30 June 2024

By Maynard Paton

Happy Sunday! I trust the first half of 2024 has been positive for your shares.

A summary of my portfolio’s progress:

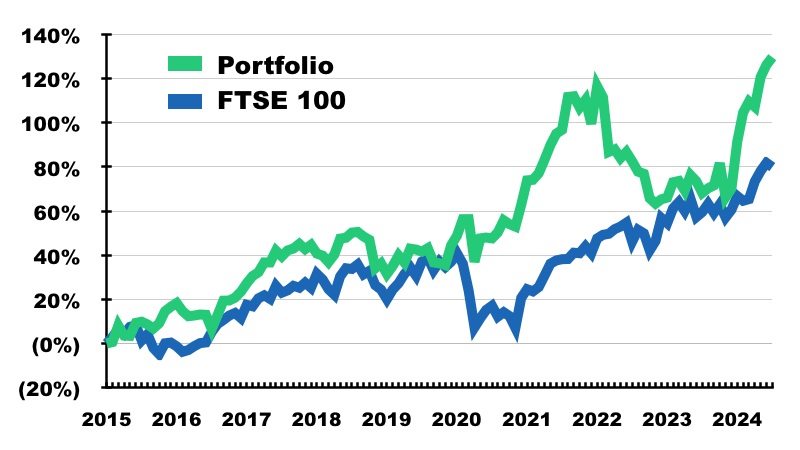

- Q2 return: +10.8%*

- Q2 trades: 3 top-ups (City of London Investment, Mountview Estates and S & U).

- YTD return: +20.0%*

- YTD winners/losers: 5 winners vs. 5 losers.

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees, paid dividends and cash interest)

This year has witnessed my best-ever H1 since I commenced this blog at the beginning of 2015. As I predicted within my 2023 review, System1 has dominated my returns and what was a large weighting has become even larger. April’s positive statement from the advert-testing specialist helped push my portfolio to new a record high.

My portfolio’s Q2 newsflow has also included some intriguing boardroom changes.

In particular, the odd management set-up at FW Thorpe has taken another twist: out go the roles of joint chief executives and in comes the combined role of chief executive and finance director! I hope to attend Thorpe’s AGM later this year to understand how this appointment was decided (in the meantime, more thoughts can be found here).

Elsewhere, Tristel has recruited its forthcoming new chief executive who, on paper at least, seems as if he could make a real go of the group’s United States potential. The outgoing chief exec is married to the current finance director, which I suspect/hope means a new finance director will be hired in due course.

Finally, M Winkworth has recruited two non-execs from corporate-finance consultancies with M&A knowledge. Could the estate-agent franchisor be soon erecting its own ‘for sale’ sign? Sector rivals Property Franchise and Belvoir recently merged and maybe Winkworth now feels susceptible to a bid.

In terms of share trading, my Q2 was relatively busy with no less than three different top-ups. I have summarised below what happened to my portfolio during April, May and June. (Read all of my previous quarterly round-ups). I will then explain how I have struggled to buy shares during market panics and prefer instead to buy after prices have flatlined for years.

Contents

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, FW Thorpe, Tristel and M Winkworth.

Q2 share trades

City of London Investment

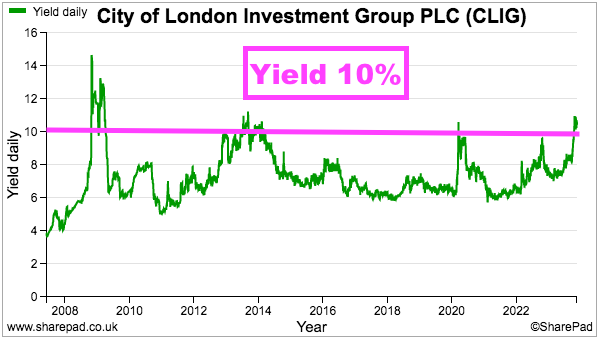

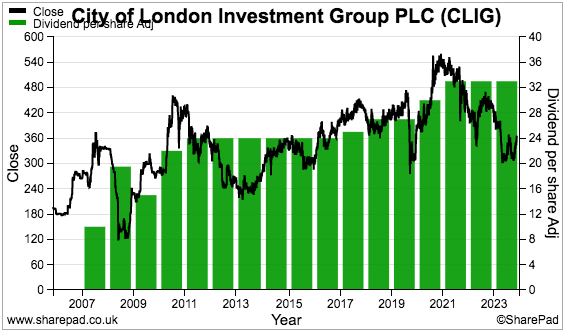

I have increased my City of London Investment (CLIG) position by approximately 20% at 332p including all costs.

The top-up was triggered by the fund manager’s Q3 2024 statement, which reported the group’s first net inflow of new client money since Q1 2023. Assisted also by favourable market movements, funds under management now top $10b for the first time since Q3 2022.

Whether the Q3 2024 statement marks a permanent change to CLIG’s fortunes is difficult to say. CLIG’s investment strategies have delivered relatively lacklustre returns over time, which persuaded clients to withdraw a net $249m from the group’s portfolios between FYs 2015 and 2023. Reduced fee rates have in turn put pressure on profit margins and dividend cover.

H1 results published during February showed client fees up 2%, underlying profit down 5% and trailing underlying earnings of 34p per share just about covering the 33p per share annual dividend.

At least FY 2025 ought to benefit from cost reductions and the closure of sub-scale funds, actions that seem triggered by 36% shareholder George Karpus.

Mr Karpus demanded a fresh board at last year’s AGM and I am hopeful his influence will in time help exploit what he describes as CLIG’s “enormous” potential. In particular, corporate cash-management services ought to generate new clients after CLIG itself enjoyed a useful 5% on its cash during H1. Other companies typically collect 3% or (much!) less.

My top-up should earn a 10% dividend yield while I await further intervention from Mr Karpus and/or a wider market rebound to lift funds under management and revive earnings. CLIG’s net cash of almost $26m should hopefully limit any short-term operational trouble. My latest CLIG review.

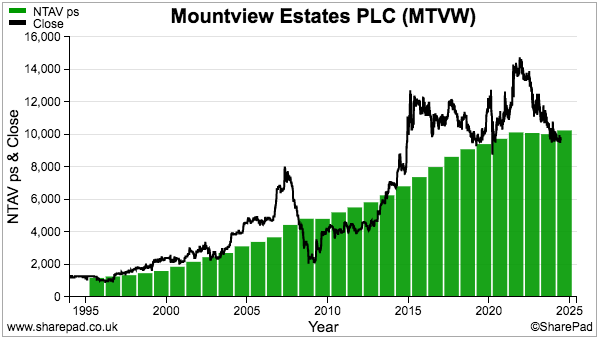

Mountview Estates

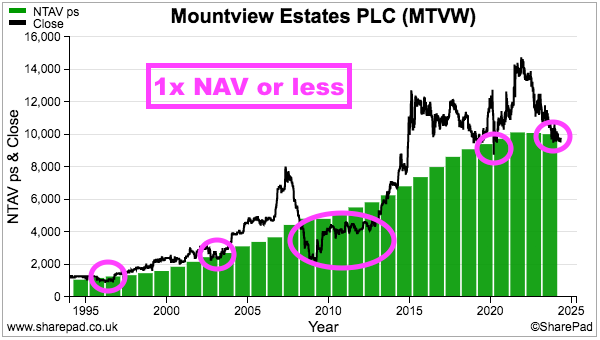

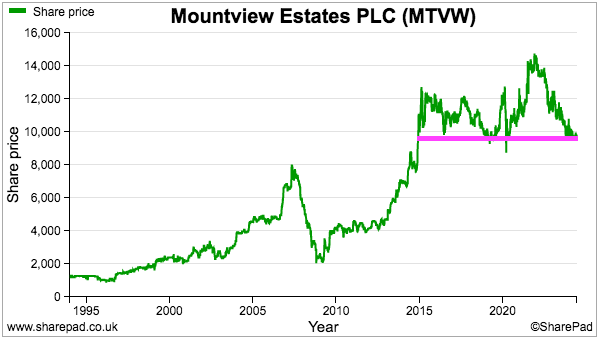

I have increased my Mountview Estates (MTVW) position by approximately 50% at £100 including all costs.

This purchase was prompted after reflecting on last year’s H1 results. The regulated-tenancy landlord is a very simple business with valuable property assets that ought to deliver a reliable shareholder income over the very long term.

My £100 buy price compares to a £102 per share net asset value that accounts for all properties at their original cost. I estimate if all MTVW’s properties ended their regulated-tenancy status today and were immediately sold at a fair market value, net asset value could be £189 per share. Investing at or below net asset value has tended to provide the best buying opportunities:

Still, MTVW is not without risk — in particular, the shares might be a ‘value trap’ because a 50% family concert party dictates proceedings and overlooks regular AGM protest votes. A growing worry is properties purchased during the last decade appear to have realised limited gains, which may explain why NAV growth has almost ground to a halt. The jury also remains out on the substantial spending on properties during the last two years.

I guess I have decided to trust MTVW’s veteran chief executive will look after all shareholders for the long run. He has, after all, lifted net asset value by 14x and the dividend by 45x since he took charge during 1990.

I speculate a trade sale could occur when the chief exec calls it a day, but that may be another decade away. Among those waiting is the chief exec’s sister, who — despite leading the protest votes against the board — has maintained a c15% shareholding since at least 1980. Both of us currently receive a 5% dividend income. My latest MTVW review.

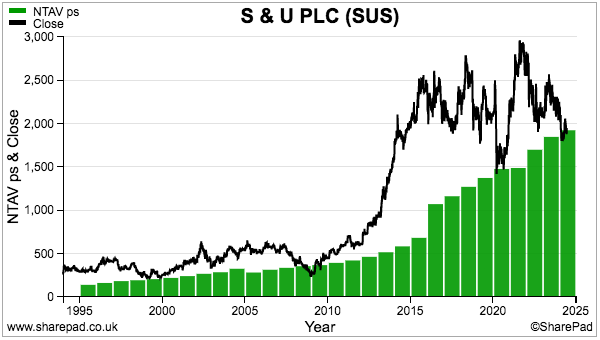

S & U

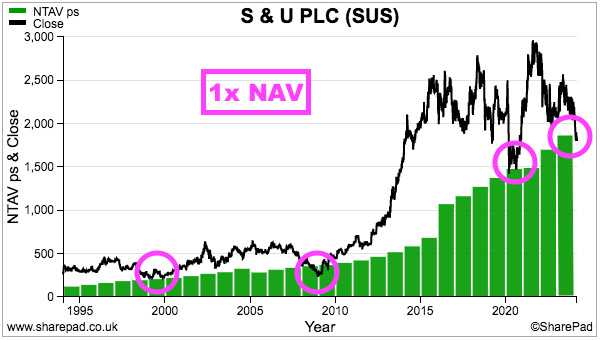

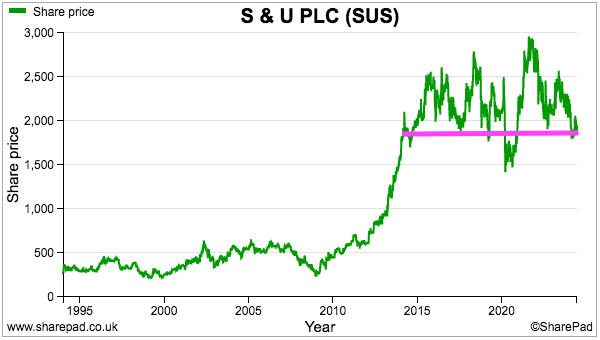

I have increased my S & U (SUS) position by approximately 50% at £18.62 including all costs.

My buying was encouraged by the share price declining to below the £19.27 per share net asset value reported within April’s FY 2024 results. Similar to MTVW, the best SUS buying opportunities tend to occur below book value:

SUS’s depressed rating naturally coincides with disappointing news. Those FY 2024 figures admitted H2 pre-tax profit had dropped 40% following an extra £10m impairment on suspected bad loans. An “upsurge” in regulatory activity persuaded the specialist lender to agree to “specific limitations on its repayment processes” as the wider sector acclimatised to the FCA’s new Consumer Duty regime.

Emphasising the seriousness of the new regulations, the final dividend was cut from 60p to 50p per share to leave the annual payout down 10%. Prior to the pandemic, SUS had never reduced its payout since at least 1987. The group’s AGM update then admitted Q1 profit had dived 35% as “temporary restrictions” caused collections from motor-loan customers to drop from 92% to 88%.

I suspect Consumer Duty will dampen the economics of all consumer-finance businesses, although I am hopeful the greater regulation can be mitigated somewhat by reduced competition. SUS successfully navigated the 2008 banking crash and, during the next few years, then recorded its best returns on capital because of fewer rivals. Unlike many of its competitors, SUS is not burdened with paying discretionary-commission compensation.

Much will depend on SUS’s seasoned executives, who reassuringly have worked at the group since the mid-1970s and have a 44%-plus family shareholding at risk. I hope to collect a 6% dividend income as Consumer Duty plays out. My latest SUS review.

Q2 portfolio news

As usual I have kept watch on all of my holdings. The Q2 developments are summarised below:

- Andrews Sykes: FY profit up 6% despite less favourable weather leading to FY revenue declining 5%.

- Bioventix: Nothing of significance.

- City of London Investment: Q3 2024 funds under management up 5% following the first net inflow of new client money ($224m) since Q1 2023.

- Mincon: A Q1 2024 admission of a “difficult start to the year“ albeit with order books recovering into Q2 and a “root and branch review” still ongoing.

- Mountview Estates: FY 2024 figures that showed the annual dividend up 5% and net asset value up 2%.

- S & U: Greater impairments and interest costs pushing H2 2024 pre-tax profit down 41% followed by Q1 2025 profit declining 35%.

- System1: Q4 platform revenue up 37%, a forthcoming dividend reappearance and an FY 2024 profit upgrade to £2.8m.

- FW Thorpe: A peculiar management change that sees one of the group’s joint chief executives become the full-time chief executive while remaining as finance director.

- Tristel: A less concerning management change that sees a senior marketing manager from $7b Nasdaq-quoted Masimo becoming chief executive.

- M Winkworth: FY 2023 profit down 25% but the Q1 2024 dividend up 3% and intriguing non-executive appointments.

Q2 portfolio returns

The chart below compares my portfolio’s monthly progress to that of the FTSE 100 total return index:

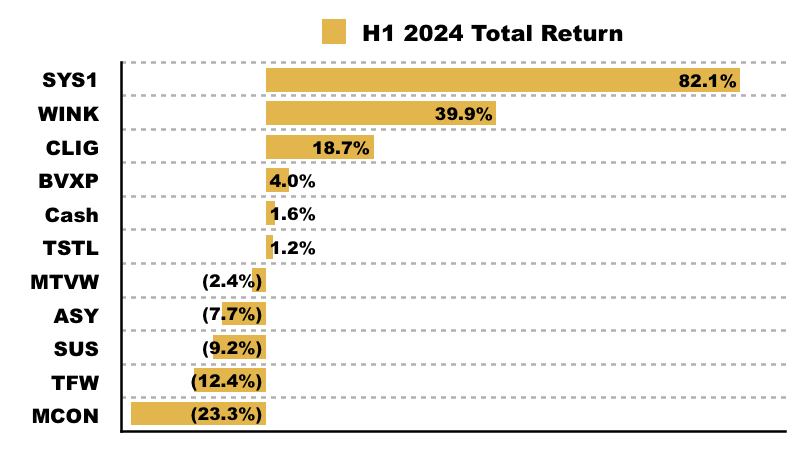

The next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me so far this year:

This chart shows each holding’s contribution towards my 20.0% YTD gain:

And this chart shows my portfolio’s holdings and their weightings at the end of H1:

‘When it’s drizzling gold, reach for a bowl‘

Warren Buffett once said:

“When it’s raining gold, reach for a bucket not a thimble.”

Easy to say, not so easy to do. Especially if you, like me, are not an investing genius.

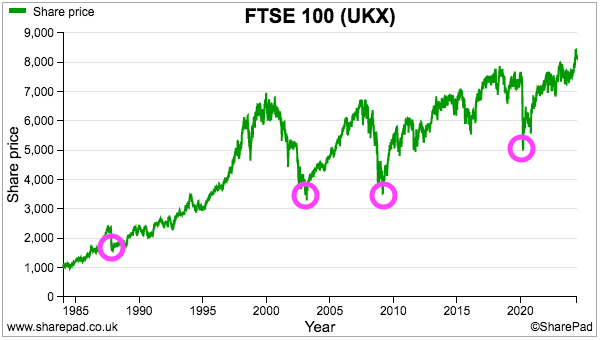

When you should have bought

I am sure you have looked at many share-price charts and wished you had bought at the bottom. The FTSE 100 index for example was established 40 years ago and has suffered four distinct crashes:

- 1987 Black Monday crash;

- 2000-2003 Dotcom crash;

- 2007-2009 Banking crash, and;

- 2020 Pandemic crash.

I wished I had bought at the bottom of those crashes. I was too young to be dabbling with shares during 1987, but I do remember the other three opportunities when the market was “raining gold” at the lows.

- Dotcom bottom: I recall being very bullish at the time, but had already bought all the way down and was fully invested when the absolute bargains emerged just before the sudden recovery.

- Banking bottom: A very scary time, when during October 2008 I wondered if my NatWest savings were going under… just before the government rescue arrived. By luck, ‘life events’ had persuaded me to sell 99% of my shares during the autumn of 2007 and I did not re-enter the market until 2011.

- Pandemic bottom: Another very scary time. From my Q1 2020 portfolio review:

“The country faces a national emergency. Lives are at risk, supermarkets have empty shelves, jobs are being lost…and the finer points of individual shares no longer seem that important.“

…

“A mix of complacency and illiquidity kept me invested as the turmoil began, and I have simply held tight onto all but one of my shares.“

I was certainly not buying.

Not reaching for a thimble let alone a bucket

My lack of buying at raining-gold bottoms probably reflects the realities of most private investors. I was either already fully invested, distracted by something beyond investing or simply too overwhelmed by the bad news to act.

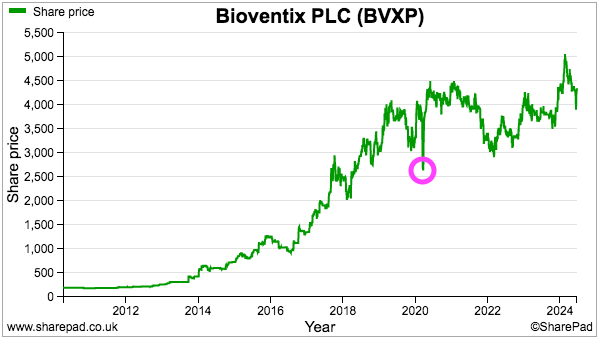

The pandemic crash in particular reminded me I am not cut out to buy amid deep market panics. Looking back I could have purchased Bioventix as low as £26:

I had the cash ready to invest, I knew Bioventix was a quality operator and I suspected the business would not suffer greatly during Covid. But I just could not summon the courage to buy during the uncertainty.

Mind you, my regret with Bioventix is counterbalanced by comfort from the pandemic plunges at some of my other shares.

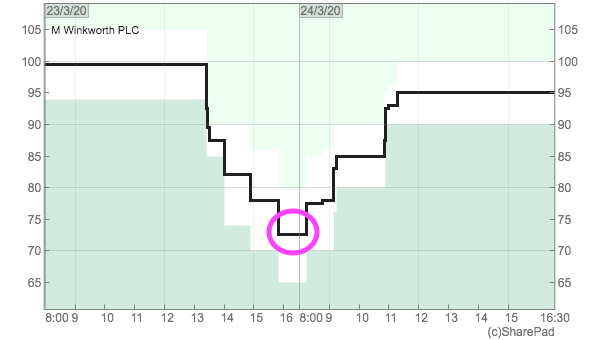

M Winkworth for instance dropped to a closing low of 72p:

But that price was available for less than one hour:

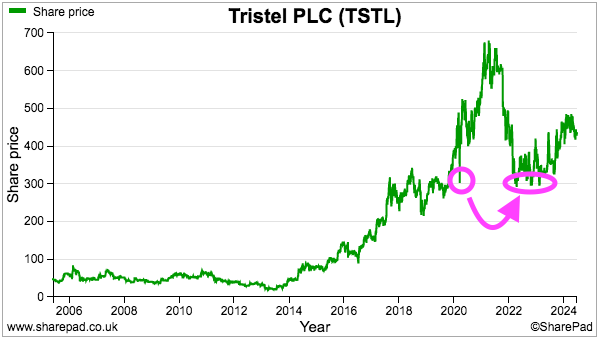

Tristel dropped to a closing low of 302p:

But that price would then reappear multiple times during 2022.

And Mincon fell to 73p:

But the shares currently trade below 50p.

As with numerous aspects of the stock market, looking back at price charts and thinking ‘what could have been’ is skewed by hindsight. We always rue what turn out to be great buying opportunities…

…but conveniently forget all the ‘bargains’ we did not buy that did not perform very well.

Ten years of flat returns

My three recent purchases are good examples of how I prefer to invest. Rather than trying to buy during market panics, I like to purchase after other investors have gradually given up on the companies in question.

City of London Investment, Mountview Estates and S & U each have share prices that have essentially flatlined for approximately ten years or more:

For various reasons, the stock market has grown increasingly despondent of the trio’s prospects. The price charts are not exactly encouraging for future outperformance.

But the three businesses have improved over time. During the last decade, City of London has lifted is dividend by almost 40%, net asset value at Mountview Estates has advanced nearly 40% while net asset value at S & U has more than tripled:

With hindsight, the market over-priced the three companies ten years ago and the shares have slowly de-rated to what I believe are now attractive valuations.

Mind you, my ‘attractive valuations’ may not be the raining-gold bargains that would prompt Mr Buffett to reach for a bucket. Around the bottom of the 2008/9 banking crash, City of London Investment offered a 15% dividend yield (now 10%), Mountview Estates traded at more than 50% below net asset value (now c2% below) while S & U traded at approximately 30% below net asset value (now c4% below).

Such raining-gold valuations may of course never re-occur. And if they do re-occur, they may be a very long time coming. That FTSE 100 chart shows four crashes over 40 years — an average of one every ten years. I could not wait in cash for ten years for the market to hit rock bottom before piling in.

From drizzle to downpour?

Only time will tell whether I was right to buy City of London Investment, Mountview Estates and S & U during this Q2… or to have instead awaited a true raining-gold opportunity. Maybe the three shares were only drizzling gold. But I am confident there was at least some precipitation.

Another question is whether my latest top-ups were bucket-sized or thimble-sized. I would probably describe them as bowl-sized, although my 13% cash weighting before the purchases were conducted was always going to limit the amount I could invest.

All three shares have now each become 8-9% of my portfolio, and therefore ought to have some impact on my overall returns. Will I buy more if the ongoing drizzle of gold turns into a sudden downpour? I would love to think so… despite my track record clearly saying I won’t!

Until next time, I wish you safe and healthy investing.

Maynard Paton

The new govt will I feel, insist on minimum energy ratings for new and current rental property. This could impact on Mountview’s profit, as they may be forced to significantly upgrade most of their housing stock in a very short period of time.

Hi Richard,

I must admit I have not checked Labour’s manifesto on this matter. I suppose many landlords would pass on the extra cost to renters, which may not be politically palatable. The government scrapped plans to tighten the minimum rental EPC rating last year, and apparently said:

“…under current plans, some property owners would’ve been forced to make expensive upgrades in just two years’ time. For a semi-detached house in Salisbury, you could be looking at a bill of £8,000. And even if you’re only renting, you’ll more than likely see some of that passed on in higher rents. That’s just wrong. So those plans will be scrapped…”

Maynard

In whatever form legislation is passed, it will likely be done on a gentle basis over several years as not to cause a sudden shock to the sector.

Many of Mountview’s properties have regulated tenants. They are there for life. Their rent is set by a rent officer, not Mountview. The rent officer decides what is a fair rent, and does NOT take other comparable property rents or economic conditions into consideration. Therefore this is an additional cost not factored in by Mountview, that cannot be recovered by raising the rent. Oh, and it wont be introduced on a gentle basis. Like the promised immediate abolition of section 21, the consequences have not been really thought about.

Hi Richard,

Agreed, MTVW will not be able to pass on the extra cost of tighter EPC regulation by simply raising the rent. The main issue is whether tighter EPC regulation will in fact be implemented at all. Many other landlords will simply pass on the extra cost to the tenant, which was not politically palatable for the Conservatives last year. I don’t know whether a new Labour government plans to revive the tighter EPC regulation.

Maynard