24 June 2023

By Maynard Paton

FY 2022 results summary for Mincon (MCON):

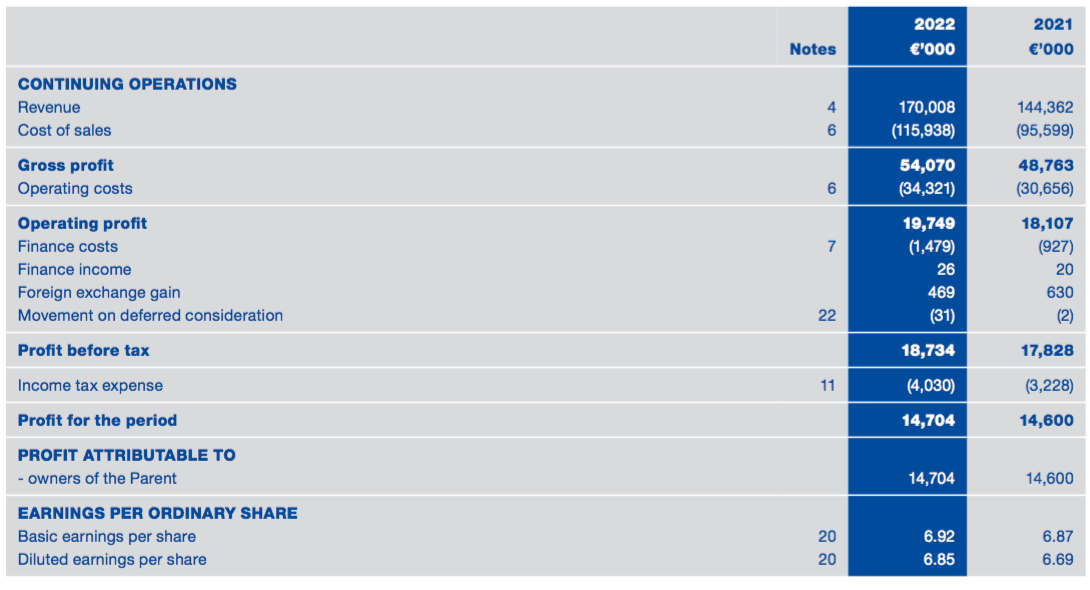

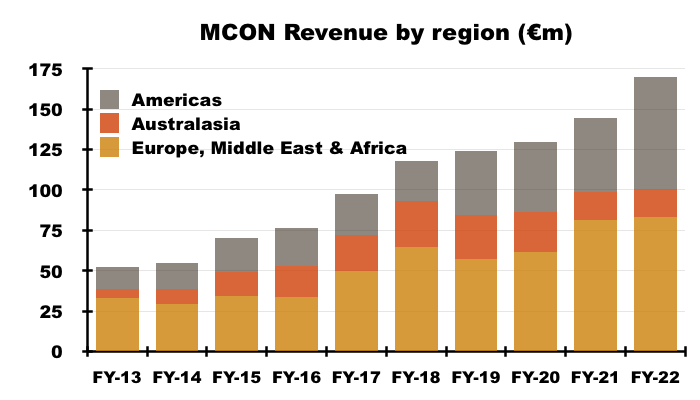

- A positive performance buoyed by healthy post-pandemic orders, showing revenue up 18% (to €170m) and profit up 9% (to €20m) to set new FY records.

- Bumper construction income, greater direct sales and increased US revenue counterbalanced weaker mining activity in Europe and Australia.

- Rig problems have beset early revenue from the “transformational” Greenhammer system, which management now believes has a 15-year useful life.

- A €14m working-capital investment pushed stock levels to a huge €77m, squeezed free cash flow to only €2m and raised questions about the debt-funded dividend.

- MCON’s “superior technical and innovative technology” is still to translate into superior financials, with obvious evidence of smart capital-allocation decisions remaining elusive. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own MCON

- Results summary

- Revenue, profit and dividend

- Sector divisions

- Greenhammer

- Subsea drilling and large-diameter hammer drilling

- Financials: Margin

- Financials: Stock

- Financials: Cash flow and net debt

- Financials: Return on equity and revenue per employee

- Valuation

News links, share data and disclosure

News: Annual results and presentation for the twelve months to 31 December 2022 published 13 March 2023 and Q1 trading update published 09 May 2023.

Share price: 90p

Share count: 212,472,413

Market capitalisation: £191m

Disclosure: Maynard owns shares in Mincon. This blog post contains SharePad affiliate links.

Why I own MCON

- Designs and manufactures industrial drills, with sales supported by established reputation, engineering excellence, technical innovation and first-class service.

- Boasts veteran family management with 46-year tenure, 56%/£108m shareholding and very long-term perspective.

- Offers higher earnings potential through increased construction-related revenue, further direct sales, greater US custom plus “transformational” new products.

Further reading: My MCON Buy report | All my MCON posts | MCON website

Results summary

Revenue, profit and dividend

- H1 revenue up 27% and H1 profit up 18% followed by an upbeat November Q3 trading update…

“The very strong revenue growth reported in the Group’s half year results to 30 June 2022 has continued in the past quarter, and revenues for the first nine months are 25% ahead of 2021. Our revenue growth has been mostly organic, supported by currency tailwinds, price increases and some contribution from acquisitions.”

- …had already indicated this FY 2022 statement would unveil positive progress.

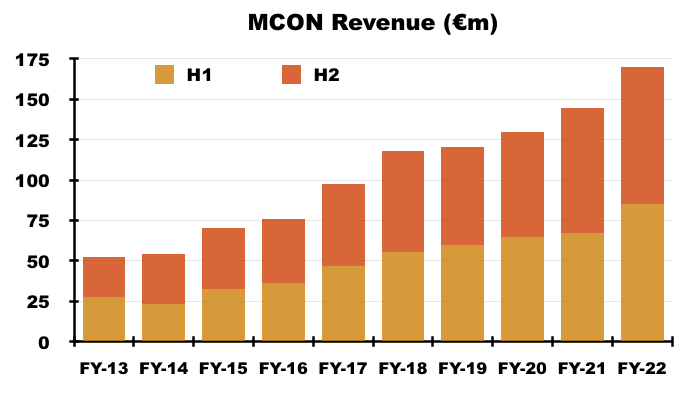

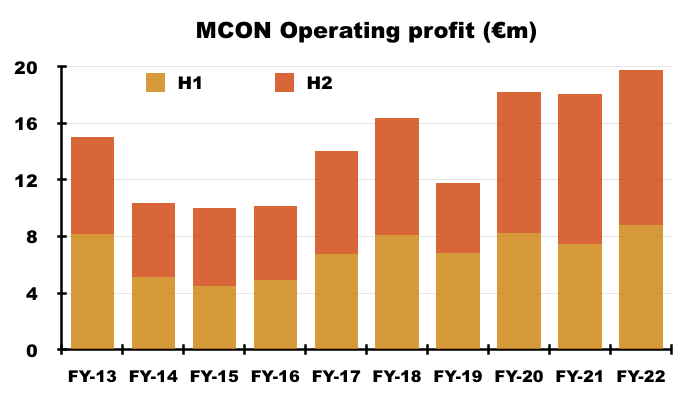

- Both revenue and profit in fact registered new FY records.

- FY revenue gained 18% to €170m while FY operating profit advanced 9% to almost €20 million:

- H2 growth was not as strong as H1 growth, as pandemic interruptions experienced during the comparable FY 2021 receded throughout FY 2022.

- H2 revenue climbed 10%, which lifted H2 profit by only 3%.

- MCON said the “vast majority” of growth had been organic, with favourable currency movements and small acquisitions complementing the performance.

- MCON confirmed sales uplifts were experienced throughout the group, but profit was restrained by “inflationary factors“:

“Revenue growth was a mix of growth across our three industries, with construction, particularly in North America, being the standout performance. However, this growth did not increase our profits significantly as inflationary factors in manufacturing held our margin back, though we did introduce price increases to offset these effects.”

- The “inflationary factors” were not surprising:

“Our manufacturing centralised in Europe did leave us exposed to higher manufacturing inflation in the first half of 2022. The impact was mostly through increased energy costs, which was more acute in Europe. Increased energy costs have considerable impacts on the manufacture of steel products.

Other high inflationary manufacturing elements were in raw material costs, employee, subcontracting and freight costs. We also experienced increased costs in the procurement of non-Mincon manufactured product.”

- A notable comment concerned freight conditions, which are starting to improve and may reduce MCON’s elevated stock position during the current year:

“Freight conditions did start to improve toward the end of the year, and this has encouraged us to look critically at our inventory levels across the group. This will be a strong focus for the year ahead and we have started a group wide project to unwind our working capital position by reducing our inventory to better match prevailing conditions.“

- MCON’s elevated stock position continues to raise doubts about the group’s inherent economics and the level of reinvestment required to deliver higher earnings (see Financials: Stock).

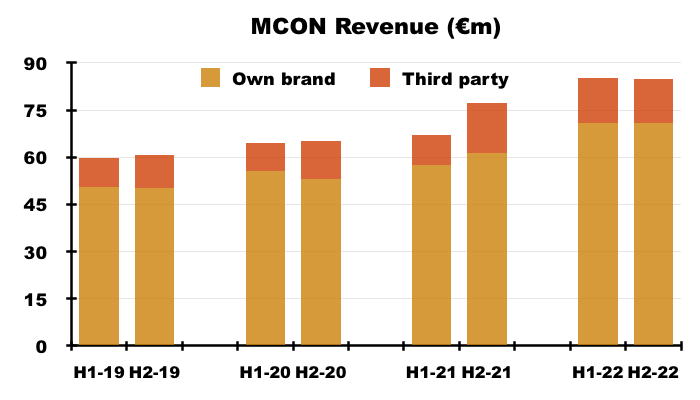

- Sales of MCON’s own-brand equipment gained 19% versus the comparable FY and were up a useful 15% on the comparable H2:

- Third-party sales during H2 fell 13%, which was due perhaps to logistical problems easing and MCON being able to supply its preferred own-brand products.

- Selling third-party equipment helps MCON satisfy a wider range of orders, but derives much lower margins than selling own-brand products.

- Influencing profit also was a share-based payment credit (€190k), greater R&D spend (€4.4m, up €0.5m), a foreign-exchange gain (€469k)…

- …and government grants, the nature of which MCON did not make clear and were in fact lower than the €194k reported for H1:

“The Group recognised €119,000 in Government Grants in 2021 [sic] (2021: €450,000). These grants differ in structure from country to country, they primarily relate to personnel costs.”

- All told, MCON’s financials once again did not showcase obvious ‘moat’-like qualities despite the group’s dedication to “superior technical and innovative technology”:

“The Mincon Group is established as The Driller’s Choice because of our superior technical and innovative technology, coupled with our unsurpassed after sales service.”

- Mind you, this FY did include two references to “return on capital employed“:

“Whilst these results may be creditable in the context of the prevailing market conditions, we are conscious of the need to achieve a greater delivery to the bottom line in the form of improved earnings per share and return on capital employed, and we will concentrate on improving those metrics during 2023.“

…

“These ambitious projects challenge us, but they are essential to underpin our future, maintain our competitive advantages and to drive our profitability and return on capital employed. It also ensures our sustainability as we develop and attract future engineering leaders within the Group.“

- MCON last mentioned “return on capital employed” within its H1 2018 statement, and I therefore trust greater attention is (finally!) being paid to converting the group’s “superior technical and innovative technology” into superior financials (see Financials: Return on equity and revenue per employee).

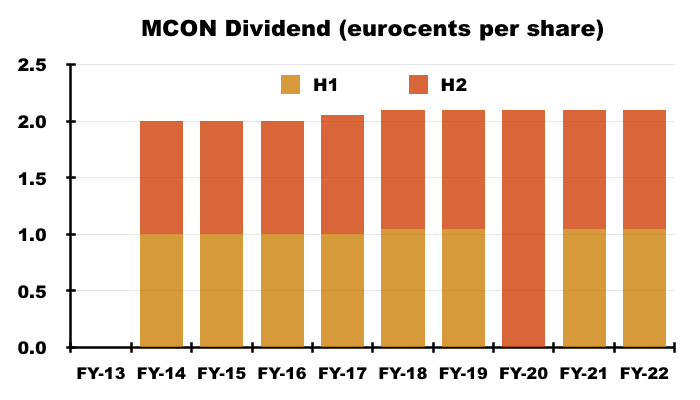

- The final FY 2022 dividend was set at 1.05 eurocents a share and left the annual payout at 2.10 eurocents for the fifth consecutive year:

Sector divisions

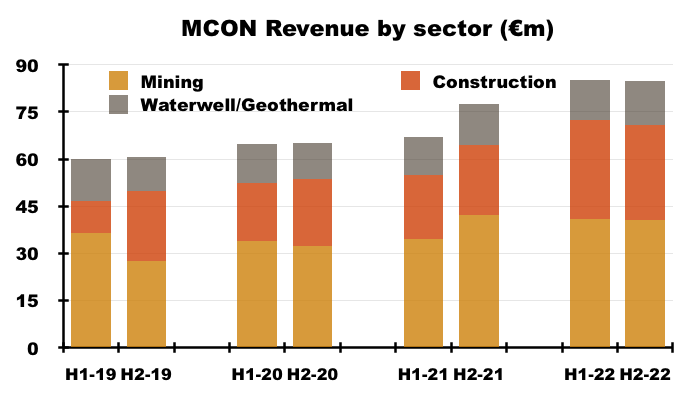

- MCON’s three sector divisions each enjoyed a positive FY:

- FY revenue from mining drills gained 6% to €81m albeit with wide regional variations:

- A greater direct-sales approach, large customers de-stocking and the absence of Russian buyers all influenced mining-related progress.

- Perhaps in response to ESG enquiries, MCON confirmed it would continue to serve the mining industry:

“Despite the difficult conditions prevailing in the global markets right now, we don’t expect any significant changes in the mining sector. There will always be a need for the materials currently being mined, although the focus may change somewhat from time to time. Our drilling tools operate effectively and efficiently in virtually any mining environment and we will continue to provide the after-sales service in the field that assists in the continuous improvement of our products.”

- A greater direct-sales approach helped FY revenue from construction drills gain an impressive 45% to €62m:

“Our direct-to-market approach for mid to large construction projects had a positive result on our construction revenue, where our patented solutions are becoming more recognised as successful application in the industry. We also expanded our footprint through distribution into our APAC region with our solutions for foundation drilling.”

- The construction division has shown superb progress over time, with revenue doubling since FY 2019 to represent 36% of group sales.

- Acquisitions and new products such as the Spiral Flush have supported construction-related revenue:

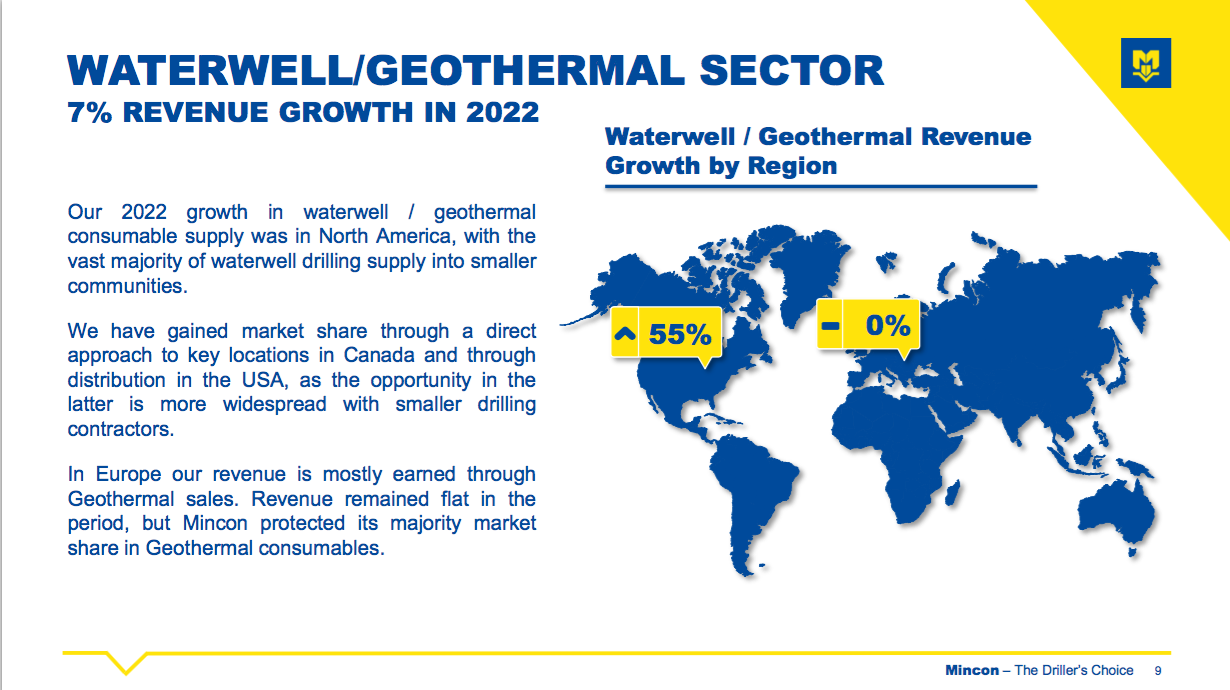

- FY revenue from waterwell/geothermal drilling advanced 7%:

- Once again progress was assisted by a direct-sales approach:

“Our growth in waterwell/geothermal consumable supply was in North America, with the vast majority in waterwell drilling supply into smaller communities. We have gained this market share through a direct approach in Canada in key locations and through distribution in the USA as the opportunity there is more widespread with smaller drilling contractors.“

- Two common themes underpinning greater revenue were highlighted throughout MCON’s sector commentary:

- The group’s direct-sales approach, and;

- Operations in the Americas.

- Four years ago MCON first talked of selling equipment direct to end customers rather than through intermediaries:

“We are differentiating ourselves from the less developed businesses in low margin activities in the sector, and we are positioning ourselves to deal directly with end customers and to win large contracts.”

…

“Going forward we plan to… seek long-term partnerships and multi-year contracts with end customers incorporating direct delivery to their sites.”

- Direct sales should benefit MCON by:

- Creating larger supply contracts;

- Cutting out the intermediary margin, and;

- Providing greater insight into future customer requirements.

- Although annual revenue has increased a welcome 44% since MCON first talked of direct sales four years ago…

- …extra resources have been required to support the approach and MCON’s profit margin remains very ordinary (see Financials: Margin).

- MCON had said direct sales represented 77% of revenue for FY 2021, but did not disclose a proportion for this FY 2022.

- FY 2022 sales to the Americas jumped a terrific 52%, with the small-print revealing United States revenue surging 74% to represent 25% of group revenue:

- US sales have expanded 269% since FY 2018 and the country has been MCON’s largest market since FY 2019.

- Australasian revenue meanwhile represented 10% of group revenue and has dropped 40% since FY 2018:

- Hopes of an Australasian recovery are pinned on MCON’s new Greenhammer drill:

“A significant part of rebuilding our revenues in the Australian market will be through our Greenhammer project.”

Greenhammer

- This FY reiterated the “transformational” potential of MCON’s most promising new product:

“We remain confident in the long-term success of this [Greenhammer] project and believe that the system will be transformational for Mincon and the hard rock surface mining industry.”

- To recap, MCON first mentioned Greenhammer within the FY 2016 results while the FY 2018 statement described the new drilling system as…

“[A] disruptive technology, offering tremendous savings in fuel, with an ambitious planned partnership programme in our customer base”.

- …and suggested the design could enjoy a strong competitive advantage:

“This is not a small system or easily replicable, and we have placed patents around the system to protect it. The system is more than just the hydraulic hammer; it includes all the drill string and the supporting on-rig infrastructure and handling.”

- MCON announced Greenhammer’s first commercial contract last September:

“Mincon is pleased to announce the signing of the first commercial contract for the Greenhammer system.

This milestone is the culmination of many years of development work and is the first step toward revenue generation with a unique drilling system that has a transformational potential for Mincon and the hard rock surface mining industry. The Greenhammer contract is with a blue-chip mining contractor operating on a major gold mine in Western Australia.“

- MCON said this first contract had the potential to become a “multi-million-euro” deal, with initial revenue expected during H2 2022:

“The contract provides for the mobilisation of the Greenhammer system to be run on a Mincon-owned test rig as well as a full Mincon team to support drilling blastholes on an agreed price per metre drilled. The Greenhammer system is expected to be onsite at the mine and generating revenue early in Q4 2022.“

- This FY statement did not mention Greenhammer revenue.

- Management commentary instead focused on (third party) rig problems:

“The Greenhammer system has performed to expectations when operating. However, it has been challenging to consistently deliver drilled metres due to reliability issues encountered with the drill rig. As a result, we had to carry out an extensive rebuild on the rig which we are confident will reliably support the system.”

- Discussions with rig manufacturers to create a reliable drilling platform…

“We believe that the successful roll out of this innovative [Greenhammer] drilling system will require that we closely collaborate with drilling manufacturers to ensure the system is properly supported on a reliable drill rig platform. With that in mind we have engaged in discussions with rig manufacturers with a view to developing mutually beneficial working relationships.”

- …suggest initial Greenhammer revenue will arrive later than expected.

- Further information about Greenhammer and its first paying customer remains frustratingly hard to find online.

- MCON has published limited pictures of Greenhammer, too:

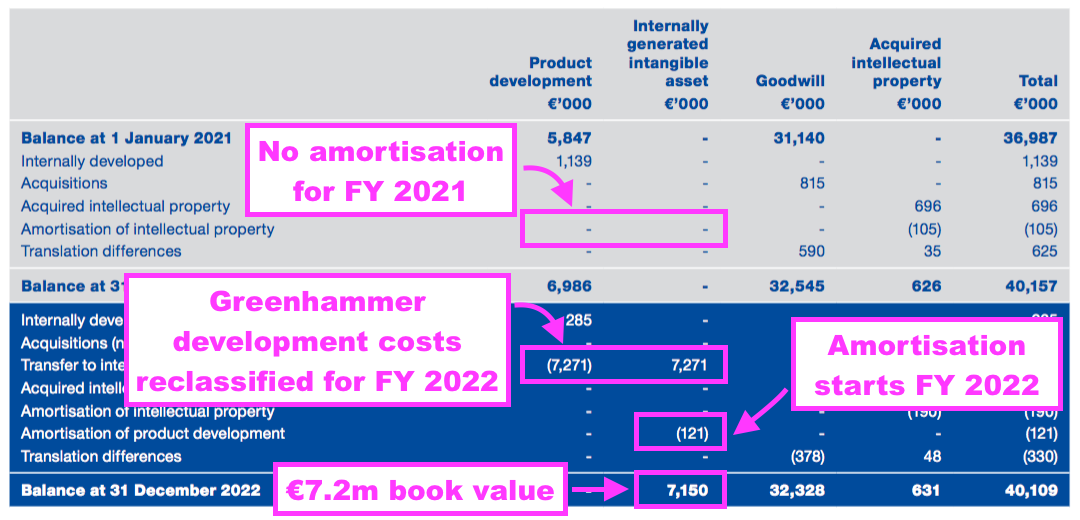

- MCON capitalised Greenhammer development costs of €0.3m during H1, but did not capitalise any Greenhammer costs during H2 following the first commercial contract.

- Greenhammer amortisation of €121k was charged during H2, leaving capitalised Greenhammer development expenditure since FY 2016 at €7.2m:

- This FY revealed an ambitious amortisation timescale for Greenhammer.

- The 2021 annual report (point 16) had said Greenhammer development costs would be written down over three-to-five years:

“Investment expenditure of €1.1 million, which has been capitalised, is in relation to ongoing product development within the Group. Amortisation will begin at the stage of commercialisation and charged to the income statement over a period of three to five years, or the capitalised amount will be written off if the project is deemed no longer viable by management.”

- But the 2022 annual report now says Greenhammer development costs will actually be written down over 15 years:

“Investment expenditure of €285,000, which has been capitalised, is in relation to ongoing product development within the Group. Amortisation began in October 2022 once the project was commercialised. Amortisation is charged into the income statement over fifteen years on a straight line basis.“

- 15 years is a long time, and implies MCON will receive income from Greenhammer systems until 2038.

- But whether Greenhammer will still be relevant to the group by 2038 remains to be seen.

- Bear in mind work on Greenhammer commenced around 2011 and the entire project lifespan would therefore appear to be 27 years.

- The risk to shareholders is the long 15-year amortisation period flatters future earnings by not adequately reflecting the possibility the product becomes obsolete in the meantime.

- If Greenhammer’s 15-year lifespan is optimistic, the directors may be optimistic about other accounting judgements, too.

- That said, MCON could currently be selling drills developed 15 years ago and 15-year shelf lives may be quite normal for the industry. (Leave a comment below if you have some insight!)

Subsea drilling and large-diameter hammer drilling

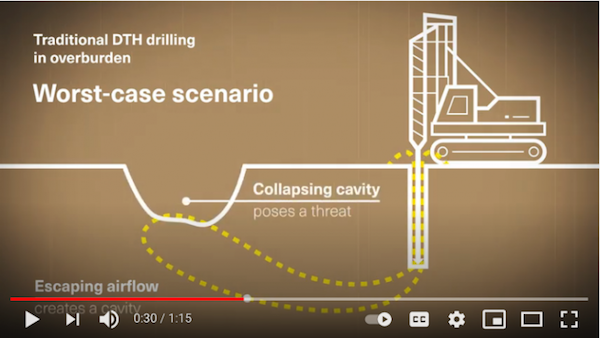

- MCON emphasised the environmental credentials of its seabed drilling venture:

“One of the biggest areas of opportunity arising today is the development of technology to facilitate the switch from fossil fuels to sustainable energy sources. To avail of the opportunities presented by the transition we are currently working on the development of a patented anchoring system for offshore wind turbines. We are developing this system in conjunction with our partners in Subsea Micropiles Limited. “

- This 1m51s video explains the subsea project in more detail:

- MCON’s robotic drill aims to overcome the disadvantages of current subsea drilling, which are: slow installations, complex hammers, dependence on large support vessels and limitations with certain seabed geologies.

- MCON added:

“The system will enable the effective anchoring of offshore platforms with reduced environmental and seabed disruption in water depths of up to 200 metres at a lower cost than the systems that are currently in use.”

- MCON sounded upbeat about recent subsea developments:

“We have successfully run the full-size water powered hammer prototype drilling system at a local quarry. The development of the overall commercial solution is well progressed with our Subsea partners with offshore testing due in H2 2023. [There is] Significant interest within the industry and a growing realisation of the importance of the system to truly scale offshore wind.”

- MCON noted additional projects outside its core mining, construction and geothermal sectors could be forthcoming:

“Our goal is to also diversify the business further into new industries through our advantage in engineering and manufacturing capability, though this process will require a considerable amount of investment. This will include partnering with others in our current industries and new industries, as we recognise that customer productivity goals, with sustainability KPIs, cannot be achieved alone.”

- The appointment of a new non-exec with a PhD that focused on “cleantech on pollution prevention” — alongside the introduction of an Environment and Sustainability board sub-committee — suggest new alternative-energy efforts will be prioritised.

- Not much commentary was devoted to MCON’s large-diameter drilling system:

“We also finally got onsite in Malaysia, after COVID-19 restrictions were lifted, to see our large diameter drilling system drilling 1750 mm diameter holes. We were very happy with the performance of the system and believe that there is a great future for this concept within our product offering for the large diameter construction piling industry.”

- This fledgling system has environmental benefits, too:

“There remains significant interest in this system from the large diameter piling industry, especially when emissions reduction requirements in construction are considered.”

- The comparable FY 2021 statement claimed the prototype had drilled the “largest holes ever… with a single hammer“:

“Another testing success was the drilling that was carried out in Malaysia with our new large diameter hammer system to drill 1750mm diameter rock socket friction piles. We believe that these are the largest holes ever drilled with a single hammer.“

Financials: Margin

- MCON said Greenhammer systems, seabed drilling and large-diameter piling would become “higher margin” activities:

“In particular, our future expansion will be in our higher margin, technically innovative products, such as the Greenhammer system, large diameter piling solutions and our novel system for anchoring offshore wind turbines to the seabed. These are the products that will set us apart from our competitors.“

- The text above reads as if MCON’s existing products will remain lower margin and/or will not set the group apart from its competitors.

- That interpretation is supported by MCON admitting its mining division faces a “more competitive marketplace“:

“The mining consumables industry has become a more competitive marketplace in most of our regions due to inflationary impacts on manufacturing and on the users of mining consumable products. Our strategy is to challenge competitors with more efficient products and thereby bringing greater efficiencies to our customers’ operations.”

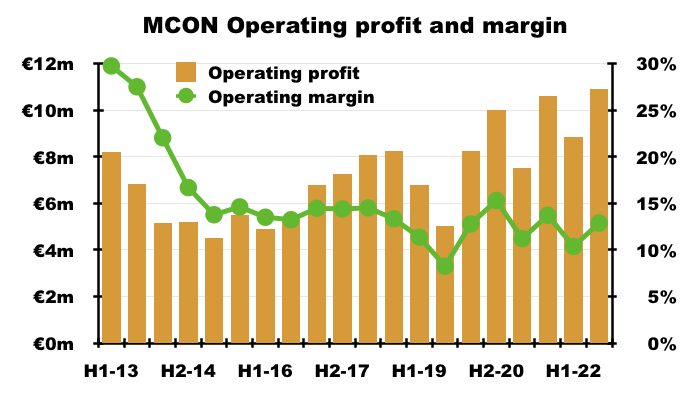

- I have bemoaned MCON’s margin performance for some time.

- I bought MCON shares during 2015 partly because of the group’s then attractive 19% operating margin:

“[H]igh margins underpin the notion that MCON has a respectable competitive advantage. The group converted 19% of revenues into profit during 2014 and above 20% during 2011, 2012 and 2013.”

- But the margin has since bobbed between 10% and 15%:

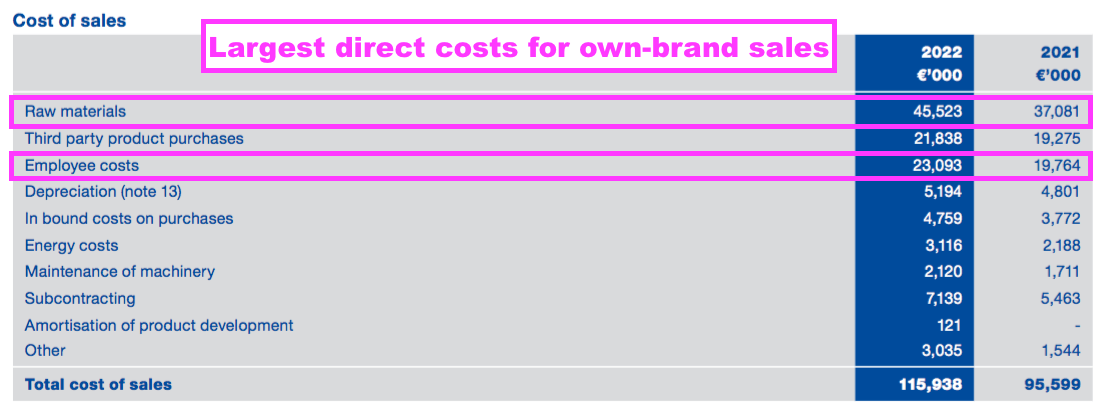

- MCON commendably lists its major operating costs:

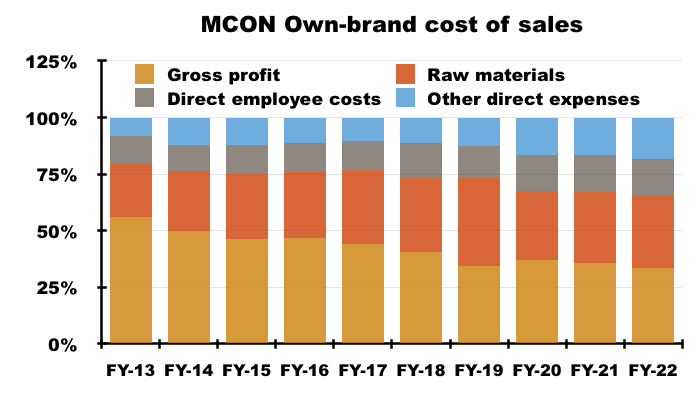

- The long-term margin decline has been caused by the greater cost of sales for its own-brand equipment:

- Since FY 2014, the gross margin on own-brand equipment has dropped from 50% to 33% due to:

- Raw materials increasing from 26% to 32%;

- Direct employee costs increasing from 12% to 16%, and;

- Other direct expenses increasing from 12% to 18%…

- …of own-brand revenue.

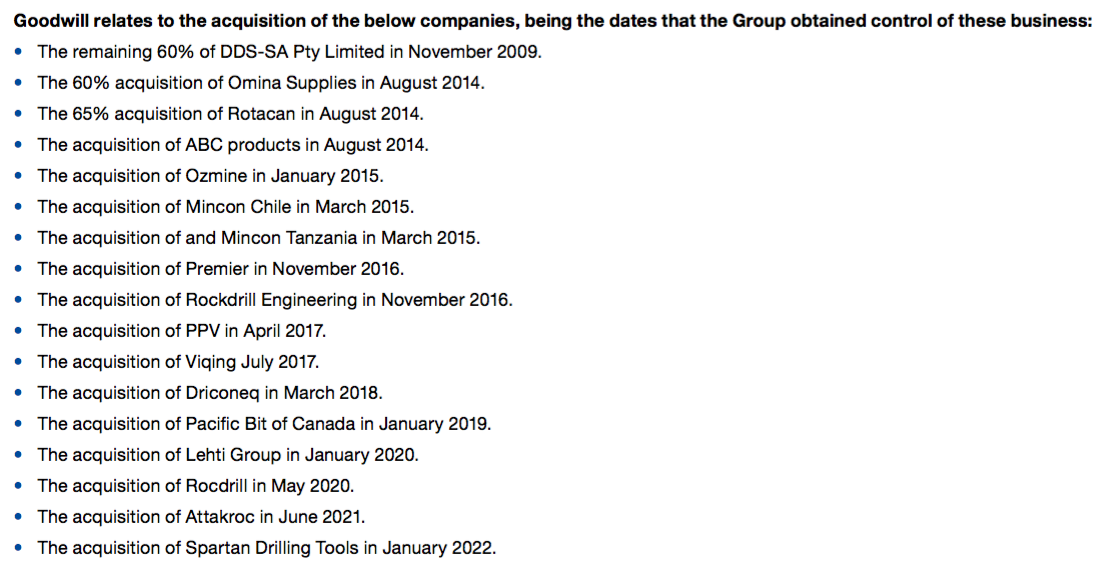

- Following the 2013 flotation, MCON has acquired at least 16 businesses to broaden its product range in order to serve customers direct….

- …and in doing so has evolved from operating as a niche, high-margin drill manufacturer with perhaps modest growth prospects into a wider, middle-margin drill supplier with possibly larger growth prospects.

- MCON reckoned its “technically superior products” could garner higher margins from construction work:

“Our technically superior products to service this sector have led to our Group becoming established as a first port of call for those responsible for large-scale, complex geotechnical/construction projects. We are intensifying our focus on this market and we expect to see further growth and increased margins in this business.“

- And last month’s Q1 2023 update also talked of higher margins:

“Our price increases, introduced in 2022 to offset manufacturing and operating cost increases, have also contributed to better margins than in the first quarter of 2022.”

…

“We continue to improve the efficiencies of our manufacturing plants which will reduce emissions and enhance our manufacturing margins.“

- But the fact remains a sub-15% operating margin since FY 2015 is not commensurate with MCON’s claim of being “the Driller’s Choice” because of “superior technical and innovative technology“…

- …and customers paying a premium for high-quality products not sold elsewhere.

- Suffice to say, MCON has a long way to go to prove the attractive economics of its industrial drills when specialist engineers such as Halma, Renishaw, Rotork and Spirax-Sarco can deliver margins of 20% or more.

Financials: Stock

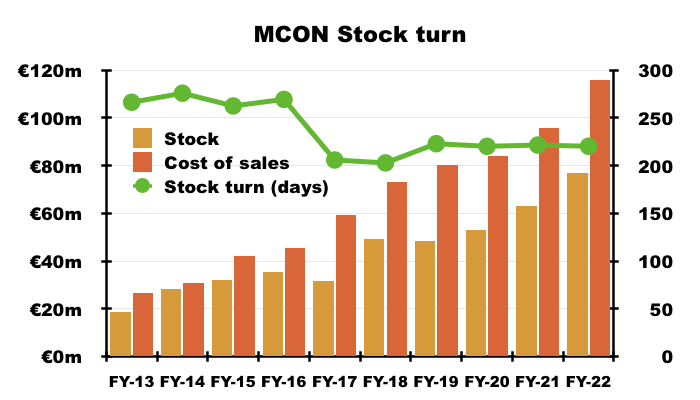

- Logistical difficulties during this FY prompted even higher levels of stock:

“We continued to navigate poor freight conditions which hampered our ability to provide the excellent service-levels our customers expect, as well as requiring working capital investment due to the higher levels of inventory required to manage extended shipping transit times.”

- Stock ended the year up €14m, or 22%, to €77m, of which €12m was added during H1 and €2m was added during H2.

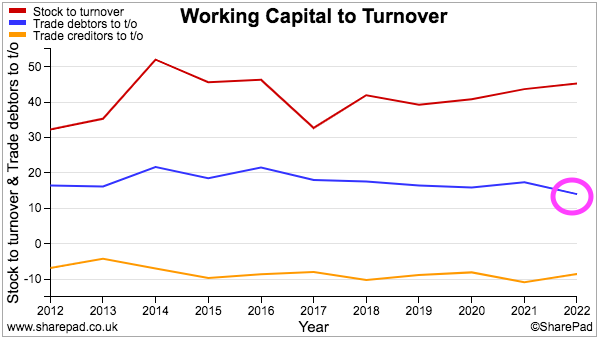

- Stock at €77m is equivalent to a huge 45% of FY 2022 revenue of €170m.

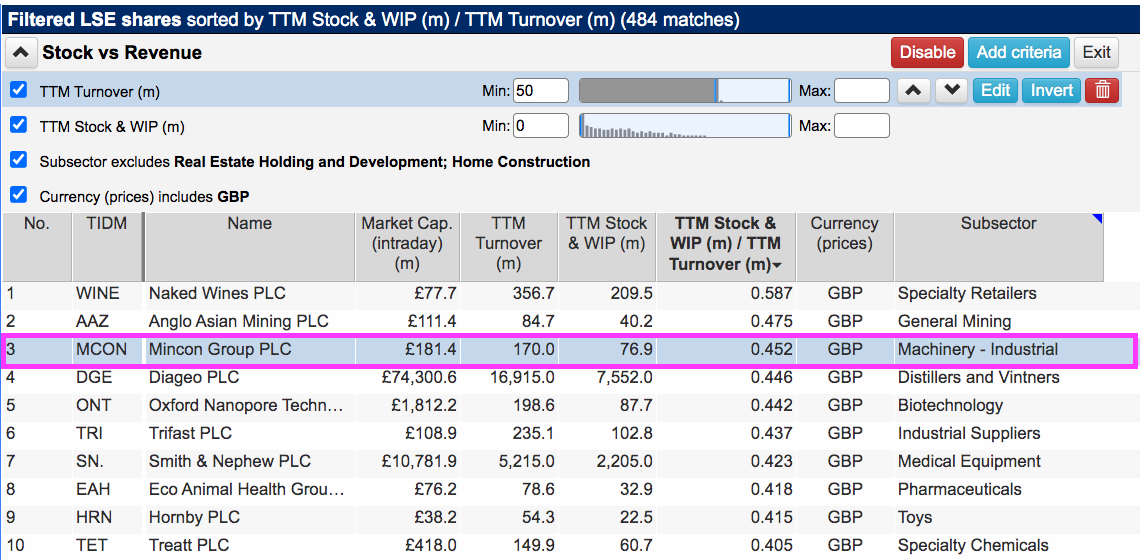

- For some perspective, SharePad shows MCON ranked 3rd out of 484 companies (excluding house builders and property developers) with revenue of £50m or more on a stock-to-revenue basis:

- True, notable stock levels can feature at ‘quality’ companies, with Diageo ranked 4th on that list.

- But Diageo’s stock is dominated by “maturing inventories of whisk(e)y, rum, tequila and Chinese white spirits”, which I understand can increase in value while stored in a warehouse.

- For most companies, carrying large amounts of stock typically means:

- Manufacturing slow-moving items that carry a greater risk of obsolescence;

- Applying inefficient working practices, and/or;

- Requiring greater cash investment into extra stock to support future growth.

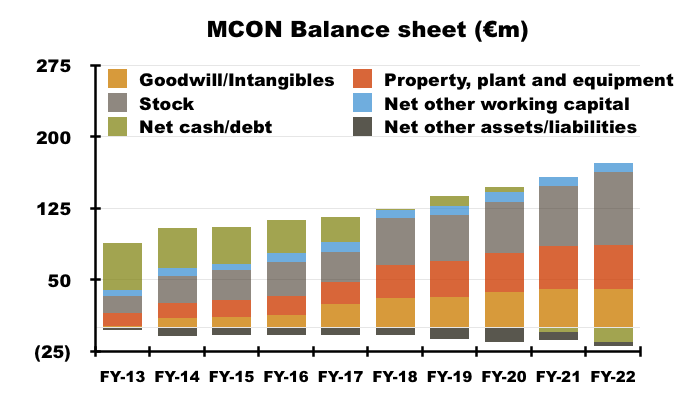

- Significant levels of stock have long been an unfortunate drawback of MCON’s balance sheet.

- Stock has grown from 21% (€18m) to represent 50% (€77m) of the group’s net asset value between FY 2013 and FY 2022:

- Elevated stock levels do seem part and parcel of MCON’s business.

- MCON’s customers are located throughout the world (often in remote mining locations) and require a “timely supply” of drilling equipment:

“The Group manufactures and sells rock drilling consumable products, and the timely supply and service of these products is paramount to our business model. Since the markets that we serve across the world are geographically dispersed, and the lead times for delivery are set by customer requirements and competition to a large degree, we have built a wide network of customer service centres backed by manufacturing plants in key markets.“

- At least MCON’s stock is not perishable and write-downs during this FY were not material at €128k.

- Stock turn has remained consistent during recent years but is still lengthy. Average inventory employed during FY 2022 divided by cost of sales incurred gives 220 days (7-8 months):

- MCON reckons stock levels will reduce during 2023:

“During 2022, we started an inventory reduction programme when there was evidence of improved freight conditions and raw material supply had begun to ease.”

…

“The reduction of inventory levels will continue through 2023 and we would expect to see a decrease in inventory weeks held by the end of this year. We would also expect to see cash released into operations as raw material levels decrease in the first half of 2023.”

- Bear in mind MCON has talked about stock reductions before…

“During 2018, inventory had increased by €13.3 million, and increased further in the first quarter of 2019, since that period inventory has decreased steadily and is now €0.8 million below the 2018 year end level, and management expect that the Groups inventory will continue to decrease.”

- …although such talk did not have a long-lasting effect.

Financials: Cash flow and net debt

- The extra stock investment extended MCON’s record of poor cash generation.

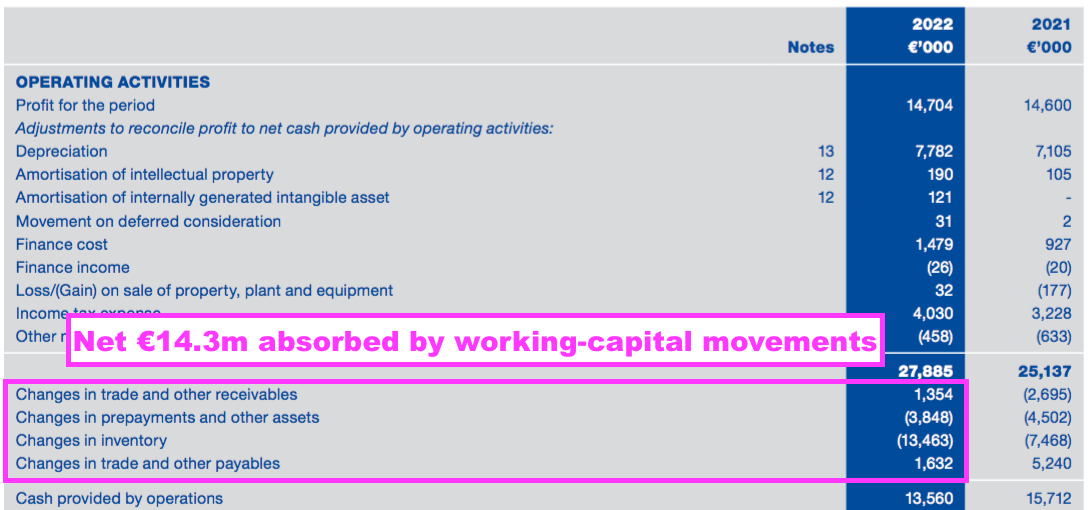

- Cash invested into working capital came to a net €14.3m, which included prepayments for manufacturing equipment of €3.8m:

- Such prepayments now stand at a not insignificant €9.9m, which suggest MCON does not enjoy fantastic purchasing power with certain equipment suppliers:

- Cash absorbed into working capital (including equipment prepayments) during the last five years totals a substantial €40m:

| Year to 31 December | 2018 | 2019 | 2020 | 2021 | 2022 |

| Operating profit (€k) | 16,352 | 11,810 | 18,249 | 18,107 | 19,749 |

| Depreciation* (€k) | 3,896 | 3,898 | 4,666 | 5,209 | 5,623 |

| Net capital expenditure** (€k) | (12,552) | (7,930) | (6,981) | (7,024) | (6,313) |

| Working-capital movements (€k) | (14,870) | 2,095 | (2,912) | (9,425) | (14,325) |

| Free cash flow (€k) | (11,118) | 3,175 | 11,393 | 3,015 | 1,466 |

| Net cash (€k) | 846 | 5,586 | 461 | (4,342) | (14,909) |

(*excludes IFRS 16 depreciation **excludes Greenhammer expenditure)

- Five-year expenditure on tangible assets beyond the depreciation charged against earnings meanwhile stands at €17m.

- Factor in €6m spent on Greenhammer, a net €19m spent on acquisitions and €22m spent on dividends, and no wonder net cash has reduced from €26m to net bank borrowings of €15m since FY 2017.

- Total gross bank loans now stand at €31m, but do not appear truly alarming versus:

- Cash of €16m;

- FY 2022 earnings of approximately €15m, and;

- An estimated 3.2% borrowing rate (interest of €870k on average €27m debt).

- But operating with net debt is never ideal and as the pandemic showed, companies with cash set aside for a rainy day stand more chance of sustaining their dividends when adverse events occur.

- Whether MCON should be declaring dividends given its significant cash expenditure is debatable.

- Free cash flow for FY 2022 was a paltry €1.5m and did not cover the annual €4.5m dividend:

| Year to 31 December | 2018 | 2019 | 2020 | 2021 | 2022 |

| Free cash flow (€k) | (11,118) | 3,175 | 11,393 | 3,015 | 1,466 |

| Dividends paid (€k) | (4,421) | (4,426) | (2,222) | (6,693) | (4,462) |

| Net acquisitions (€k) | (9,264) | 6,147 | (9,910) | (2,652) | (3,642) |

- On a five-year view, total free cash flow of €7.9m has not covered the €22m used to pay dividends (let alone acquisition spend of €19m) during the same time.

- MCON’s dividends ought really to be funded by surplus-to-requirements cash flow and not by extra borrowings.

- MCON must consider whether its €4.5m annual dividend remains appropriate if further working-capital investments and acquisitions continue to necessitate significant extra debt.

- Evidence to date of fantastic returns from the debt-funded investments and acquisitions is not entirely obvious (see Financials: Return on equity and revenue per employee).

- Elsewhere in the accounts, year-end trade receivables at €24m represented a welcome 14% of revenue — their lowest proportion for at least ten years:

- MCON’s accounts are not complicated by defined-benefit pension obligations.

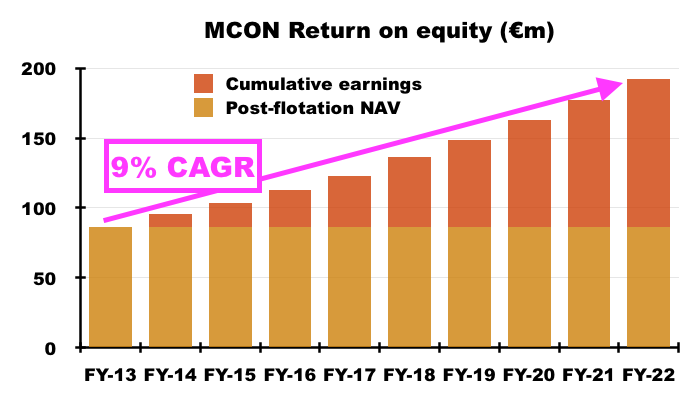

Financials: Return on equity and revenue per employee

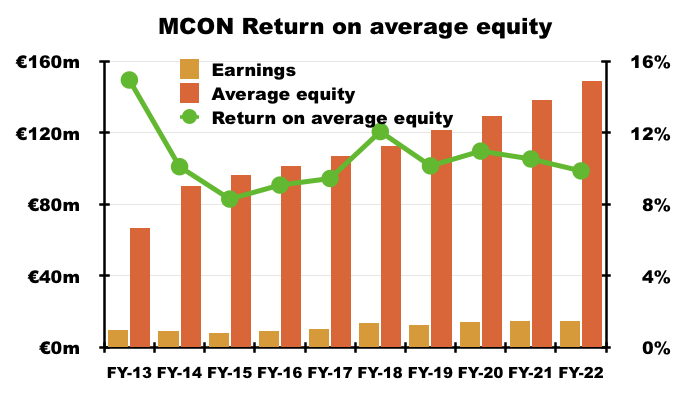

- MCON’s ordinary margin and hefty cash expenditure have translated into return on equity numbers of approximately 10%:

- The 10% calculation is underpinned by evaluating MCON’s progress following the group’s 2013 flotation.

- When MCON became a public company, shareholder equity was €86m and net cash was flush from the flotation proceeds at €49m.

- Subsequent reported earnings have totalled €106m:

- Effectively investing €86m to earn a cumulative €106m over nine years equates to a 9% annual average compound return.

- Earning 9% a year on shareholders’ equity is not awful but is not exceptional either.

- For some perspective, the same nine-year calculation for fellow portfolio member Andrews Sykes is 16% (based on an aggregate £126m earned from a £43m starting equity base).

- Perhaps one day Greenhammer, the large-diameter drills and/or the seabed micro-piling will attract more customers prepared to pay premium prices for advanced equipment, which in turn lifts equity returns to more respectable levels.

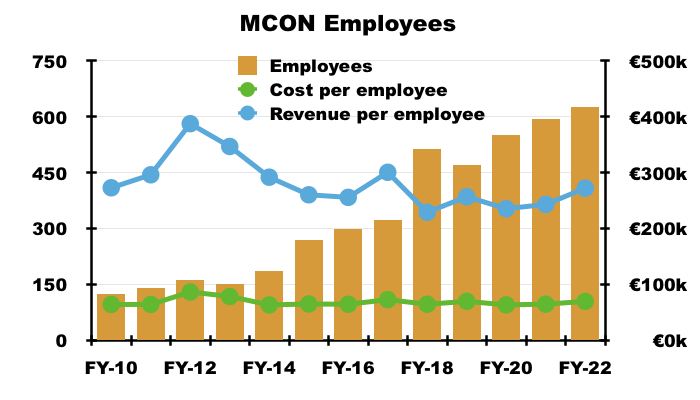

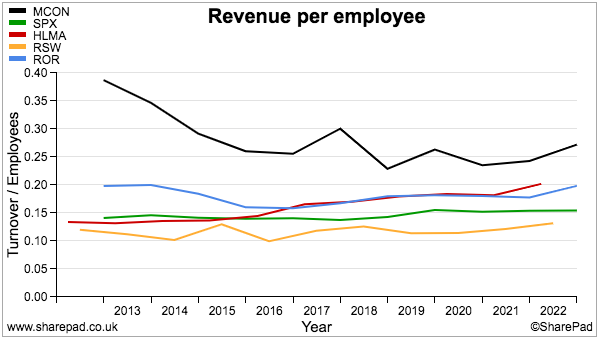

- Right now only revenue per employee provides hope that MCON is an above-average business.

- During the nine years following the flotation, revenue per employee has averaged a useful €260k and improved during this FY to €272k per head, the highest level since FY 2017 (€300k):

- My rule of thumb with revenue per employee is anything beyond £200k might indicate the employees develop higher-value products that could sustain a competitive ‘moat’.

- For perspective, specialist engineers Halma, Renishaw, Rotork and Spirax-Sarco have revenue per employee measures of £200k or less:

- This comparison suggests MCON’s products are indeed high value, which in turn implies the group’s sub-15% margins are due to the inherent greater costs (e.g. raw materials) involved with manufacturing and supplying industrial drills.

- I trust MCON’s revenue per employee can continue to improve over time to reflect higher selling prices, larger supply contracts and new product launches.

Valuation

- MCON implied its construction division would be the group’s best performer during FY 2023:

“In the context of the many uncertainties described above, we expect that some of our markets will experience turbulence from time to time. However, we believe that significant expenditure on infrastructural projects will continue for the foreseeable future in developed economies, especially in the United States.

Our technically superior products to service this sector have led to our Group becoming established as a first port of call for those responsible for large-scale, complex geotechnical/construction projects. We are intensifying our focus on this market and we expect to see further growth and increased margins in this business. “

- May’s Q1 update confirmed positive construction progress:

“Our revenue in the construction industry remains strong and we continue to make progress in winning small to mid-size construction projects in Europe and North America. The very strong construction revenue growth in North America during 2022 has continued at the same level into Q1 2023. Coupled with this, we have also seen good growth in construction revenue for the first quarter in the European market.“

- But the Q1 update admitted lower-than-expected revenue from mining customers:

“While revenue in Q1 2023 was marginally behind the same period in the prior year, we are pleased with further improvement in our gross margin in the first quarter. The reduced revenue in Q1 is a result of lower revenue than expected in the mining industry, due to reduced activity in the exploration sector during the quarter and resultant lower orders from some specific large customers as they adjust their inventories in response. However, we remain confident in our outlook for this segment and expect that our mining revenue will improve as the year progresses.”

- At least the Q1 2023 margin was greater than the Q1 2022 margin:

“Our price increases, introduced in 2022 to offset manufacturing and operating cost increases, have also contributed to better margins than in the first quarter of 2022. “

- MCON expressed optimism towards FY 2023, profit margins and environmental tailwinds:

* “We maintain a positive outlook, both for the remainder of 2023 and on our long-term outlook for the industries in which we operate. Our ambitious product development programs should serve us well in the global challenges ahead to reduce carbon emissions. We continue to improve the efficiencies of our manufacturing plants which will reduce emissions and enhance our manufacturing margins.”

- FY 2022 operating profit was €19.7m, which after 25% tax gives earnings of €14.8m or 6.0p per share with GBP:EUR at 1.16.

- Adjusting the £191m market cap for cash of €16m, borrowings of €31m and a deferred consideration of €2m gives an enterprise value of £206m, or 97p per share.

- Dividing that 97p per share by my 6.0p per share earnings guess then gives a possible P/E of 16.

- While the sums could be fine-tuned for lease financing, Greenhammer amortisation and minor other items, my rudimentary multiple does not appear ridiculously cheap nor bonkers expensive.

- Given MCON’s ever-ballooning stock level, an alternative valuation yardstick is the balance sheet.

- This FY showed net tangible assets at €113m or 46p per share, which represents 51% of the 90p share price:

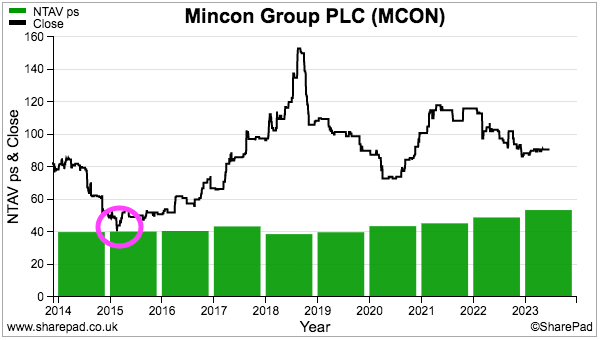

- The shares looked much better value on a net tangible asset basis when I invested at 45p during early 2015.

- For now I am hopeful a mix of:

- An easing of cost pressures leading to improved margins;

- Further robust demand from the construction sector;

- Greater direct sales of equipment;

- Greater sales from the United States, and/or;

- Greenhammer and other development projects bearing fruit…

- …can lead to respectable financial progress during the next few years.

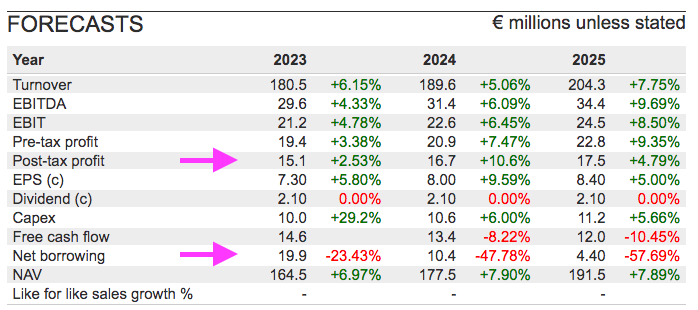

- For what they are worth, broker forecasts show profit increasing and net debt decreasing:

- Long-term share-price success will depend upon management’s commitment to superior product quality eventually translating into financial evidence of a superior competitive ‘moat’.

- Right now, MCON’s financials frustratingly do not indicate an obvious competitive advantage… which is perhaps why the shares currently trade at levels first achieved during 2017.

- The stock position needs to reduce and cash conversion needs to improve, and the board really ought to consider whether dividends should be maintained when the payouts have been effectively funded by extra debt during the last few years.

- That said, MCON was established during 1977 and very much remains a family-run business with a corresponding long-term perspective.

- MCON’s founder still works as a board non-exec in his 80s while his two sons are the lead executives. The family members own a collective 56%/£108m shareholding.

- No family member sold a share at the 2013 flotation and none has sold a share thereafter.

- I am therefore hopeful:

- The dominant family shareholders are true owner-managers and have everything in hand;

- The very ordinary financials of recent years will improve over time, and;

- Long-haul investors who stay the course will (eventually) be rewarded.

- But I do worry:

- The dominant family shareholders may continue to focus on costly expansion and overlook logical capital-allocation decisions;

- The sub-optimal financials of recent years won’t improve over time, and;

- Long-haul investors who stay the course end up trapped in a ‘fiefdom’ under-performer and illiquid share.

- As clear signs of moat-like financials are awaited, the trailing 2.1 eurocents, or 1.8p, per share dividend supports a modest 2.1% income (before Irish withholding taxes for UK-resident investors).

Maynard Paton

Mincon (MCON)

Publication of 2022 annual report

Here are the points of interest beyond those noted in the blog post above:

——————————————————————————————————————

1) BUSINESS MODEL AND STRATEGY

Some new explanatory text introduced for 2022:

“Mincon’s strategy is to develop long-term sustainable competitive advantage through designing and manufacturing world class products, that will bring value for our shareholders and stakeholders. Our business development is focused on growth, creating new opportunities and continued improvement in all aspects of our business, and we can accomplish this through our strategic goals:

• To market competitive products centred on an ethos of innovative engineering and service that is committed to adding value for our customers.

• To seek new opportunities in new markets and to diversify our income streams to increase our global footprint.

• To manufacture our products in strategic locations that allows a better service for our customers and reduce the requirement for trans-ocean distribution of our products.

• To meaningful contribute to the environment, through investing in manufacturing that requires less energy, and to make positive contributions in the communities where we have businesses.”

The group’s competitive advantage remains supported by the following commitments:

”We are committed to:

• innovative engineering and industry-leading quality;

• the creation of new drilling products and technologies and associated intellectual property, supported, inter alia, by patents

• industry-leading field service delivery, and

• improving the skill sets of our teams”

The 2022 text repeats previous text explaining the need for high stock levels: i.e. the “timely supply” of products with “long manufacturing lead times” to “geographically dispersed” customers:

“The Group manufactures and sells rock drilling consumable products, and the timely supply and service of these products is paramount to our business model.

Since the markets that we serve across the world are geographically dispersed, and the lead times for delivery are set by customer requirements and competition to a large degree, we have built a wide network of customer service centres backed by manufacturing plants in key markets.

We continue to review our factory operations and from time to time we relocate the manufacture or part manufacture of some products from one factory to another, in some cases, to achieve better economies of scale, and in other cases, to manufacture products with long lead times closer to their markets so that we can adapt to changing customer needs in a more timely fashion and reduce our trans-ocean freight costs. These factory reviews are ongoing as part of the company’s rolling strategic plan.”

2) PRINCIPAL RISKS AND UNCERTAINITIES

No changes here for 2022.

The main shareholder dangers remain cyclical markets, economic conditions, less developed overseas legal systems, innovation failure, copycat competitors, facility failures, industry competition, currency movements, contractual arrangements, customer concentrations, pricing of raw materials, Covid-19, climate change and cyber attacks.

Worth repeating this text that reiterates MCON’s competitive market and larger rivals:

“The markets for the Group’s products are highly competitive in terms of pricing, product design, service and quality, the timing and development and introduction of new products, customer services and terms of financing. The Group faces intense competition from significant competitors and to a lesser extent small regional companies

The Group is subject to competition in the markets in which it operates and some of its competitors are significantly larger and have significantly greater resources than the Group. The Group’s principal competitors are Epiroc which is headquartered in Stockholm, Sweden, with a global reach spanning more than 150 countries and Sandvik, which is also headquartered in Stockholm, Sweden, with business activities in more than 160 countries.”

October’s warning of delayed/postponed contracts underlines the “non-recurring nature of some transactions“.

“Contractual Arrangements:

The Group derives some of its revenue from large transactions (which may be non-recurring in nature). Prospective sales are subject to delays or cancellations over which the Group has little, or no control and these delays could adversely affect results, The Group focuses on securing new lines of business on a regular basis to address the non-recurring nature of some transactions. ”

At least MCON’s customer base has become more diverse. The top-ten revenue proportion has declined from 28% for 2021 to 24%:

“Customer Concentration :

During 2022, the Group’s top ten customers have accounted for approximately 24% of its revenues. If, in the future, these customers fail to meet their contractual obligations, decide not to purchase the Group’s products or decide to purchase fewer products, this could disrupt the Group’s business and require it to expend time and effort to develop relationships with new customers, which could have a material adverse effect on the Group’s business, results of operations and financial condition. There can be no assurance that, even if the Group could find alternate customers, the Group could receive the same price for its products.”

3) REGIONS

MCON provides stats for each of its regions:

a) Europe/Middle East: 301 staff, 2 service centres, 4 factories = 19.4k sqm

b) Asia Pacific: 76 staff, 2 service centres, 1 factory = 5.5k sqm

c) Americas: 177 staff, 11 service centres, 2 factories = 9.6k sqm

d) Africa: 79 staff, 3 service centres, 1 factory = 6.4k sqm

Americas has 41% of sales (€70m of €170m) but only 23% of manufacturing space (9.6k sqm of 40.9k sqm).

Maybe that earlier text — “from time to time we relocate the manufacture or part manufacture of some products… to closer to their markets so that we can adapt to changing customer needs in a more timely fashion and reduce our trans-ocean freight costs” — reflects the need for greater manufacturing in the Americas.

Americas manufacturing facilities were 7.9k sqm for 2021, so expansion has occurred.

4) DIRECTORS

The 2022 report includes the bio for the non-exec appointed during March 2022, who sports a CV with useful ESG credentials:

“PIRITA MIKKANEN

Non-Executive Director Age 57 Pirita is currently a Vice President of Energy with the Metsä Group, a Finnish forest industry group operating in international markets, focused on the responsible processing of northern wood into first-class products. Her team at Metsä works to ensure reliable and cost-effective energy production and leads the sustainable development of Metsä utilities. Prior to joining Metsä, her experience included roles with TM Systems Oy, an industrial air systems company with a focus on reducing energy usage and emissions, and serving as CEO of Lifa Air Ltd Oy, a pioneer in the development of services, machines and equipment that enable cleaner and healthier indoor air. She has acted as a fund manager and board member of climate funds. Pirita holds a Ph.D in Applied Physics, focusing on cleantech on pollution prevention, from the Helsinki University of Technology.”

5) DIRECTORS’ REPORT

No major changes in this section. MCON’s vision remains the same:

“Mincon has a clear vision and determined focus giving priority towards:

• Highest design specifications

• Best manufacturing methods and processes and;

• Delivery of superior products to our customers”

MCON’s references to KPIs is poor. The KPI text was limited to only:

“The Director’s review KPIs for Operating Profit, Inventory and Debtors throughout the year.”

KPIs really should be listed with the exact ratios (i.e. how exactly is Inventory reviewed?) and management’s own calculations. MCON also reckons it monitors return on capital (see point 23).

The director appointments show founder Patrick Purcell now having served as a non-exec since 2013 — i.e. more than the best-practice nine years. But he and his family own a collective 56% and I dare say his experience running the business from 1977 up to 2012 serves the other 44% of shareholders well.

The auditor has changed from KPMG to Grant Thornton :

“Auditor:

Grant Thornton, Chartered Accountants continue in office in accordance with Section 383(2) of the Companies Act 2014.”

6) CORPORATE GOVERNANCE

No changes here for 2022.

Director shareholdings reveal of the four non-family non-execs, one owns 47k shares, another owns 35k shares and the other two both own zero. So relatively token holdings, but they are ‘independent’:

“The Board considers itself to be sufficiently independent. The QCA Code suggests that a board should have at least two independent non-executive Directors. One of the five non-executive directors, Mr. Patrick Purcell, is the company founder and majority shareholder through a trust. None of the rest of the Board is a significant shareholder, save through that trust for certain executive members. The Senior Independent Non-Executive director is Mr. John Doris, who is also the Chairman of the Audit Committee.

Given the text below, I wonder if MCON is up for an appearance on Investor Meet Company?

“The Company is also a regular presenter at invited investor events, providing an opportunity for investors to meet with representatives from the Group in a more informal setting.”

Engagement with UK-resident investors is non-existent from what I can tell.

7) AUDIT COMMITTEE REPORT

All the same text for 2022 save for the appointment of Grant Thornton through an audit tender:

“The Committee is responsible for ensuring that the Group Auditor is objective and independent. KPMG had been the Group’s Auditor from 2013 to 2021. After putting the audit to tender to three Top Ten audit firms, including the resigning auditors KPMG, the committee made the decision to appoint Grant Thornton as Group Auditor in May 2022.”

As per 2021, 2022 witnessed three audit meetings with everyone attending and the main accounting discussion item was goodwill impairment testing.

8) NOMINATIONS COMMITTEE REPORT

Some new text for 2022 highlighting a new ESG committee and actions on succession planning.

The ESG background of the aforementioned new non-exec was put to good use quite quickly:

“The committee suggested the Board might consider creating a new subcommittee of the Board – the Environment and Sustainability Committee – and that Pirita Mikkanen would chair such a committee. The committee was officially set up and the committee terms of reference for this committee were adopted on 04th August 2022.“

The Purcell family seems happy running MCON, with founder Patrick Purcell, age 85, remaining an influential director. But two long-time non-execs may be exiting during the next year or so:

“Board and Executive Succession planning:

The Committee reviewed a report from the Executive on executive succession planning. It was found that executive succession planning was appropriate and dealt satisfactorily with the Company’s requirements. The Committee reviewed the composition of the Board in the context of the normal terms of service of the existing directors. It was agreed to explore the possibility of extending the terms of service of Patrick Purcell in view of his singular understanding of the Company’s business. It was noted that the normal terms of service of Hugh McCullough and John Doris expired at the end of this year and early next year respectively. It was agreed to keep the composition of the Board under review, especially in terms of diversity of experience and expertise, gender balance and geographic diversity.”

Non-exec John Doris will leave MCON on 1 Feb and a new non-exec — Orla O’Gorman — has now joined the board (as per the Dec 2022 RNS here).

9) REMUNERATION COMMITTEE REPORT

An extra primary responsibility for the committee was listed for 2022:

“• direct and recommend for approval by the Board targets and quantum of awards issued under the long term incentive programme”

The committee met three times and reference to a quorum implies not every member attended:

“During 2022, the Committee met on three occasions and had a quorum of members present for all these meetings.”

Targets for annual bonuses remained unchanged:

“The Committee agreed a short-term incentive program for the 2022 financial year, through which the senior management team could earn up to 50% of their salary based on:

• The achievement of budgeted profit after tax for the year (up to 40% of salary)

• The delivery of targeted number of weeks’ inventory being carried at the end of the year (up to 7.5% of salary)

• The delivery of a targeted number of debtors days (up to 2.5% of salary)”

Some new text concerning the new LTIP. Targets are three-year EPS CAGR of 7% and ROCE at 13% or more (but only in the year prior to vesting:

“Proposed Amendment for new LTIP plan to replace 2013 LTIP plan:

The Committee discussed the proposed amendments to the 2013 LTIP plan and agreed the final instructions to be given to William Fry for the preparation of the new 2022 LTIP plan to be put before the shareholders at the AGM. The finalised amendments as summarised on pages 11 to 13 of the AGM circular to our shareholders, per the below link, were approved at the AGM.

https://corporate.mincon.com/wp-content/uploads/2022/04/5-April-2022_Mincon-Group-plc_AGM-Notice-and-Chairmans-Letter.pdf”

Discussion on performance conditions attaching to awards under 2022 LTIP scheme

The Committee reviewed a document prepared by our broker and Nomad Davy setting out performance conditions utilised by some listed Irish PLCs as well as listed industry peers from different jurisdictions. Thereafter it was agreed that future awards would be conditional as to 50% on the achievement of EPS growth targets and 50% as to achievement on ROCE targets. The specific targets proposed and approved by the Remuneration Committee and Board are as follows:

• EPS CAGR in excess of 7% for the three years prior to vesting

• ROCE at or above 13% in the financial year prior to vesting”

The 2021 annual report noted options were previously granted with a three-year EPS CAGR of 5%+CPI target. The new ROCE target seems positive, but targeting 13% ROCE only in the third year provides some leeway for lower ROCE in years one and two. ROCE is a good measure to assess management by outside shareholders given the very large inventory position held by the group.

The basic pay for the chief exec was €200k for the third consecutive year and does not seem huge for a €20m profit business:

The other executive was paid more than his brother through a €228k salary (although EUR:USD fluctuations may influence the figures).

Founder Patrick Purcell declined his non-exec fees during 2022.

Executive bonuses at c40% of salaries do not seem extravagant. The remuneration text does not show the directors owning any options.

The non-execs will receive an extra €5k for 2023:

“It was put to the Remuneration Committee that it would be appropriate that chairpersons of all board sub committees should receive an additional €5,000 in remuneration to reflect the incremental commitment from those roles. The Committee and Board approved this proposal.“

The board described the group’s 2022 effort as “good“:

“The Group’s performance for 2022 was good, particularly in light of the difficulties associated with the war in Europe and the after effects of the COVID-19 pandemic as it unwinds. More insight into the challenges faces is detailed in the Chief Financial Officer’s report on pages 20 to 23.”

10) ENVIRONMENTAL & SUSTAINABILITY COMMITTEE REPORT

A new board committee for 2022:

“On behalf of the Environment & Sustainability Committee and the Board, I am pleased to present the report of the Committee for the year ended 31 December 2022. This report details the Environment & Sustainability Committees responsibilities and how the Committee discharged these duties in 2022.

Responsibilities of the Environment & Sustainability Committee:

The role, responsibilities and authorities of the Environmental and Sustainability Committee are clearly communicated in the Committee’s Terms of Reference’ as displayed on our corporate website. The primary duties include the following:

• Assess the effectiveness of the Group’s policies, programmes, practices and systems for: identifying, managing, and mitigating or eliminating Environmental and Sustainability risks in connection with the Group’s operations and corporate activity; and ensuring compliance with relevant legal and regulatory requirements and industry standards and guidelines applicable to Environmental and Sustainability matters;

• monitor and review current and emerging Environmental and Sustainability trends, relevant international standards and legislative requirements and identify how these are likely to impact on the strategy, operations, and reputation of the Group; and determine whether and how these are incorporated into or reflected in the Group’s Environmental and Sustainability policies and objectives;

• assess the performance of the Group with regard to the impact of decisions relating to Environmental and Sustainability matters, including any social or community projects undertaken, and related actions upon employees, communities and other third parties;

• review the quality and integrity of internal and external reporting of Environmental and Sustainability matters and performance to ensure that the Company provides appropriate information, complies with reporting obligations and good industry practice;

• support and provide guidance to management in developing and updating policies and procedures relating to employee health and safety, environment and social responsibility; and

• make recommendations to the Board on any of the matters listed above that the Committee considers appropriate.

Membership:

Members, including the Chairman, are appointed to the Committee by the Board. The Environment & Sustainability Committee comprises Pirita Mikkanen (chair), Hugh McCullough, Paul Lynch and Patrick Purcell. Only members of the Committee and the Committee Secretary have the right to attend Committee meetings. However, other individuals, including the Chairman of the Board (where not a member of the Committee), the Group Chief Executive Officer (where not a member of the Committee), and other Mincon executives from within individual business units of the Company and its subsidiaries (the “Group”) and external advisers may be invited by the Committee Chair to attend for all or part of any meeting when considered appropriate. The Company Secretary acts as the secretary to the Committee.

Meetings:

The committee shall meet at least two times in each year, and at such other times as the Committee Chair may determine. The committee was officially set up and the committee terms of reference were adopted on 04th August 2022. A preliminary meeting to plan the Committee activities with the personnel responsible of ESG activities within the company was held on 7th December 2022.

Performance Outcome and Environment & Sustainability for 2022:

The very first Sustainability report of Mincon was published in August 2022. This report included the measures and initiatives to meet the company’s sustainability goals by 2040. In addition, the Board of Directors set the Net zero carbon emissions goal and formalised the Social Impact Programme. Mincon next sustainability report will be published in H2 2022.”

The latest sustainability report was published during August 2023:

https://corporate.mincon.com/wp-content/uploads/2023/08/FINAL_Mincon_2023-Sustainability-Report-08082023v2.pdf

11) CORPORATE RESPONSIBILITY

Some text revisions here, which may suggest some tweaking of ESG efforts. For example. this text from 2021…

“Potential solutions for energy optimisation are continuously being evaluated by Mincon facilities, in conjunction with independent suppliers. Solutions under consideration include heat-treatment equipment that will help reduce reliance on natural gas as a fuel source, which will bring a commensurate reduction in carbon dioxide emissions. In areas where it is feasible, heat reclamation technologies are being considered to harvest wasted energy from the heat-treatment process and use it for heating water in facilities. Investigations are also underway to determine the possibility of installing solar panels at sites that have the available space, thus reducing the reliance on a grid that may use fossil fuels for electricity generation”

…was replaced by this text for 2022:

“Efficiency and sustainability is integral to our business growth strategy. We have manufacturing facilities in the same regions as customer operations in order to drastically reduce our reliance on carbon-intensive intercontinental logistics, while simultaneously improving our customer service.

The core focus of all Mincon’s engineering efforts is to improve the energy efficiency of our products. As such, we’re also motivated to reduce the energy requirements – and related emissions – associated with the manufacturing of our products. Our engineering and environmental ethos ensures that there will be ongoing savings once products are in our customers’ hands.”

So I am not sure whether the “heat reclamation” and “solar panels” efforts from 2021 have continued into 2022.

The text introduced a 2040 target for net zero:

“Our goal is to achieve net zero emissions by 2040 – one decade ahead of the 2050 deadline for EU member states to achieve carbon neutrality”

Some text was removed for 2022, including:

“Where possible, products are manufactured as close as possible to customer operations, thus reducing or avoiding carbon emissions for the transport of those products.”

…and:

“We select those suitable for employment solely based on merit. Any job advertisements, application forms and publicity material will encourage applications from all suitable candidates and will not discriminate against any group or individual on any unjustifiable grounds. The objective is to ensure that all candidates have equality of access to all job vacancies.”

I would like to think these removals were oversights rather than deliberate changes to current business practice.

12) INDEPENDENT AUDITOR’S REPORT

A new auditor brings revamped text. Grant Thornton’s evaluation of MCON’s going concern consisted of:

“ • Gaining an understanding of the business and the associated processes of management in the going concern assessment

• Evaluating management’s future cash flow forecasts, the process by which they were prepared, and assessed the calculations are mathematically accurate the cash flow forecast is prepared up to 31 December 2025

• Challenging the underlying key assumptions such as expected cash inflow from product sales and cash outflow from purchases of inventory and other operating expenses

• Regarding revenue expectations, challenging the estimates made by management by assessing whether the estimates regarding sales forecasts and sales prices are in line with historical revenues to date and current contracts in place

• We also assessed a sensitivity analysis of management using the low end of revenue forecasts and accompanying key assumptions to ascertain the extent of change in those assumptions that either individually or collectively would lead to alternative conclusions

• Making inquiries with management and reviewing the board minutes and available other available written communication in order to understand the future plans and to identify potential contradictory information

• Assessing the adequacy of the disclosures with respect to the going concern assertion ”

Full-scope audits were limited to subsidiaries representing quite a low aggregate 76% of revenue:

“We performed and audit of the complete financial information of 10 components and performed audit procedures on specific balances for a further five components. The components we performed an audit of the complete financial information accounted for 76% of total assets, 75% of total inventories and 76% of total revenue before consolidation adjustments. The components we performed audit procedures on specific balances accounted for another 8% of total assets, 16% of total inventories and 15% of total revenue before consolidation adjustments. ”

Not ideal that c25% of group revenue, assets etc is not assessed using “complete financial information“.

Mind you, KPMG took a similar approach for 2021 (and did not specify the percentage of revenue etc covered by the full-scope audits):

“Of the Group’s 42 (2020: 43) reporting components, we subjected 11 (2020: 11) to full scope audits for Group purposes. An additional 3 components (2020: 2) were subjected to account balance testing in order to provide sufficient coverage over the Group’s key financial statement lines“.

Materiality remains at 5% of pre-tax profit at €800k.

Key audit matters remain revenue recognition, valuation of intangibles/goodwill and investment in subsidiary undertakings (for the company accounts only). The auditor’s procedures and response did not reveal any unfavourable text.

13) SIGNIFICANT ACCOUNTING PRINCIPLES, ACCOUNTING ESTIMATES AND JUDGEMENTS

A fair amount of next text here, maybe due to the new auditor.

New text includes new confirmation of one reportable segment…

“Segment Reporting An operating segment is a component of the Group that engages in business activities from which it may earn revenue and incur expenses, and for which discrete financial information is available. The operating results of the operating segment is reviewed regularly by the Board of Directors, the chief operating decision maker, to make deci¬sions about allocation of resources and also to assess performance. Results are reported in a manner consistent with the internal reporting provided to the chief operating decision maker (CODM). Our CODM has been identified as the Board of Directors. The Group has determined that it has one reportable segment (see Note 5). The Group is managed as a single business unit that sells drilling equipment, primarily manufactured by Mincon manufacturing sites.

…extra confirmation about government grants…

”Current government grants have no conditions attached

…new confirmation about intangible-development amortisation over 15 years (see blog post above)…

“Recognising an internally developed intangible assets post the development phase once the company has assessed the development phase is complete and the asset is ready for use. Internally generated assets have an infinite life. They will be amortised over a fifteen year period on a straight line basis. Currently there is fourteen years and nine months remaining on the amortisation.”

…new confirmation about impairment assessments…

”Distinguishing the research and development phase, determining the useful life, and deciding whether the recognition requirements for the capitalisation of development costs of new projects are met all require judgement. These judgements are based on historical experience and various other factors that are believed to be reasonable under the prevailing circumstances. After capitalisation, management monitors whether the recognition requirements continue to be met and whether there are any indicators that capitalised costs may be impaired.”

…new confirmation that financial assets are now assessed using IFRS 9…

“Financial assets are assessed from initial recognition and at each reporting date to determine whether there is a requirement for impairment. Financial assets require there expected lifetime losses to be recognised from initial recognition. IFRS 9’s impairment requirements use forward‐looking information to recognise expected credit losses – the ‘expected credit loss (ECL) model’. Instruments within the scope of the requirements included loans and other debt‐type financial assets measured at amortised cost, trade and other receivables.”

…extra confirmation about share-option charges…

“It is reversed only where entitlements do not vest because all non‐market performance conditions have not been met or where an employee in receipt of share entitlements leaves the Group before the end of the vesting period and forfeits those options in consequence.”

…and new confirmation about climate-change matters:

“Consistent with the prior year, as at 31 December 2022, the Group has not identified significant risks induced by climate changes that could negatively and materially affect the estimates and judgements currently used in the Group’s financial statements. Management continuously assesses the impact of climate‐related matters.”

With revenue recognition, MCON reiterated customers can receive discounts but do not receive cash refunds:

”Discounts are provided from time‐to‐time to customers. Customers may be permitted to return goods where issues are identified with regard to quality of the product. Returned goods are exchanged only for new goods or a credit note. No cash refunds are offered.”

14) COST OF SALES AND OPERATING EXPENSES

MCON commendably continues to divulge a range of direct and indirect expenses:

As noted in the blog post above, MCON’s gross margin has reduced over time.

During 2022, revenue gained 18% but total (direct) cost of sales gained 21%, with raw materials up 23%, distribution costs up 26%, energy costs up 42%, maintenance of machinery up 24% and subcontracting up 31%.

During the five years from 2017, revenue has gained 75% but cost of sales have gained 88% with raw materials up 86%, employee costs up 141%, distribution costs up 151%, energy charges up 184% and maintenance of machinery up 127%.

Ascertaining exactly what has happened is difficult, and R&D spend of €4m underlines that not every expense has an associated source of income.

But expenses have fundamentally risen faster than sales, which suggests some competitive faltering as MCON i) has been unable to pass on higher costs to customers, and/or ii) has been deliberately selling reduced-priced items to maintain market share.

Neither option underpins the notion of a great ‘moat’ for the business.

At least a lid has been kept on (indirect) operating costs, which have risen less than revenue over one year (+12% vs +18%) and five years (+39% vs +75%).

Notable indirect-cost changes over five years are professional costs, up 115%, travel expenses, up 4% and marketing charges, up 20%.

Extra professional costs are not surprising as adviser fees etc just seem to rise in line with greater regulation etc. Perhaps of more insight is marketing costs not following revenue higher — maybe MCON needs to promote its products more?

Travel was €1,927k for 2022= c€3k per employee, so some workers are getting out and about.

15) EMPLOYEE INFOMATION

Productivity ratios improved last year but have not shown amazing progress over the longer term:

Sales per employee advanced 12% to almost €272k, the highest since 2017 (€300k), while cost per employee gained 8% to almost €70k, the highest since 2019 (€70k). Staff costs as a percentage of revenue therefore decreased, from 26.6% to 25.6%, the lowest since 2017 (24.2%).

For perspective, revenue per employee exceeded last year’s €272k during 2010, 2011, 2012, 2013, 2014 and 2017. Employee costs as a proportion of revenue was lower than last year’s 25.6% between 2010 and 2017.

One brewing employee issue perhaps is the growing bias towards manufacturing, service and development personnel. Such workers have gained 121% in number since 2017 (from 189 to 417), versus +55% for sales and distribution staffers and +53% for general/admin bods.

MCON’s acquisition drive to supply the full ‘drill string’ and therefore be able to engage direct with the drillers — rather than sell through intermediaries — has required extra sales/distribution people, but their proportion of the workforce is now 21% versus 26% in 2017 and 30%-plus for 2014 and 2015.

I speculate more effort is needed to bolster the sales team and improve the efficiency of the manufacturing, which would rebalance the workforce and lead to possibly higher sales and higher margins.

16) ACQUISITIONS & DISPOSALS

The small €1,014k purchase of Spartan Drilling Tools came with net assets of €853k, which equates to 1.2x book and may have implications for why MCON itself does not trade all that far away from NAV (i.e. why should the stock market value MCON much above book if MCON does not value acquisitions much above book?):

Talk of a loss may have explained the low purchase price:

“The loss from the acquisition of Spartan Drilling Tools has been consolidated into the Mincon Group 2022 profit for the reporting period.”

17) STATUTORY AND OTHER REQUIRED DISCLOSURES

The switch from KPMG to Grant Thornton looks to have prompted lower audit fees:

The €225k fee for audit services is a lowly 0.1% of revenue. Mind you, the auditors provided full-scope audits at subsidiaries representing only three-quarters of the group (see point 12).

18) INTANGIBLE ASSETS AND GOODWILL

The only movement of significance was the reclassification of capitalised Greenhammer development costs as an ‘internally generated intangible asset’:

MCON helpfully provides a list of past acquisitions:

The goodwill impairment assumptions have been tweaked, with an Ebitda margin of 20.2% a notable increase versus 16.7% and 17.8% for the prior two years:

The Ebitda assumption within the 2023 report will be interesting to see after October’s profit warning.

Headroom for the goodwill was more that double the goodwill’s €32m carrying value:

”The carrying amount of the CGU was determined to be lower than its fair value less costs of disposal by €52.4 million (2021: €42.9 million), giving management substantial headroom and comfort in the above stated impairment assessment.”

The stock market is presently not assessing goodwill the same way as MCON though!

The market cap at the recent 53p is £113m, versus a net book value of €154m = £131m at GBP:EUR 1.17. Exclude the intangibles/goodwill of €40m and net book value becomes €114m = £97m = 46p per share.

19) PROPERTY, PLANT AND EQUIPMENT

Always a bit confusing this note. Additions were between €10-11m for the last two years:

Yet purchases of property, plant and equipment in the cash flow statement were between €7-8m.

The differences I believe are due to the prepayment of plant and equipment:

For example, I reckon MCON’s additions to property, plant and equipment for 2022 of €10,190k was made up of cash capex of €7,309k plus a transfer of c€2.9m from prepayments of plant and equipment made in prior years.

‘Plant and machinery prepaid and under commission’ increased by €4,071k to €9,852k for 2022, so I believe total spend on prepaid capex was €2.9m + €4,071k = c€7m.

20) INVENTORY AND CAPITAL EQUIPMENT

As mentioned in the blog post above, stock of €77m was huge versus revenue of €170m:

Raw materials represented 21% of total stock, up from 18% the year before but within the 18-22% range seen since 2017.

Cost of sales of €116m were 1.66x the year-average stock value of €70m, and that ratio has been very stable at 1.64x, 1.66x and 1.65x during the prior three years. So at least the stock build-up has not reflected slower stock-turn.

Stock provisions at £128k remain small and imply little risk of product obsolescence.

21) TRADE AND OTHER RECEIVABLES

Nothing untoward here. The provision for impairment was 4% of gross trade receivables, and at the bottom of the 4%-15% range seen since 2015.

Net trade receivables at 14% of revenue was the lowest since at least 2009. Between 2010 and 2021, the range was 16-22%.

26% of trade receivables are past due, which is not ideal but not outside historical norms either. Prior to 2020, MCON did not report receivables not past due, but instead reported trade receivables less than 60 days due, which had been no higher than 84% of all trade receivables. Yet for 2022 the equivalent figure was 97% (and 98% for 2021 and 90% for 2020). So again, no obvious deterioration to customer credit quality.

Note 22 gives this breakdown of trade receivables:

Trade receivables as a proportion of revenue was 12% for Americas, 20% for Australasia and 15% for EMEA.

22) TRADE CREDITORS

No issues here. Trade creditors continue to bounce between 8% and 11% of revenue:

23) CAPITAL MANAGEMENT

Interesting text in this section that was repeated from 2021 (and before):

“The Group’s policy is to have a strong capital base in order to maintain investor, creditor and market confidence and to sustain future development of the business. Management monitors the return on capital, as well as the level of dividends to ordinary shareholders. The Board of Directors seeks to maintain a balance between the higher returns that might be possible with higher levels of borrowing and the advantages and security afforded by a sound capital position. The Group monitors capital using a ratio of ‘net debt’ to equity. Net debt is calculated as total liabilities less cash and cash equivalents (as shown in the statement of financial position).”

Return on capital was not deemed to be a formal KPI with the Directors’ Report (see point 5). But it is being used as a LTIP target (13%) (see point 9).

MCON’s reference to net debt seems confusing. The conventional method I have always used is cash less bank debt. Given the high levels of stock, shareholders could be excused for thinking a “strong capital base” might not be an “efficient capital base“.

24) LOANS AND BORROWINGS

Oh dear. This small-print has become concerning following October’s profit warning:

“The Group has a number of bank loans and lease liabilities with a mixture of variable and fixed interest rates. The Group has not been in default on any of these debt agreements during any of the periods presented. The loans are secured against the assets for which they have been drawn down for. The Group has been in compliance with all debt agreements during the periods presented. The loan agreements in Ireland of €13.5 million (2020: €10.5 million) carry restrictive financial covenants including, EBITA to be no less than €18 million at end of each reporting period, interest cover to be 3:1 and to maintain a minimum cash balance of €5 million.

Interest rates on current borrowings are at an average rate of 4.89%

During 2022, the Group availed of the option to enter into overdraft facilities and to draw down loans of €11.5 million, €8.8 million in loans and €2.7 million in overdraft facilities.

Loans are repayable in line with their specific terms, the Group has one bullet repayment due in 2026 of €5 million.”

October’s update said:

“In light of the above, looking ahead to the remainder of the year we now expect to deliver full year EBITDA of approximately €20 million”

So, forthcoming EBITDA of €20m versus EBITA (no D!) of at least €18m to keep the bank happy. The D (depreciation) was €7m-plus for 2022 and 2021, so EBITDA of €20m translates into EBITA of €13m, which seems to break a covenant :-(

The associated covenants relate to loans of €13.5m versus total bank loans of €30.8m. So not every loan is involved here, and the other covenants may save the day. For example, MCON had cash of €13m at the subsequent H1 2023 versus a covenant minimum of €5m.

I suspect MCON and the banks will re-arrange the debts/covenants without too much heartache for shareholders, but both parties will become somewhat more circumspect with EBIT(D)A covenants and MCON will probably pay a higher rate.

Interest on bank borrowings was stated as 4.89%, and finance costs of €870k over year-average bank borrowings of €27.1m = 3.2%.