29 March 2019

By Maynard Paton

Results verdict on FW Thorpe (TFW):

- Lower revenue and profit due to “challenging trading conditions” caused perhaps by the collapse of Carillion.

- The statement’s highlight was management talk of orders having returned to “record levels”.

- Fresh product developments continue and include “radical” new range of workplace lighting.

- Accounts showcase huge £53m cash pile while dividend on course for 17th consecutive annual increase.

- Underlying P/E of 21 seems optimistic given recent progress. I continue to hold.

Contents

- Event link and share data

- Why I own TFW

- Results summary

- Revenue, profit and dividend

- Divisions

- Financials

- Current trading and product developments

- Valuation

Event link and share data

Event: Interim results for the six months to 31 December 2018 published 21 March 2019

Price: 320p

Shares in issue: 116,120,658

Market capitalisation: £372m

Why I own TFW

- Manufactures commercial lighting systems and boasts a long-established reputation for high product quality, leading technical innovation and top customer service.

- Board led by veteran executive and assisted by family management that continues to enjoy 50%-plus shareholding.

- Conservative accounts offer asset-flush balance sheet and illustrious rising dividend.

Further reading: My TFW Buy report | All my TFW posts

Results summary

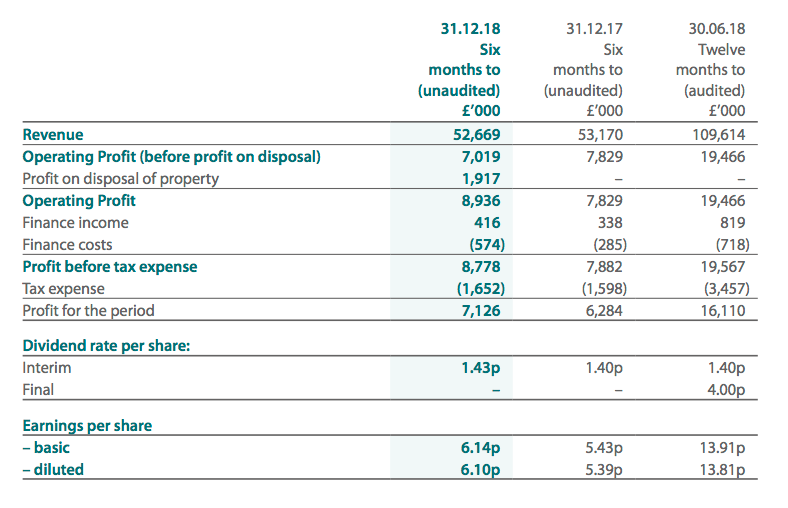

Revenue, profit and dividend

- November’s AGM statement had already predicted these half-year figures would show operating profit down 10%.

- The results did indeed reveal operating profit down 10%, with revenue 1% lower.

- Exclude the purchase of Famostar, and revenue would have dropped 8% while operating profit would have dropped 15%.

- “Challenging trading conditions” at Thorlux, the group’s main division, were cited for the shortfall.

- Management comments within the 2018 annual report (point 1) hinted that the collapse of Carillion may have affected orders.

- Brexit was also cited for “business confidence” having yet to return to “more normal levels”.

- Recent trading has thankfully improved. Orders at Thorlux have apparently rebounded to “record levels”.

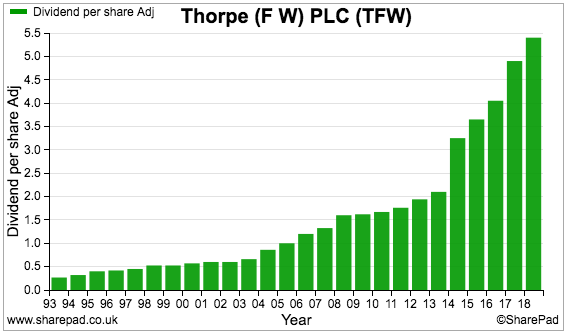

- The only first-half number making positive ground was the dividend, up 2%.

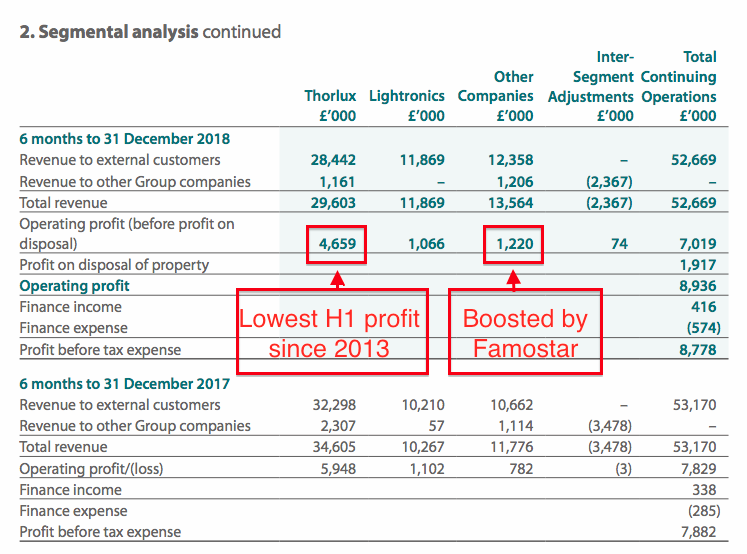

Divisions

- TFW’s divisions delivered very mixed performances.

- Thorlux’s revenue and profit dived 12% and 22% respectively. The subsidiary represents approximately 60% of the entire group.

- Thorlux’s £4.7m profit was the division’s lowest for six years.

- Thorlux’s 16.4% first-half operating margin was the division’s thinnest for at least 10 years. Thorlux has typically converted 20%-plus of revenue into profit.

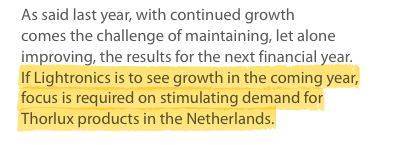

- Progress at Lightronics was mixed. Revenue gained 16% but profit fell 3%. The Dutch subsidiary appears to be winning less-profitable orders — its margin was just 9%.

- Following initial stellar progress, profit at Lightronics has now stagnated since 2016.

- Attempts to sell Thorlux equipment through Lightronics have yet to really succeed.

- TFW’s seven smaller divisions delivered aggregate revenue down 18% but profit up 3%.

Enjoy my blog posts through an occasional email newsletter. Click here for details.

Financials

- The downturn at Thorlux and the lower-margin Lightronics revenue left the wider group margin at just 13% — the lowest since at least 2007.

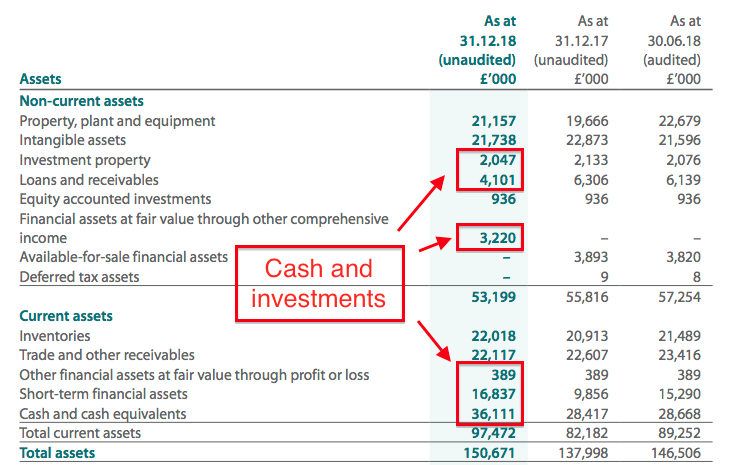

- At least TFW’s balance sheet remains super-impressive.

- Cash in the bank has surpassed £50m for the first time to reach £53m.

- Cash flow was assisted by a £3.8m property disposal and a £2m receipt from a loan note (point 17).

- First-half expenditure on tangible and intangible items was covered by the depreciation and amortisation charged against earnings.

- Working-capital movements released £2m, which supported total cash generation of £12m before dividends of £4.6m.

- Balance-sheet assets also include a £2m investment property, a £3m share portfolio and £4m of loan notes.

- TFW’s major liabilities are acquisition-related earn-outs that total £11m.

- There is no debt.

- Net cash and investments is therefore arguably £53m plus £9m less £11m = £51m, equivalent to 44p per share or 14% of the current market cap.

- Management has never really explained why such a high level of cash is hoarded.

- Acquisitions seem a likely reason. The purchase of Dutch firms Lightronics and Famostar have cost the group £13m to date.

- Surplus cash could also reassure customers and suppliers that, during recessions, orders will still be completed and bills will still be paid.

- Could another special dividend be declared?

- Special payouts were distributed during 2014 (1.5p per share) and 2016 (2p per share), when my calculation of net cash and investments stood at £40m.

- A £51m net cash/investment position is by no means the worst problem to face in the stock market.

- TFW’s defined benefit-pension scheme remains in surplus and current ‘catch-up’ contributions are only £160k a year.

Current trading and product developments

- Supported by the aforementioned upturn at Thorlux, current trading conditions are “more buoyant than… previously predicted” and a “strong finish to the year” is now anticipated.

- A new lighting range that will “reinvigorate the workplace” may soon derive extra sales.

- This “radical” new range is called Flex System and “breaks from convention [by] taking the lighting outside of the ceiling tile, offering freedom and flexibility of scheme design.”

- In addition, the system’s “dual light engine… brings a touch of the outside inside with its illuminated picture window.”

- Meanwhile, orders for wireless lighting control systems “rocketed” last year (point 1) and I dare say may continue to do so this year.

- Various other product innovations and factory upgrades are underway that may also support future progress.

Valuation

- TFW still reckons underlying operating profit for 2019 will not match that reported for 2018.

- The trailing twelve-month operating profit is £18.4m. The 2018 operating profit was £19.2m.

- Applying the 19% tax applied in these results to the trailing £18.4m operating profit gives earnings of £14.9m or 12.8p per share.

- Subtract the 44p per share net cash position from the 320p share price, and the underlying P/E could be 21.

- The 21x multiple appears optimistic given revenue and profit have come to a standstill.

- Nonetheless, perhaps TFW will extend the “strong finish” of this year right through into 2020 — with earnings growth amplified as higher revenue leads to a margin rebound.

- The 2% interim divided lift gives a trailing 5.43p per share payout and a meagre 1.7% income.

- Assuming the final payout is not cut, the 2019 results will deliver TFW’s 17th consecutive annual dividend increase.

Maynard Paton

PS: You can receive my blog posts through an occasional email newsletter. Click here for details.

Disclosure: Maynard owns shares in FW Thorpe.

Hi Maynard ,

Great article we meet briefly at London Mello we spoke about Andrew Sykes and Fulham Shore not if you remember .

I am keen to learn I am a holder in FWT

”Net cash and investments is therefore arguably £53m plus £9m less £11m = £51m, equivalent to 44p per share or 14% of the current market cap”

Can you please tell me how to work out the 44p per share bit ?

Thanks

Tony

Hello Tony

Yes, I remember. You featured on a conkers3 Mello video, so I then matched the name to the face :-) Hopefully the debts and leases won’t prove a problem at FUL, but if earnings do wobble then problems could occur. I should know — I own shares in TAST.

The 44p is calculated by dividing the £51m by the number of TFW shares in issue.

I used 116,120,658 as per this RNS which gives £51m/116m = 44p.

Maynard