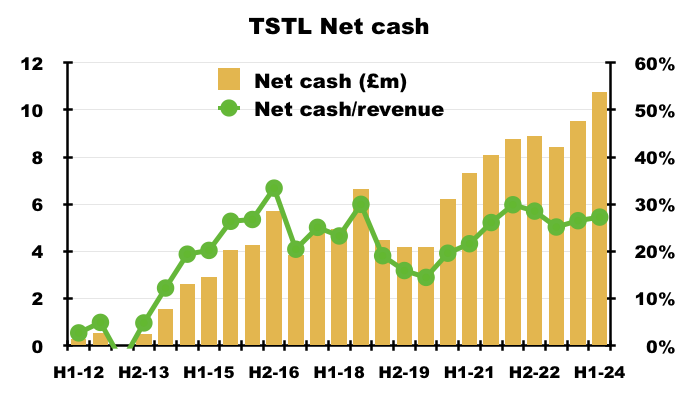

- TSTL’s accounts remain free of debt and H1 cash of £10.8m is equivalent to 27% of trailing twelve-month revenue of £39.5m:

- TSTL declared special dividends during FYs 2015, 2016 and 2022 when net cash reached approximately 30% of revenue.

- A post-H1 update revealed cash finishing FY 2024 at £11.6m — equivalent to nearly 28% of FY 2024 revenue of £41.9m (see Valuation).

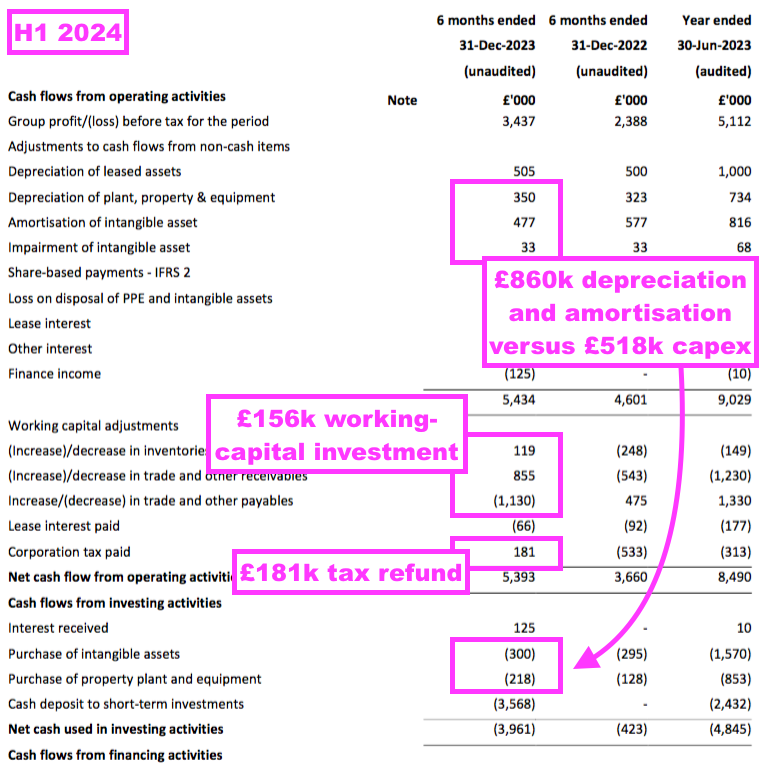

- Cash flow was very respectable during this H1, with adjusted earnings of £4.1m translating favourably into free cash of £4.6m.

- Welcome cash movements during this H1 included:

- Cash capex of just £518k versus depreciation and amortisation of £860k charged to the income statement;

- A working-capital investment of only £156k, and;

- A net £181k tax refund:

- TSTL’s balance sheet still implies the business remains an inherently capital-light operation.

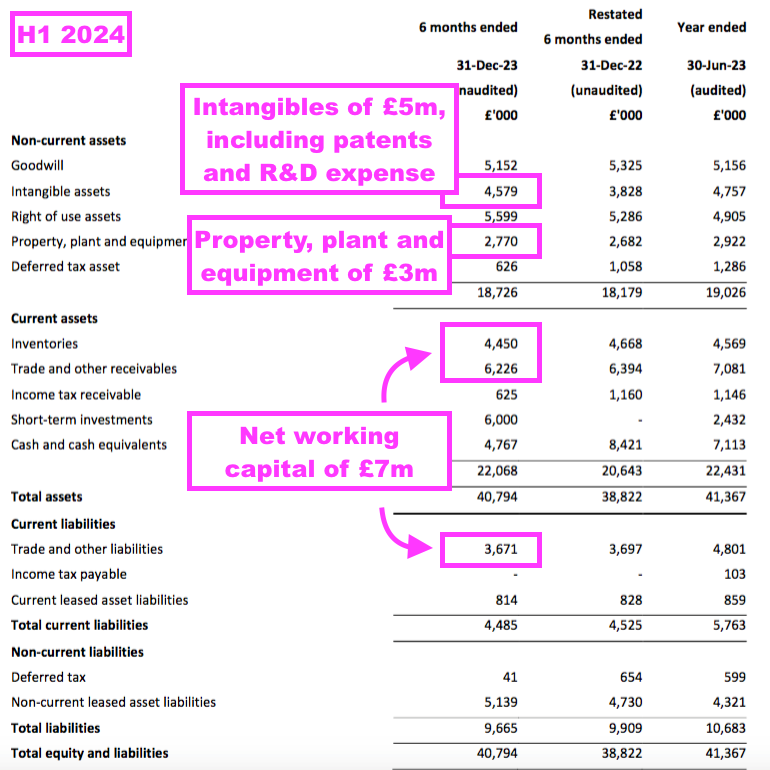

- Net assets of £31m less goodwill (£5m) and cash (£11m) leaves £15m, represented mostly by working capital (£7m), various intangibles (£5m) and property, plant and equipment (£3m):

- That £15m compares to an FY 2024 pre-tax profit (before share-based payments) of at least £8m (see Valuation), and implies TSTL may not need to reinvest significant amounts within the business to advance profit further.

- TSTL carries no final-salary pension obligations.

Valuation

- A post-H1 update during July summarised “a strong trading performance ahead of market expectations and the Company’s own performance targets”:

[RNS July 2024]

“• Revenues for the year were up 16.4% to £41.9m (FY 2023: £36.0m), ahead of market expectations and above the Company’s performance target for revenue growth (an annual average of 10-15% over three years).

• Adjusted profit before tax* will be no less than £8.0m, ahead of market expectations and 29% ahead of last year (FY 2023: £6.2m).

• Tristel continues to be debt free and cash generative. Cash balances on 30 June 2024 were £11.6m (30 June 2023: £9.5m).”

- H2 2024 revenue was therefore £21m — up 13% on H2 2023.

- If the 12% average price increase enjoyed during this H1 was experienced during H2 2024, then perhaps H2 2024 experienced only 1% volume growth.

- H2 revenue of £21m matched this H1’s revenue, as indeed did the H2 pre-tax profit before share payments of £4m match this H1’s pre-tax profit before share payments.

- FY 2024 cash up by £2.1m to £11.6m implies cash generation during FY 2024 was £8.7m after adding back £6.2m paid as dividends (13.1p*c47.6 million shares).

- Note: £6.2m paid as dividends equates to approximately 70% of that £8.7m cash generation, indicating TSTL is commendably returning a significant proportion of cash flow back to shareholders.

- The predicted pre-tax profit (before share payments) of £8m less standard 25% UK tax gives possible FY 2024 earnings of £6m or 12.6p per share.

- The 400p shares trade at 32x that 12.6p earnings calculation.

- Assume the new chief executive does indeed keep his predecessor’s ambition of “doubling revenue over the medium term“…

- … then perhaps FY 2029 might witness earnings double that 12.6p estimate at 25p per share.

- My valuation sums could be fine-tuned for margin improvements, lease costs, the cash position, option dilution and tax intricacies, but the 400p share price at 16x this 25p per share estimate — for FY 2029! — does not indicate an obvious bargain.

- My decision to purchase TSTL during 2013 and 2014 was made much easier because the 46p shares were then valued at a more modest c12x P/E multiple.

- TSTL’s elevated rating assumes:

- Very lucrative US royalties and significant progress within other new territories;

- Further meaningful growth from established products within established markets;

- Ongoing pricing power over customers (even the NHS), underpinned by a durable competitive advantage through secret chemistries;

- Attractive returns from TANK and other R&D projects. and;

- Stronger business acumen following the appointment of the new chief executive.

- But TSTL’s elevated rating may be overlooking:

- Enhanced competition from (now FDA-approved!) UV-disinfection machines, and a greater industry acceptance of automated disinfection generally;

- The unexplained retirement of the previous chief executive despite saying TSTL’s current prospects were the strongest for 30 years;

- Recent growth being supported mostly by price increases rather than higher volumes;

- Expansion in the US proving slow due to protracted customer “beta testing“, and;

- Weaker business acumen following the appointment of the new chief executive.

- As shareholders prepare to judge the new chief exec, the trailing 13.1p per share ordinary dividend supports a 3.3% income at 400p.

Maynard Paton

Another very good deep dive post, Maynard.

I am also looking forward to seeing if there are any changes in direction/acceleration when the company presents its preliminary results later this month. The share price has drifted on much not news recently, other than the share sale by Liz Dixon and the latest FDA filing for tonometers, plus the positive July TU.

On the NHS pricing, I remember that Liz Dixon explained back in February 2024 that NHS wanted pricing certainty and so TSTL front-loaded prices and will benefit now, but don’t expect price increases any time soon, although volumes may well increase. The UK is obviously becoming a decreasing part of the overall business.

As to Bart Leemans, my impression from talking to him a few times is that he is a very decent guy, but does not like the cut and thrust of public scrutiny. I am pleased that he is staying engaged in the business.

I have not seen you at the last couple of TSTL presentations, so maybe you will be able to ask your difficult questions at the next presentation later this month? I intend to be there. I am guessing that Paul Swinney will be sitting in the aisles.

Thanks Andrew. Yes, I have not attended the last few in-person presentations although the NHS snippet from the FD reminds me such events can provide much more info than the IMC online equivalents. I will endeavour to make the October event, if only to meet the new chief exec. Not sure he would want the old chief exec in the aisles, but let’s see!

Maynard